The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Debt Ceiling, Interest Rates, an Economic Outlook and more stock news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Portfolio Trades – 3 Transactions for 3 Accounts

Week in Review – Handsome Gains Thanks to Big Friday Rally

Debt Ceiling – Disaster Averted…for the 79th Time

Economic Outlook – Pessimism Remains High But Still No Contraction

Reason & Evaluation – Recessions/The Great Inflation and Equity Returns

Goldilocks – Monthly Jobs Report Almost Perfect

Interest Rates – Low By Historical Standards; Historical Perspective; Stocks Remain Attractively Valued

Making Stuff Up – VZ the Latest to Fall on Questionable “News”

Stock News – Updates on nine stocks across six different sectors

Week in Review – Handsome Gains Thanks to Big Friday Rally

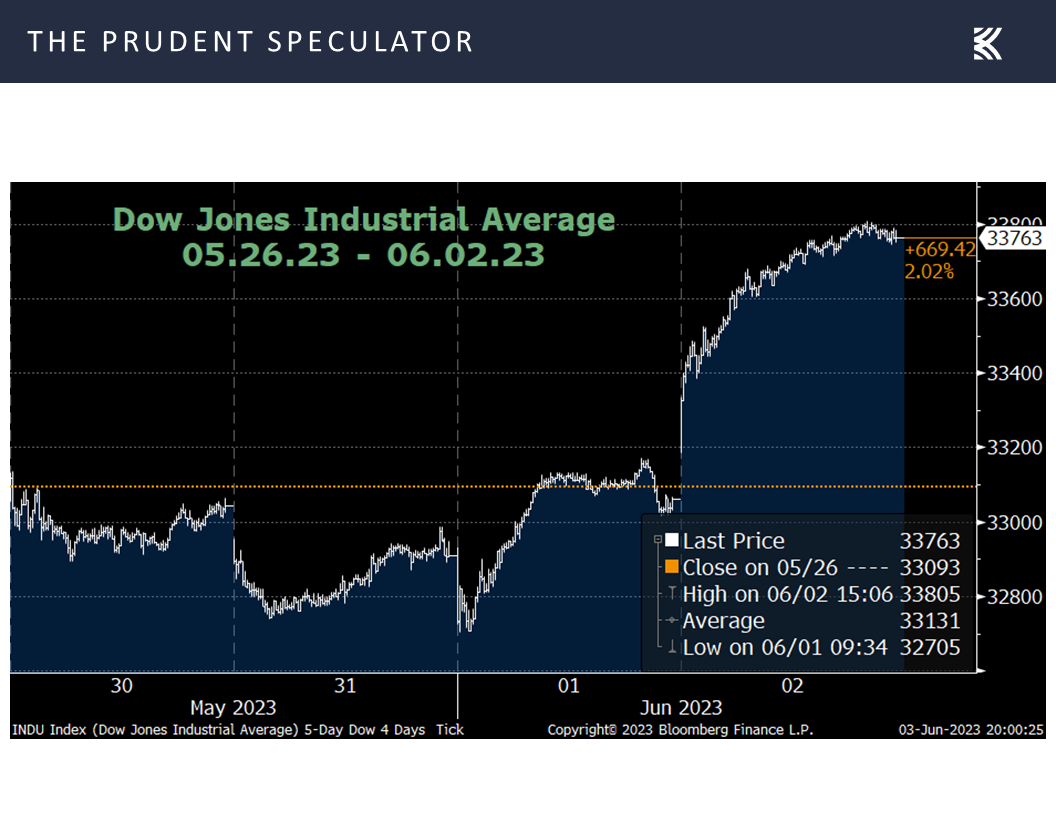

Given that the Dow Jones Industrial Average closed the holiday-shortened trading week up better than 2% and more than 1000 points above its weekly low-water mark set shortly after the open on Thursday, the equity markets offered another reminder that volatility works in both directions.

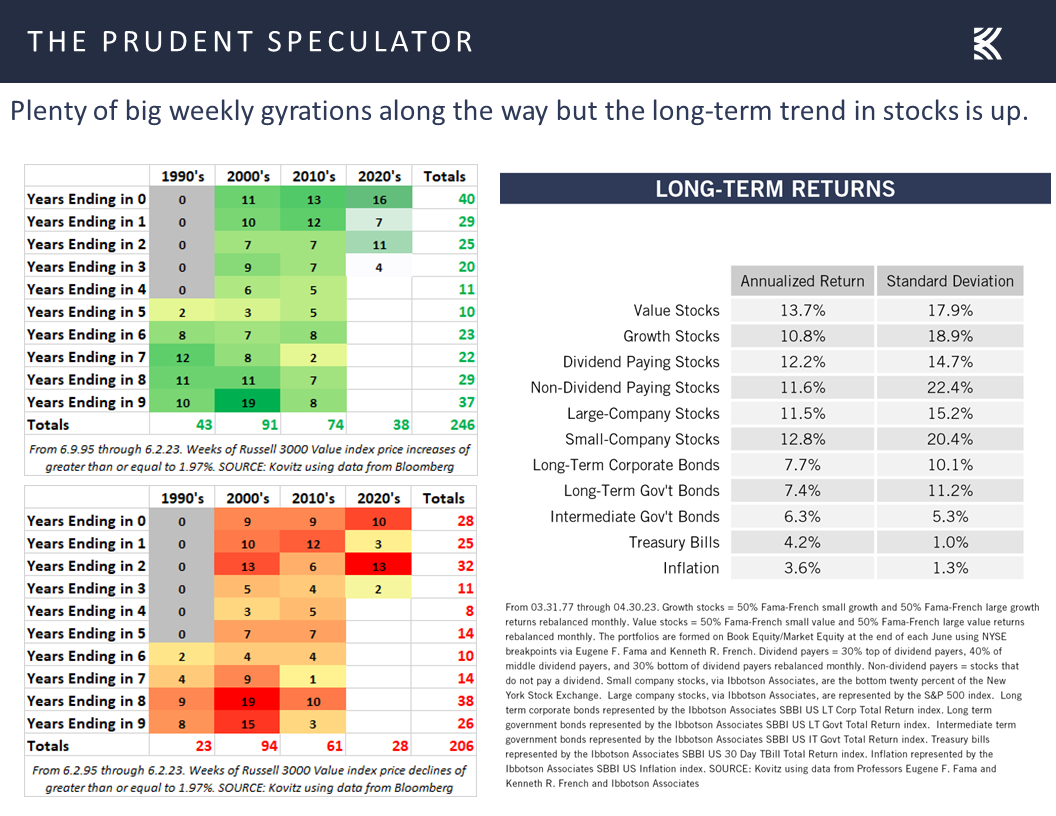

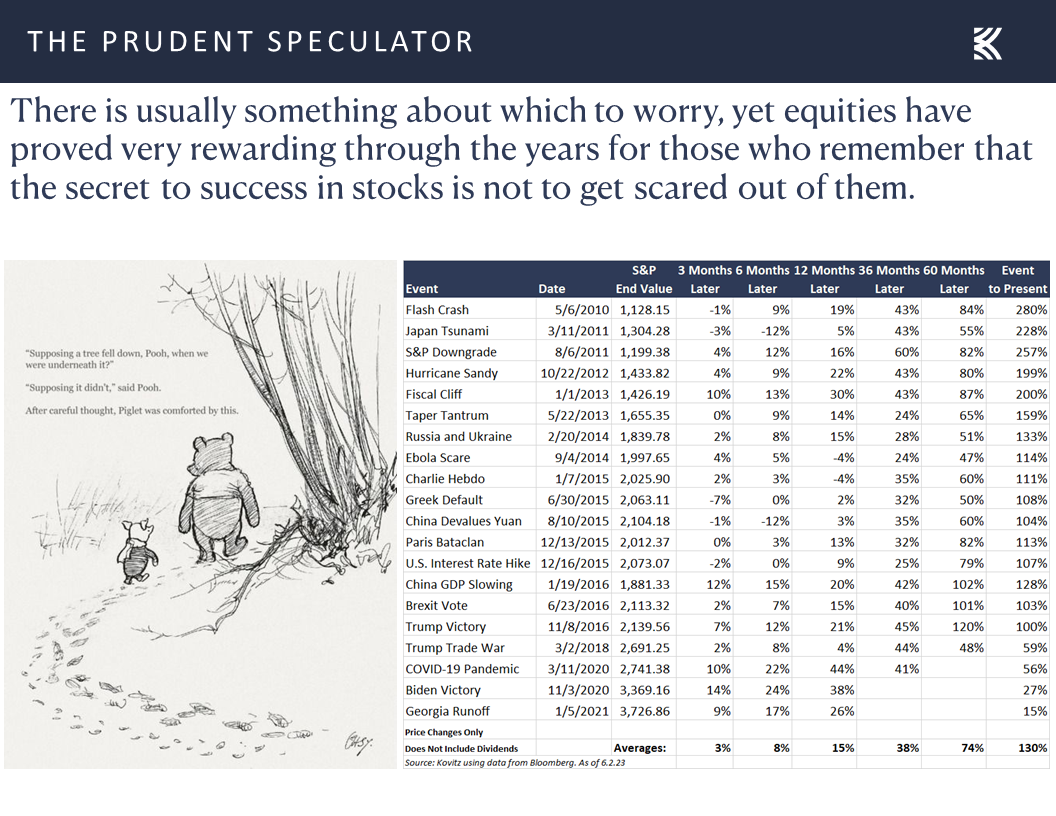

Happily, there have been more strongly positive weeks than decidedly negative weeks throughout history, so much so that the long-term trend for stocks is significantly higher, with gains for Value Stocks averaging 13.7% per annum since the launch of The Prudent Speculator in March 1977.

