The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the market of stocks, econ stats, inflation and more stock news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Market of Stocks – Nice Week, But Average Stock Still Down on the Year

Volatility – The Longer the Measuring Stick, the Less Risky Equities Become

Econ Stats – A Slew of Weaker-than-Expected Numbers and a Few Good Ones

Econ Outlook – Real GDP Growth in ’24 Still Likely; EPS Estimates on the Rise

Inflation – PCE Arrives as Expected; Rates Fall

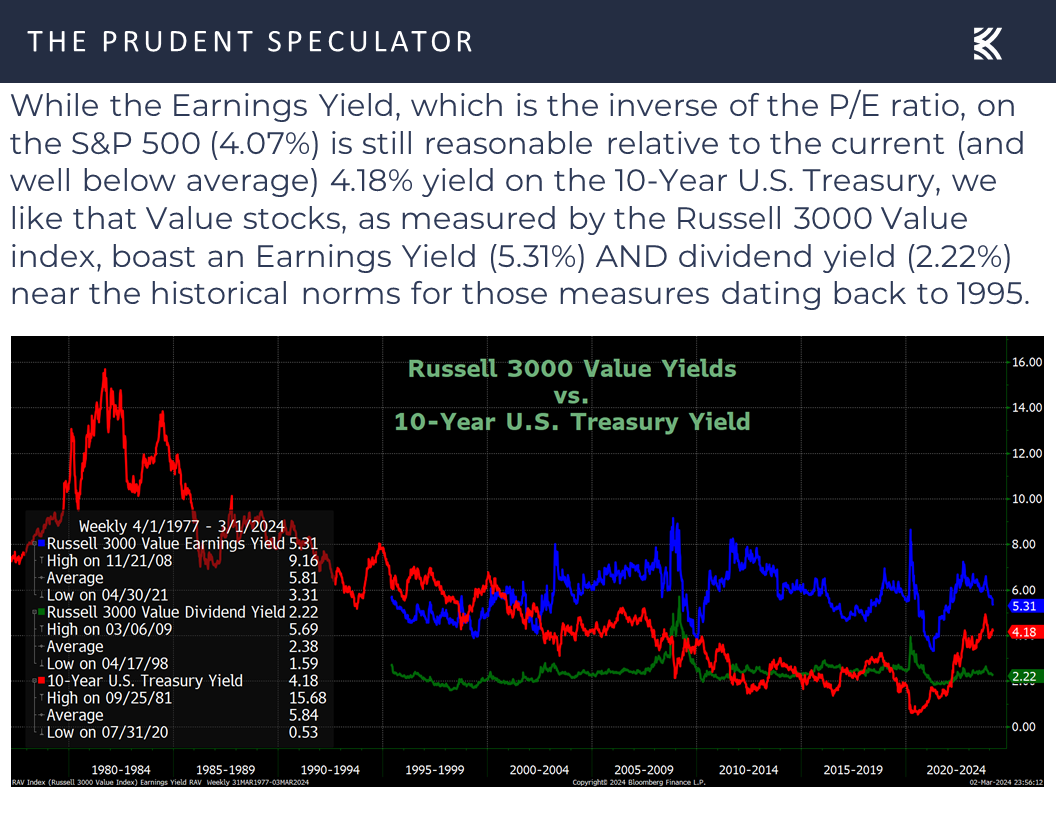

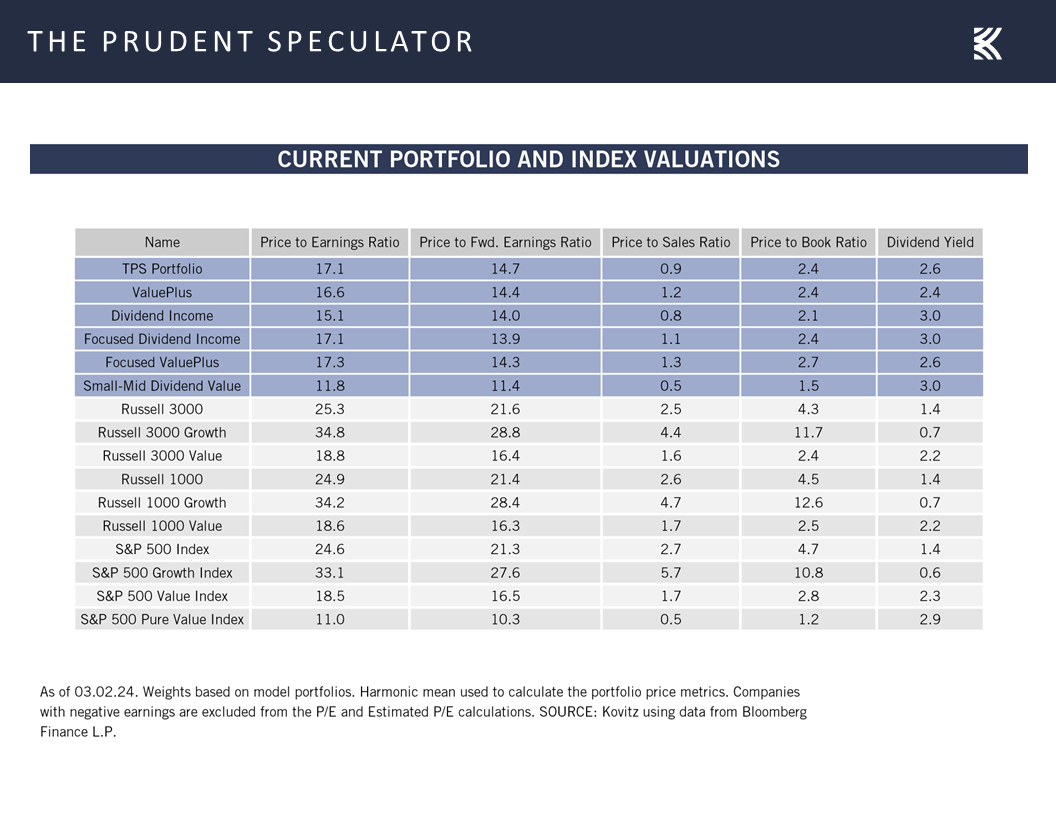

Valuations – Value Stocks Attractively Priced

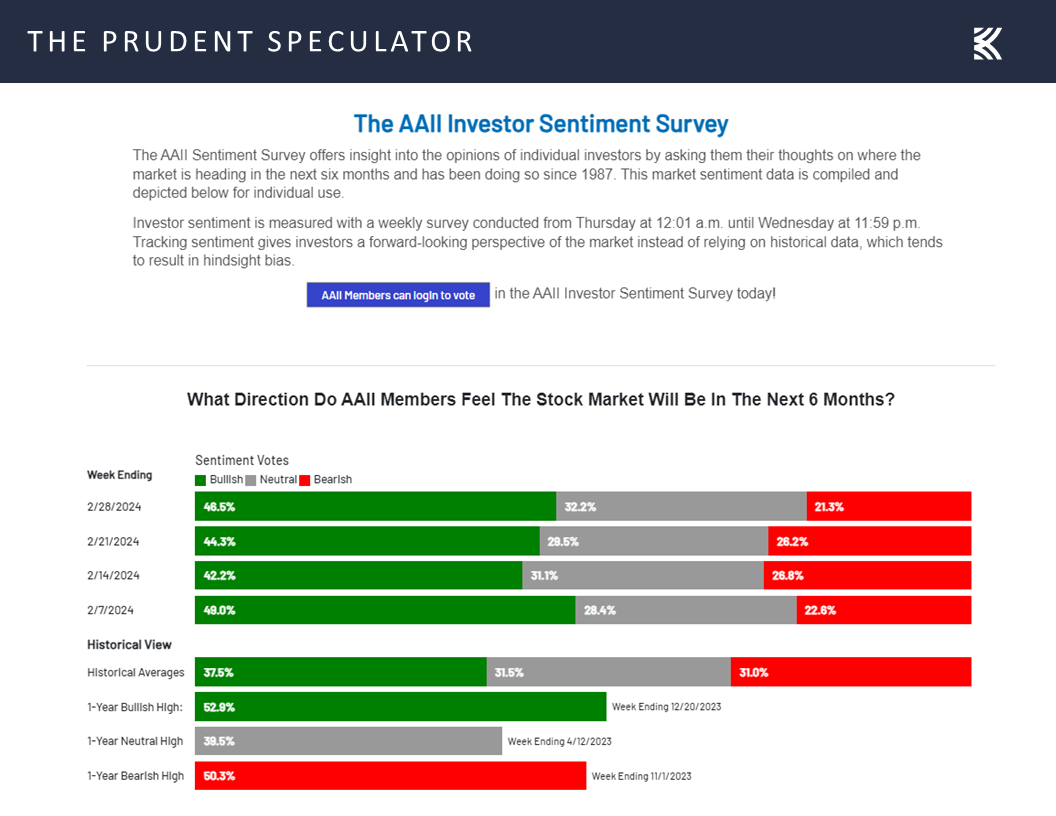

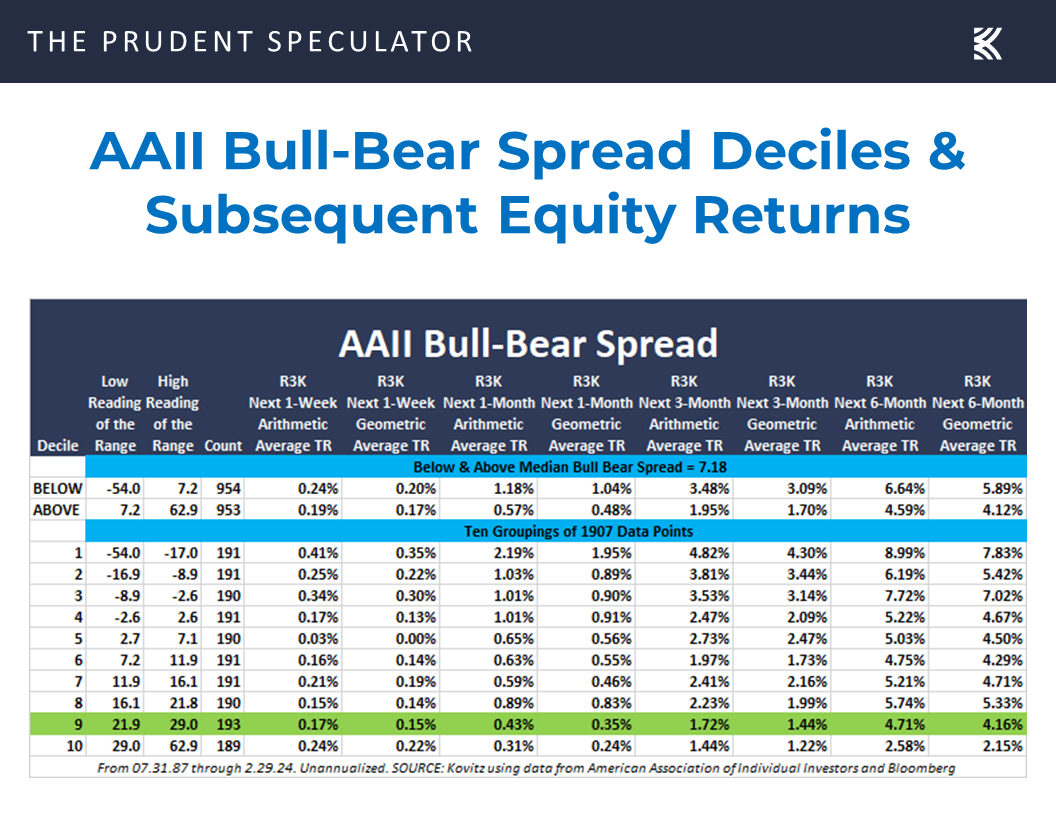

Sentiment – AAII Still Optimistic

