The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss profit taking, interest rates, corporate profits, valuations and more econ news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – 5 Buys Across Four Accounts

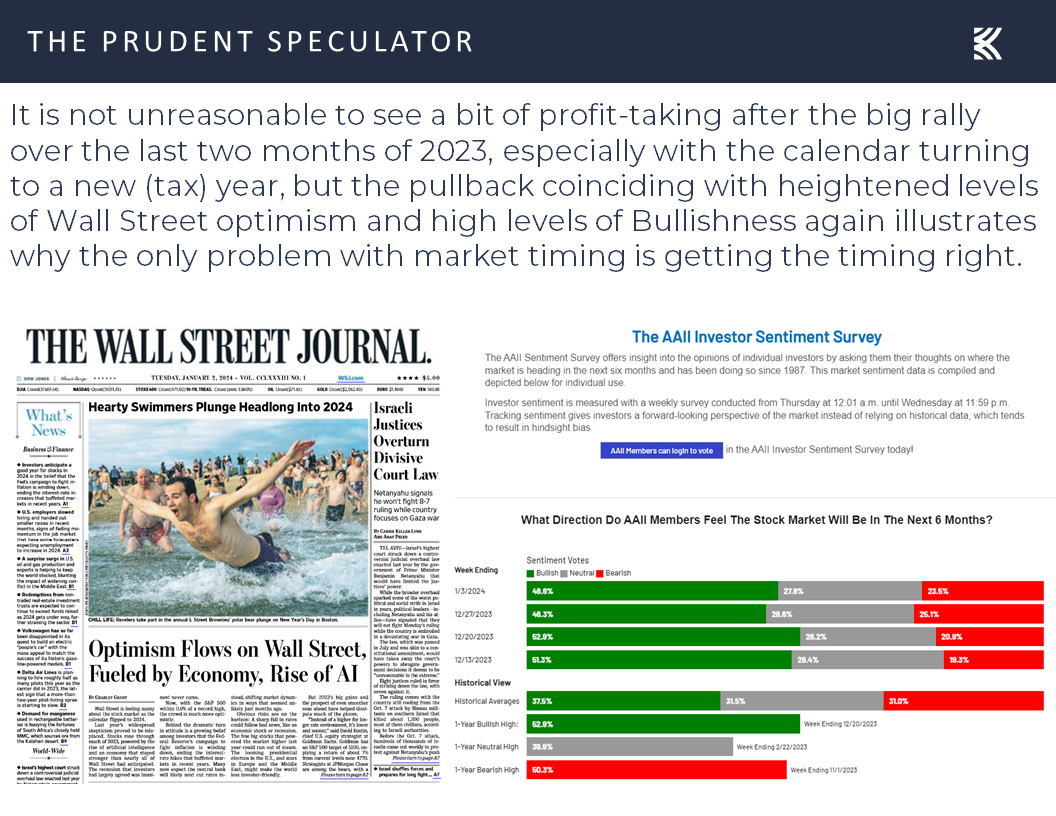

Sentiment – Lots of Optimism as ’24 Gets Underway

Profit Taking – Value Outperforms, but Stocks Pull Back

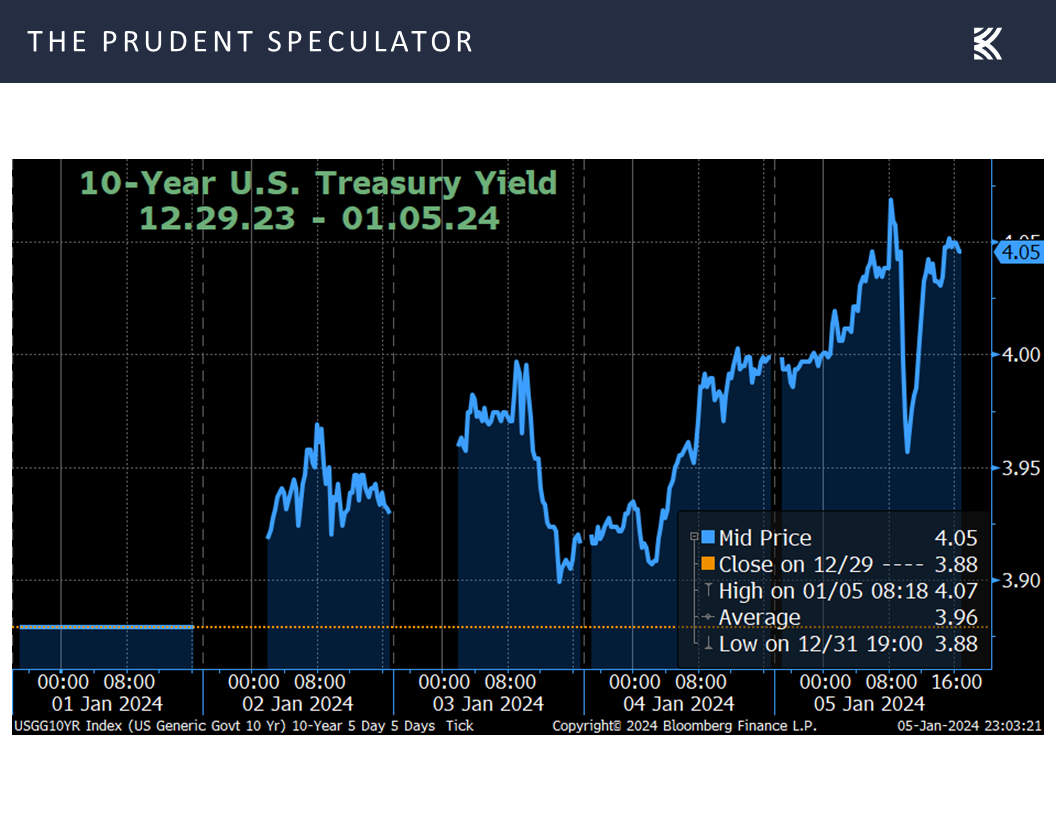

Interest Rates – Yields Rise

Econ News – Solid Jobs Report but ISM’s Suggest No or Modest Growth

Corporate Profits – EPS Expected to Grow in ’24

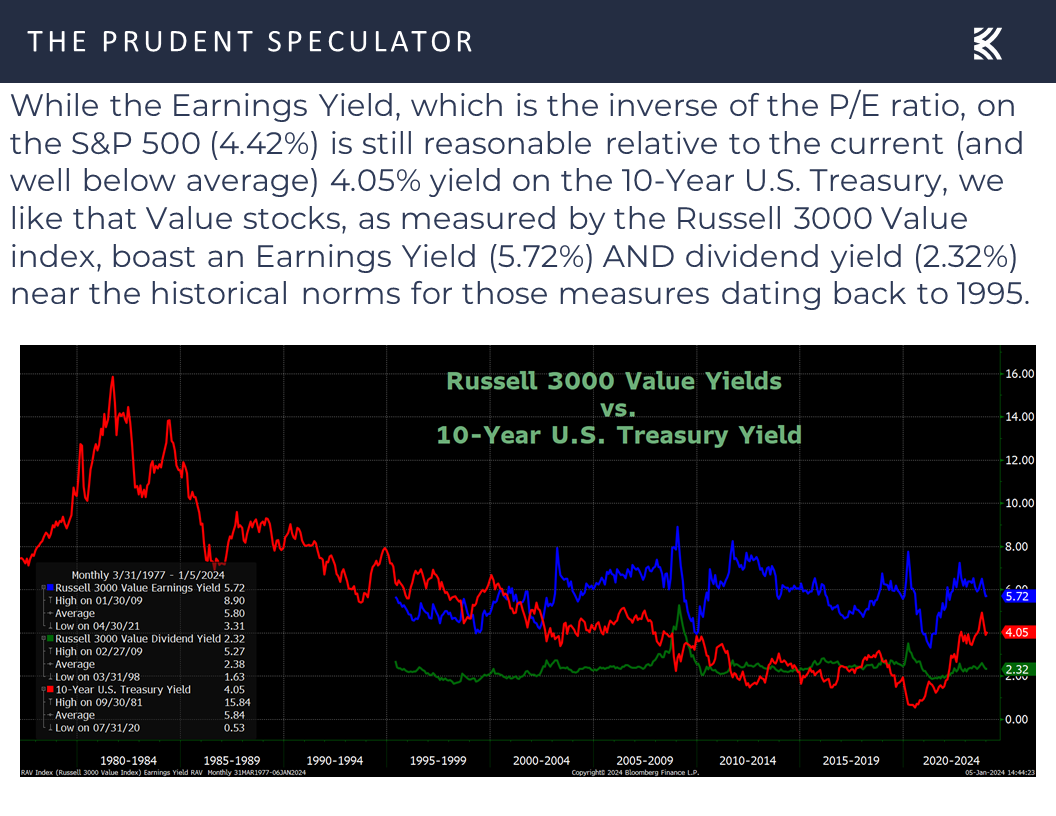

