The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the jobs report, economic forecasts, treasuries vs. stocks and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – 9 Buys Across 4 Portfolios

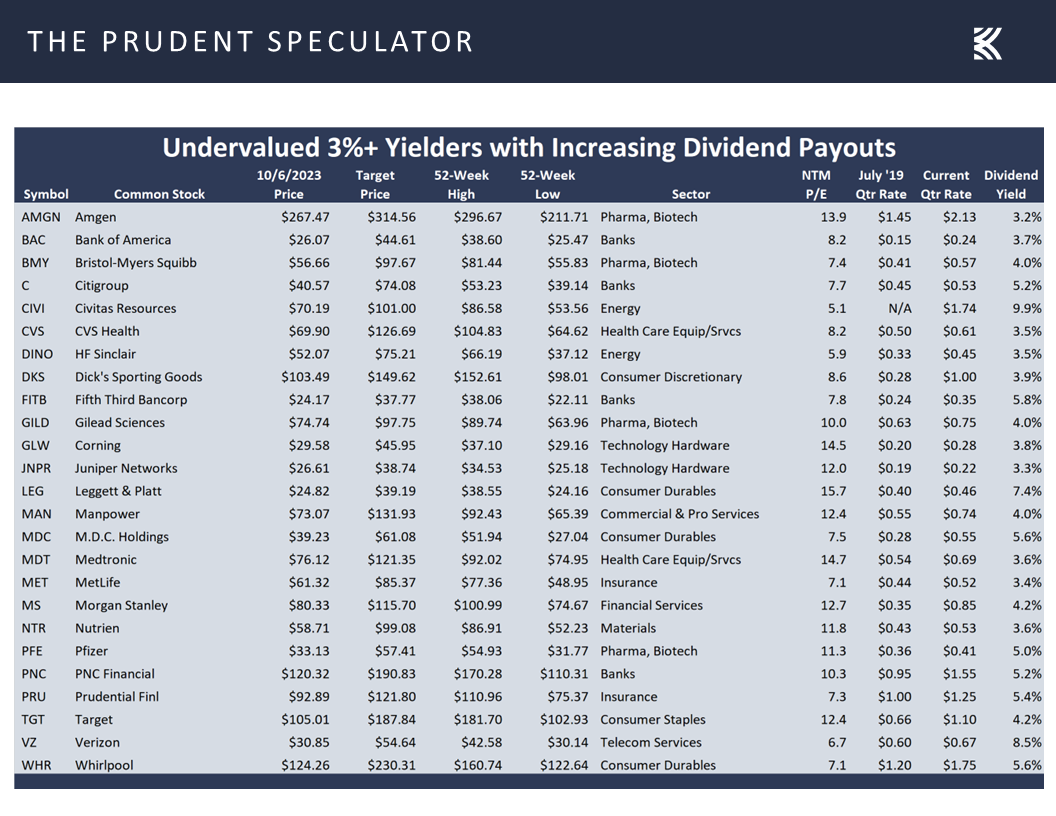

Forbes Cruise – 25 Undervalued, Dividend-Raising, 3%+ Yielders

Historical Perspective – 19 Years Since Buckingham was First at Sea

Week in Review – Most Stocks Sink Despite Favorable Economic News

Jobs Report – Friday Roller-Coaster Ride

Econ Forecasts – Fed Funds, Recession and GDP Outlooks More or Less Unchanged Last Week

Valuations – Liking the Metrics Associated with our Portfolios

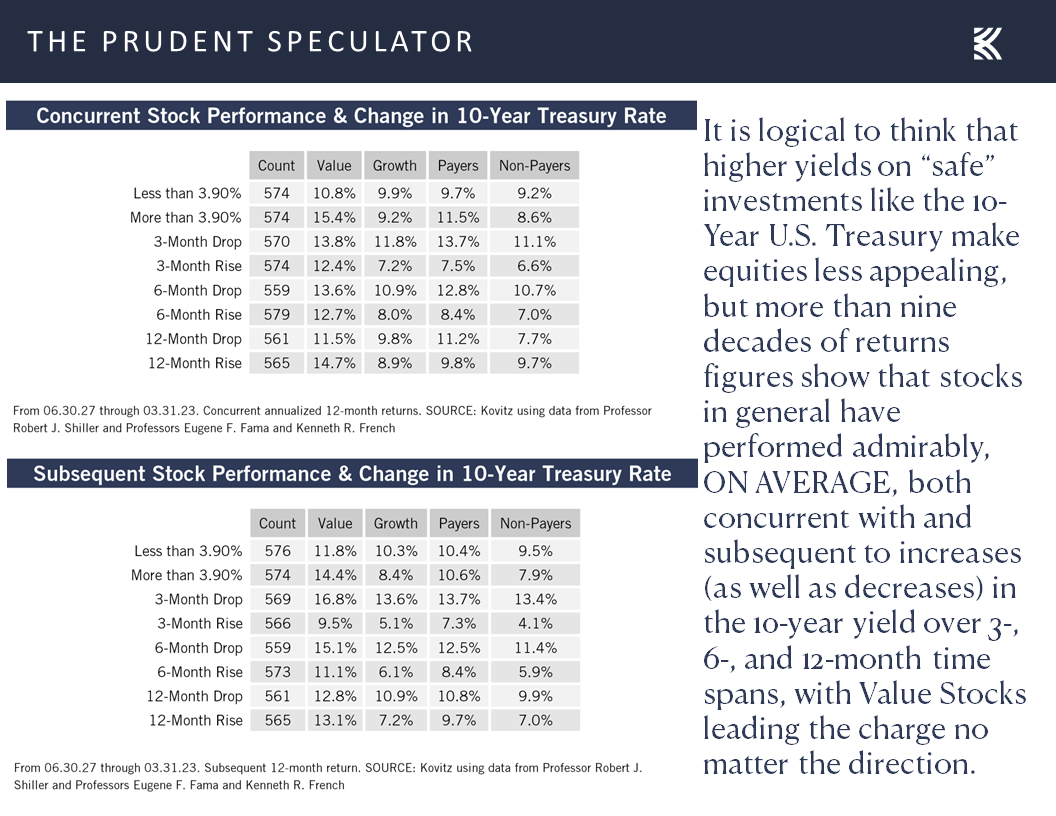

Treasuries vs. Stocks – Historical Odds Still Favor Value and Dividend Payers by a Wide Margin

Stock News – Updates on four stocks across four different sectors

Forbes Cruise – 25 Undervalued, Dividend-Raising, 3%+ Yielders

Greetings from Lipari, Italy, where the 40th Forbes Cruise for Investors is in its penultimate day. It has been an enjoyable voyage with spectacular weather and calm seas, and the crowd seemed to enjoy your Editor’s presentation, The Value of Dividends. Along with many of the charts that appear in these missives, we offered 25 undervalued stocks yielding more than 3% with increasing dividend payouts (50% on average) since the last Buckingham Forbes Cruise in the summer of 2019.