Stock News – Updates on five stocks across five different sectors

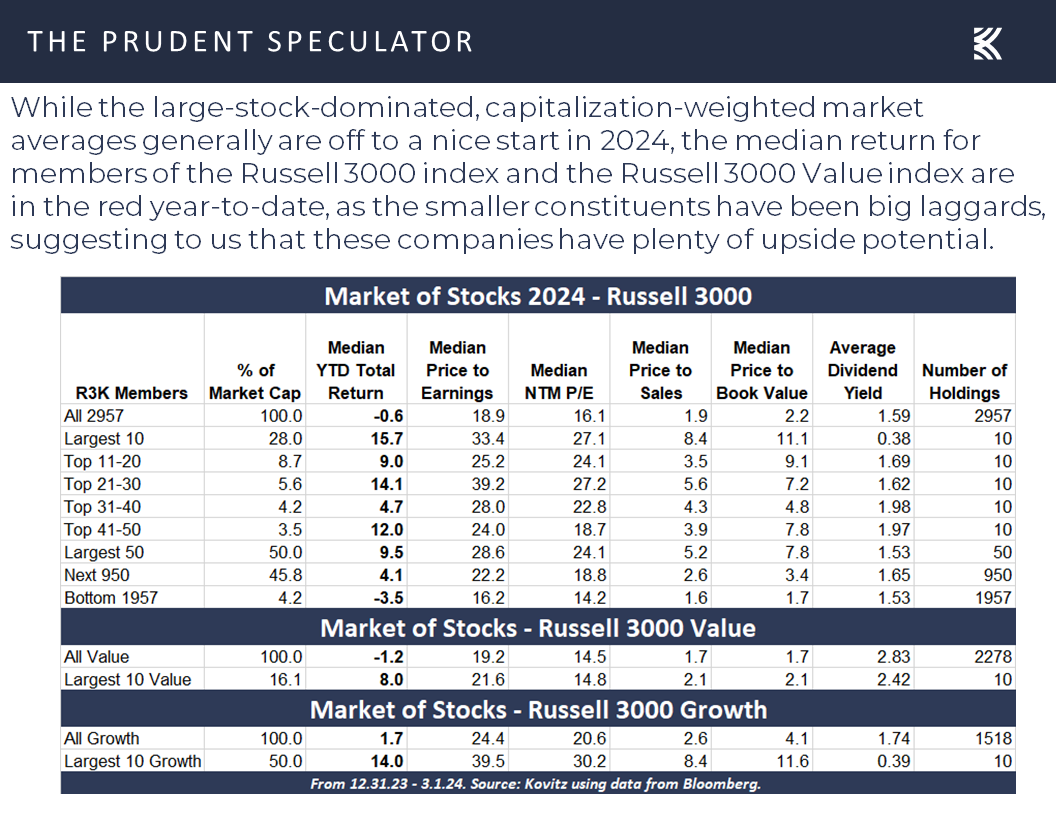

Market of Stocks – Nice Week, But Average Stock Still Down on the Year

While the median return for stocks in the Russell 3000 is still negative for the year,

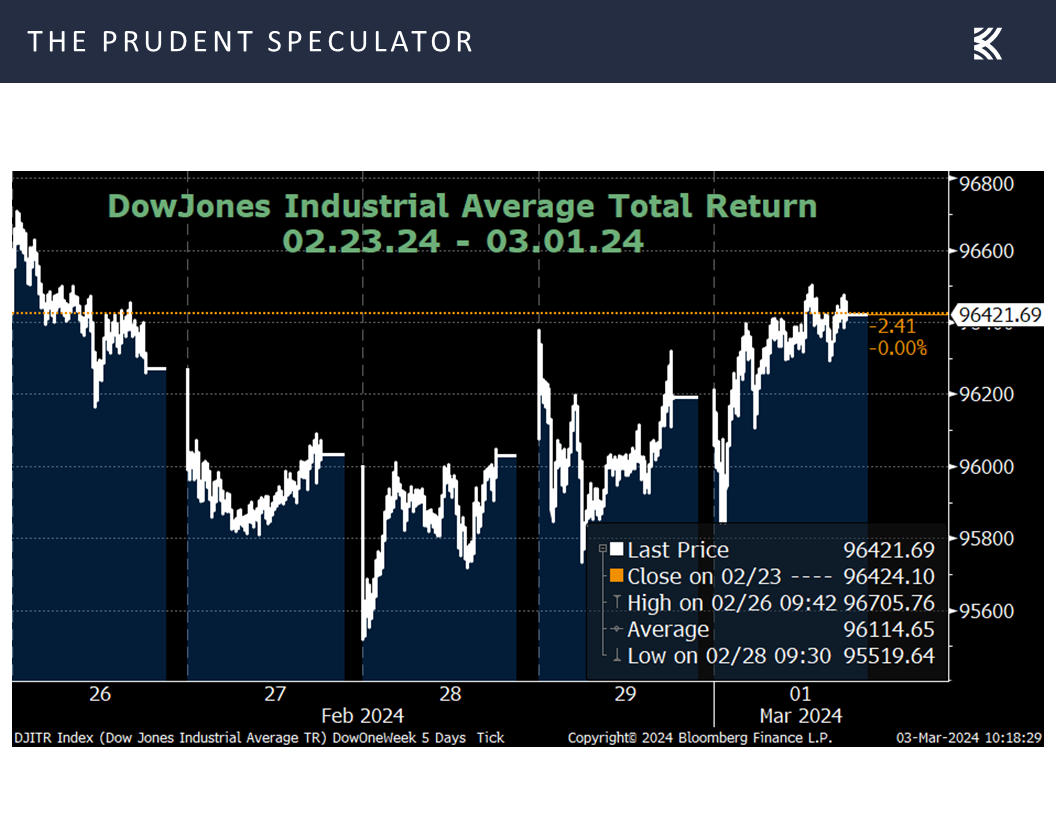

and the Dow Jones Industrial Average on a Total Return basis was essentially flat over the last five days,

Volatility – The Longer the Measuring Stick, the Less Risky Equities Become

illustrating why we like to say that volatility can be mitigated by looking through a longer-term lens,

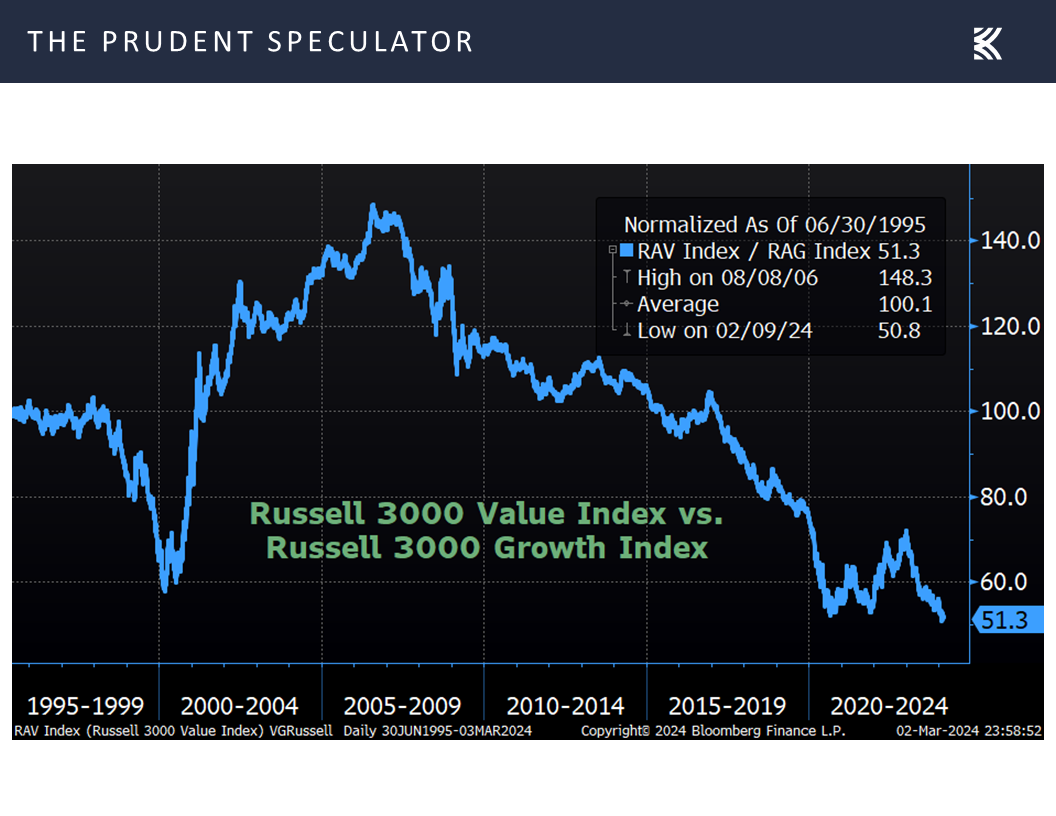

it was another favorable market week for equities in general, with even the Russell 3000 Value index hitting an all-time high on Friday, finally eclipsing the prior record set on 1.12.22.

