The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss interest rates, valuations, inflation, AAII Sentiment and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

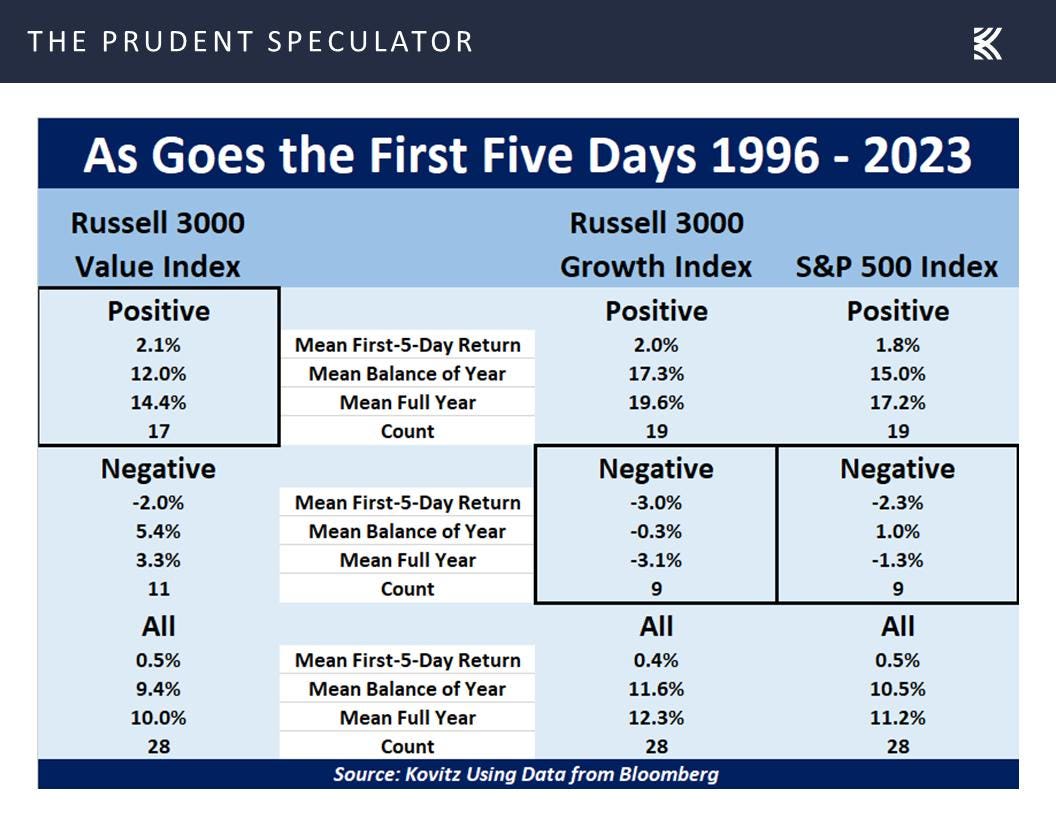

First Five Days of the Year – Value Positive; Growth & S&P 500 Negative

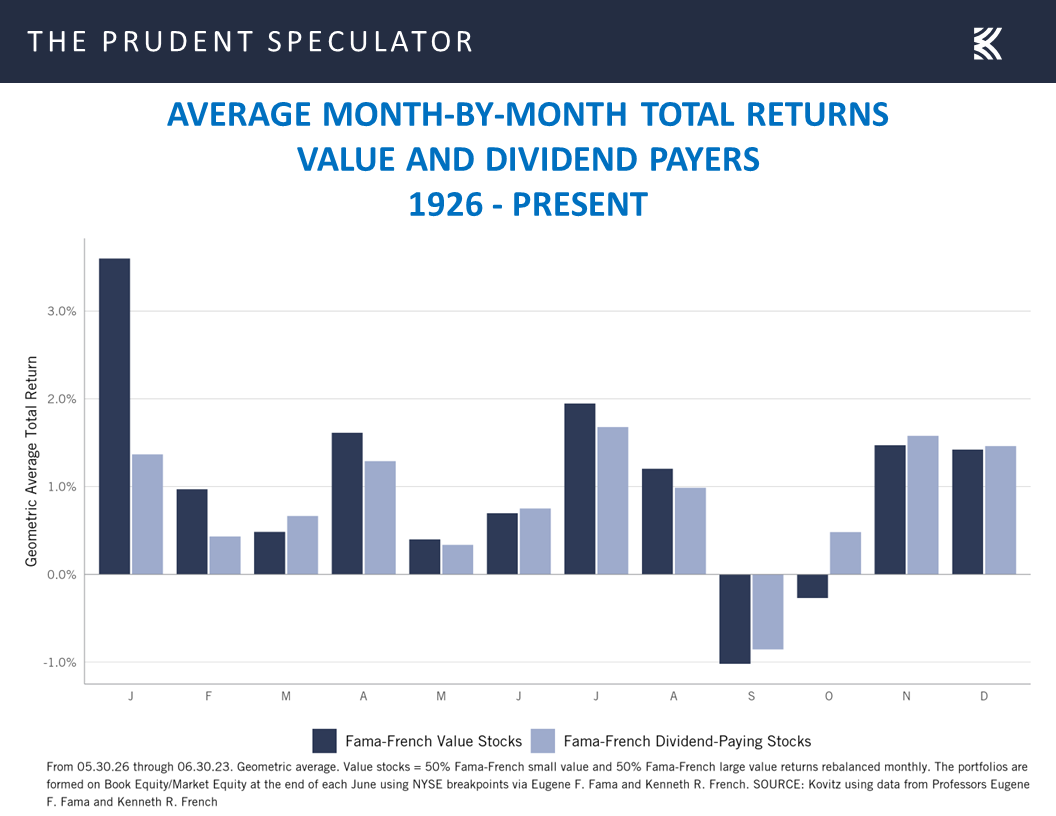

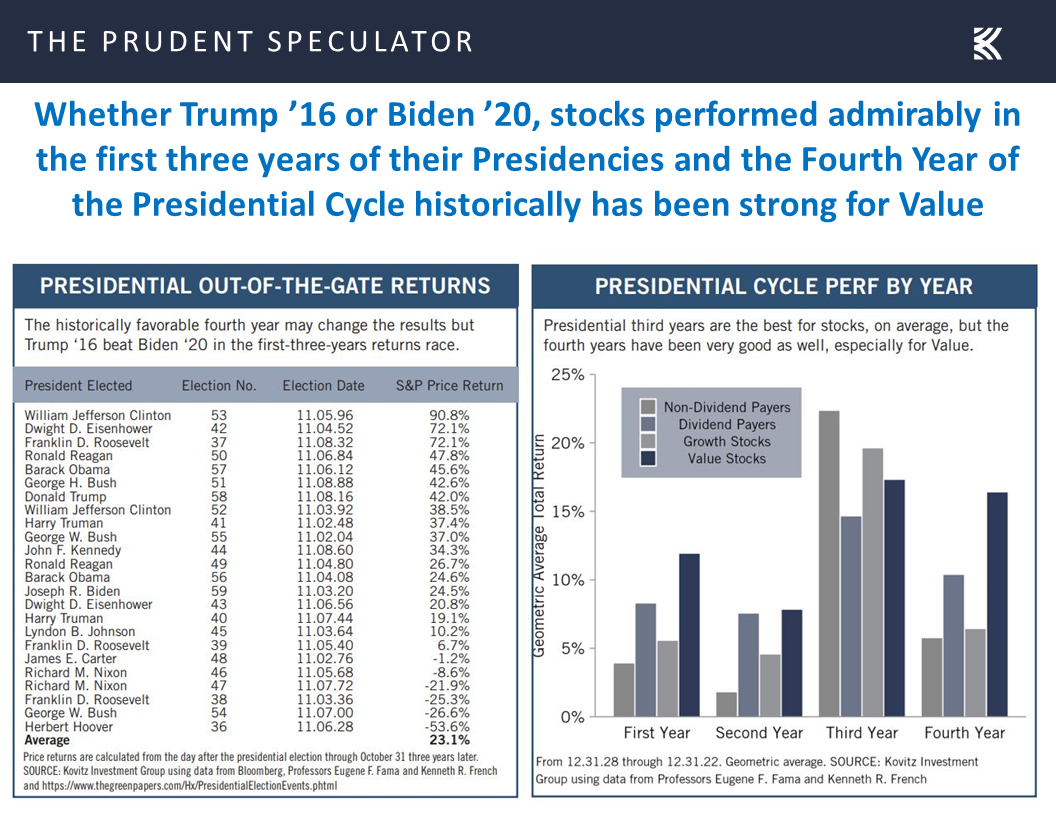

Calendar – Numbers Support Value

Interest Rates – Fed Funds Futures and 10-Year Yields Move Lower

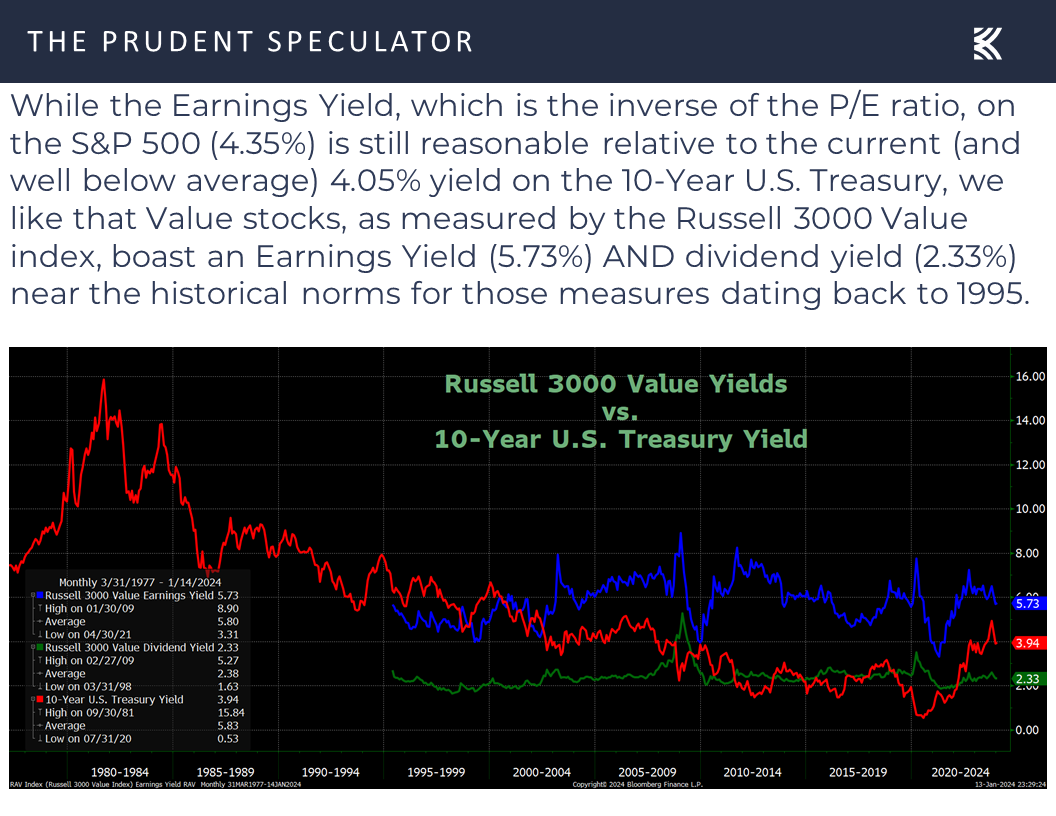

Valuations – Value Stocks Still Reasonably Priced

Inflation – December Data Mixed, But CPI & PPI Headed in the Right Direction

Sentiment – Lots of Optimism as ’24 Gets Underway

Stock News – Updates on eight stocks across four different sectors

First Five Days of the Year – Value Positive; Growth & S&P 500 Negative

It was a tough five days for Value stocks relative to growth, with the Value indexes all in the red for the week ended January 12, but this past Monday’s big rally carried the Russell 3000 Value index into the green by 0.25% for the first five days of the trading year, whereas the Growth Indexes, S&P 500 and Dow Jones Industrial Average all were in the red for the year at the close on January 8.

Although many would argue that there is little in the way of predictive significance to the First Five Days of the Year, we aren’t unhappy that the Russell Value and Growth indexes show interesting statistics. True, there is just 28 years in the dataset as daily data for the Russell style indexes did not begin until mid-1995, but the 17 previous times the First Five Days were positive for the Russell 3000 Value index, the mean return for the balance of the year was 14.4%. Contrast this to the 9 times the Russell 3000 Growth index and S&P 500 were negative, where the mean return for the balance of the year was -0.3% and 1.0%, respectively.

Calendar – Numbers Support Value

Happily, there are other statistical factors in support of the near-term prospects for Value, including the average returns for January, February and April,

