The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Market Rebound, Corporate Profits, Interest Rates and AAII Sentiment. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Market Rebound – Big Bounce off the Siegel Low Continues

Econ Outlook – Soft Landing Still Seems Likely

Inflation – PCE Continuing to Trend in a Good Direction

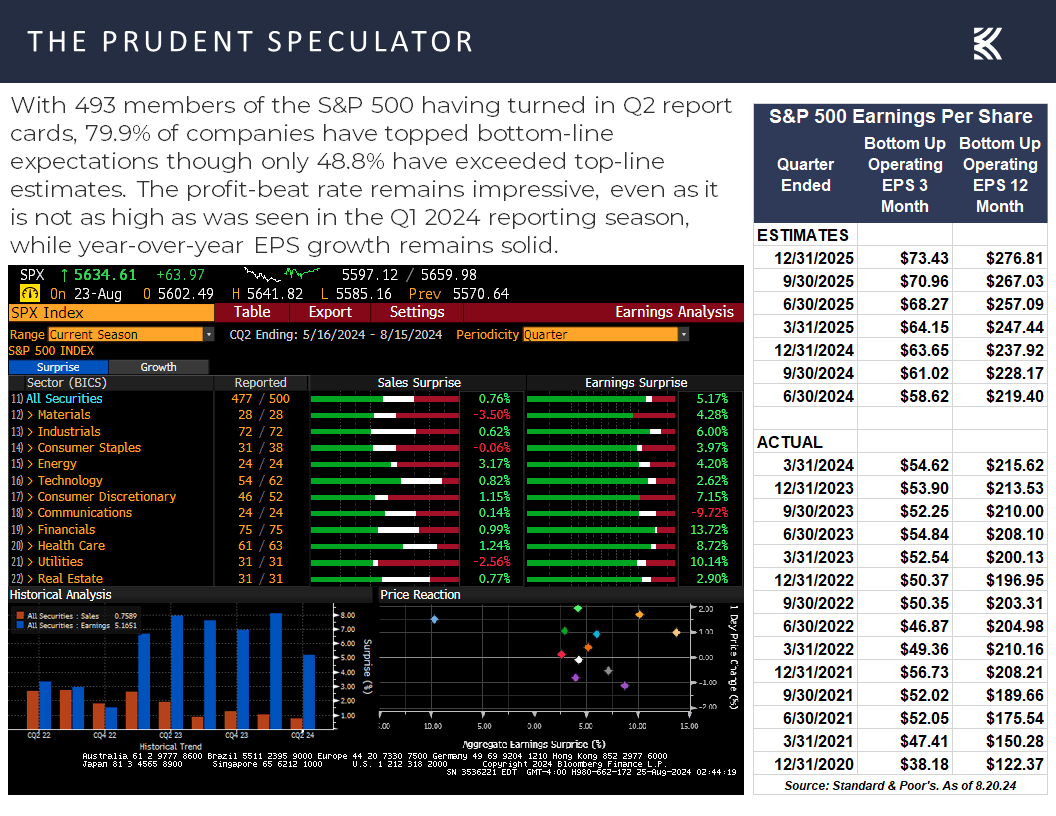

Corporate Profits – Solid EPS Growth Remains the Forecast

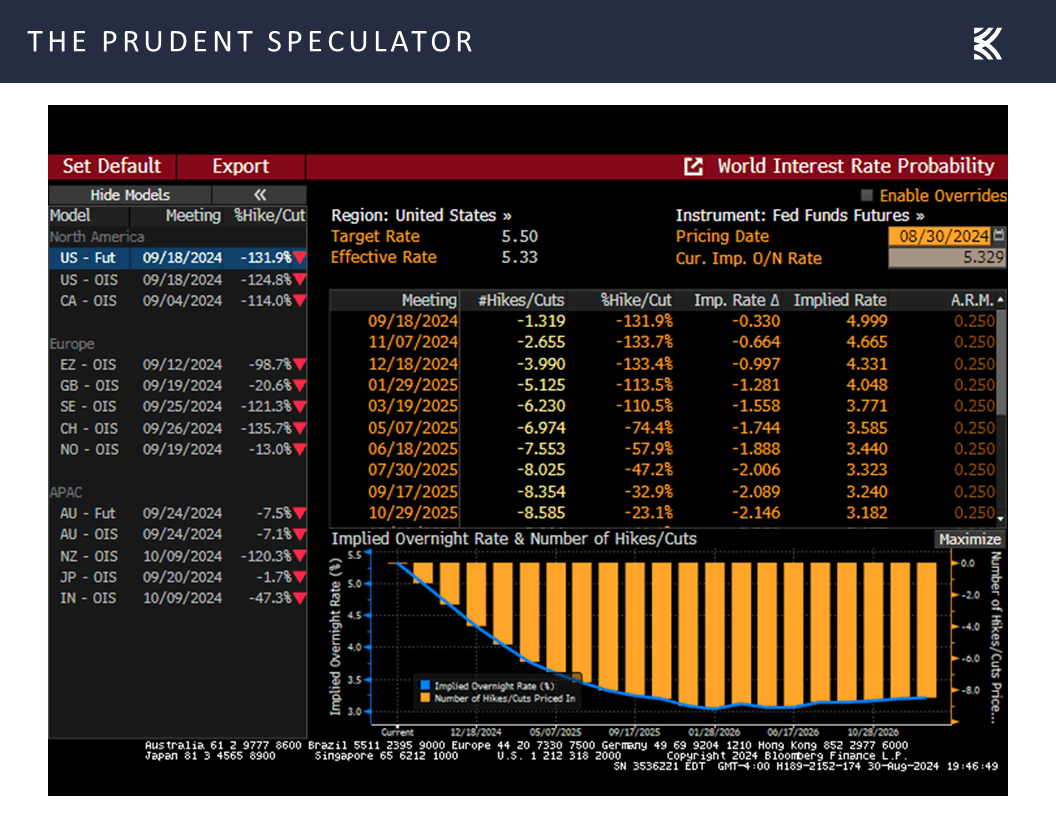

Interest Rates – Fed Cuts Coming; Stocks Have Performed Well Whether Rates Rise or Fall

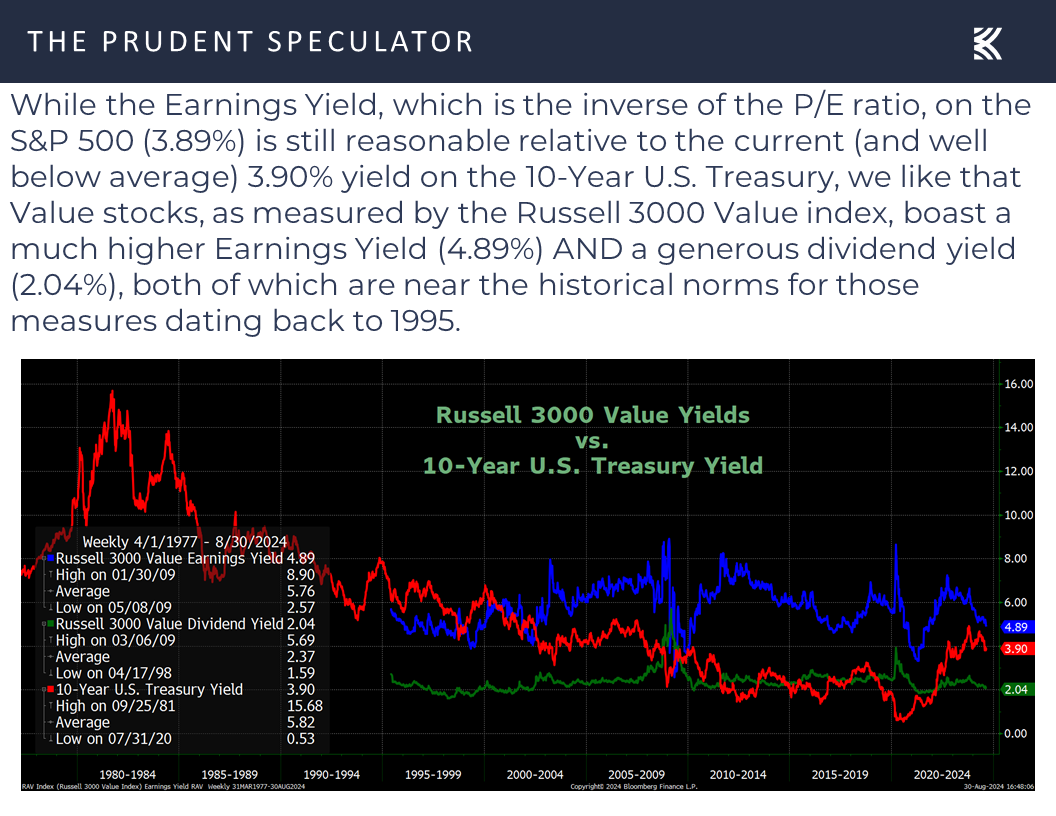

Valuations – Value Remains Attractive

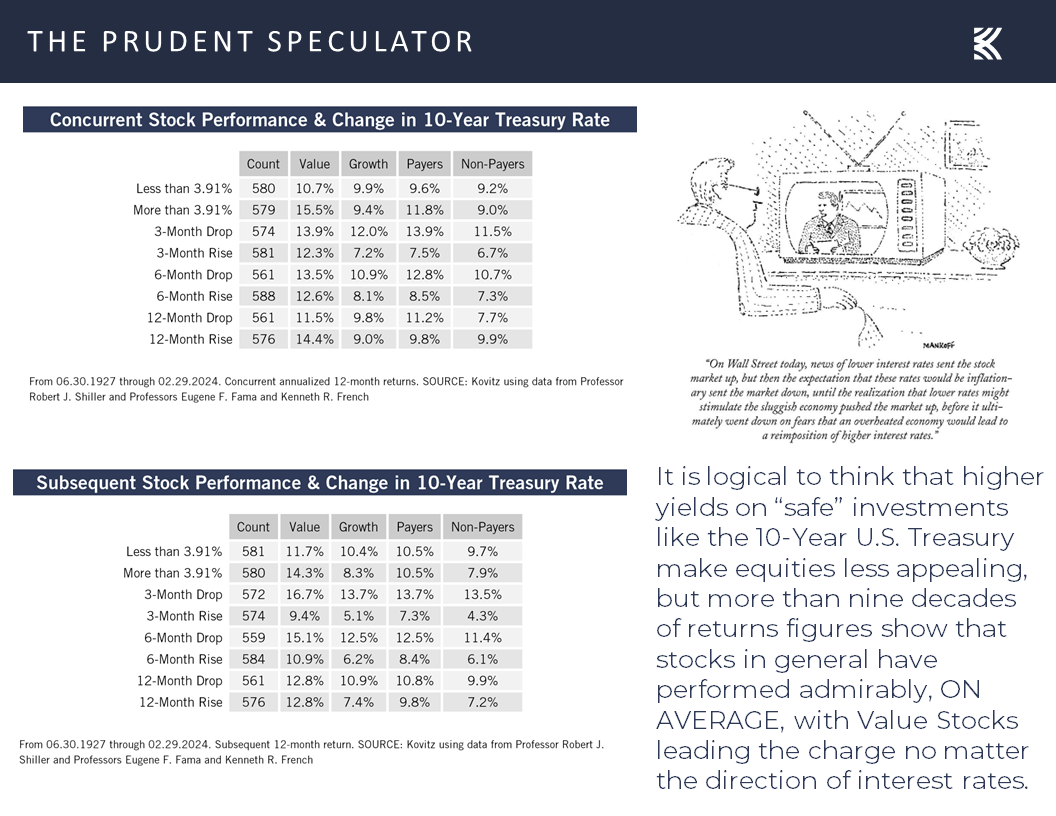

Market History – Volatility & Disconcerting Headlines Through the Years but Long-Term Trend for Stocks is Up