Historical Perspective – 19 Years Since Buckingham was First at Sea

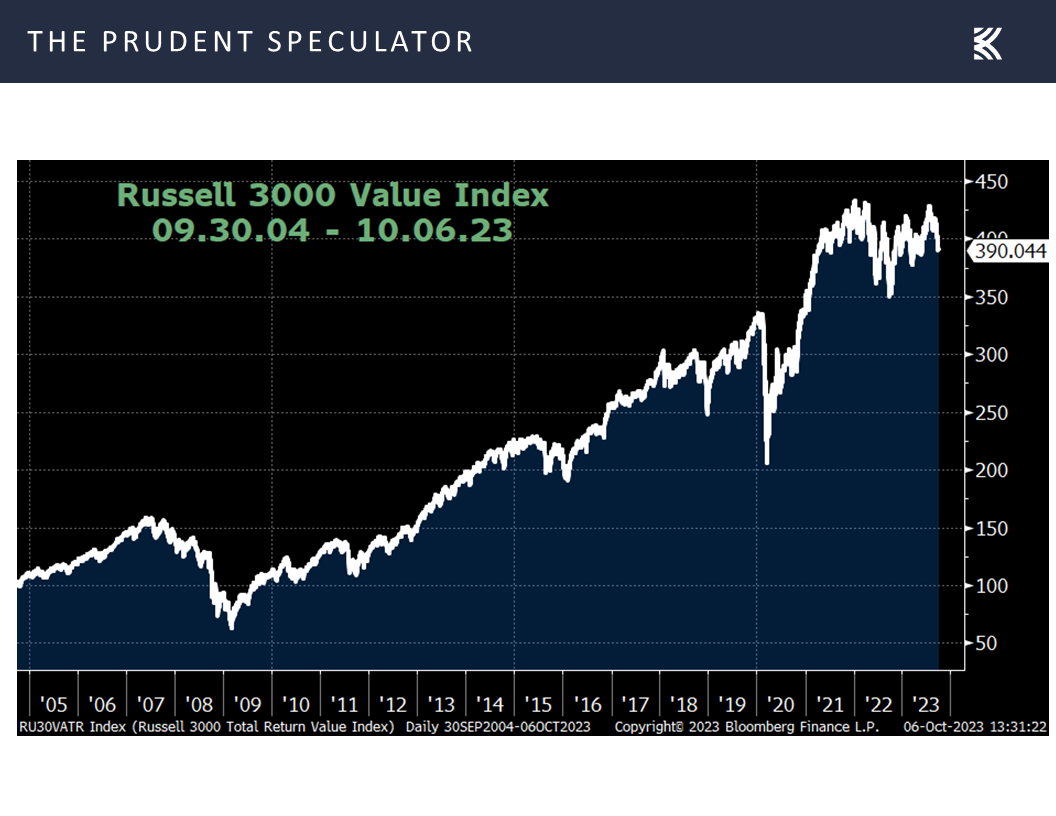

This was my 12th Forbes Cruise since the first journey in September 2004, and, as I joked during my presentation, all of those downward blips on the stock chart below since then seemed to coincide with my time at sea, even as Value stocks have posted handsome overall gains over the past 19 years,

despite plenty of disconcerting events along the way.

Week in Review – Most Stocks Sink Despite Favorable Economic News

With the equal-weight S&P 500 and Russell 3000 Value indexes dropping 1.19% and 1.57%, respectively, and the small-cap Russell 2000 index skidding more than 2%, the latest week seemingly continued the Buckingham-at-sea-equals-rough-sailing-for-stocks trend. This was the case even as the week prior’s late-Friday selloff on fears of a government shutdown appeared to be misguided when Congress over the ensuing weekend passed legislation to keep Uncle Sam open for business, for 45 days at least.

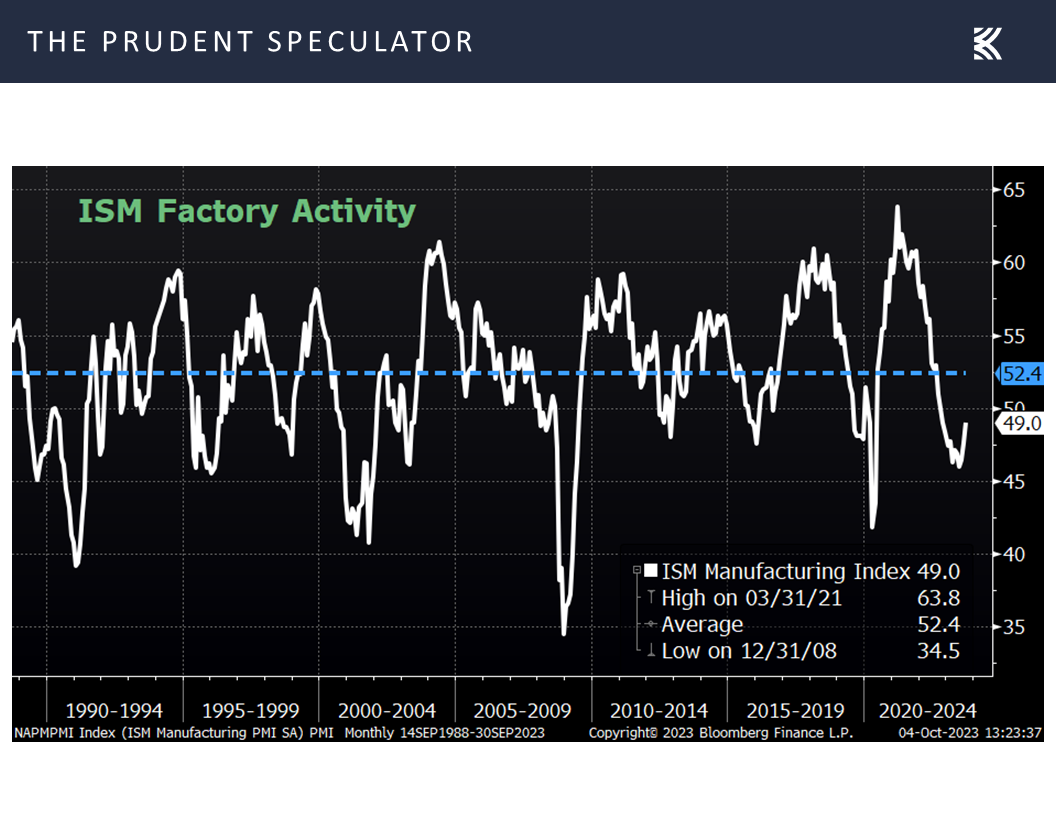

We might also argue that Value stocks, which generally are more economically sensitive, should have railed last week, given that the ISM Manufacturing Index came in at 49.0 for September, ahead of the 47.9 consensus estimate and the 47.6 reading in August.

