The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss interest rates, inflation, corporate profits, valuations and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Week In Review – Stocks Pull Back Again

Patience – Lots to Worry About Along the Way, But Over Time Equities Have Proved Rewarding

Interest Rates – Treasury Yields Low By Historical Standards

Inflation – Mixed Data on CPI & PPI; Expectations Still Well Contained

Econ News – Generally Favorable Numbers; Q3 GDP Outlook Improves

Corporate Profits – Excellent Q2 Reports; Forward Estimates Rise

Valuations – Inexpensive Multiples for our Stocks

Stock News – Updates on eleven stocks across eight different sectors

Week In Review – Stocks Pull Back Again

Value again fared better than Growth, but it was a second straight down week, with the average stock in the Russell 3000 index losing 1.45% as smaller-capitalization companies suffered the biggest decline. Certainly, it is not unusual to see downside volatility, especially after the terrific gains enjoyed by the S&P 500 since March 17, 2023, and the broad-based advance in the equity markets during June and July.

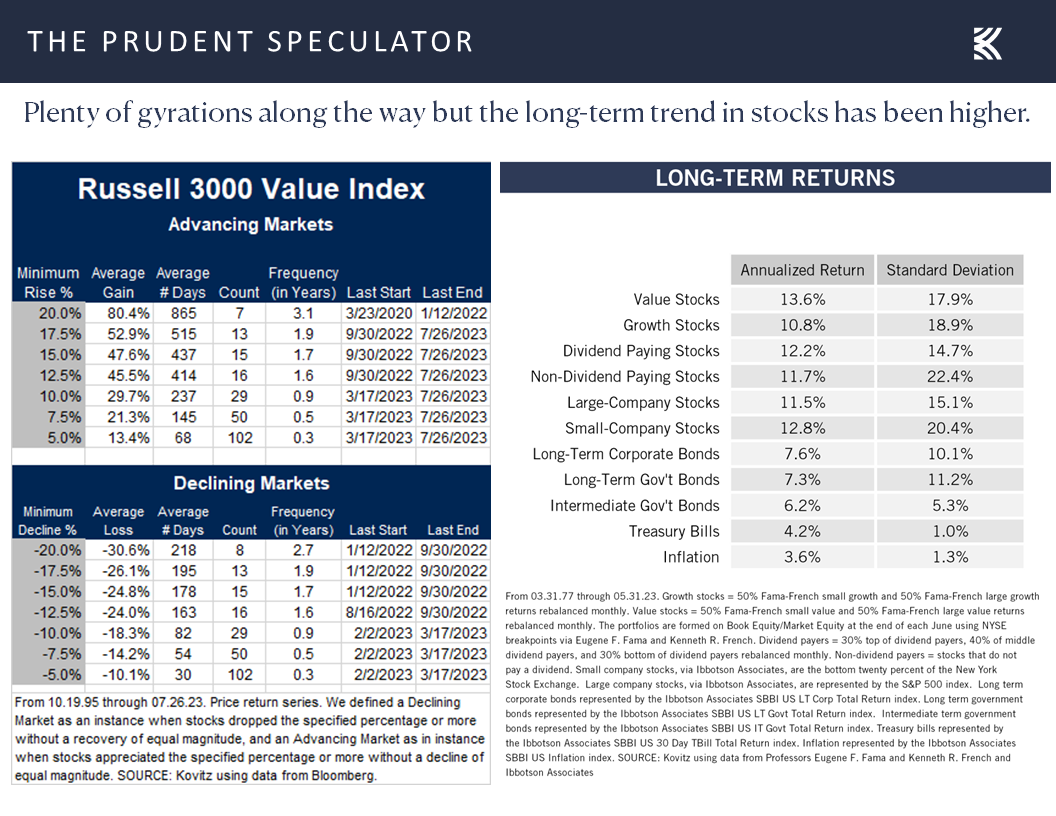

Patience – Lots to Worry About Along the Way, But Over Time Equities Have Proved Rewarding

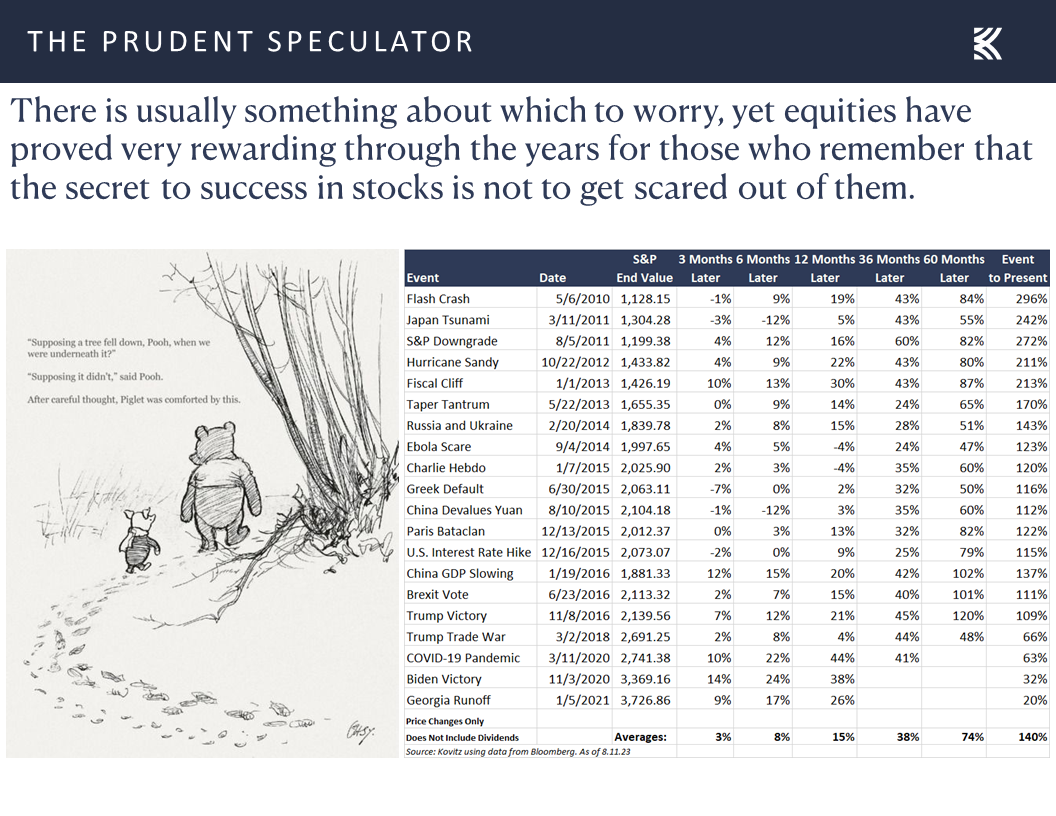

After all, despite stocks turning in excellent long-term returns over the years, trips south are part of the process. Indeed, 5% drops (this setback has more to go to get to that level) happen three times a year on average, 10% corrections take place every 11 months on average, and 20% Bear Markets occur every 2.7 years on average. Happily, rallies of even greater magnitude have occurred with equal frequency, and history shows that it is best to listen to advice from Warren Buffett if trying to time the inevitable ups and downs: “The fact that people will be full of greed, fear, or folly is predictable. The sequence is not predictable.”

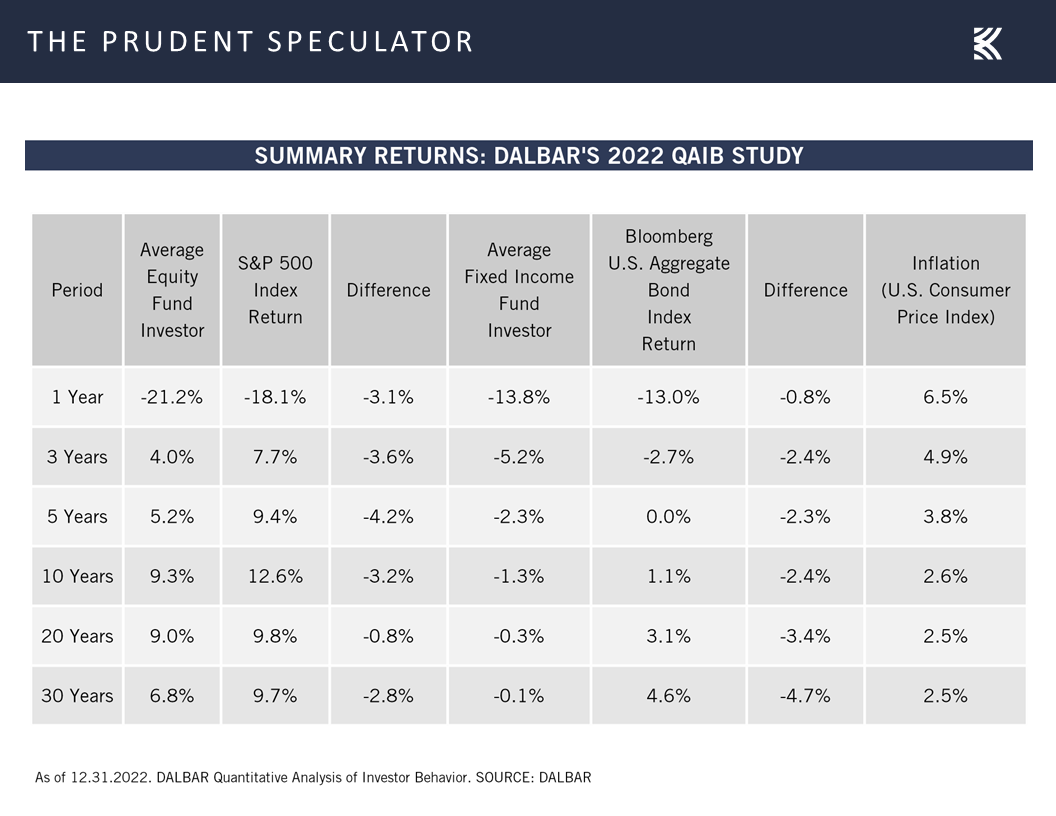

We have long believed that time in the market trumps market timing, and it is fascinating to see how poorly mutual fund investors have done over the years with their efforts to get in ahead of an advance and get out ahead of a decline. The DALBAR figures on investor returns are eye-opening, especially for Fixed Income fund owners. Hard to believe that the average bond fund player has lost money over the last 1, 3, 5, 10, 20 and 30 years. And stocks are supposedly the risky asset class?