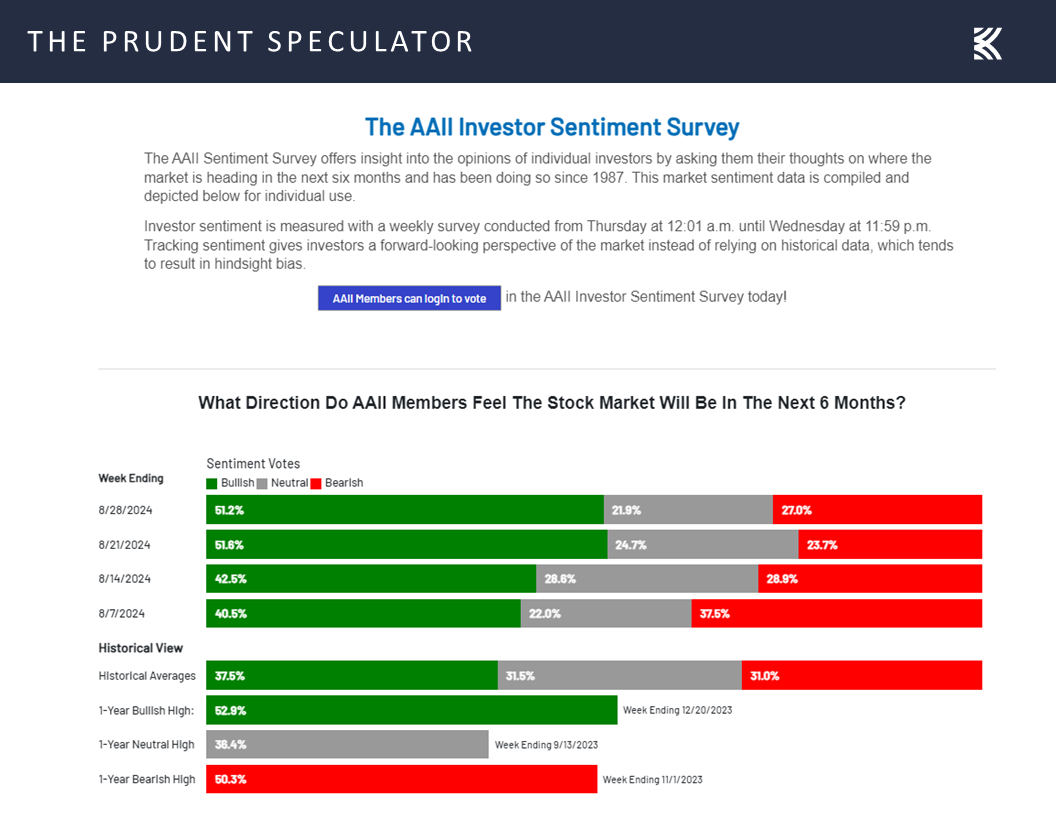

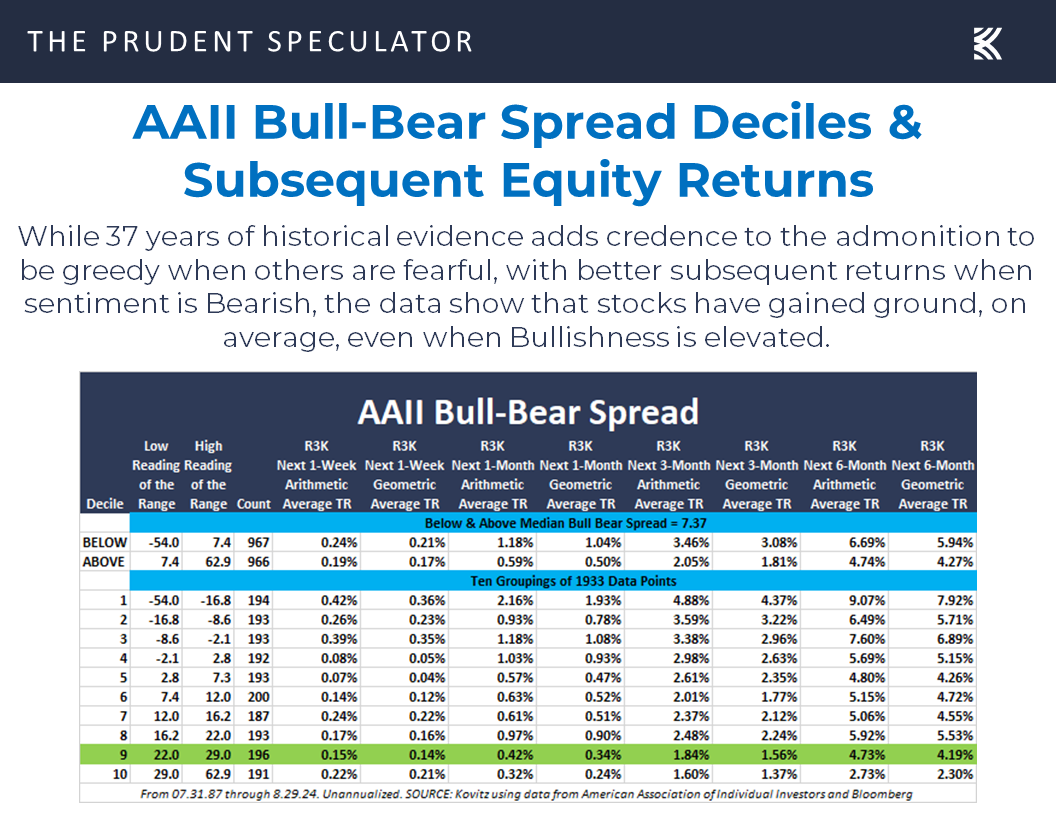

Sentiment – AAII Bullish

Stock News – Updates on FL, JWN, KSS & NTAP

Market Rebound – Big Bounce off the Siegel Low Continues

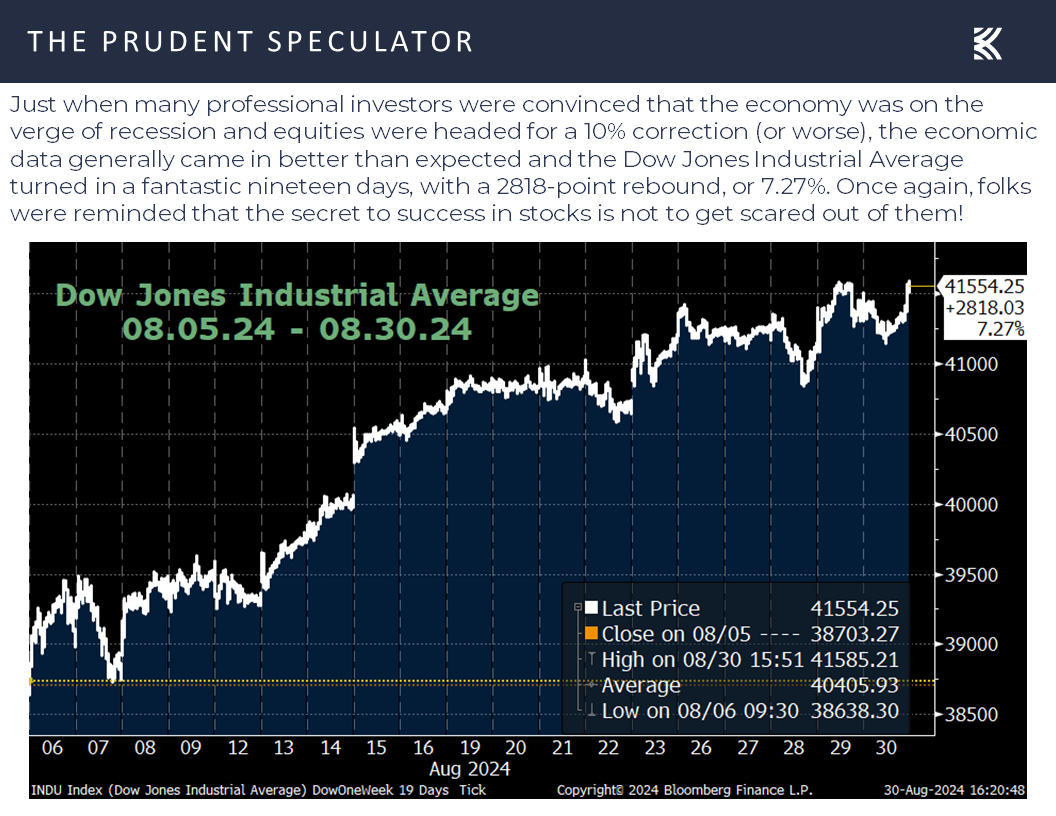

The equity market rebound off of the “Siegel Meltdown” lows of August 5 continued last week with stocks moving modestly higher on the week and sending the Dow Jones Industrial Average to a gain of more than 7% in the 19 days since,