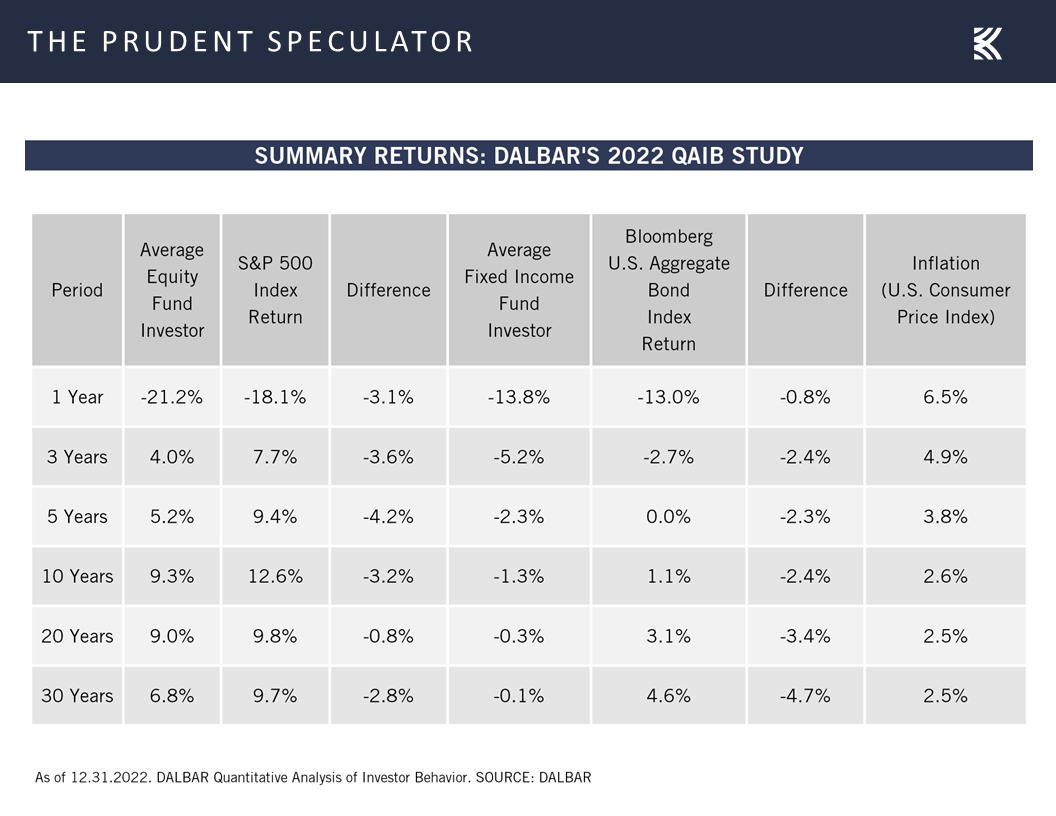

Of course, very few investors have managed to achieve that sort of return, primarily because they forget that the secret to success in stocks is not to get scared out of them. Sadly, as our oft-cited data from research firm DALBAR shows, equity (and fixed income) fund investors have proved to be lousy market timers, costing themselves 2.8% per annum (stocks) and 4.7% (bonds) per annum over the past 30 years. No doubt, there is a lot of buying high and selling low going on.

Debt Ceiling – Disaster Averted…for the 79th Time

The challenge, of course, is coping with disconcerting events such as the recent debt-ceiling drama. Folks were faced with warnings from the main-stream media and financial press that a polarized Congress might let Uncle Sam default on its obligations with disastrous implications for the economy and investments.

To be sure, there was no assurance that Washington would agree on legislation before the so-called X-Date when the Treasury essentially would run out of money, but here is what had happened direct from the Treasury’s website the previous six-and-one-half-dozen times the country faced such a potentially monumental problem,…

Congress has always acted when called upon to raise the debt limit. Since 1960, Congress has acted 78 separate times to permanently raise, temporarily extend, or revise the definition of the debt limit – 49 times under Republican presidents and 29 times under Democratic presidents. Congressional leaders in both parties have recognized that this is necessary.

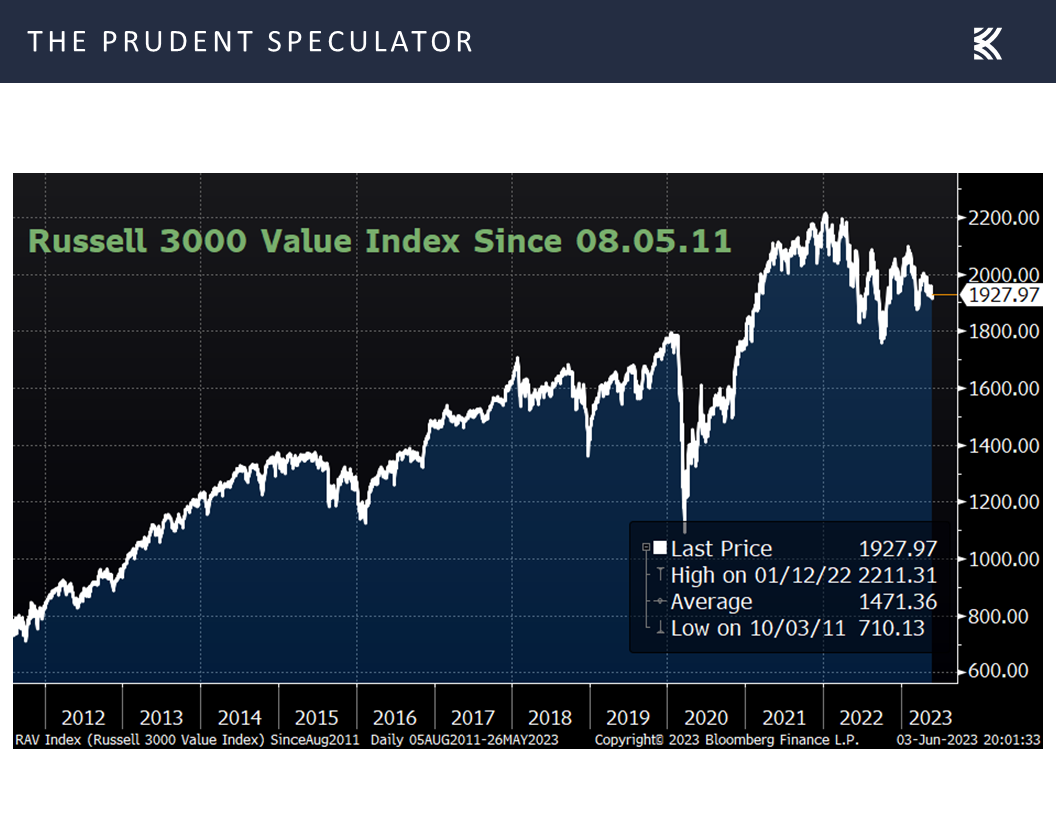

…while arguably the most difficult debt-ceiling battle that ever occurred (back in 2011) proved to be a great time for long-term-oriented investors to be buying stocks, despite Standard & Poor’s downgrading the U.S. credit rating on August 5 of that year.

Obviously, it isn’t easy to keep the faith through thick and thin, but we find the Vannevar Bush admonition helpful, “Fear cannot be banished, but it can be calm and without panic; it can be mitigated by reason and evaluation.”

After all, there seemingly is always something for equity participants to worry about. Just since the end of the Great Financial Crisis, there have been numerous scary events, yet equities generally have proved very rewarding in the fullness of time for those who remember that time in the market trumps market timing.

Economic Outlook – Pessimism Remains High But Still No Contraction

Alas, we find that even professional investors and market pundits often are not interested in Mr. Bush’s reason and evaluation, choosing instead to pontificate on what they think should happen and ignoring what has occurred previously.

We can debate the value of studying the past, as the Greek philosopher Heraclitus states, “No man ever steps in the same river twice. For it’s not the same river and he’s not the same man.”