and the Fourth Year of the Presidency,

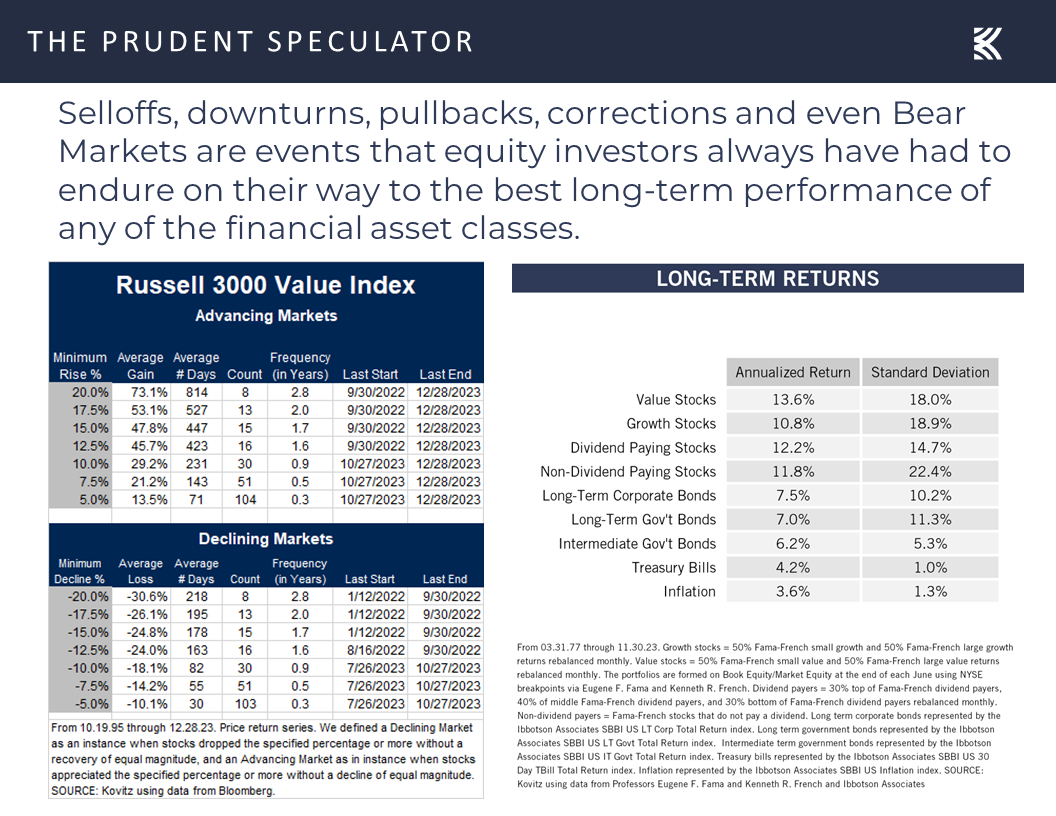

while the long-term evidence since the launch of The Prudent Speculator nearly 47 year ago favors the kind of companies that we have long championed,

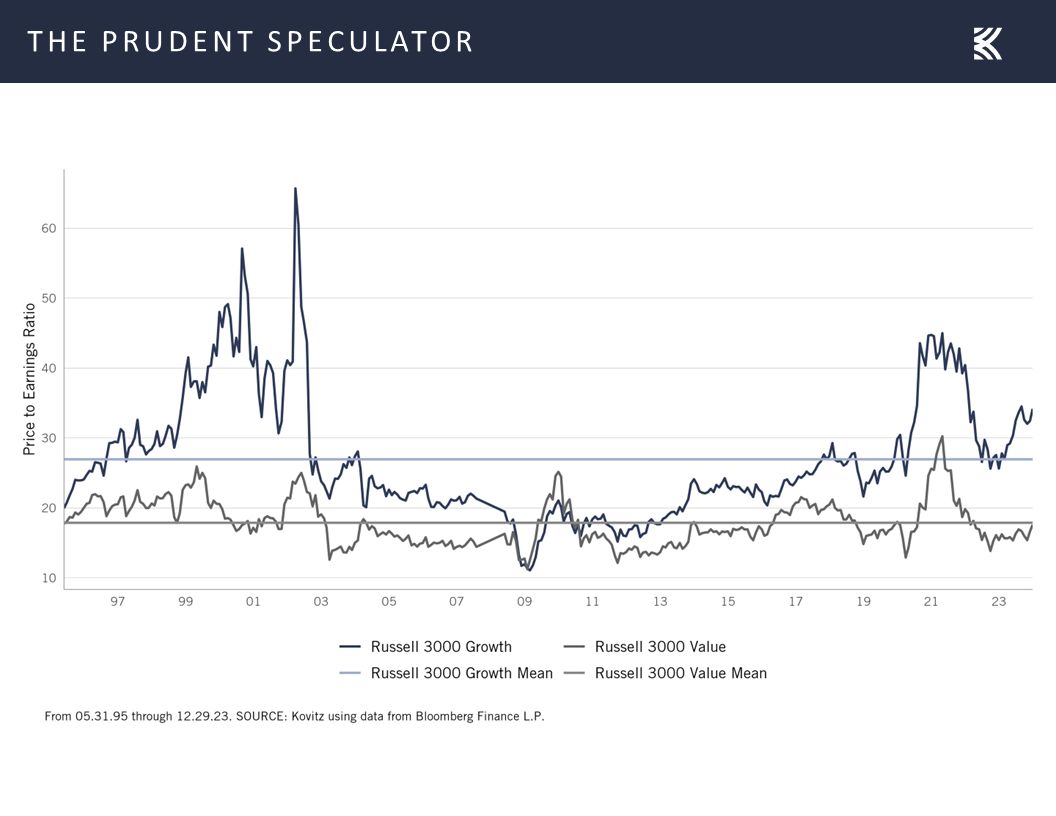

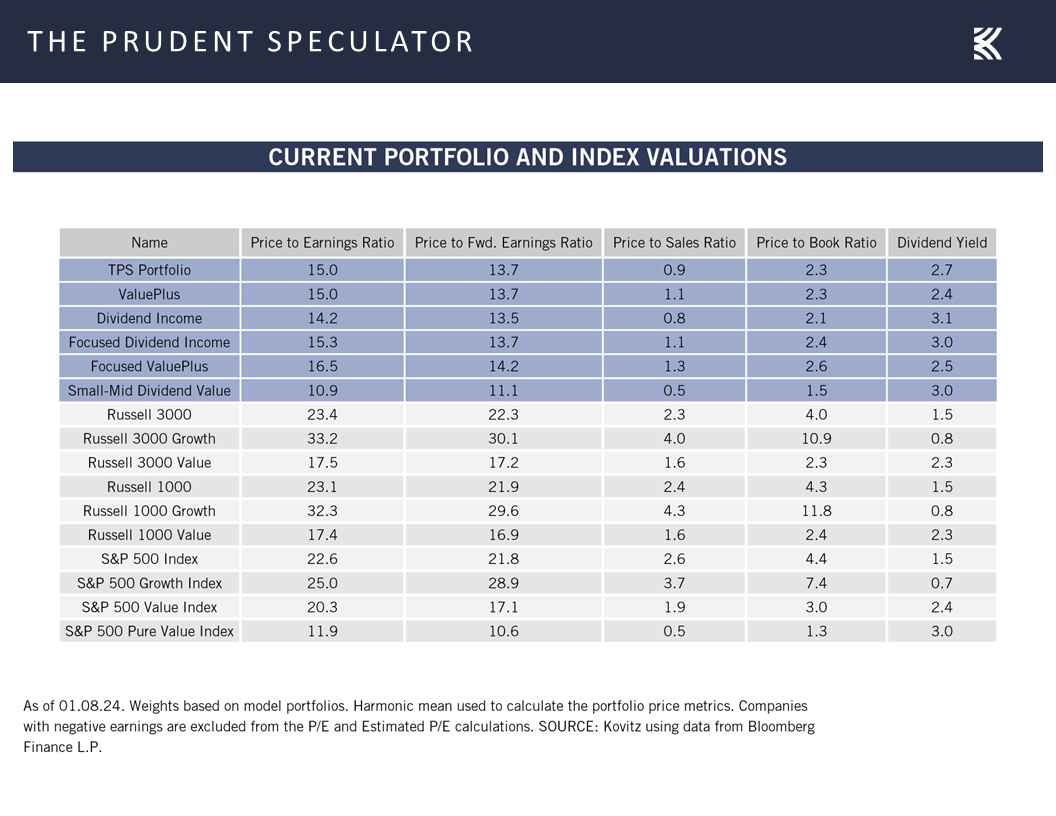

and inexpensively priced stocks today are far less expensive on an earnings basis to their 28-year norms than their more-richly valued peers.