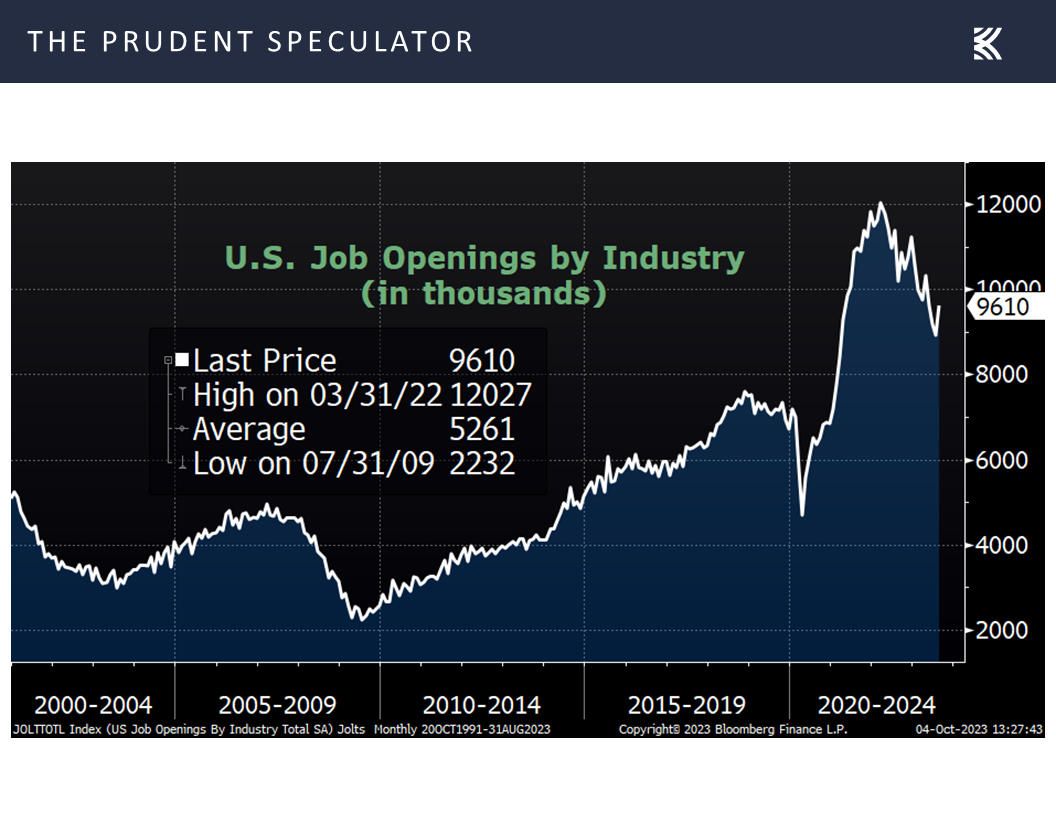

Also, job openings for August rose to 9.6 million, well ahead of expectations and up from 8.9 million the month prior,

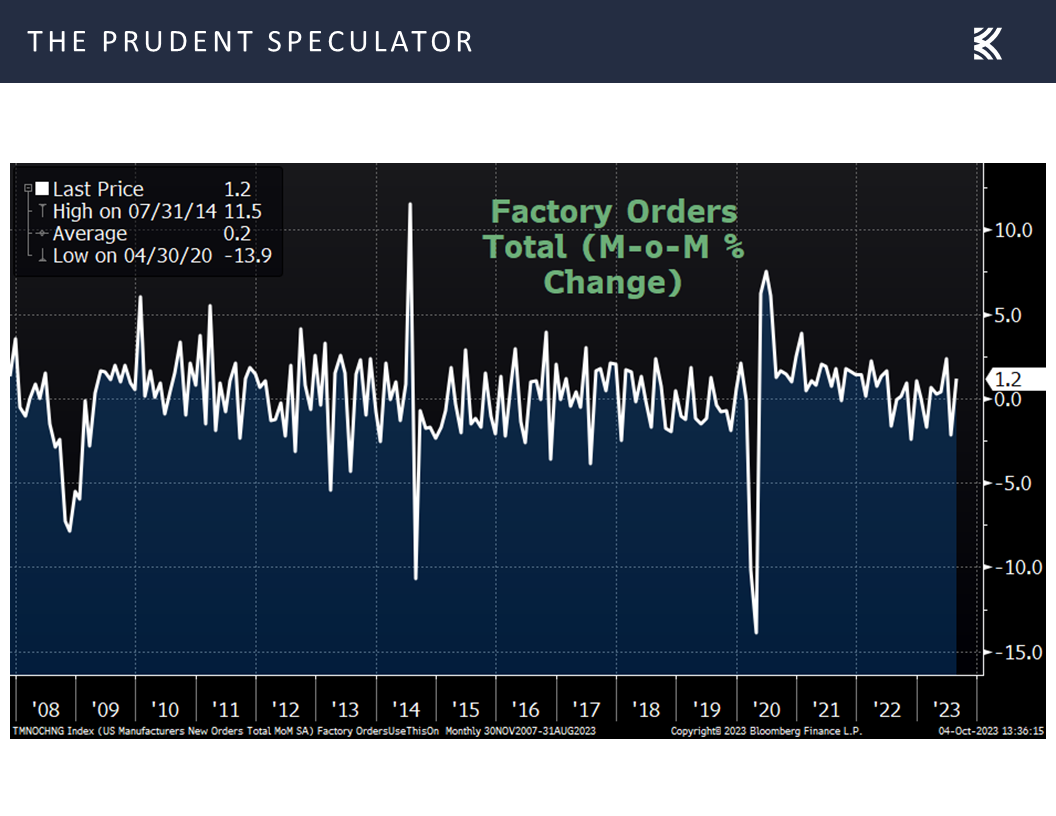

while factory orders for August topped projections with a 1.2% advance,

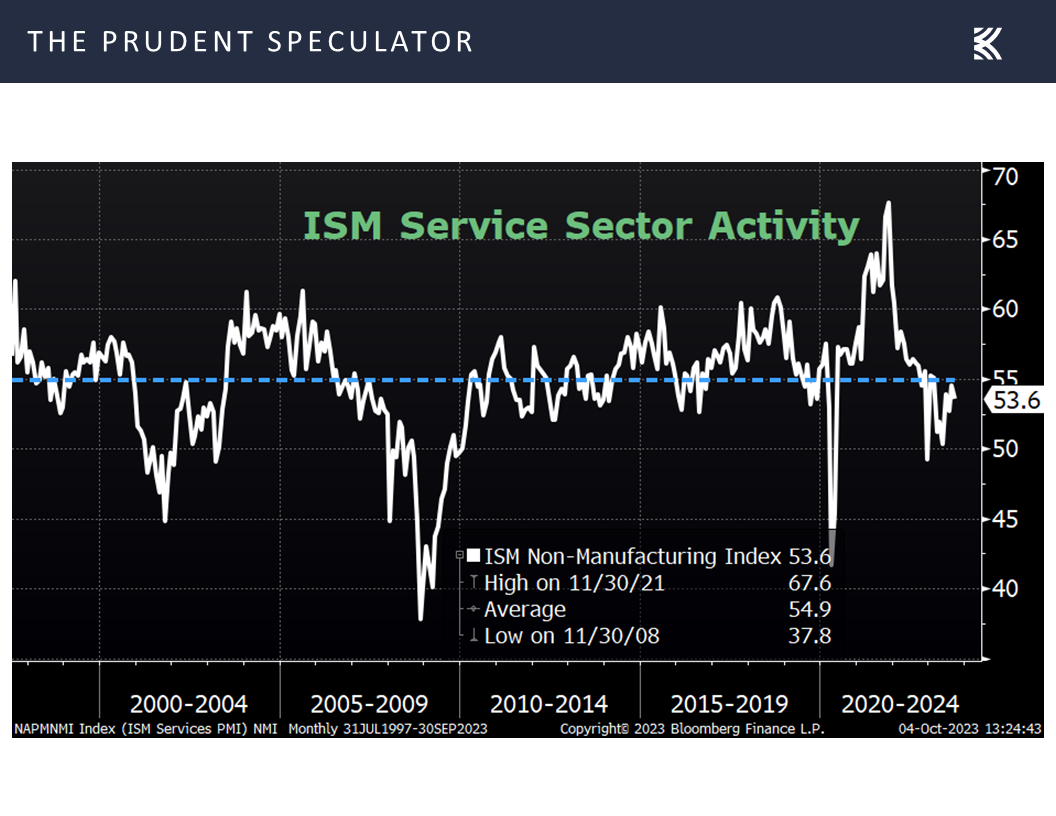

and the ISM Non-Manufacturing Index for September edged above forecasts, coming in at 53.6.

and the ISM Non-Manufacturing Index for September edged above forecasts, coming in at 53.6.