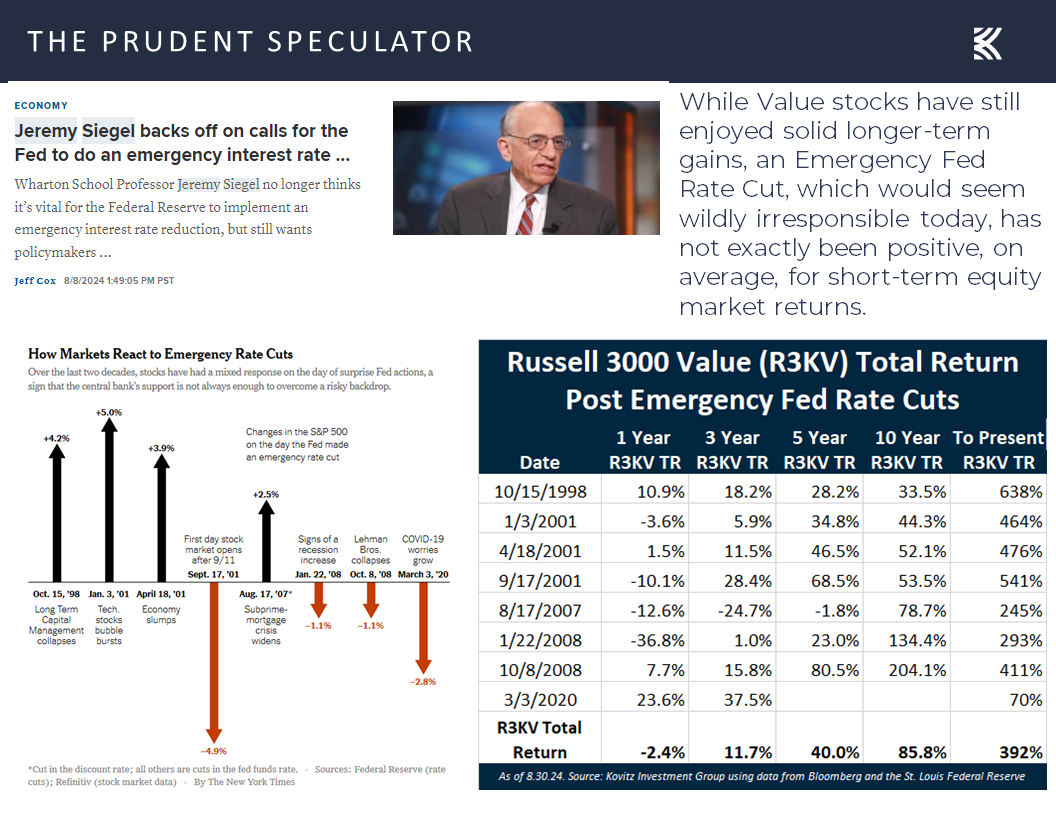

the heretofore even-keeled author of the long-term-oriented-investor bible, Stocks for the Long Run, temporarily lost his mind in calling for an emergency Fed rate cut of 75 basis points in reaction to a couple of weaker-than-expected economic statistics.

Happily, the Wizard of Wharton quickly came to his senses in the days that followed, as the negative message that would have been sent by an emergency rate cut by the data-dependent Fed would likely have sent stocks plunging in the short run and potentially dragged the economy down in the process.

Econ Outlook – Soft Landing Still Seems Likely

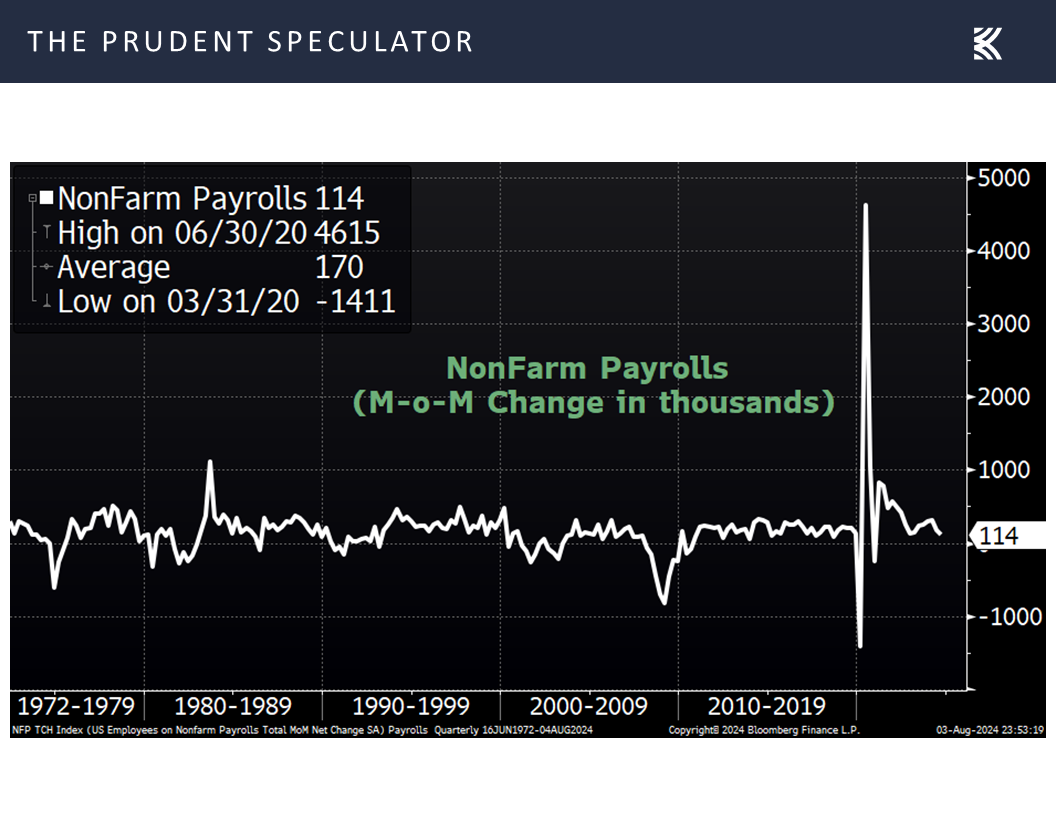

Obviously, the subsequent data could have confirmed that the weaker-than-expected monthly labor report for July, which saw 114,000 new payrolls created (hardly a horrible figure),

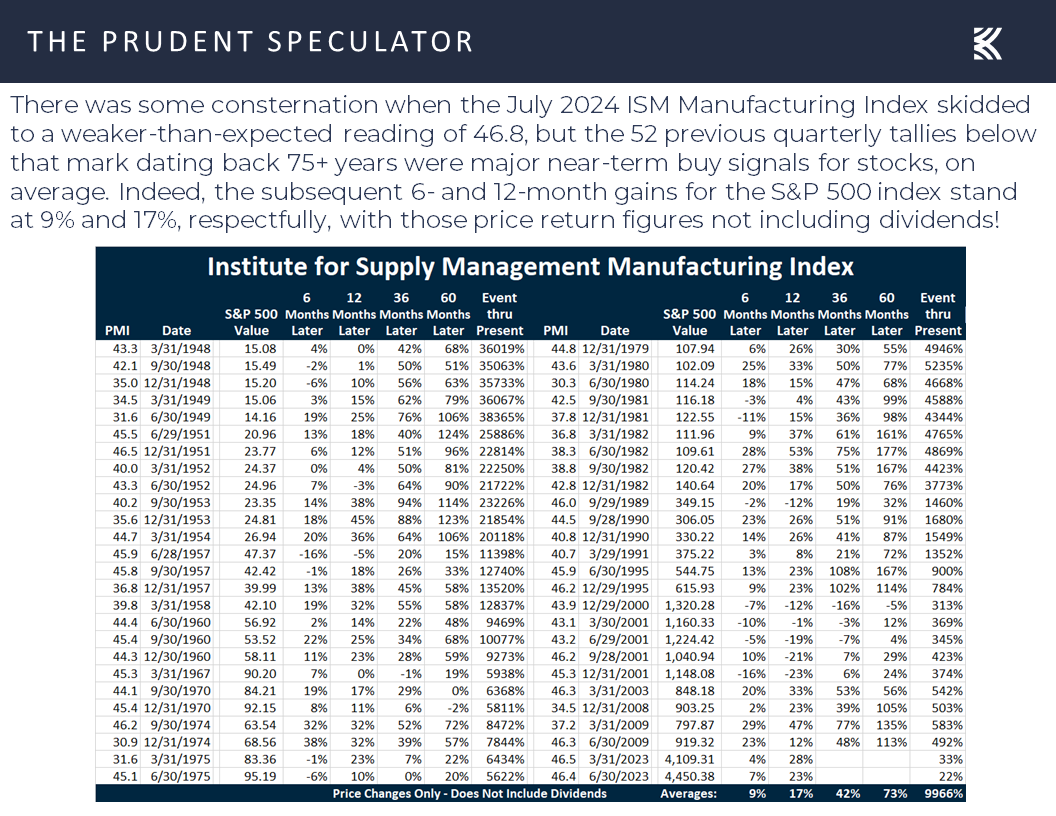

and disappointing July ISM Manufacturing number (at a level that historically has been a major buy signal, on average, for stocks),