Interest Rates – Fed Funds Futures and 10-Year Yields Move Lower

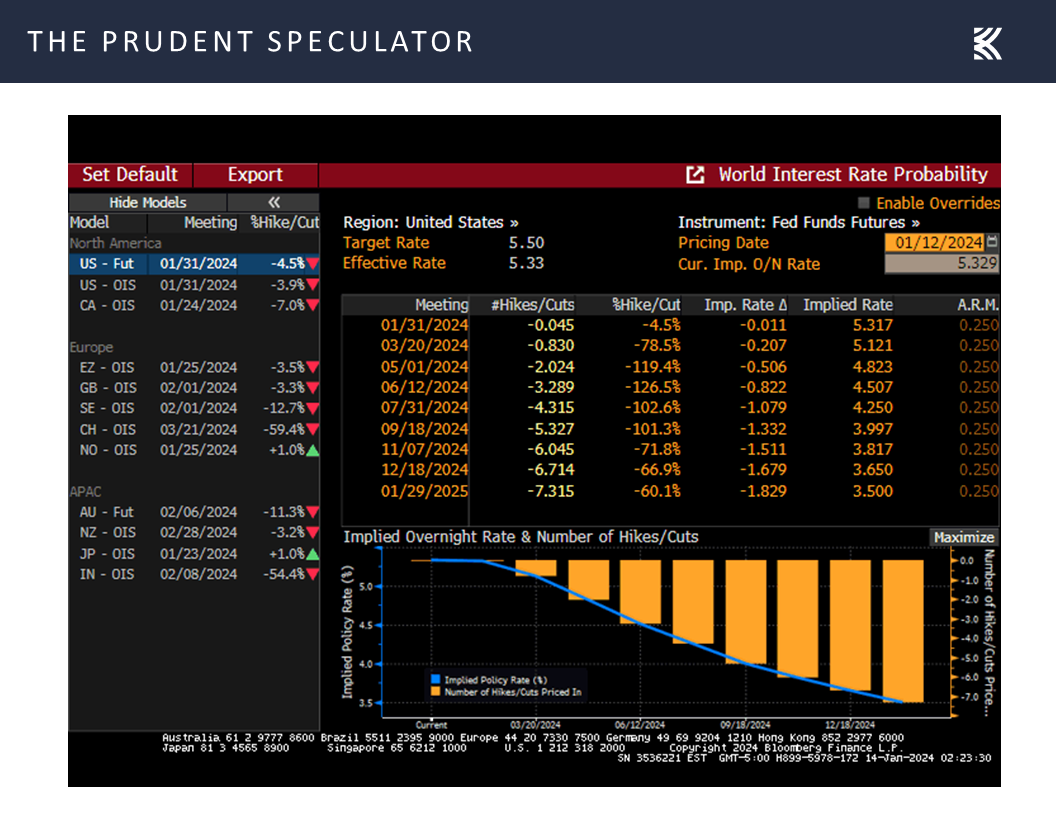

Of course, the odds may favor Value, but anything can happen going forward, especially with so much attention paid to the Federal Reserve and the timing of interest rate cuts. Interestingly, the betting in the Fed Funds futures market last week showed a year-end-2024 target for the central-bank lending rate of 3.65%, down from 3.95% the week prior, and the current 5.50% level,

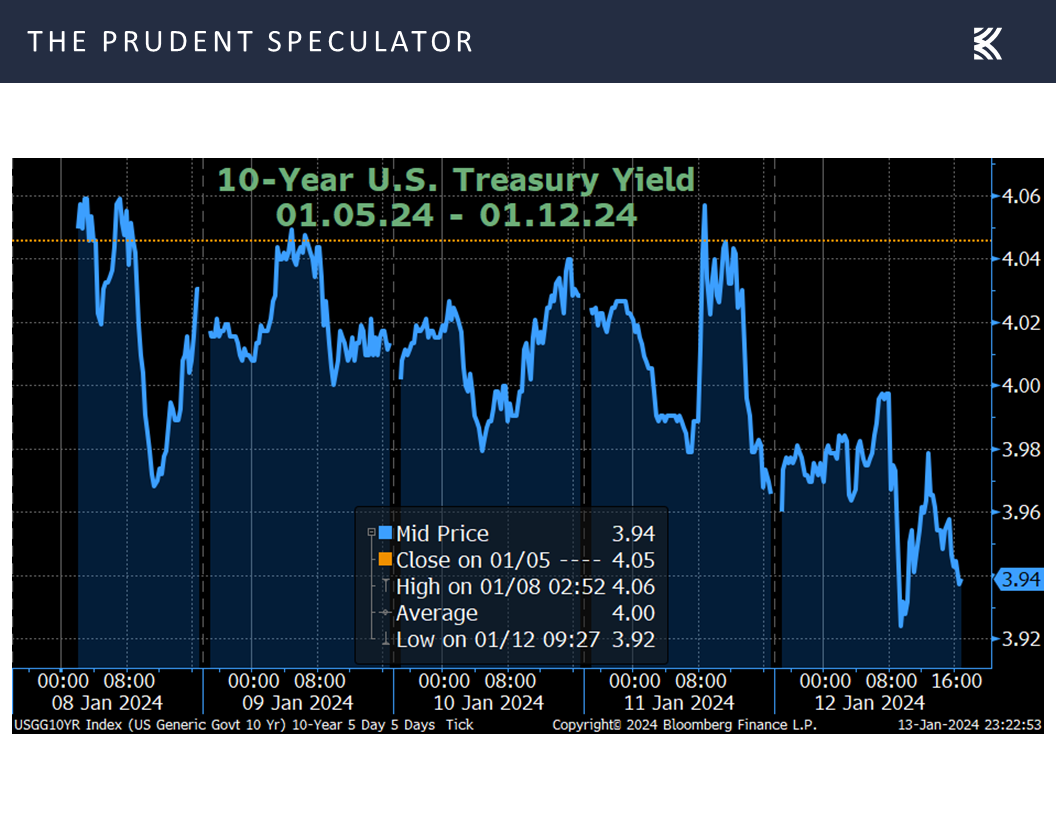

while the yield on the benchmark 10-Year U.S. Treasury fell back below 4.0%,

which we think should add to the appeal of Value in general,

Valuations – Value Stocks Still Reasonably Priced

and our broadly diversified portfolios of what we believe to be undervalued stocks in particular,