No doubt, equity investors must contend with plenty of disconcerting headlines, but those that keep the faith through thick and thin have been handsomely rewarded in the fullness of time. No two events are ever alike, as Heraclitus states, “No man ever steps in the same river twice, for it’s not the same river and he’s not the same man,” but we think that there is great value in studying market history.

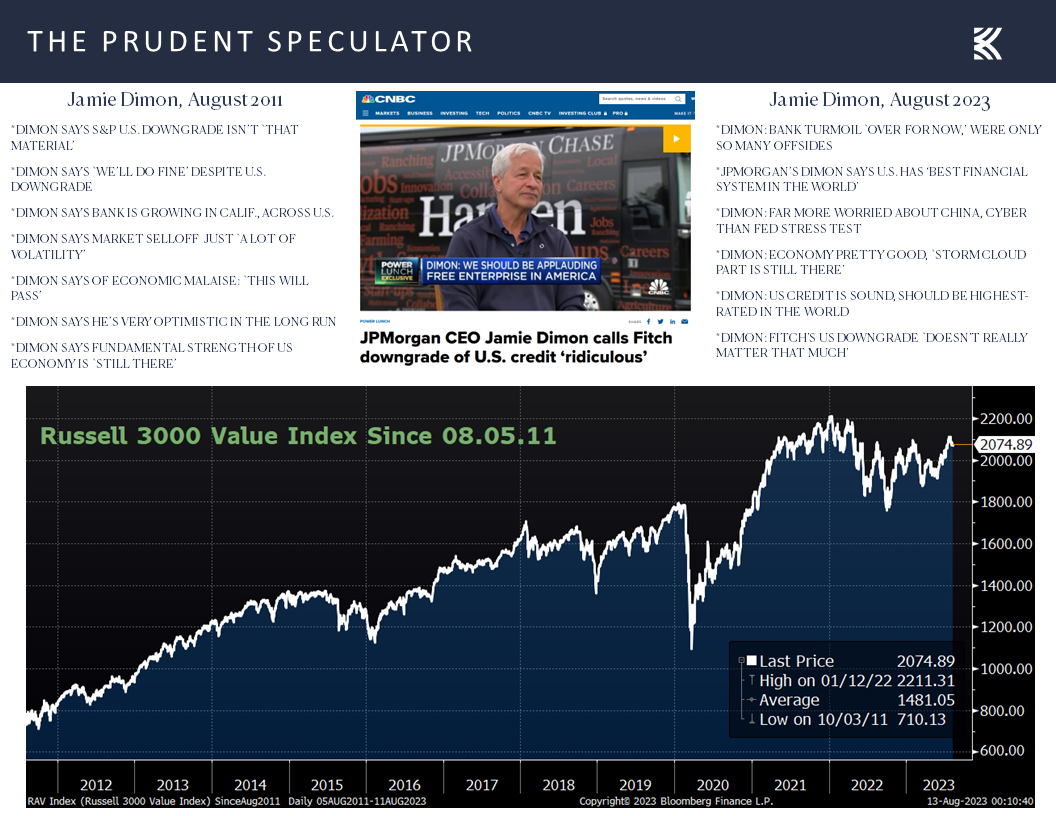

For example, the latest bogeyman and arguably the catalyst for the August swoon has been the downgrade of the rating on U.S. credit by Fitch Ratings, an event that took place 12 years ago when Standard & Poor’s did the same thing. We might question where Fitch has been all this time, especially as the political drama over raising the debt ceiling in 2011 was far worse than it was this go round, but we note that the short-term damage caused back then was overcome relatively quickly, with stocks substantially higher today.

