The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Recession Chances, Earnings, Inflation, FOMC Decision more Economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Week in Review – Rally Continues

Econ News – Favorable Numbers

FOMC Decision – As Expected, Fed Raises Rates 25 Basis Points

Recession Chances – World Bank and Fed Now Saying No U.S. Contraction This Year

Inflation – PCE Price Growth Slows Markedly, Wage Pressures Ease

Sentiment – AAII Bullishness Moderates Somewhat

Earnings – Strong Q2 Results; Growth Still the Forecast This Year and in 2024

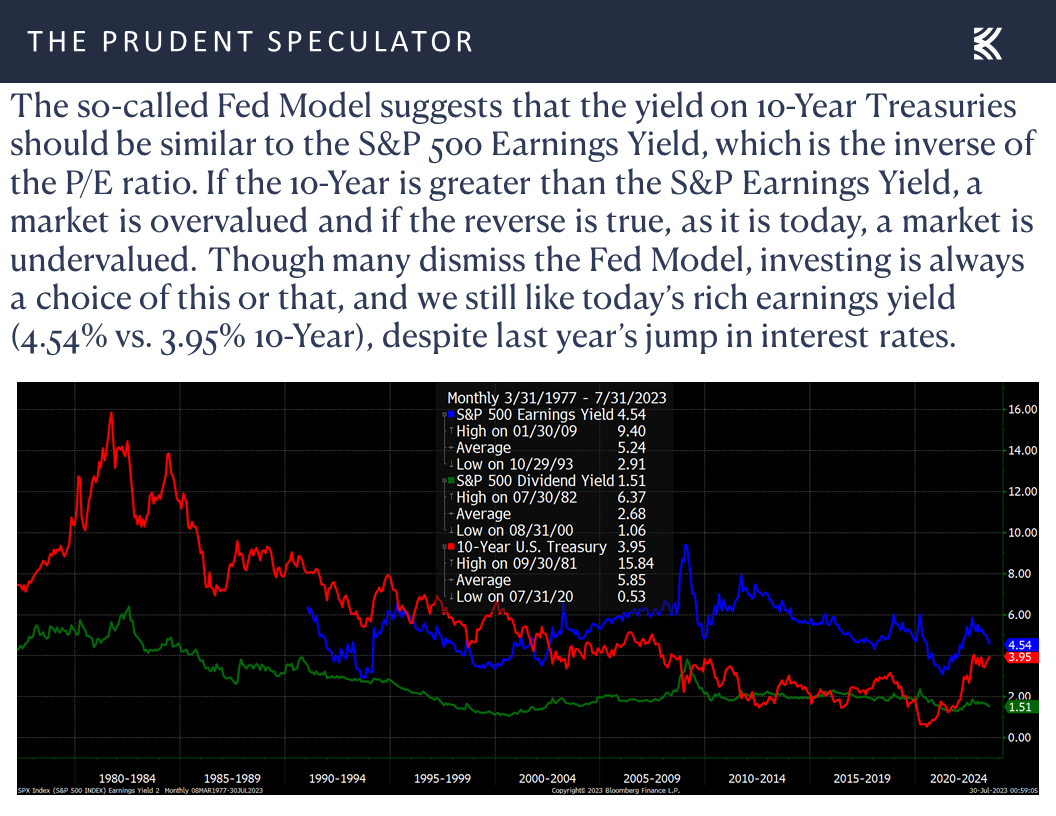

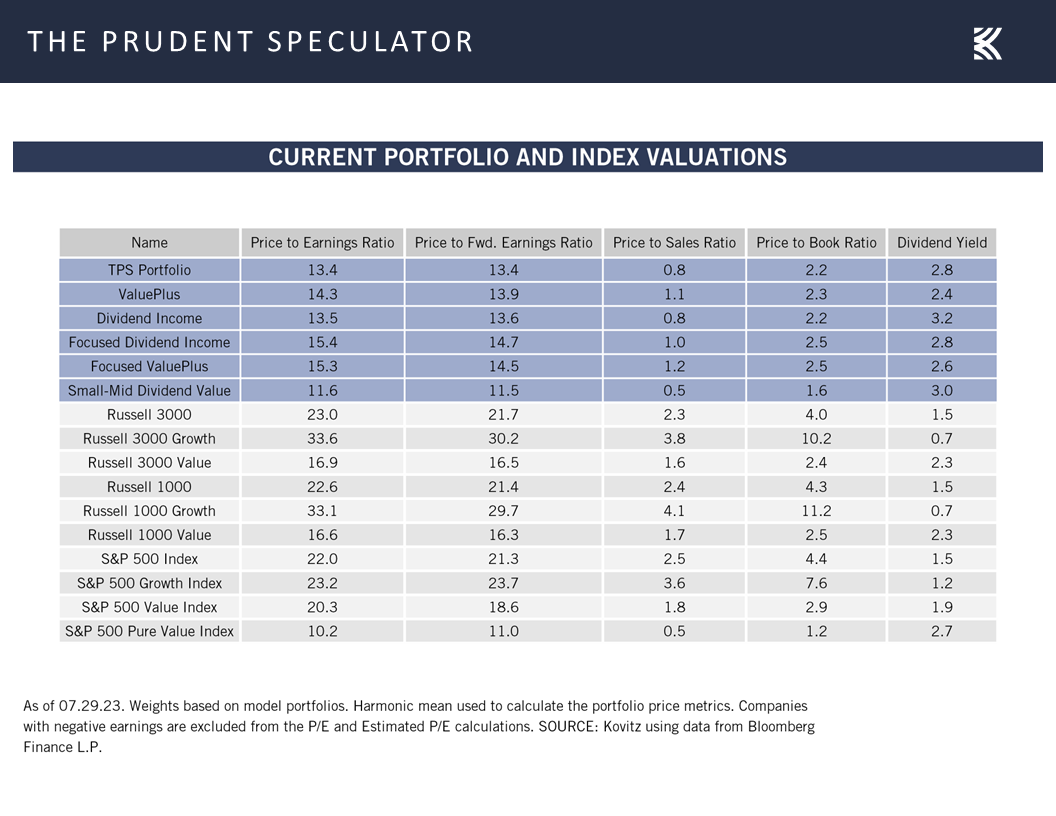

Valuations – Inexpensive Multiples for our Stocks

Stock News – Updates on GOOG, MSFT, META, LRCX, GLW, INTC, GD, MDC, CMCSA, SNY, DLR, BMY, ONB, NYCB & MMM