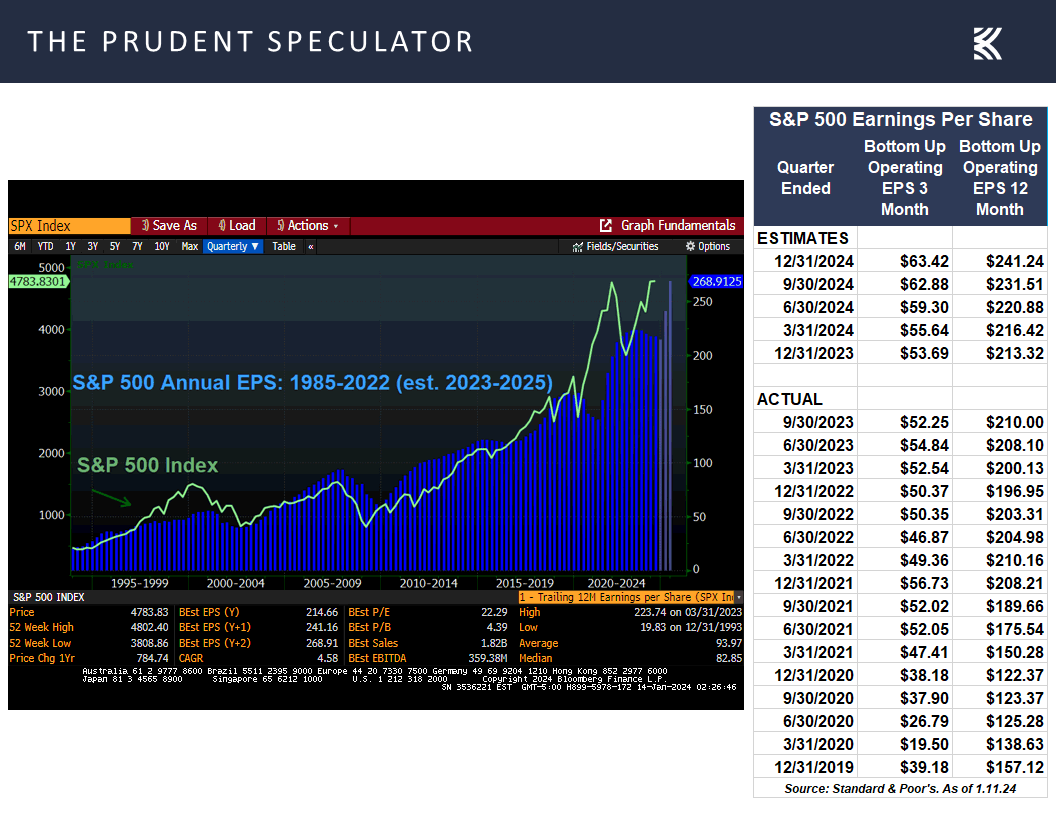

especially with corporate profits likely to show solid growth this year.

Inflation – December Data Mixed, But CPI & PPI Headed in the Right Direction

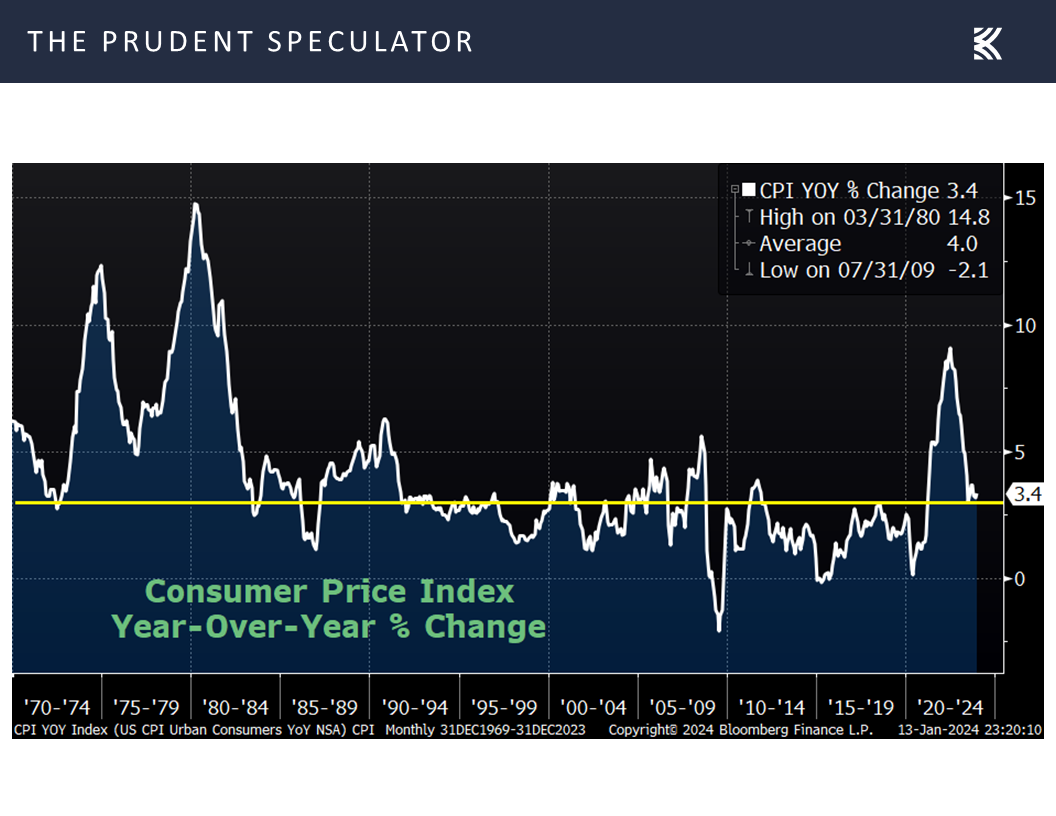

Inflation is the big wildcard, and there were mixed readings out last week, with the Consumer Price Index (CPI) for December coming in at 3.4%, up from 3.1% in November,

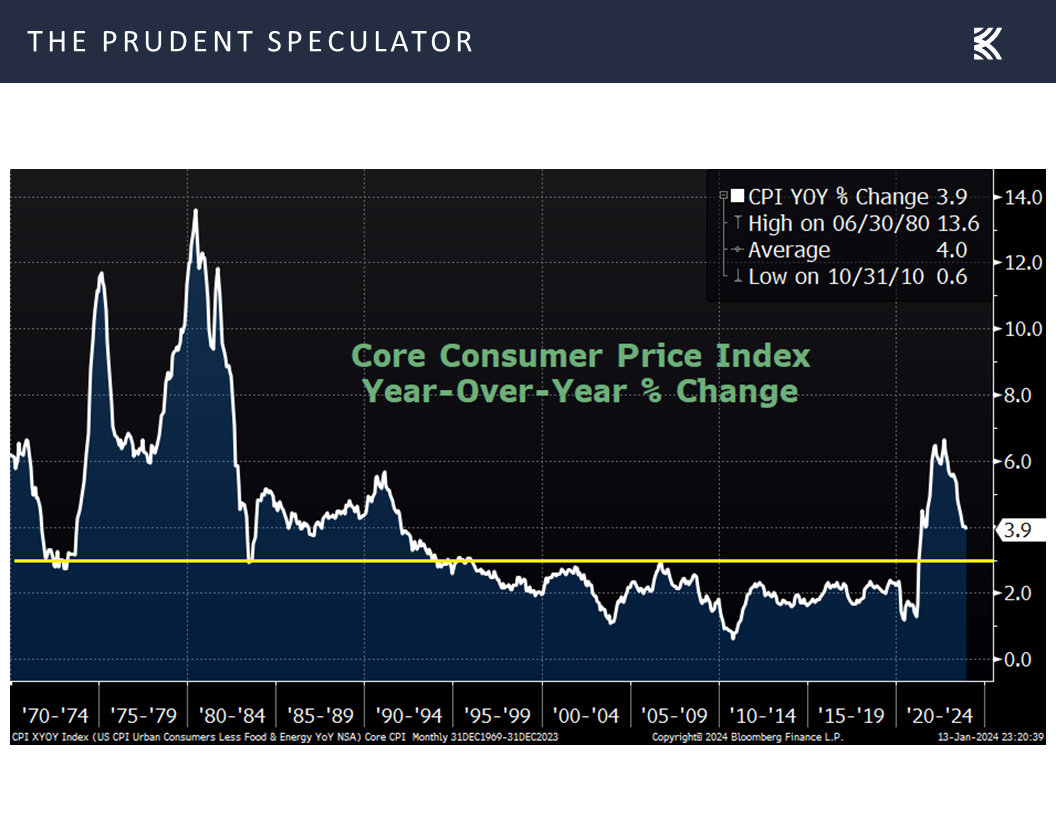

even as the so-called Core CPI (excludes volatile food and energy prices) ticked down last month to 3.9%, compared to 4.0% the month prior.