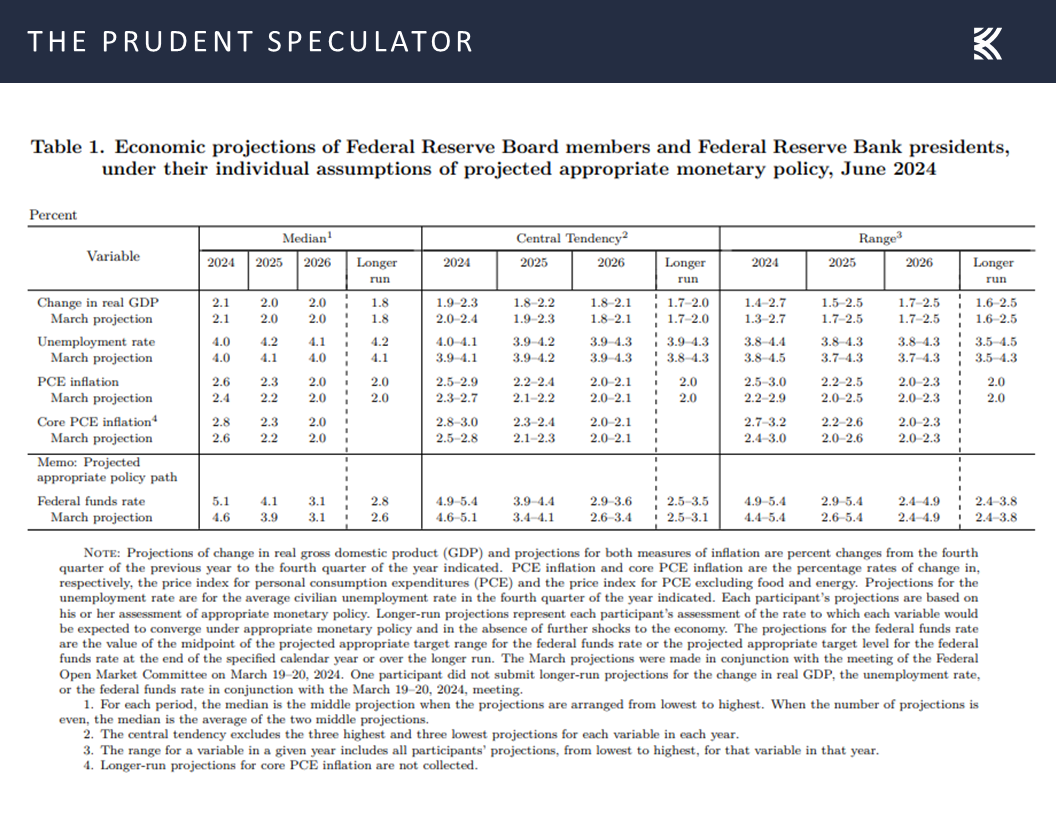

were signals that the so-called “soft-landing” economic outlook that was projected by Federal Reserve Board members and Federal Reserve Bank presidents back in June was not likely to occur.

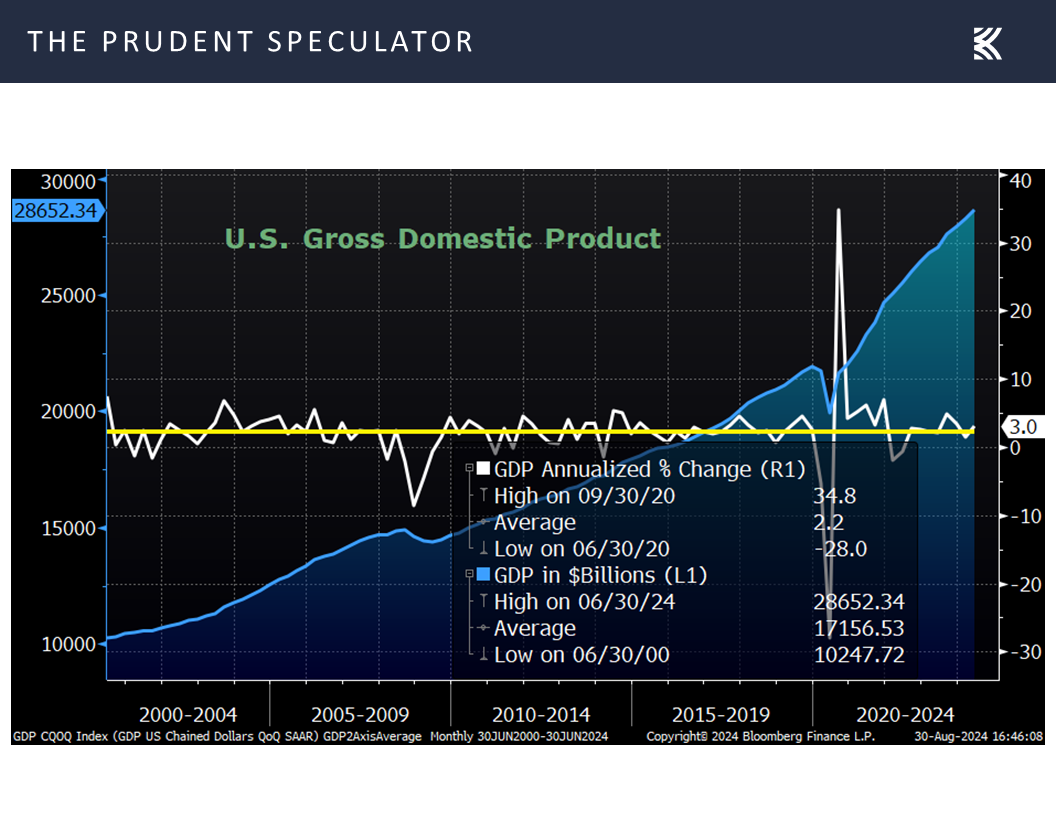

Of course, the economic numbers since have argued that the economy is continuing to hold up well, with last week’s data seeing an uptick in the estimate of real (inflation-adjusted) Q2 U.S. GDP growth to a healthy 3.0%,

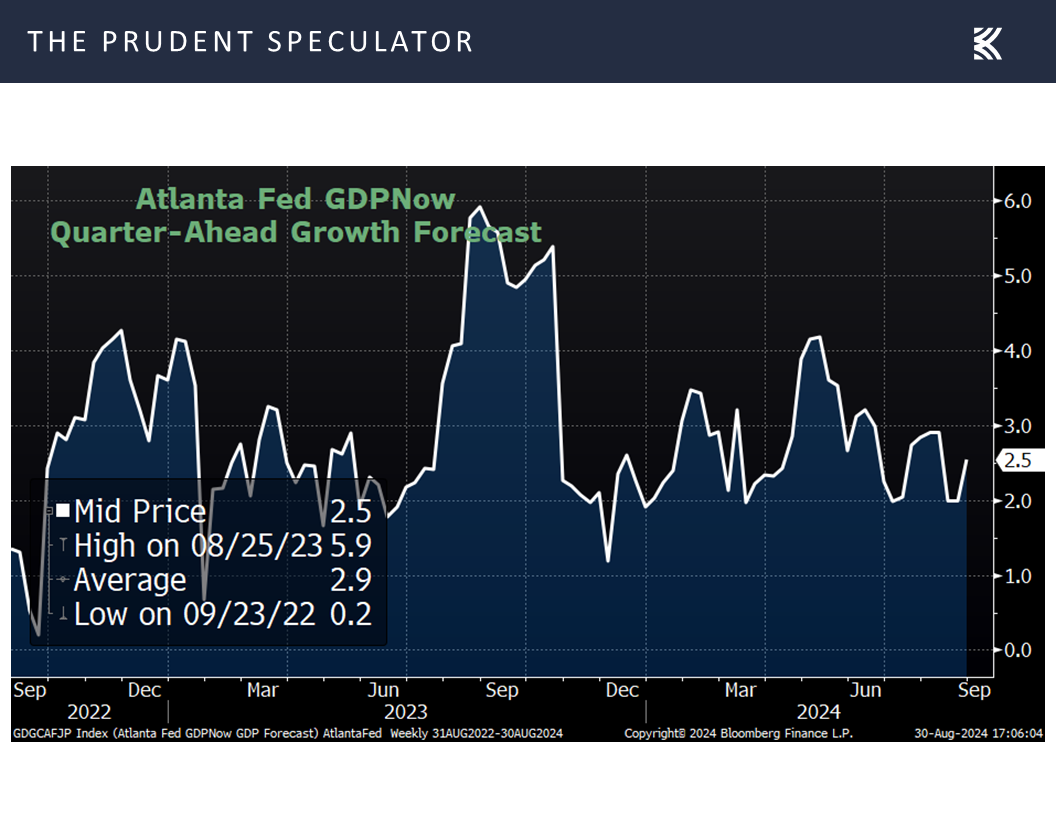

and the Atlanta Fed boosting its forecast for real Q3 U.S. GDP growth to a solid 2.5%.

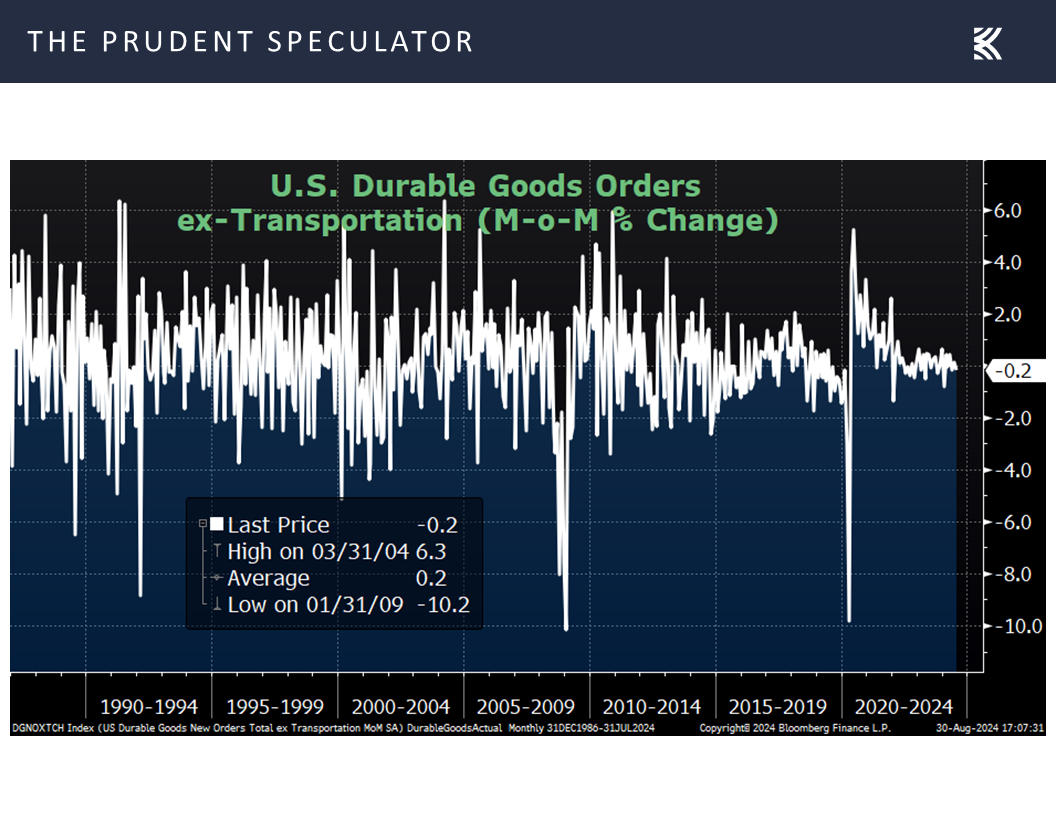

To be sure, not all of the stats last week were robust as orders for durable goods excluding the volatile transportation sector declined by a worse-than-expected 0.2% in July,