Week in Review – Rally Continues

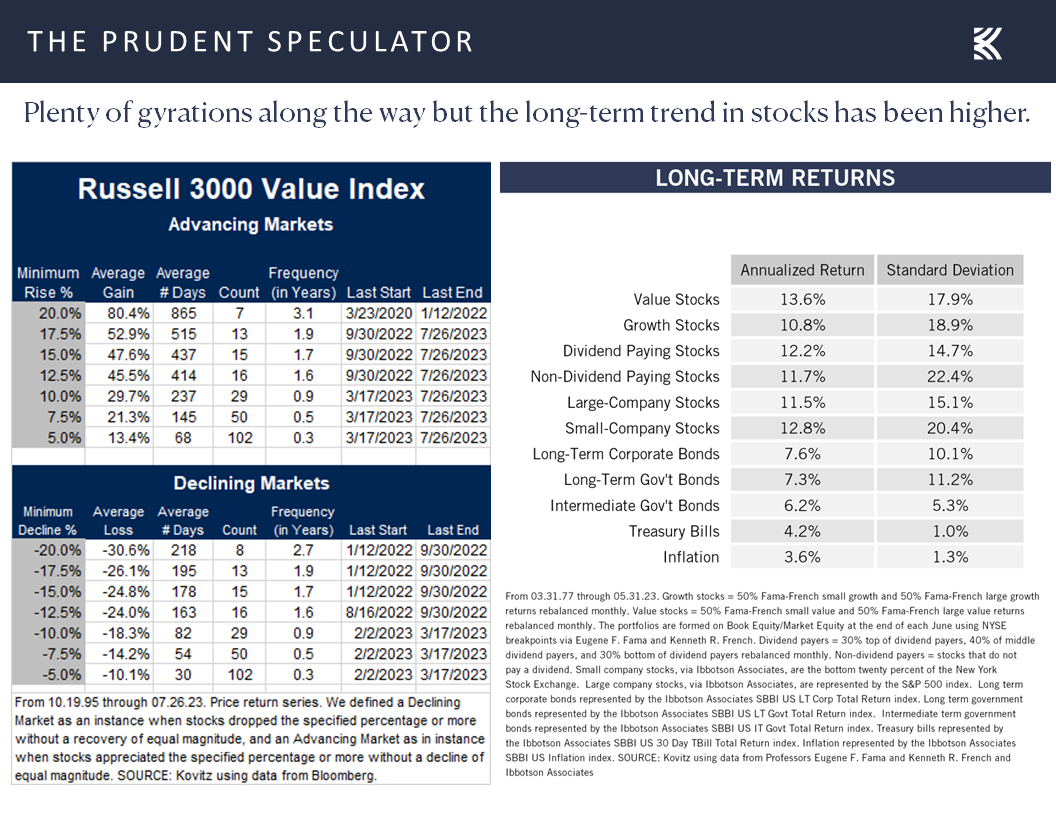

Although the winning streak for the Dow Jones Industrial Average came to an end after 13 days and the average stock did not perform nearly as well as the price- and market-capitalization- weighted indexes, it was another positive week for equity prices. The sizable advance, especially with market breadth broadening considerably since the end of May, provides more support for the assertion that time in the market trumps market timing,

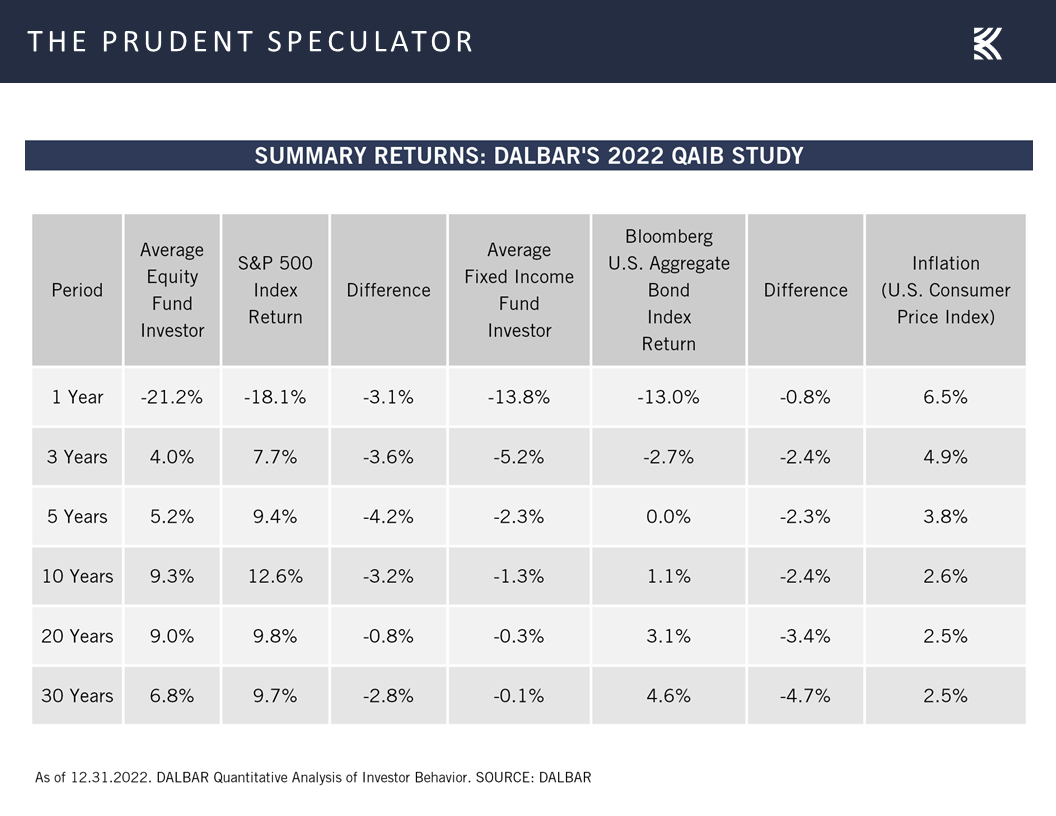

even as our oft-stated admonition often falls on deaf ears, as evidenced by the miserable long-term returns put up by mutual fund investors in both stocks and bonds, per analytics from data-provider DALBAR.