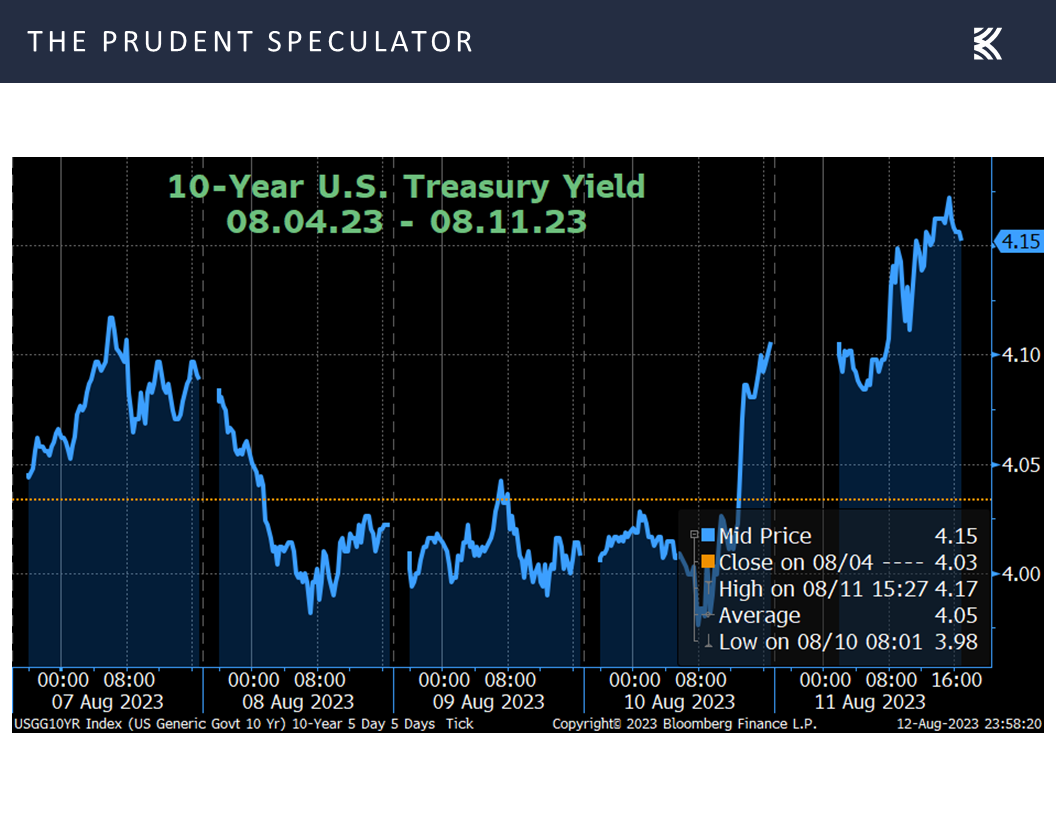

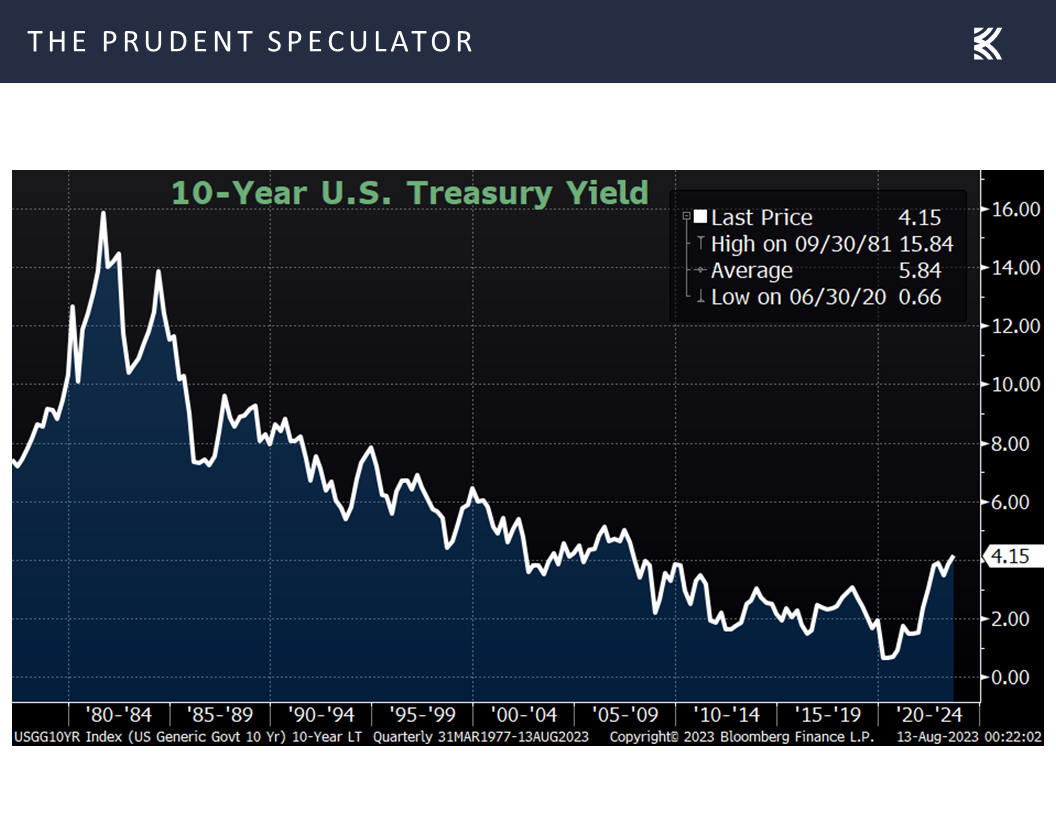

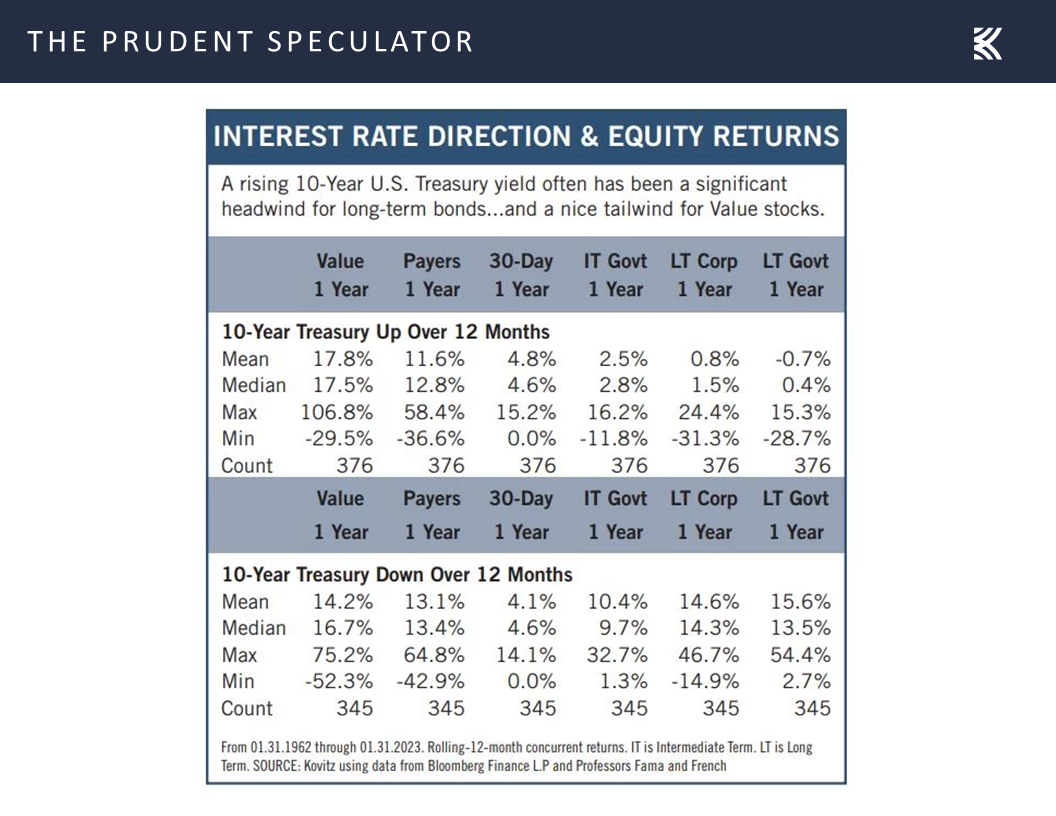

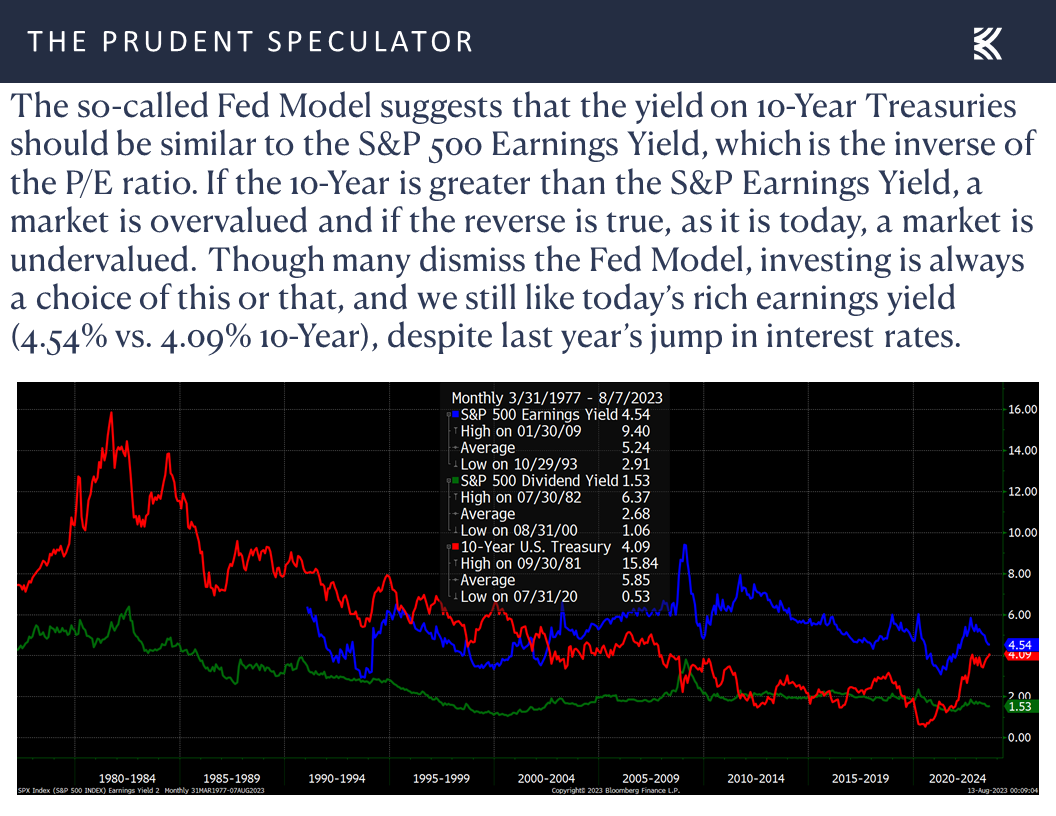

Interest Rates – Treasury Yields Low By Historical Standards

To be sure, there are other issues about which folks are concerned, as many are fretting about the rise in the yield on the 10-Year U.S. Treasury.

This is the case, even as today’s 4.15% benchmark government bond yield remains well below the 5.84% average since the inaugural edition of The Prudent Speculator was published in March 1977,

and market history shows that about the only conclusion that can be drawn from rising rates is that they are bad for the performance of…long-term bonds, though, as those big negative “Min” return figures in the chart below tell us, anything can happen.