Econ Stats – A Slew of Weaker-than-Expected Numbers and a Few Good Ones

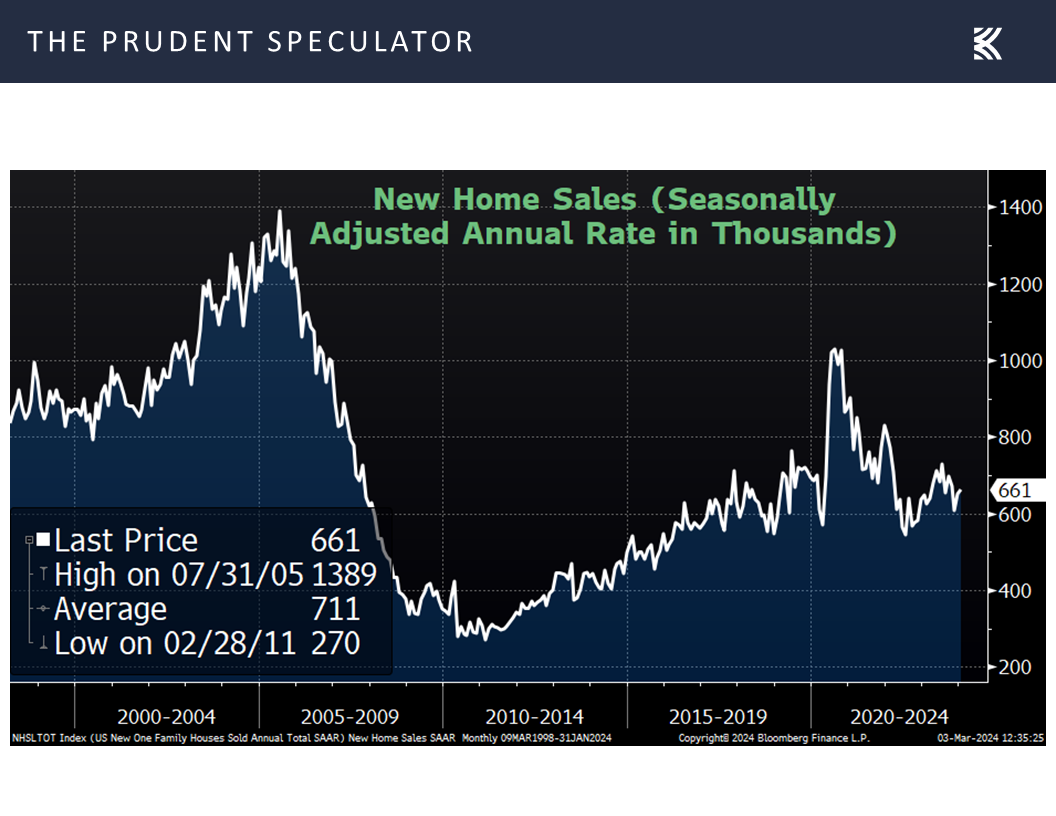

Interestingly, aside from continued excitement for all things A.I., the majority of stocks seemed to catch a bid on weaker-than-expected economic numbers. New home sales for January of 661,000 (est. 684,000) trailed forecasts,

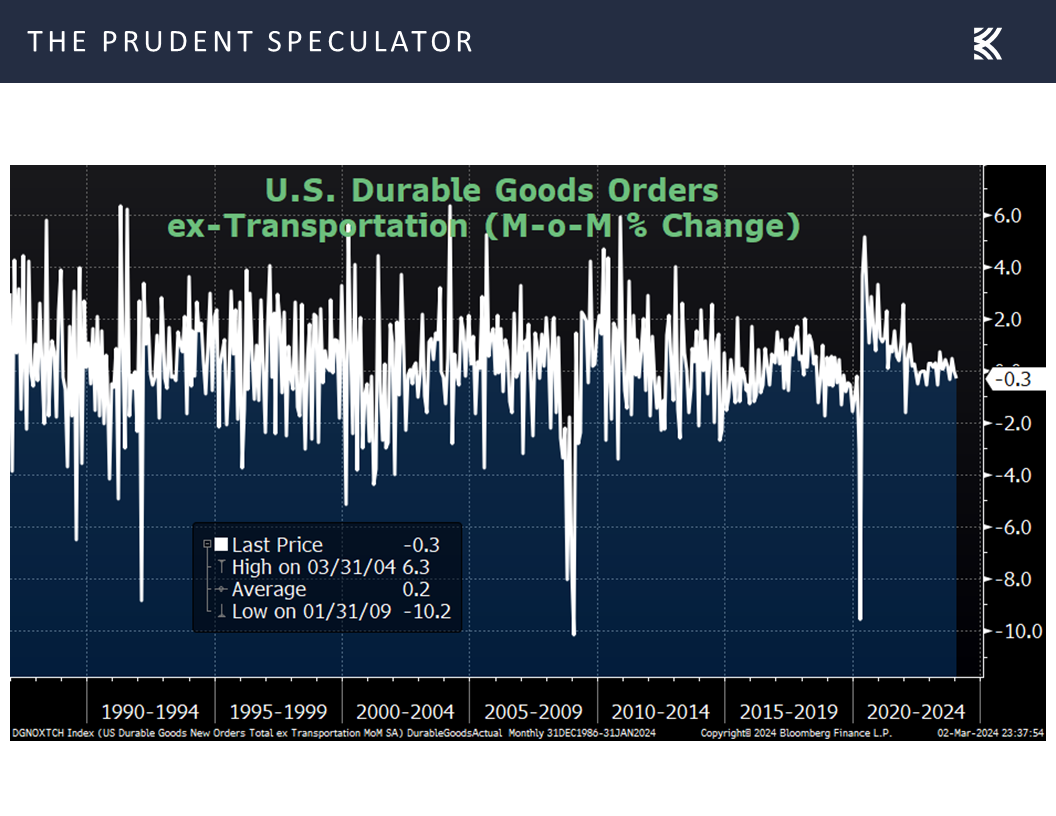

durable goods orders excluding the volatile transportation sector in January slipped 0.3% (est. 0.2% increase),

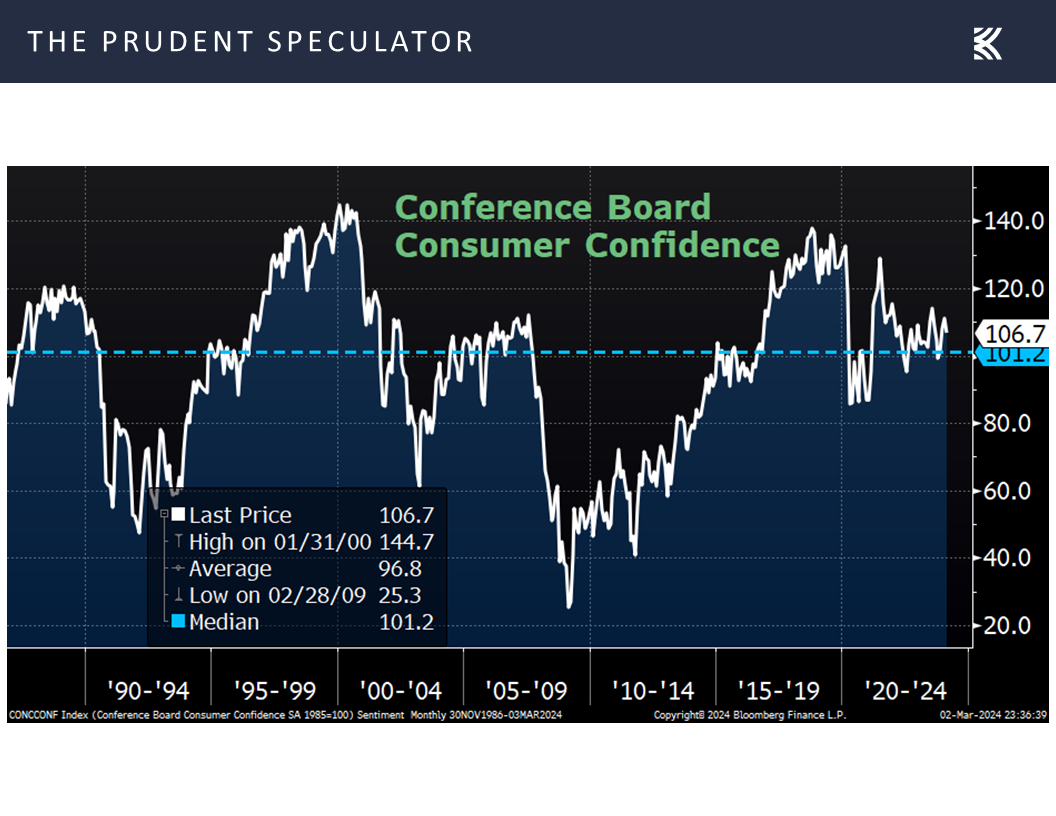

the Conference Board’s Consumer Confidence gauge for February dropped to 106.7 (est. 115.0), down from a revised 110.9 in January,