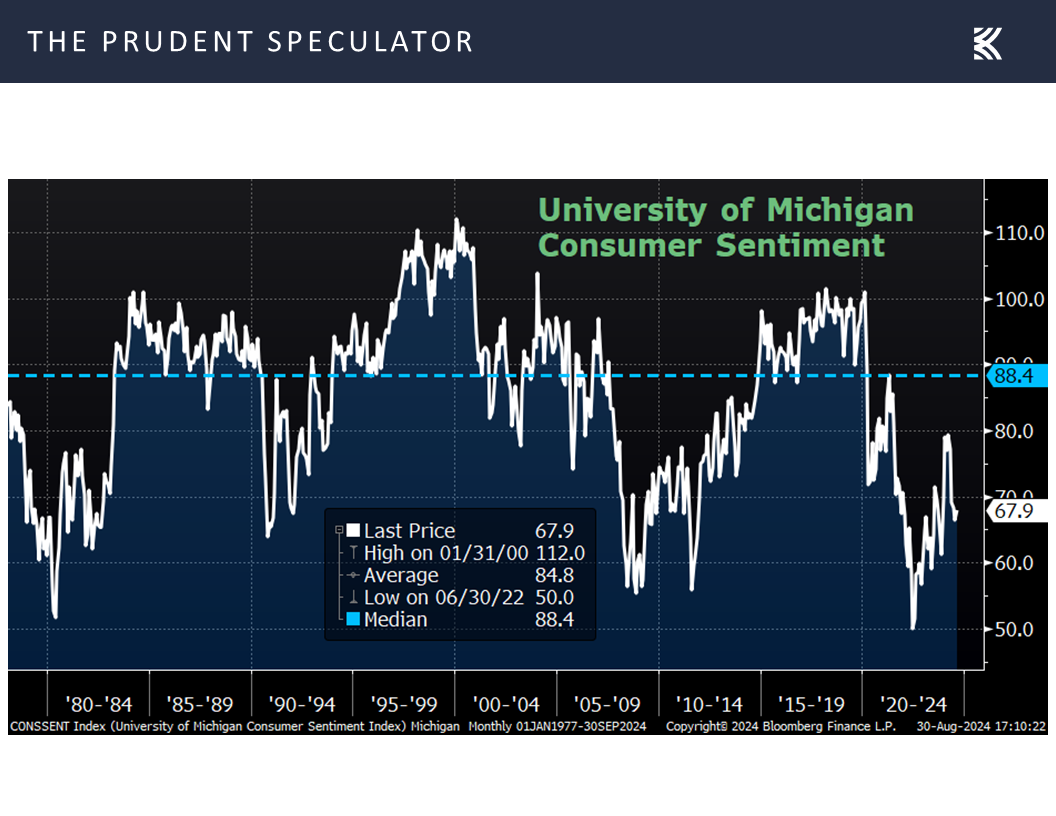

while the University of Michigan’s Consumer Sentiment gauge for August trailed expectations with a historically low reading of 67.9.

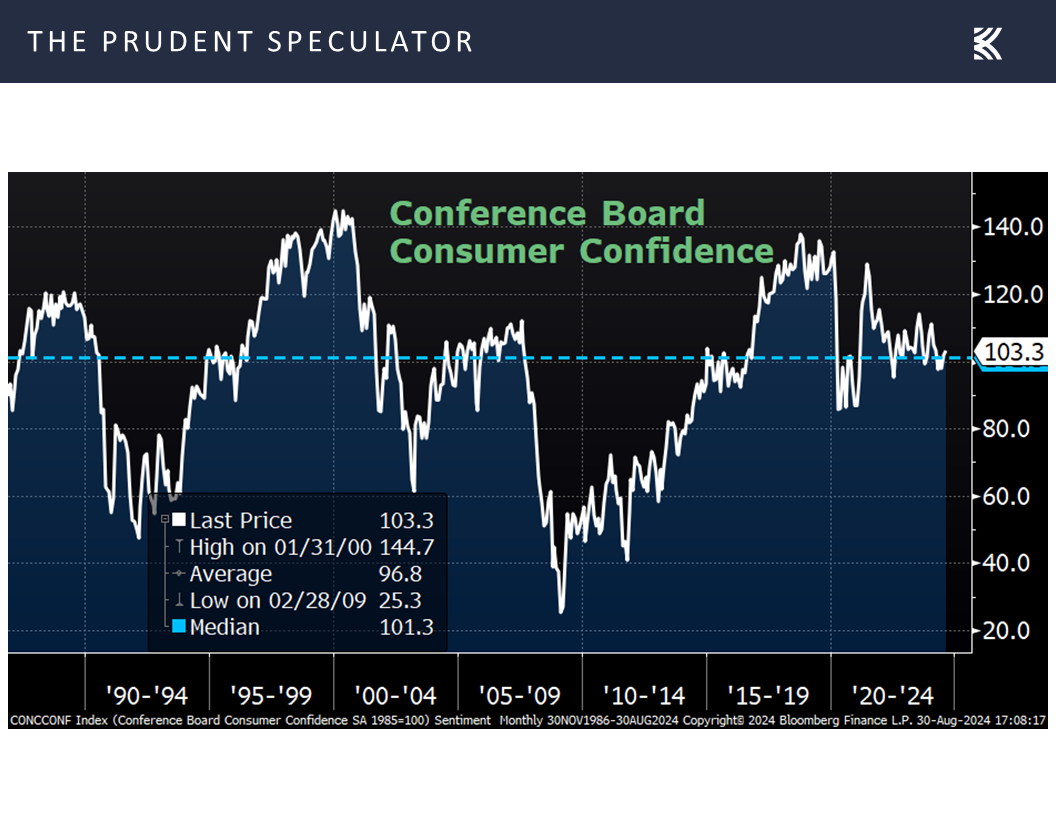

On the other hand, the Conference Board’s measure of Consumer Confidence for August rose to a better-than-estimated 103.3, versus expectations of 100.8 and July’s revised tally of 101.9,

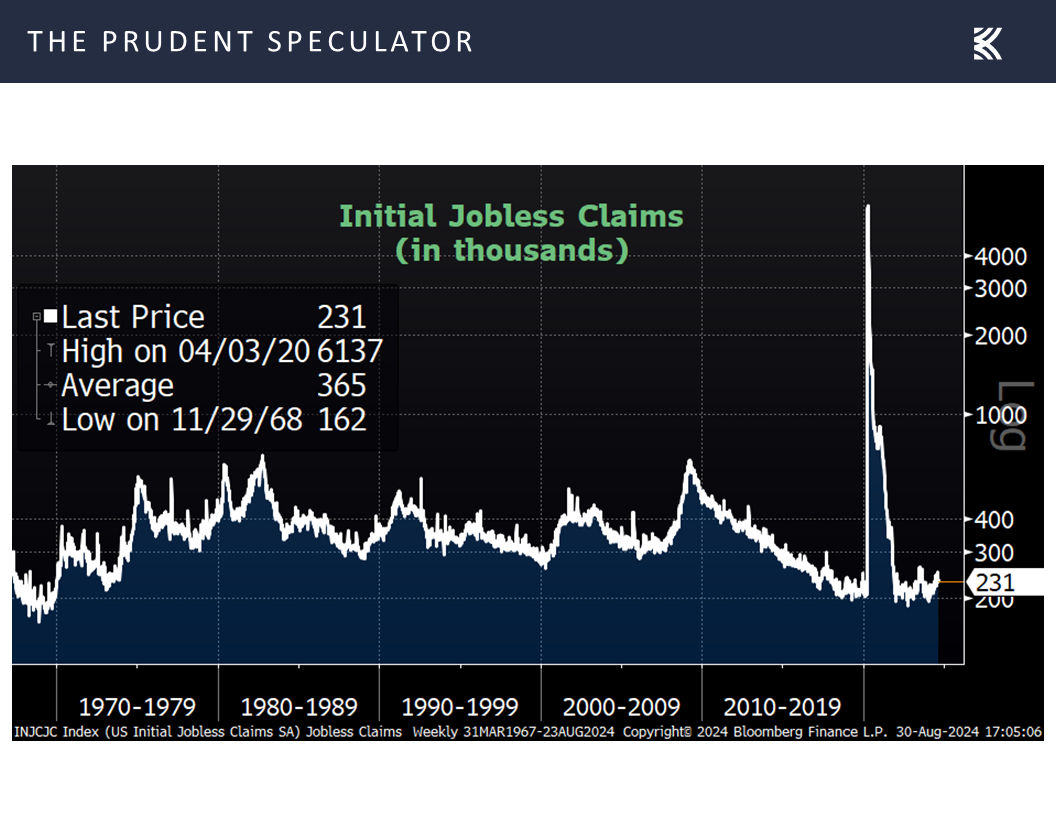

while first-time filings for unemployment benefits continued to reside near multi-generational lows.