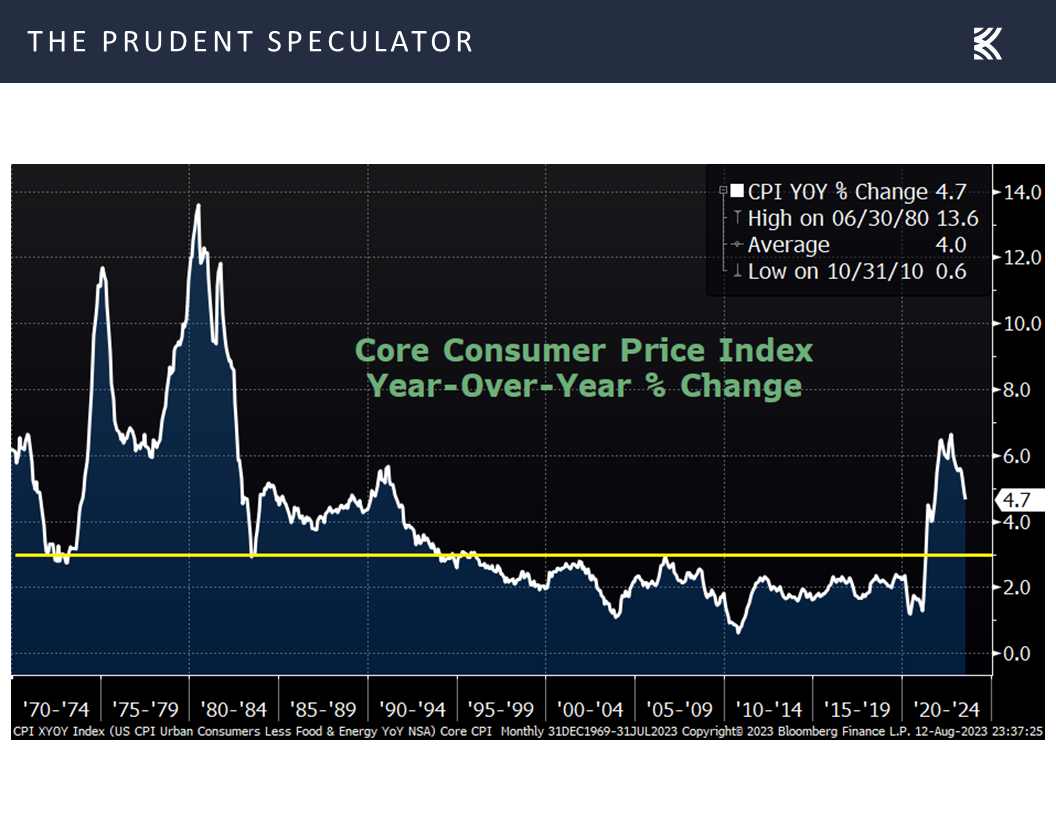

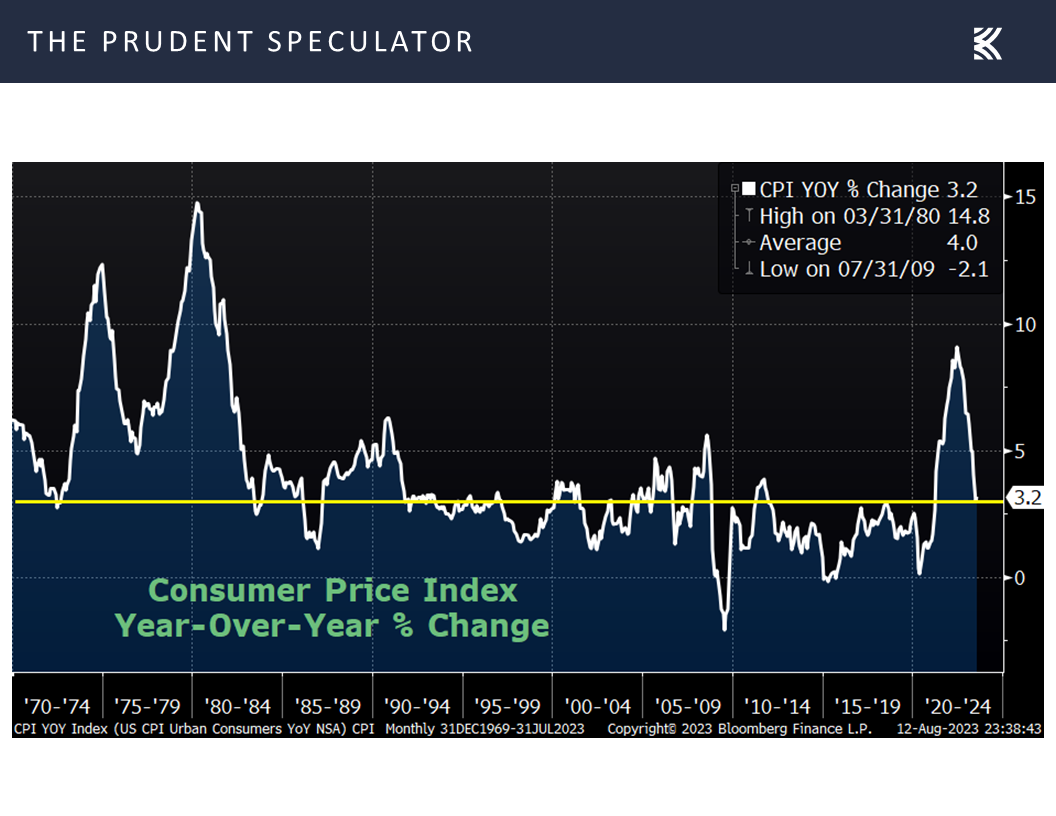

Inflation – Mixed Data on CPI & PPI; Expectations Still Well Contained

Certainly, the attention of traders last week was on the inflation figures, with stocks starting off Thursday’s action on the plus side, following news that the core (excludes volatile food and energy prices) Consumer Price Index (CPI) ticked down to 4.7% in July, compared to 4.8% in June,

while the actual CPI came in at 3.2%, up from 3.0% in June, but below projections for a 3.3% advance.

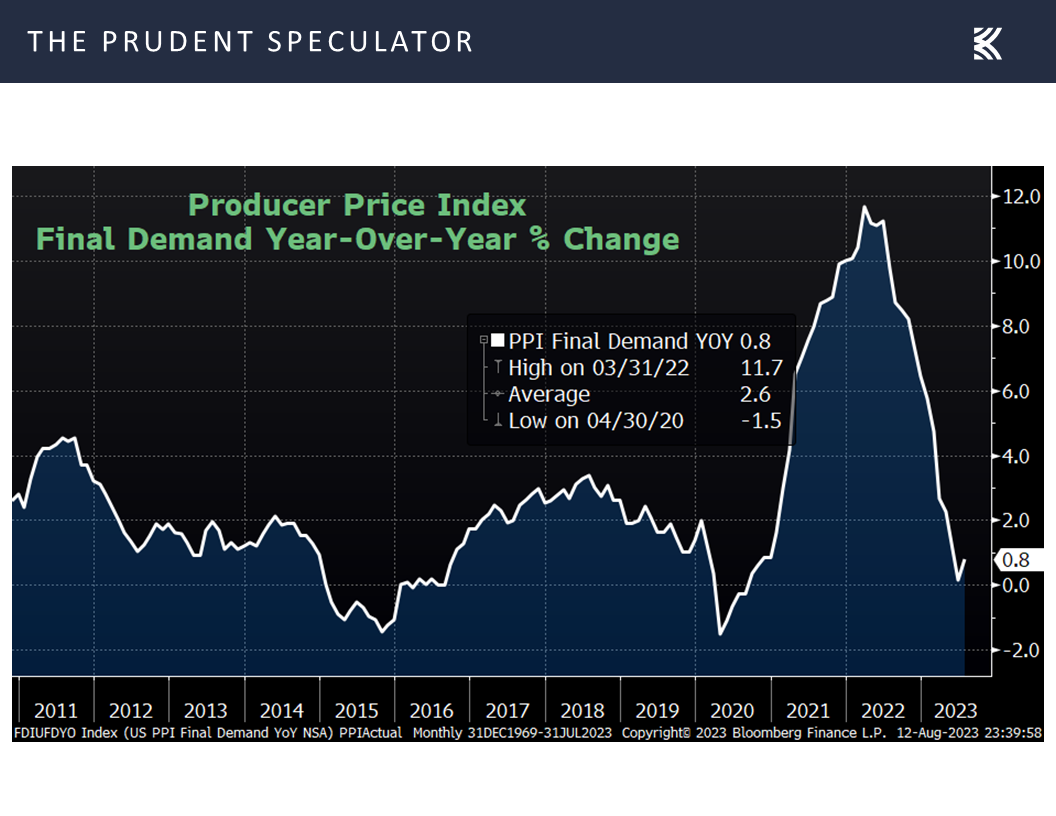

Alas, the rally on Thursday morning was short-lived as Friday saw the report of inflation at the wholesale level come in worse than expected. The Final Demand Producer Price (PPI) Index for July advanced 0.8%, up from a 0.1% increase in June, and above the 0.7% estimate, while the core (excluding food & energy) rate rose 2.4% on a year-over-year basis, in line with the prior month’s reading.

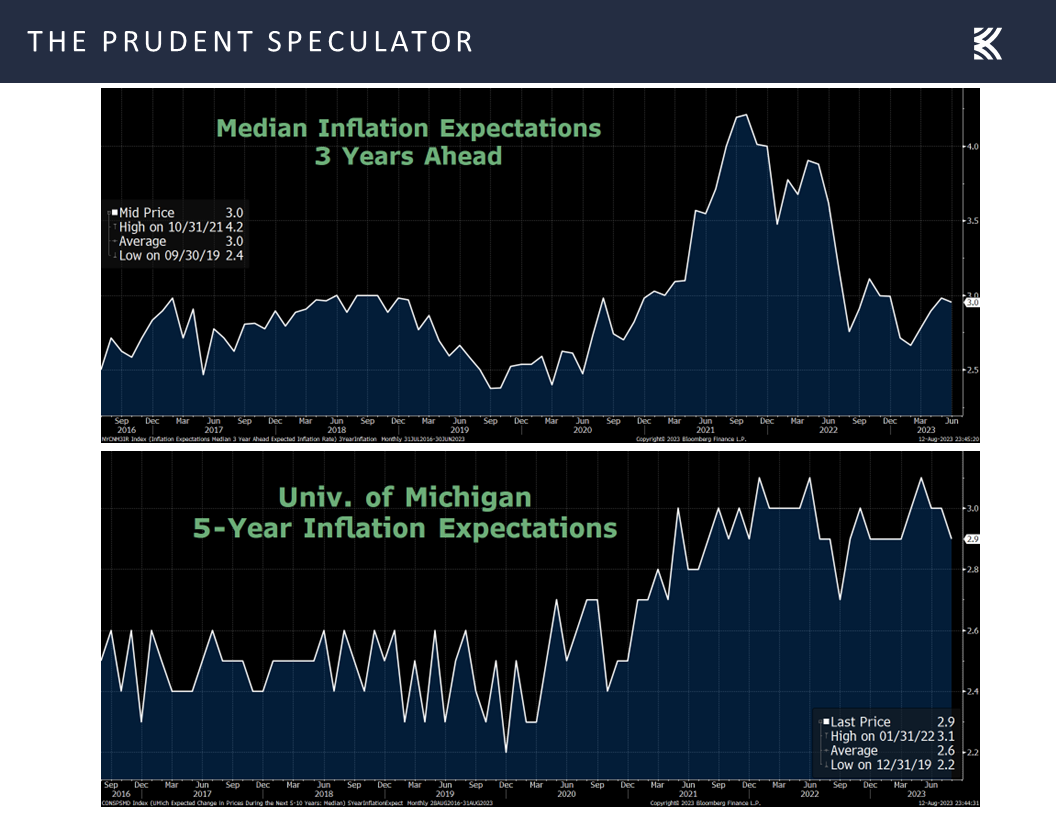

Of course, inflation expectations over the next three and five years remain well-contained, per readings from the Univ. of Michigan and the New York Fed,

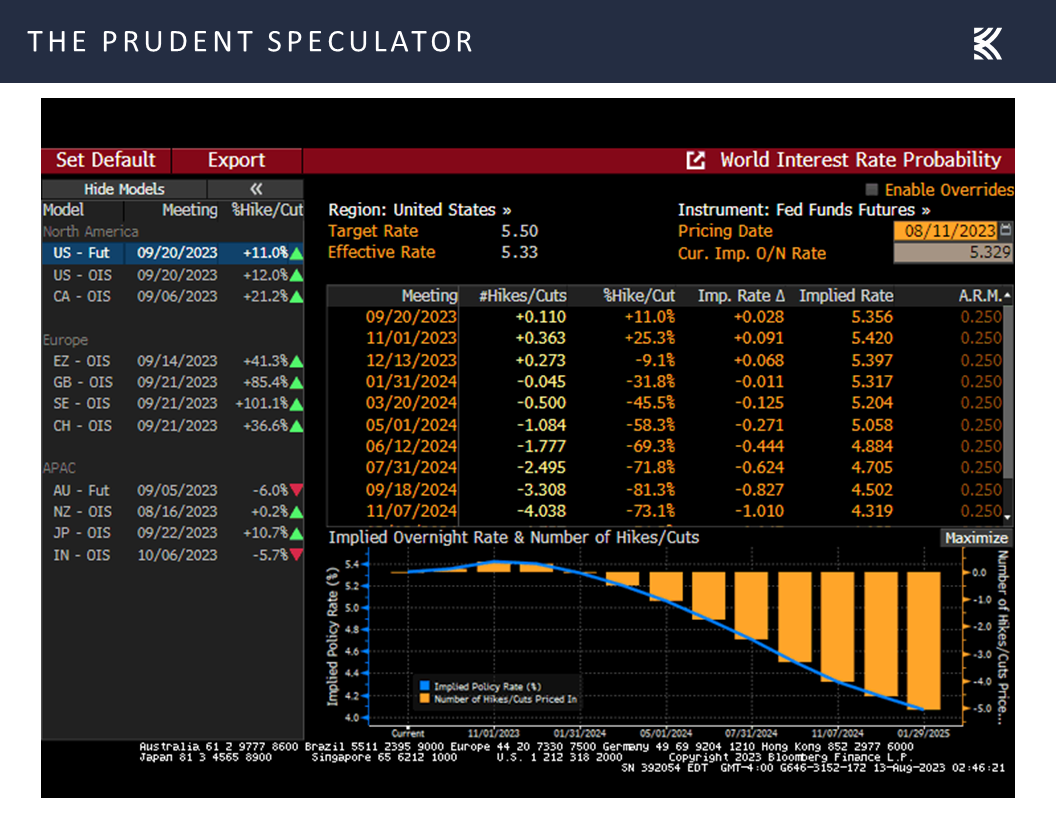

…while the Federal Funds futures market continues to forecast that Jerome H. Powell & Co. are near the end of their rate hiking cycle, with expectations that there will be several interest rate cuts in 2024.