Valuations – Value Stocks Still Reasonably Priced

Stock News – Updates on GBX and ’24 First-Week Winners & Losers

Sentiment – Lots of Optimism as ’24 Gets Underway

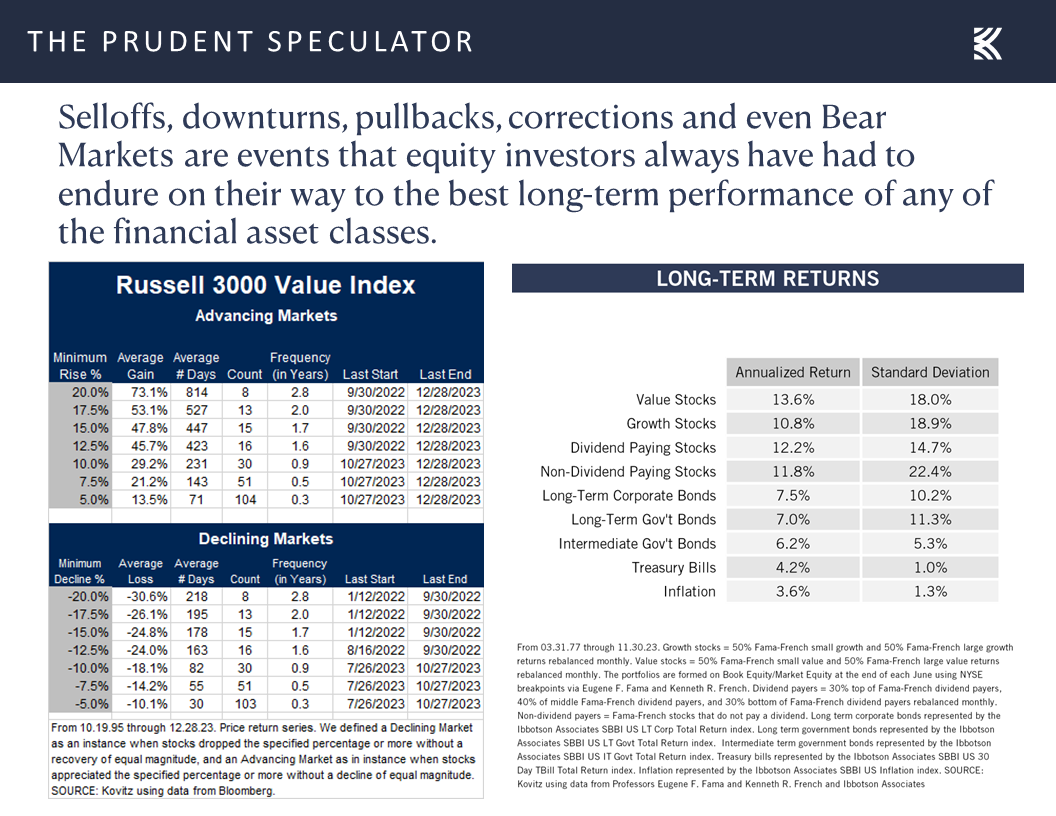

Although we were pleased to see Value outperform Growth by a wide margin, the first week of trading in 2024 saw the major equity market averages end decidedly in the red. Of course, stocks had marched rapidly higher since the recent October 27 lows, and volatility is a normal part of the investment process, so we can’t say we are surprised by the modest retreat.

