The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Liberation Day, Volatility, Interesting Rates and Recessions. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – 9 Buys Across 4 Portfolios

Buckingham AAII Appearance – San Diego, April 12, 2025, at 9:00 A.M Pacific

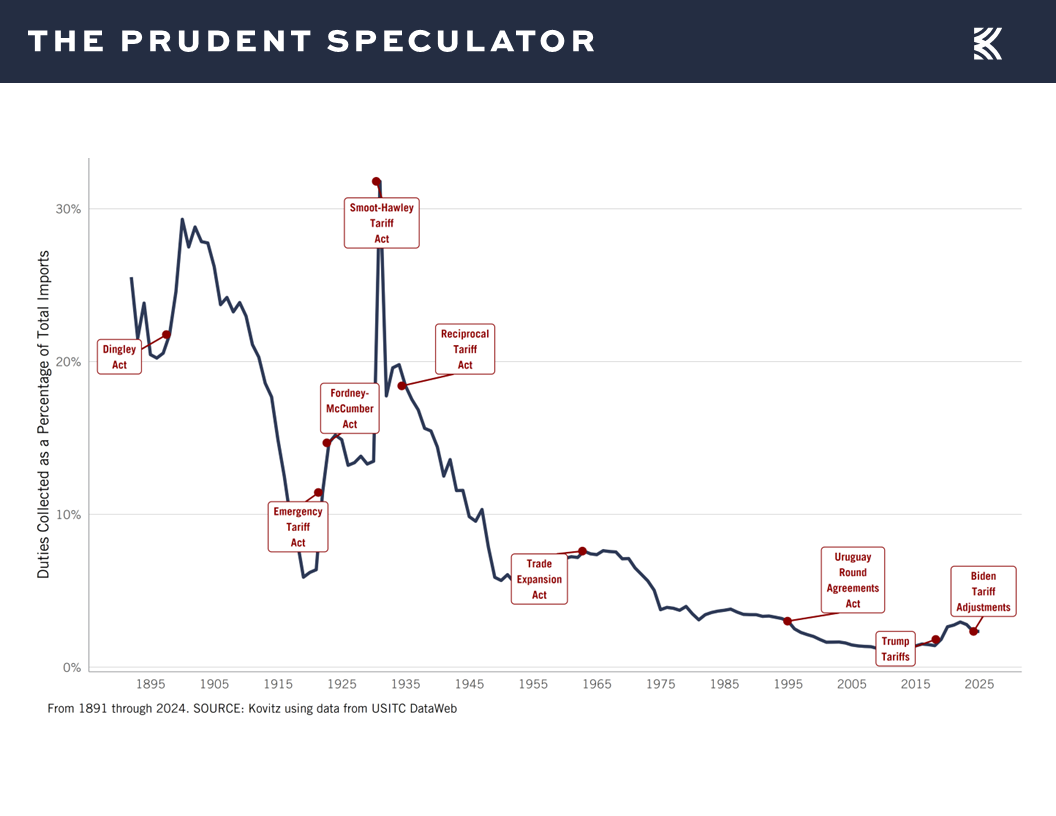

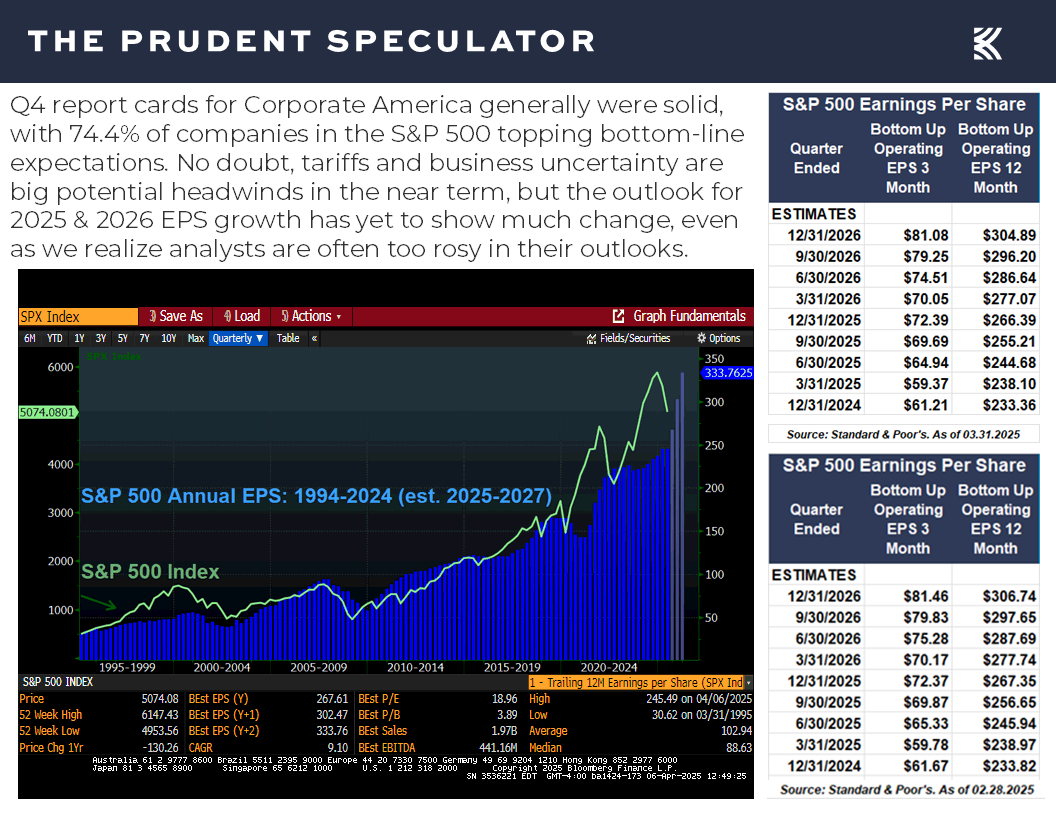

Liberation Day – More Severe-than-Expected Tariffs Sends Stocks Plunging

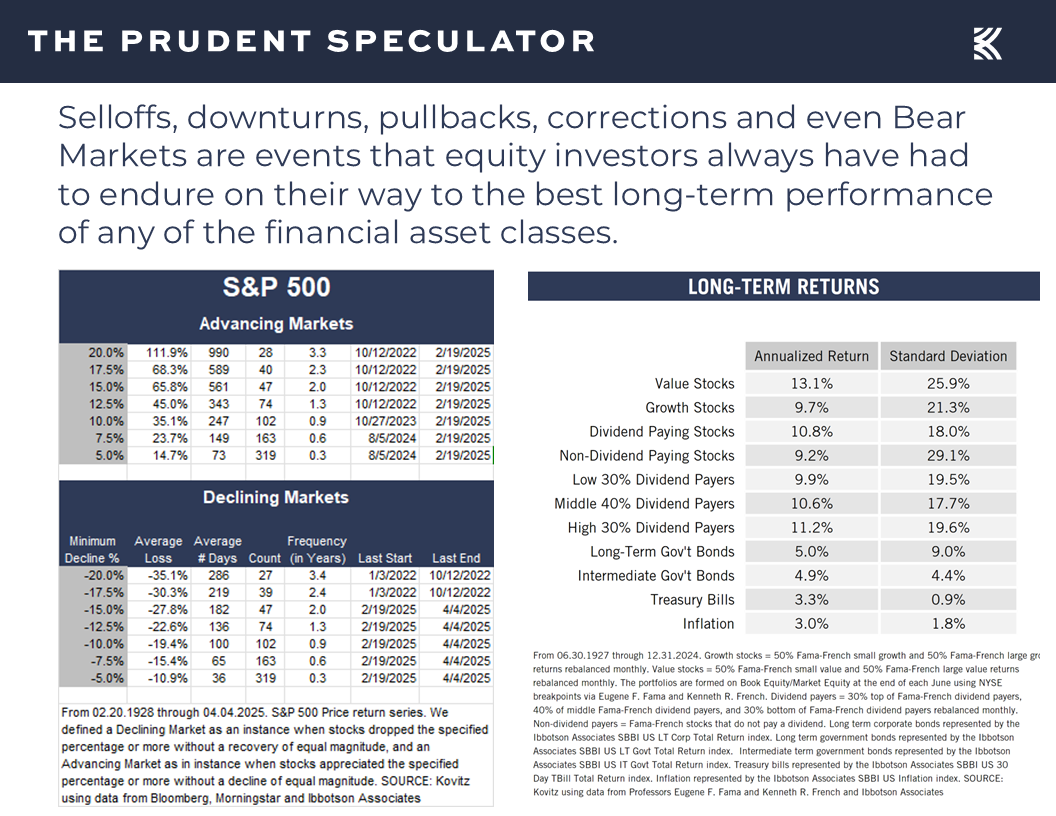

Volatility – Corrections…and Even Bear Markets…are Part of the Investment Process