Econ News – Favorable Numbers

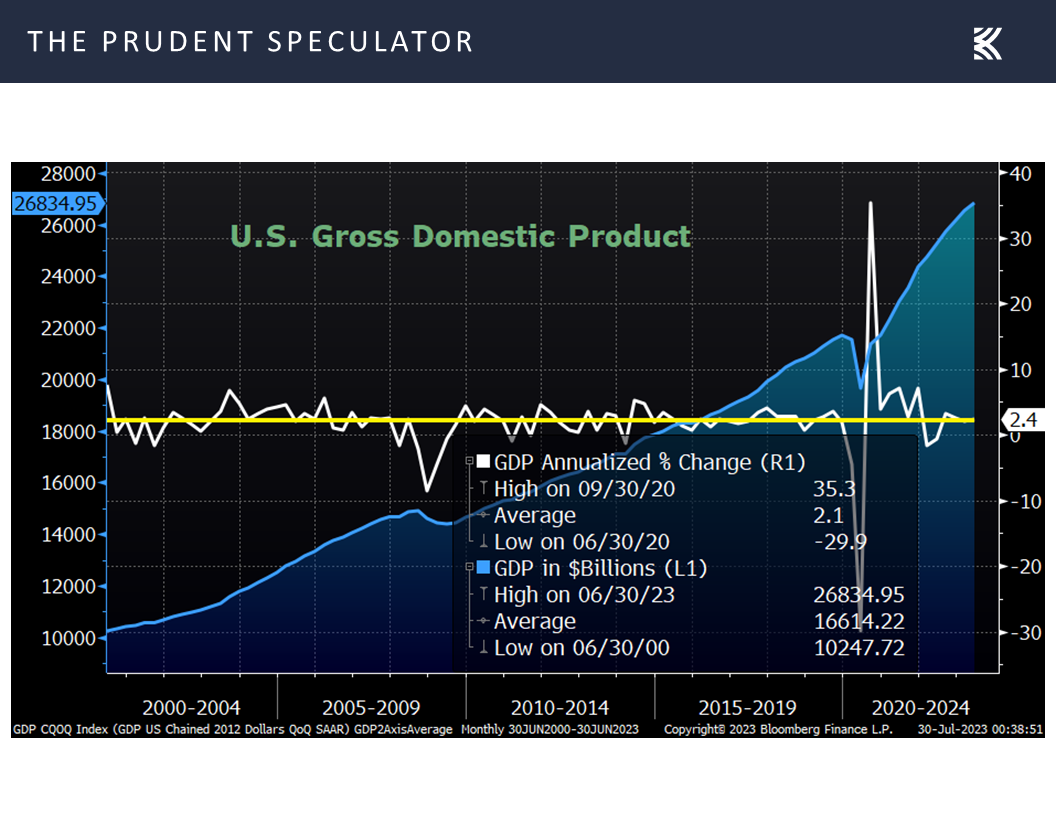

No doubt, the gains last week were fueled by favorable economic statistics, with the first estimate of second quarter real (inflation-adjusted) GDP growth coming in at 2.4%, above expectations in the 1.8% to 2.0% range