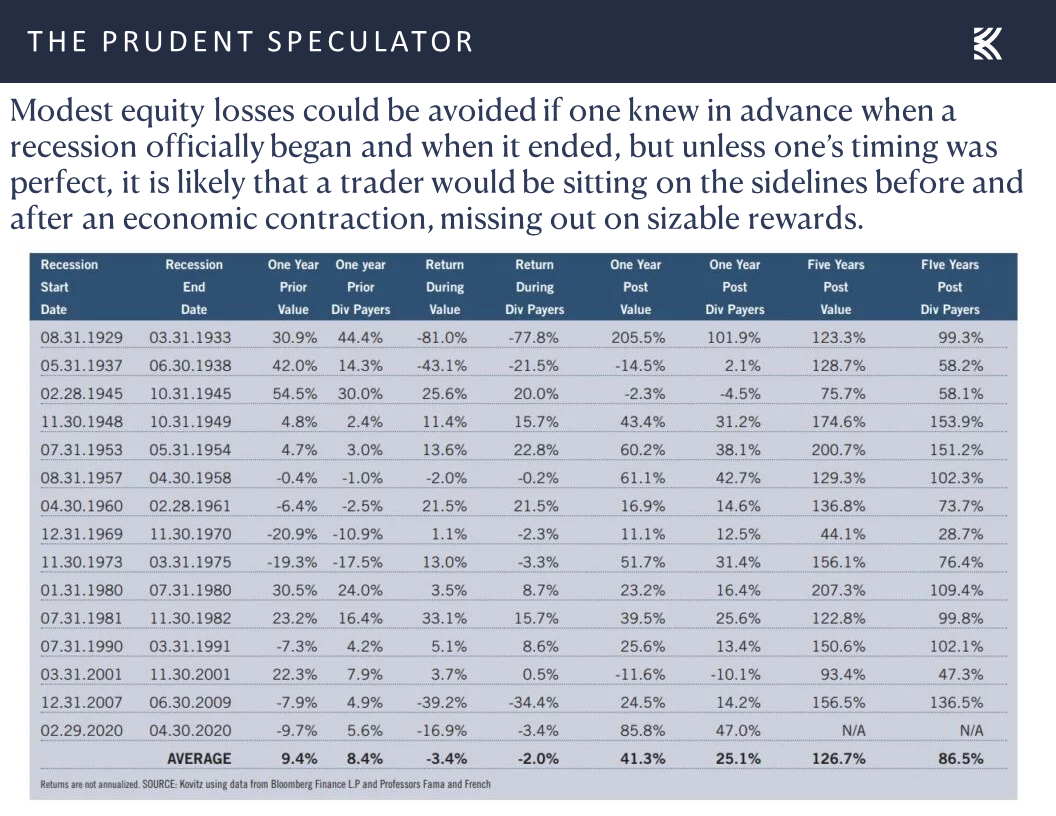

However, we are flabbergasted when seemingly smart-sounding financial experts tell us, for example, that you don’t want to be in stocks if a recession is on the horizon. On the surface, that is logical, and we concede that it would be nice to have avoided the modest average loss during the 15 recessions that have taken place since 1929, but, as the saying goes, economists have predicted nine of the last five recessions.

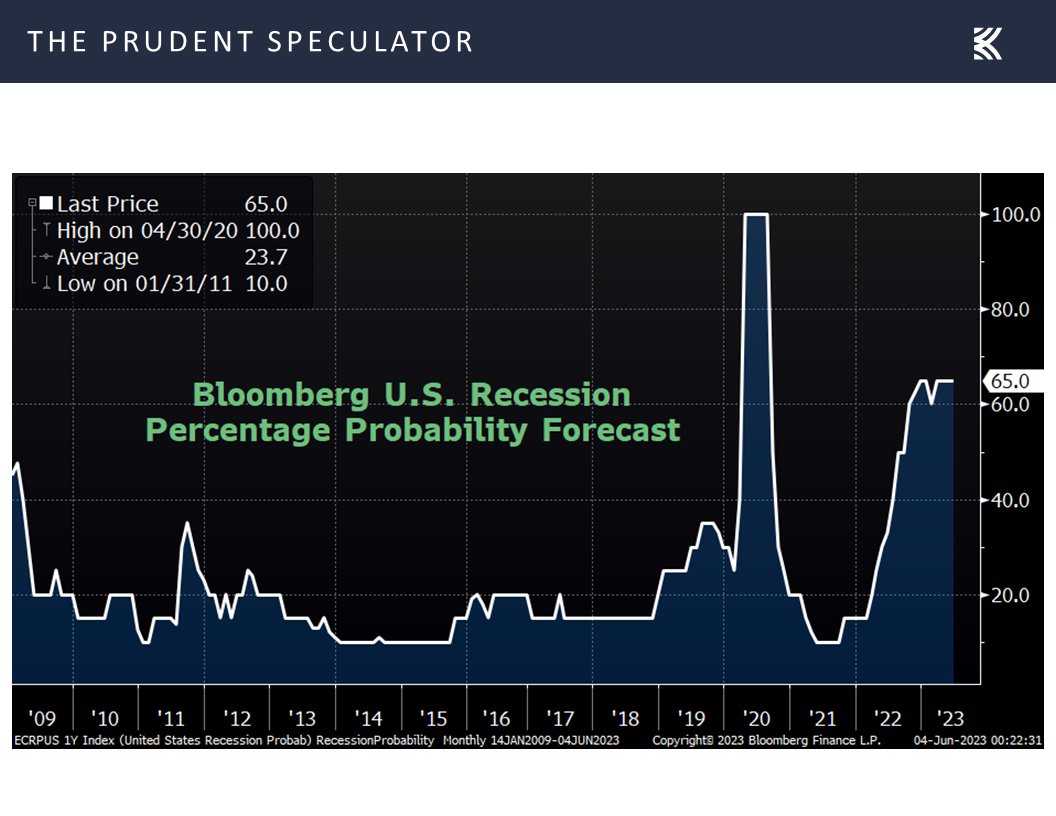

Given that the National Bureau of Economic Research (the “official” statistician) does not determine the dates until after the fact, knowing in advance when contractions will begin and end is virtually impossible, as evidenced by the fact that the odds of a U.S. recession over the ensuing 12 months (tabulated by Bloomberg), have been at 50% or greater since August 2022,

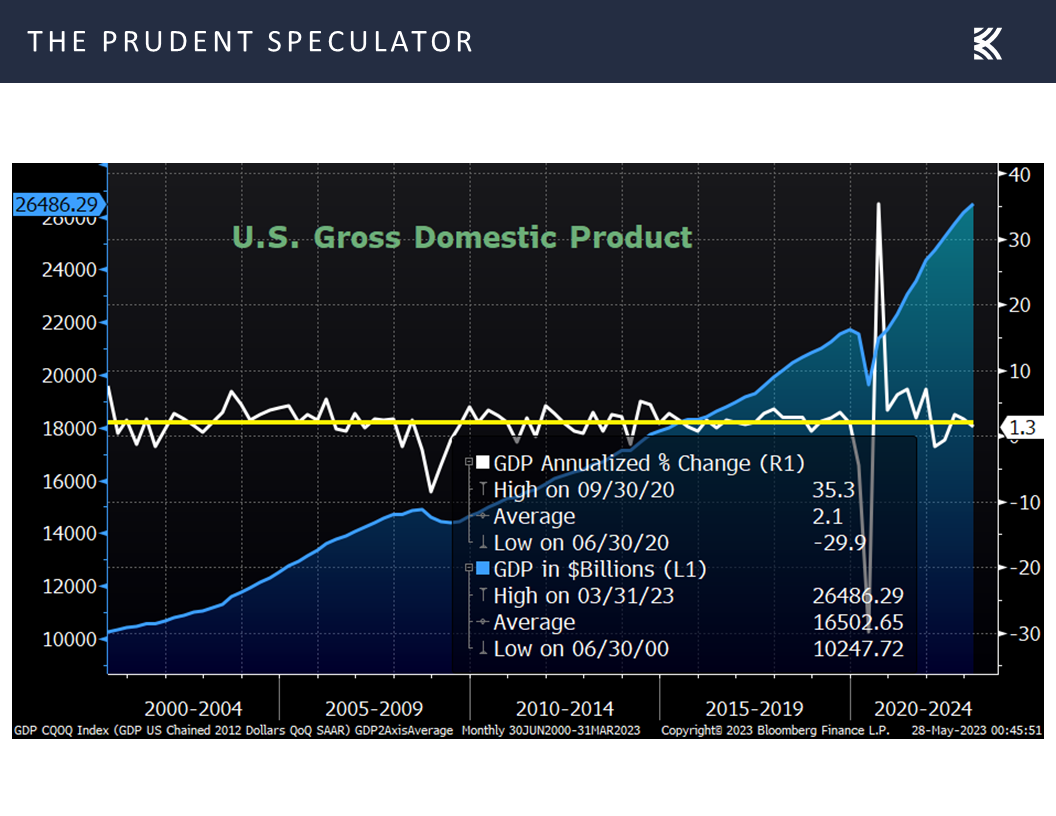

yet Q3 2022 and Q4 2022 real (inflation adjusted) GDP growth came in at impressive rates of 3.2% and 2.6%, respectively, while Q1 2023 growth was a decent 1.3%,

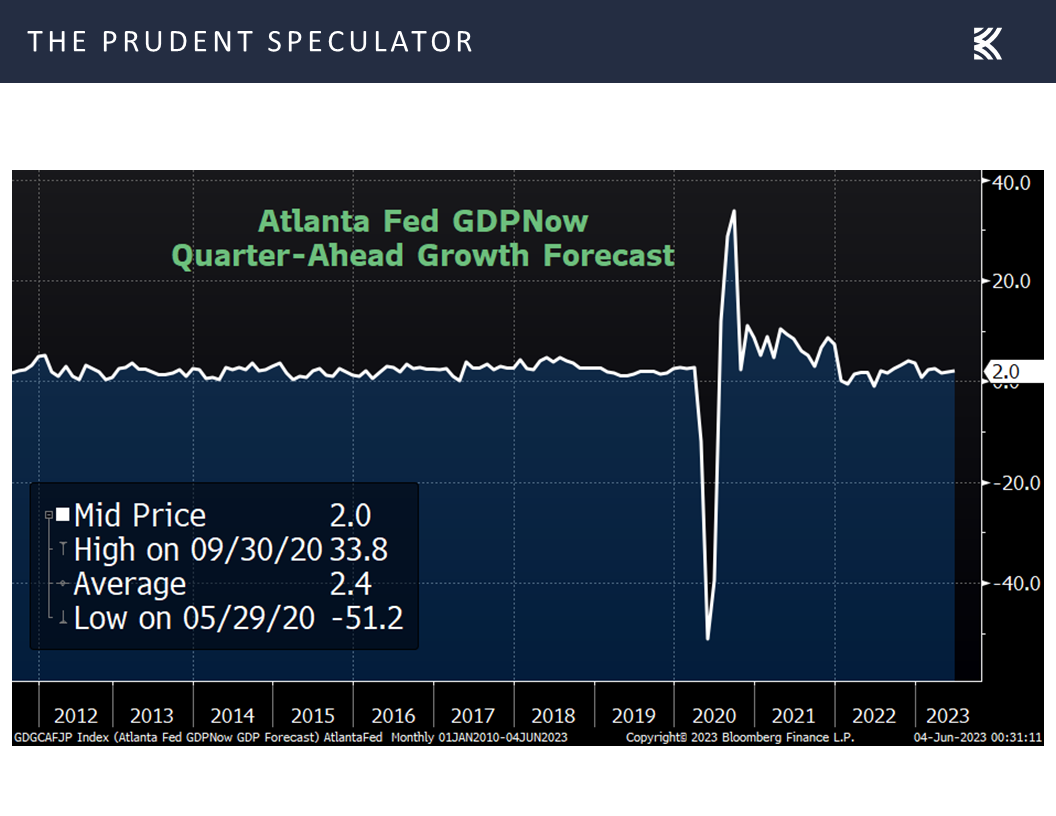

and the current estimate for domestic Q2 2023 growth from the Atlanta Fed is 2.0%

and the current estimate for domestic Q2 2023 growth from the Atlanta Fed is 2.0%

