The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss AAII sentiment, a wall of worry, interest rates, valuations and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – 7 Buys for 3 Accounts

Contrarian Sentiment – AAII Becomes Bullish; Average Stock Skidded in Price Last Week

Wall of Worry – Stocks Have Overcome Plenty of Disconcerting Headlines

History – Economy and Earnings Have Risen Over Time

Powell Speaks – Fed Chair Continues to Talk Tough on Inflation

Interest Rates – Yields Edge Higher

Valuations – Stocks, Especially Value, Reasonably Priced

Calendar – Seasonally Favorable Periods Upon Us

Stock News – Updates on eleven stocks across seven different sectors

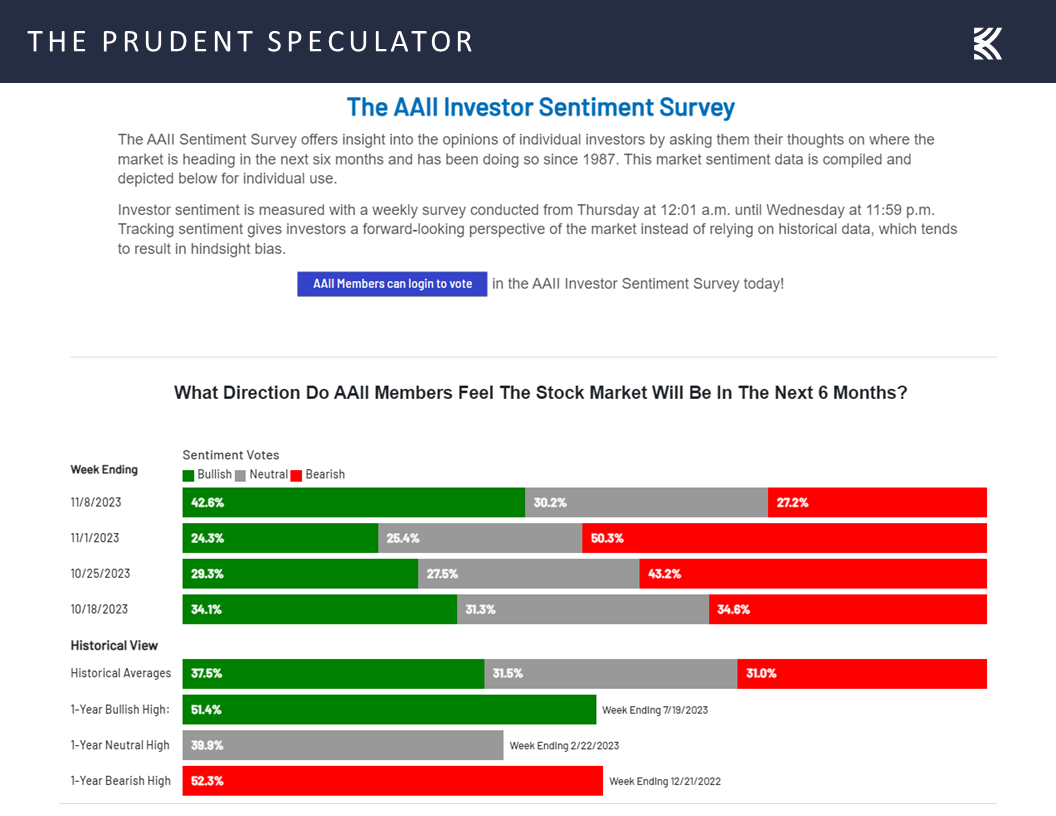

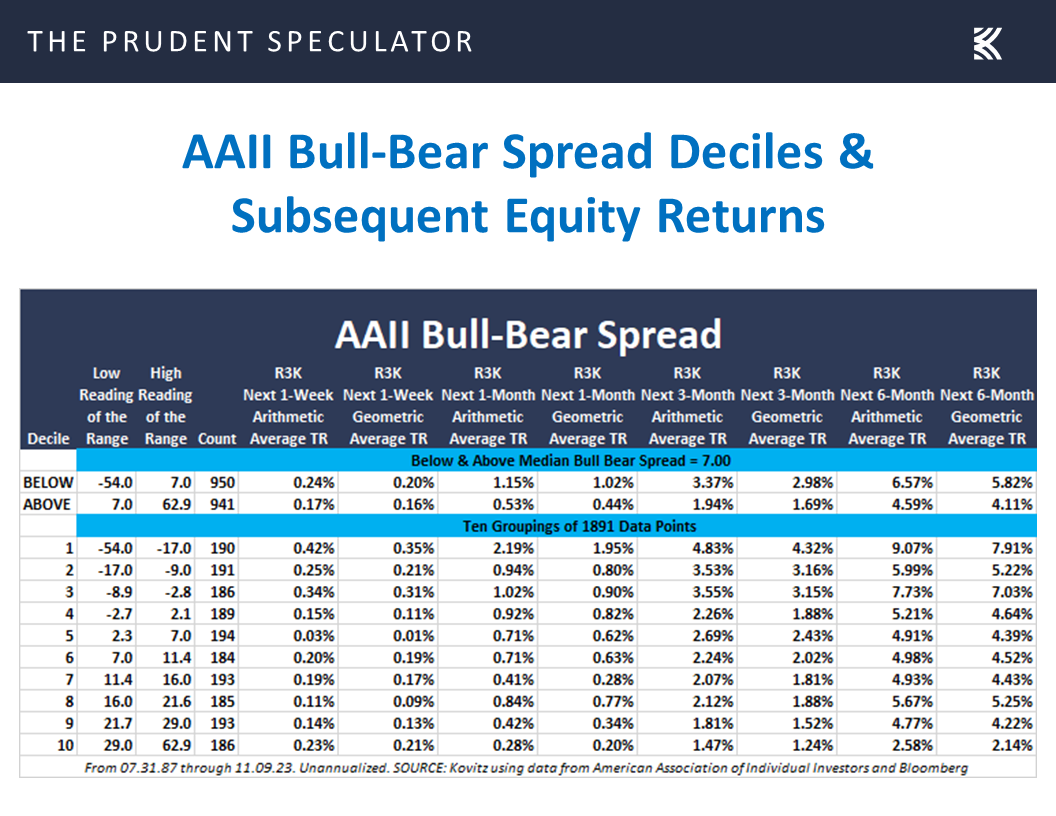

Contrarian Sentiment – AAII Becomes Bullish; Average Stock Skidded in Price Last Week

With the average stock in the Russell 3000 index needing a big rally on Friday to cut its weekly loss to 3.6%, while the Equal-Weight S&P 500 Index dropped 0.6% over the prior five days, we might blame the good folks at the American Association of Individual Investors (AAII) for the red ink. Incredibly, after arguably missing the massive gains the week prior when there was a preponderance of pessimism in the Sentiment Survey, the latest reading turned decidedly optimistic, with a huge jump in Bulls from 24.3% to 42.6% and a tremendous plunge in the Bears from 50.3% to 27.2%.

‘Twas ever thus, our founder Al Frank liked to say, as the AAII history books show that stocks perform better when there is greater investor negativity and less well when there is an abundance of positivity,

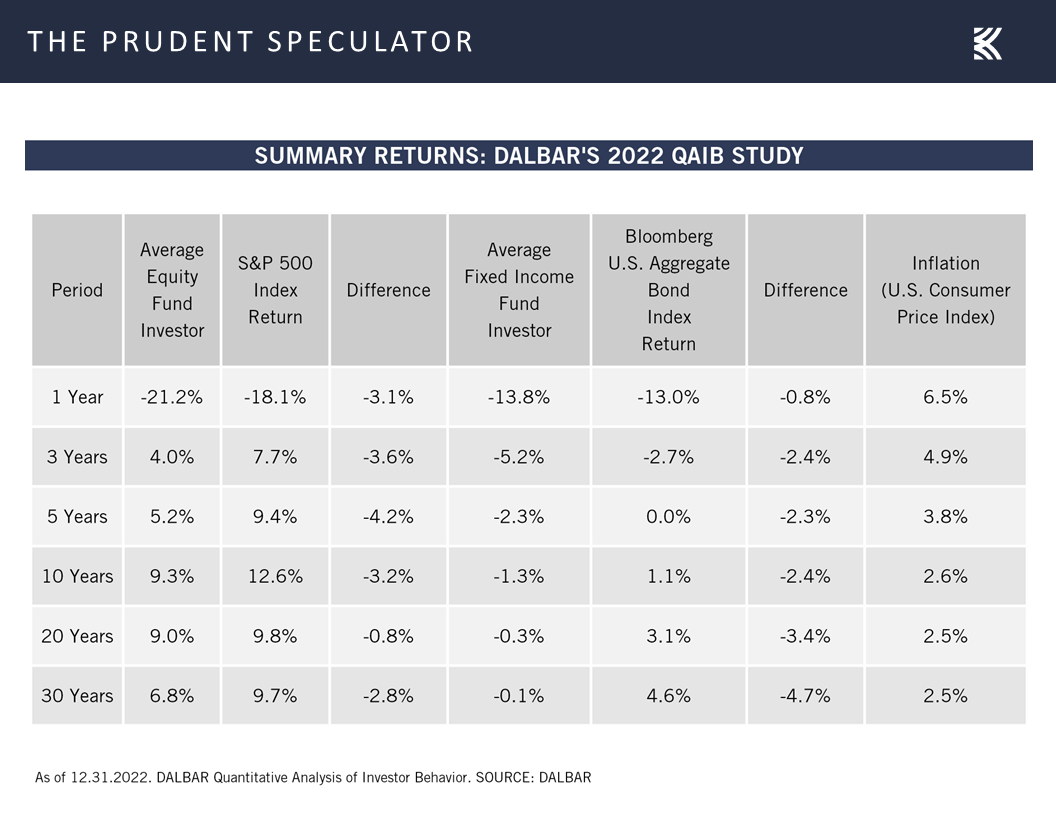

as far too many seem to have a propensity for selling low and buying high. Indeed, poor market timing decisions have proved hazardous to their wealth, per data from DALBAR on stock and bond fund returns versus actual investor returns in those funds.