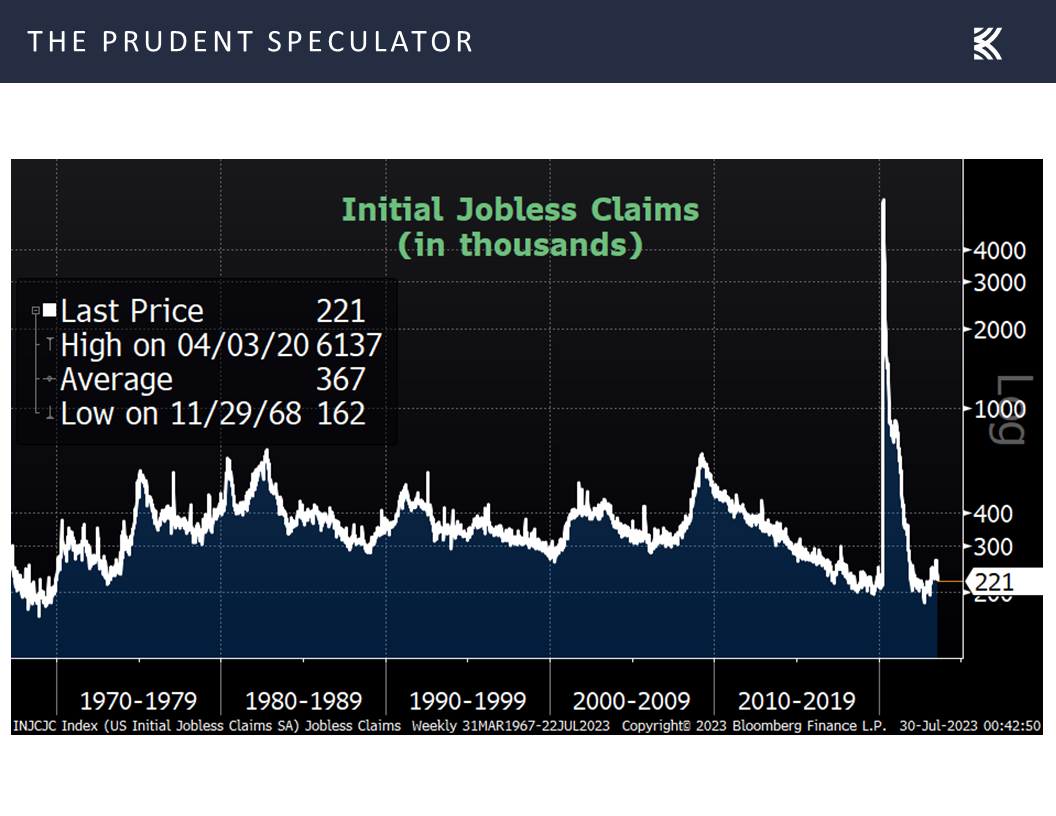

the number of initial filings for unemployment benefits in the latest week dropping to a lower-than-projected 221,000