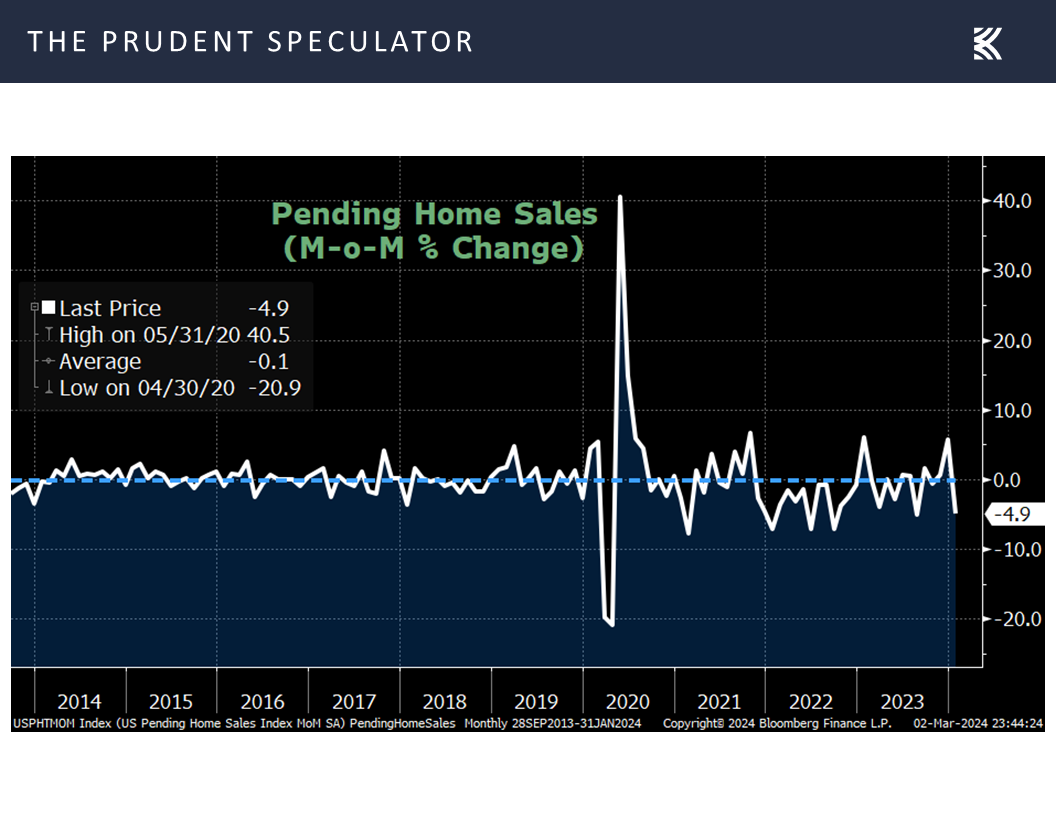

pending home sales for January dipped 4.9% (est. 1.1% increase),

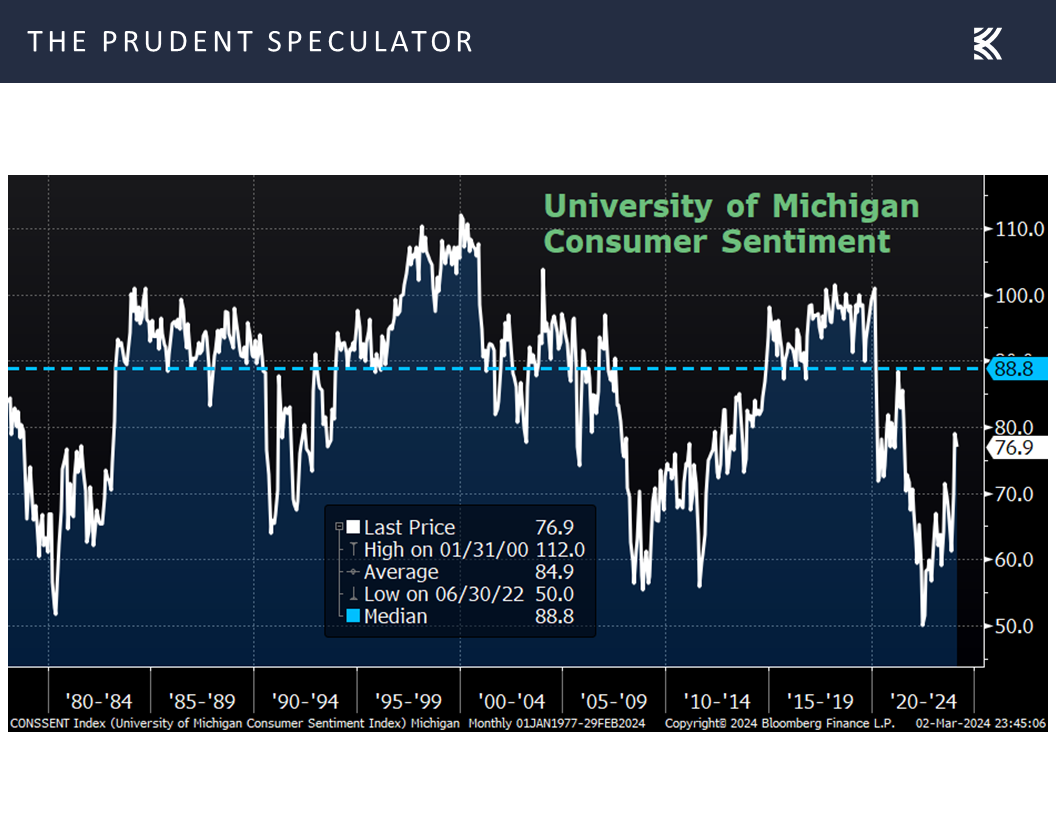

the final University of Michigan Consumer Sentiment measure for February skidded to 76.9 (est. 79.6), down from 79.6 in January,

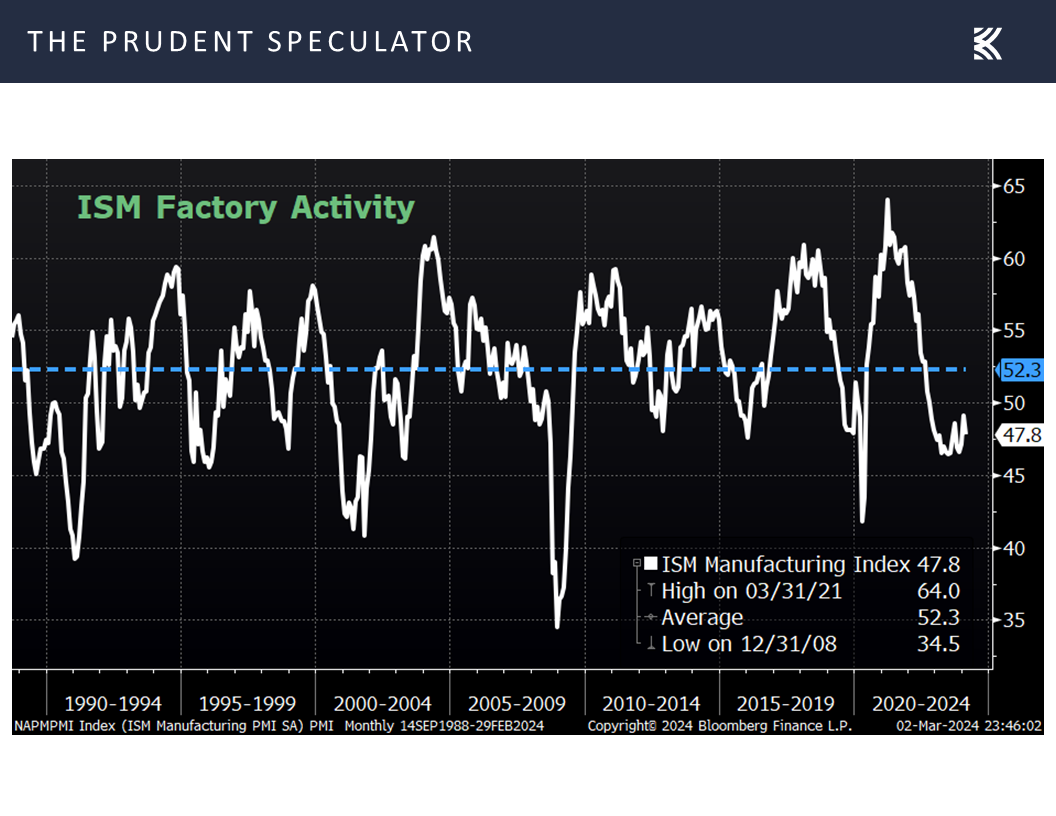

and the Institute for Supply Management’s (ISM) Manufacturing PMI declined to 47.8 in February (est. 49.5), compared to 49.1 in January.

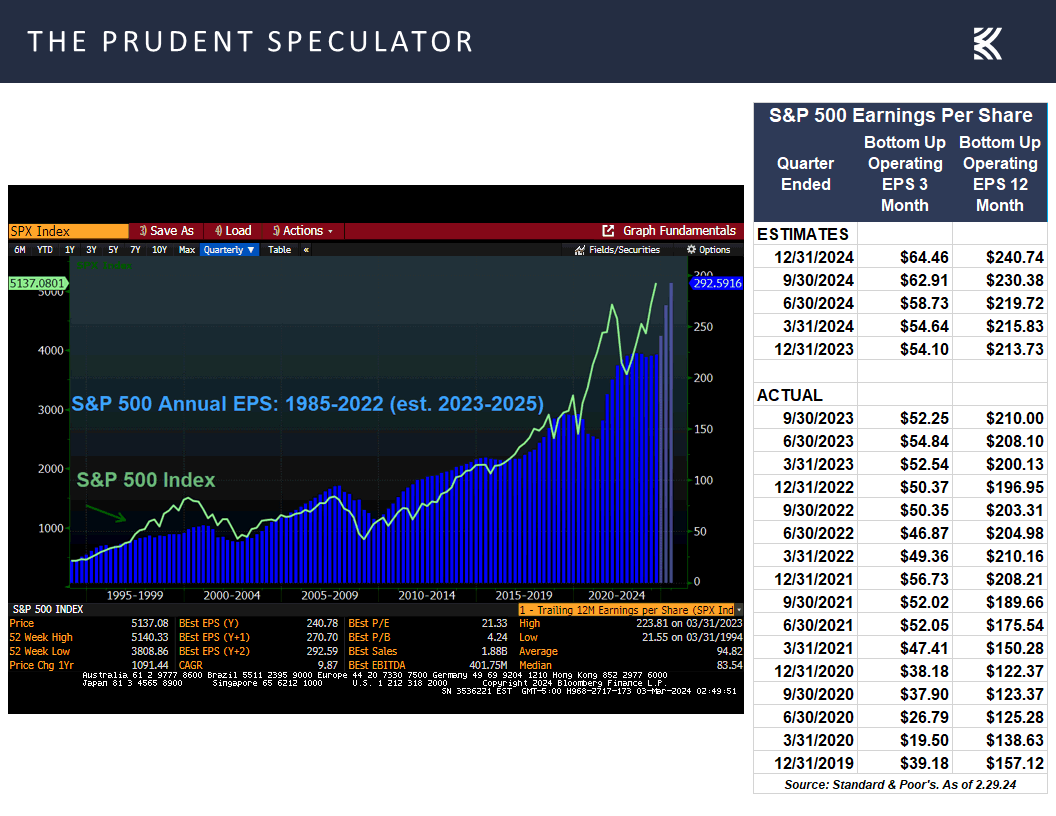

Econ Outlook – Real GDP Growth in ’24 Still Likely; EPS Estimates on the Rise

Of course, the economy is hardly falling off a cliff as ISM states, “A Manufacturing PMI® above 42.5 percent, over a period of time, generally indicates an expansion of the overall economy. Therefore, the February Manufacturing PMI® indicates the overall economy grew for the 46th straight month after one month of contraction (April 2020). The past relationship between the Manufacturing PMI® and the overall economy indicates that the February reading (47.8 percent) corresponds to a change of plus-1.5 percent in real gross domestic product (GDP) on an annualized basis.”