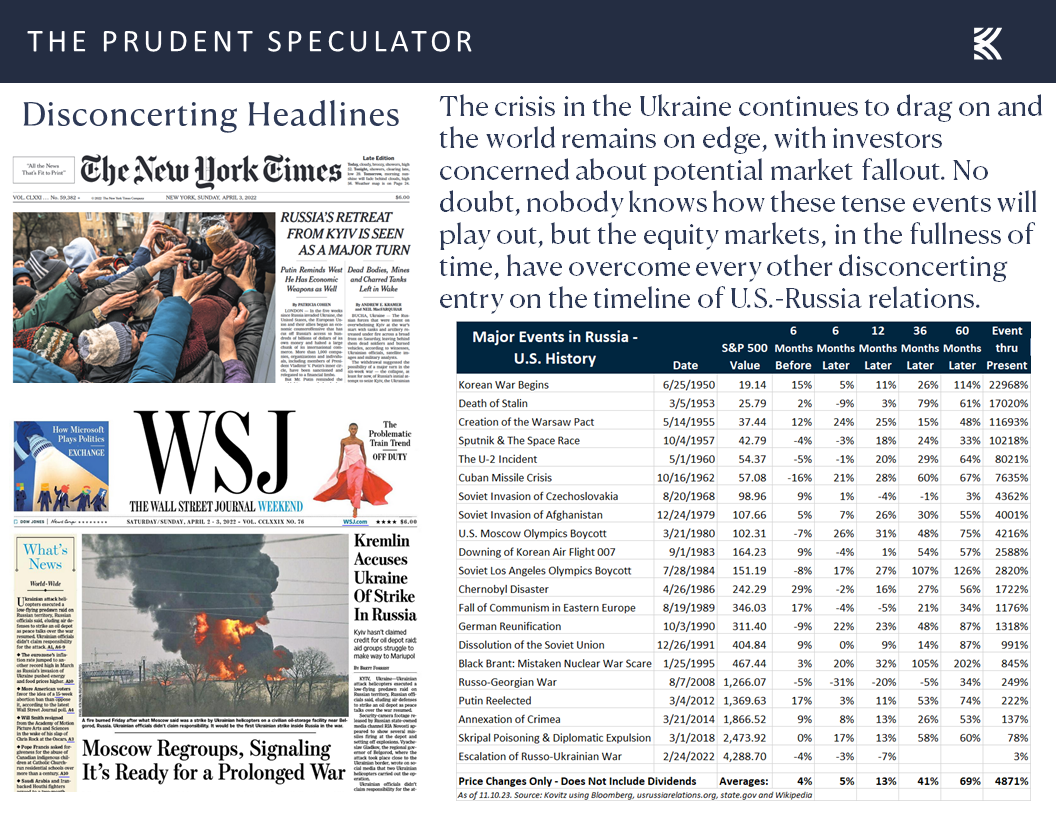

Wall of Worry – Stocks Have Overcome Plenty of Disconcerting Headlines

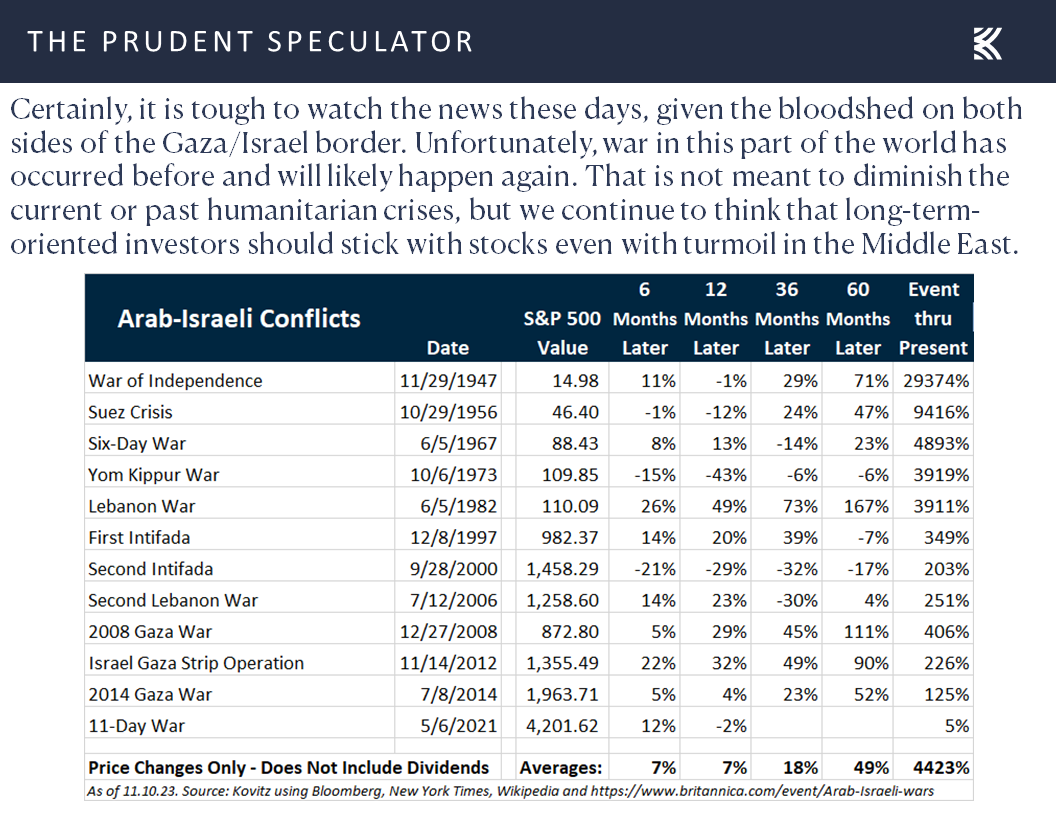

No doubt, it is harder for many to stick to their long-term investment plan these days, as news from the Middle East remains very troubling,