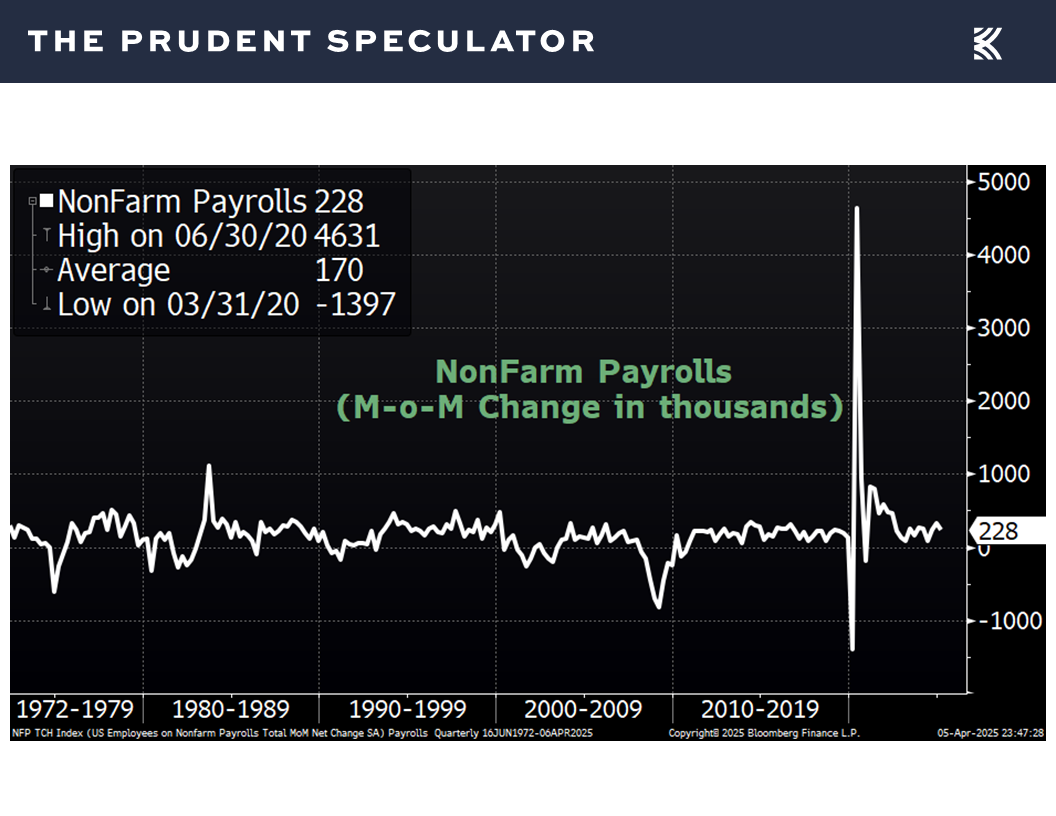

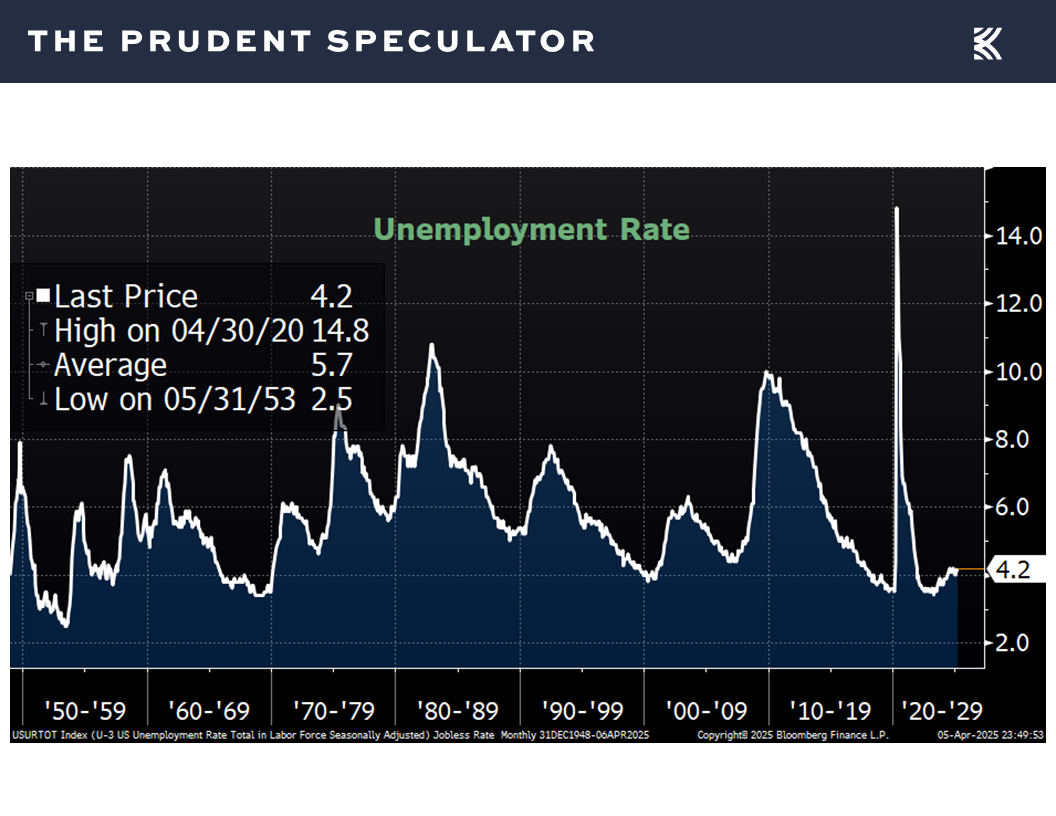

Econ News – Solid Jobs Numbers; Even Relatively Weak ISM Numbers Have Correlated in the Past to Real GDP Growth

Powell – Fed Chair Waiting for Greater Clarity Before Making Adjustments to Monetary Policy

Interest Rates – Big Drop in the 10-Year Adds to Equity Attractiveness; Fed Expected to Cut Rates Several Times Before Year-End

Sentiment – Headlines Super Negative at Market Bottoms; AAII and CNN Fear & Greed Index Flashing Contrarian Buy Signals

Recessions – Risk Has Spiked, But History Shows Staying the Course the Right Move Even if a Contraction Were to Occur

2020 – Far Worse COVID-19 Massacre for Stocks; But the Year Ended Higher than it Began

Patience – The Longer the Hold the Better the Chance of Success

Valuations – Liking the Metrics on our Portfolios

Dividends – Focusing on Income Received vs. Stock-Price Gyrations Can Provide Better Slumber

Stock News – Two-Dozen Hard-Hit Liberation Day Stocks

Buckingham AAII Appearance – San Diego, April 12, 2025, at 9:00 A.M Pacific

Your Editor will be speaking in San Diego on Saturday, April 12, 2025, at 9:00 AM Pacific. Registration info for that presentation is available here:

Upcoming Chapter Events – AAII San Diego

Note, too, that the AAII folks are making the presentation available via Zoom.

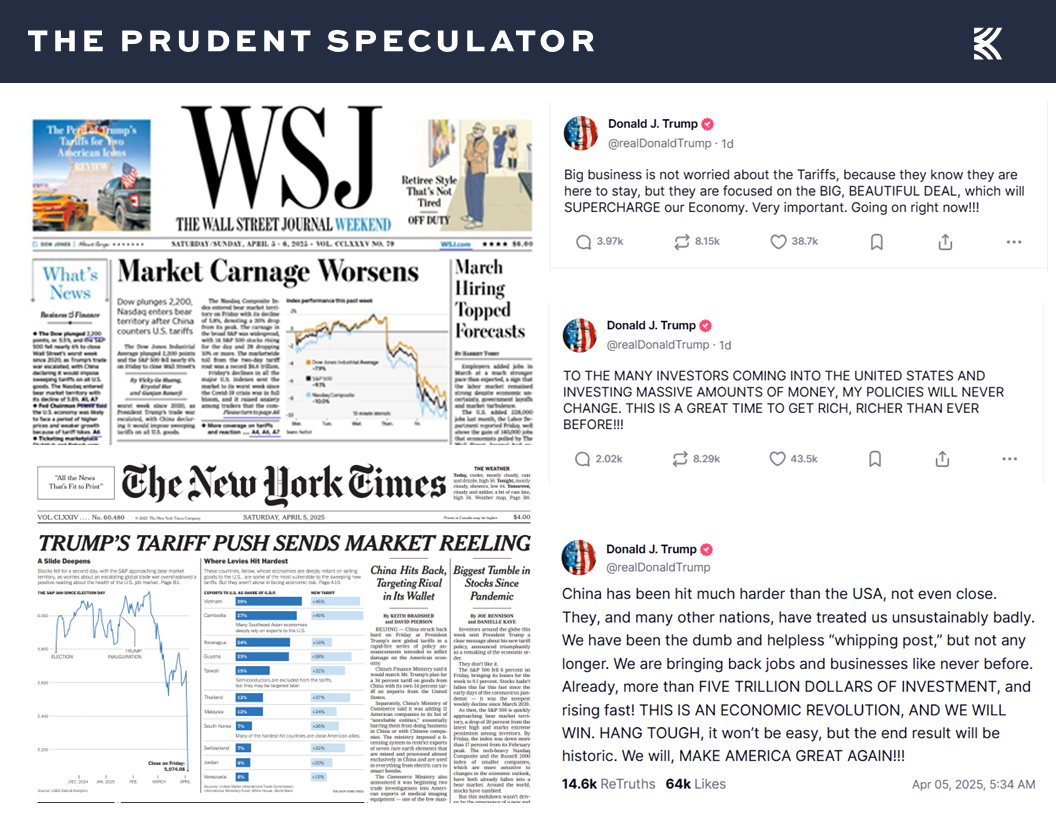

Liberation Day – More Severe-than-Expected Tariffs Sends Stocks Plunging

RH (Restoration Hardware) CEO Gary Friedman exclaimed, “Oh, sh—, OK. OK. I just looked at the screen. I had to look at it. It got hit when I think the tariff came out,” on the quarterly earnings call seeing the after-hours plunge in the furniture retailer’s stock on Wednesday afternoon. No doubt, most investors uttered the same expletive in reaction to last week’s carnage in the equity markets, with stocks enduring back-to-back massive selloffs on Thursday and Friday.

Obviously, the catalyst for the bloodbath was the “Liberation Day” ceremony in the Rose Garden, as the White House announced 10% across-the-board tariffs on all imports (which became effective April 5) and reciprocal higher tariffs on counties with which the U.S. has the largest trade deficits (which go into effect April 9). While President Trump proclaimed, “Jobs and factories will come roaring back into the country,” the tariffs were far more drastic than expected and China quickly retaliated with reciprocal tariffs of its own on U.S. goods.

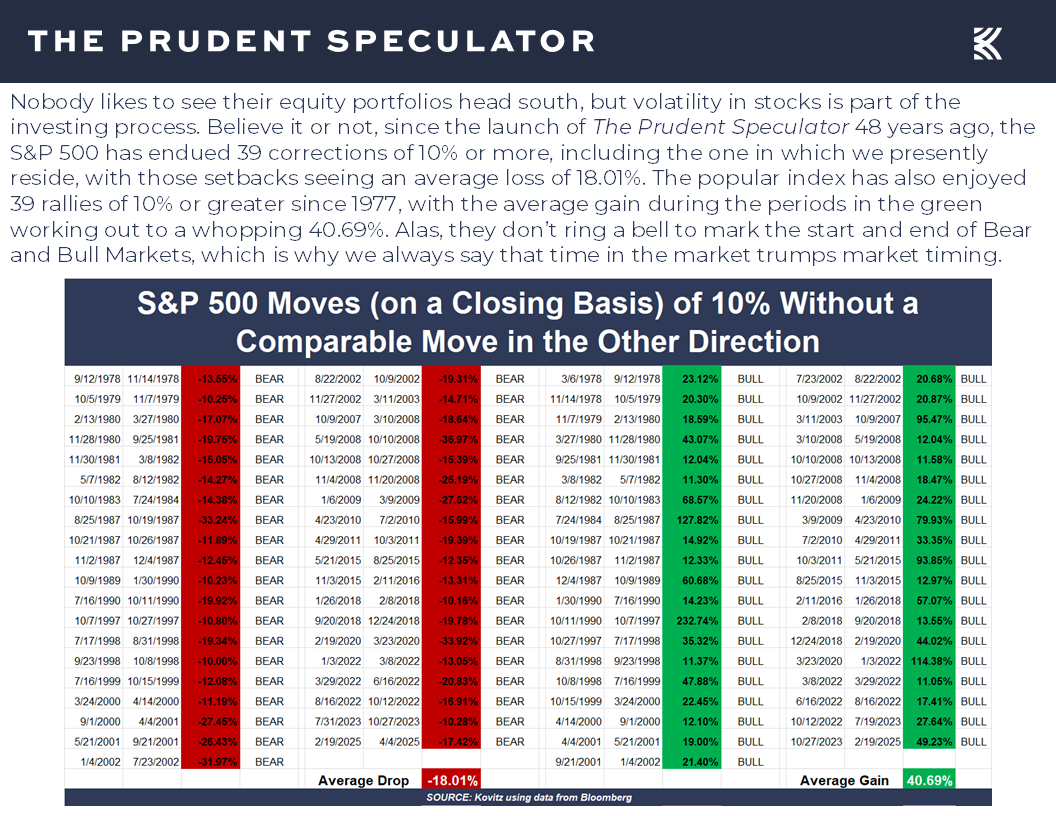

Volatility – Corrections…and Even Bear Markets…are Part of the Investment Process

Most think the tariffs are a salvo in Trump’s Art of the Deal, and Vietnam (which manufactures a major portion of apparel for U.S. companies) evidently was on the phone with the President on Friday to supposedly try to cut a deal to lower its tariffs to zero, while the White House said on Sunday that over 50 countries have contacted the U.S. in a bid to negotiate the tariffs. Still, the markets thus far have decided to shoot first and ask questions later, with stocks of virtually all stripes taken out to the proverbial woodshed.