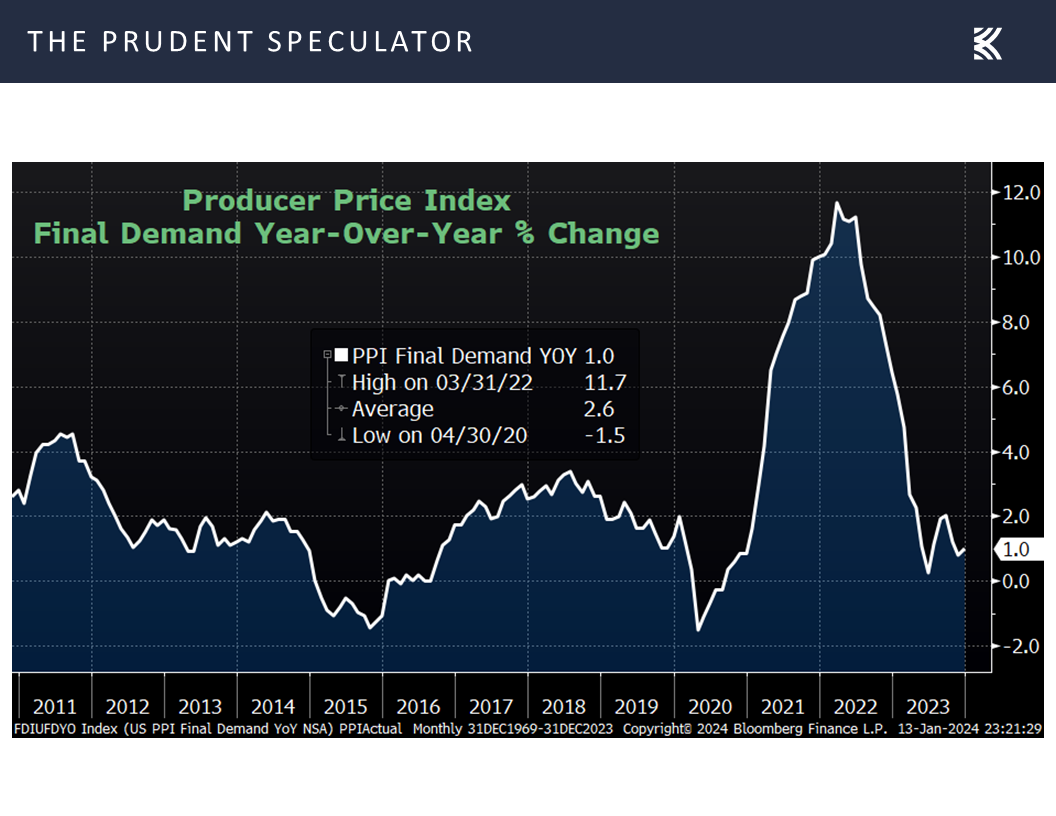

Meanwhile, inflation at the wholesale level came in well below forecasts in December as the Producer Price Index rose 1.0%, versus a 1.3% consensus projection,

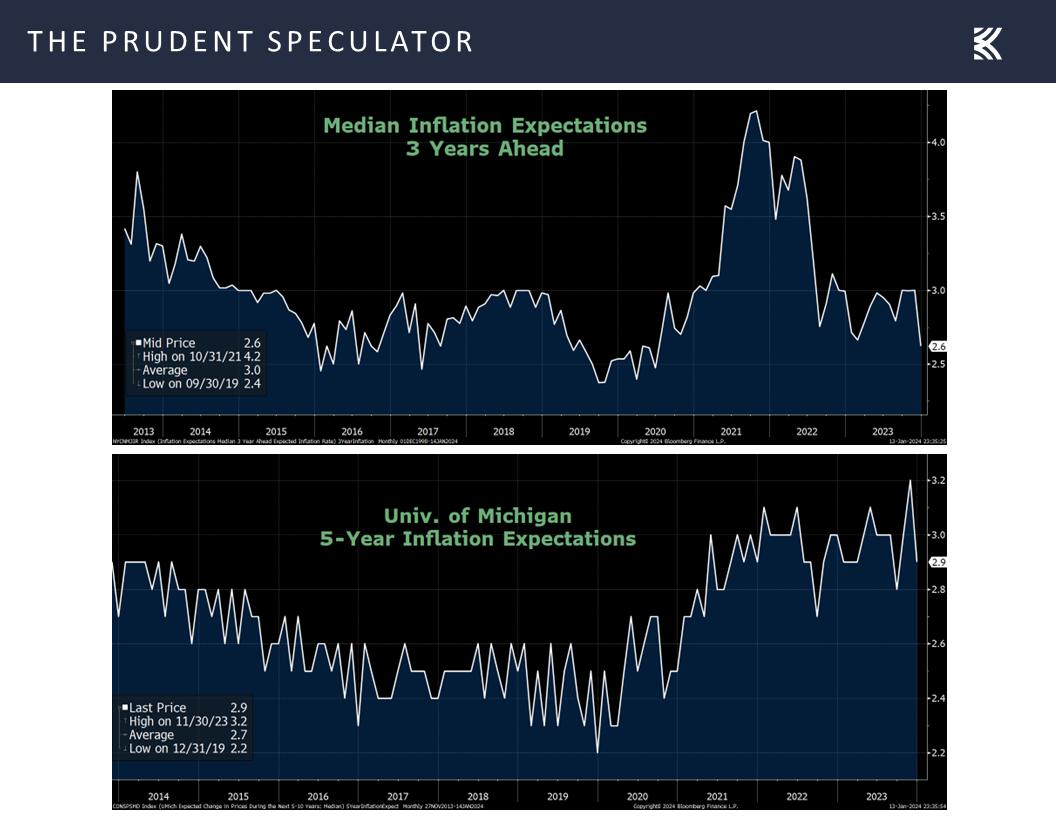

and longer-term inflation expectations continue to remain well anchored.