Inflation – PCE Continuing to Trend in a Good Direction

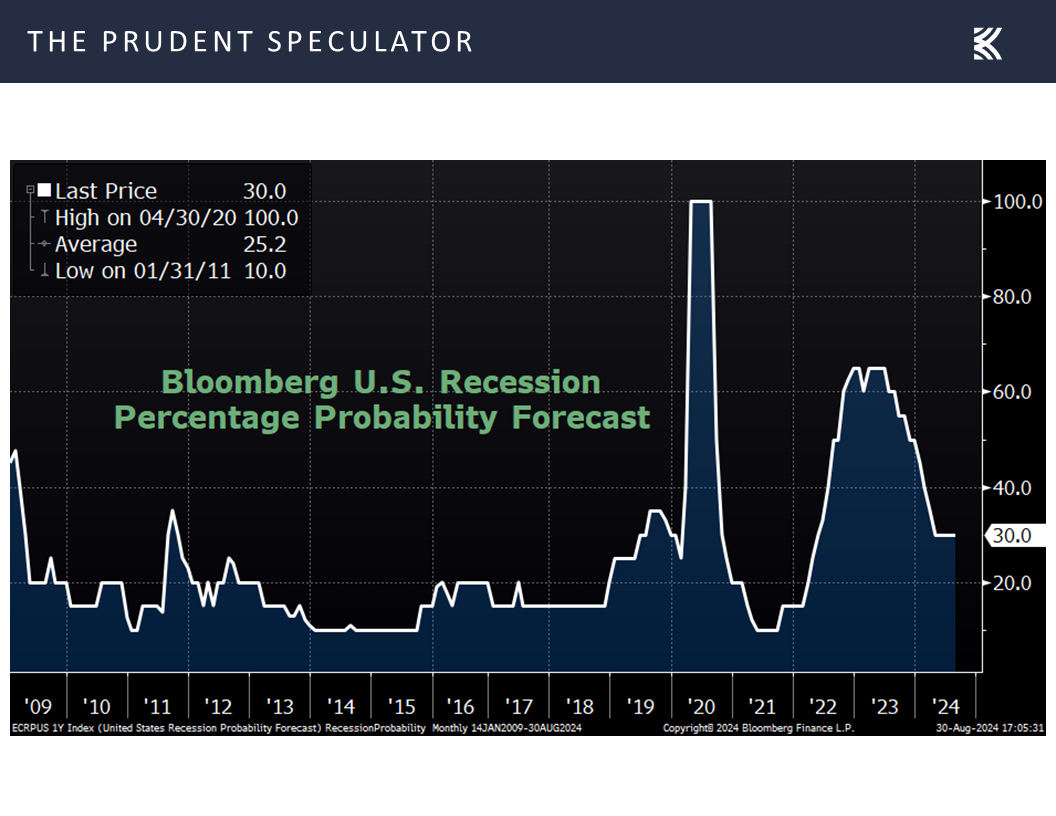

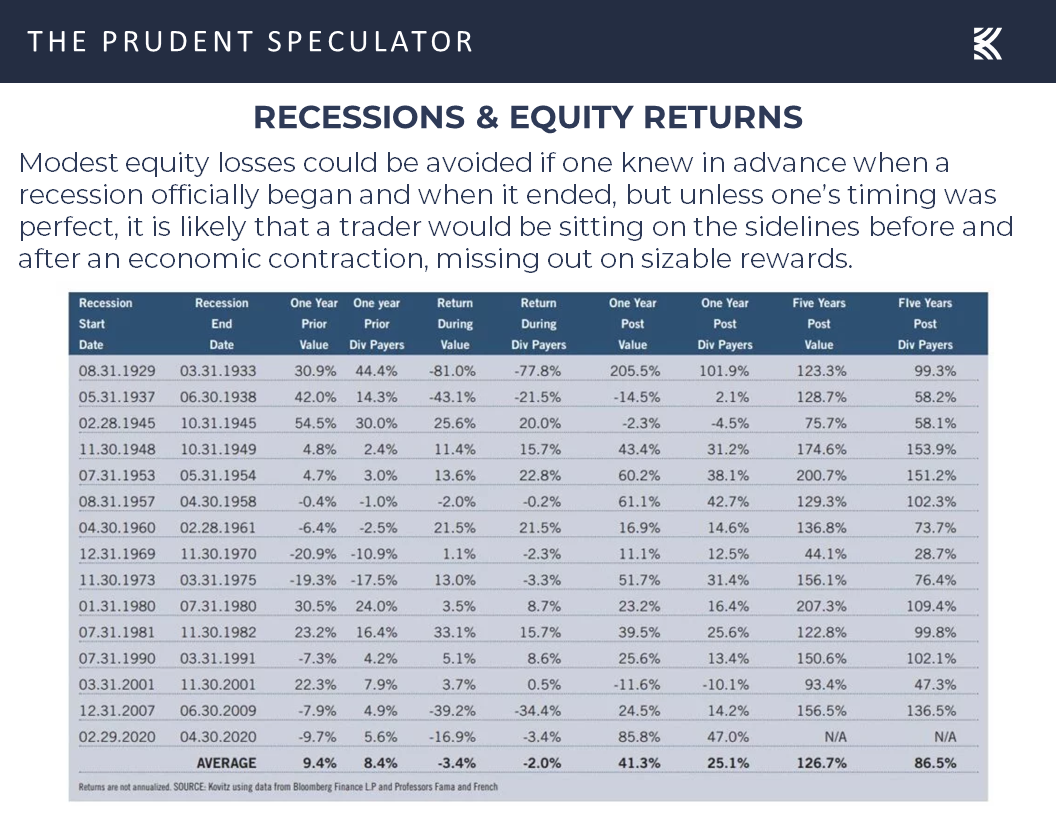

Certainly, we respect that many will continue to worry that a recession is still on the horizon, even as the odds of such an occurrence remain low,

and history argues that one would have to have perfect timing to avoid equity market losses during an economic contraction AND not miss the massive rebound in stock prices that have occurred, on average, coming out of recessions.

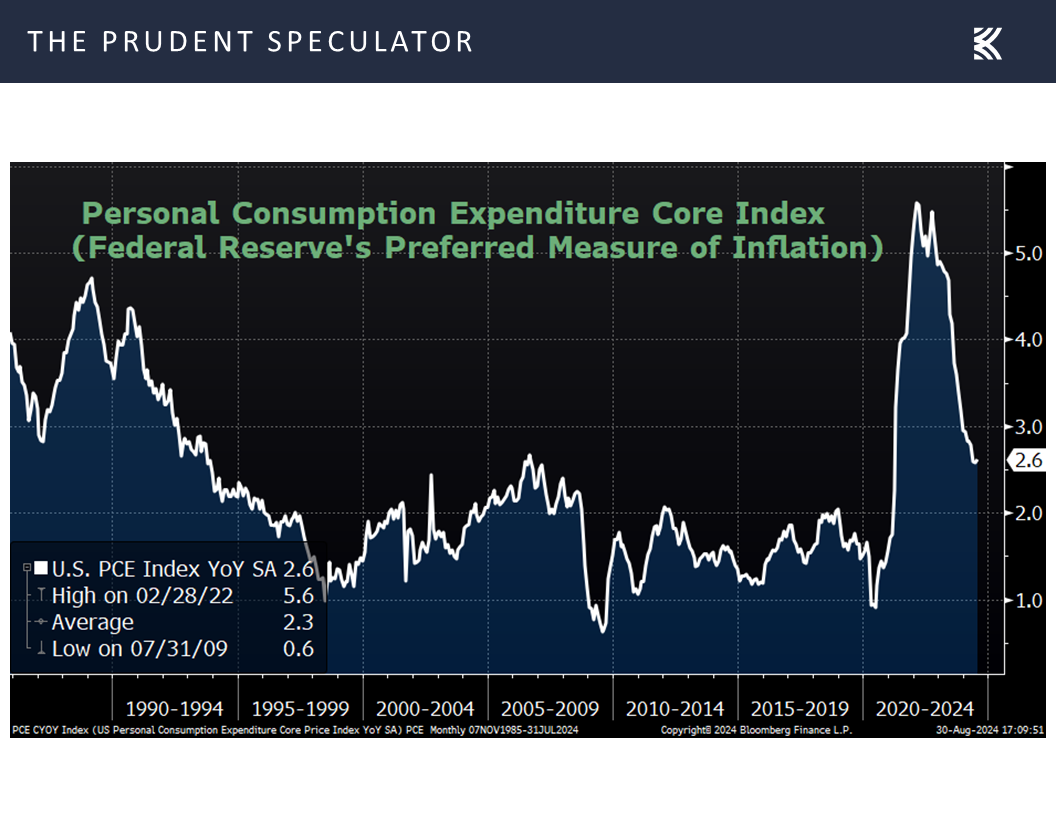

Even more important last week on the economic docket was the release of the Federal Reserve’s preferred gauge of inflation. The Core Personal Consumption Expenditure (PCE) index came in at a 2.6% increase in July, better than the consensus forecast of 2.7% and in line with June’s reading.