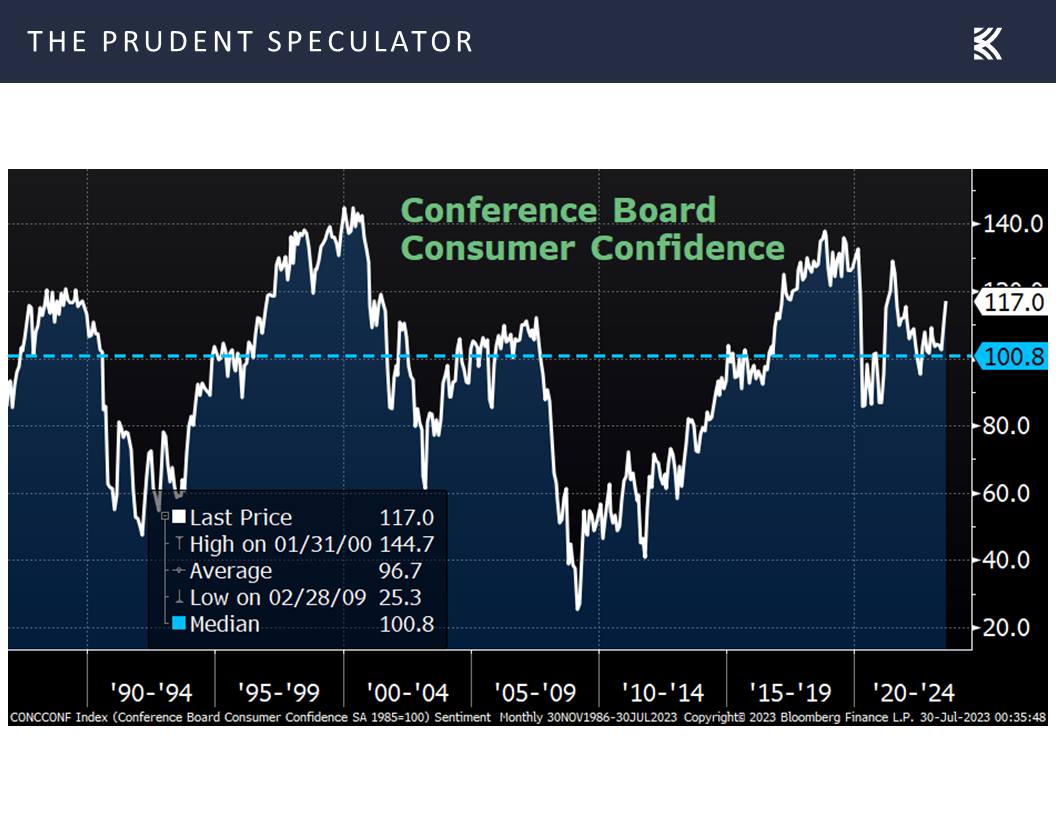

and the Conference Board’s measure of Consumer Confidence jumping to a two-year high in July and rising to 117.0, well above the long-term average of 96.7.

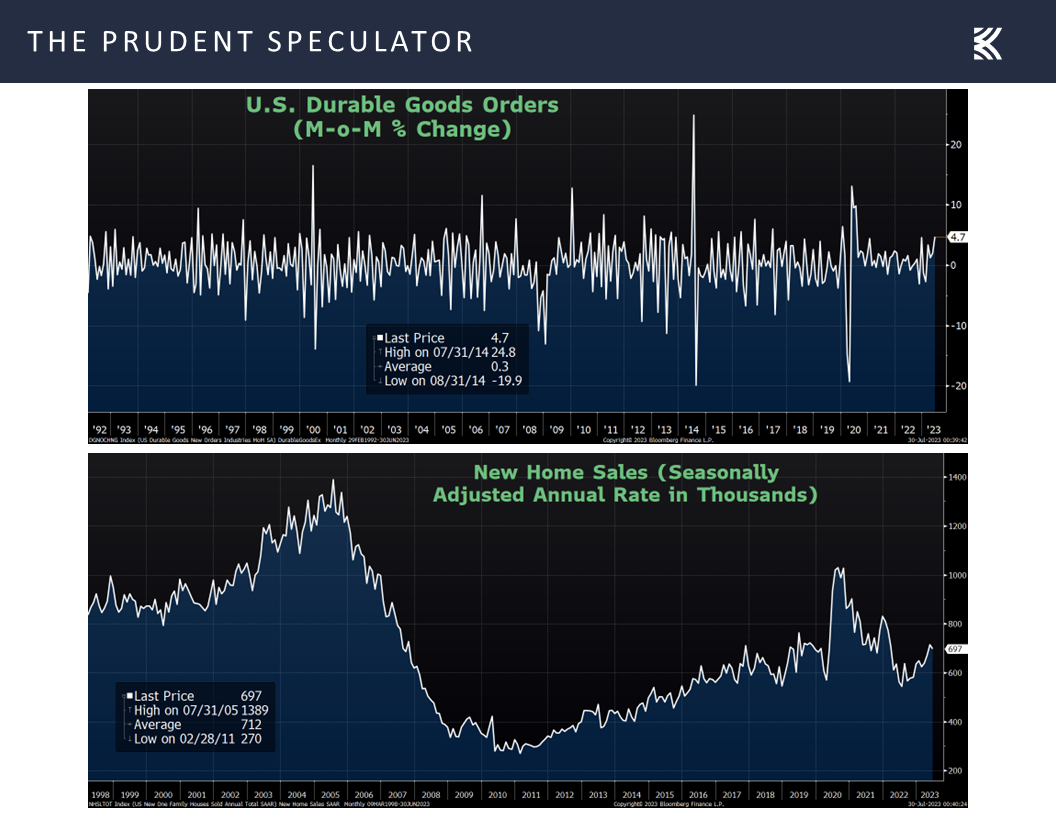

Other economic numbers were mixed as orders for durable goods bounded 4.7% higher in June, led by aircraft contracts, but new home sales last month fell short of estimates, falling 2.5% from the month prior’s revised figure to a seasonally adjusted annual rate of 697,000