Profit Taking – Value Outperforms, but Stocks Pull Back

Still, we suspect that many will blame the decline on the elevated levels of enthusiasm for stocks from market participants as the new year began,

Interest Rates – Yields Rise

Aside from what we would argue was many folks waiting until January to sell a few stocks, so as not to realize outsized gains in late-December, it would seem that the culprit for the red ink last week was a jump in interest rates,

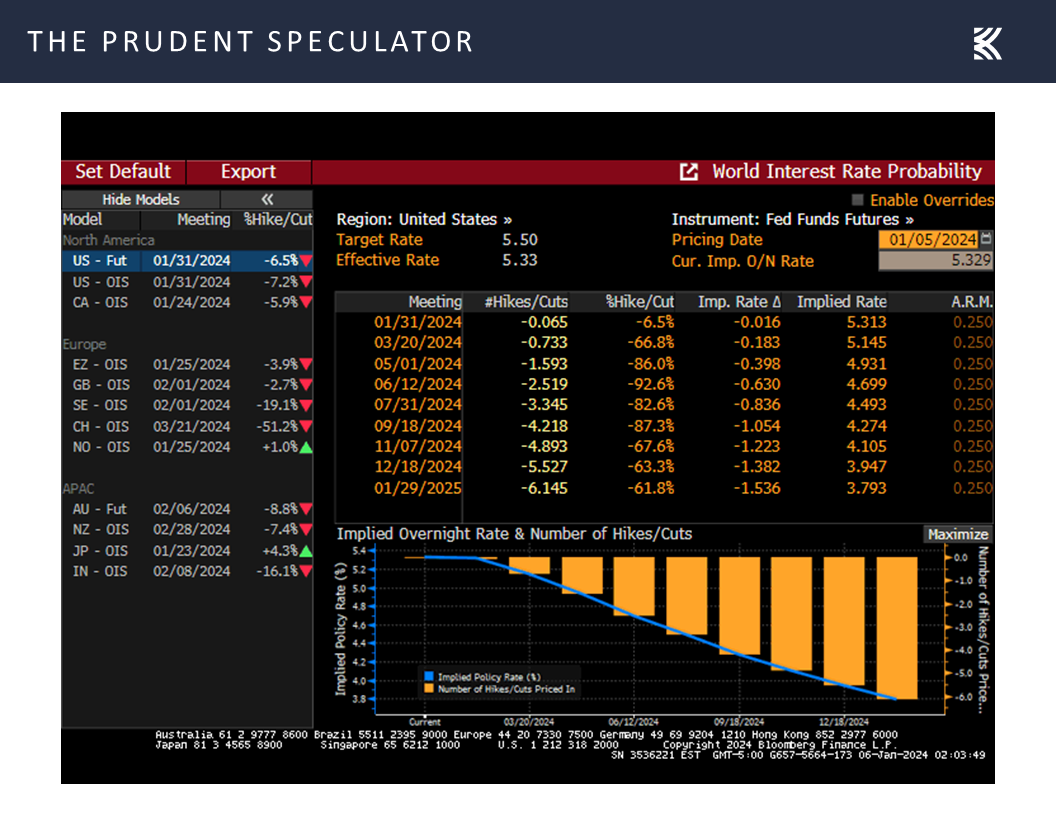

as traders rejiggered their thinking on the timing and number of cuts likely in the Fed Funds rate this year. The latest betting in the futures market now suggests a 67% chance that the first reduction in the benchmark U.S. central bank lending rate will occur in March, with the expected year-end Fed Funds rate now standing at 3.95%. One week ago, those respective figures were 84% and 3.75%.