Econ News – Generally Favorable Numbers; Q3 GDP Outlook Improves

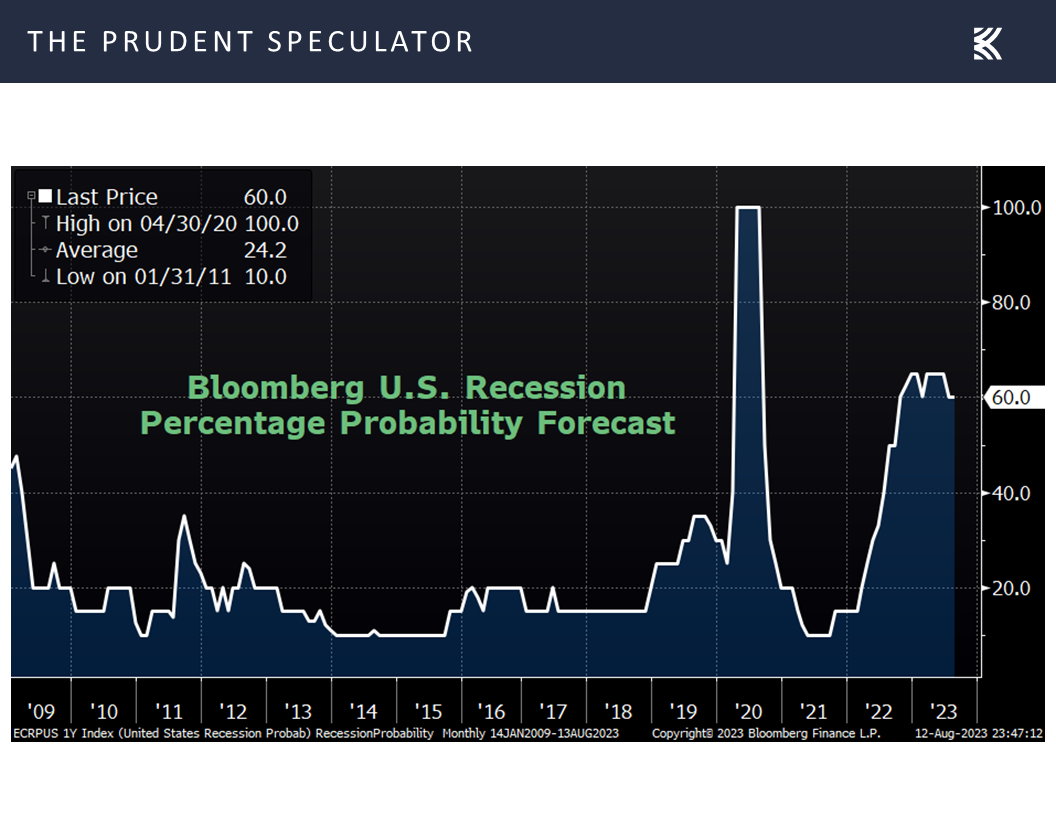

The strength of the U.S. economy remains another worry, especially with Bloomberg calculations continuing to show a 60% chance of recession in the next 12 months.

The surprisingly robust real (inflation-adjusted) GDP growth in recent quarters (3.2% in Q3 2022, 2.6% in Q4 2022, 2.0% on Q1 2023 and 2.6% in Q2 2023) calls into question those Bloomberg projections as the odds of a contraction have been 50% or greater for a year now.

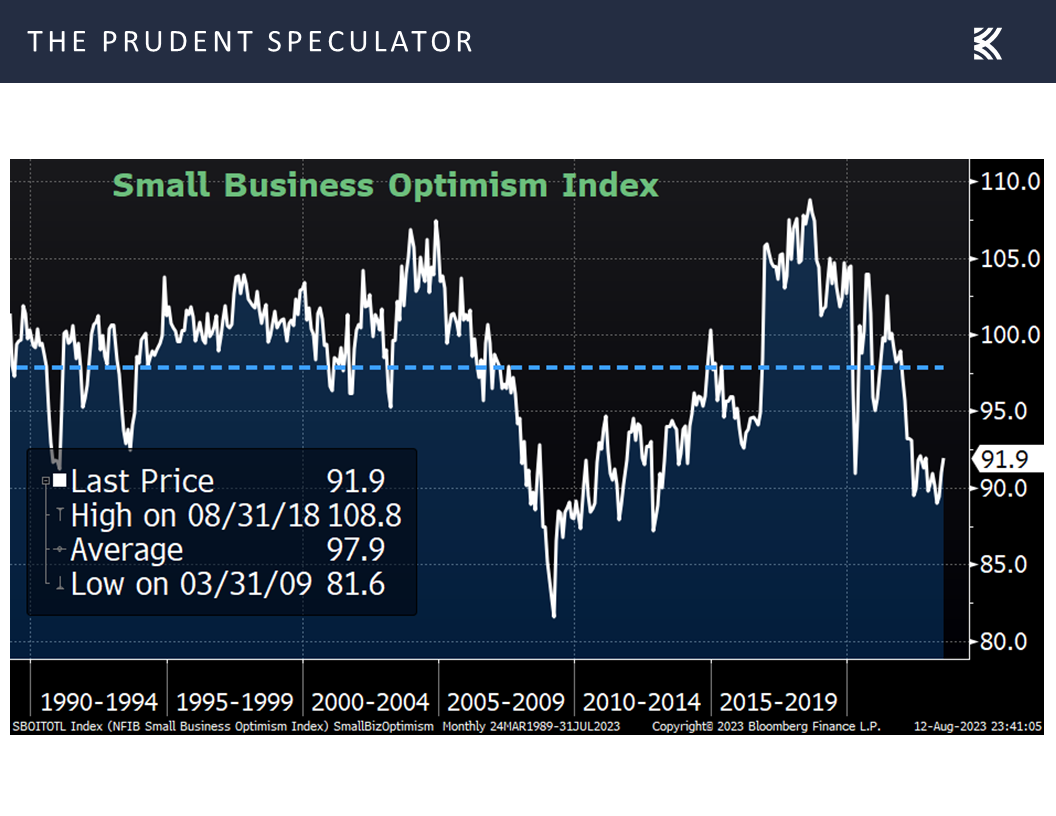

Is it any wonder that John Kenneth Galbraith proclaimed, “The only function of economic forecasting is to make astrology look respectable?” Needless to say, nobody knows for sure which way the economic data will trend, but the latest read on small-business optimism for July topped expectations,

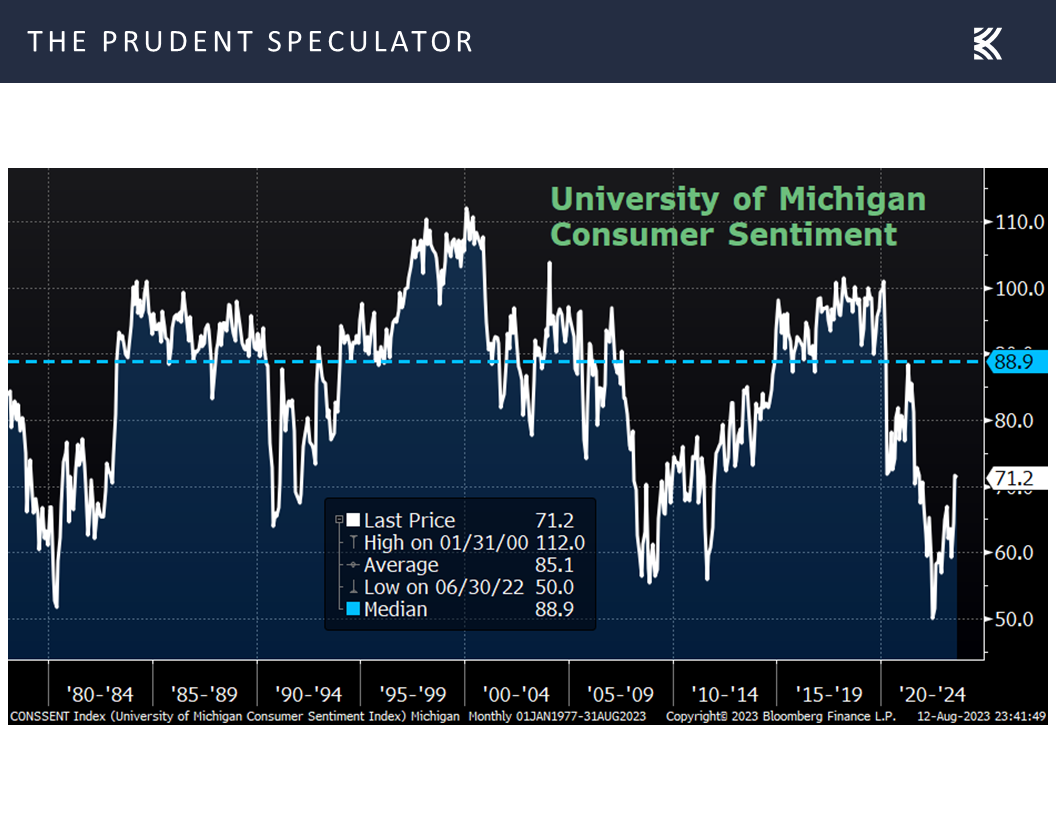

while the preliminary measure of Consumer Sentiment for August from the Univ. of Michigan matched estimates,