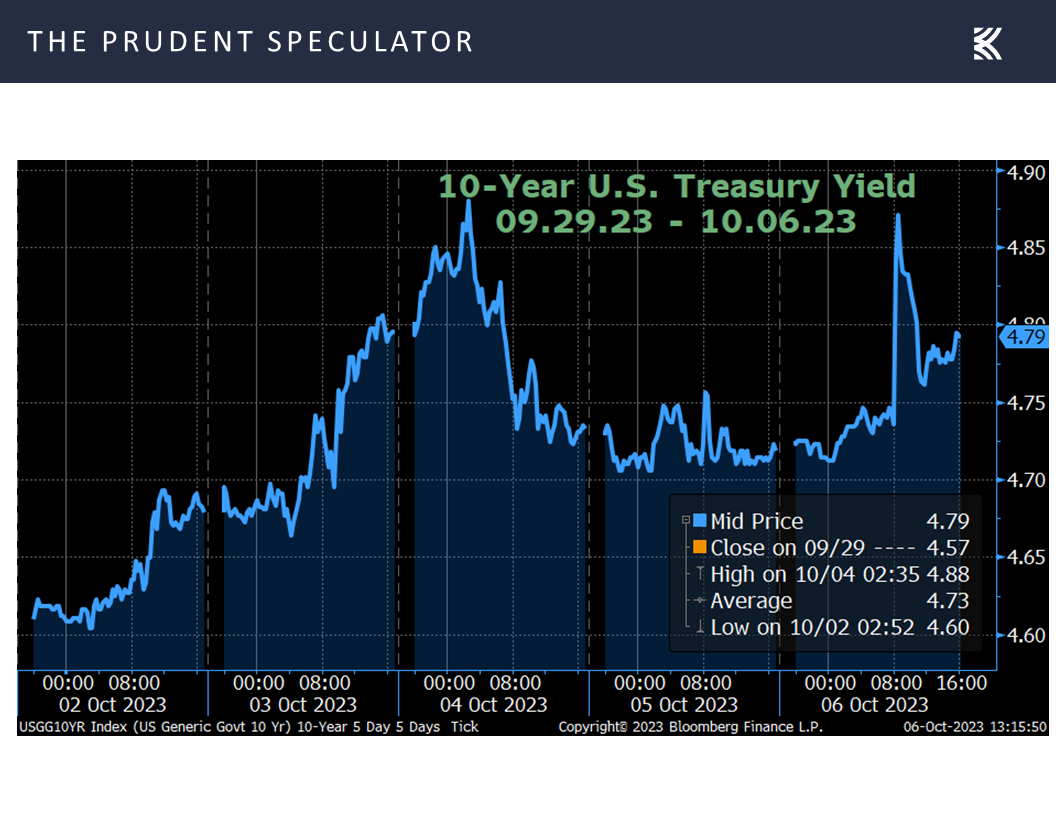

Of course, all of those positive economic stats led to another jump in interest rates,

though we note that stocks of all varieties have performed fine, on average, whether the 10-year U.S. Treasury yield is rising or falling.