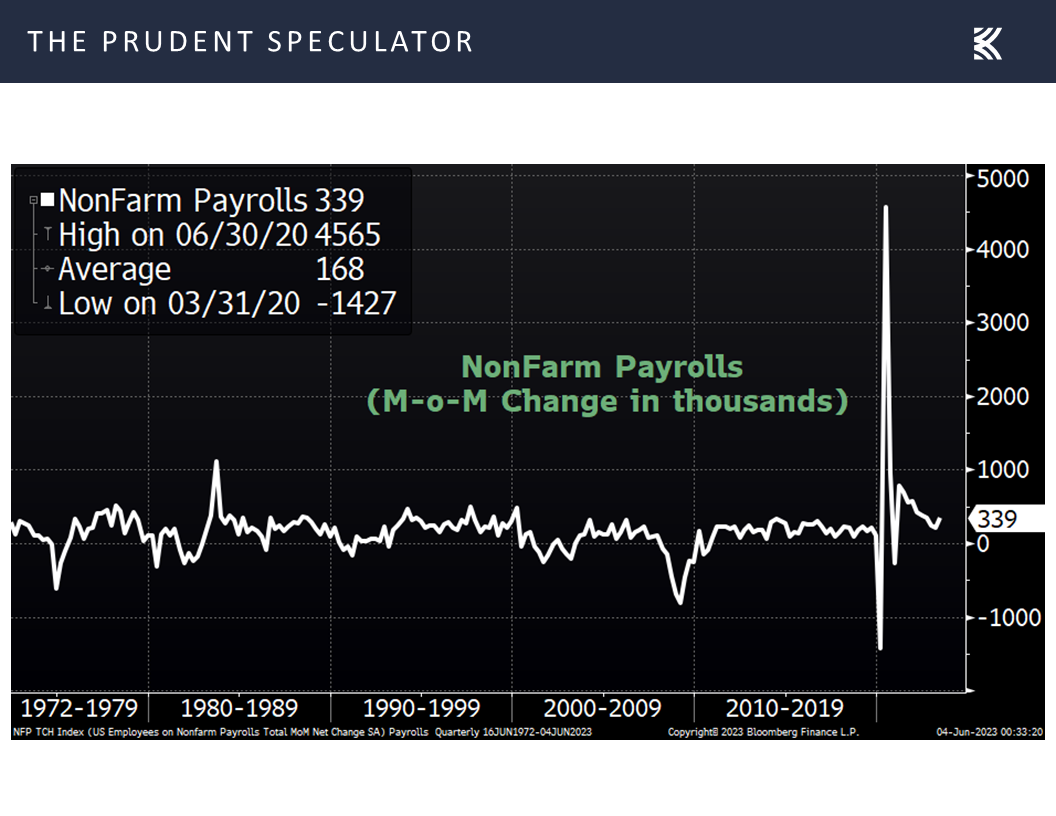

with said projection made prior to Friday’s much-better-than-expected labor situation report in which 339,000 new jobs were created and the prior two month’s tallies were revised upward by a combined 93,000 payrolls.

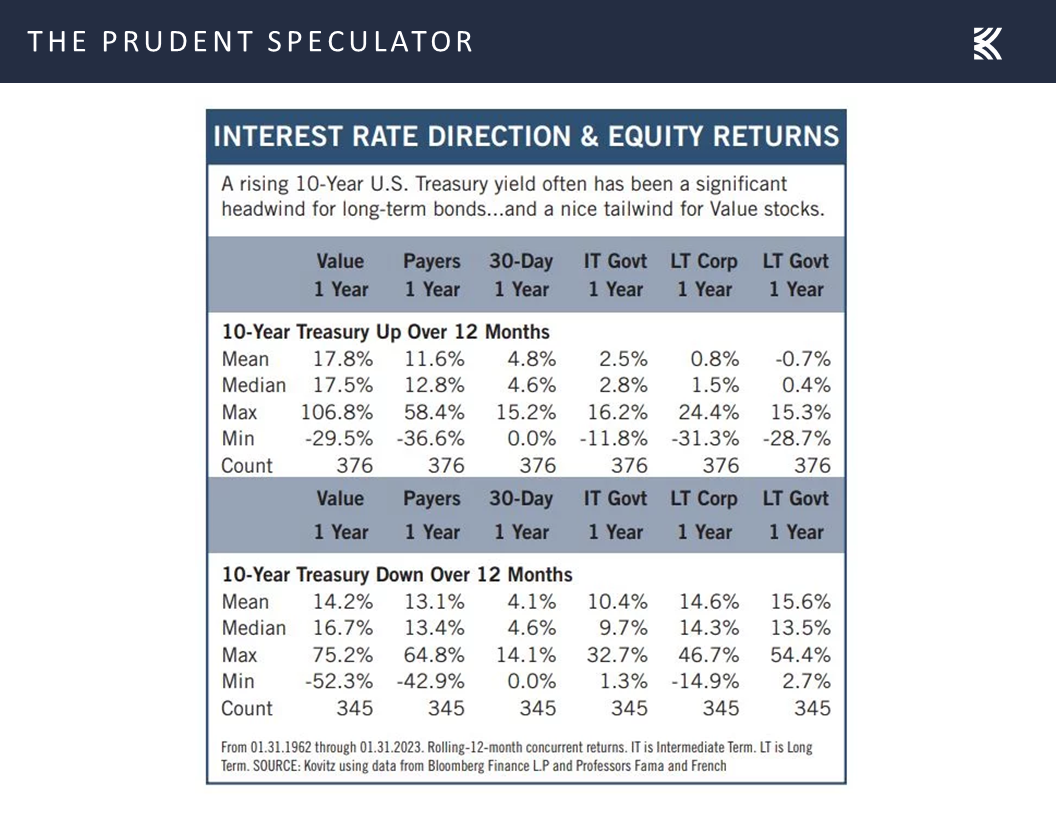

Famed fund manager Peter Lynch once remarked, “Far more money has been lost by investors in preparing for corrections, or anticipating corrections, than has been lost in the corrections themselves.” The table below vividly confirms his assertion as folks fearing that a recession is around the corner likely missed out on the solid gains, on average, in the year before the official downturn starts. Even worse, they are likely to have missed out on spectacular returns, on average, in the year after a recession ends, as all-clear signals are seldom issued…or believed.

Reason & Evaluation – Recessions/The Great Inflation and Equity Returns

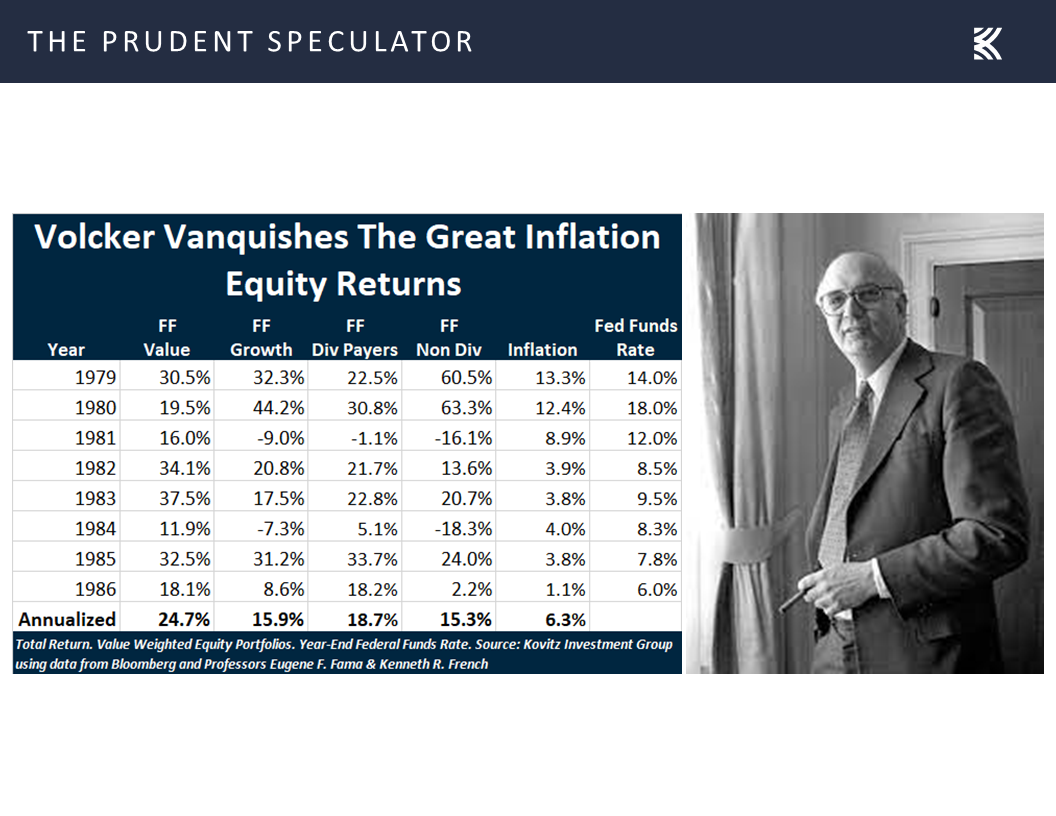

This is not to say that it might not be different this time…so we offer another example of reason and evaluation to hopefully help to mitigate fear. Those concerned that the Federal Reserve’s current fight with inflation will end miserably for stocks, might want to consider the last such battle during the late-1970’s and early-1980’s. With a double-digit percentage increase in the consumer price index wreaking havoc, the Paul Volcker Fed vanquished the Great Inflation, but not without causing two recessions in 1980 and 1981.