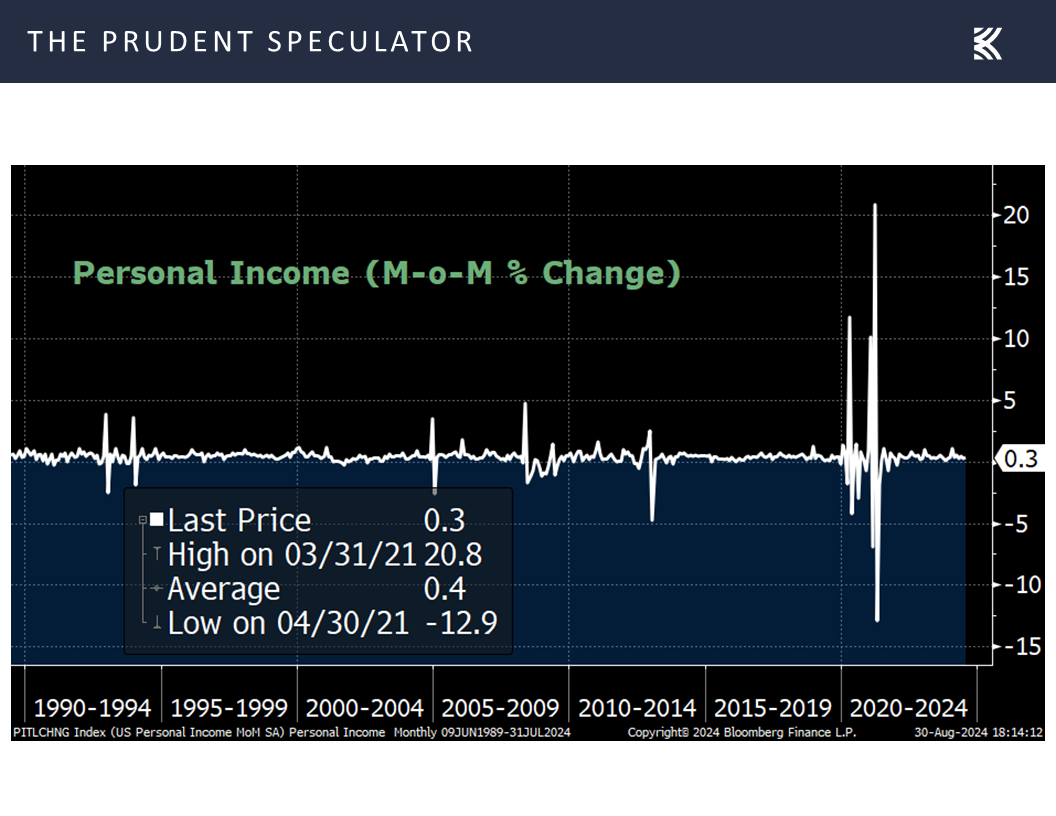

Personal incomes in July,

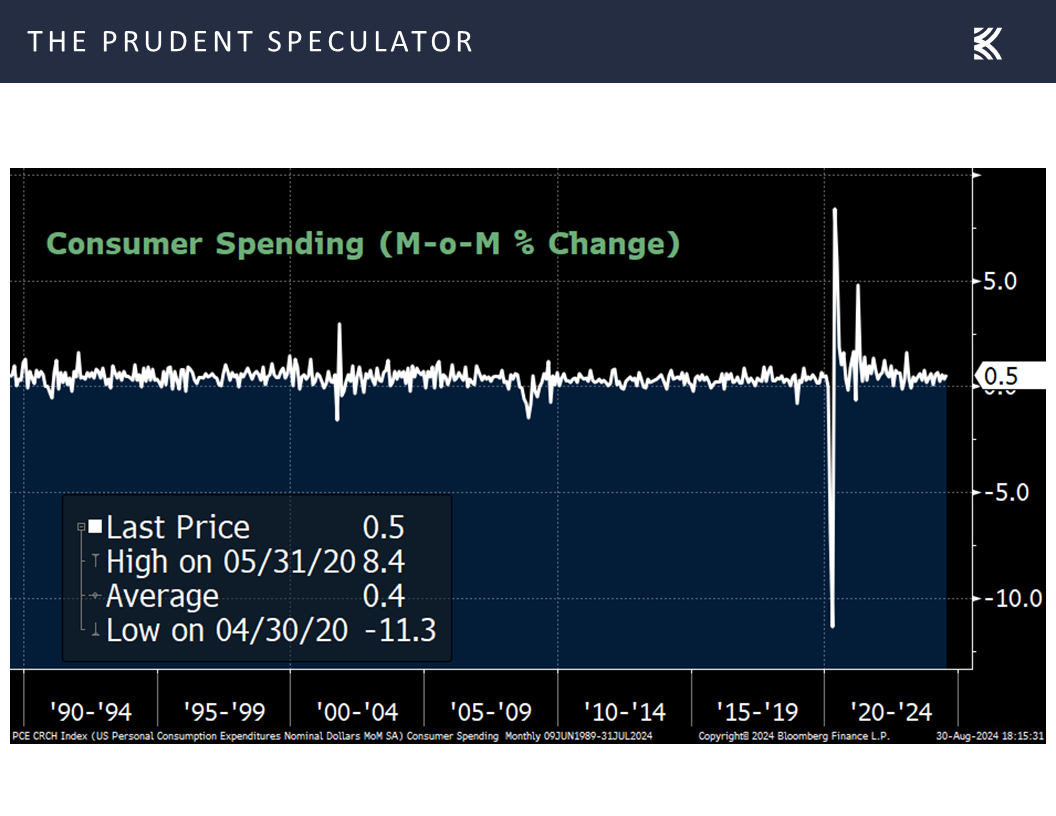

and consumer spending still held up well,

Corporate Profits – Solid EPS Growth Remains the Forecast

both of which suggest that corporate profit growth should remain decent,

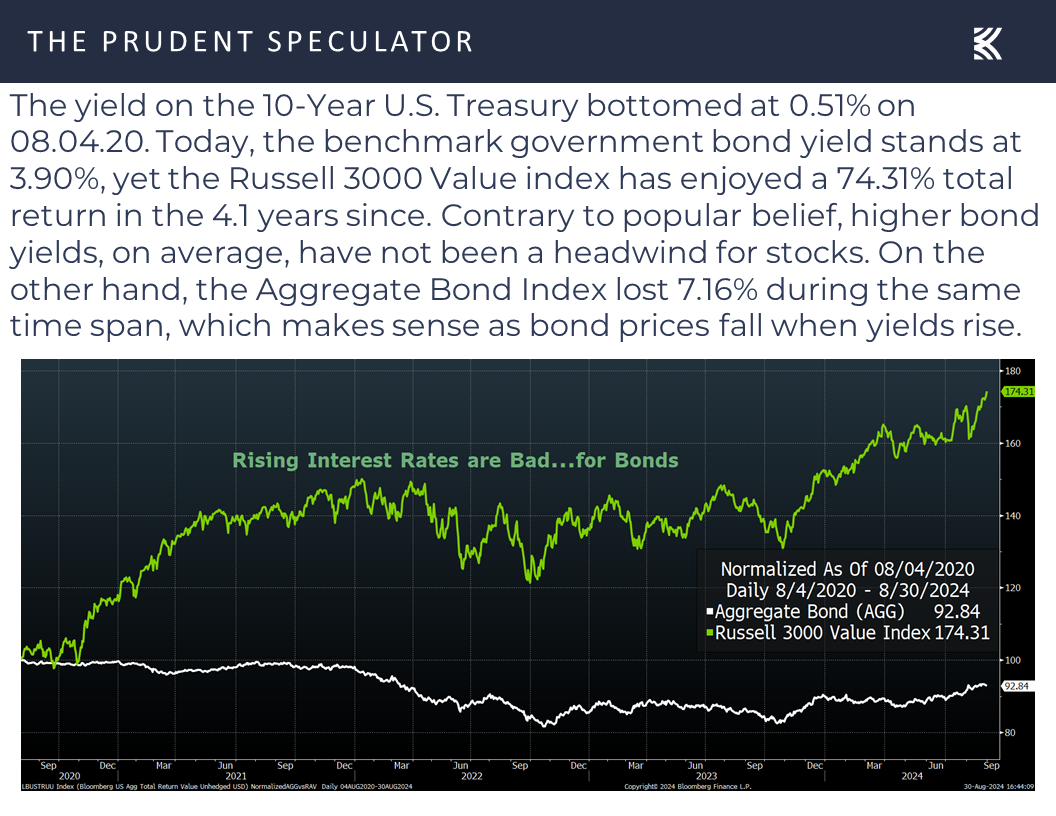

Interest Rates – Fed Cuts Coming; Stocks Have Performed Well Whether Rates Rise or Fall

especially considering that the financial markets are betting on a series of cuts in the Fed Funds rate from Jerome H. Powell & Co. starting later this month.

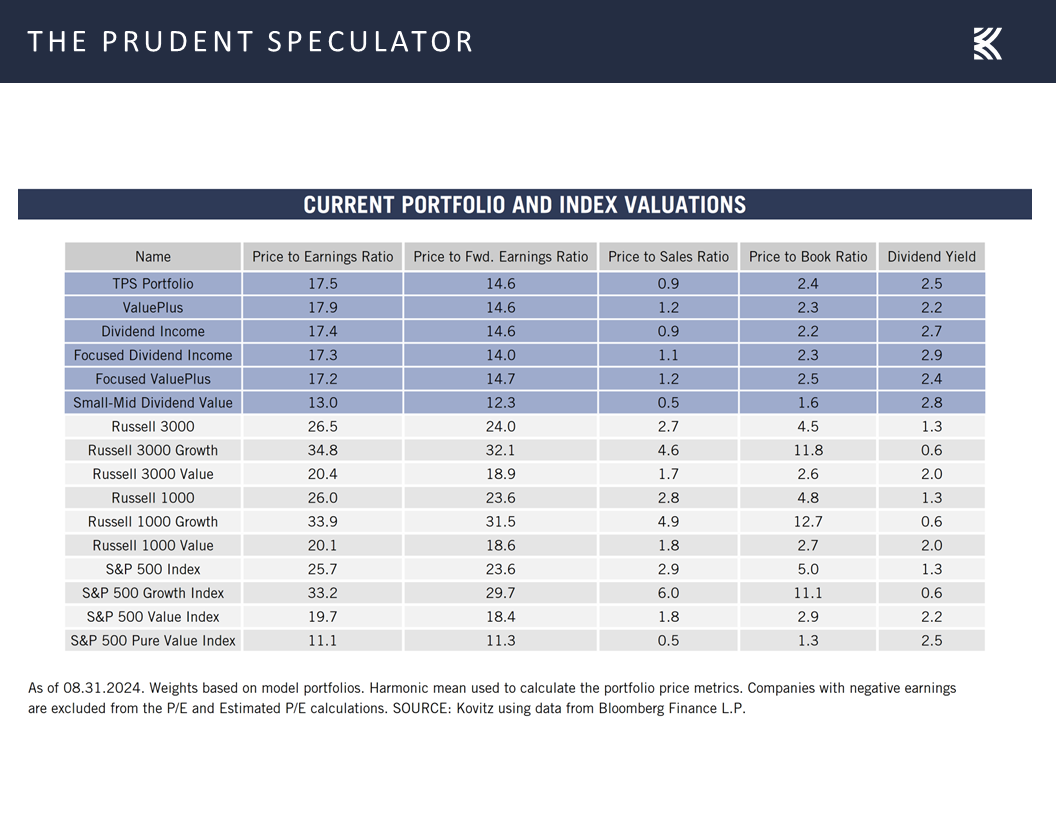

Valuations – Value Remains Attractive

No doubt, lower interest rates add to the appeal of equities on both an earnings- and dividend-yield standpoint,