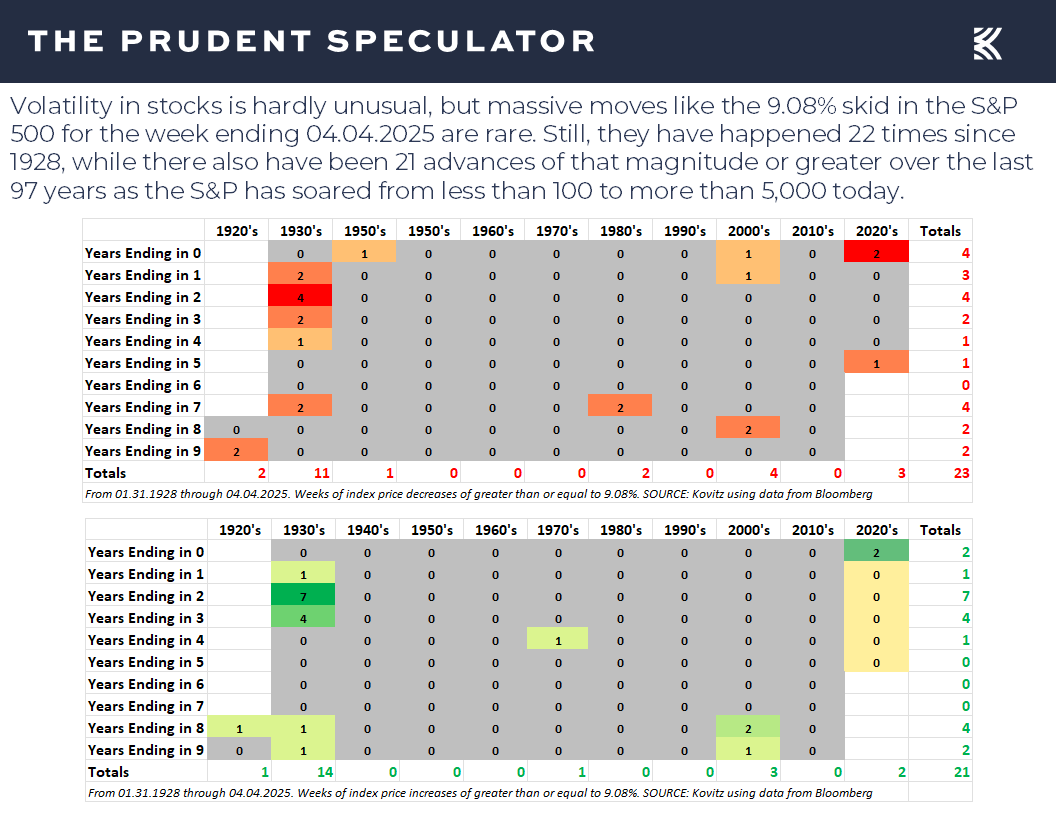

When all was said and done, the market averages endured one of their worst weeks in history, with the S&P 500’s tumble of more than 9% the biggest weekly setback since 2020,

extending the 2025 pullback from recent all-time highs to mid-teen-to 20%+ percentage levels.

Certainly, the speed of the drop is disconcerting, and nerves are on edge, so we encourage those who share our long-term time horizon to channel Vannevar Bush. The American engineer and investor said, “Fear cannot be banished, but it can be calm and without panic; it can be mitigated by reason and evaluation.”

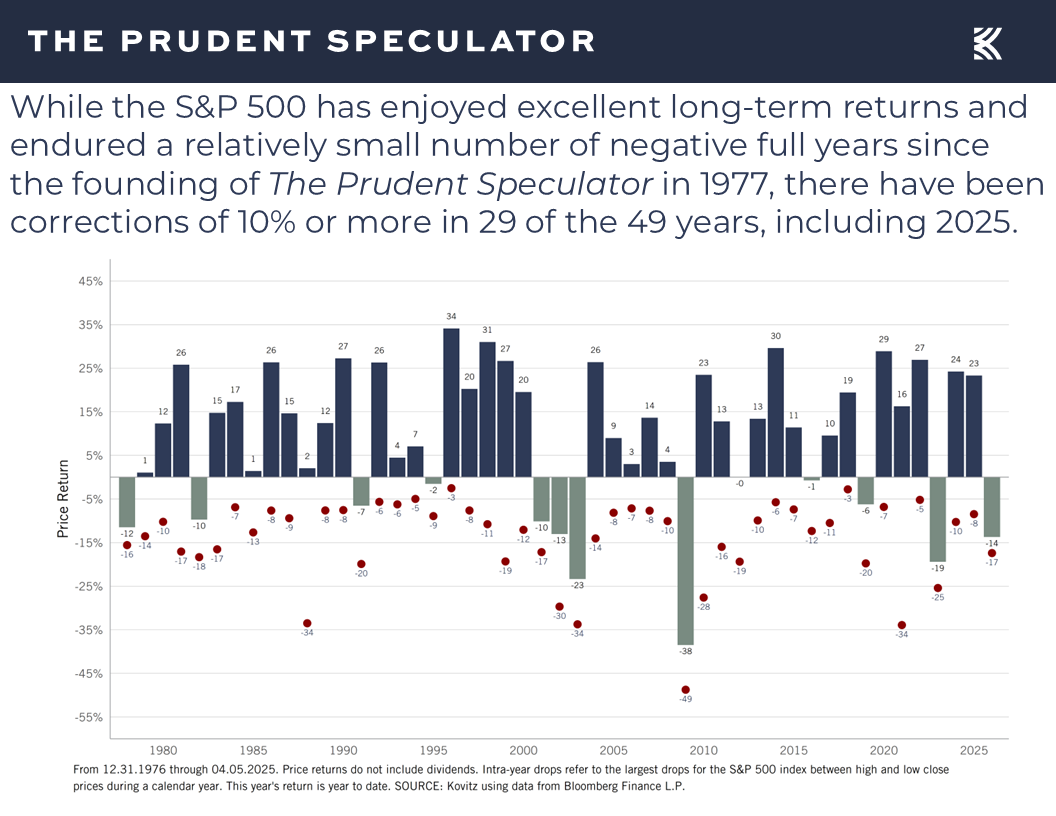

As painful as last week was, downturns are a very normal part of the investment process, some worse than others happening every year,

while the magnitude of this correction (the 39th setback of 10% or more without an intervening rally of at least 10% that has been endured since we launched The Prudent Speculator in 1977) is about average by historical standards.

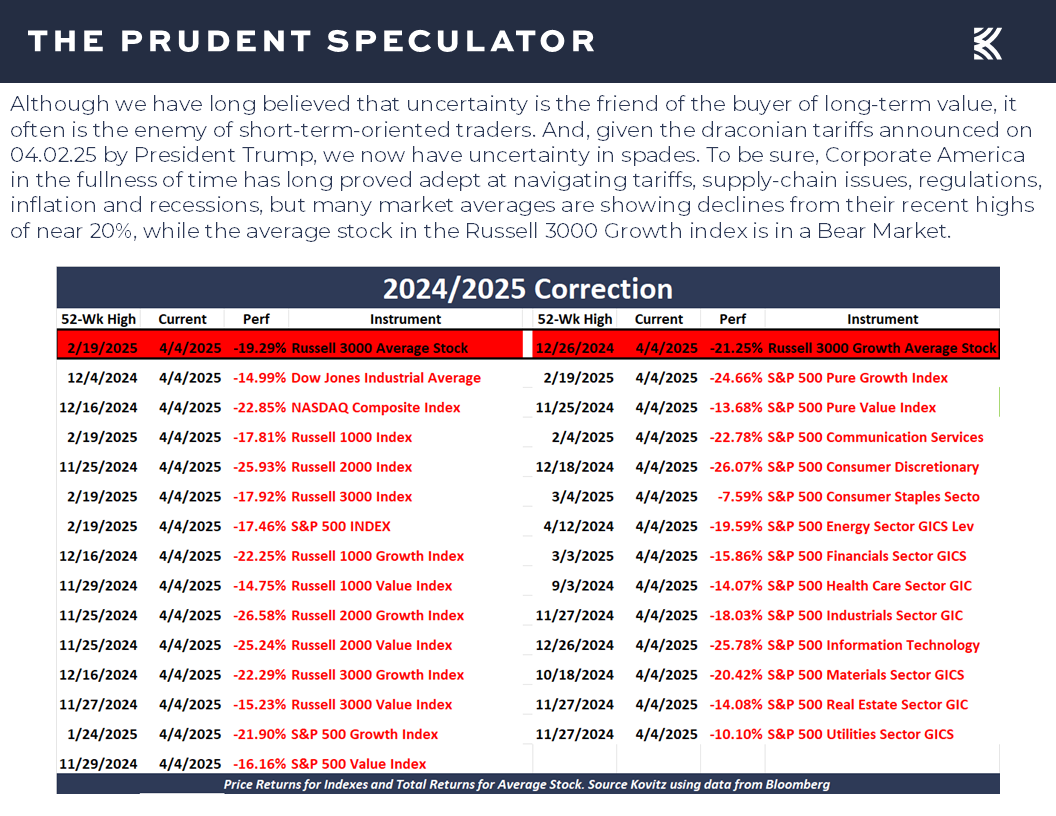

True, we are not that far away from an official Bear Market for the S&P 500, but that popular index has suffered drops of 20% or more every 3.4 years on average, yet equities, led by Value Stocks have still enjoyed sensational long-term returns,

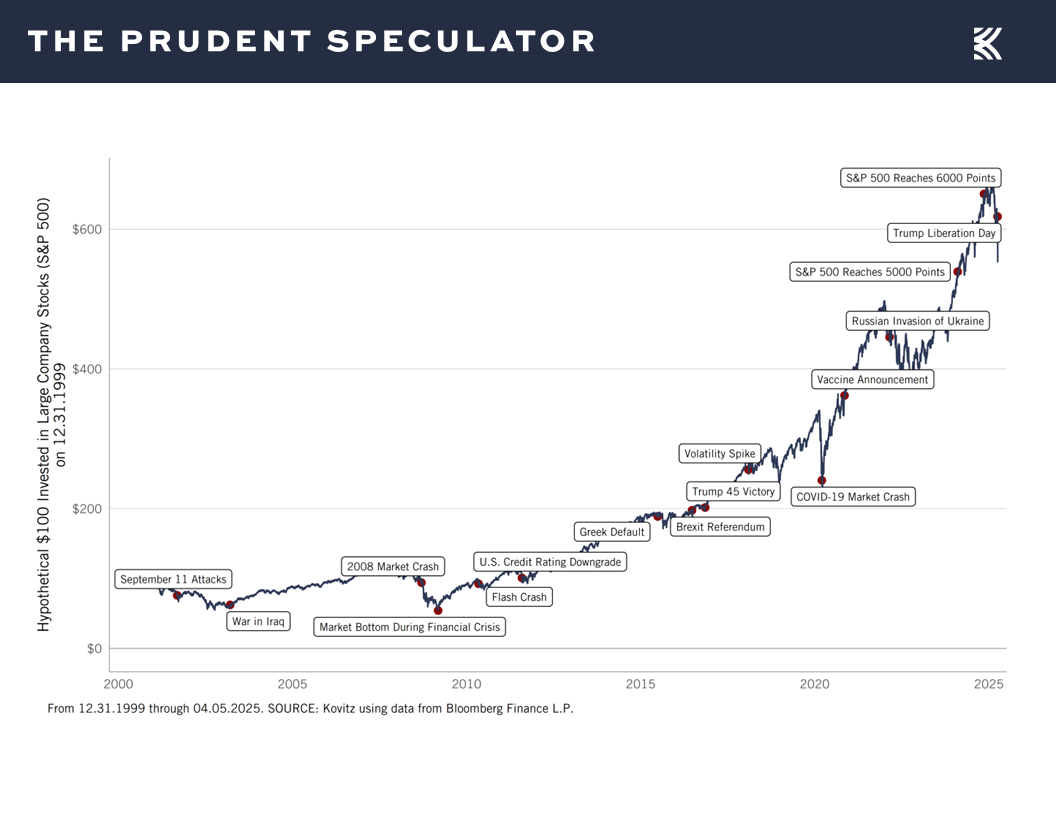

eventually overcoming all prior frightening events in the fullness of time,

with troubles of the past often not more than a small blip on a long-term chart of market returns.

with troubles of the past often not more than a small blip on a long-term chart of market returns.

Without question, this time (and every time) is different, even as tariffs have long been part of the landscape,

Econ News – Solid Jobs Numbers; Even Relatively Weak ISM Numbers Have Correlated in the Past to Real GDP Growth

but the U.S. economy ended March with better-than-average and better-than-estimated net-new-job creation as 228,000 payrolls were created in the month,

and the unemployment rate at 4.2% was well below the historical average,

Powell – Fed Chair Waiting for Greater Clarity Before Making Adjustments to Monetary Policy

with Jerome H. Powell stating on Friday, April 4…

Looking across many indicators, the labor market appears to be broadly in balance and is not a significant source of inflationary pressure. This morning’s jobs report shows the unemployment rate at 4.2 percent in March, still in the low range where it has held since early last year. Over the first quarter, payrolls grew by an average of 150,000 jobs a month. The combination of low layoffs, moderating job growth, and slowing labor force growth has kept the unemployment rate broadly stable.