while the War in Ukraine continues to drag on,

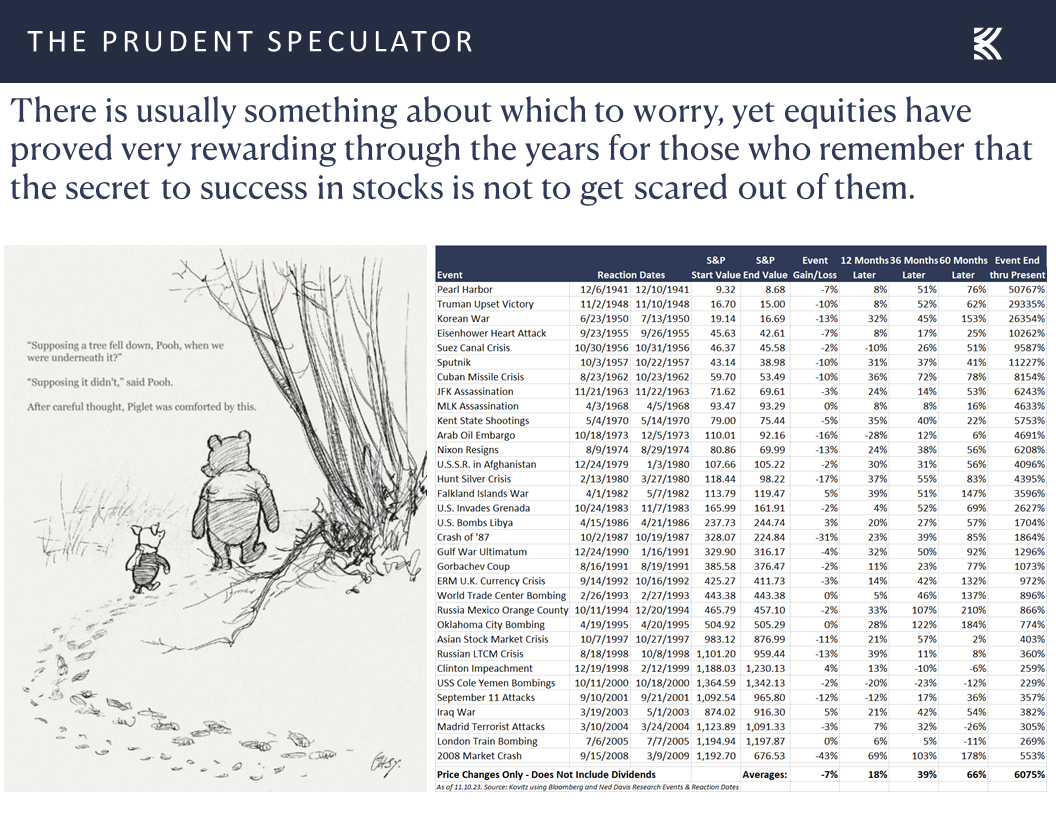

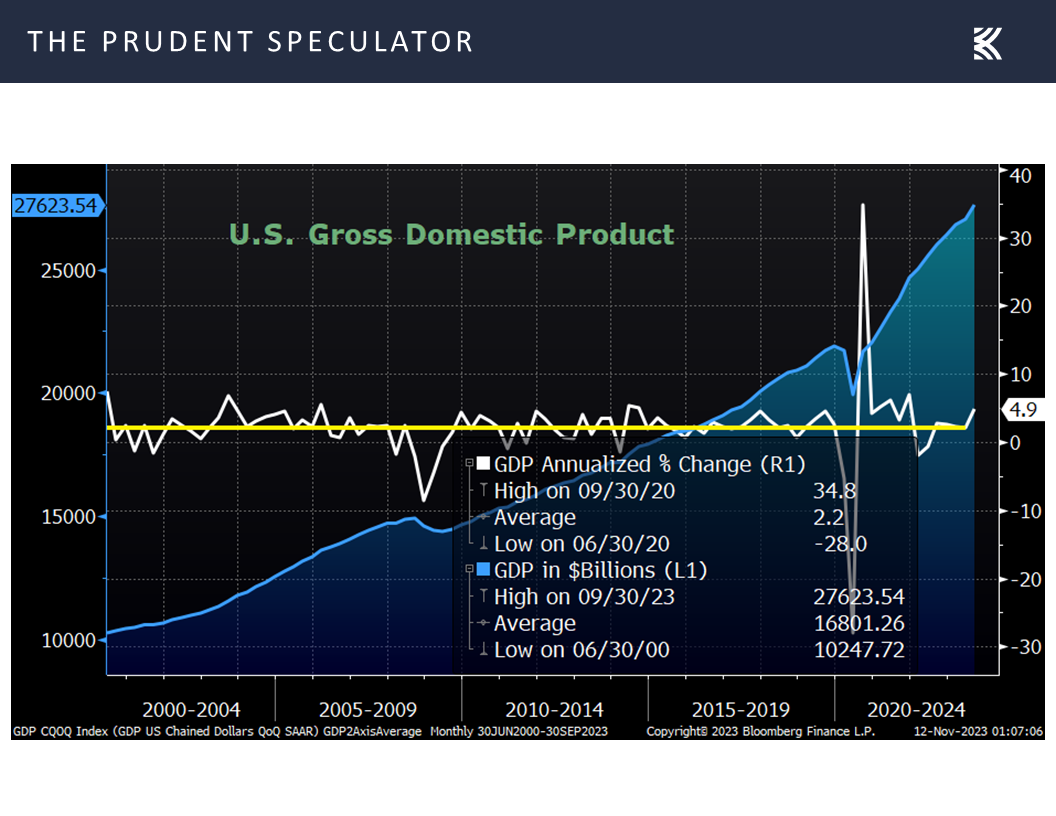

History – Economy and Earnings Have Risen Over Time

but, at the risk of sounding insensitive, there always seems to be something to worry about as there have been plenty of frightening events over the last eight decades,

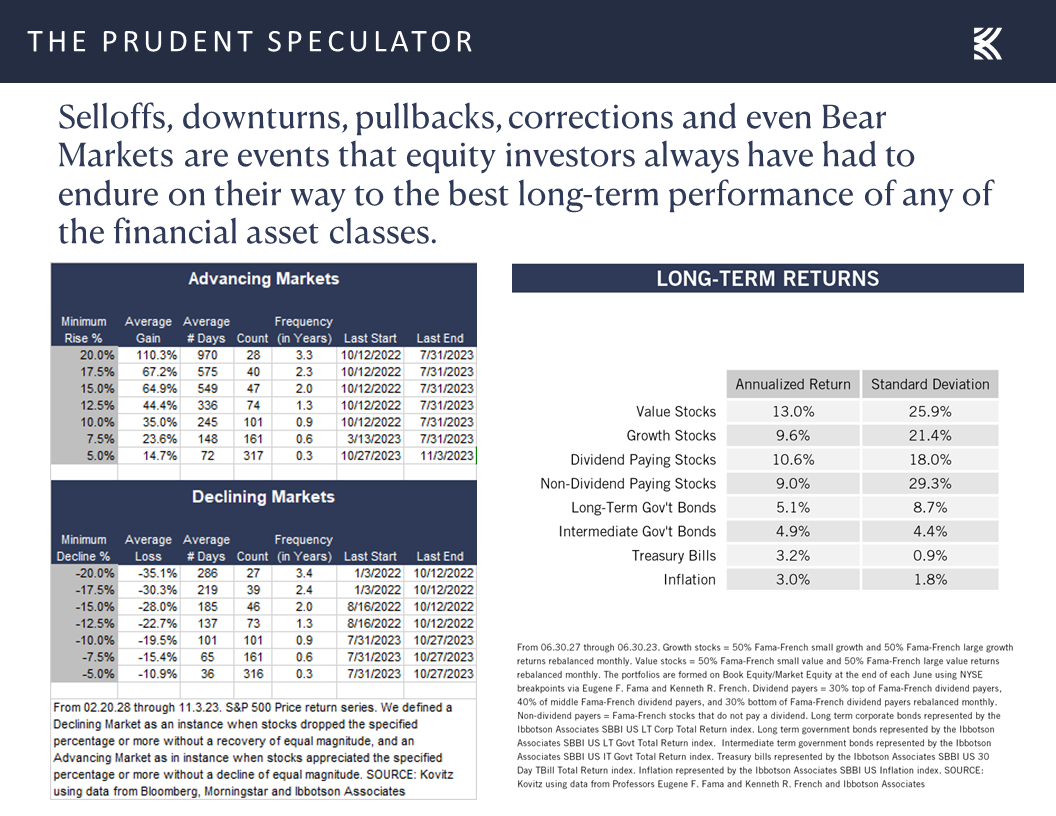

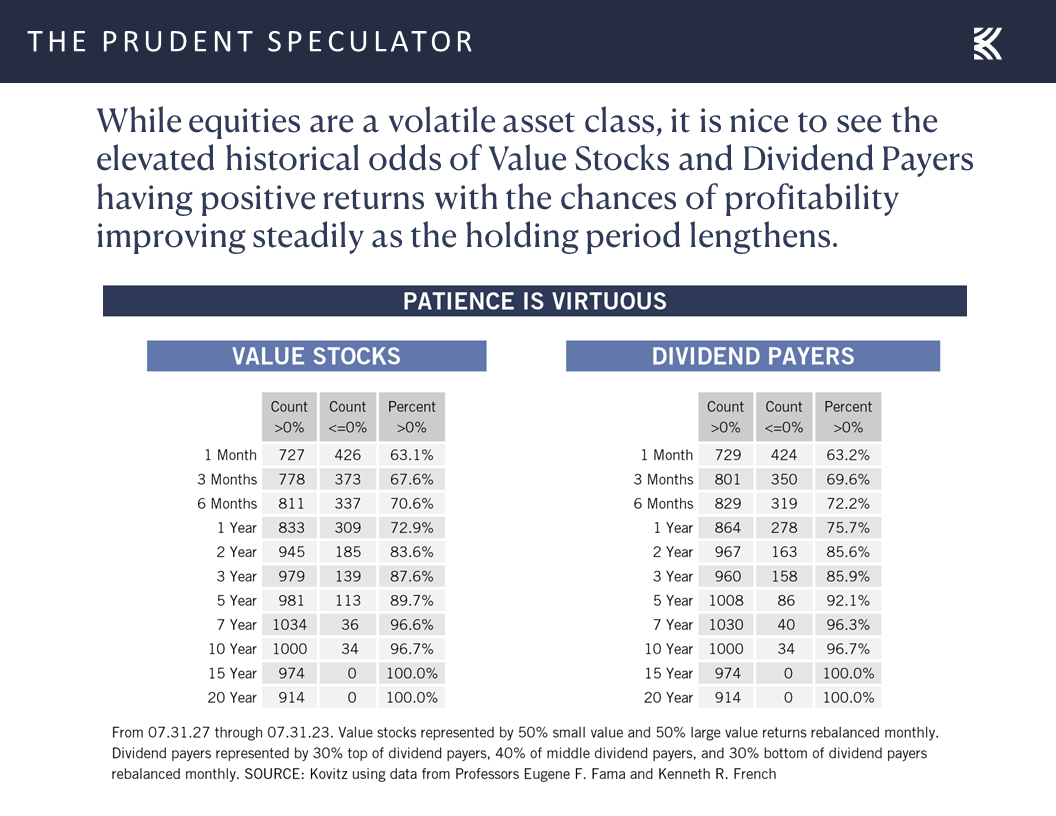

yet equities have provided terrific long-term rewards for those who have remembered that despite significant volatility along the way, the secret to success in stocks is to not get scared out of them.