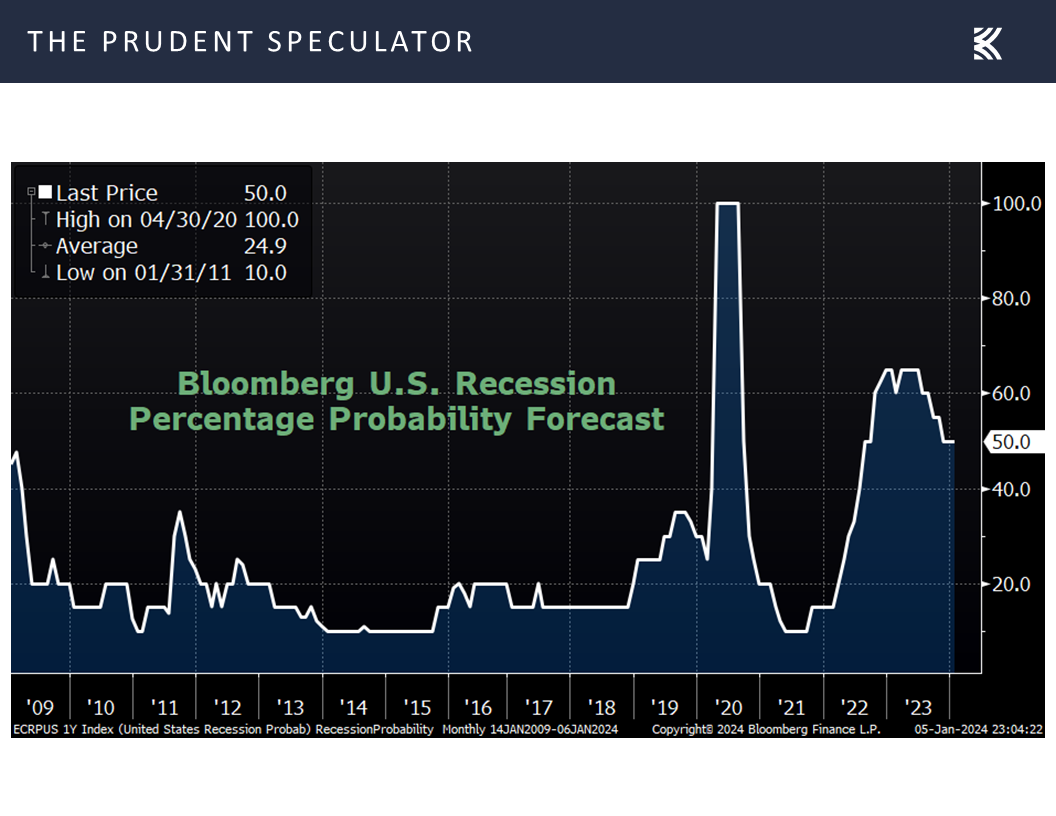

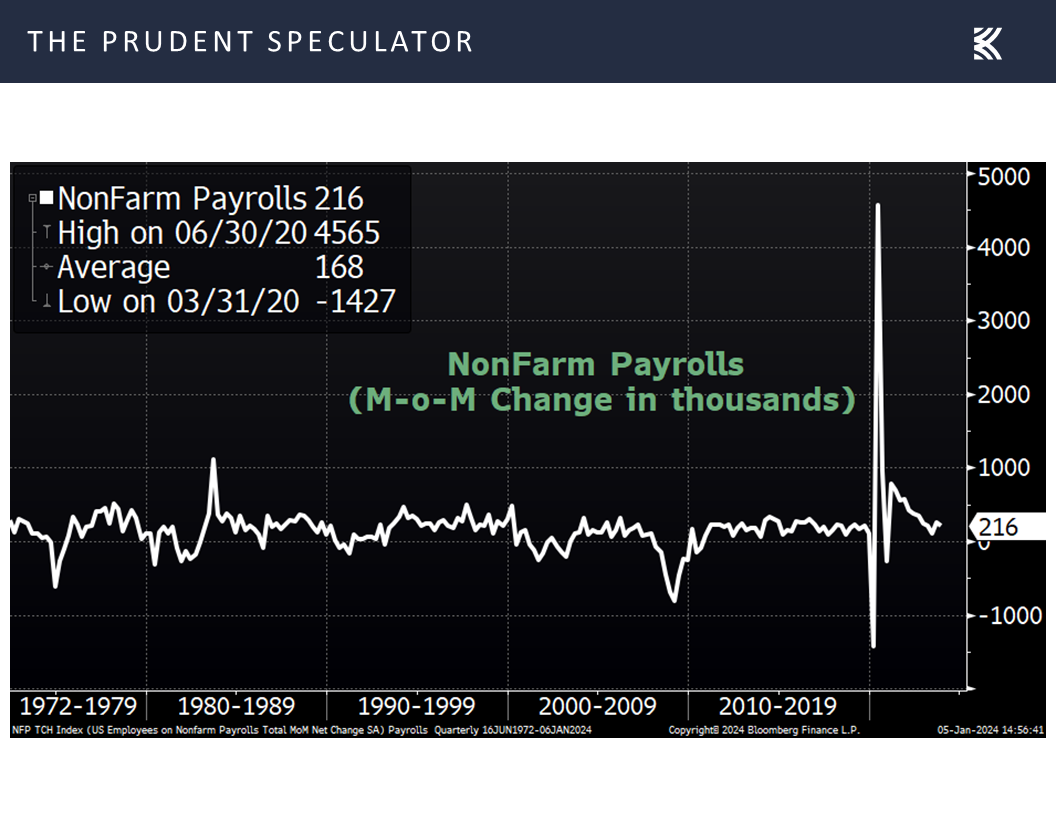

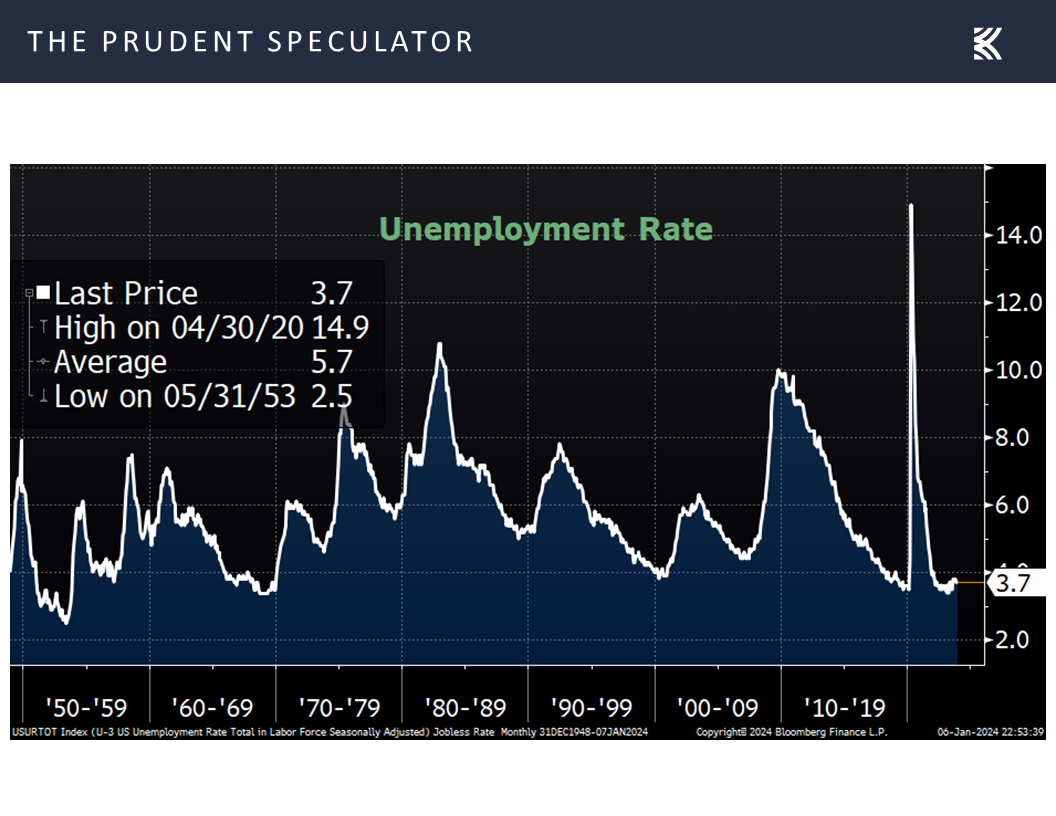

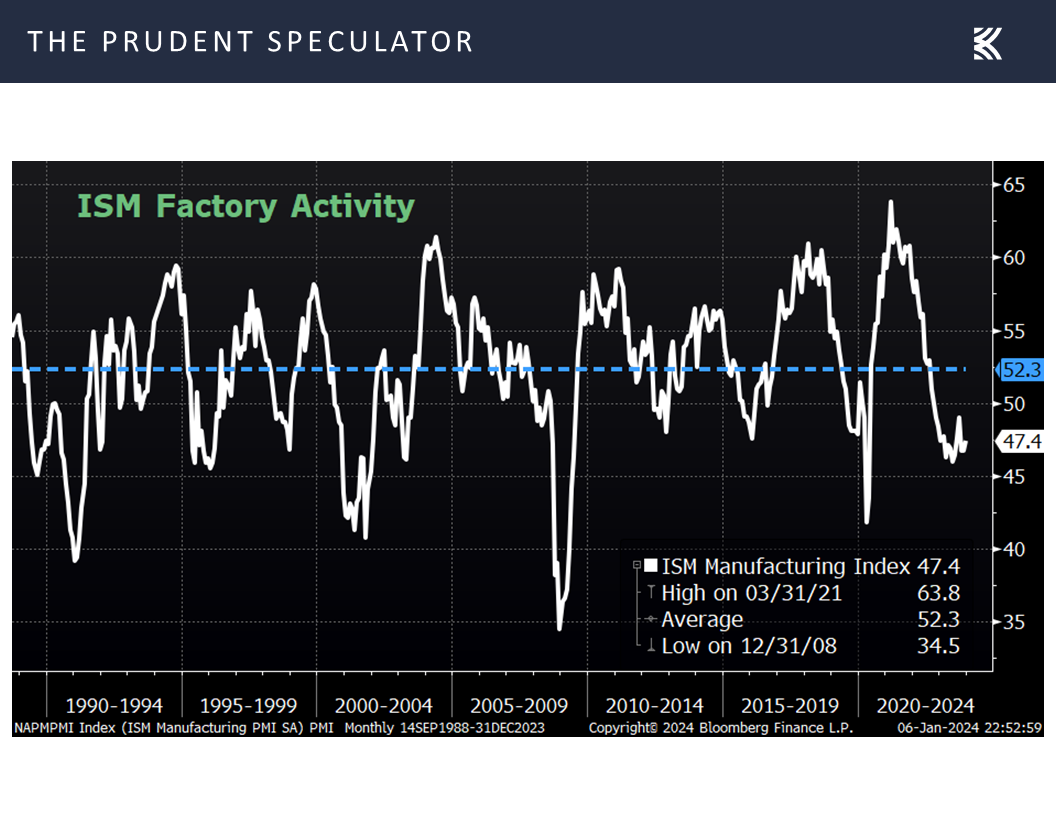

Econ News – Solid Jobs Report but ISM’s Suggest No or Modest Growth

No doubt, even as the odds of recession in the next 12 months as calculated by Bloomberg remained at 50%,

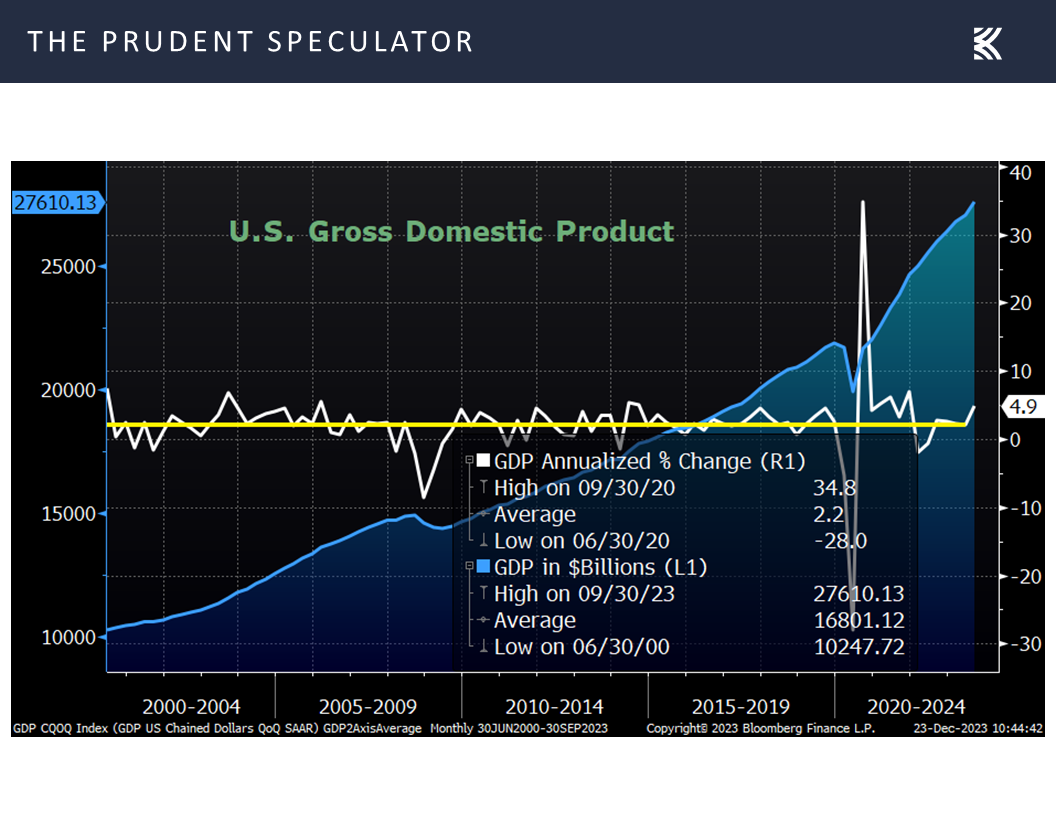

an improvement last week in the Q4 real (inflation-adjusted) GDP outlook from the Atlanta Fed to 2.5%,

and a better-than-expected monthly jobs report,

with the unemployment rate holding steady in December at a slightly better-than-estimated 3.7% had many rethinking how loose the Federal Reserve will be with monetary policy in the near term.

Of course, we are not unhappy to see the overall economy holding up reasonably well, especially as the December read on the health of the factory sector from the Institute for Supply Management (ISM) came in at 47.4, up from 46.7 in November but corresponding to a change of minus-0.5 percent in real gross domestic product on an annualized basis, per historical correlations.