On the subject of inflation, in that same speech, the Fed Chair added…

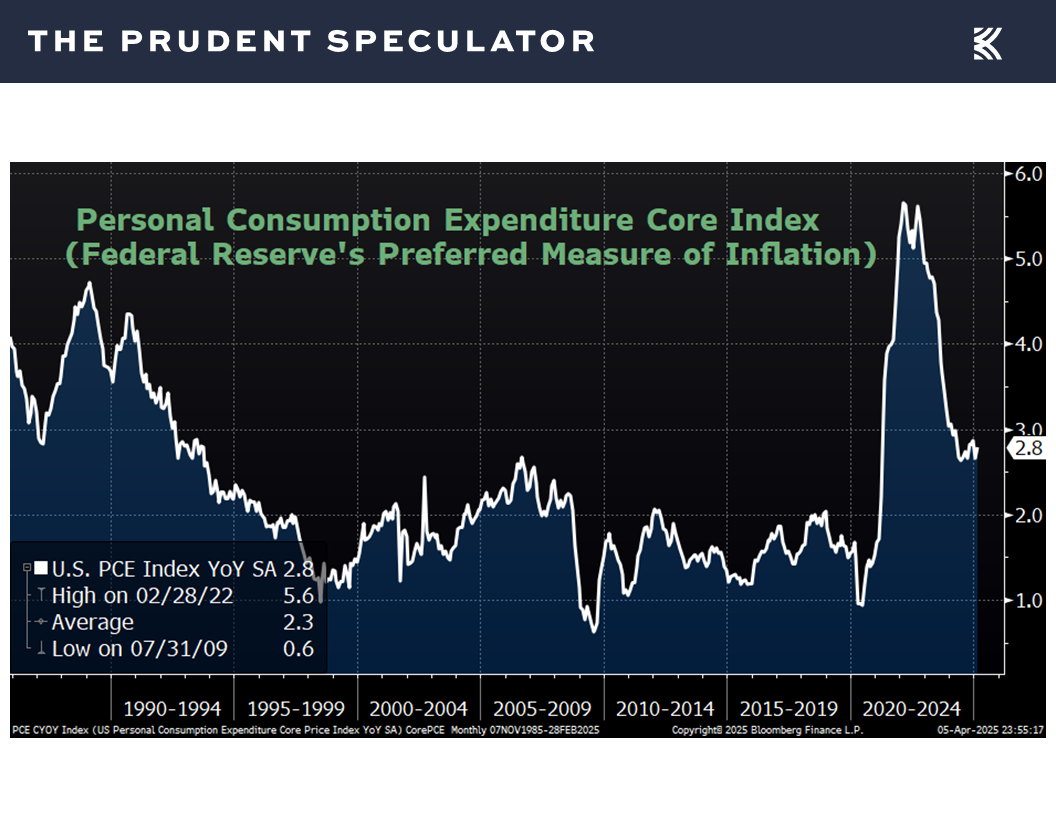

Turning to the other leg of our dual mandate, inflation has declined sharply from its pandemic highs of mid-2022. It has done so without the kind of painful rise in unemployment that has often accompanied periods of tight monetary policy that are needed to reduce inflation. More recently, progress toward our 2 percent inflation objective has slowed. Total PCE prices rose 2.5 percent over the 12 months ending in February. Core PCE prices, which exclude the volatile food and energy categories, rose 2.8 percent. Looking ahead, higher tariffs will be working their way through our economy and are likely to raise inflation in coming quarters. Reflecting this, both survey- and market-based measures of near-term inflation expectations have moved up. By most measures, longer-term inflation expectations—those beyond the next few years—remain well anchored and consistent with our 2 percent inflation goal. We remain committed to returning inflation sustainably to our 2 percent objective.

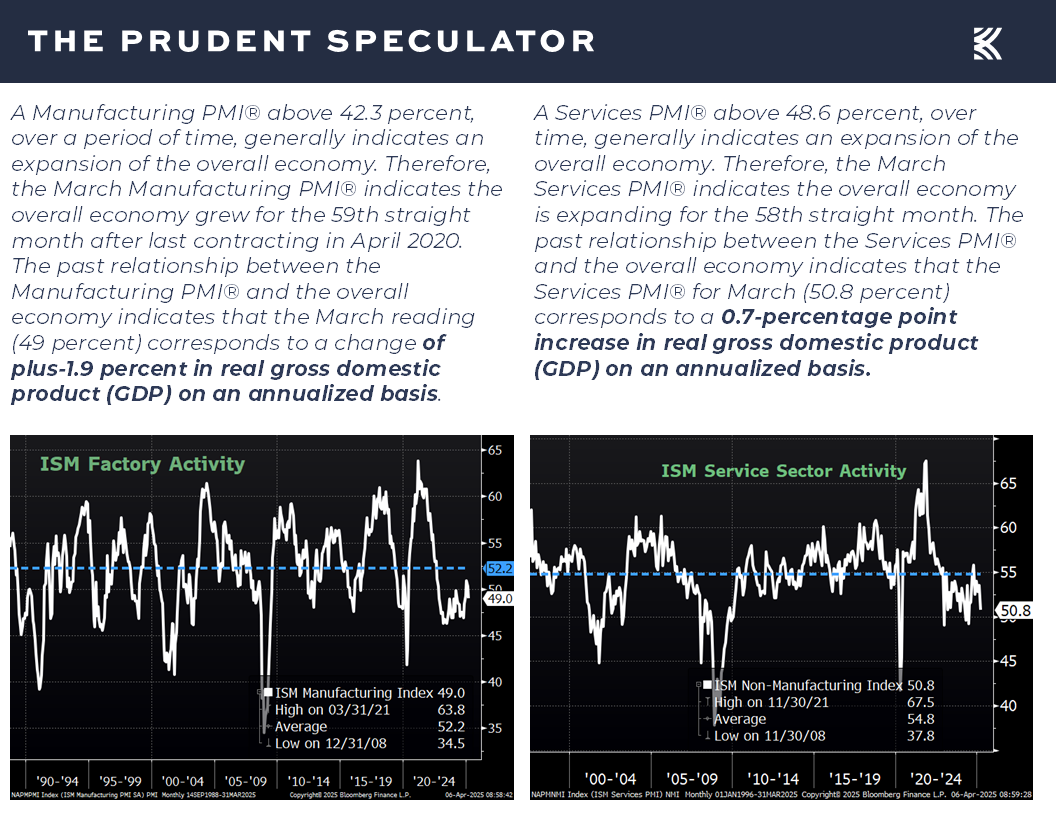

No doubt, there are significant questions about the labor market and inflation picture going forward, not to mention the health of the economy, as both the manufacturing and services indices for March from the Institute for Supply Management came in weaker than expected, though both still were suggesting that real (inflation-adjusted) GDP growth was in the cards,

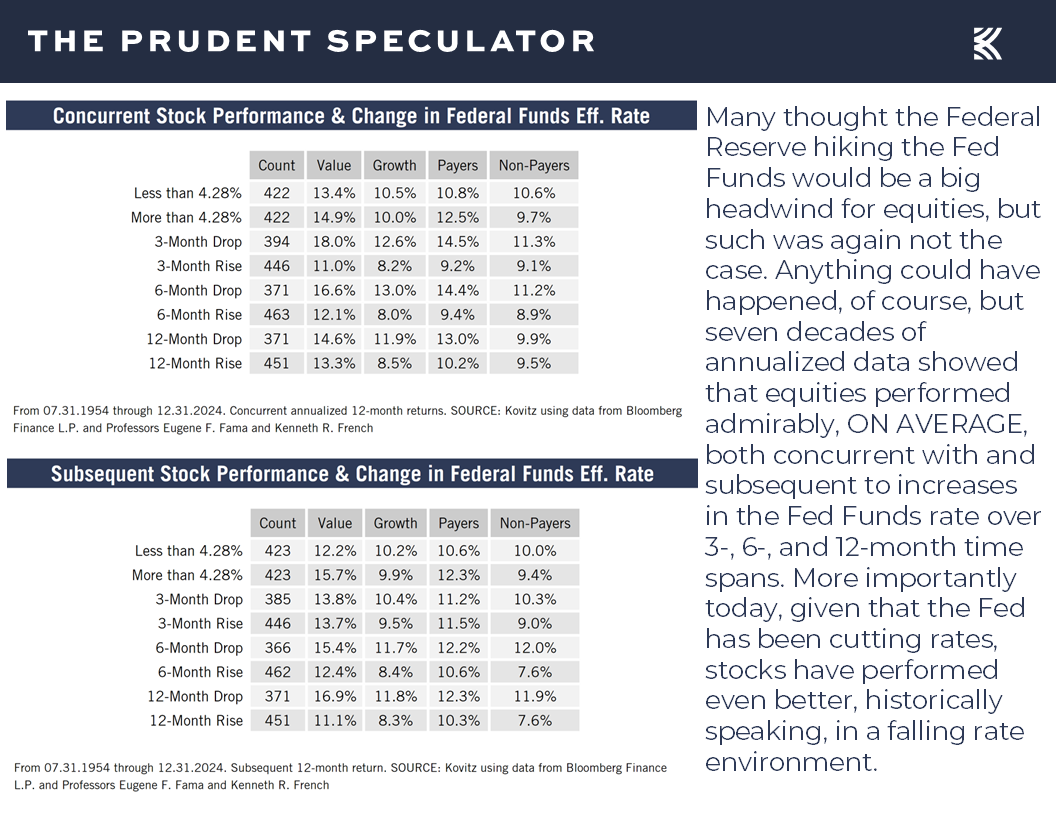

Interest Rates – Big Drop in the 10-Year Adds to Equity Attractiveness; Fed Expected to Cut Rates Several Times Before Year-End

and Mr. Powell concluded his Friday speech with the following…

We have stressed that it will be very difficult to assess the likely economic effects of higher tariffs until there is greater certainty about the details, such as what will be tariffed, at what level and for what duration, and the extent of retaliation from our trading partners. While uncertainty remains elevated, it is now becoming clear that the tariff increases will be significantly larger than expected. The same is likely to be true of the economic effects, which will include higher inflation and slower growth. The size and duration of these effects remain uncertain. While tariffs are highly likely to generate at least a temporary rise in inflation, it is also possible that the effects could be more persistent. Avoiding that outcome would depend on keeping longer-term inflation expectations well anchored, on the size of the effects, and on how long it takes for them to pass through fully to prices. Our obligation is to keep longer-term inflation expectations well anchored and to make certain that a one-time increase in the price level does not become an ongoing inflation problem.

We will continue to carefully monitor the incoming data, the evolving outlook, and the balance of risks. We are well positioned to wait for greater clarity before considering any adjustments to our policy stance. It is too soon to say what will be the appropriate path for monetary policy.