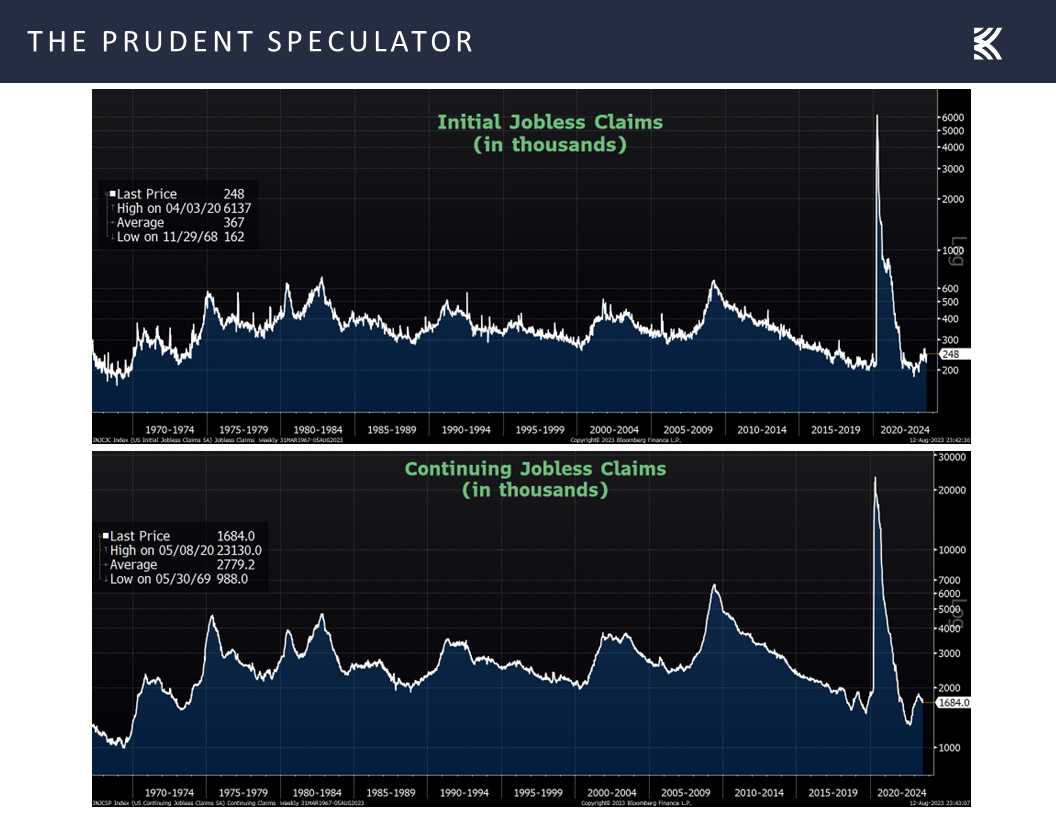

and the labor market continued to show very healthy weekly numbers on first-time filings for unemployment benefits.

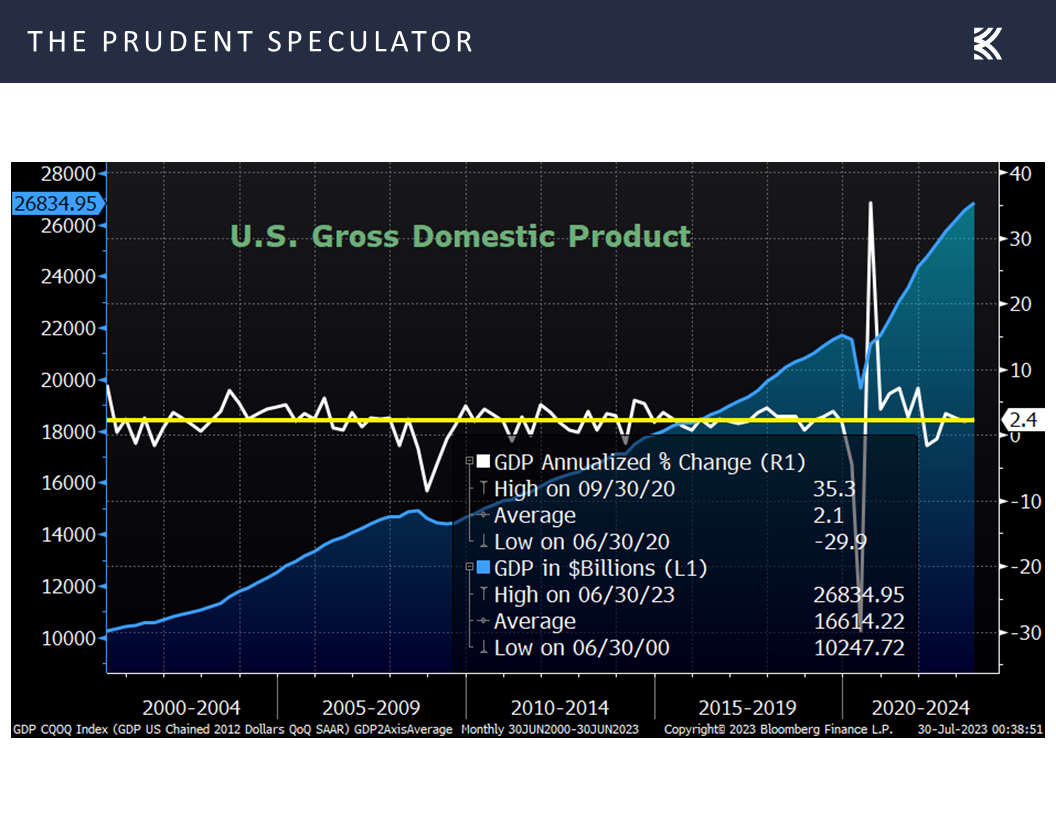

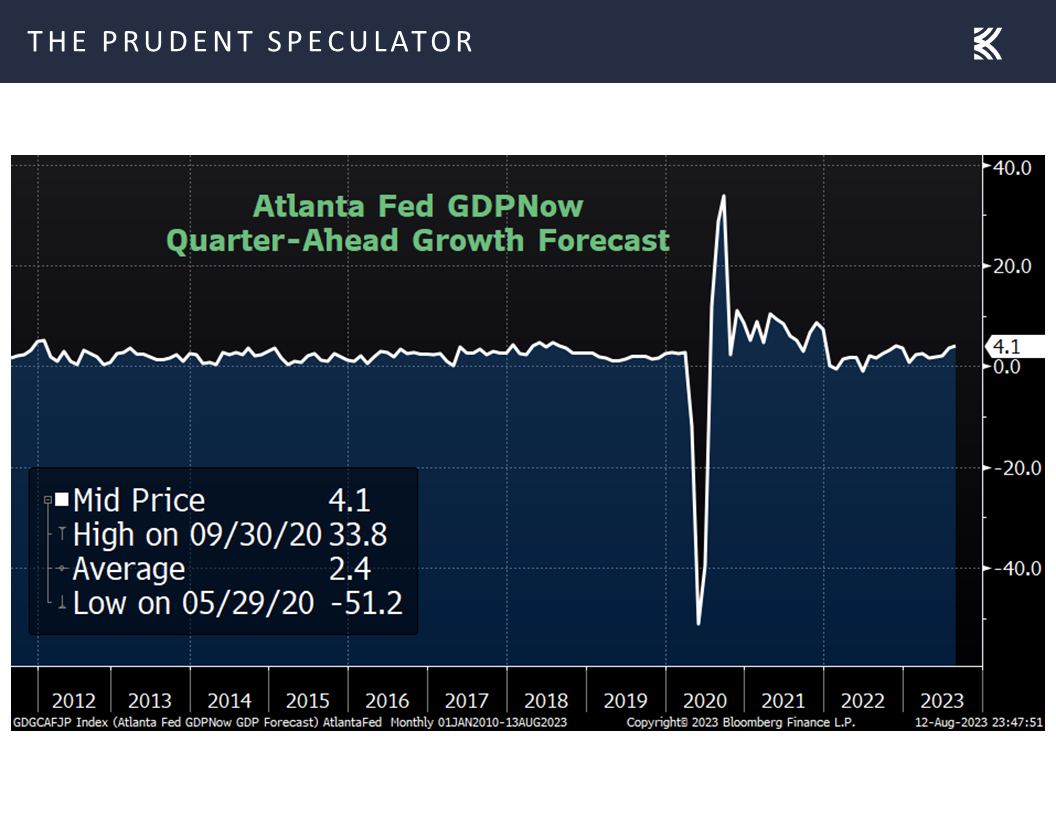

Incredibly, in the eyes of many, the current forecast for real Q3 GDP growth from the Atlanta Fed is a very robust 4.1%, so the chance of a recession starting this quarter would appear very remote,