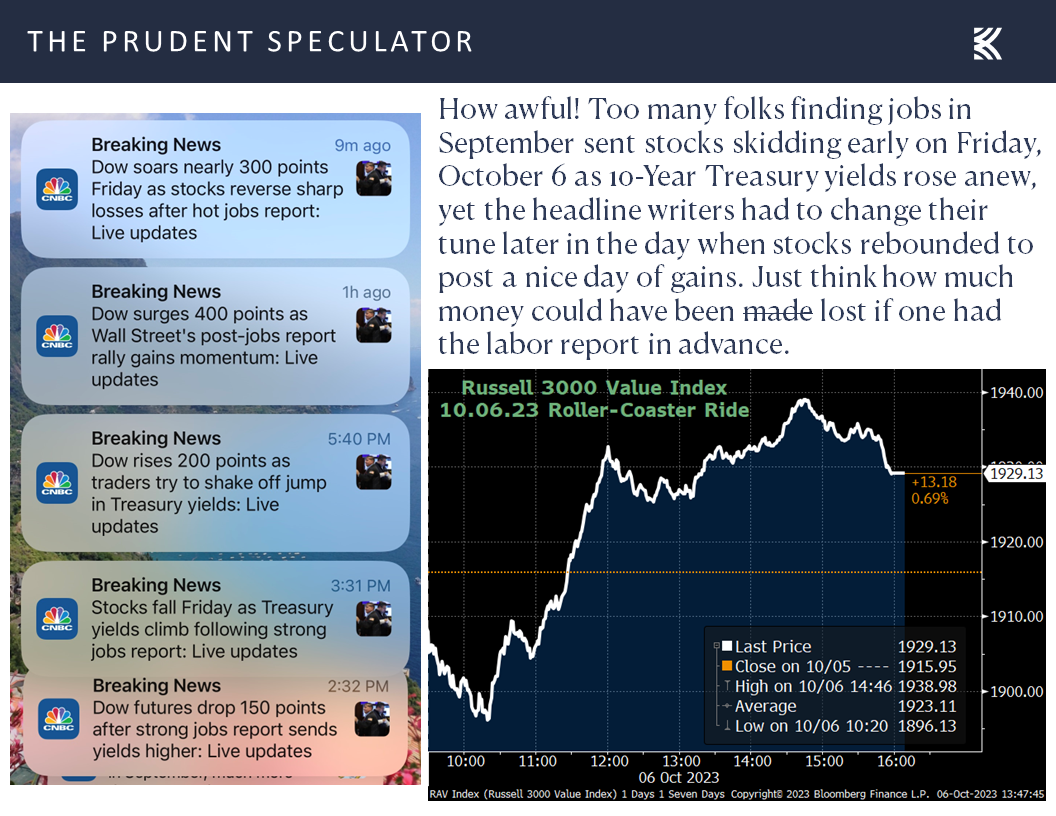

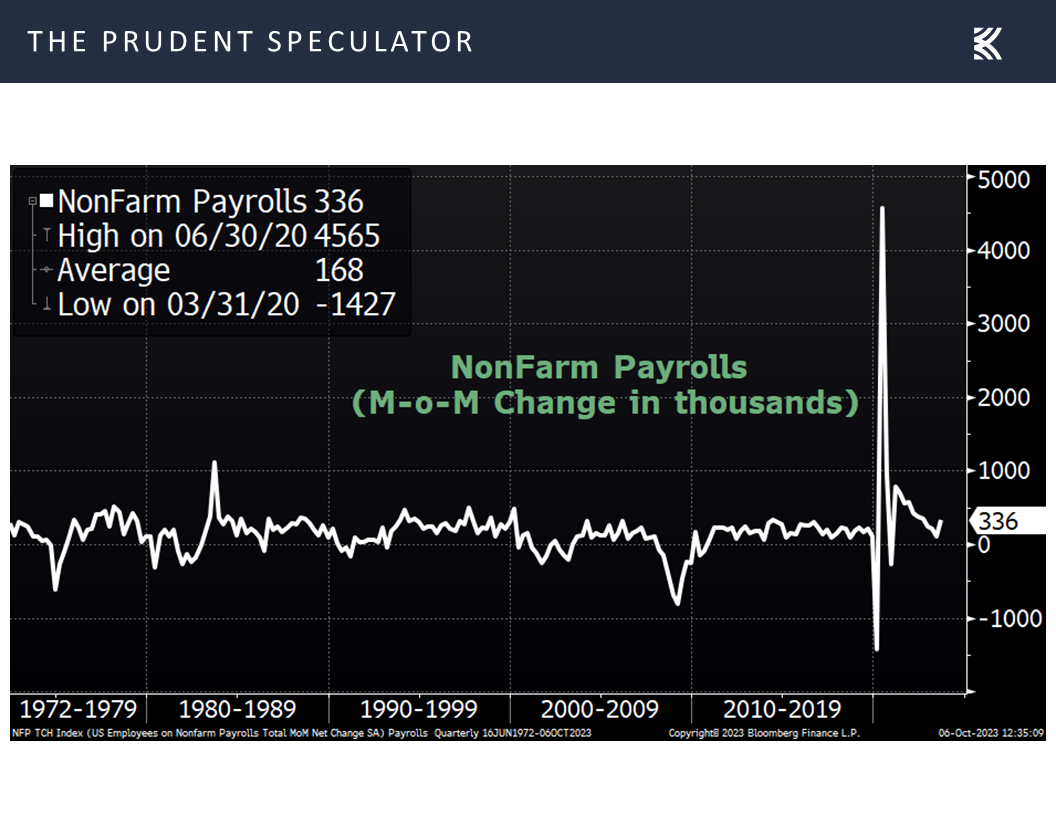

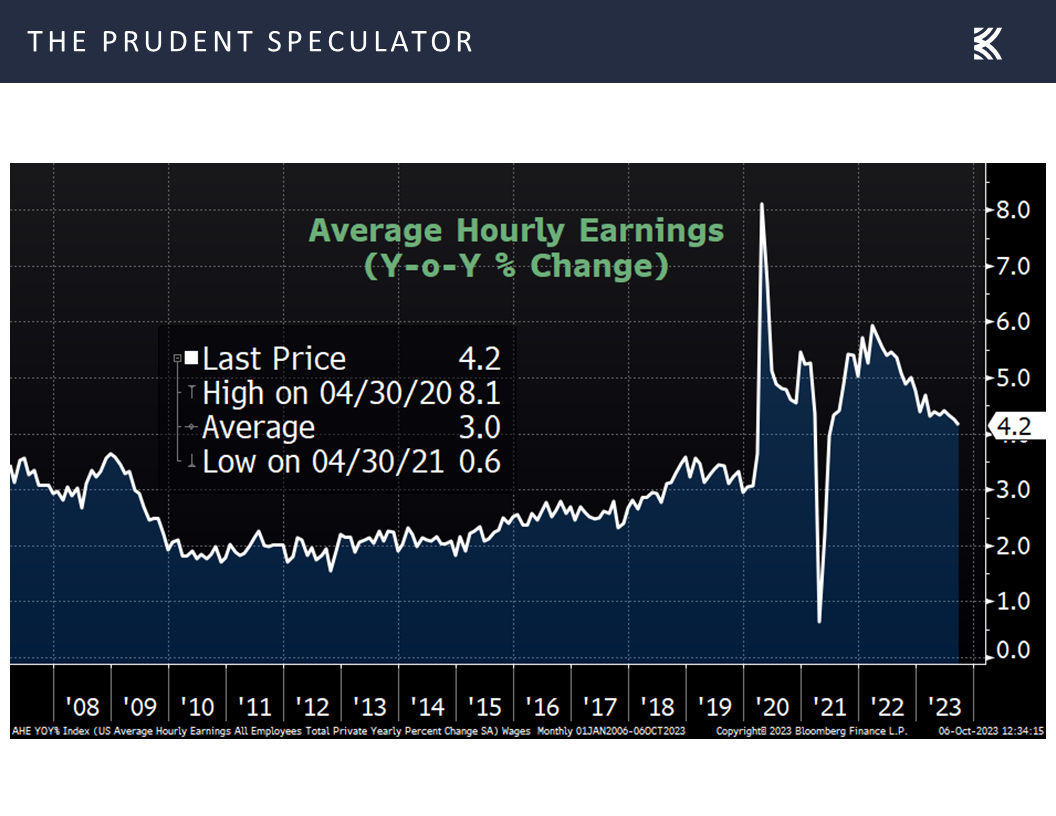

Jobs Report – Friday Roller-Coaster Ride

Interestingly, traders and the media didn’t know what to make of Friday’s impressive jobs report,

with stocks evidently falling on the view that the big jump in payrolls,

might lead the Federal Reserve to keep interest rates higher for longer, but then rebounding on the thinking that the lower-than-expected increase in wages is what Jerome H. Powell & Co. are wanting to see.

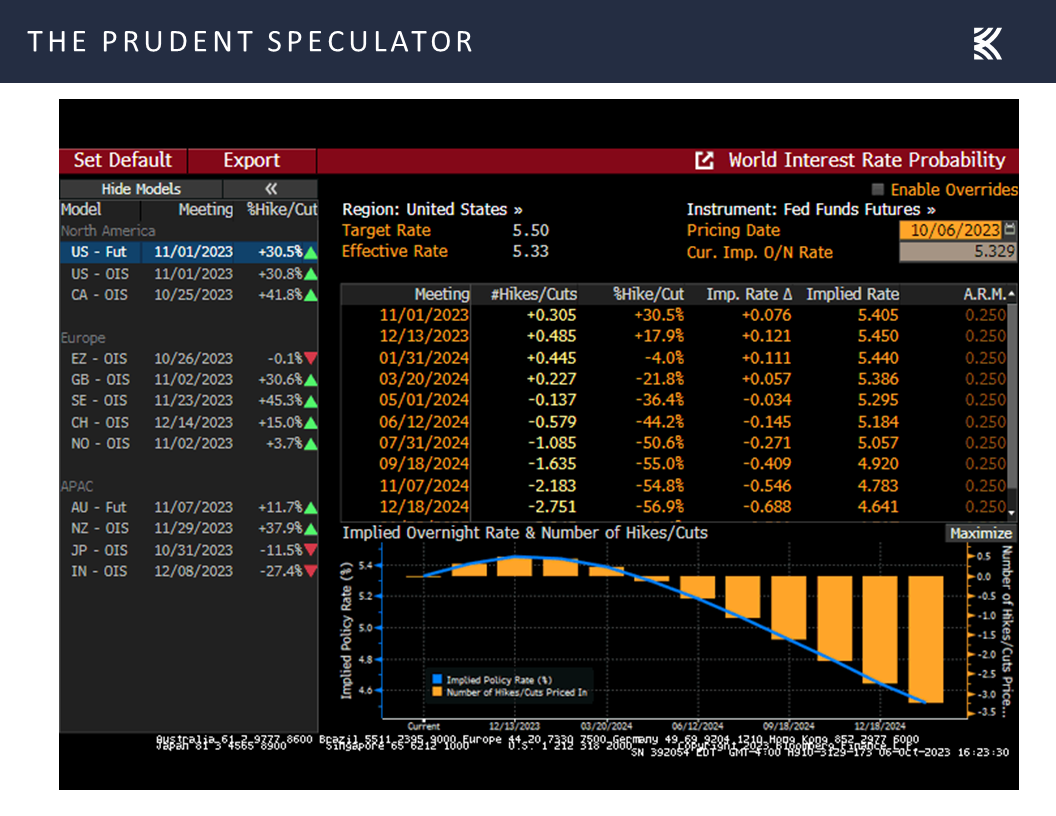

Econ Forecasts – Fed Funds, Recession and GDP Outlooks More or Less Unchanged Last Week