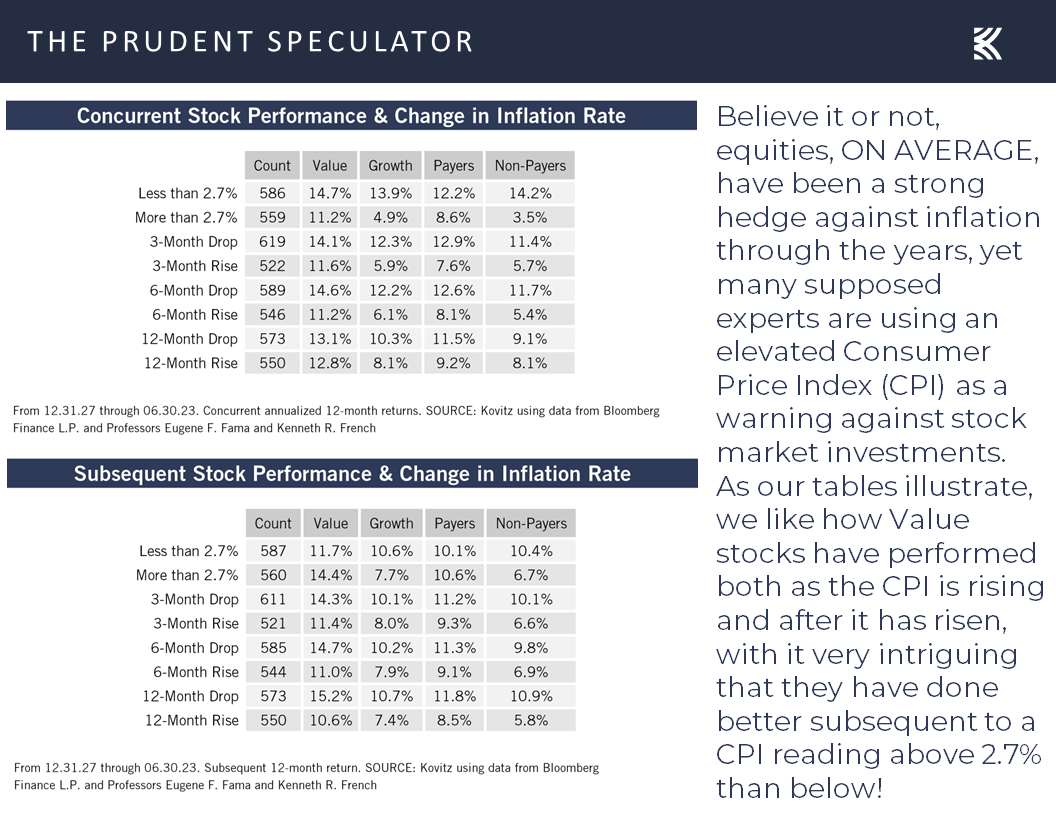

No doubt, most think continued progress on inflation will be the catalyst for Jerome H. Powell & Co. to loosen monetary policy this year, but we would not lose sleep if the Fed battle takes longer than expected, given how Value has performed when inflation is elevated and when it is moving higher,

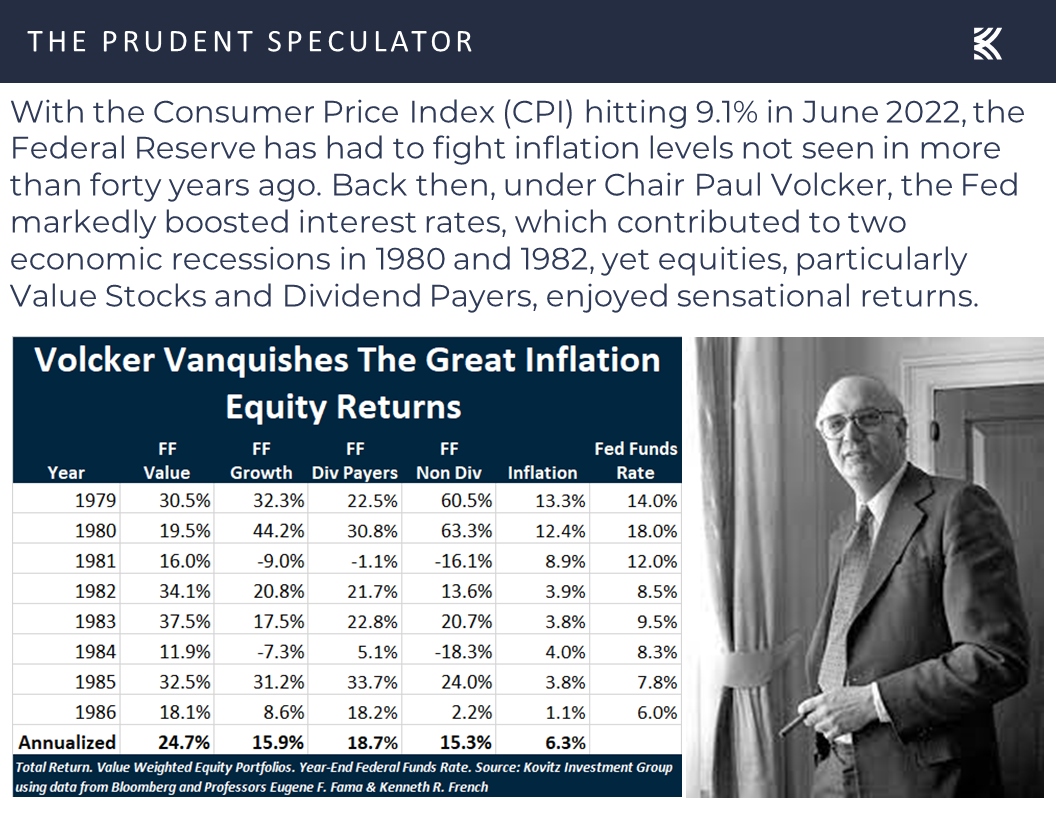

not to mention the historical return figures during the Volker Fed’s fight with the Great Inflation of the late 1970’s.