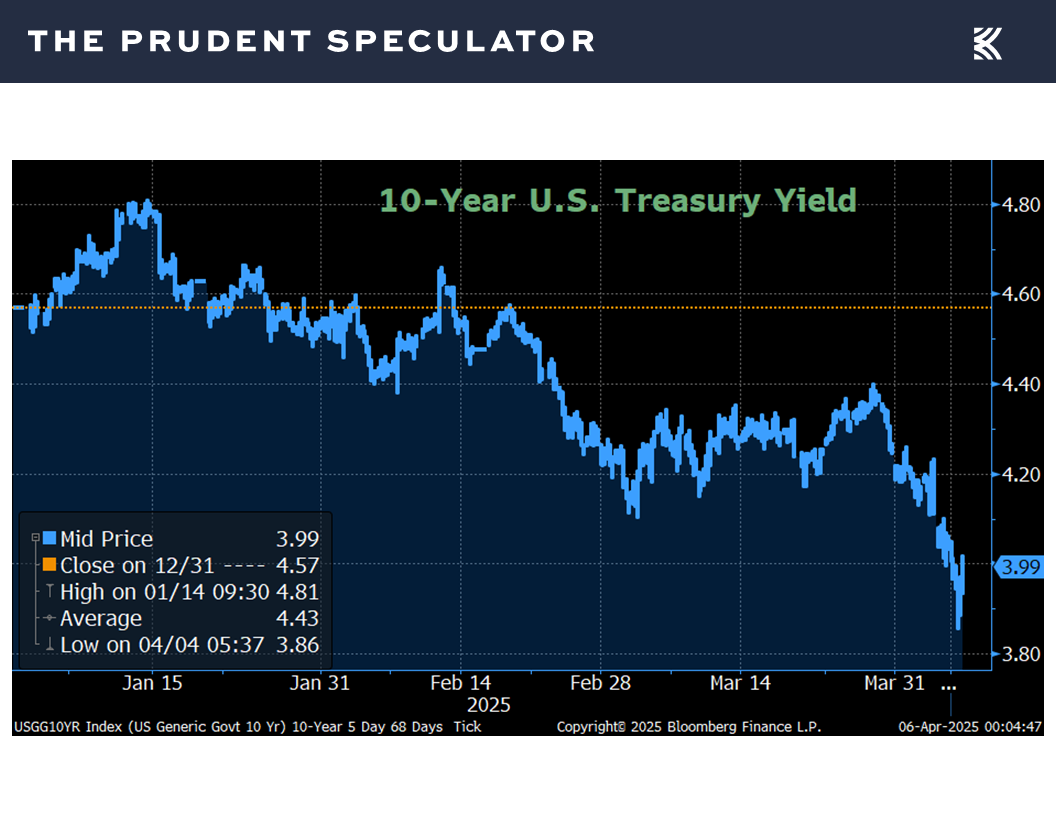

Traders were not overly thrilled with the patience Chair Powell showed, but the Fed has always been data dependent, and there is no way of knowing the impact of changing tariff policy on the economy. Still, interest rates fell sharply last week with the yield on the 10-Year U.S. Treasury dropping below 4.0%,

and lower yields on “safe” investments improving the attractiveness of equities on a valuation basis,

while the betting odds increased to four 25-basis-point Federal Reserve rate cuts before year-end as economists were busy raising their projections for the chance of recession.

History shows that a friendly Federal Reserve easing monetary policy has led to favorable equity returns, on average, both on a concurrent-with and subsequent-to basis.

Certainly, significant headwinds for consumer spending and corporate profits can lead to an economic contraction, though one can argue that the 2025 selloff has already discounted a significant portion of such an event. Further, the rebound in the 12 months from the end of prior recessions, on average, has not been something a long-term-oriented investor would have wanted to miss, with one-year gains for Value Stocks averaging a whopping 41%.

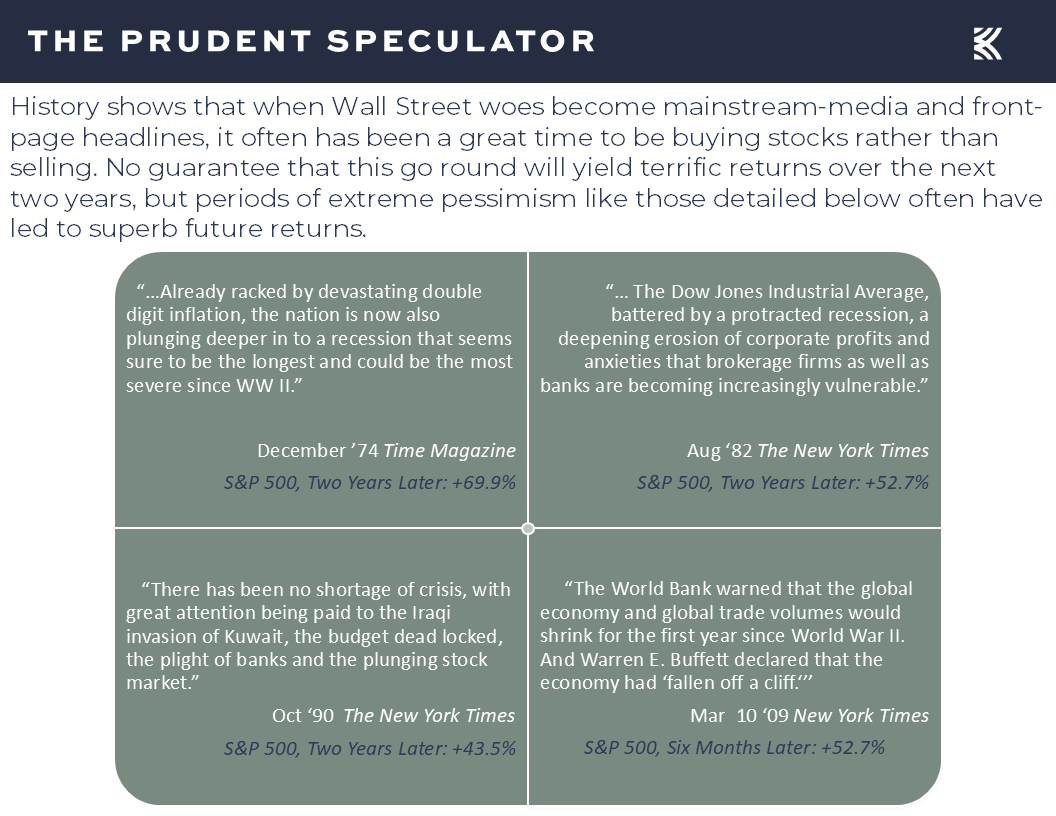

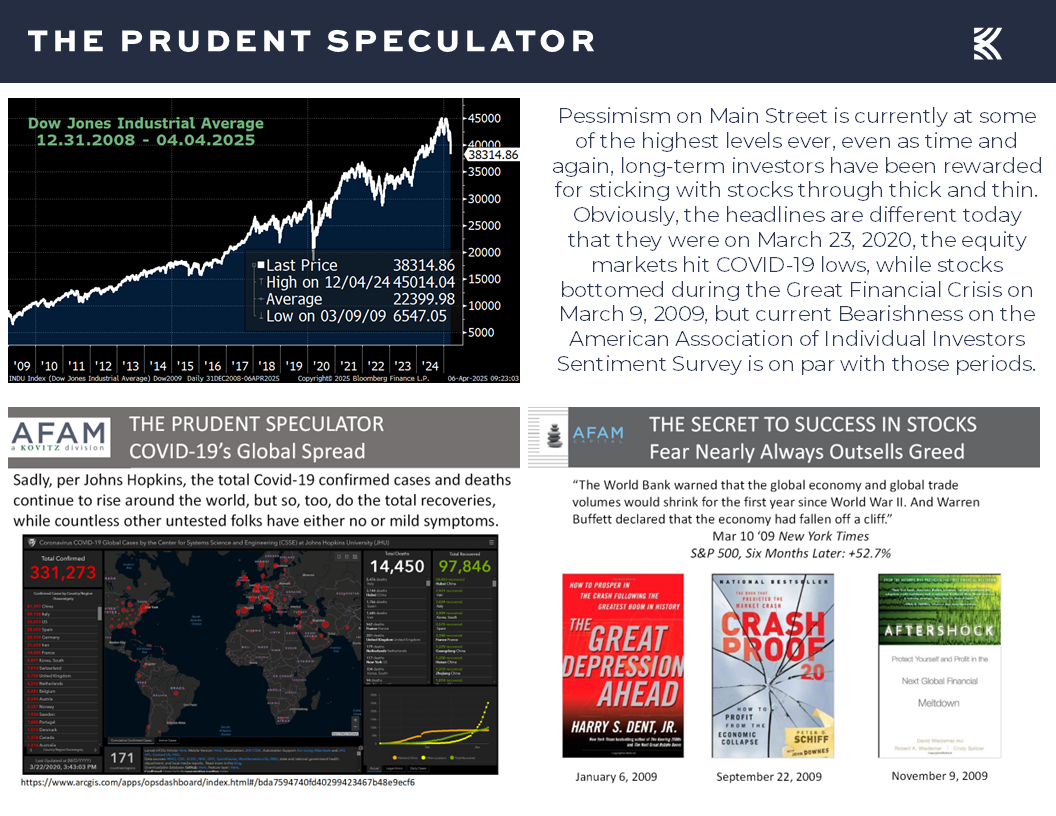

Sentiment – Headlines Super Negative at Market Bottoms; AAII and CNN Fear & Greed Index Flashing Contrarian Buy Signals

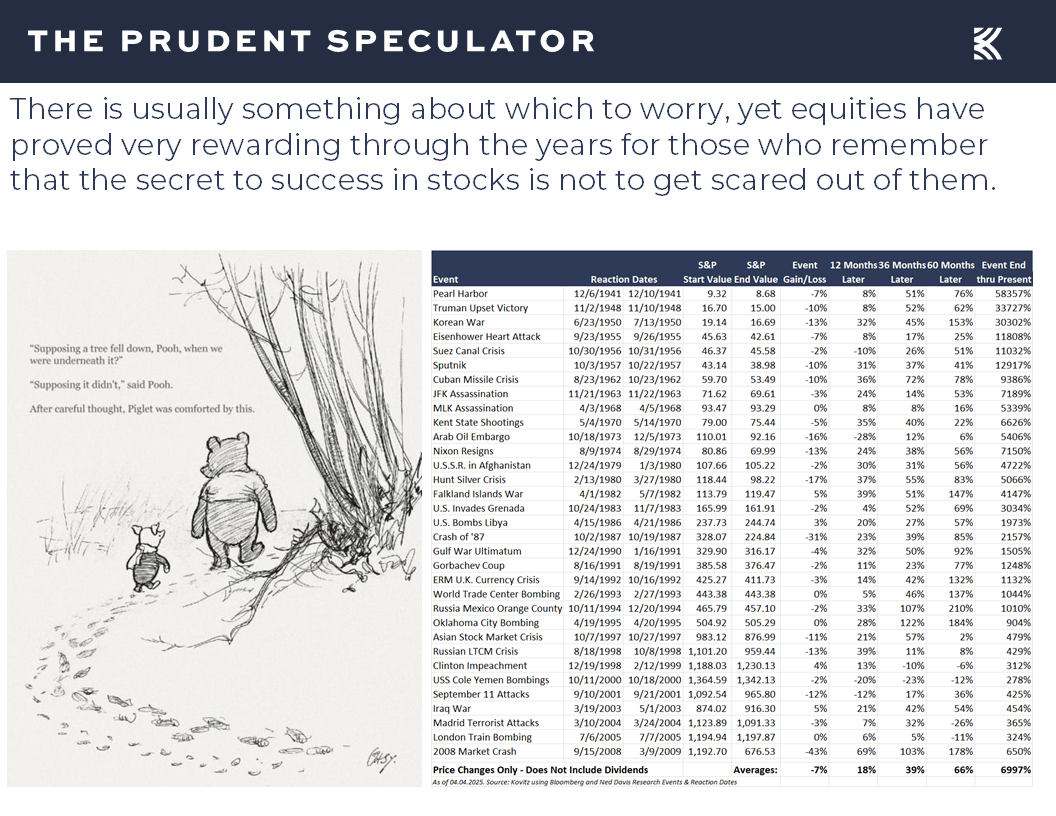

We understand that the near-term outlook is murky, but we have been through more than a few equity market wars in our time, and our advice has remained consistent. We must not lose sight of the fact that stocks historically have returned 9% to 13% per annum, that economic slowdowns and recessions ultimately give way to recoveries and expansions and that the markets have survived wars, impeachments, assassinations, depressions, accounting scandals, terrorist attacks and pandemics. As our founder Al Frank would say, this too shall pass, though not without some more scary moments.