Happily, the longer one holds equities, the better the chance of making money as, unlike at the tables in Las Vegas, the odds are stacked decidedly in favor of patient long-term-oriented investors.

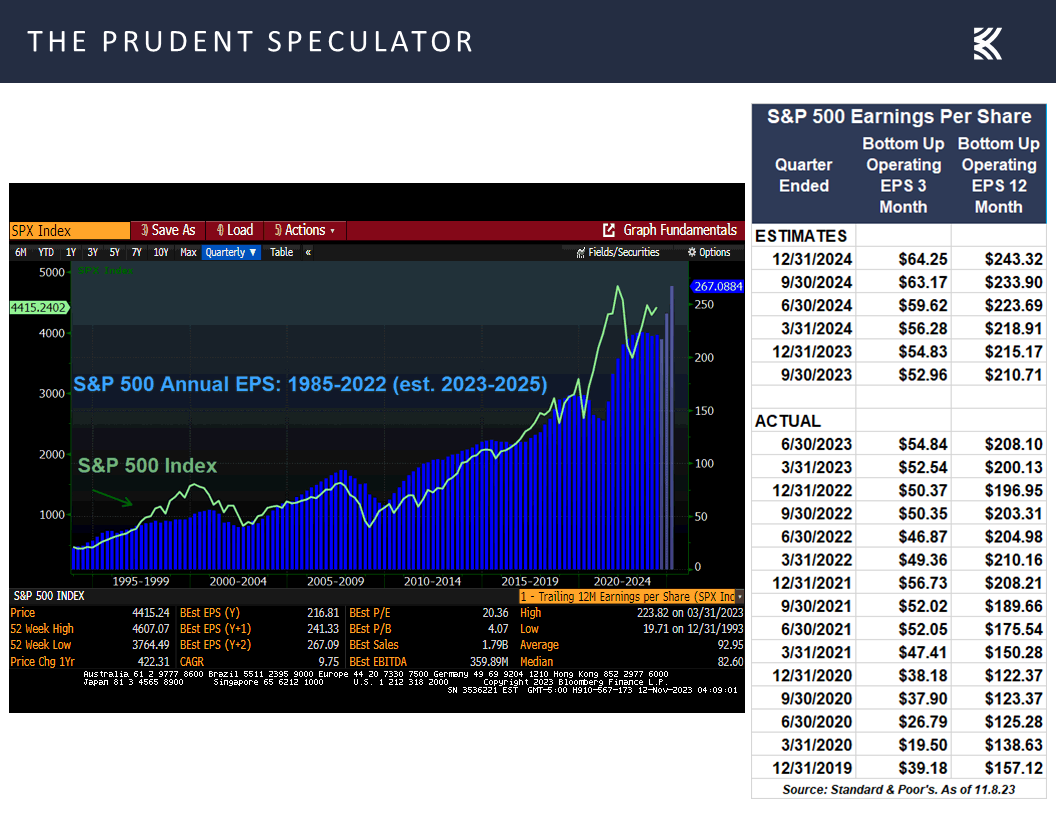

Of course, stocks have appreciated in value over time because the U.S. economy has grown on both a real (inflation-adjusted) and a nominal (actual) basis,

while corporate profits (which are reported in nominal dollars) have followed suit…and are expected to still show handsome year-over-year improvement this year and in 2024.

Powell Speaks – Fed Chair Continues to Talk Tough on Inflation

We understand that we will always have to put up with potholes on the road to long-term success as stock prices will always be volatile. For example, the markets saw a big plunge this past Thursday after Federal Reserve Chair Jerome H. Powell had the following to say (we have added illustrative charts) at an International Monetary Fund conference:

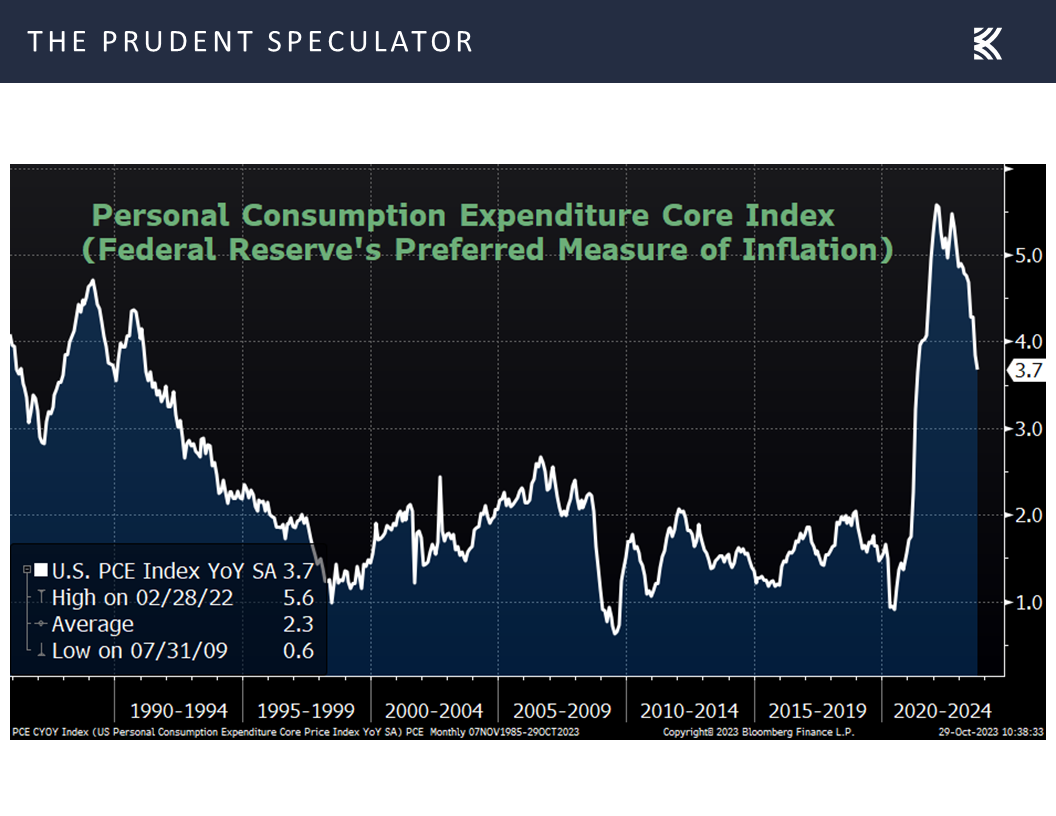

U.S. inflation has come down over the past year but remains well above our 2 percent target. My colleagues and I are gratified by this progress but expect that the process of getting inflation sustainably down to 2 percent has a long way to go.