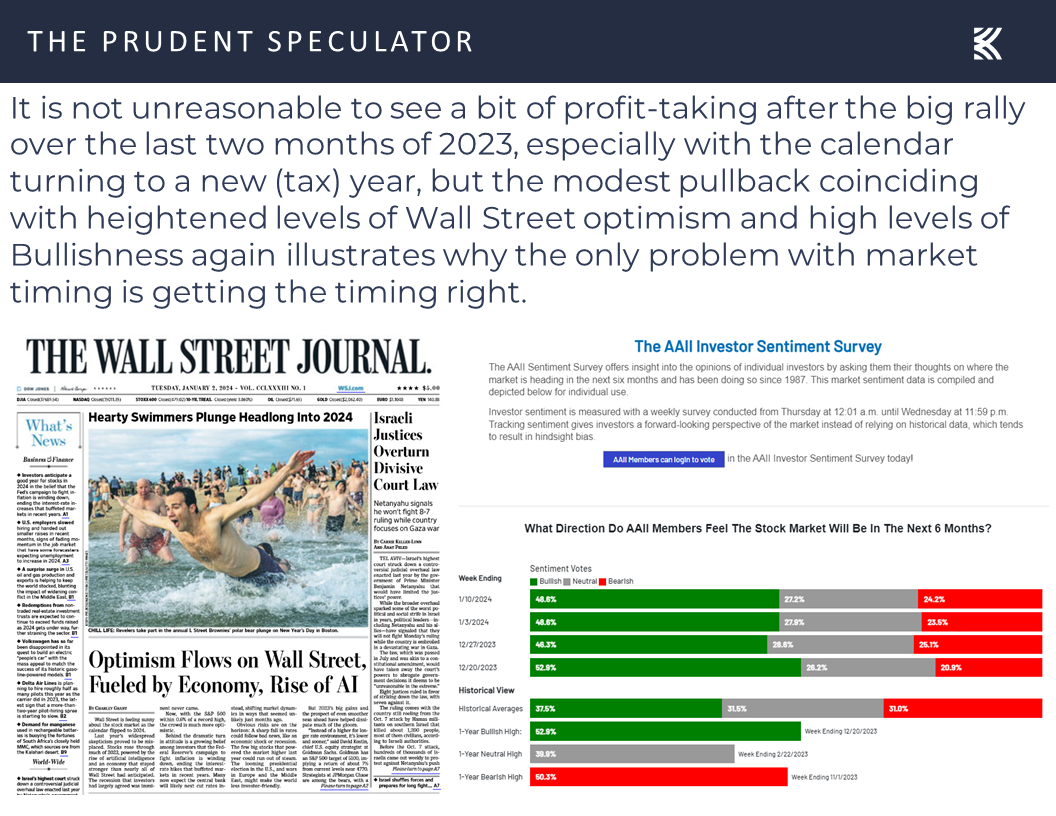

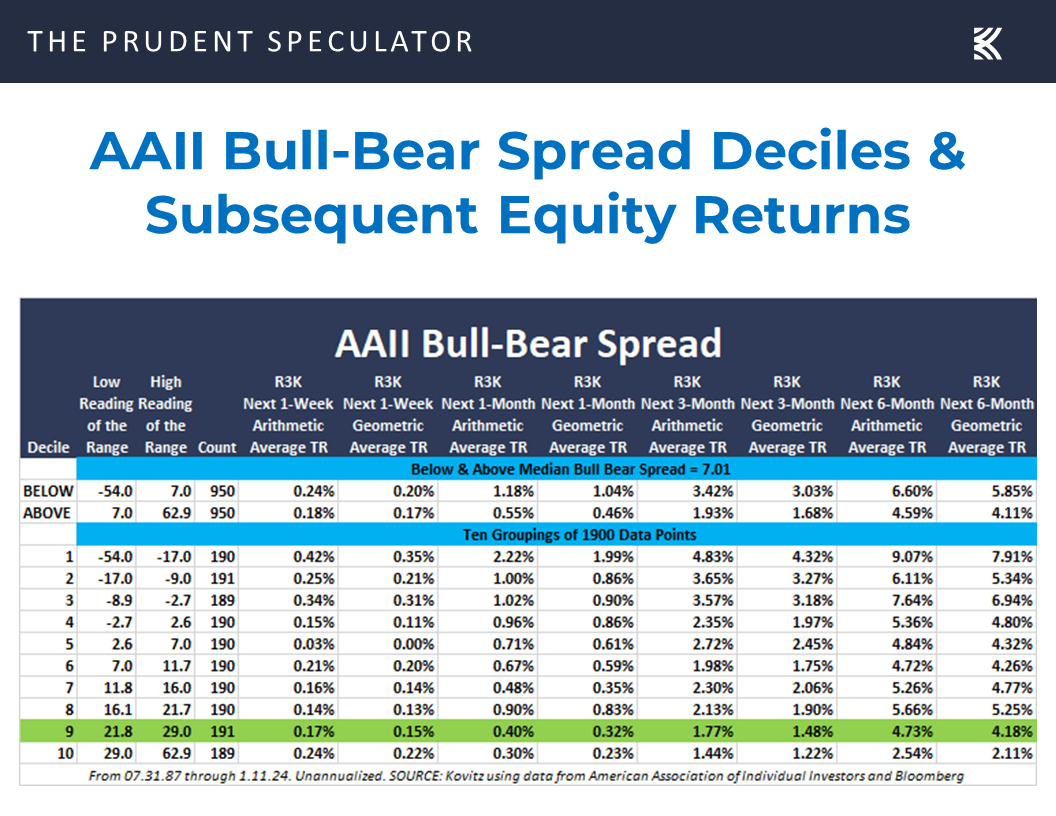

Sentiment – Lots of Optimism as ’24 Gets Underway

So, while we are always braced for downside volatility, we retain our enthusiasm for equities, even as we might prefer that fewer folks shared our optimism.

Still, we offer the friendly reminder that history shows that being greedy when others are fearful has proved far more rewarding than being fearful when others are greedy, at least as measured by subsequent returns and the American Association of Individual Investors Sentiment Survey.

Stock News – Updates on eight stocks across four different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Interest Rates, Valuations, Inflation, AAII Sentiment and more Econ News

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss interest rates, valuations, inflation, AAII Sentiment and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

First Five Days of the Year – Value Positive; Growth & S&P 500 Negative

Calendar – Numbers Support Value

Interest Rates – Fed Funds Futures and 10-Year Yields Move Lower

Valuations – Value Stocks Still Reasonably Priced

Inflation – December Data Mixed, But CPI & PPI Headed in the Right Direction

Sentiment – Lots of Optimism as ’24 Gets Underway

Stock News – Updates on eight stocks across four different sectors

First Five Days of the Year – Value Positive; Growth & S&P 500 Negative

It was a tough five days for Value stocks relative to growth, with the Value indexes all in the red for the week ended January 12, but this past Monday’s big rally carried the Russell 3000 Value index into the green by 0.25% for the first five days of the trading year, whereas the Growth Indexes, S&P 500 and Dow Jones Industrial Average all were in the red for the year at the close on January 8.

Although many would argue that there is little in the way of predictive significance to the First Five Days of the Year, we aren’t unhappy that the Russell Value and Growth indexes show interesting statistics. True, there is just 28 years in the dataset as daily data for the Russell style indexes did not begin until mid-1995, but the 17 previous times the First Five Days were positive for the Russell 3000 Value index, the mean return for the balance of the year was 14.4%. Contrast this to the 9 times the Russell 3000 Growth index and S&P 500 were negative, where the mean return for the balance of the year was -0.3% and 1.0%, respectively.

Calendar – Numbers Support Value

Happily, there are other statistical factors in support of the near-term prospects for Value, including the average returns for January, February and April,

and the Fourth Year of the Presidency,

while the long-term evidence since the launch of The Prudent Speculator nearly 47 year ago favors the kind of companies that we have long championed,

and inexpensively priced stocks today are far less expensive on an earnings basis to their 28-year norms than their more-richly valued peers.

Interest Rates – Fed Funds Futures and 10-Year Yields Move Lower

Of course, the odds may favor Value, but anything can happen going forward, especially with so much attention paid to the Federal Reserve and the timing of interest rate cuts. Interestingly, the betting in the Fed Funds futures market last week showed a year-end-2024 target for the central-bank lending rate of 3.65%, down from 3.95% the week prior, and the current 5.50% level,

while the yield on the benchmark 10-Year U.S. Treasury fell back below 4.0%,

which we think should add to the appeal of Value in general,

Valuations – Value Stocks Still Reasonably Priced

and our broadly diversified portfolios of what we believe to be undervalued stocks in particular,

especially with corporate profits likely to show solid growth this year.

Inflation – December Data Mixed, But CPI & PPI Headed in the Right Direction

Inflation is the big wildcard, and there were mixed readings out last week, with the Consumer Price Index (CPI) for December coming in at 3.4%, up from 3.1% in November,

even as the so-called Core CPI (excludes volatile food and energy prices) ticked down last month to 3.9%, compared to 4.0% the month prior.

Meanwhile, inflation at the wholesale level came in well below forecasts in December as the Producer Price Index rose 1.0%, versus a 1.3% consensus projection,

and longer-term inflation expectations continue to remain well anchored.

No doubt, most think continued progress on inflation will be the catalyst for Jerome H. Powell & Co. to loosen monetary policy this year, but we would not lose sleep if the Fed battle takes longer than expected, given how Value has performed when inflation is elevated and when it is moving higher,

not to mention the historical return figures during the Volker Fed’s fight with the Great Inflation of the late 1970’s.

Sentiment – Lots of Optimism as ’24 Gets Underway

So, while we are always braced for downside volatility, we retain our enthusiasm for equities, even as we might prefer that fewer folks shared our optimism.

Still, we offer the friendly reminder that history shows that being greedy when others are fearful has proved far more rewarding than being fearful when others are greedy, at least as measured by subsequent returns and the American Association of Individual Investors Sentiment Survey.

Stock News – Updates on eight stocks across four different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.