“Let me comment briefly on recent developments in the banking sector. Conditions in that sector have broadly improved since early March, and the U.S banking system is sound and resilient.” So proclaimed Jerome H. Powell on May 3 as he and his colleagues at the Federal Reserve decide to raise their target for the Federal Funds rate by another 25 basis points to a range of 5.0% to 5.25%.

That statement came three days after the hasty weekend sale of First Republic (FRC), the troubled lender whose $173 billion in loans and $30 billion of securities were sold to JPMorgan Chase (JPM), which also assumed $92 billion in deposits. Flighty depositors pulled $100 billion from FRC in Q1, joining the runs on the bank at Silicon Valley Bancorp and Signature Bank that led to the March demise of those institutions.

Of course, all three failed banks shared the same fast-growth-from-wealthy-mostly-uninsured-depositors profile, which provided plenty of support for JPM CEO Jamie Dimon to declare, “There may be another small one, but this pretty much resolves them all. This part of the crisis is over.”

JUST THE FACTS MA’AM

Those who choose to pay attention to the numbers would find it hard to argue with either Chair Powell and Mr. Dimon, given that deposits for most regional banks not named Silicon Valley, Signature or First Republic have held steady throughout the “crisis.” Let us repeat that. Despite suggestions from more than a few prominent market watchers, there has NOT been a massive run on the regional banks…as far as we know from regulatory filings.

True, we have not had updates for five weeks from many of these companies, but we note that the two banks supposedly in the most distress, as determined by the collapse in their stock prices, confirmed the view that there has not, as yet, been a systemic run on the bank.

After Bloomberg ran a misleading story the evening of May 4,

PacWest Bancorp., a regional bank teetering following the collapse of three rival California-based lenders, has been weighing a range of strategic options, including a sale, according to people familiar with the matter.

the Los Angeles bank responded,

Our message remains consistent with what was conveyed last week with earnings. As previously announced, the Company has explored strategic asset sales, including moving the $2.7 billion

Lender Finance loan portfolio to held for sale in 1Q23. This planned sale remains on track and upon completion will accelerate our CET1 capital ratio to 10%+ (from 9.21% at 1Q23). Additionally, in accordance with normal practices the Company and its Board of Directors continuously review strategic options. Recently, the Company has been approached by several potential partners and investors – discussions are ongoing. The company will continue to evaluate all options to maximize shareholder value.

The bank has not experienced out-of-the-ordinary deposit flows following the sale of First Republic Bank and other news. Core customer deposits have increased since March 31, 2023, with total deposits totaling $28 billion as of May 2, 2023 with insured deposits totaling 75% vs. 71% at quarter end and 73% as of April 24, 2023. In addition, the company recently paid down $1 billion of borrowings with our excess liquidity. Our cash and available liquidity remains solid and exceeded our uninsured deposits, representing 188% as of May 2, 2023.

At the beginning of the year, the Company announced a new strategic plan designed to maximize shareholder value by focusing on various elements, including strengthening our community bank focus, growing our HOA business, exiting non-core products, and improving our operational efficiency. We have been executing this strategy and have accelerated many of these goals in response to recent market volatility in the banking industry.

True, PacWest’s shares have collapsed, losing 50% on May 4 alone, but there is often a disconnect between the price of a stock and the value of the underlying business, with the “meme stock” craze the last few years offering vivid illustration. After all, we hardly think a 40% two-day-rebound May 3-4 in bankrupt Bed, Bath & Beyond shares tells us that the stock won’t eventually be worthless.

And, if PacWest wasn’t exactly “teetering” as Bloomberg claimed, what are we to think of Western Alliance, which was forced to respond to a patently wrong story published by The Financial Times on May 3 that led to the Phoenix-based lender offering the following rebuttal on May 4:

The Financial Times’ report today that Western Alliance is considering a potential sale of all or part of its business is categorically false in all respects. There is not a single element of the article that is true. Western Alliance is not exploring a sale, nor has it hired an advisor to explore strategic options.

It is shameful and irresponsible that the Financial Times has allowed itself to be used as an instrument of short sellers and as a conduit for spreading false narratives about a financially sound and profitable bank.

We are considering all of our legal options in response to today’s article.

Oh, by the way, Western on May 2 declared its regular $0.36 per share quarterly dividend and on May 3, the company said it had not experienced unusual deposit flows after the sale of First Republic Bank and other recent industry news. Total deposits were $48.8 billion as of Tuesday, May 2, up from $48.2 billion as of May 1 and flat compared with April 28, while insured deposits were 74% of total deposits.