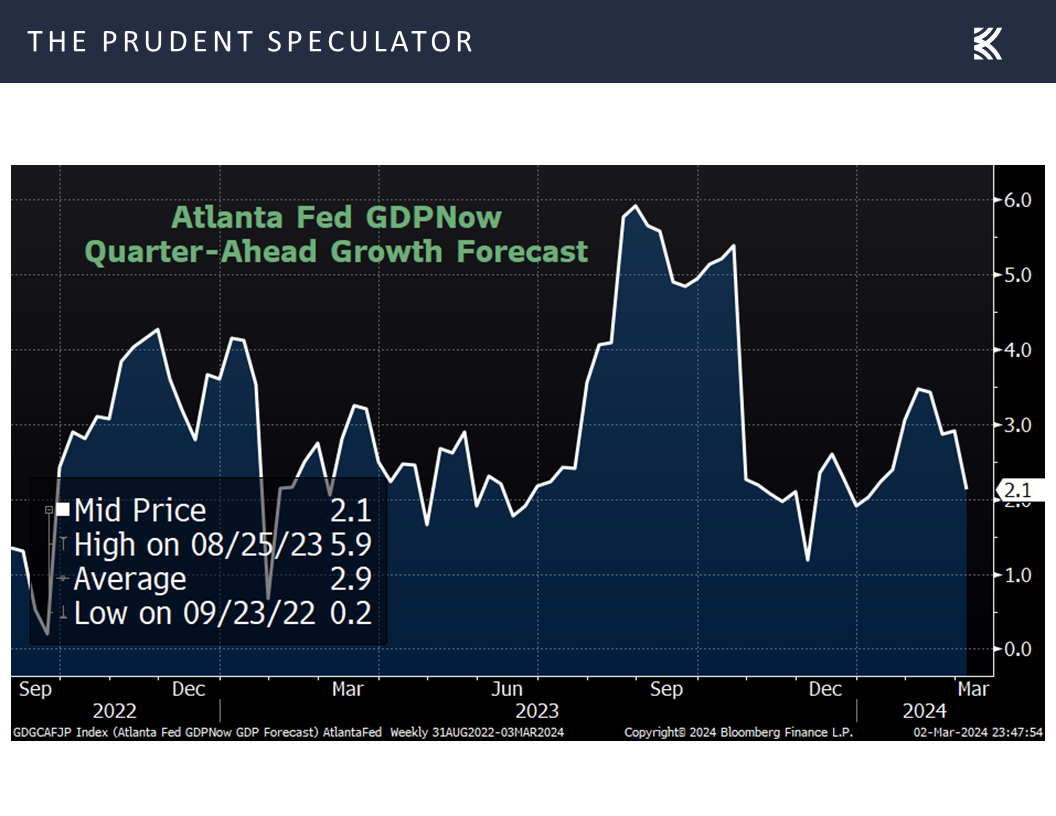

Echoing the ISM projection of growth for U.S. GDP was the latest Q1 estimate of 2.1% from the Atlanta Fed,

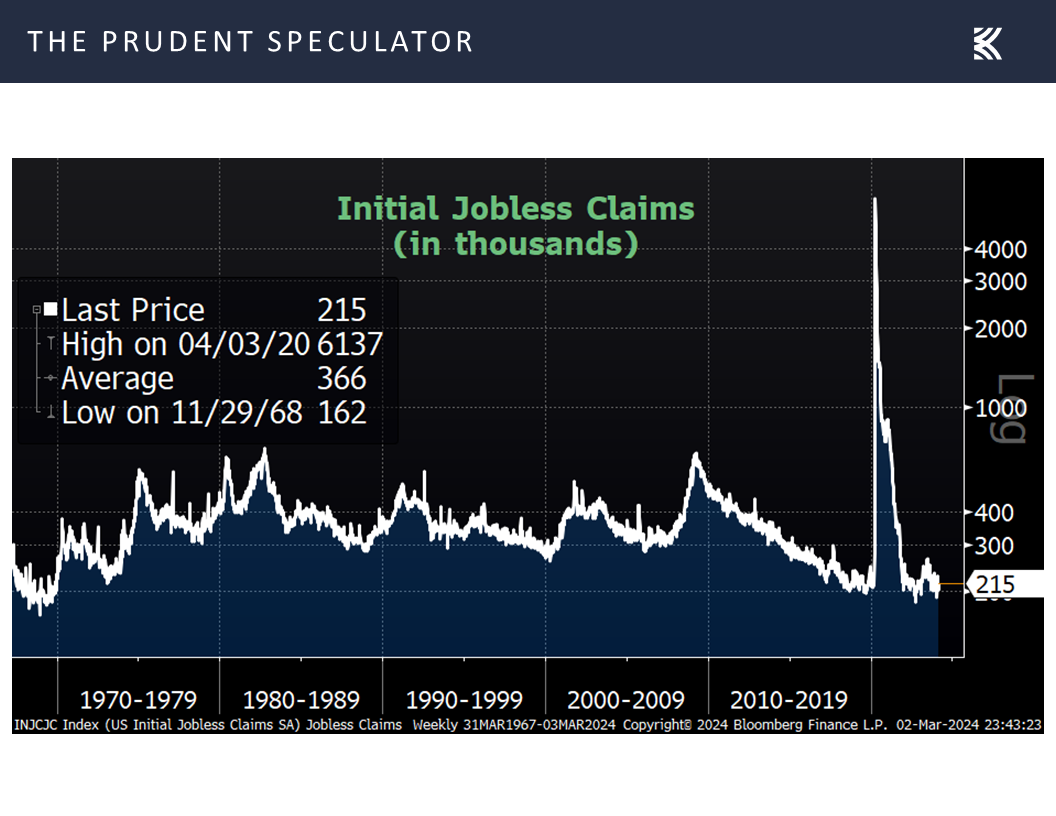

as the labor market remains healthy, with first-time filings for unemployment benefits in the latest week continuing to reside at multi-generational lows,