When all was said and done, there really wasn’t much change in the Fed Funds rate outlook (one more hike possible this year before cuts begin in 2024) last week,

while the estimate for real U.S. GDP growth in Q3 held steady at a robust 4.9%,

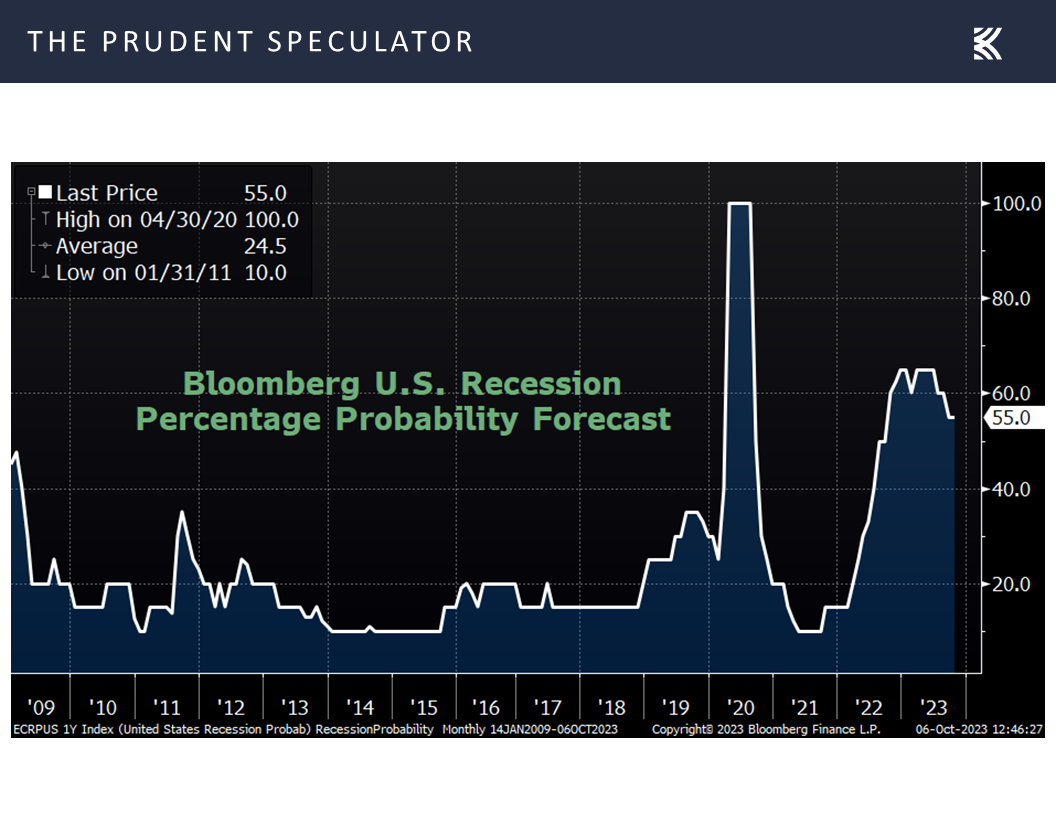

and the recession probability in the next 12 months, per calculations from Bloomberg, remained at 55%.