This is just one data point and interest rates were sky high back then, so statisticians might dismiss the relevancy, but Value Stocks enjoyed a superlative 24.7% average return during the eight Volcker years and Dividend Payers turned in an 18.7% annualized return. Remember that those figures are per year, meaning a more than four-fold advance for Value and a nearly three-fold advance for Dividend Payers over the full eight years. Ah, the miracle of compounding!

Goldilocks – Monthly Jobs Report Almost Perfect

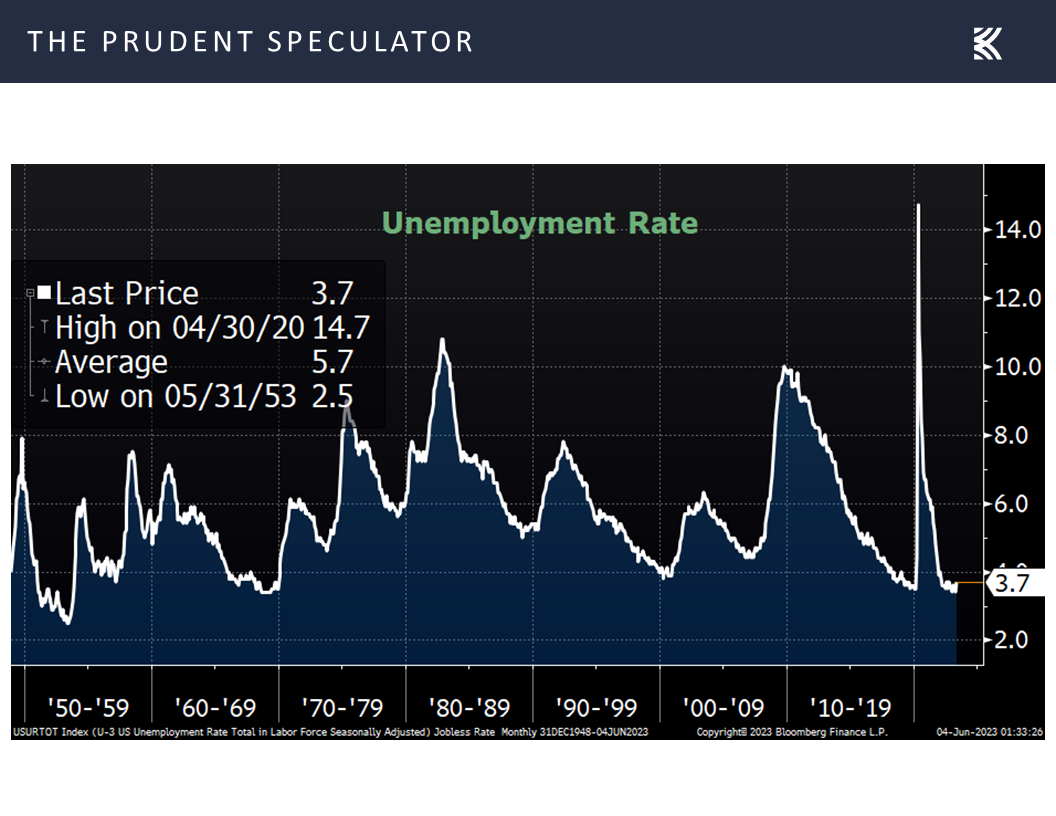

Anything can happen as we go forward, and we realize that future economic numbers may not be as Goldilocks-like as was Friday’s employment report, with the higher-than-expected increase in the jobless rate to 3.7%,

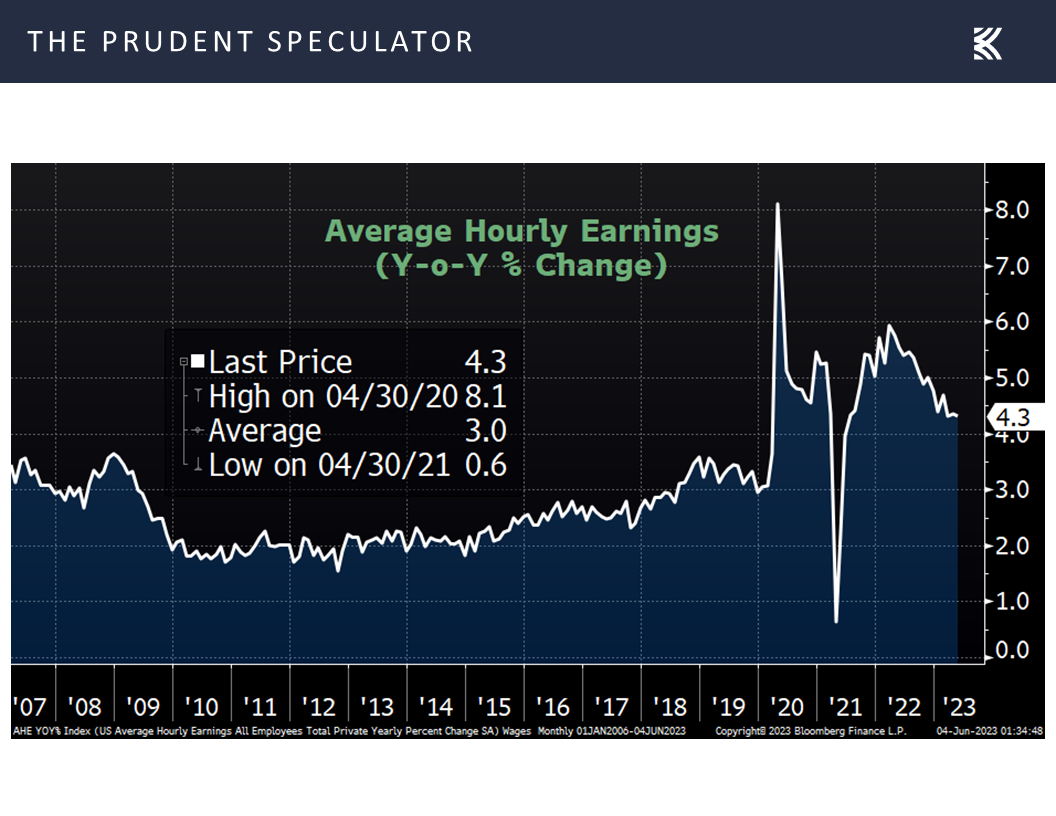

and the surprising tick down in wage growth to 4.3%

suggesting to some that the Federal Reserve has more room to be patient with future hikes in the Fed Funds rate.

Interest Rates – Low By Historical Standards; Historical Perspective; Stocks Remain Attractively Valued