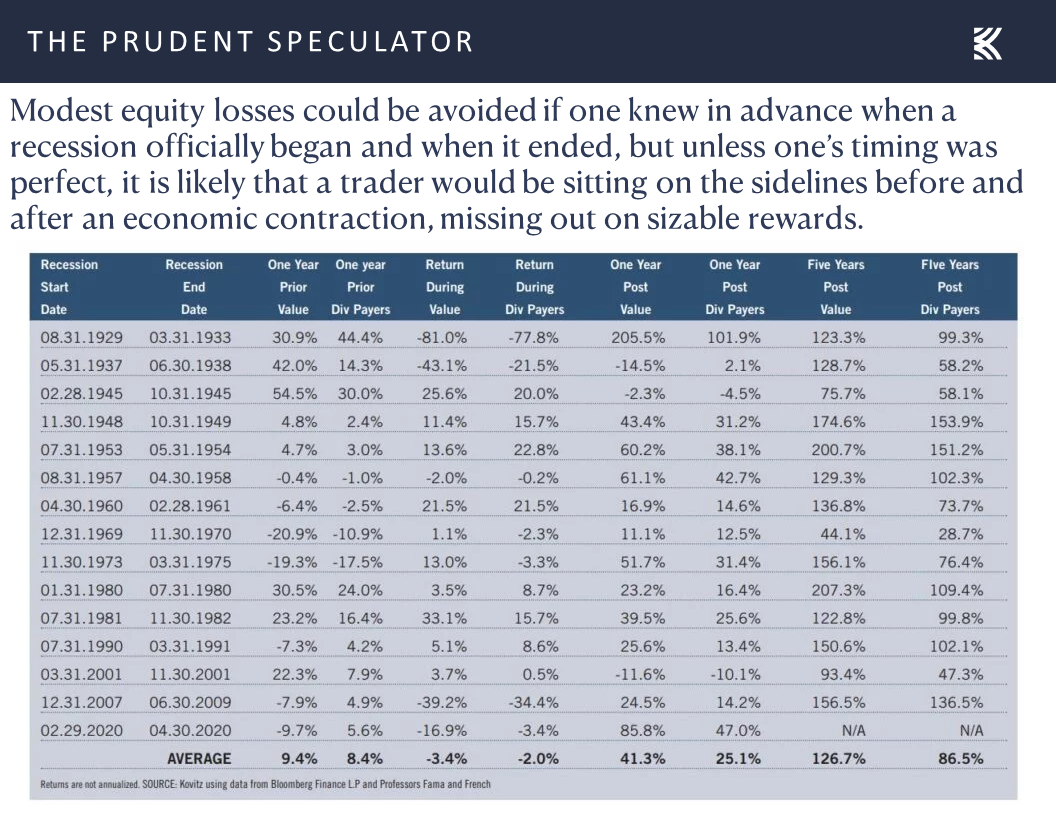

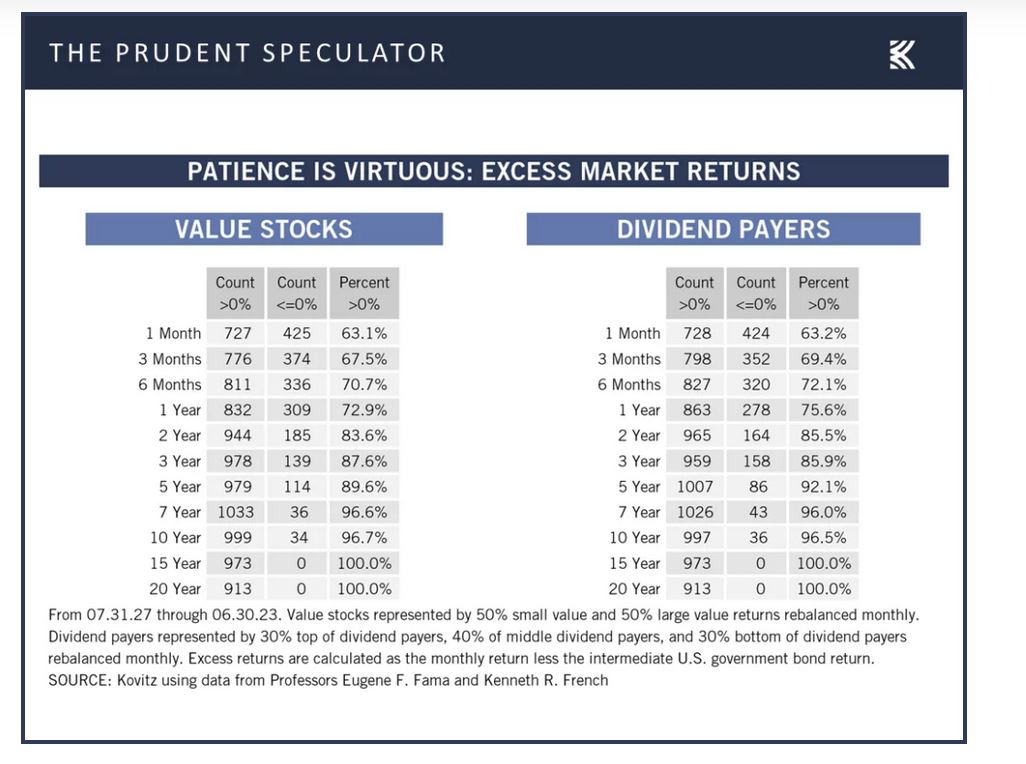

but we continue to lose little sleep worrying about a contraction, given what the historical evidence shows about the performance of Value Stocks and Dividend Payers, like those that we have long championed, before, during and especially after economic downturns.

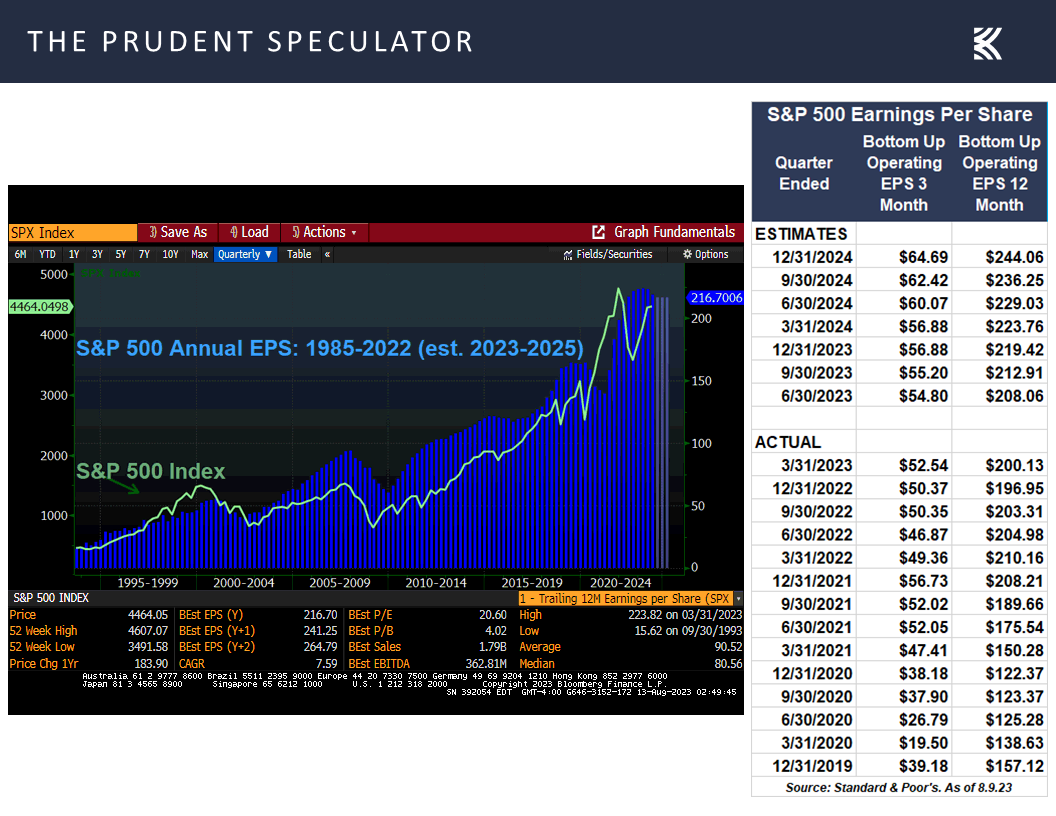

Corporate Profits – Excellent Q2 Reports; Forward Estimates Rise

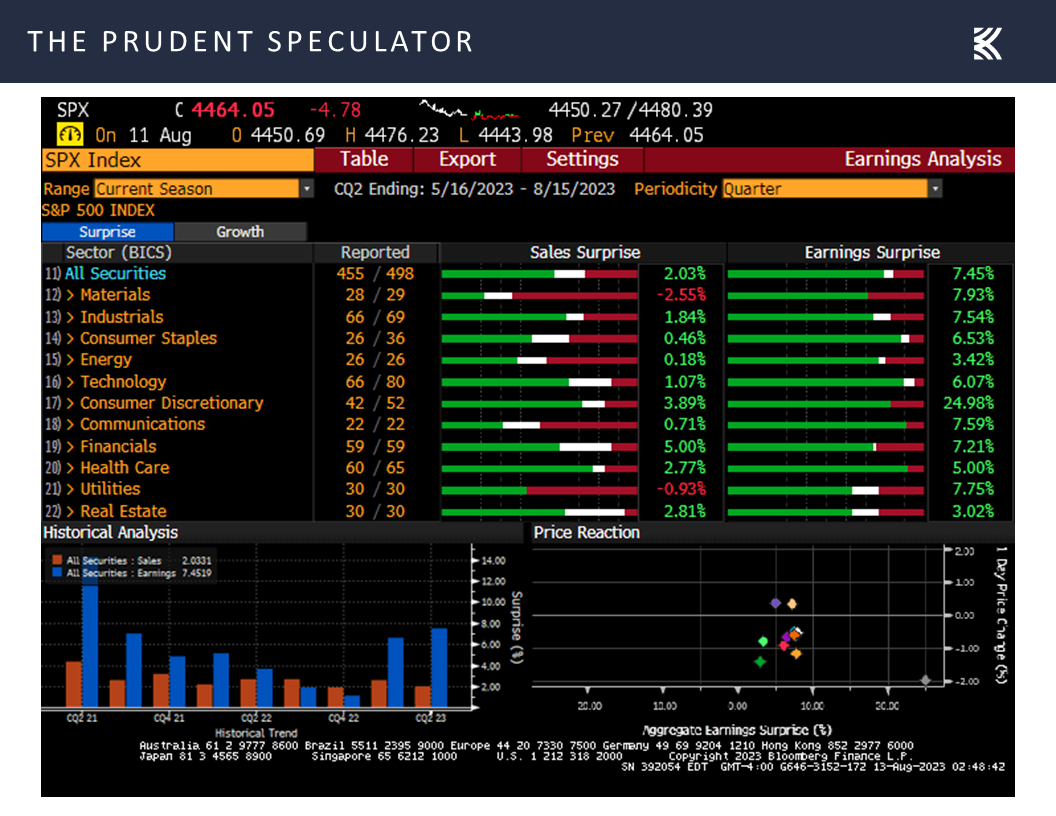

We also like what we have been seeing on the corporate profits front, as Q2 report cards have continued to impress. Indeed, with reporting season now in the late innings, 79.7% of the S&P 500 companies to have announced second quarter results have beat EPS expectations and 57.9% have exceeded top-line projections.