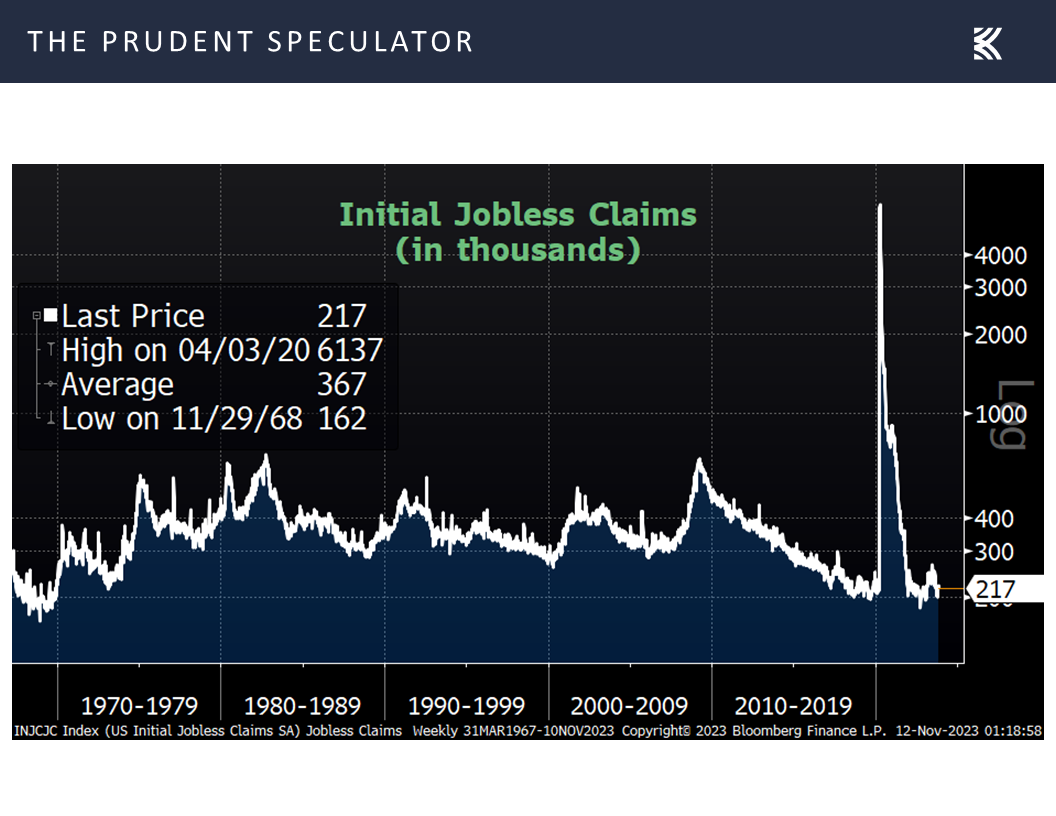

The labor market remains tight, although improvements in labor supply and a gradual easing in demand continue to move it into better balance.

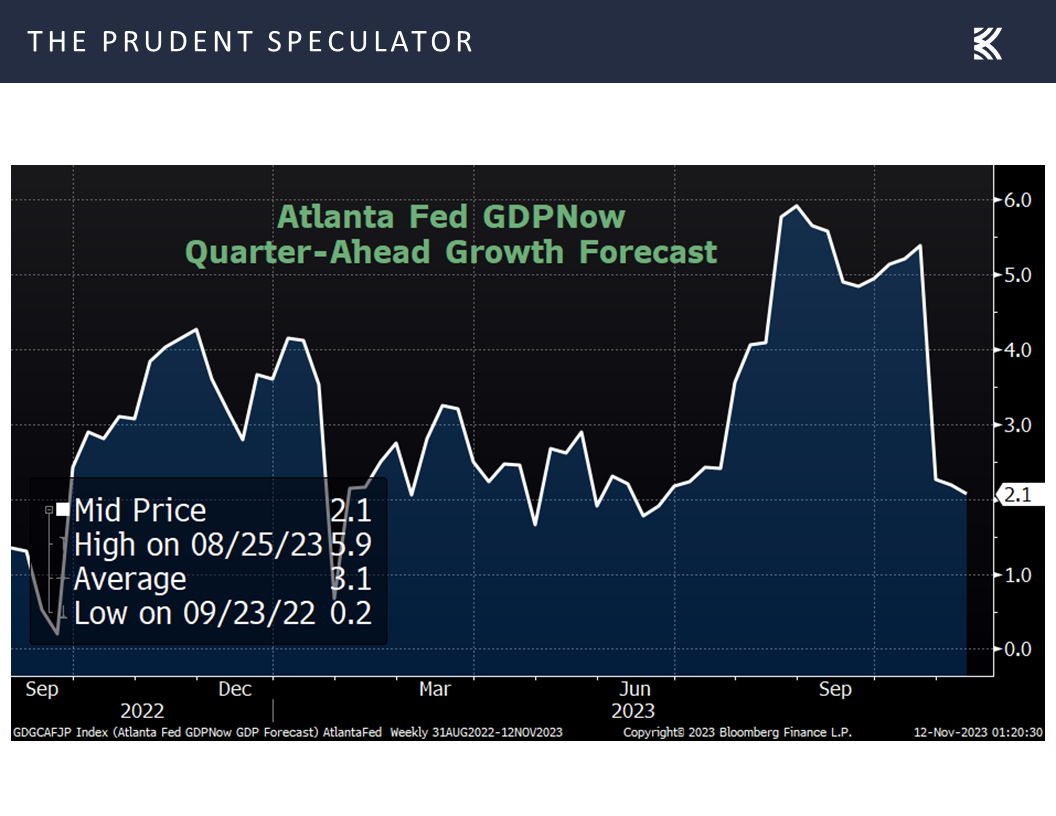

Gross domestic product growth in the third quarter was quite strong, but, like most forecasters, we expect growth to moderate in coming quarters.

Of course, that remains to be seen, and we are attentive to the risk that stronger growth could undermine further progress in restoring balance to the labor market and in bringing inflation down, which could warrant a response from monetary policy. The Federal Open Market Committee (FOMC) is committed to achieving a stance of monetary policy that is sufficiently restrictive to bring inflation down to 2 percent over time; we are not confident that we have achieved such a stance. We know that ongoing progress toward our 2 percent goal is not assured: Inflation has given us a few head fakes. If it becomes appropriate to tighten policy further, we will not hesitate to do so.

We will continue to move carefully, however, allowing us to address both the risk of being misled by a few good months of data, and the risk of overtightening. We are making decisions meeting by meeting, based on the totality of the incoming data and their implications for the outlook for economic activity and inflation, as well as the balance of risks, determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time. We will keep at it until the job is done.

Interest Rates – Yields Edge Higher

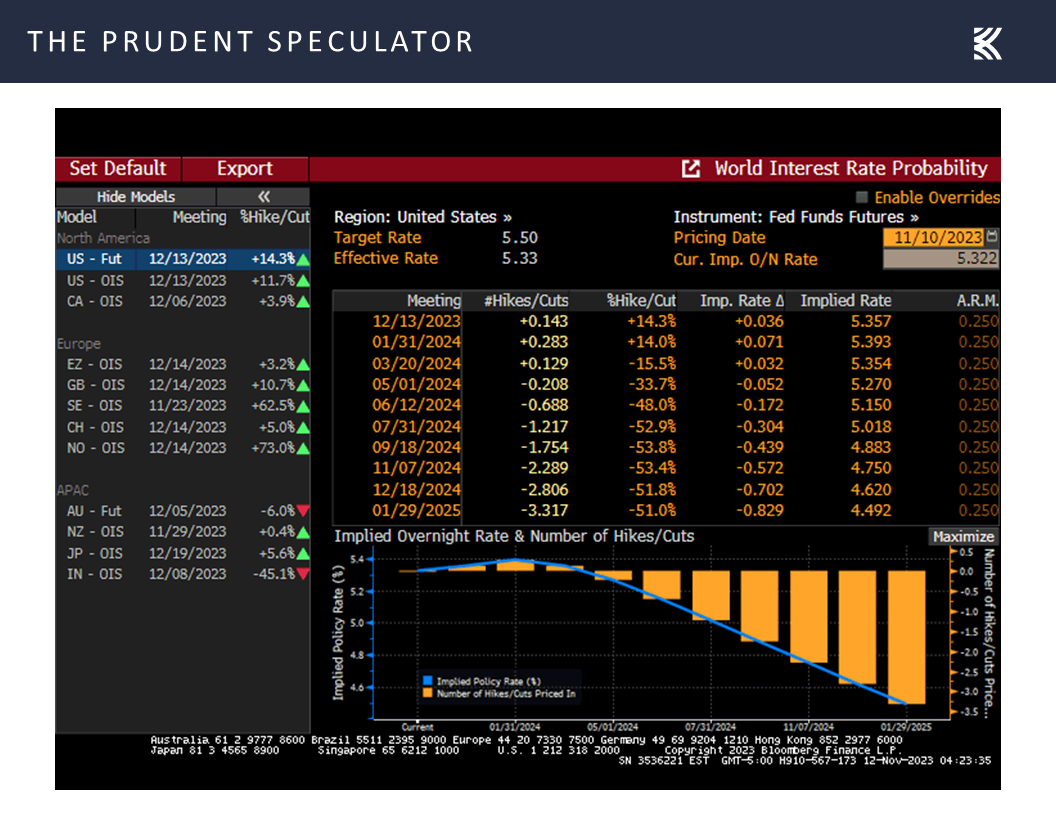

As the chart above showing the current wagering in the futures market indicates, those betting on the Fed Funds rate still expect the Fed to ease in 2024 with several cuts likely from the current target rate of 5.25% to 5.5%. However, next year’s year-end effective rate forecast rose to 4.62% last week from 4.35% the week prior,