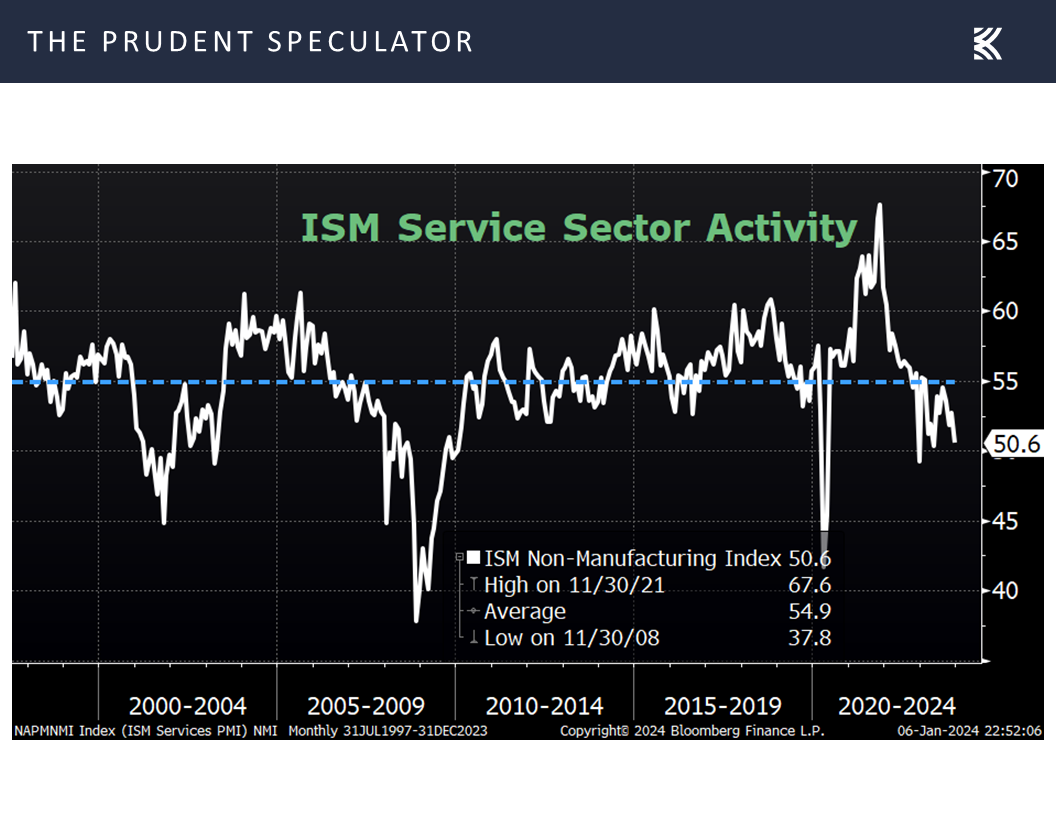

ISM’s report on conditions in the important services sector retreated to 50.6 in December, down from 52.7 the month prior. Per ISM, “The past relationship between the Services PMI and the overall economy indicates that the Services PMI for December corresponds to a 0.3-percent increase in real gross domestic product on an annualized basis.”

Certainly, there are plenty of question marks about the strength of the economy this year, but when is there ever certainty? What we do know is that over time, both real and nominal GDP have grown,

Corporate Profits – EPS Expected to Grow in ’24

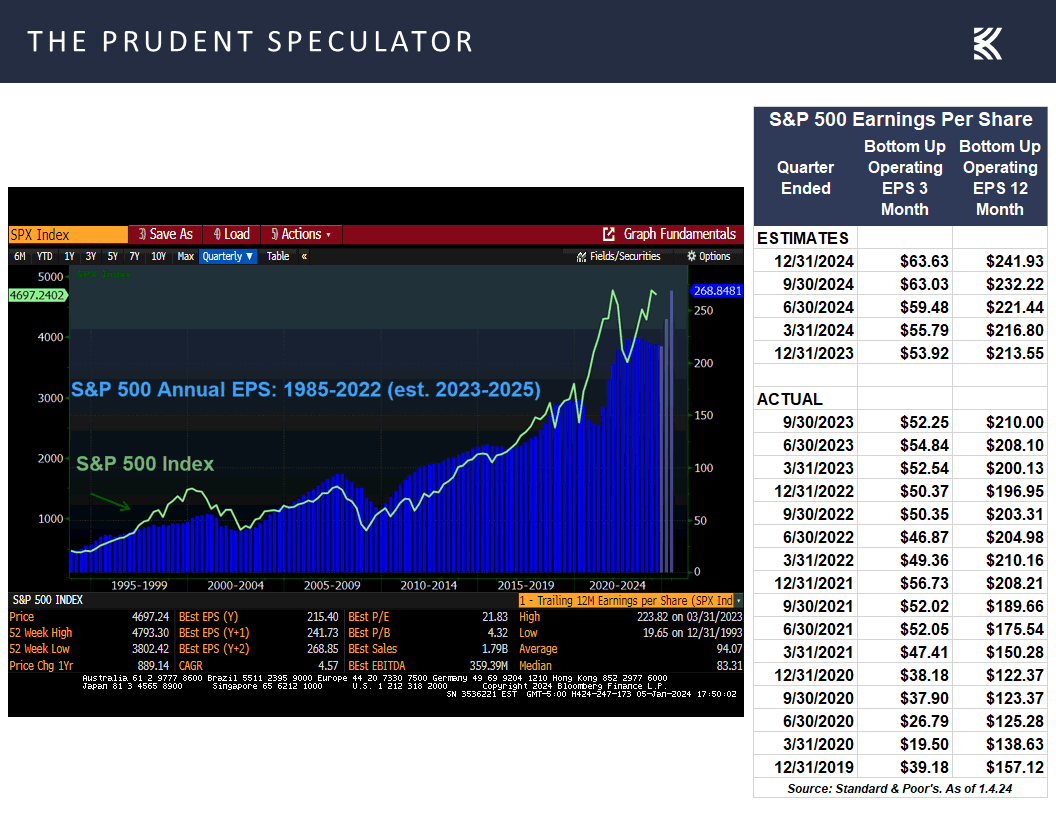

while most remain of the mind that corporate profits will show solid growth in 2024,

the achievement of which, we think, supports the valuation argument for Value stocks in general,