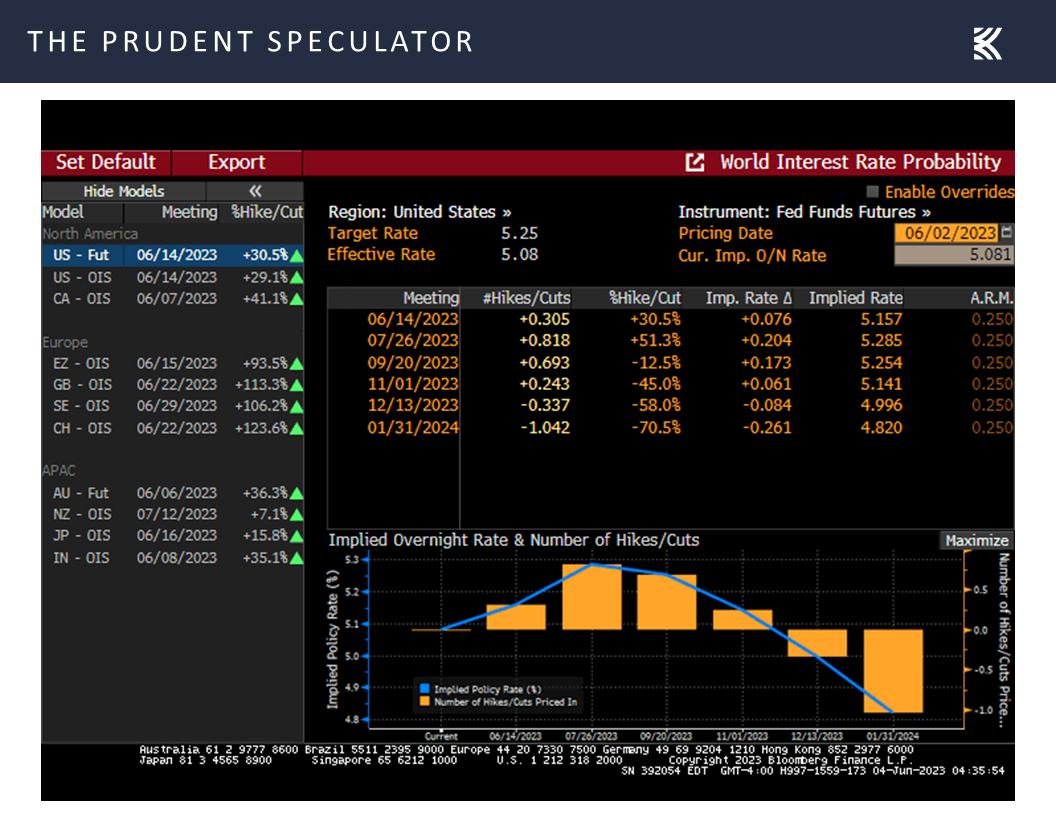

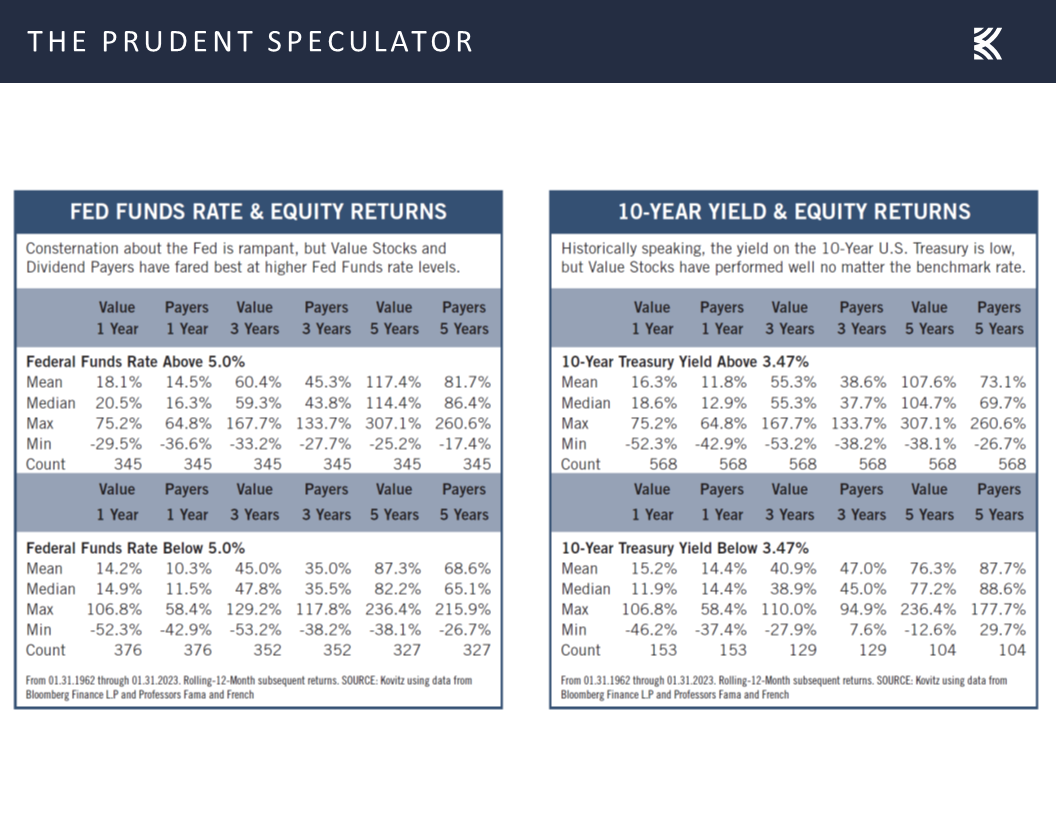

We’ll let traders worry about the Fed as we think Jerome H. Powell & Co. are not far from the end of the tightening cycle, while the historical evidence suggests that stocks have performed fine, on average, whether interest rates are high or low,

with about the only conclusion that can be drawn about interest rates and asset prices being that a rising long-term government bond rate is bad for long-term government bond prices.

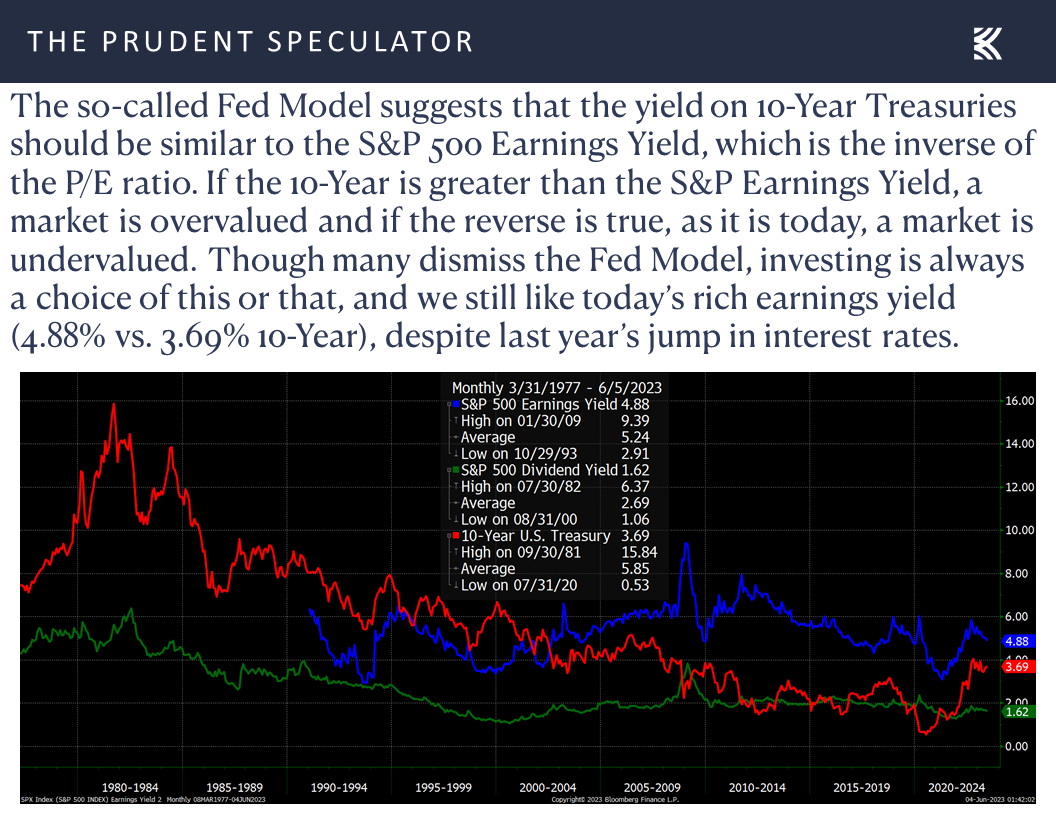

Further, though rates definitely are higher than where they had been for much of the last decade, the current 3.69% yield on the 10-Year U.S. Treasury is well below the 5.85% average since the launch of The Prudent Speculator more than 46 years ago. As such, we think long-term interest rates remain low by historical standards, providing support for equities in general,

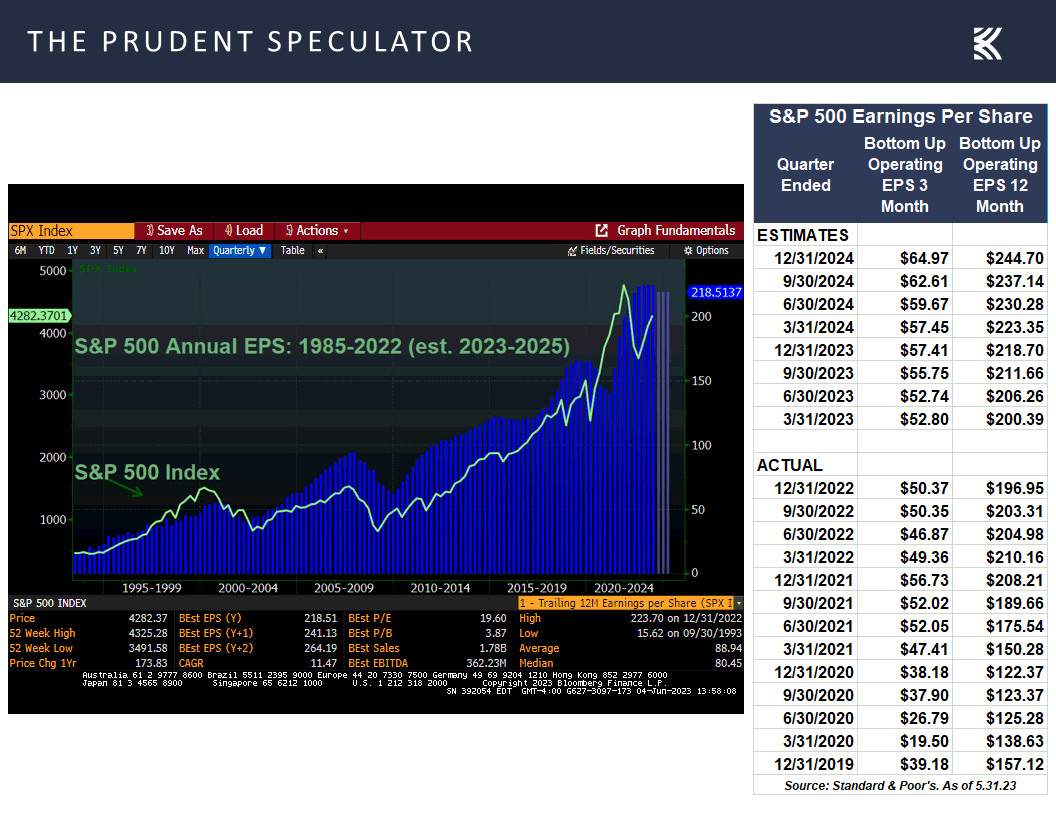

especially as corporate profits are likely to continue to grow, with estimates from Standard & Poor’s for EPS for the S&P 500 this year and next increasing last week.