It is hard to envision that the days and weeks ahead won’t be rocky, so we are braced for more than usual volatility, but we offer the observation that if we went back in time to choose some of the best moments in history in which to invest, they would look a lot like what we are seeing today in terms of sensational headlines,

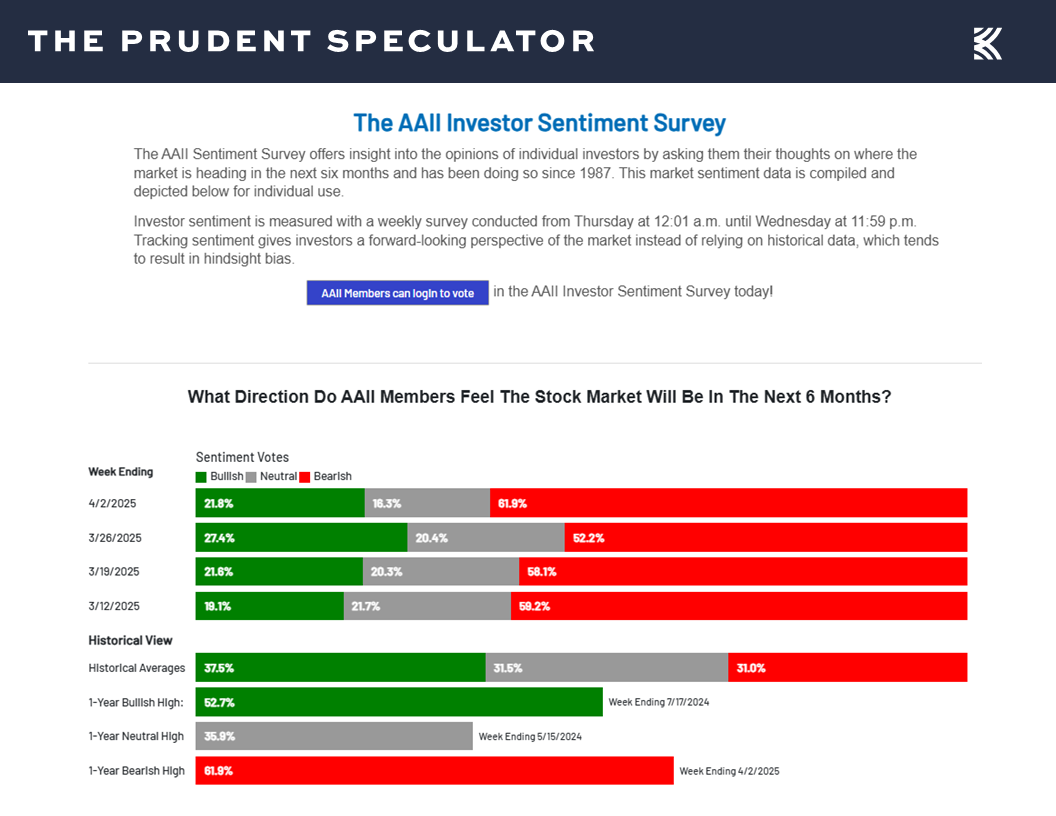

and pessimistic investor sentiment. On that score, the CNN Fear and Greed Index of seven factors now stands at a reading of 4, which is uber-pessimistic and in the Extreme Fear zone, given the range of scores from 0 to 100. As Warren Buffett states, “We should be greedy when others are fearful, and fearful when others are greedy,” so our contrarian nature also can’t help but be excited by the latest weekly sentiment survey from the American Association of Individual Investors.

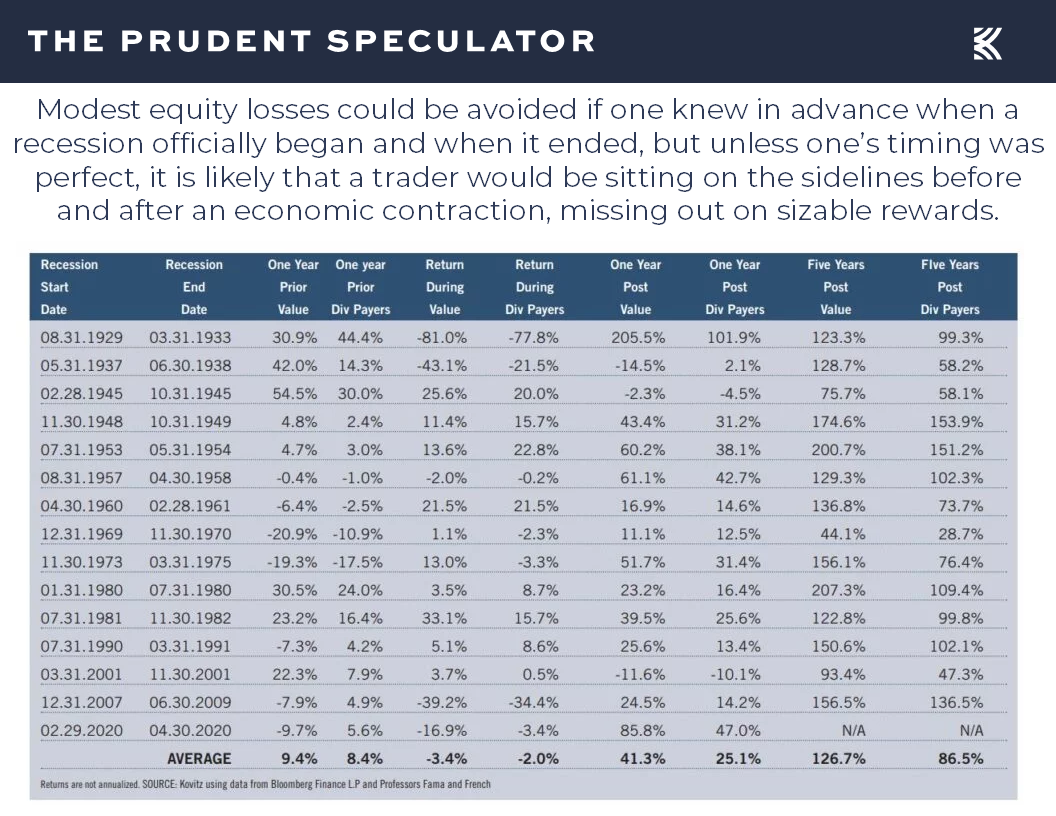

Recessions – Risk Has Spiked, But History Shows Staying the Course the Right Move Even if a Contraction Were to Occur

Since 1987, there have been only two other weekly tallies that were more Bearish. The first of these was on October 18, 1990, during the first Gulf War, and the second was March 5, 2009, four days before stocks bottomed during the Great Financial Crisis. There are never any guarantees that history repeats, but the six-month forward returns for the broad-based Russell 3000 Index were 32.1% and 52.7%, respectively.

Incredibly, folks seem more scared today than they were during the Great Financial Crisis, not to mention the COVID-19 pandemic,

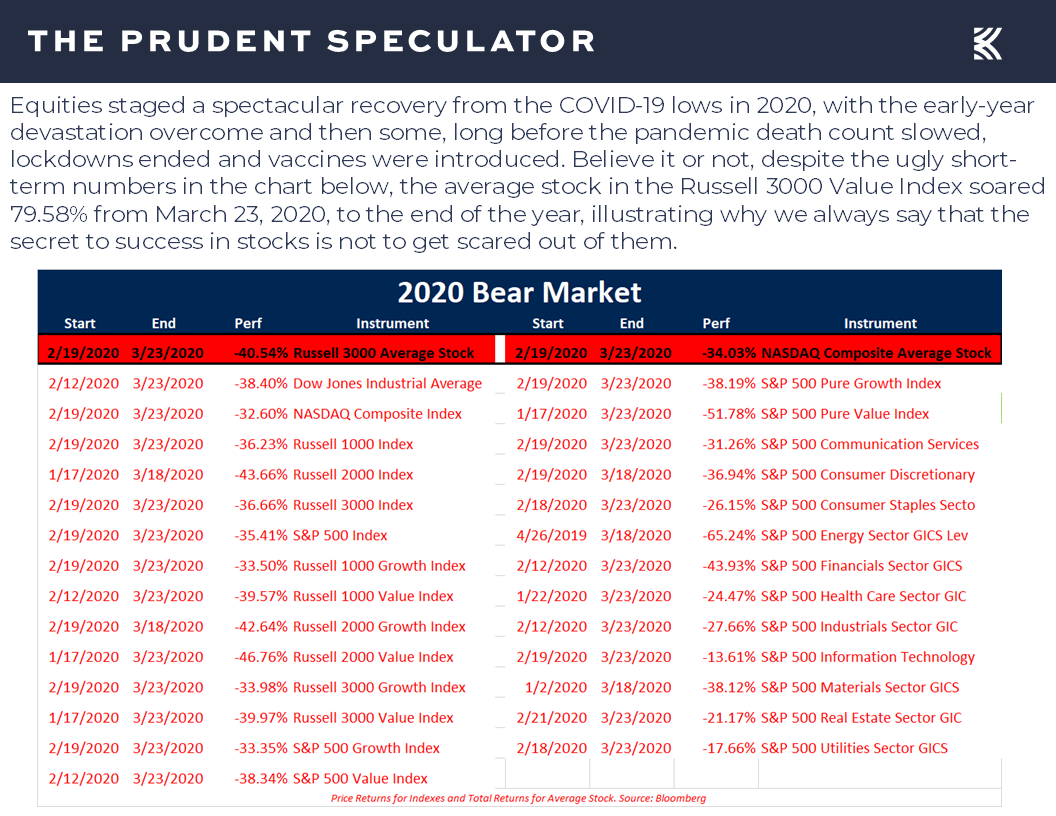

2020 – Far Worse COVID-19 Massacre for Stocks; But the Year Ended Higher than it Began

which was the last time stocks endured daily moves to the downside like we saw on Thursday and Friday. Let’s hope the short-term paper losses don’t approach those in 2020 that are detailed in the chart below,

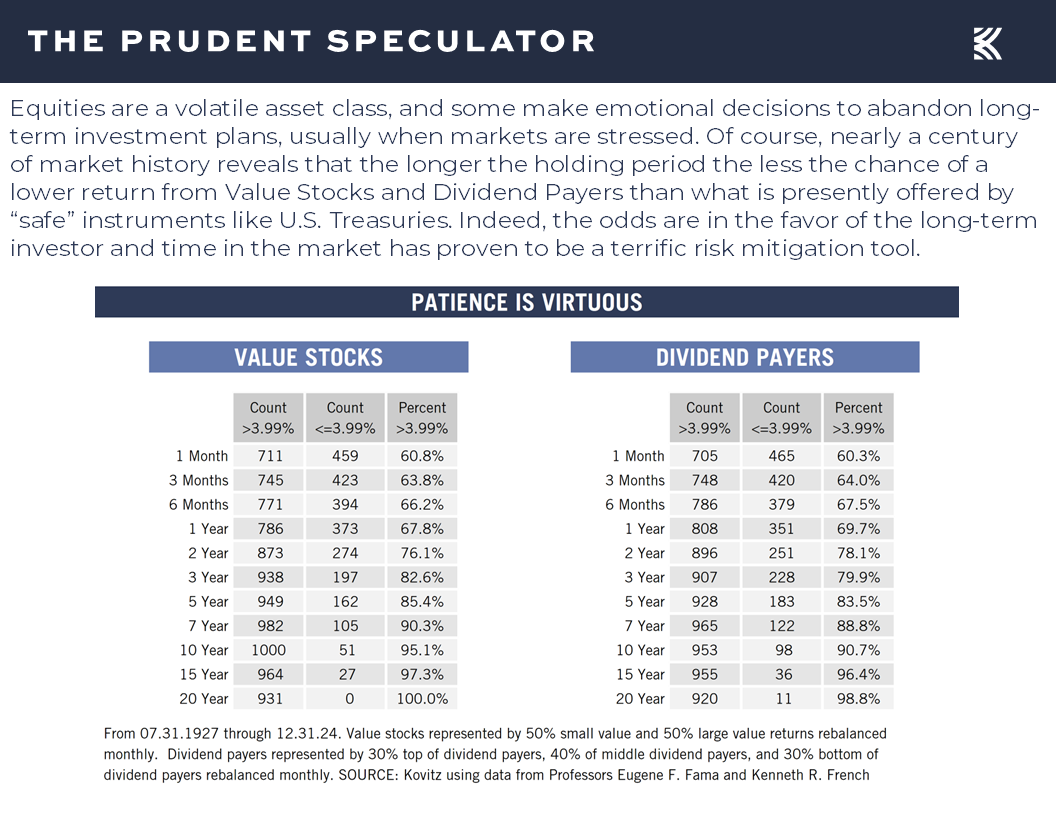

Patience – The Longer the Hold the Better the Chance of Success

but those who kept the faith five years ago were rewarded with a full recovery by the end of that tumultuous year, offering a reminder that patience can be a strong risk mitigation tool.