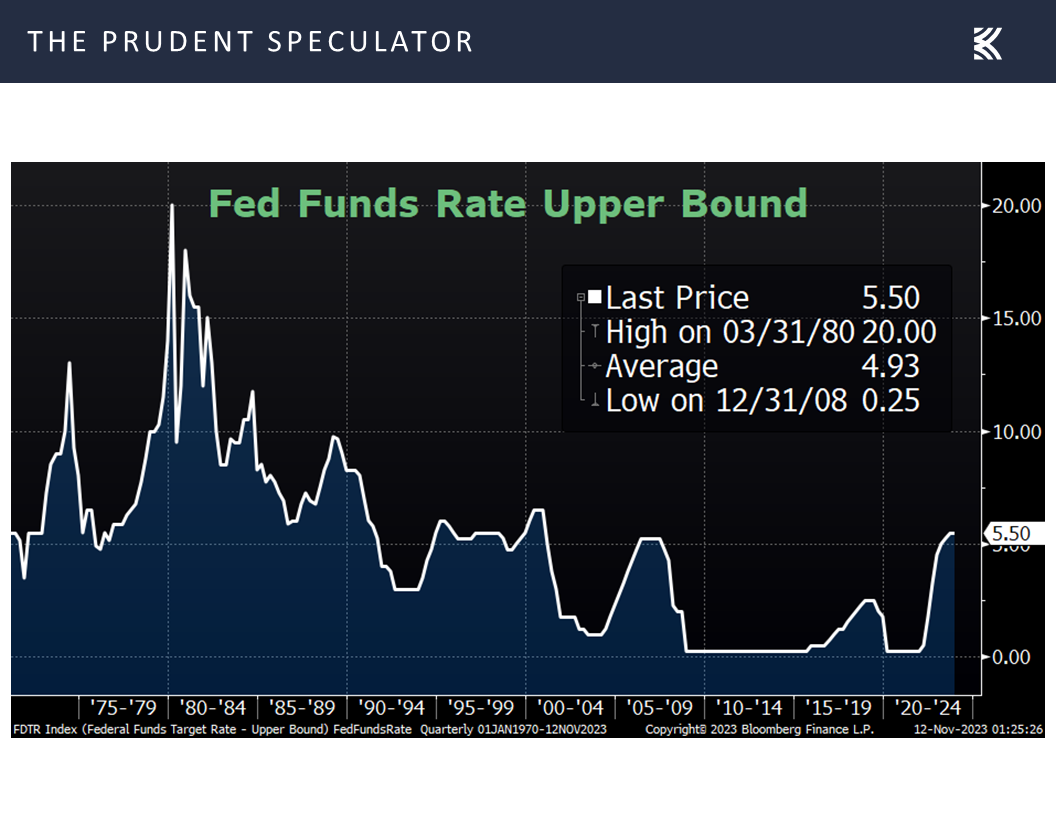

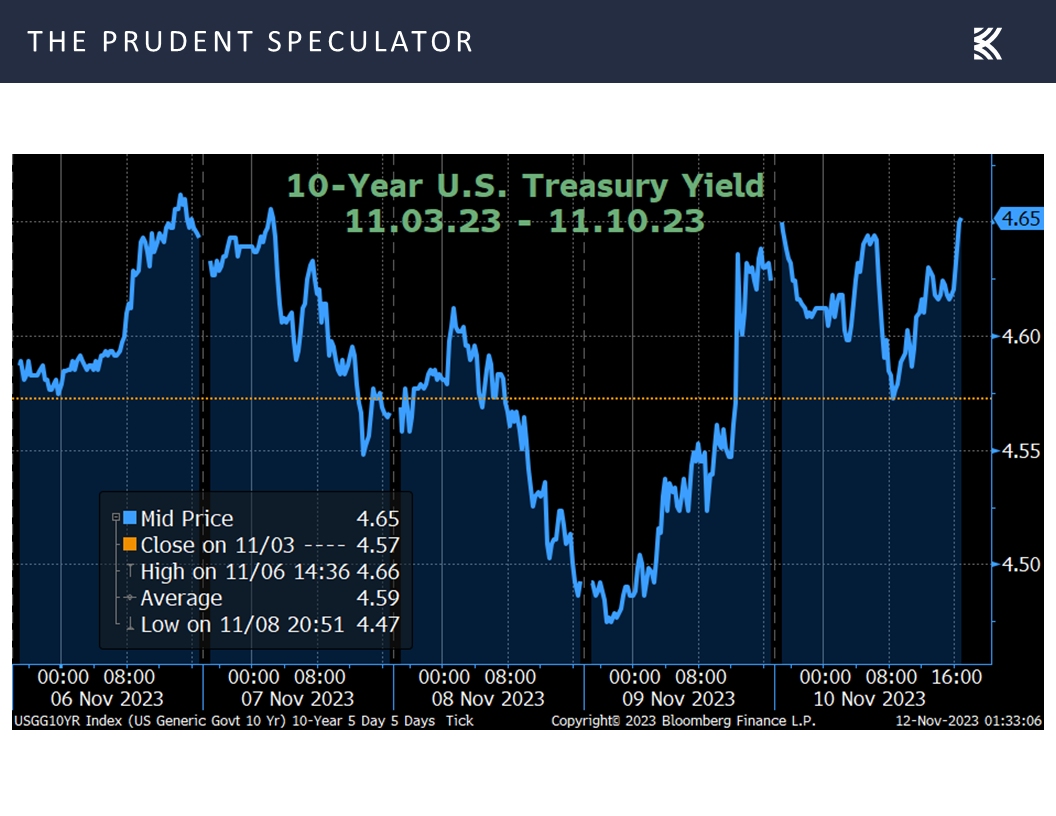

and there was a modest increase in the benchmark U.S. government bond yield,

but nothing that Chair Powell said on Thursday struck us as anything different than what he has been saying for a while now – the Fed will continue to do all it can to keep inflation in check while treading carefully, given that monetary policy works with a lag, and remaining dependent on incoming data.

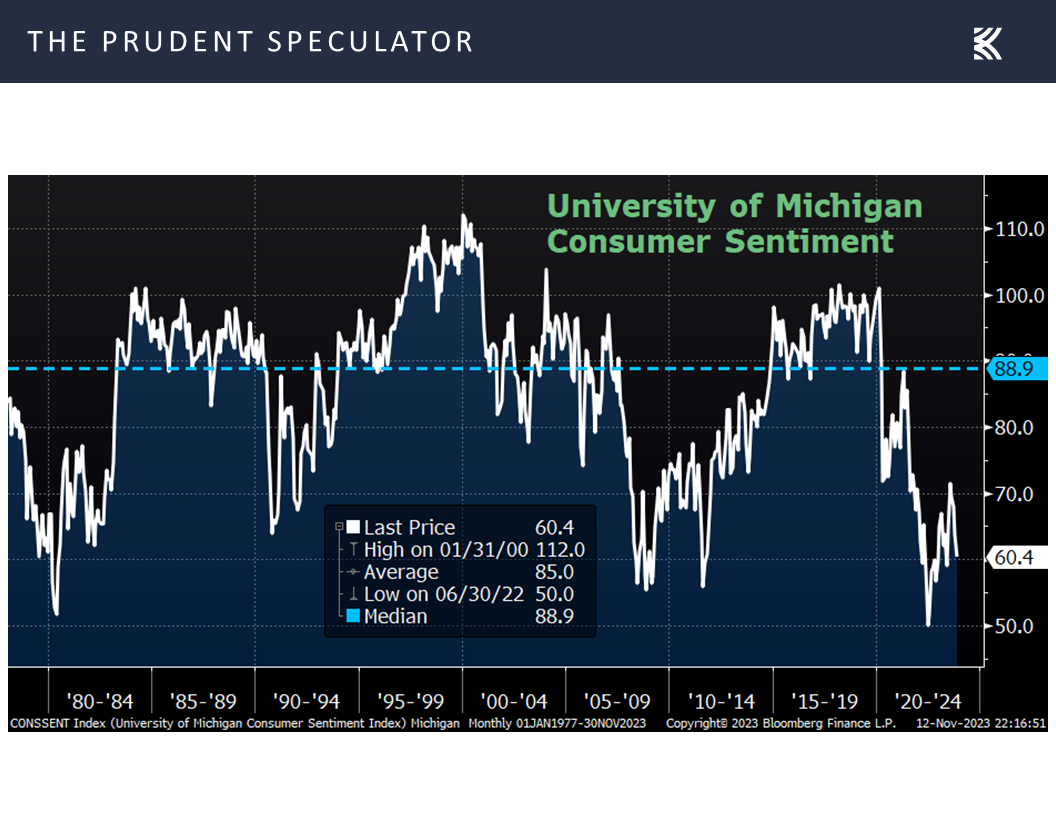

And speaking of data, we suppose Friday’s big bounce higher in stocks had a great deal to do with the report that morning of worse-than-expected numbers on consumer confidence from the Univ. of Michigan, continuing the recent trend where weaker economic news is good for stocks, as it lessens the risk of addition Fed policy firming, and vice versa.