Clearly, the value of Western Alliance’s business was not worth 38% less on May 4 than it was on May 3, even as the market argued otherwise.

YELLING FIRE IN A CROWDED SWIMMING POOL

Unfortunately, facts don’t seem to matter to some market watchers, many of whom have a vested interest in spreading incorrect information. After all, even those who we might think are well intentioned in their pleas for Uncle Sam to step in with higher deposit insurance limits are not being genuine in their arguments.

Hedge fund manager Bill Ackman tweeted this week, “The regional banking system is at risk. SVB’s depositors’ bad weekend woke up uninsured depositors everywhere. The rapid rise in rates impaired assets and drained deposits. Zeroing out shareholders and bondholders massively increased the banks’ cost of capital. CRE losses loom. Meanwhile, higher-yield, more user-friendly alternatives beckon.”

There has not been a systemwide drain of deposits, while higher-yielding alternatives have been beckoning for more than a few quarters. Yes, many wealthy investors have just woken up to the fact that money market funds and T-Bills offer higher yields, but for our managed-account clients we made the shift nine months ago.

To be fair, Mr. Ackman went on to say, “Banking is a confidence game. At this rate, no regional bank can survive bad news or bad data as a stock price plunge inevitably follows, insured and uninsured deposits are withdrawn and ‘pursuing strategic alternatives’ means an FDIC shutdown over the coming weekend. And there is no incentive to bid until Sunday after the failure.”

Of course, share prices for nearly every regional bank have been under pressure since March and yet there has not yet been a flood of withdrawals, but we very much realize that banking is a confidence game. Yes, depositors could choose to flee in the days and weeks ahead, but that is not what we think will happen, given that customer relationships generally are long in tenure, the deposit bases generally are very diverse in nature and many folks need easy access to their cash.

NOT FOR THE FAINT OF HEART

As we said in our prior update on the subject, for our managed account strategies, we hold an assortment of stocks in the Financials sector, including those in the industry groups Financial Services, Insurance and Banks. The whack to those holdings wasn’t helpful to recent performance, but the broad diversification we have long employed did its job in limiting overall downside.

And as we frequently note in these pages, we use market turbulence to make opportunistic changes in our portfolios. We thoroughly enjoy buying things on sale and some of the discounts in the Financials sector lately have been terrific in our view. Of course, the steeper the discount, the more excited we get, so it was tempting to buy large quantities of beaten-down banks. We did make changes, but still are partial to the broad industry and sector diversification we have employed for more than four decades.

We do not mean to suggest that there are not higher-yielding alternatives to bank accounts elsewhere nor that today’s near pristine credit quality won’t give way to a rise in non-performing assets. Further, we understand that additional regulation will be coming, while banks will bear additional deposit insurance costs. Clearly, regional banks have high risk today to go along with their high reward potential, so investors should tread carefully, even as we never lose sight of Warren Buffett’s admonition, “Uncertainty is the friend of the buyer of long-term values.”

PUNISHMENT DOES NOT FIT THE CRIME

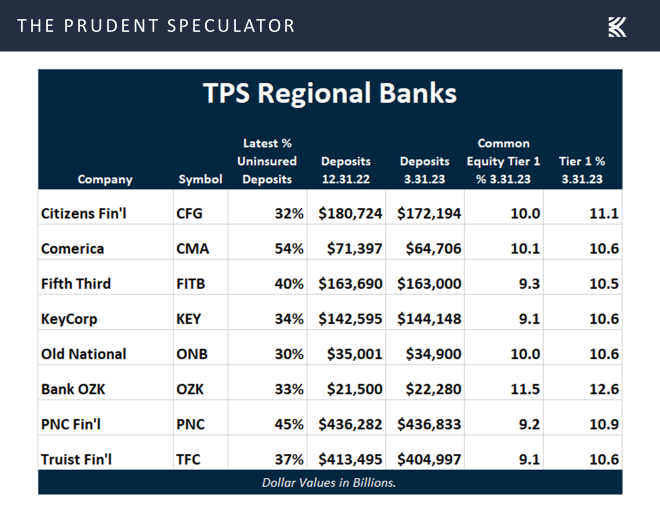

For those looking to do a little shopping in the bargain-basement-banking bin, here are three of the banks that we think will survive the current near-term carnage and will go on to provide significant long-term share price appreciation and dividend rewards.