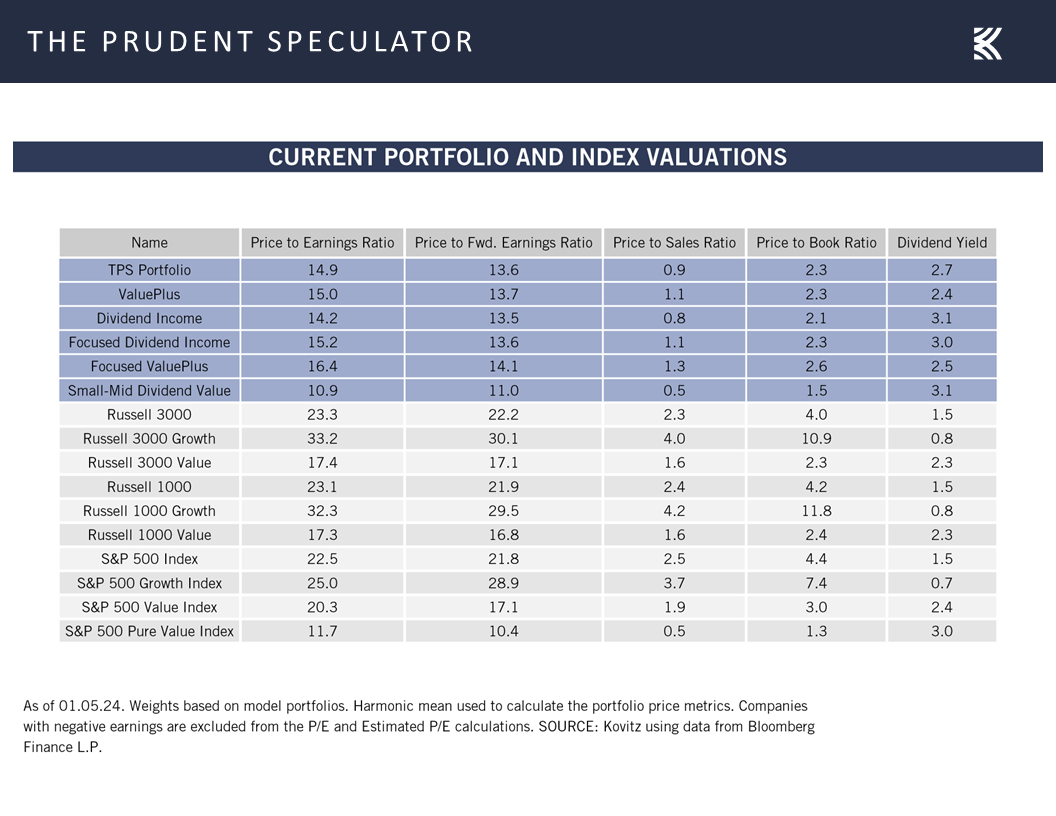

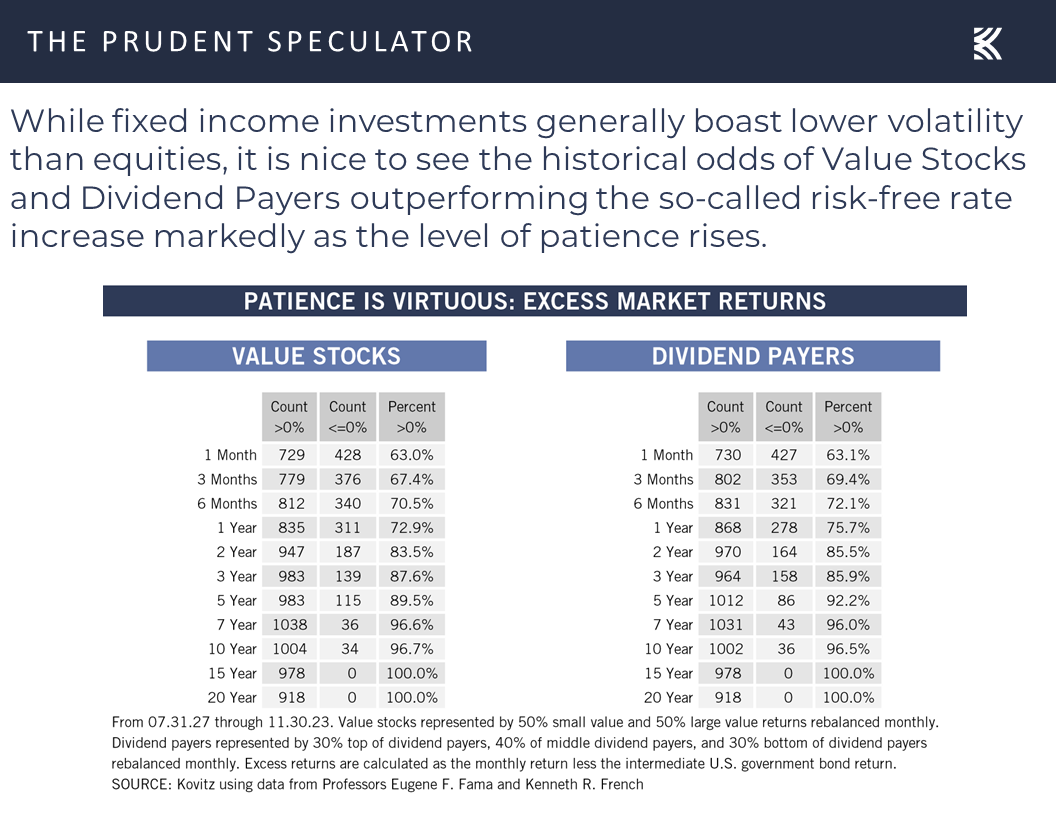

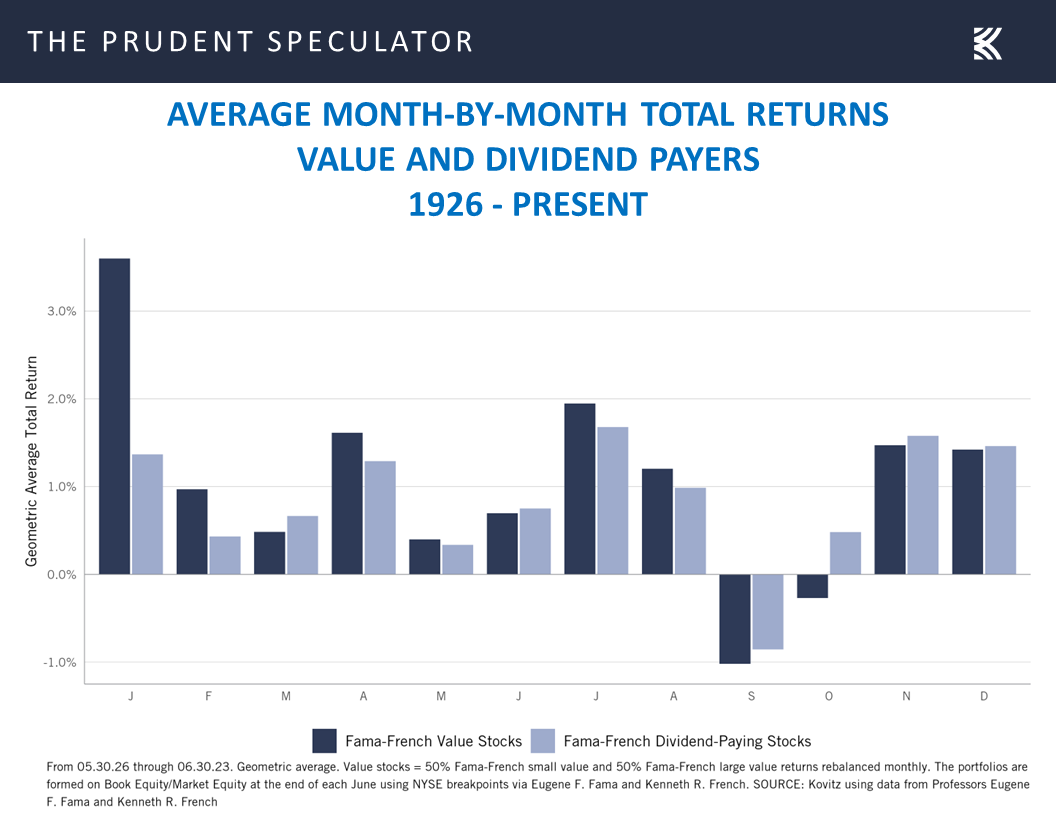

Valuations – Value Stocks Still Reasonably Priced

and our broadly diversified portfolios of what we believe to be undervalued stocks in particular.