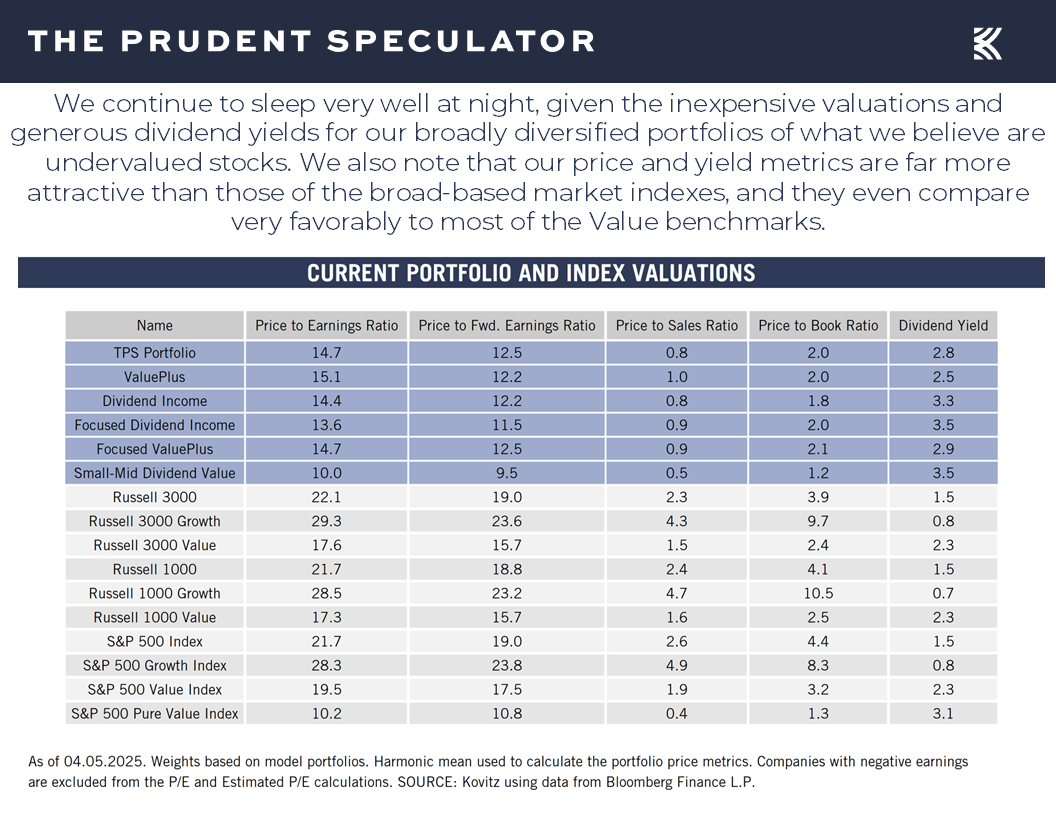

Valuations – Liking the Metrics on our Portfolios

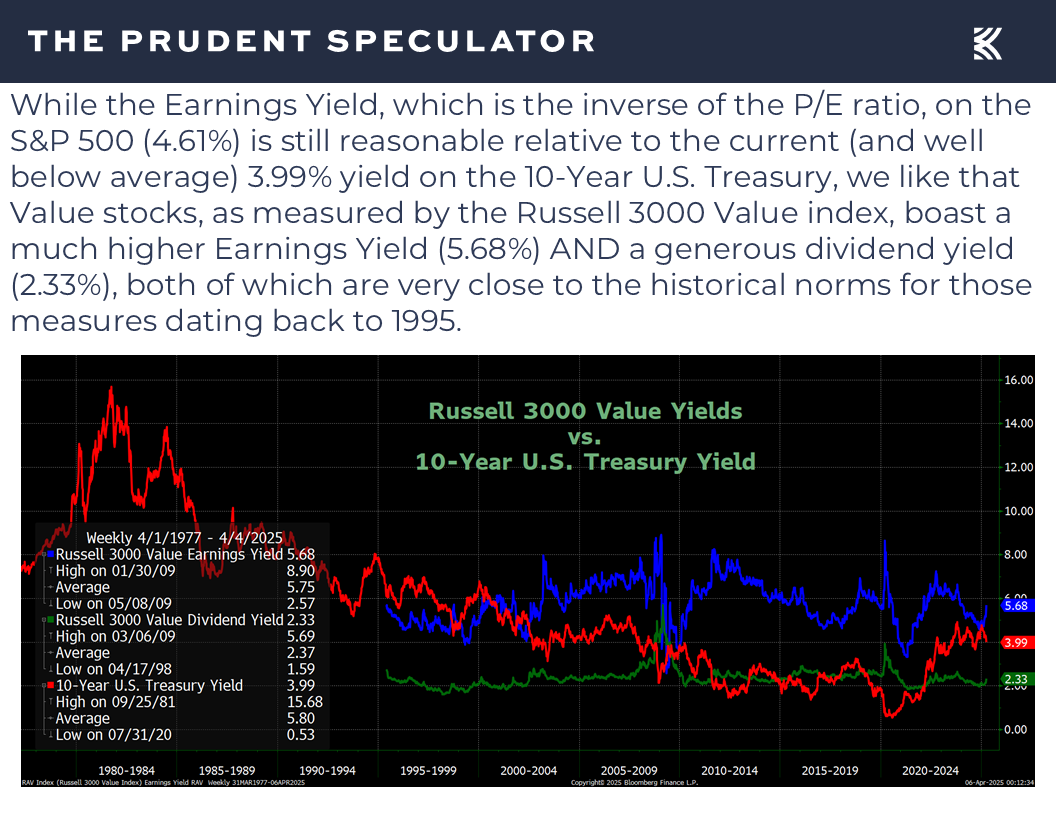

Come what may, we remain comfortable with the inexpensive valuation metrics and generous dividend yields on our broadly diversified portfolios of what we believe are undervalued stocks.

Yes, the earnings outlook is highly suspect,

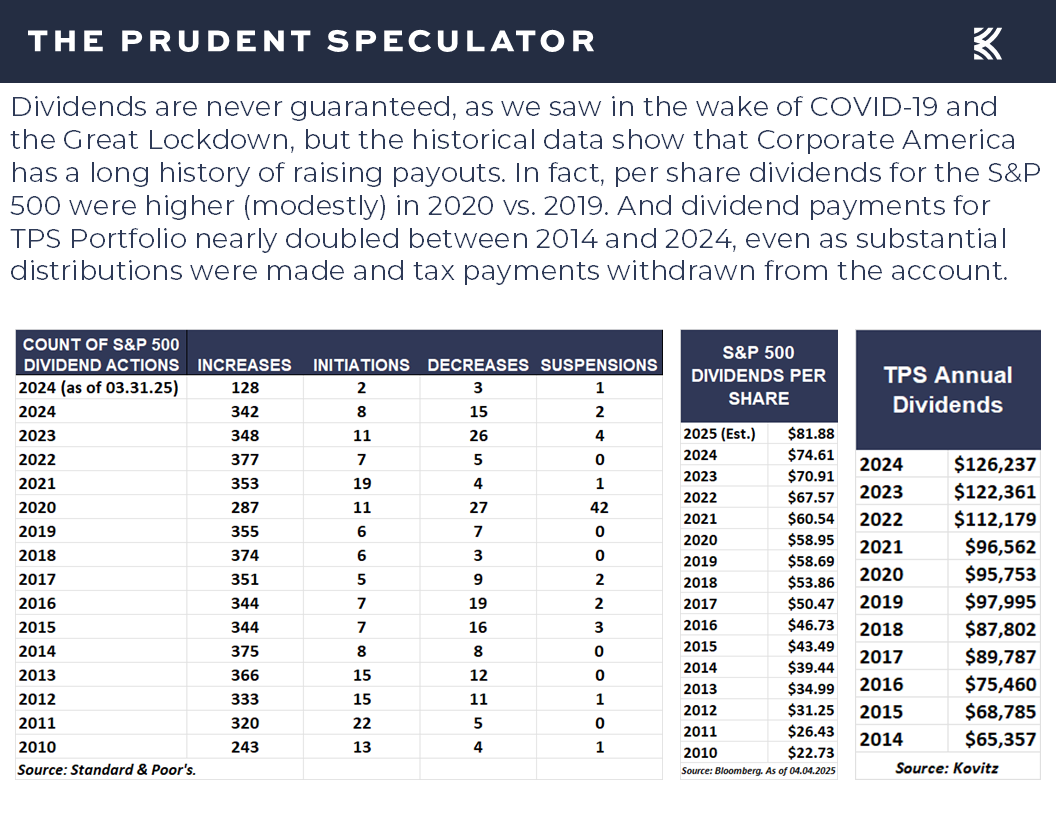

Dividends – Focusing on Income Received vs. Stock-Price Gyrations Can Provide Better Slumber

but we encourage those trying to keep their emotions in check while the stocks they own gyrate wildly in price to focus instead on the growing dividend stream provided by their portfolios. After all, those who own rental properties usually care about the income they are receiving and don’t have a great need to worry if a comparable building in their vicinity sold at a higher or lower price…if they have no intention of selling.

Stock News – Updates on Two-Dozen Hard-Hit Liberation Day Stocks

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Liberation Day, Volatility, Interest Rates, Recessions and Patience

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Liberation Day, Volatility, Interesting Rates and Recessions. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – 9 Buys Across 4 Portfolios

Buckingham AAII Appearance – San Diego, April 12, 2025, at 9:00 A.M Pacific

Liberation Day – More Severe-than-Expected Tariffs Sends Stocks Plunging

Volatility – Corrections…and Even Bear Markets…are Part of the Investment Process

Econ News – Solid Jobs Numbers; Even Relatively Weak ISM Numbers Have Correlated in the Past to Real GDP Growth

Powell – Fed Chair Waiting for Greater Clarity Before Making Adjustments to Monetary Policy

Interest Rates – Big Drop in the 10-Year Adds to Equity Attractiveness; Fed Expected to Cut Rates Several Times Before Year-End

Sentiment – Headlines Super Negative at Market Bottoms; AAII and CNN Fear & Greed Index Flashing Contrarian Buy Signals

Recessions – Risk Has Spiked, But History Shows Staying the Course the Right Move Even if a Contraction Were to Occur

2020 – Far Worse COVID-19 Massacre for Stocks; But the Year Ended Higher than it Began

Patience – The Longer the Hold the Better the Chance of Success

Valuations – Liking the Metrics on our Portfolios

Dividends – Focusing on Income Received vs. Stock-Price Gyrations Can Provide Better Slumber

Stock News – Two-Dozen Hard-Hit Liberation Day Stocks

Buckingham AAII Appearance – San Diego, April 12, 2025, at 9:00 A.M Pacific

Your Editor will be speaking in San Diego on Saturday, April 12, 2025, at 9:00 AM Pacific. Registration info for that presentation is available here:

Upcoming Chapter Events – AAII San Diego

Note, too, that the AAII folks are making the presentation available via Zoom.

Liberation Day – More Severe-than-Expected Tariffs Sends Stocks Plunging

RH (Restoration Hardware) CEO Gary Friedman exclaimed, “Oh, sh—, OK. OK. I just looked at the screen. I had to look at it. It got hit when I think the tariff came out,” on the quarterly earnings call seeing the after-hours plunge in the furniture retailer’s stock on Wednesday afternoon. No doubt, most investors uttered the same expletive in reaction to last week’s carnage in the equity markets, with stocks enduring back-to-back massive selloffs on Thursday and Friday.