Analysts are often overly rosy in their projections, and they did just boost their estimates last week, but we think profit growth will remain solid overt the balance of 2023 and into 2024,

which, all things being equal, would boost the earnings yield and add to the appeal of equities, in general,

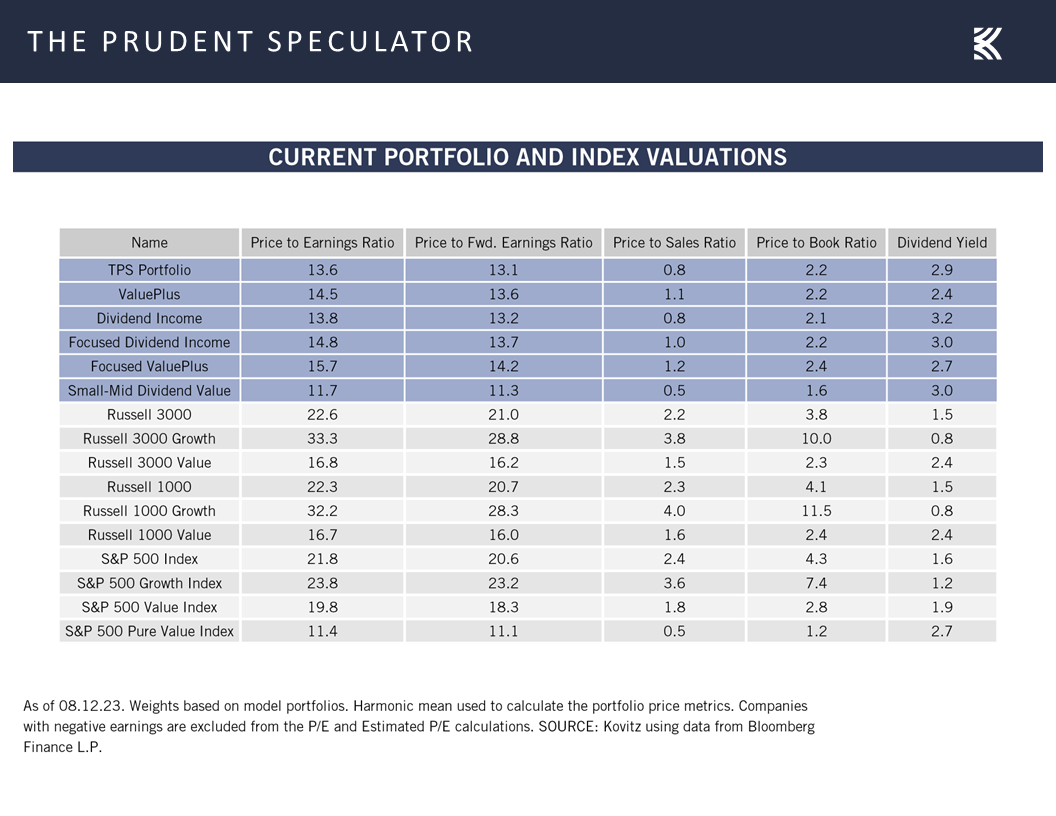

Valuations – Inexpensive Multiples for our Stocks

and our broadly diversified portfolios of what we believe to be undervalued stocks, in particular.

Our long-term optimism notwithstanding, we are always braced for a continuation of downside volatility in the near-term, and the equity futures on Sunday evening were pointing toward a lower opening when trading resumes this week, but we continue to believe that the longer we hold our stocks, the greater the chance of investment success!

Stock News – Updates on eleven stocks across eight different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Interest Rates, Inflation, Corporate Profits and Valuations

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss interest rates, inflation, corporate profits, valuations and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Week In Review – Stocks Pull Back Again

Patience – Lots to Worry About Along the Way, But Over Time Equities Have Proved Rewarding

Interest Rates – Treasury Yields Low By Historical Standards

Inflation – Mixed Data on CPI & PPI; Expectations Still Well Contained

Econ News – Generally Favorable Numbers; Q3 GDP Outlook Improves

Corporate Profits – Excellent Q2 Reports; Forward Estimates Rise

Valuations – Inexpensive Multiples for our Stocks

Stock News – Updates on eleven stocks across eight different sectors

Week In Review – Stocks Pull Back Again

Value again fared better than Growth, but it was a second straight down week, with the average stock in the Russell 3000 index losing 1.45% as smaller-capitalization companies suffered the biggest decline. Certainly, it is not unusual to see downside volatility, especially after the terrific gains enjoyed by the S&P 500 since March 17, 2023, and the broad-based advance in the equity markets during June and July.

Patience – Lots to Worry About Along the Way, But Over Time Equities Have Proved Rewarding

After all, despite stocks turning in excellent long-term returns over the years, trips south are part of the process. Indeed, 5% drops (this setback has more to go to get to that level) happen three times a year on average, 10% corrections take place every 11 months on average, and 20% Bear Markets occur every 2.7 years on average. Happily, rallies of even greater magnitude have occurred with equal frequency, and history shows that it is best to listen to advice from Warren Buffett if trying to time the inevitable ups and downs: “The fact that people will be full of greed, fear, or folly is predictable. The sequence is not predictable.”

We have long believed that time in the market trumps market timing, and it is fascinating to see how poorly mutual fund investors have done over the years with their efforts to get in ahead of an advance and get out ahead of a decline. The DALBAR figures on investor returns are eye-opening, especially for Fixed Income fund owners. Hard to believe that the average bond fund player has lost money over the last 1, 3, 5, 10, 20 and 30 years. And stocks are supposedly the risky asset class?

No doubt, equity investors must contend with plenty of disconcerting headlines, but those that keep the faith through thick and thin have been handsomely rewarded in the fullness of time. No two events are ever alike, as Heraclitus states, “No man ever steps in the same river twice, for it’s not the same river and he’s not the same man,” but we think that there is great value in studying market history.

For example, the latest bogeyman and arguably the catalyst for the August swoon has been the downgrade of the rating on U.S. credit by Fitch Ratings, an event that took place 12 years ago when Standard & Poor’s did the same thing. We might question where Fitch has been all this time, especially as the political drama over raising the debt ceiling in 2011 was far worse than it was this go round, but we note that the short-term damage caused back then was overcome relatively quickly, with stocks substantially higher today.

Interest Rates – Treasury Yields Low By Historical Standards

To be sure, there are other issues about which folks are concerned, as many are fretting about the rise in the yield on the 10-Year U.S. Treasury.

This is the case, even as today’s 4.15% benchmark government bond yield remains well below the 5.84% average since the inaugural edition of The Prudent Speculator was published in March 1977,

and market history shows that about the only conclusion that can be drawn from rising rates is that they are bad for the performance of…long-term bonds, though, as those big negative “Min” return figures in the chart below tell us, anything can happen.

Inflation – Mixed Data on CPI & PPI; Expectations Still Well Contained

Certainly, the attention of traders last week was on the inflation figures, with stocks starting off Thursday’s action on the plus side, following news that the core (excludes volatile food and energy prices) Consumer Price Index (CPI) ticked down to 4.7% in July, compared to 4.8% in June,

while the actual CPI came in at 3.2%, up from 3.0% in June, but below projections for a 3.3% advance.

Alas, the rally on Thursday morning was short-lived as Friday saw the report of inflation at the wholesale level come in worse than expected. The Final Demand Producer Price (PPI) Index for July advanced 0.8%, up from a 0.1% increase in June, and above the 0.7% estimate, while the core (excluding food & energy) rate rose 2.4% on a year-over-year basis, in line with the prior month’s reading.

Of course, inflation expectations over the next three and five years remain well-contained, per readings from the Univ. of Michigan and the New York Fed,

…while the Federal Funds futures market continues to forecast that Jerome H. Powell & Co. are near the end of their rate hiking cycle, with expectations that there will be several interest rate cuts in 2024.

Econ News – Generally Favorable Numbers; Q3 GDP Outlook Improves

The strength of the U.S. economy remains another worry, especially with Bloomberg calculations continuing to show a 60% chance of recession in the next 12 months.

The surprisingly robust real (inflation-adjusted) GDP growth in recent quarters (3.2% in Q3 2022, 2.6% in Q4 2022, 2.0% on Q1 2023 and 2.6% in Q2 2023) calls into question those Bloomberg projections as the odds of a contraction have been 50% or greater for a year now.

Is it any wonder that John Kenneth Galbraith proclaimed, “The only function of economic forecasting is to make astrology look respectable?” Needless to say, nobody knows for sure which way the economic data will trend, but the latest read on small-business optimism for July topped expectations,

while the preliminary measure of Consumer Sentiment for August from the Univ. of Michigan matched estimates,

and the labor market continued to show very healthy weekly numbers on first-time filings for unemployment benefits.

Incredibly, in the eyes of many, the current forecast for real Q3 GDP growth from the Atlanta Fed is a very robust 4.1%, so the chance of a recession starting this quarter would appear very remote,

but we continue to lose little sleep worrying about a contraction, given what the historical evidence shows about the performance of Value Stocks and Dividend Payers, like those that we have long championed, before, during and especially after economic downturns.

Corporate Profits – Excellent Q2 Reports; Forward Estimates Rise

We also like what we have been seeing on the corporate profits front, as Q2 report cards have continued to impress. Indeed, with reporting season now in the late innings, 79.7% of the S&P 500 companies to have announced second quarter results have beat EPS expectations and 57.9% have exceeded top-line projections.

Analysts are often overly rosy in their projections, and they did just boost their estimates last week, but we think profit growth will remain solid overt the balance of 2023 and into 2024,

which, all things being equal, would boost the earnings yield and add to the appeal of equities, in general,

Valuations – Inexpensive Multiples for our Stocks

and our broadly diversified portfolios of what we believe to be undervalued stocks, in particular.

Our long-term optimism notwithstanding, we are always braced for a continuation of downside volatility in the near-term, and the equity futures on Sunday evening were pointing toward a lower opening when trading resumes this week, but we continue to believe that the longer we hold our stocks, the greater the chance of investment success!

Stock News – Updates on eleven stocks across eight different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.