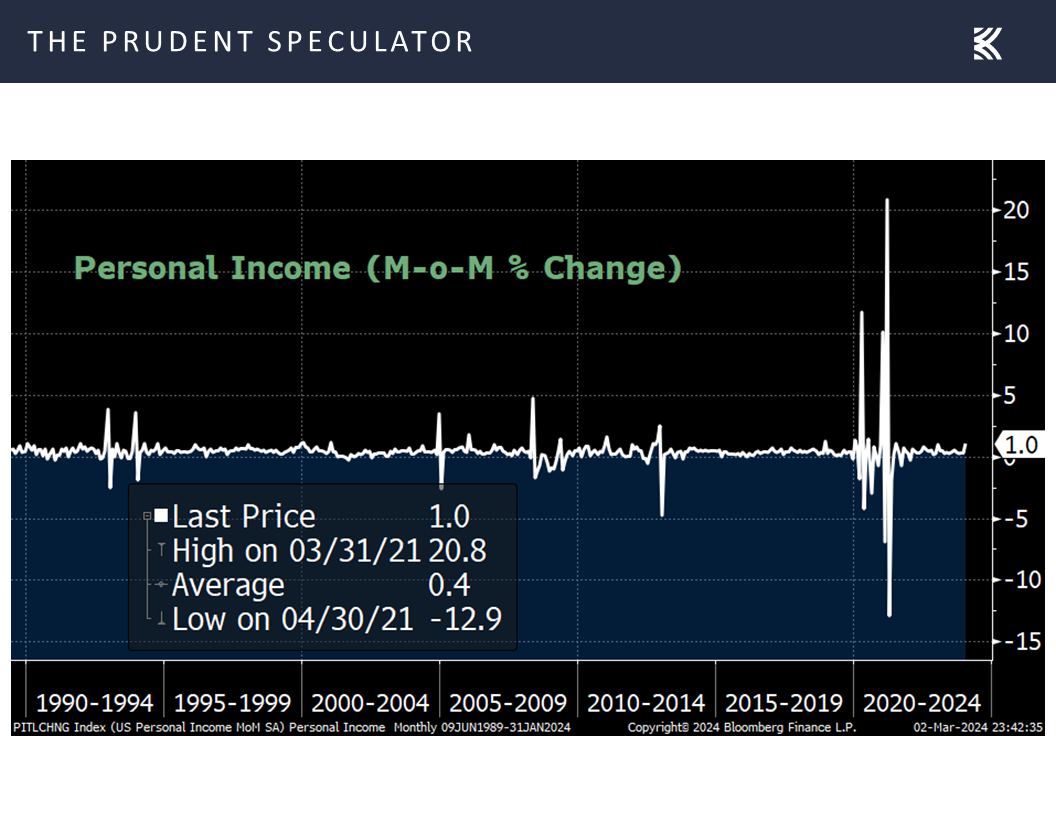

personal income for January climbing a better-than-expected 1.0%,

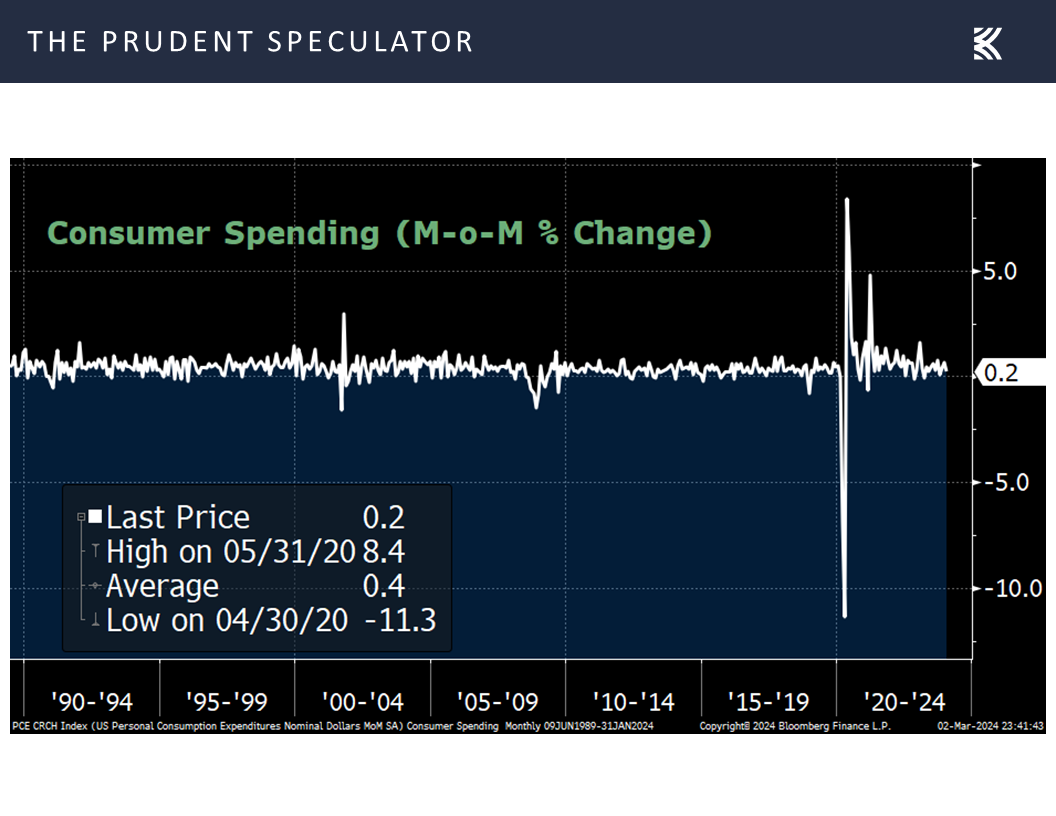

…and consumer spending in January holding up well with a 0.2% rise.

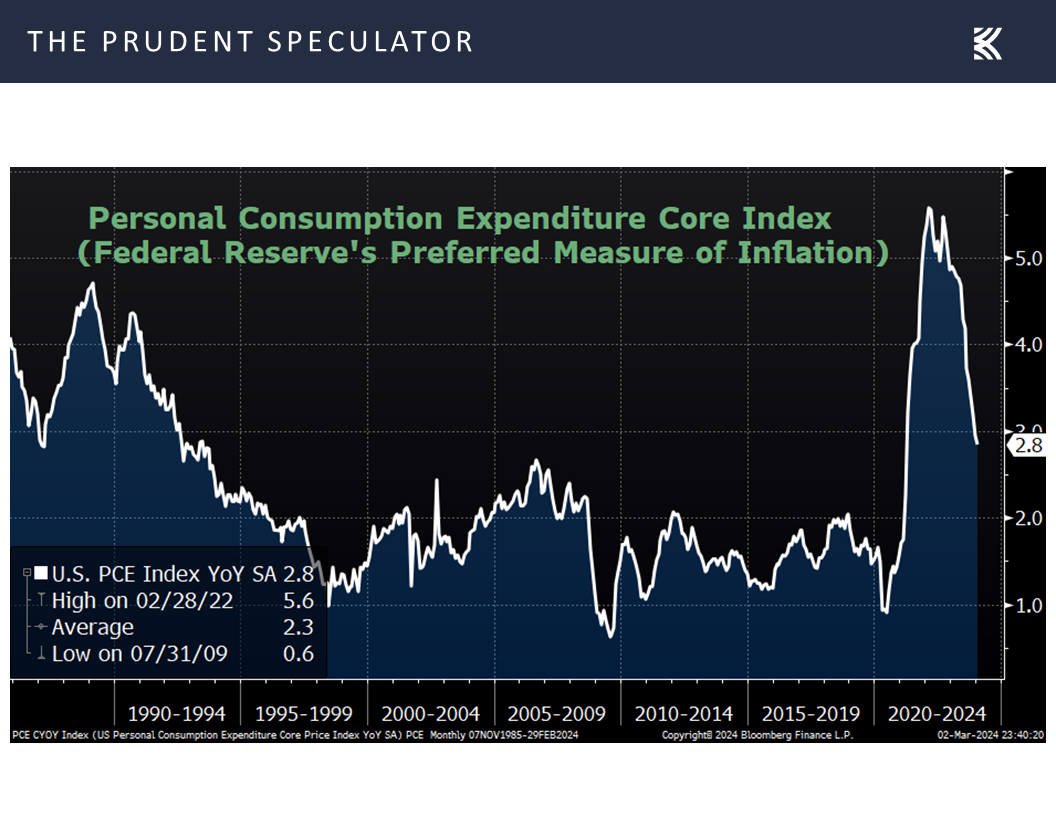

Inflation – PCE Arrives as Expected; Rates Fall

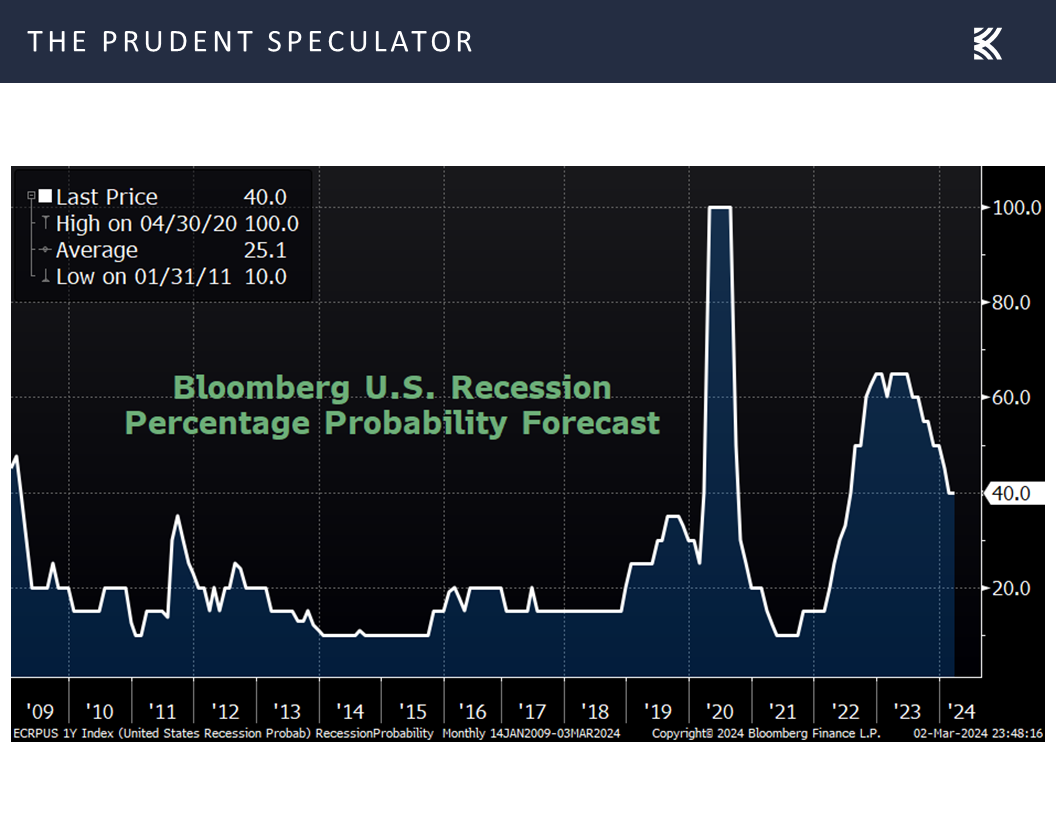

True, Bloomberg tabulations still suggest a 40% chance of recession in the next 12 months,

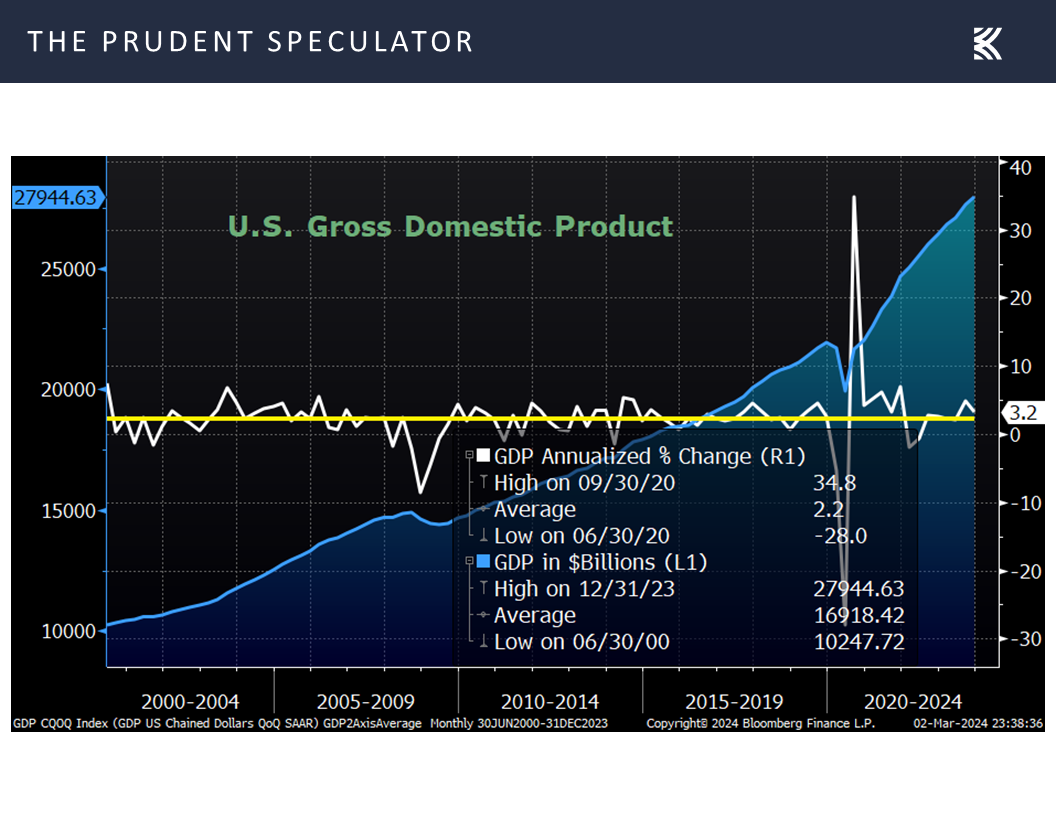

but real (inflation-adjusted) Q4 2023 GDP came in at a solid, though revised-lower, figure of 3.2%,

and corporate earnings projections were lifted upward last week by Standard & Poor’s.