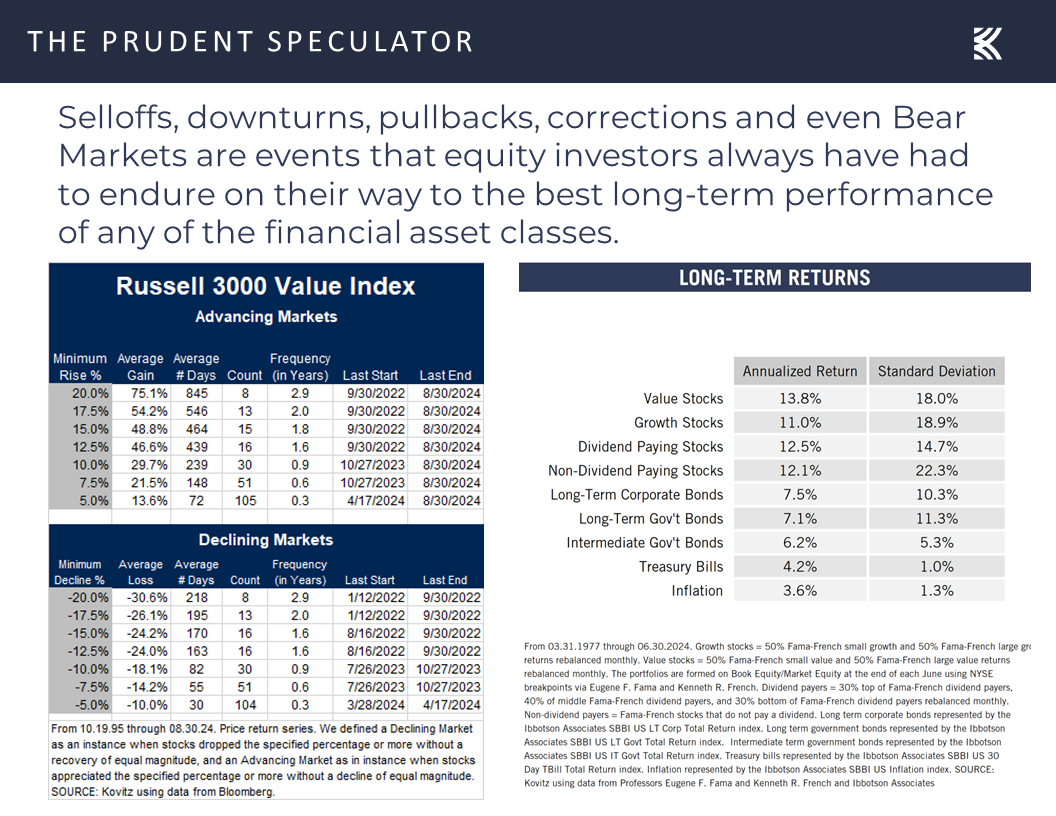

Market History – Volatility & Disconcerting Headlines Through the Years but Long-Term Trend for Stocks is Up

but history shows one would not want to sell stocks even if rates were rising,

with the returns on Value stocks vs. bonds over the last four-plus years vividly illustrating the point.

Not surprisingly, we remain optimistic about the long-term prospects of our broadly diversified portfolios of what we believe are undervalued stocks,

even as we are always braced for downside volatility, given that 5% dips happen three times per year, on average, and 10% corrections occur every 11 months.

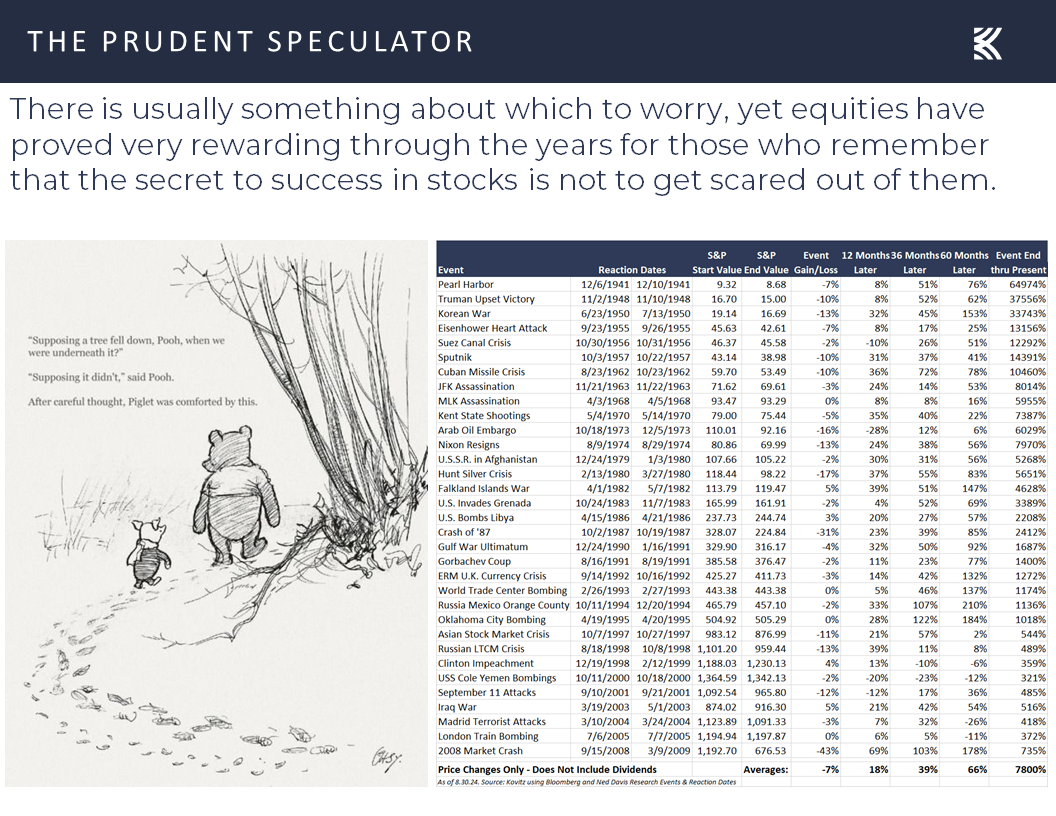

We also know that events on the geopolitical stage are a wildcard, but history shows that patience always has been rewarded in the fullness of time,

Sentiment – AAII Bullish

while even the heightened level of enthusiasm for stocks we are witnessing today on Main Street,

does not suggest that a downturn is imminent.

Stock News – Updates on four stocks across two different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Market Rebound, Corporate Profits, Interest Rates and AAII Sentiment

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Market Rebound, Corporate Profits, Interest Rates and AAII Sentiment. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Market Rebound – Big Bounce off the Siegel Low Continues

Econ Outlook – Soft Landing Still Seems Likely

Inflation – PCE Continuing to Trend in a Good Direction

Corporate Profits – Solid EPS Growth Remains the Forecast

Interest Rates – Fed Cuts Coming; Stocks Have Performed Well Whether Rates Rise or Fall

Valuations – Value Remains Attractive

Market History – Volatility & Disconcerting Headlines Through the Years but Long-Term Trend for Stocks is Up

Sentiment – AAII Bullish

Stock News – Updates on FL, JWN, KSS & NTAP

Market Rebound – Big Bounce off the Siegel Low Continues

The equity market rebound off of the “Siegel Meltdown” lows of August 5 continued last week with stocks moving modestly higher on the week and sending the Dow Jones Industrial Average to a gain of more than 7% in the 19 days since,

the heretofore even-keeled author of the long-term-oriented-investor bible, Stocks for the Long Run, temporarily lost his mind in calling for an emergency Fed rate cut of 75 basis points in reaction to a couple of weaker-than-expected economic statistics.

Happily, the Wizard of Wharton quickly came to his senses in the days that followed, as the negative message that would have been sent by an emergency rate cut by the data-dependent Fed would likely have sent stocks plunging in the short run and potentially dragged the economy down in the process.

Econ Outlook – Soft Landing Still Seems Likely

Obviously, the subsequent data could have confirmed that the weaker-than-expected monthly labor report for July, which saw 114,000 new payrolls created (hardly a horrible figure),

and disappointing July ISM Manufacturing number (at a level that historically has been a major buy signal, on average, for stocks),

were signals that the so-called “soft-landing” economic outlook that was projected by Federal Reserve Board members and Federal Reserve Bank presidents back in June was not likely to occur.

Of course, the economic numbers since have argued that the economy is continuing to hold up well, with last week’s data seeing an uptick in the estimate of real (inflation-adjusted) Q2 U.S. GDP growth to a healthy 3.0%,

and the Atlanta Fed boosting its forecast for real Q3 U.S. GDP growth to a solid 2.5%.

To be sure, not all of the stats last week were robust as orders for durable goods excluding the volatile transportation sector declined by a worse-than-expected 0.2% in July,

while the University of Michigan’s Consumer Sentiment gauge for August trailed expectations with a historically low reading of 67.9.

On the other hand, the Conference Board’s measure of Consumer Confidence for August rose to a better-than-estimated 103.3, versus expectations of 100.8 and July’s revised tally of 101.9,

while first-time filings for unemployment benefits continued to reside near multi-generational lows.

Inflation – PCE Continuing to Trend in a Good Direction

Certainly, we respect that many will continue to worry that a recession is still on the horizon, even as the odds of such an occurrence remain low,

and history argues that one would have to have perfect timing to avoid equity market losses during an economic contraction AND not miss the massive rebound in stock prices that have occurred, on average, coming out of recessions.

Even more important last week on the economic docket was the release of the Federal Reserve’s preferred gauge of inflation. The Core Personal Consumption Expenditure (PCE) index came in at a 2.6% increase in July, better than the consensus forecast of 2.7% and in line with June’s reading.

Personal incomes in July,

and consumer spending still held up well,

Corporate Profits – Solid EPS Growth Remains the Forecast

both of which suggest that corporate profit growth should remain decent,

Interest Rates – Fed Cuts Coming; Stocks Have Performed Well Whether Rates Rise or Fall

especially considering that the financial markets are betting on a series of cuts in the Fed Funds rate from Jerome H. Powell & Co. starting later this month.

Valuations – Value Remains Attractive

No doubt, lower interest rates add to the appeal of equities on both an earnings- and dividend-yield standpoint,

Market History – Volatility & Disconcerting Headlines Through the Years but Long-Term Trend for Stocks is Up

but history shows one would not want to sell stocks even if rates were rising,

with the returns on Value stocks vs. bonds over the last four-plus years vividly illustrating the point.

Not surprisingly, we remain optimistic about the long-term prospects of our broadly diversified portfolios of what we believe are undervalued stocks,

even as we are always braced for downside volatility, given that 5% dips happen three times per year, on average, and 10% corrections occur every 11 months.

We also know that events on the geopolitical stage are a wildcard, but history shows that patience always has been rewarded in the fullness of time,

Sentiment – AAII Bullish

while even the heightened level of enthusiasm for stocks we are witnessing today on Main Street,

does not suggest that a downturn is imminent.

Stock News – Updates on four stocks across two different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.