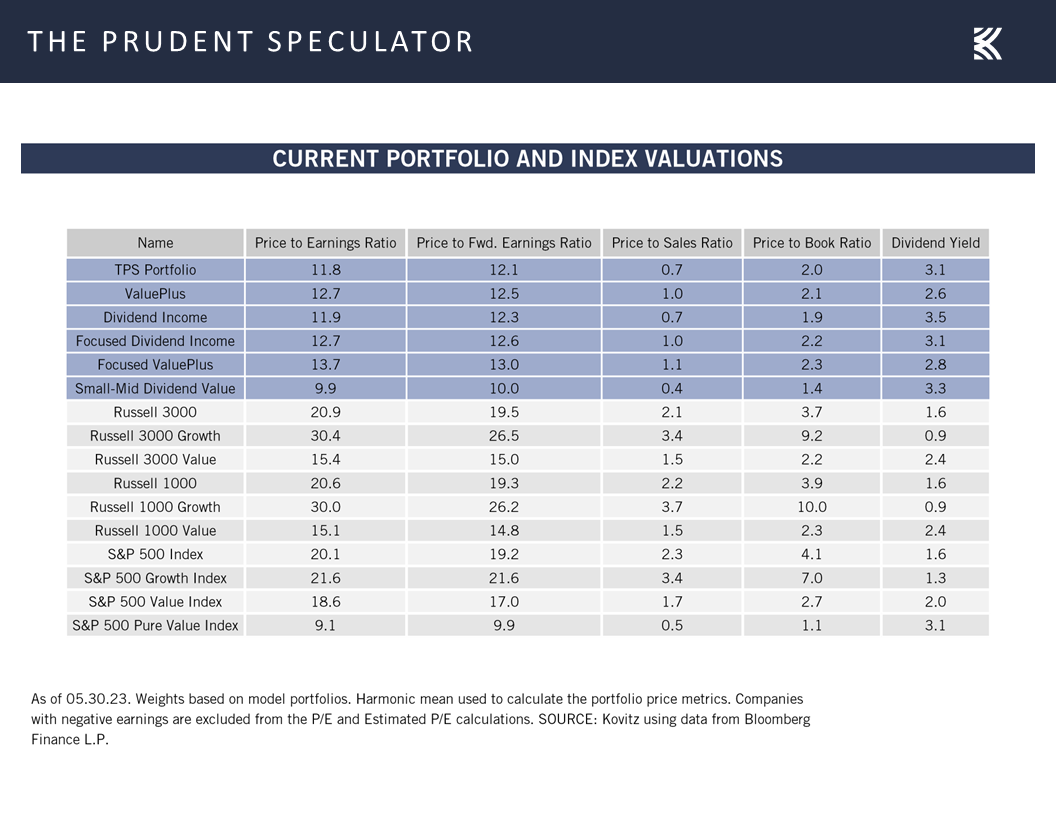

More importantly, we like the valuation metrics associated with our broadly diversified portfolios of what we believe to be undervalued stocks.

Making Stuff Up – VZ the Latest to Fall on Questionable “News”

As we said in the June Edition of The Prudent Speculator, it would seem that we need an entire salt shaker rather than just a grain of salt to navigate the headlines. This is especially true today when half-truths and untruths can go viral on social media, with large pools of money having a vested interest in influencing short-term trading.

We discussed one such incident in our recent Regional Bank Blog Post involving a company called Western Alliance, which was forced to respond to a patently wrong story published by The Financial Times on May 3. Believe it or not, a piece that cited only, “two people briefed on the matter,” caused a 38% one-day plunge in the share price of the Phoenix-based lender.

The company offered the following rebuttal on May 4:

The Financial Times’ report today that Western Alliance is considering a potential sale of all or part of its business is categorically false in all respects. There is not a single element of the article that is true. Western Alliance is not exploring a sale, nor has it hired an advisor to explore strategic options.

It is shameful and irresponsible that the Financial Times has allowed itself to be used as an instrument of short sellers and as a conduit for spreading false narratives about a financially sound and profitable bank.

We are considering all of our legal options in response to today’s article.

Oh, by the way, Western on May 2 declared its regular $0.36 per share quarterly dividend and on May 3, the company said it had not experienced unusual deposit flows after the sale of First Republic Bank and other recent industry news. Total deposits were $48.8 billion as of Tuesday, May 2, up from $48.2 billion as of May 1 and flat compared with April 28, while insured deposits were 74% of total deposits.

Since then, Western disclosed that as of May 12, deposits exceeded $49.6 billion, up more than $2 billion since the March 31, while insured deposits were more than 79% of total deposits.

Western’s stock closed at $37.95 on Friday, versus a $29.57 price the day before The Financial Times piece ran, so many would say no harm, no foul, and we have not heard anything further on the legal options the company is considering.

Why bring up Western Alliance again?

The short-term damage was not as great, but we might think that some less-than-scrupulous scheme was at play on Friday morning when Bloomberg proclaimed, “Amazon Is in Talks to Offer Free Mobile Service to U.S. Prime Members.”

Not surprisingly, the “news” spread like wildfire, sending shares of telecom companies sharply lower, including those of Verizon (VZ – $34.58), with its stock hitting a 12-year low on worries of further pricing pressures for wireless services.

Never mind that the Bloomberg sources were, “Two people briefed on the matter,” while Amazon felt compelled to put out the following statement: “We are always exploring adding even more benefits for Prime members, but don’t have plans to add wireless at this time.” And, T-Mobile, AT&T and Verizon all said they were not currently in discussions with Amazon about wireless service.

“Verizon is not in negotiations with Amazon regarding the resale of its wireless network,” VZ spokesman Rich Young said. “Our company is always open to new and potential opportunities, but we have nothing to report at this time.”

True, sometimes where there is smoke there is fire, and Bloomberg claimed that Amazon was negotiating with the providers to get the lowest possible wholesale prices to offer Prime members wireless plans for $10 a month or possibly for free.

“Amazon’s talks with cellular carriers have been going on for six to eight weeks and have also included AT&T at times,” Bloomberg asserted, though it conceded, “But the mobile service plans may take several more months to launch and could be scrapped.”

Of course, we would tend to agree with an RBC analyst who stated, “We struggle with where AMZN’s pricing leverage vs. the (wireless) carriers would come from. Obviously, the carriers aren’t going to enter into an unprofitable deal.”

Hopefully needless to say, we continue to like VZ and the stock yields 7.5% today, while trading for less than 8 times forward earnings expectations. Yes, competition is fierce, but we note that the last time the stock traded at the current price, EPS was just north of $2.00 and the quarterly dividend was $0.50 per share. Today, the consensus forecast for EPS this year is $4.68 while the dividend payout is $0.6525 per quarter.

Our Target Price stands at $59, but the utility-stock-like yield requires little in the way of capital appreciation for us to think VZ will be a rewarding long-term investment.

Given all the misinformation facing investors, we suspect we often will be referencing the Abraham Lincoln quotation, “How many legs does a dog have if you call his tail a leg? Four. Saying that a tail is a leg doesn’t make it a leg.”

Stock Market News: Updates on nine stocks across six different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Interest Rates, Debt Ceiling, an Economic Outlook and more Stock News

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Debt Ceiling, Interest Rates, an Economic Outlook and more stock news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Portfolio Trades – 3 Transactions for 3 Accounts

Week in Review – Handsome Gains Thanks to Big Friday Rally

Debt Ceiling – Disaster Averted…for the 79th Time

Economic Outlook – Pessimism Remains High But Still No Contraction

Reason & Evaluation – Recessions/The Great Inflation and Equity Returns

Goldilocks – Monthly Jobs Report Almost Perfect

Interest Rates – Low By Historical Standards; Historical Perspective; Stocks Remain Attractively Valued

Making Stuff Up – VZ the Latest to Fall on Questionable “News”

Stock News – Updates on nine stocks across six different sectors

Week in Review – Handsome Gains Thanks to Big Friday Rally

Given that the Dow Jones Industrial Average closed the holiday-shortened trading week up better than 2% and more than 1000 points above its weekly low-water mark set shortly after the open on Thursday, the equity markets offered another reminder that volatility works in both directions.

Happily, there have been more strongly positive weeks than decidedly negative weeks throughout history, so much so that the long-term trend for stocks is significantly higher, with gains for Value Stocks averaging 13.7% per annum since the launch of The Prudent Speculator in March 1977.

Of course, very few investors have managed to achieve that sort of return, primarily because they forget that the secret to success in stocks is not to get scared out of them. Sadly, as our oft-cited data from research firm DALBAR shows, equity (and fixed income) fund investors have proved to be lousy market timers, costing themselves 2.8% per annum (stocks) and 4.7% (bonds) per annum over the past 30 years. No doubt, there is a lot of buying high and selling low going on.