No doubt, markets were cheered when the Federal Reserve’s preferred measure of inflation, the core personal consumption expenditure (PCE) index, matched expectations with a 2.8% year-over-year increase in January, down from a 2.9% rise the month prior,

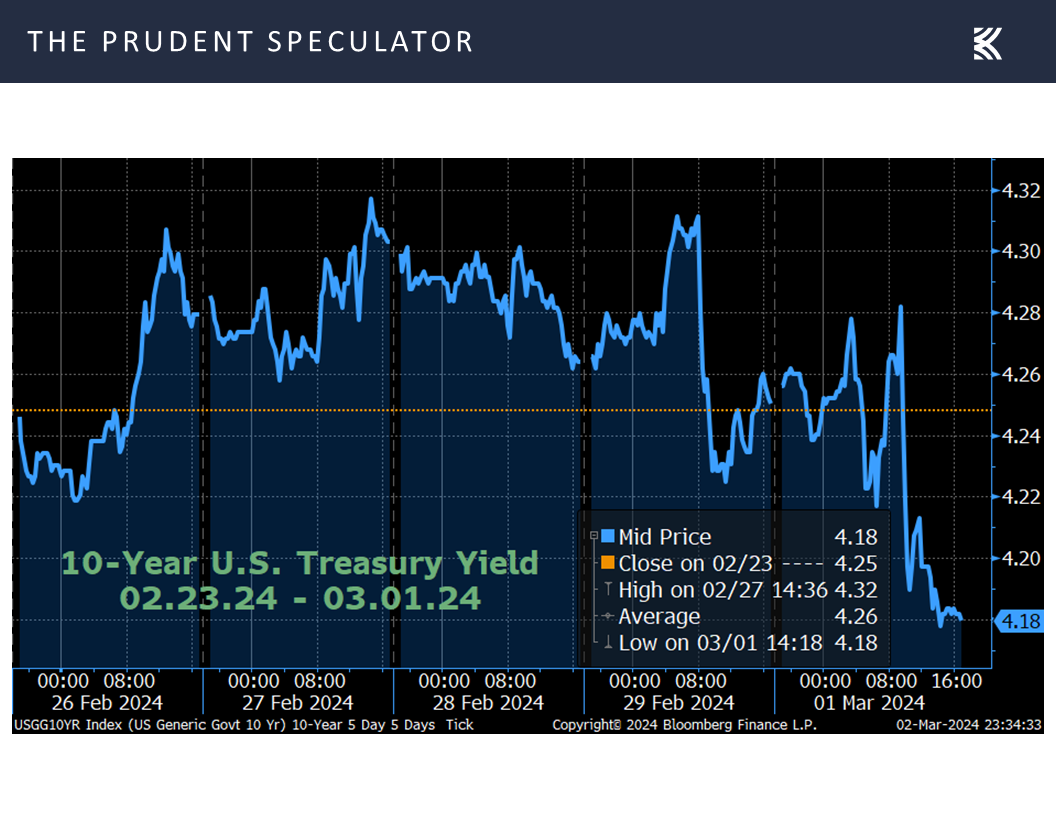

as Treasury prices rallied (yields fell),

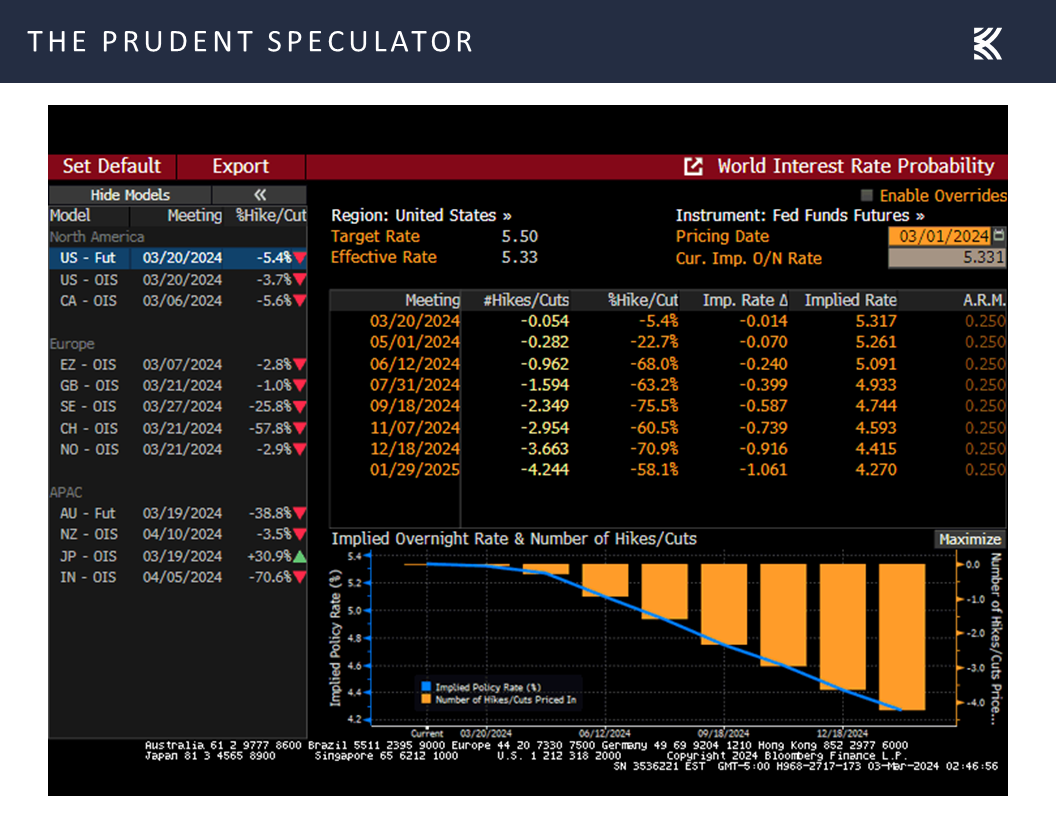

and the betting on Fed Funds in the futures market targeted a year-end 4.42% rate, versus a 4.51% rate at the end of the preceding week,

with the decline in yields adding to the appeal of the Russell 3000 Value index,

and especially our broadly diversified portfolios of what we believe to be undervalued stocks.

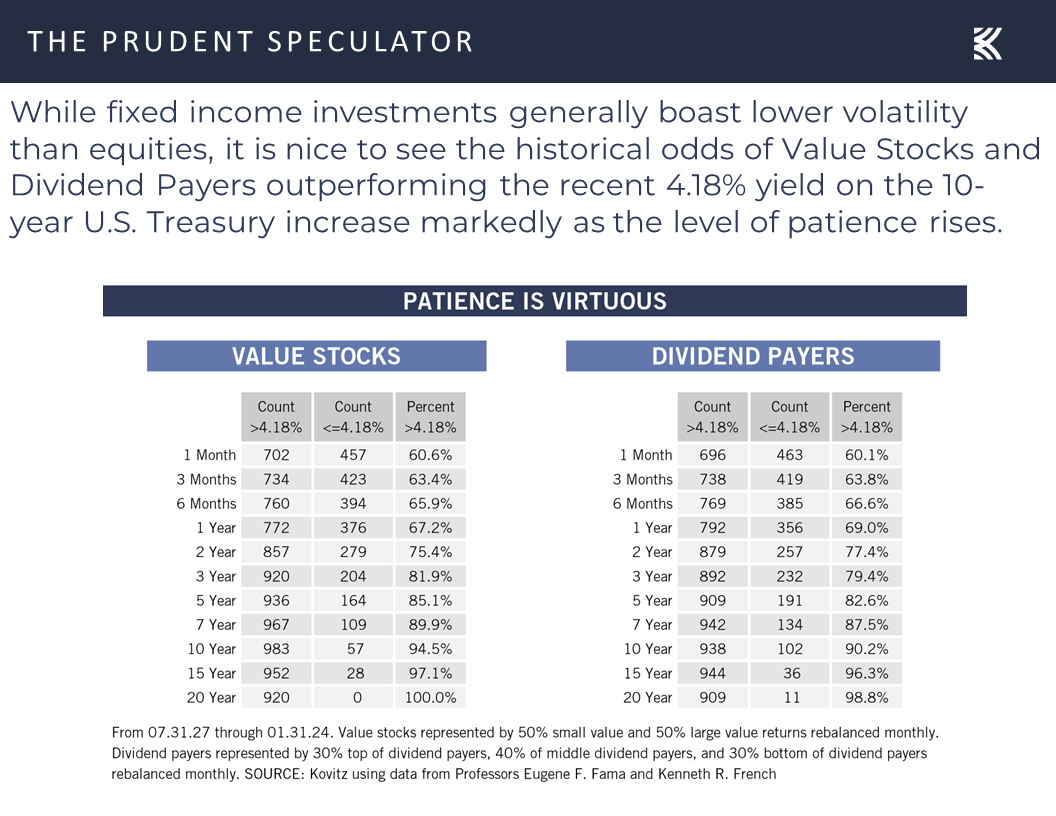

Valuations – Value Stocks Attractively Priced

and especially our broadly diversified portfolios of what we believe to be undervalued stocks.