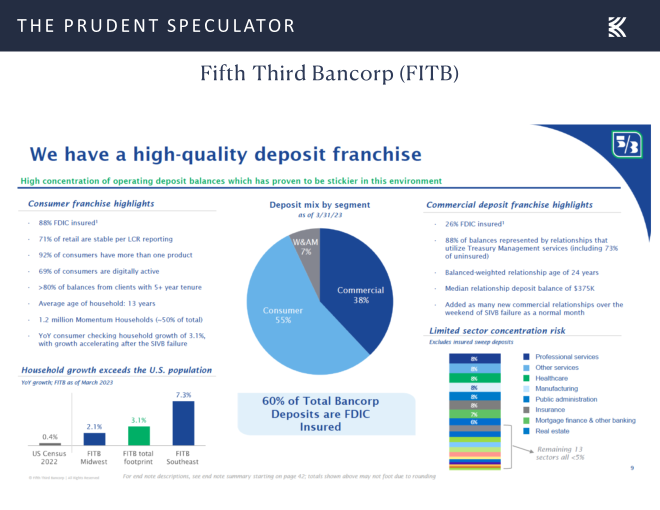

FIFTH THIRD BANCORP (FITB)

Fifth Third is a diversified financial services company with $208 billion in assets, operating numerous full-service banking centers in the Midwest and Southeastern U.S.

Using lessons from the Great Financial Crisis, management has endeavored to de-risk the loan book over the past decade, with office commercial real estate loans of $1.6 billion representing just 1.3% of total loans as of the end of Q1. CEO Tim Spence recently reminded, “While the economic environment remains uncertain, Fifth Third has spent nearly a decade focused on positioning the bank to generate sustainable financial results. As we navigate the environment, we will follow our guiding principles of stability, profitability, and growth – in that order.”

Additionally, FITB’s diverse base of fee-generating businesses (across card/payment, investment banking/management, mortgage, etc.) adds stability even if higher interest rates dent loan demand. Regional banks have been under severe pressure lately, but FITB saw deposits (a relatively low 40% are uninsured) hold steady in Q1 and the company classified almost no securities as held-to-maturity at the end of 2022. The forward P/E below 8 is near the lowest relative to the S&P 500 in the past decade, presenting an attractive opportunity to own a stable regional bank with a substantial 5% dividend yield.

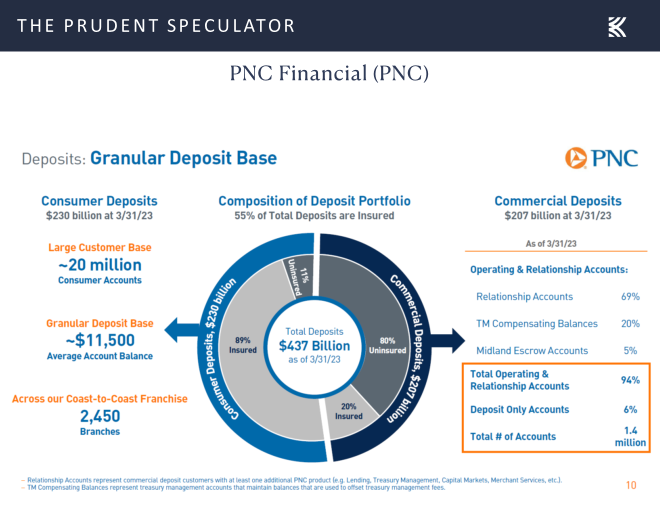

PNC FINANCIAL (PNC)

Pittsburgh-based regional banking powerhouse PNC, which was one of the bidders for First Republic, earned $3.98 per share in the latest quarter, a gain both year over year and quarter over quarter. Loans and deposits both grew modestly versus the prior quarter, efficiency and operating leverage improved, and charge-offs declined.

PNC’s CFO Robert Reilly took care to provide detail related to several issues affecting regional banks today like their deposit base and the impact of security valuations on balance sheet equity. He also addressed commercial credit quality (office lending in particular), a segment for which credit has noticeably tightened this year.

At the end of the first quarter our deposits were 53% consumer and 47% commercial. Inside of our $230 billion of consumer deposits, approximately 90% are FDIC insured. The portfolio is very granular with an average account balance of approximately $11,500 across nearly 20 million accounts throughout our Coast-to-Coast franchise. Our $207 billion of commercial deposits are 20% insured, but importantly, approximately 95% of the total balance are held in operating and relationship accounts.