Obviously, the catalyst for the bloodbath was the “Liberation Day” ceremony in the Rose Garden, as the White House announced 10% across-the-board tariffs on all imports (which became effective April 5) and reciprocal higher tariffs on counties with which the U.S. has the largest trade deficits (which go into effect April 9). While President Trump proclaimed, “Jobs and factories will come roaring back into the country,” the tariffs were far more drastic than expected and China quickly retaliated with reciprocal tariffs of its own on U.S. goods.

Volatility – Corrections…and Even Bear Markets…are Part of the Investment Process

Most think the tariffs are a salvo in Trump’s Art of the Deal, and Vietnam (which manufactures a major portion of apparel for U.S. companies) evidently was on the phone with the President on Friday to supposedly try to cut a deal to lower its tariffs to zero, while the White House said on Sunday that over 50 countries have contacted the U.S. in a bid to negotiate the tariffs. Still, the markets thus far have decided to shoot first and ask questions later, with stocks of virtually all stripes taken out to the proverbial woodshed.

When all was said and done, the market averages endured one of their worst weeks in history, with the S&P 500’s tumble of more than 9% the biggest weekly setback since 2020,

extending the 2025 pullback from recent all-time highs to mid-teen-to 20%+ percentage levels.

Certainly, the speed of the drop is disconcerting, and nerves are on edge, so we encourage those who share our long-term time horizon to channel Vannevar Bush. The American engineer and investor said, “Fear cannot be banished, but it can be calm and without panic; it can be mitigated by reason and evaluation.”

As painful as last week was, downturns are a very normal part of the investment process, some worse than others happening every year,

while the magnitude of this correction (the 39th setback of 10% or more without an intervening rally of at least 10% that has been endured since we launched The Prudent Speculator in 1977) is about average by historical standards.

True, we are not that far away from an official Bear Market for the S&P 500, but that popular index has suffered drops of 20% or more every 3.4 years on average, yet equities, led by Value Stocks have still enjoyed sensational long-term returns,

eventually overcoming all prior frightening events in the fullness of time,

Without question, this time (and every time) is different, even as tariffs have long been part of the landscape,

Econ News – Solid Jobs Numbers; Even Relatively Weak ISM Numbers Have Correlated in the Past to Real GDP Growth

but the U.S. economy ended March with better-than-average and better-than-estimated net-new-job creation as 228,000 payrolls were created in the month,

and the unemployment rate at 4.2% was well below the historical average,

Powell – Fed Chair Waiting for Greater Clarity Before Making Adjustments to Monetary Policy

with Jerome H. Powell stating on Friday, April 4…

Looking across many indicators, the labor market appears to be broadly in balance and is not a significant source of inflationary pressure. This morning’s jobs report shows the unemployment rate at 4.2 percent in March, still in the low range where it has held since early last year. Over the first quarter, payrolls grew by an average of 150,000 jobs a month. The combination of low layoffs, moderating job growth, and slowing labor force growth has kept the unemployment rate broadly stable.

On the subject of inflation, in that same speech, the Fed Chair added…

Turning to the other leg of our dual mandate, inflation has declined sharply from its pandemic highs of mid-2022. It has done so without the kind of painful rise in unemployment that has often accompanied periods of tight monetary policy that are needed to reduce inflation. More recently, progress toward our 2 percent inflation objective has slowed. Total PCE prices rose 2.5 percent over the 12 months ending in February. Core PCE prices, which exclude the volatile food and energy categories, rose 2.8 percent. Looking ahead, higher tariffs will be working their way through our economy and are likely to raise inflation in coming quarters. Reflecting this, both survey- and market-based measures of near-term inflation expectations have moved up. By most measures, longer-term inflation expectations—those beyond the next few years—remain well anchored and consistent with our 2 percent inflation goal. We remain committed to returning inflation sustainably to our 2 percent objective.

No doubt, there are significant questions about the labor market and inflation picture going forward, not to mention the health of the economy, as both the manufacturing and services indices for March from the Institute for Supply Management came in weaker than expected, though both still were suggesting that real (inflation-adjusted) GDP growth was in the cards,

Interest Rates – Big Drop in the 10-Year Adds to Equity Attractiveness; Fed Expected to Cut Rates Several Times Before Year-End

and Mr. Powell concluded his Friday speech with the following…

We have stressed that it will be very difficult to assess the likely economic effects of higher tariffs until there is greater certainty about the details, such as what will be tariffed, at what level and for what duration, and the extent of retaliation from our trading partners. While uncertainty remains elevated, it is now becoming clear that the tariff increases will be significantly larger than expected. The same is likely to be true of the economic effects, which will include higher inflation and slower growth. The size and duration of these effects remain uncertain. While tariffs are highly likely to generate at least a temporary rise in inflation, it is also possible that the effects could be more persistent. Avoiding that outcome would depend on keeping longer-term inflation expectations well anchored, on the size of the effects, and on how long it takes for them to pass through fully to prices. Our obligation is to keep longer-term inflation expectations well anchored and to make certain that a one-time increase in the price level does not become an ongoing inflation problem.

We will continue to carefully monitor the incoming data, the evolving outlook, and the balance of risks. We are well positioned to wait for greater clarity before considering any adjustments to our policy stance. It is too soon to say what will be the appropriate path for monetary policy.

Traders were not overly thrilled with the patience Chair Powell showed, but the Fed has always been data dependent, and there is no way of knowing the impact of changing tariff policy on the economy. Still, interest rates fell sharply last week with the yield on the 10-Year U.S. Treasury dropping below 4.0%,

and lower yields on “safe” investments improving the attractiveness of equities on a valuation basis,

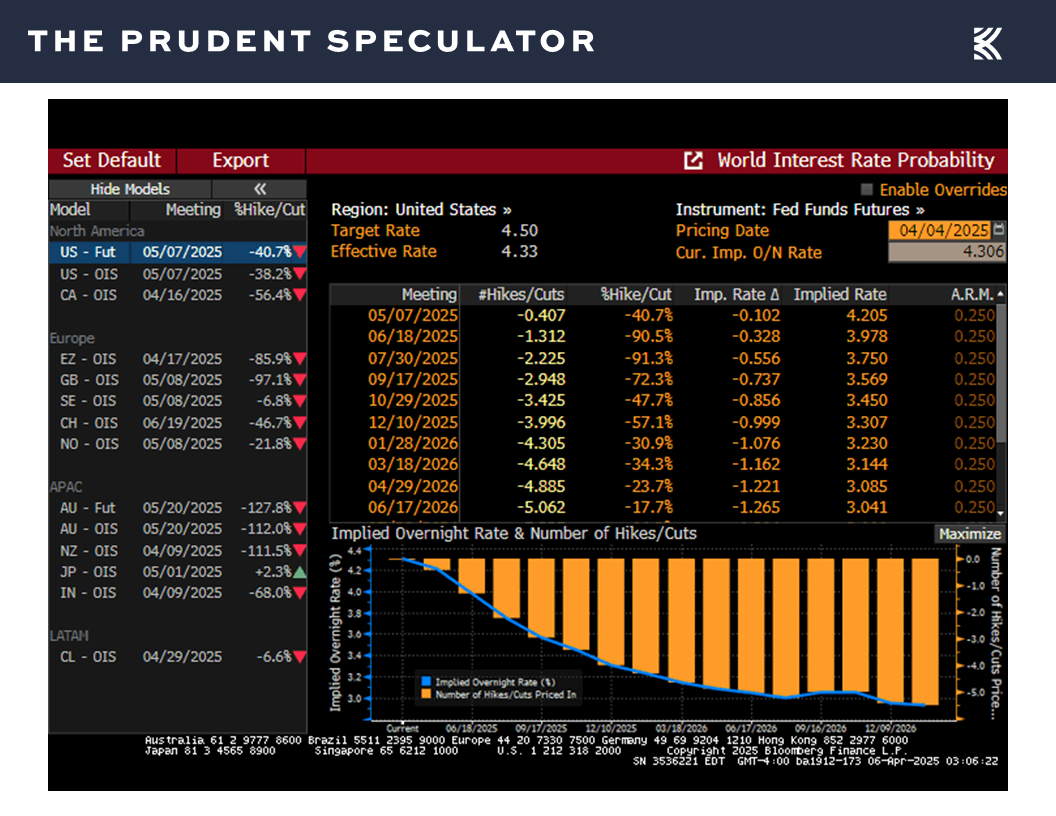

while the betting odds increased to four 25-basis-point Federal Reserve rate cuts before year-end as economists were busy raising their projections for the chance of recession.

History shows that a friendly Federal Reserve easing monetary policy has led to favorable equity returns, on average, both on a concurrent-with and subsequent-to basis.

Certainly, significant headwinds for consumer spending and corporate profits can lead to an economic contraction, though one can argue that the 2025 selloff has already discounted a significant portion of such an event. Further, the rebound in the 12 months from the end of prior recessions, on average, has not been something a long-term-oriented investor would have wanted to miss, with one-year gains for Value Stocks averaging a whopping 41%.

Sentiment – Headlines Super Negative at Market Bottoms; AAII and CNN Fear & Greed Index Flashing Contrarian Buy Signals

We understand that the near-term outlook is murky, but we have been through more than a few equity market wars in our time, and our advice has remained consistent. We must not lose sight of the fact that stocks historically have returned 9% to 13% per annum, that economic slowdowns and recessions ultimately give way to recoveries and expansions and that the markets have survived wars, impeachments, assassinations, depressions, accounting scandals, terrorist attacks and pandemics. As our founder Al Frank would say, this too shall pass, though not without some more scary moments.

It is hard to envision that the days and weeks ahead won’t be rocky, so we are braced for more than usual volatility, but we offer the observation that if we went back in time to choose some of the best moments in history in which to invest, they would look a lot like what we are seeing today in terms of sensational headlines,

and pessimistic investor sentiment. On that score, the CNN Fear and Greed Index of seven factors now stands at a reading of 4, which is uber-pessimistic and in the Extreme Fear zone, given the range of scores from 0 to 100. As Warren Buffett states, “We should be greedy when others are fearful, and fearful when others are greedy,” so our contrarian nature also can’t help but be excited by the latest weekly sentiment survey from the American Association of Individual Investors.

Recessions – Risk Has Spiked, But History Shows Staying the Course the Right Move Even if a Contraction Were to Occur

Since 1987, there have been only two other weekly tallies that were more Bearish. The first of these was on October 18, 1990, during the first Gulf War, and the second was March 5, 2009, four days before stocks bottomed during the Great Financial Crisis. There are never any guarantees that history repeats, but the six-month forward returns for the broad-based Russell 3000 Index were 32.1% and 52.7%, respectively.

Incredibly, folks seem more scared today than they were during the Great Financial Crisis, not to mention the COVID-19 pandemic,

2020 – Far Worse COVID-19 Massacre for Stocks; But the Year Ended Higher than it Began

which was the last time stocks endured daily moves to the downside like we saw on Thursday and Friday. Let’s hope the short-term paper losses don’t approach those in 2020 that are detailed in the chart below,

Patience – The Longer the Hold the Better the Chance of Success

but those who kept the faith five years ago were rewarded with a full recovery by the end of that tumultuous year, offering a reminder that patience can be a strong risk mitigation tool.

Valuations – Liking the Metrics on our Portfolios

Come what may, we remain comfortable with the inexpensive valuation metrics and generous dividend yields on our broadly diversified portfolios of what we believe are undervalued stocks.

Yes, the earnings outlook is highly suspect,

Dividends – Focusing on Income Received vs. Stock-Price Gyrations Can Provide Better Slumber

but we encourage those trying to keep their emotions in check while the stocks they own gyrate wildly in price to focus instead on the growing dividend stream provided by their portfolios. After all, those who own rental properties usually care about the income they are receiving and don’t have a great need to worry if a comparable building in their vicinity sold at a higher or lower price…if they have no intention of selling.

Stock News – Updates on Two-Dozen Hard-Hit Liberation Day Stocks

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.