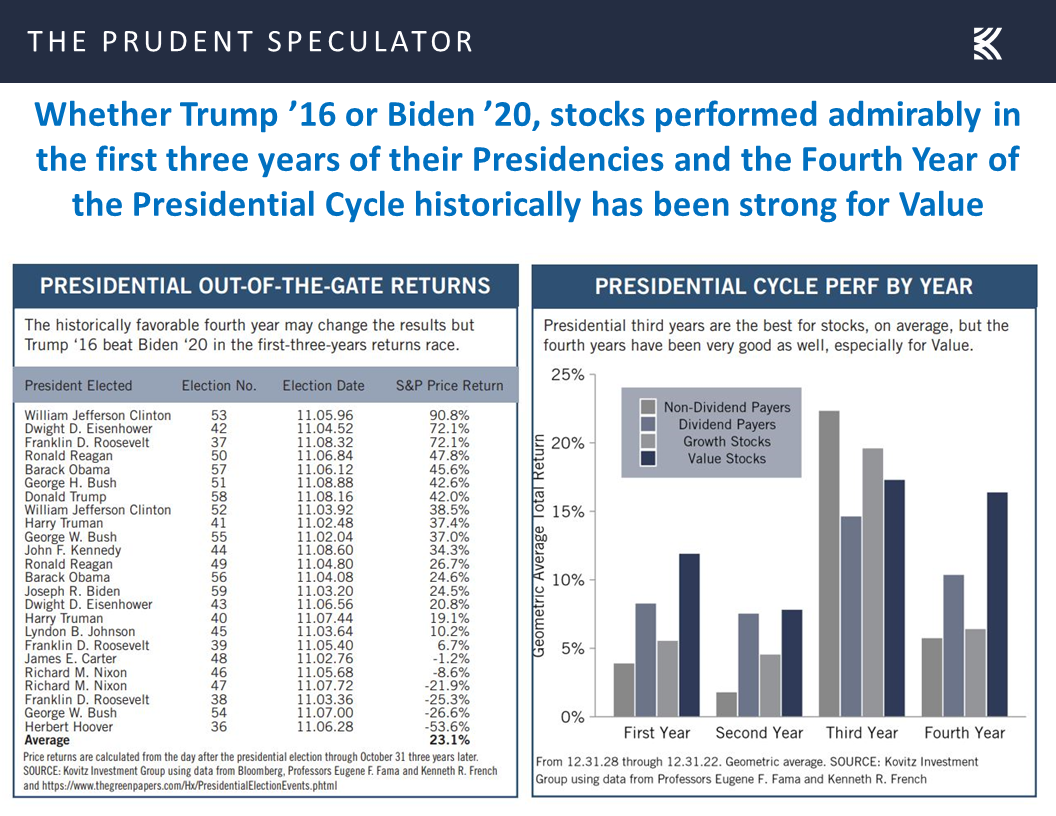

True, anything can happen in the short run, but the long-term probabilities very much favor equities continuing to provide handsome rewards,

while we now reside in the seasonally more favorable six months of the year,

and the Fourth Year of the Presidency historically has seen Value stocks enjoy terrific returns, on average.

Stock News – Updates Greenbrier Companies, Inc. (GBX) and ’24 First-Week Winners and Losers

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Profit Taking, Interest Rates, Corporate Profits, Valuations and more Econ News

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss profit taking, interest rates, corporate profits, valuations and more econ news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – 5 Buys Across Four Accounts

Sentiment – Lots of Optimism as ’24 Gets Underway

Profit Taking – Value Outperforms, but Stocks Pull Back

Interest Rates – Yields Rise

Econ News – Solid Jobs Report but ISM’s Suggest No or Modest Growth

Corporate Profits – EPS Expected to Grow in ’24

Valuations – Value Stocks Still Reasonably Priced

Stock News – Updates on GBX and ’24 First-Week Winners & Losers

Sentiment – Lots of Optimism as ’24 Gets Underway

Although we were pleased to see Value outperform Growth by a wide margin, the first week of trading in 2024 saw the major equity market averages end decidedly in the red. Of course, stocks had marched rapidly higher since the recent October 27 lows, and volatility is a normal part of the investment process, so we can’t say we are surprised by the modest retreat.

Profit Taking – Value Outperforms, but Stocks Pull Back

Still, we suspect that many will blame the decline on the elevated levels of enthusiasm for stocks from market participants as the new year began,

Interest Rates – Yields Rise

Aside from what we would argue was many folks waiting until January to sell a few stocks, so as not to realize outsized gains in late-December, it would seem that the culprit for the red ink last week was a jump in interest rates,

as traders rejiggered their thinking on the timing and number of cuts likely in the Fed Funds rate this year. The latest betting in the futures market now suggests a 67% chance that the first reduction in the benchmark U.S. central bank lending rate will occur in March, with the expected year-end Fed Funds rate now standing at 3.95%. One week ago, those respective figures were 84% and 3.75%.

Econ News – Solid Jobs Report but ISM’s Suggest No or Modest Growth

No doubt, even as the odds of recession in the next 12 months as calculated by Bloomberg remained at 50%,

an improvement last week in the Q4 real (inflation-adjusted) GDP outlook from the Atlanta Fed to 2.5%,

and a better-than-expected monthly jobs report,

with the unemployment rate holding steady in December at a slightly better-than-estimated 3.7% had many rethinking how loose the Federal Reserve will be with monetary policy in the near term.

Of course, we are not unhappy to see the overall economy holding up reasonably well, especially as the December read on the health of the factory sector from the Institute for Supply Management (ISM) came in at 47.4, up from 46.7 in November but corresponding to a change of minus-0.5 percent in real gross domestic product on an annualized basis, per historical correlations.

ISM’s report on conditions in the important services sector retreated to 50.6 in December, down from 52.7 the month prior. Per ISM, “The past relationship between the Services PMI and the overall economy indicates that the Services PMI for December corresponds to a 0.3-percent increase in real gross domestic product on an annualized basis.”

Certainly, there are plenty of question marks about the strength of the economy this year, but when is there ever certainty? What we do know is that over time, both real and nominal GDP have grown,

Corporate Profits – EPS Expected to Grow in ’24

while most remain of the mind that corporate profits will show solid growth in 2024,

the achievement of which, we think, supports the valuation argument for Value stocks in general,

Valuations – Value Stocks Still Reasonably Priced

and our broadly diversified portfolios of what we believe to be undervalued stocks in particular.

True, anything can happen in the short run, but the long-term probabilities very much favor equities continuing to provide handsome rewards,

while we now reside in the seasonally more favorable six months of the year,

and the Fourth Year of the Presidency historically has seen Value stocks enjoy terrific returns, on average.

Stock News – Updates Greenbrier Companies, Inc. (GBX) and ’24 First-Week Winners and Losers

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.