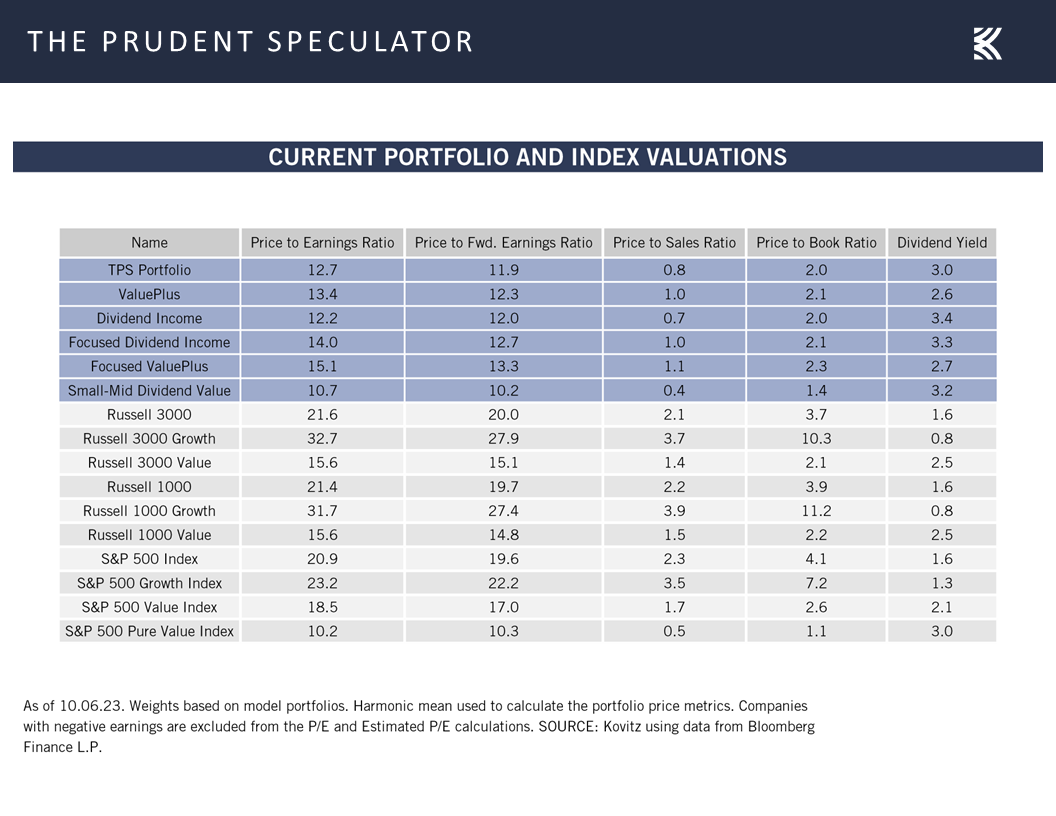

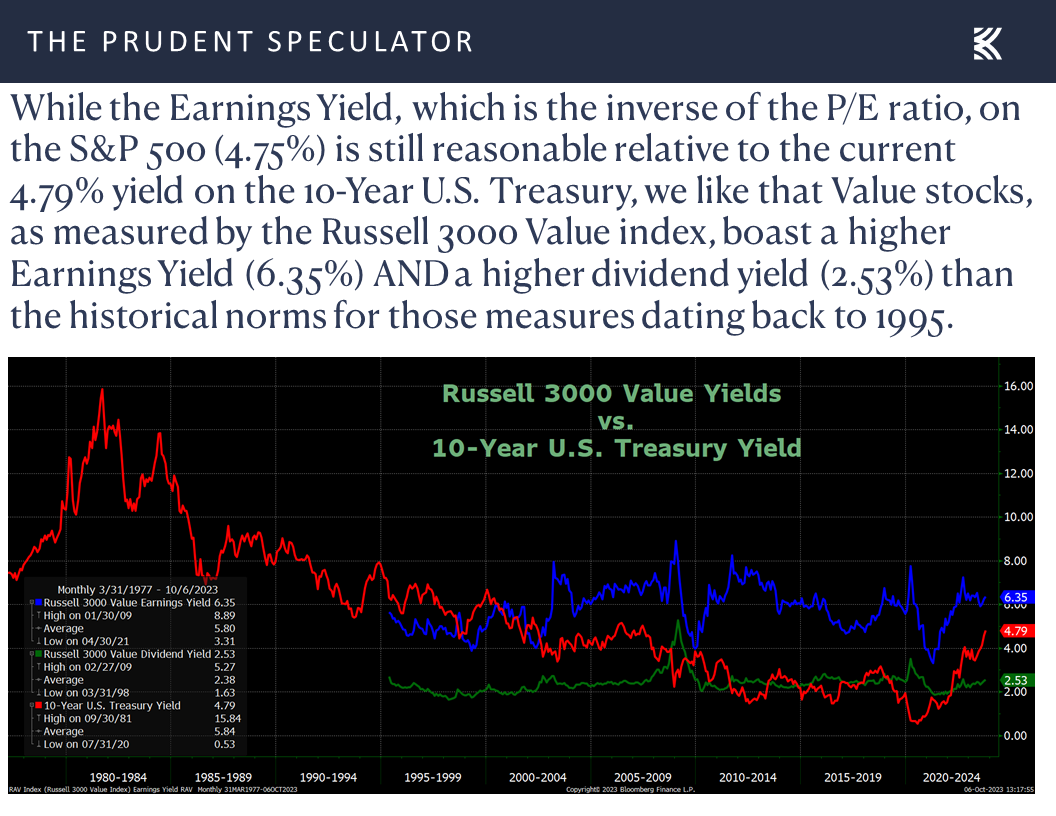

Valuations – Liking the Metrics Associated with our Portfolios

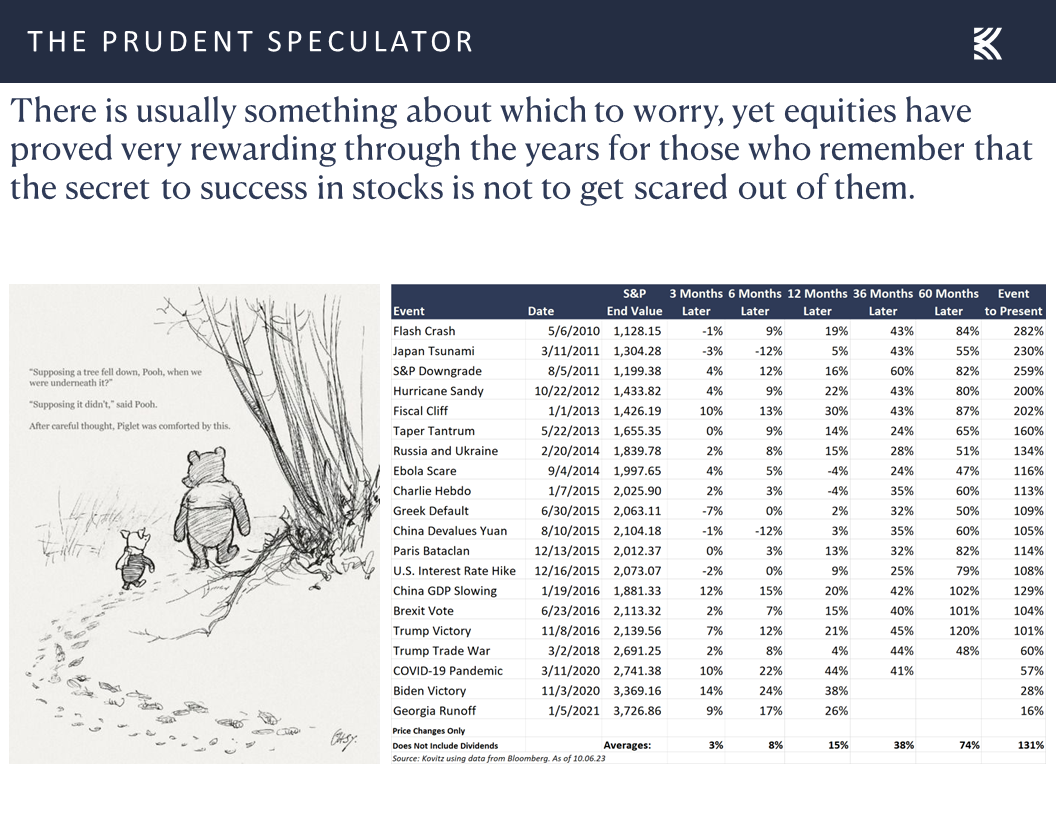

No doubt, the Hamas/Israel conflict that erupted over the weekend adds an additional brick to the proverbial Wall of Worry for the near-term outlook for stocks, but we retain our optimism for the long-term prospects of our broadly diversified portfolio of what we believe to be undervalued stocks.