In light of the current environment, we anticipate that we will be subject to a total loss absorbing capacity requirement in some form and at some point, with a reasonable phase-in period. Importantly, as our borrowed funds continue to return to a more normalized level, we would expect to be compliant through our current issuance plans under existing TLAC requirements…As a Category III institution, we don’t include AOCI in our CET1 ratio [9.2% at quarter end], but understand why there is focus on this ratio with the inclusion of AOCI. As of March 31, 2023, our CET1 ratio including AOCI was estimated to be 7.5%, which remains above our 7.4% required level, taking into account our current stress capital buffer…While AOCI takes into account the current valuation of the securities and certain portions of our swap portfolios, it does not account for the valuation of the deposit book, which can be a meaningful offset in a rising interest rate environment. In fact, looking at PNC’s change in market value of equity over the past year, the increase in the market value of our deposits in the rapidly rising interest rate environment has significantly outpaced all unrealized losses on the asset side of the balance sheet, including securities and fixed rate loans.

While credit quality is strong across the majority of our CRE book, office is a segment receiving a lot of attention in this environment due to the shift to remote work and higher interest rates…The office portfolio was originated with an approximate loan to value of 55% to 60% and a significant majority of those properties are defined as Class A…To appropriately sensitize our portfolio, we significantly discounted net operating income levels and property values across the entire office book…Additionally, tenant retention, build-out costs and concession levels are all updated to accurately reflect market conditions. Credit quality in our office portfolio remains strong today with only 0.2% of loans delinquent, 3.5% nonperforming and a net charge-off rate of 47 basis points over the last 12 months.

PNC appears well suited to weather the latest banking predicament given shorter-duration instruments on the balance sheet and a relatively small unrealized loss on its held-to-maturity securities compared to peers. Nevertheless, shares have skidded more than 40% since the beginning of 2022 even as the company further expanded its reach via the acquisition of BBVA’s U.S. retail operation in 2021. Shares trade for less than 9 times the NTM EPS estimate and yield a whopping 5.3%, with a dividend coverage of more than 2X.

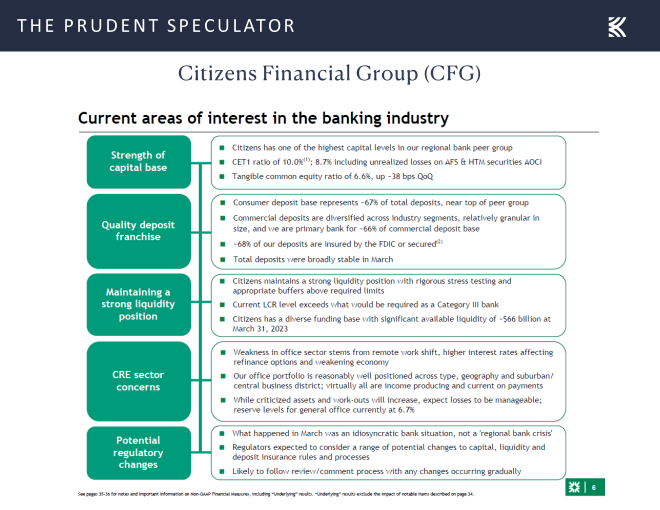

CITIZENS FINANCIAL (CFG)

Rhode Island-based regional bank Citizens Financial turned in adjusted EPS of $1.10 (vs. $1.13 est.) in Q1. Management said that churn in the deposit market continues to diminish since the bank failures, with deposits stabilizing in March.

CEO Bruce Van Saun stated, “The first quarter brought unexpected challenges in the environment, but we proved adaptable and resilient, successfully navigating through them and delivering solid financial results. Our capital, liquidity and funding position remains strong, and our deposits were broadly stable over the month of March. We remain focused on our deposit initiatives, taking care of our customers and protecting key investments while trimming expenses where we can. We are hopeful that market turmoil continues to subside, and we expect that we will be able to deliver attractive mid-teens ROTCE for the year.”

He added, “Our outlook for 2023 still shows attractive proxy for the full year, despite the challenging environment. There’s still a great deal of uncertainty which makes forecasting more difficult, but we remain confident in the strength of our franchise and the ability to weather the storm. We are building a great bank and we remain excited about our future. Our capital strength and attractive franchise should position us to be nimble and to take advantage of opportunities as they arise.”

Following the purchase of HSBC branches within its market and the acquisition of Investors Bancorp in 2021, Citizens has grown its deposit franchise by over 17% year-over-year. We think the moves complement and round out its existing territory, while adding JMP Group (securities) into the fold (also in 2021) brings diversification through additional fee generation. Fee generating activity has slowed, although not as much as for some, while a focus on maximizing operating leverage for an expanded operation prime the bank for higher returns in the current year. Shares trade for less than 6 times estimated earnings and now offer a 6.8% dividend yield.