Valuations – Stocks, Especially Value, Reasonably Priced

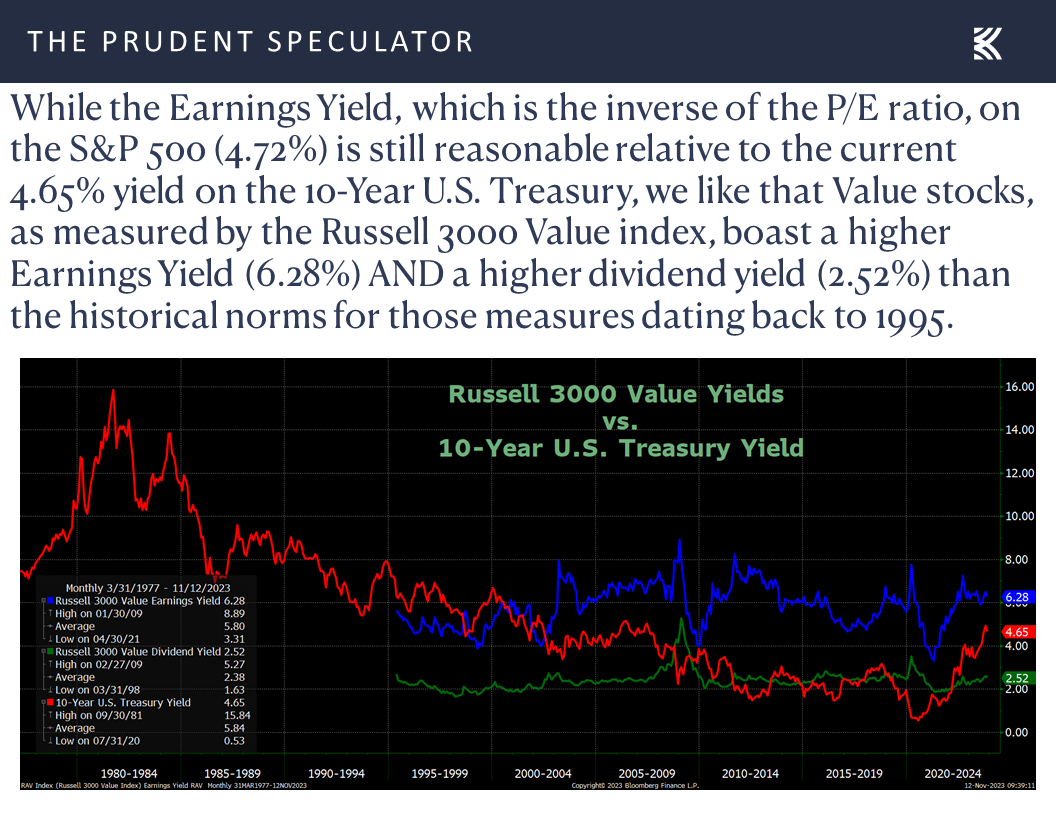

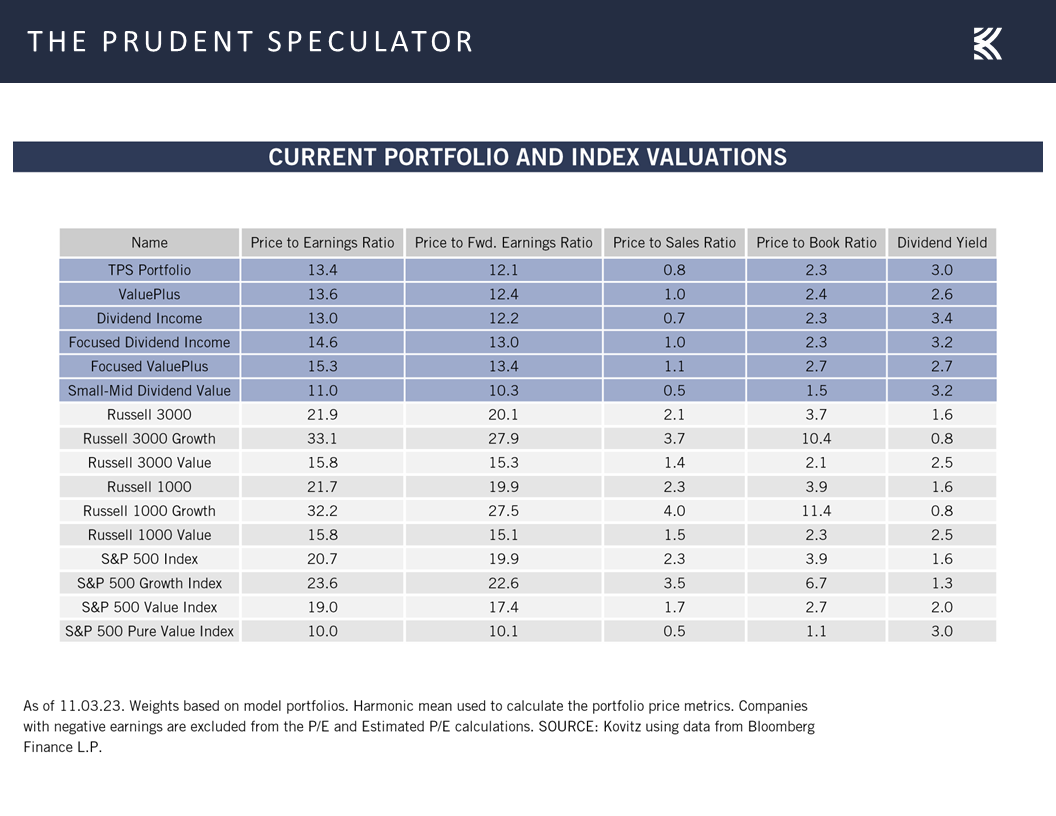

So, though we suspect that volatility will remain elevated, and stocks are poised to open lower when trading resumes this week on Friday afternoon’s downgrade of the U.S. credit outlook by Moody’s, we see no reason to alter our enthusiasm for the long-term prospects of the inexpensively priced companies that we have long championed. This is especially true as through Friday, the average Russell 3000 member has lost 2.4% and the Equal-Weight S&P 500 has gained just 1.2% in 2023, while relative valuations for Value in general,

and our broadly diversified portfolios of what we believe to be undervalued stocks in particular continue to be very attractive.