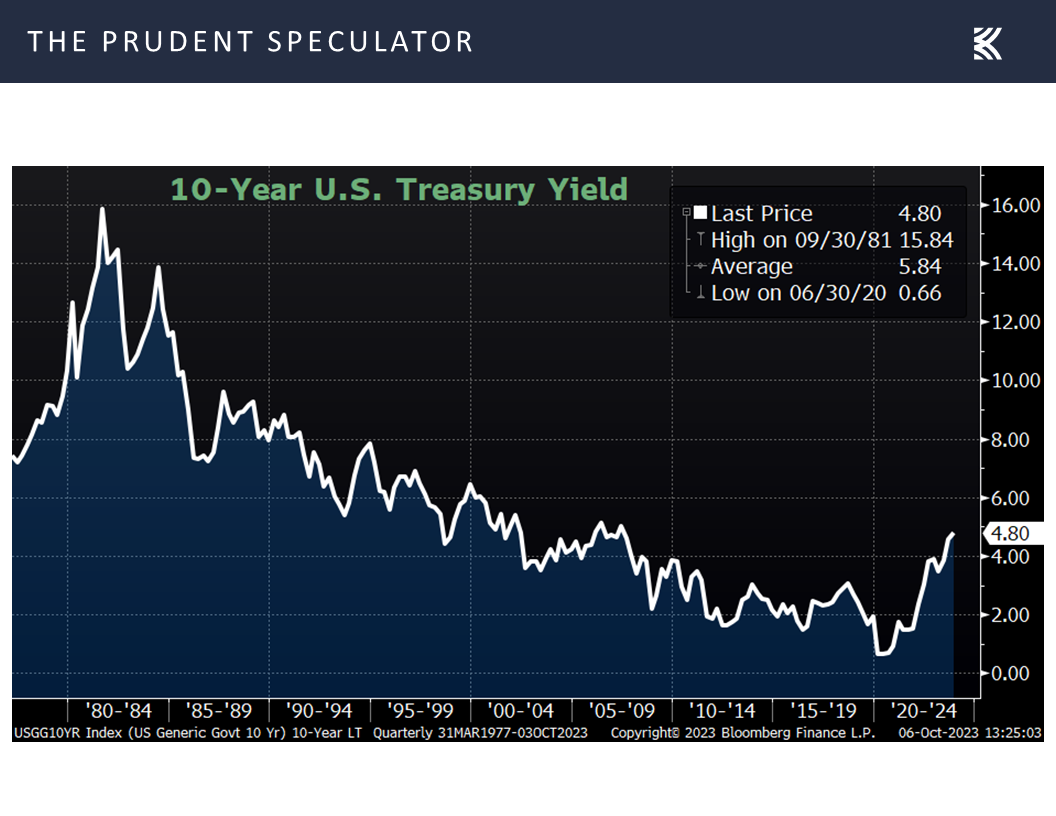

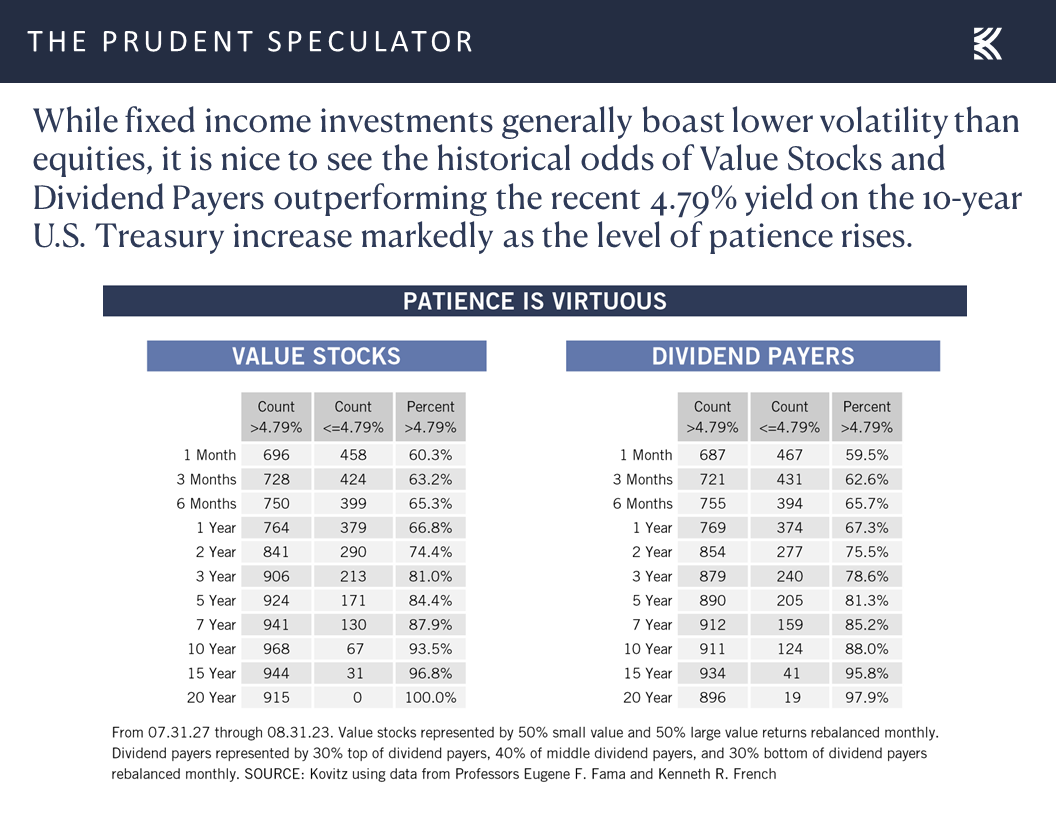

Treasuries vs. Stocks – Historical Odds Still Favor Value and Dividend Payers by a Wide Margin

True, the jump in interest rates adds competition to stocks for those seeking income, but the 10-year Treasury yield today is still well below the 5.84% average since the launch of The Prudent Speculator in 1977,

while the Value segment of the market remains inexpensively priced relative to the “risk-free” rate on an earnings yield basis,

and the historical odds overwhelmingly show that Value Stocks and Dividend Payers have provided better returns than what can be had on “safe” government bonds today, even for those with shorter-term time horizons.

Stock News – Updates on four stocks across four different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Jobs Report, Economic Forecasts, Treasuries vs. Stocks and More

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the jobs report, economic forecasts, treasuries vs. stocks and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – 9 Buys Across 4 Portfolios

Forbes Cruise – 25 Undervalued, Dividend-Raising, 3%+ Yielders

Historical Perspective – 19 Years Since Buckingham was First at Sea

Week in Review – Most Stocks Sink Despite Favorable Economic News

Jobs Report – Friday Roller-Coaster Ride

Econ Forecasts – Fed Funds, Recession and GDP Outlooks More or Less Unchanged Last Week

Valuations – Liking the Metrics Associated with our Portfolios

Treasuries vs. Stocks – Historical Odds Still Favor Value and Dividend Payers by a Wide Margin

Stock News – Updates on four stocks across four different sectors

Forbes Cruise – 25 Undervalued, Dividend-Raising, 3%+ Yielders

Greetings from Lipari, Italy, where the 40th Forbes Cruise for Investors is in its penultimate day. It has been an enjoyable voyage with spectacular weather and calm seas, and the crowd seemed to enjoy your Editor’s presentation, The Value of Dividends. Along with many of the charts that appear in these missives, we offered 25 undervalued stocks yielding more than 3% with increasing dividend payouts (50% on average) since the last Buckingham Forbes Cruise in the summer of 2019.

Historical Perspective – 19 Years Since Buckingham was First at Sea

This was my 12th Forbes Cruise since the first journey in September 2004, and, as I joked during my presentation, all of those downward blips on the stock chart below since then seemed to coincide with my time at sea, even as Value stocks have posted handsome overall gains over the past 19 years,

despite plenty of disconcerting events along the way.

Week in Review – Most Stocks Sink Despite Favorable Economic News

With the equal-weight S&P 500 and Russell 3000 Value indexes dropping 1.19% and 1.57%, respectively, and the small-cap Russell 2000 index skidding more than 2%, the latest week seemingly continued the Buckingham-at-sea-equals-rough-sailing-for-stocks trend. This was the case even as the week prior’s late-Friday selloff on fears of a government shutdown appeared to be misguided when Congress over the ensuing weekend passed legislation to keep Uncle Sam open for business, for 45 days at least.

We might also argue that Value stocks, which generally are more economically sensitive, should have railed last week, given that the ISM Manufacturing Index came in at 49.0 for September, ahead of the 47.9 consensus estimate and the 47.6 reading in August.

Also, job openings for August rose to 9.6 million, well ahead of expectations and up from 8.9 million the month prior,

while factory orders for August topped projections with a 1.2% advance,

Of course, all of those positive economic stats led to another jump in interest rates,

though we note that stocks of all varieties have performed fine, on average, whether the 10-year U.S. Treasury yield is rising or falling.

Jobs Report – Friday Roller-Coaster Ride

Interestingly, traders and the media didn’t know what to make of Friday’s impressive jobs report,

with stocks evidently falling on the view that the big jump in payrolls,

might lead the Federal Reserve to keep interest rates higher for longer, but then rebounding on the thinking that the lower-than-expected increase in wages is what Jerome H. Powell & Co. are wanting to see.

Econ Forecasts – Fed Funds, Recession and GDP Outlooks More or Less Unchanged Last Week

When all was said and done, there really wasn’t much change in the Fed Funds rate outlook (one more hike possible this year before cuts begin in 2024) last week,

while the estimate for real U.S. GDP growth in Q3 held steady at a robust 4.9%,

and the recession probability in the next 12 months, per calculations from Bloomberg, remained at 55%.

Valuations – Liking the Metrics Associated with our Portfolios

No doubt, the Hamas/Israel conflict that erupted over the weekend adds an additional brick to the proverbial Wall of Worry for the near-term outlook for stocks, but we retain our optimism for the long-term prospects of our broadly diversified portfolio of what we believe to be undervalued stocks.

Treasuries vs. Stocks – Historical Odds Still Favor Value and Dividend Payers by a Wide Margin

True, the jump in interest rates adds competition to stocks for those seeking income, but the 10-year Treasury yield today is still well below the 5.84% average since the launch of The Prudent Speculator in 1977,

while the Value segment of the market remains inexpensively priced relative to the “risk-free” rate on an earnings yield basis,

and the historical odds overwhelmingly show that Value Stocks and Dividend Payers have provided better returns than what can be had on “safe” government bonds today, even for those with shorter-term time horizons.

Stock News – Updates on four stocks across four different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.