Sentiment – AAII Still Optimistic

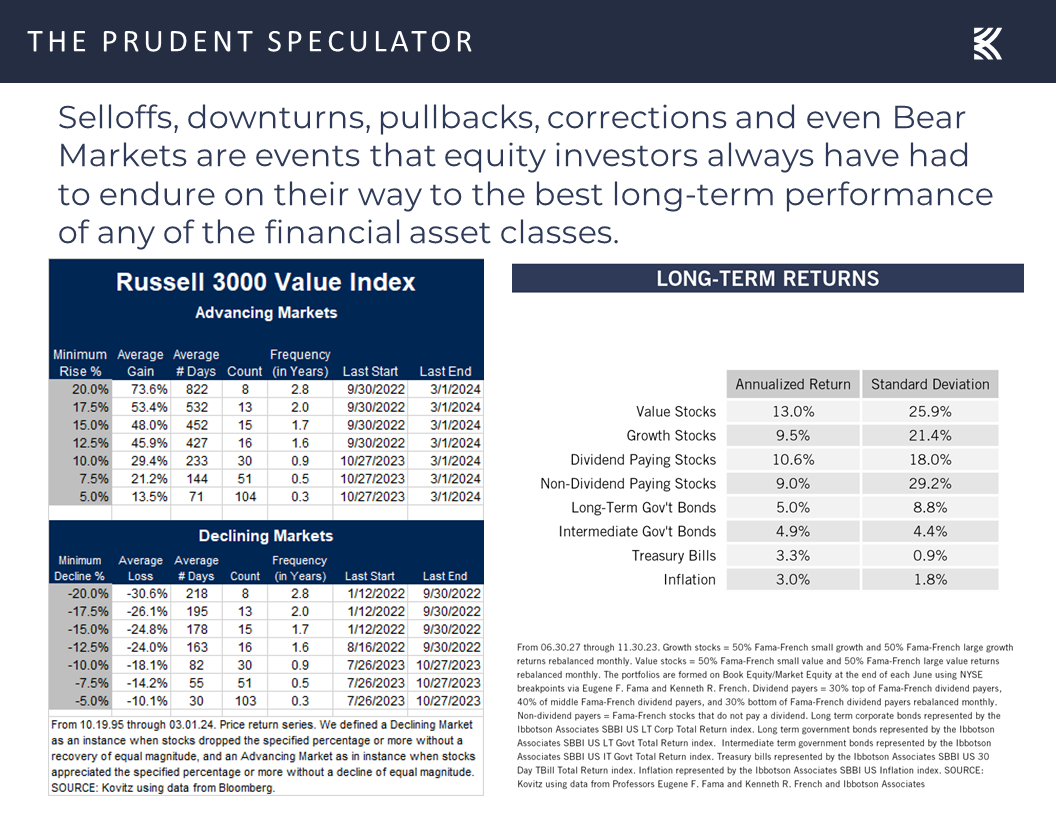

Certainly, we realize that stocks prices move in both directions, so we always are braced for downside volatility, especially with so many seemingly bullish on equities,

but just about every way historical precedents may be sliced and diced supports sticking with stocks through thick and thin,

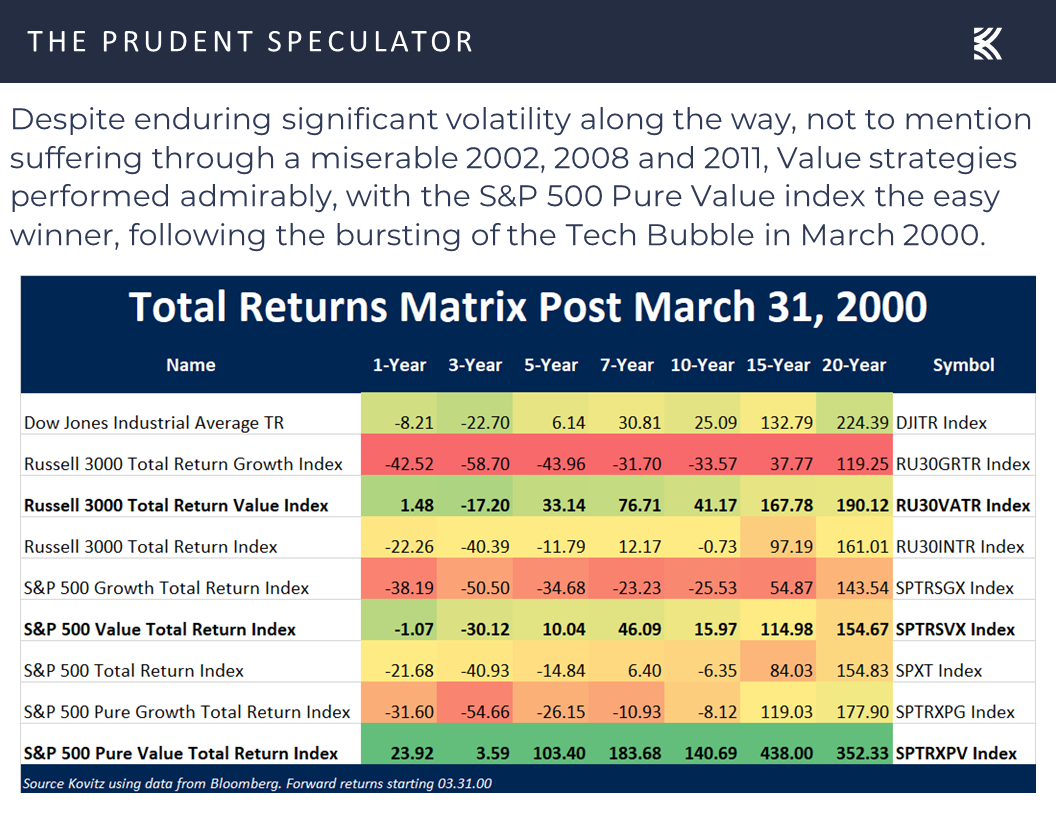

while we can’t help but like that Value is as attractive today relative to Growth, as it was at the peak of the Tech Bubble in 2000,

with those ensuing years turning out very well for reasonably priced companies!

Stock News – Updates on five stocks across five different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Market of Stocks, Econ Stats, Inflation and more Stock News

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the market of stocks, econ stats, inflation and more stock news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Market of Stocks – Nice Week, But Average Stock Still Down on the Year

Volatility – The Longer the Measuring Stick, the Less Risky Equities Become

Econ Stats – A Slew of Weaker-than-Expected Numbers and a Few Good Ones

Econ Outlook – Real GDP Growth in ’24 Still Likely; EPS Estimates on the Rise

Inflation – PCE Arrives as Expected; Rates Fall

Valuations – Value Stocks Attractively Priced

Sentiment – AAII Still Optimistic

Stock News – Updates on five stocks across five different sectors

Market of Stocks – Nice Week, But Average Stock Still Down on the Year

While the median return for stocks in the Russell 3000 is still negative for the year,

and the Dow Jones Industrial Average on a Total Return basis was essentially flat over the last five days,

Volatility – The Longer the Measuring Stick, the Less Risky Equities Become

illustrating why we like to say that volatility can be mitigated by looking through a longer-term lens,

it was another favorable market week for equities in general, with even the Russell 3000 Value index hitting an all-time high on Friday, finally eclipsing the prior record set on 1.12.22.

Econ Stats – A Slew of Weaker-than-Expected Numbers and a Few Good Ones

Interestingly, aside from continued excitement for all things A.I., the majority of stocks seemed to catch a bid on weaker-than-expected economic numbers. New home sales for January of 661,000 (est. 684,000) trailed forecasts,

durable goods orders excluding the volatile transportation sector in January slipped 0.3% (est. 0.2% increase),

the Conference Board’s Consumer Confidence gauge for February dropped to 106.7 (est. 115.0), down from a revised 110.9 in January,

pending home sales for January dipped 4.9% (est. 1.1% increase),

the final University of Michigan Consumer Sentiment measure for February skidded to 76.9 (est. 79.6), down from 79.6 in January,

and the Institute for Supply Management’s (ISM) Manufacturing PMI declined to 47.8 in February (est. 49.5), compared to 49.1 in January.

Econ Outlook – Real GDP Growth in ’24 Still Likely; EPS Estimates on the Rise

Of course, the economy is hardly falling off a cliff as ISM states, “A Manufacturing PMI® above 42.5 percent, over a period of time, generally indicates an expansion of the overall economy. Therefore, the February Manufacturing PMI® indicates the overall economy grew for the 46th straight month after one month of contraction (April 2020). The past relationship between the Manufacturing PMI® and the overall economy indicates that the February reading (47.8 percent) corresponds to a change of plus-1.5 percent in real gross domestic product (GDP) on an annualized basis.”

Echoing the ISM projection of growth for U.S. GDP was the latest Q1 estimate of 2.1% from the Atlanta Fed,

as the labor market remains healthy, with first-time filings for unemployment benefits in the latest week continuing to reside at multi-generational lows,

personal income for January climbing a better-than-expected 1.0%,

…and consumer spending in January holding up well with a 0.2% rise.

Inflation – PCE Arrives as Expected; Rates Fall

True, Bloomberg tabulations still suggest a 40% chance of recession in the next 12 months,

but real (inflation-adjusted) Q4 2023 GDP came in at a solid, though revised-lower, figure of 3.2%,

and corporate earnings projections were lifted upward last week by Standard & Poor’s.

No doubt, markets were cheered when the Federal Reserve’s preferred measure of inflation, the core personal consumption expenditure (PCE) index, matched expectations with a 2.8% year-over-year increase in January, down from a 2.9% rise the month prior,

as Treasury prices rallied (yields fell),

and the betting on Fed Funds in the futures market targeted a year-end 4.42% rate, versus a 4.51% rate at the end of the preceding week,

with the decline in yields adding to the appeal of the Russell 3000 Value index,

and especially our broadly diversified portfolios of what we believe to be undervalued stocks.

Valuations – Value Stocks Attractively Priced

and especially our broadly diversified portfolios of what we believe to be undervalued stocks.

Sentiment – AAII Still Optimistic

Certainly, we realize that stocks prices move in both directions, so we always are braced for downside volatility, especially with so many seemingly bullish on equities,

but just about every way historical precedents may be sliced and diced supports sticking with stocks through thick and thin,

while we can’t help but like that Value is as attractive today relative to Growth, as it was at the peak of the Tech Bubble in 2000,

with those ensuing years turning out very well for reasonably priced companies!

Stock News – Updates on five stocks across five different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.