Debt Ceiling – Disaster Averted…for the 79th Time

The challenge, of course, is coping with disconcerting events such as the recent debt-ceiling drama. Folks were faced with warnings from the main-stream media and financial press that a polarized Congress might let Uncle Sam default on its obligations with disastrous implications for the economy and investments.

To be sure, there was no assurance that Washington would agree on legislation before the so-called X-Date when the Treasury essentially would run out of money, but here is what had happened direct from the Treasury’s website the previous six-and-one-half-dozen times the country faced such a potentially monumental problem,…

Congress has always acted when called upon to raise the debt limit. Since 1960, Congress has acted 78 separate times to permanently raise, temporarily extend, or revise the definition of the debt limit – 49 times under Republican presidents and 29 times under Democratic presidents. Congressional leaders in both parties have recognized that this is necessary.

…while arguably the most difficult debt-ceiling battle that ever occurred (back in 2011) proved to be a great time for long-term-oriented investors to be buying stocks, despite Standard & Poor’s downgrading the U.S. credit rating on August 5 of that year.

Obviously, it isn’t easy to keep the faith through thick and thin, but we find the Vannevar Bush admonition helpful, “Fear cannot be banished, but it can be calm and without panic; it can be mitigated by reason and evaluation.”

After all, there seemingly is always something for equity participants to worry about. Just since the end of the Great Financial Crisis, there have been numerous scary events, yet equities generally have proved very rewarding in the fullness of time for those who remember that time in the market trumps market timing.

Economic Outlook – Pessimism Remains High But Still No Contraction

Alas, we find that even professional investors and market pundits often are not interested in Mr. Bush’s reason and evaluation, choosing instead to pontificate on what they think should happen and ignoring what has occurred previously.

We can debate the value of studying the past, as the Greek philosopher Heraclitus states, “No man ever steps in the same river twice. For it’s not the same river and he’s not the same man.”

However, we are flabbergasted when seemingly smart-sounding financial experts tell us, for example, that you don’t want to be in stocks if a recession is on the horizon. On the surface, that is logical, and we concede that it would be nice to have avoided the modest average loss during the 15 recessions that have taken place since 1929, but, as the saying goes, economists have predicted nine of the last five recessions.

Given that the National Bureau of Economic Research (the “official” statistician) does not determine the dates until after the fact, knowing in advance when contractions will begin and end is virtually impossible, as evidenced by the fact that the odds of a U.S. recession over the ensuing 12 months (tabulated by Bloomberg), have been at 50% or greater since August 2022,

yet Q3 2022 and Q4 2022 real (inflation adjusted) GDP growth came in at impressive rates of 3.2% and 2.6%, respectively, while Q1 2023 growth was a decent 1.3%,

with said projection made prior to Friday’s much-better-than-expected labor situation report in which 339,000 new jobs were created and the prior two month’s tallies were revised upward by a combined 93,000 payrolls.

Famed fund manager Peter Lynch once remarked, “Far more money has been lost by investors in preparing for corrections, or anticipating corrections, than has been lost in the corrections themselves.” The table below vividly confirms his assertion as folks fearing that a recession is around the corner likely missed out on the solid gains, on average, in the year before the official downturn starts. Even worse, they are likely to have missed out on spectacular returns, on average, in the year after a recession ends, as all-clear signals are seldom issued…or believed.

Reason & Evaluation – Recessions/The Great Inflation and Equity Returns

This is not to say that it might not be different this time…so we offer another example of reason and evaluation to hopefully help to mitigate fear. Those concerned that the Federal Reserve’s current fight with inflation will end miserably for stocks, might want to consider the last such battle during the late-1970’s and early-1980’s. With a double-digit percentage increase in the consumer price index wreaking havoc, the Paul Volcker Fed vanquished the Great Inflation, but not without causing two recessions in 1980 and 1981.

This is just one data point and interest rates were sky high back then, so statisticians might dismiss the relevancy, but Value Stocks enjoyed a superlative 24.7% average return during the eight Volcker years and Dividend Payers turned in an 18.7% annualized return. Remember that those figures are per year, meaning a more than four-fold advance for Value and a nearly three-fold advance for Dividend Payers over the full eight years. Ah, the miracle of compounding!

Goldilocks – Monthly Jobs Report Almost Perfect

Anything can happen as we go forward, and we realize that future economic numbers may not be as Goldilocks-like as was Friday’s employment report, with the higher-than-expected increase in the jobless rate to 3.7%,

and the surprising tick down in wage growth to 4.3%

suggesting to some that the Federal Reserve has more room to be patient with future hikes in the Fed Funds rate.

Interest Rates – Low By Historical Standards; Historical Perspective; Stocks Remain Attractively Valued

We’ll let traders worry about the Fed as we think Jerome H. Powell & Co. are not far from the end of the tightening cycle, while the historical evidence suggests that stocks have performed fine, on average, whether interest rates are high or low,

with about the only conclusion that can be drawn about interest rates and asset prices being that a rising long-term government bond rate is bad for long-term government bond prices.

Further, though rates definitely are higher than where they had been for much of the last decade, the current 3.69% yield on the 10-Year U.S. Treasury is well below the 5.85% average since the launch of The Prudent Speculator more than 46 years ago. As such, we think long-term interest rates remain low by historical standards, providing support for equities in general,

especially as corporate profits are likely to continue to grow, with estimates from Standard & Poor’s for EPS for the S&P 500 this year and next increasing last week.

More importantly, we like the valuation metrics associated with our broadly diversified portfolios of what we believe to be undervalued stocks.

Making Stuff Up – VZ the Latest to Fall on Questionable “News”

As we said in the June Edition of The Prudent Speculator, it would seem that we need an entire salt shaker rather than just a grain of salt to navigate the headlines. This is especially true today when half-truths and untruths can go viral on social media, with large pools of money having a vested interest in influencing short-term trading.

We discussed one such incident in our recent Regional Bank Blog Post involving a company called Western Alliance, which was forced to respond to a patently wrong story published by The Financial Times on May 3. Believe it or not, a piece that cited only, “two people briefed on the matter,” caused a 38% one-day plunge in the share price of the Phoenix-based lender.

The company offered the following rebuttal on May 4:

The Financial Times’ report today that Western Alliance is considering a potential sale of all or part of its business is categorically false in all respects. There is not a single element of the article that is true. Western Alliance is not exploring a sale, nor has it hired an advisor to explore strategic options.

It is shameful and irresponsible that the Financial Times has allowed itself to be used as an instrument of short sellers and as a conduit for spreading false narratives about a financially sound and profitable bank.

We are considering all of our legal options in response to today’s article.

Oh, by the way, Western on May 2 declared its regular $0.36 per share quarterly dividend and on May 3, the company said it had not experienced unusual deposit flows after the sale of First Republic Bank and other recent industry news. Total deposits were $48.8 billion as of Tuesday, May 2, up from $48.2 billion as of May 1 and flat compared with April 28, while insured deposits were 74% of total deposits.

Since then, Western disclosed that as of May 12, deposits exceeded $49.6 billion, up more than $2 billion since the March 31, while insured deposits were more than 79% of total deposits.

Western’s stock closed at $37.95 on Friday, versus a $29.57 price the day before The Financial Times piece ran, so many would say no harm, no foul, and we have not heard anything further on the legal options the company is considering.

Why bring up Western Alliance again?

The short-term damage was not as great, but we might think that some less-than-scrupulous scheme was at play on Friday morning when Bloomberg proclaimed, “Amazon Is in Talks to Offer Free Mobile Service to U.S. Prime Members.”

Not surprisingly, the “news” spread like wildfire, sending shares of telecom companies sharply lower, including those of Verizon (VZ – $34.58), with its stock hitting a 12-year low on worries of further pricing pressures for wireless services.

Never mind that the Bloomberg sources were, “Two people briefed on the matter,” while Amazon felt compelled to put out the following statement: “We are always exploring adding even more benefits for Prime members, but don’t have plans to add wireless at this time.” And, T-Mobile, AT&T and Verizon all said they were not currently in discussions with Amazon about wireless service.

“Verizon is not in negotiations with Amazon regarding the resale of its wireless network,” VZ spokesman Rich Young said. “Our company is always open to new and potential opportunities, but we have nothing to report at this time.”

True, sometimes where there is smoke there is fire, and Bloomberg claimed that Amazon was negotiating with the providers to get the lowest possible wholesale prices to offer Prime members wireless plans for $10 a month or possibly for free.

“Amazon’s talks with cellular carriers have been going on for six to eight weeks and have also included AT&T at times,” Bloomberg asserted, though it conceded, “But the mobile service plans may take several more months to launch and could be scrapped.”

Of course, we would tend to agree with an RBC analyst who stated, “We struggle with where AMZN’s pricing leverage vs. the (wireless) carriers would come from. Obviously, the carriers aren’t going to enter into an unprofitable deal.”

Hopefully needless to say, we continue to like VZ and the stock yields 7.5% today, while trading for less than 8 times forward earnings expectations. Yes, competition is fierce, but we note that the last time the stock traded at the current price, EPS was just north of $2.00 and the quarterly dividend was $0.50 per share. Today, the consensus forecast for EPS this year is $4.68 while the dividend payout is $0.6525 per quarter.

Our Target Price stands at $59, but the utility-stock-like yield requires little in the way of capital appreciation for us to think VZ will be a rewarding long-term investment.

Given all the misinformation facing investors, we suspect we often will be referencing the Abraham Lincoln quotation, “How many legs does a dog have if you call his tail a leg? Four. Saying that a tail is a leg doesn’t make it a leg.”

Stock Market News: Updates on nine stocks across six different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.