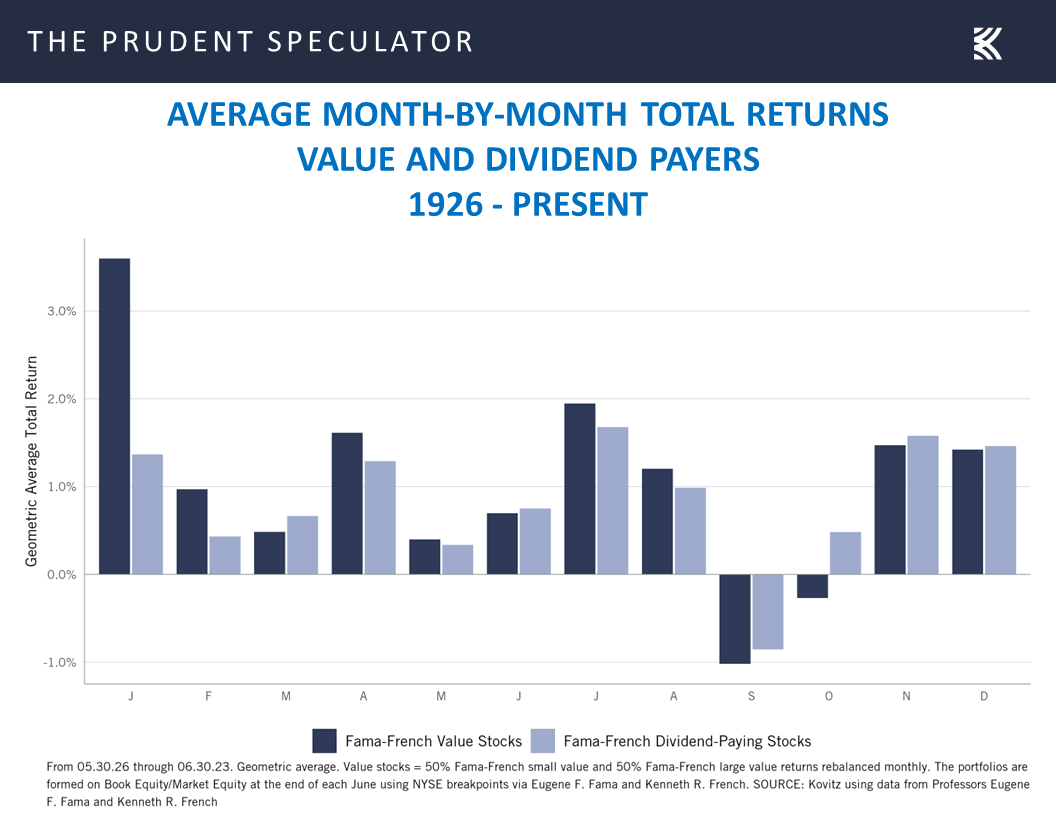

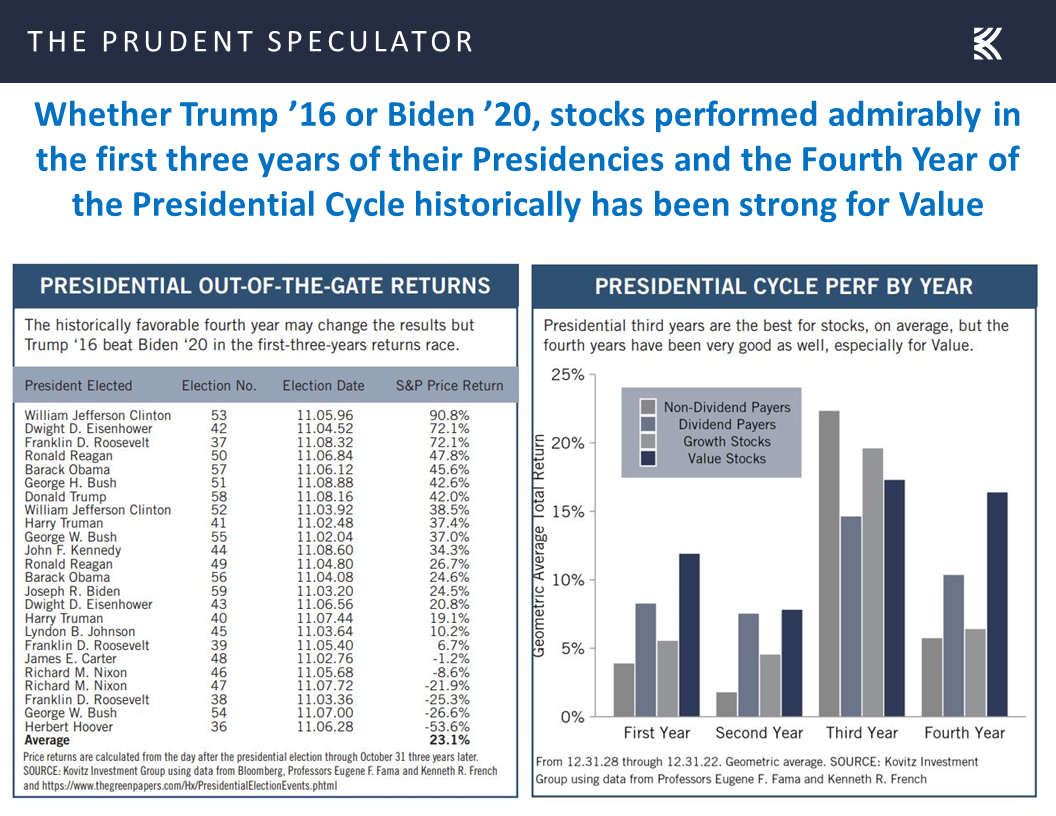

Calendar – Seasonally Favorable Periods Upon Us

And, we can’t forget the calendar as we are now in the seasonally favorable six months of the year,

while the upcoming fourth year of the Presidential Cycle historically has been very favorable, on average!

Stock News – Updates on eleven stocks across seven different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Interest Rates, Valuations, A Wall of Worry and the AAII Sentiment

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss AAII sentiment, a wall of worry, interest rates, valuations and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – 7 Buys for 3 Accounts

Contrarian Sentiment – AAII Becomes Bullish; Average Stock Skidded in Price Last Week

Wall of Worry – Stocks Have Overcome Plenty of Disconcerting Headlines

History – Economy and Earnings Have Risen Over Time

Powell Speaks – Fed Chair Continues to Talk Tough on Inflation

Interest Rates – Yields Edge Higher

Valuations – Stocks, Especially Value, Reasonably Priced

Calendar – Seasonally Favorable Periods Upon Us

Stock News – Updates on eleven stocks across seven different sectors

Contrarian Sentiment – AAII Becomes Bullish; Average Stock Skidded in Price Last Week

With the average stock in the Russell 3000 index needing a big rally on Friday to cut its weekly loss to 3.6%, while the Equal-Weight S&P 500 Index dropped 0.6% over the prior five days, we might blame the good folks at the American Association of Individual Investors (AAII) for the red ink. Incredibly, after arguably missing the massive gains the week prior when there was a preponderance of pessimism in the Sentiment Survey, the latest reading turned decidedly optimistic, with a huge jump in Bulls from 24.3% to 42.6% and a tremendous plunge in the Bears from 50.3% to 27.2%.

‘Twas ever thus, our founder Al Frank liked to say, as the AAII history books show that stocks perform better when there is greater investor negativity and less well when there is an abundance of positivity,

as far too many seem to have a propensity for selling low and buying high. Indeed, poor market timing decisions have proved hazardous to their wealth, per data from DALBAR on stock and bond fund returns versus actual investor returns in those funds.

Wall of Worry – Stocks Have Overcome Plenty of Disconcerting Headlines

No doubt, it is harder for many to stick to their long-term investment plan these days, as news from the Middle East remains very troubling,

while the War in Ukraine continues to drag on,

History – Economy and Earnings Have Risen Over Time

but, at the risk of sounding insensitive, there always seems to be something to worry about as there have been plenty of frightening events over the last eight decades,

yet equities have provided terrific long-term rewards for those who have remembered that despite significant volatility along the way, the secret to success in stocks is to not get scared out of them.

Happily, the longer one holds equities, the better the chance of making money as, unlike at the tables in Las Vegas, the odds are stacked decidedly in favor of patient long-term-oriented investors.

Of course, stocks have appreciated in value over time because the U.S. economy has grown on both a real (inflation-adjusted) and a nominal (actual) basis,

while corporate profits (which are reported in nominal dollars) have followed suit…and are expected to still show handsome year-over-year improvement this year and in 2024.

Powell Speaks – Fed Chair Continues to Talk Tough on Inflation

We understand that we will always have to put up with potholes on the road to long-term success as stock prices will always be volatile. For example, the markets saw a big plunge this past Thursday after Federal Reserve Chair Jerome H. Powell had the following to say (we have added illustrative charts) at an International Monetary Fund conference:

U.S. inflation has come down over the past year but remains well above our 2 percent target. My colleagues and I are gratified by this progress but expect that the process of getting inflation sustainably down to 2 percent has a long way to go.

The labor market remains tight, although improvements in labor supply and a gradual easing in demand continue to move it into better balance.

Gross domestic product growth in the third quarter was quite strong, but, like most forecasters, we expect growth to moderate in coming quarters.

Of course, that remains to be seen, and we are attentive to the risk that stronger growth could undermine further progress in restoring balance to the labor market and in bringing inflation down, which could warrant a response from monetary policy. The Federal Open Market Committee (FOMC) is committed to achieving a stance of monetary policy that is sufficiently restrictive to bring inflation down to 2 percent over time; we are not confident that we have achieved such a stance. We know that ongoing progress toward our 2 percent goal is not assured: Inflation has given us a few head fakes. If it becomes appropriate to tighten policy further, we will not hesitate to do so.

We will continue to move carefully, however, allowing us to address both the risk of being misled by a few good months of data, and the risk of overtightening. We are making decisions meeting by meeting, based on the totality of the incoming data and their implications for the outlook for economic activity and inflation, as well as the balance of risks, determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time. We will keep at it until the job is done.

Interest Rates – Yields Edge Higher

As the chart above showing the current wagering in the futures market indicates, those betting on the Fed Funds rate still expect the Fed to ease in 2024 with several cuts likely from the current target rate of 5.25% to 5.5%. However, next year’s year-end effective rate forecast rose to 4.62% last week from 4.35% the week prior,

and there was a modest increase in the benchmark U.S. government bond yield,

but nothing that Chair Powell said on Thursday struck us as anything different than what he has been saying for a while now – the Fed will continue to do all it can to keep inflation in check while treading carefully, given that monetary policy works with a lag, and remaining dependent on incoming data.

And speaking of data, we suppose Friday’s big bounce higher in stocks had a great deal to do with the report that morning of worse-than-expected numbers on consumer confidence from the Univ. of Michigan, continuing the recent trend where weaker economic news is good for stocks, as it lessens the risk of addition Fed policy firming, and vice versa.

Valuations – Stocks, Especially Value, Reasonably Priced

So, though we suspect that volatility will remain elevated, and stocks are poised to open lower when trading resumes this week on Friday afternoon’s downgrade of the U.S. credit outlook by Moody’s, we see no reason to alter our enthusiasm for the long-term prospects of the inexpensively priced companies that we have long championed. This is especially true as through Friday, the average Russell 3000 member has lost 2.4% and the Equal-Weight S&P 500 has gained just 1.2% in 2023, while relative valuations for Value in general,

and our broadly diversified portfolios of what we believe to be undervalued stocks in particular continue to be very attractive.

Calendar – Seasonally Favorable Periods Upon Us

And, we can’t forget the calendar as we are now in the seasonally favorable six months of the year,

while the upcoming fourth year of the Presidential Cycle historically has been very favorable, on average!

Stock News – Updates on eleven stocks across seven different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.