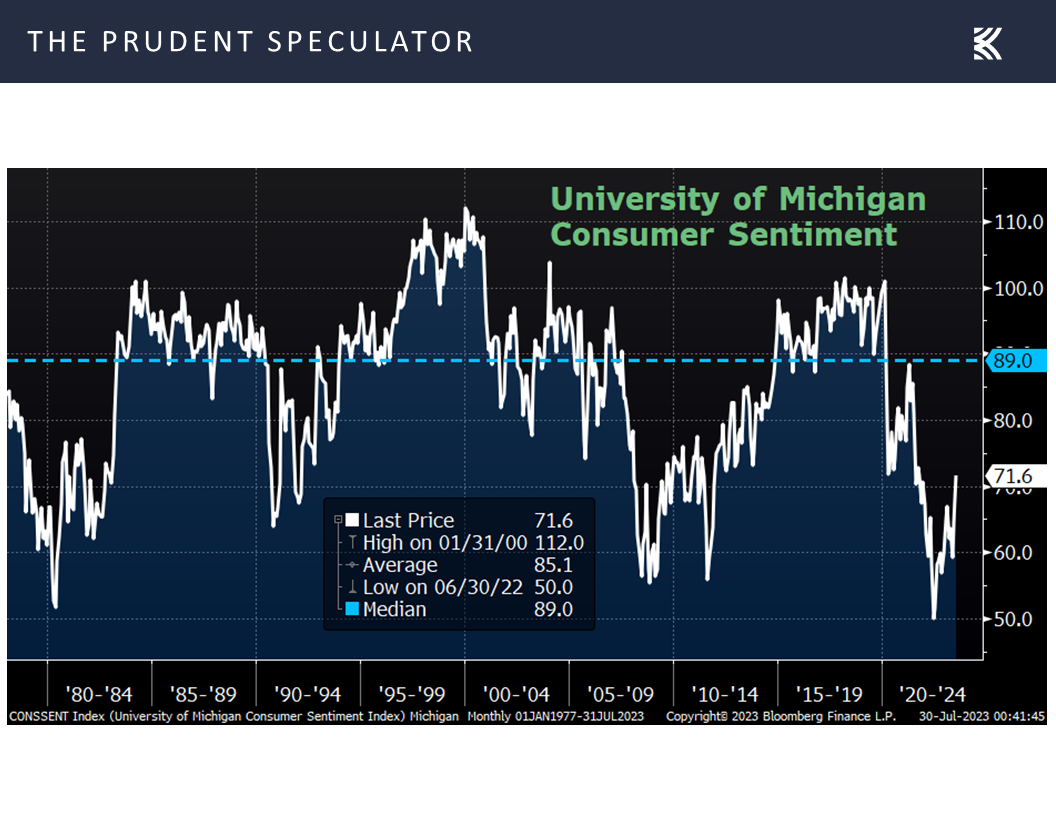

while the University of Michigan’s final Consumer Sentiment gauge reading for July hit 71.6, down from a preliminary figure of 72.6 and well-below the historical norm, even as it was up sharply from June’s tally of 64.4.

FOMC Decision – As Expected, Fed Raises Rates 25 Basis Points

Not surprisingly, given that the Federal Reserve has long stated that it is data-dependent, Jerome H. Powell was relatively upbeat in his economic assessment featured in his opening remarks for his Press Conference this past Wednesday following the decision on interest rates.

Recent indicators suggest that economic activity has been expanding at a moderate pace. Growth in consumer spending appears to have slowed from earlier in the year. Although activity in the housing sector has picked up somewhat, it remains well below levels of a year ago, largely reflecting higher mortgage rates. And higher interest rates and slower output growth also appear to be weighing on business fixed investment.

The labor market remains very tight. Over the past three months, job gains averaged 244 thousand jobs per month, a pace below that seen earlier in the year but still a strong pace. The unemployment rate remains low, at 3.6 percent. There are some continuing signs that supply and demand in the labor market are coming into better balance. The labor force participation rate has moved up since last year, particularly for individuals aged 25 to 54 years.

Nominal wage growth has shown some signs of easing, and job vacancies have declined so far this year. While the jobs-to-workers gap has narrowed, labor demand still substantially exceeds the supply of available workers.

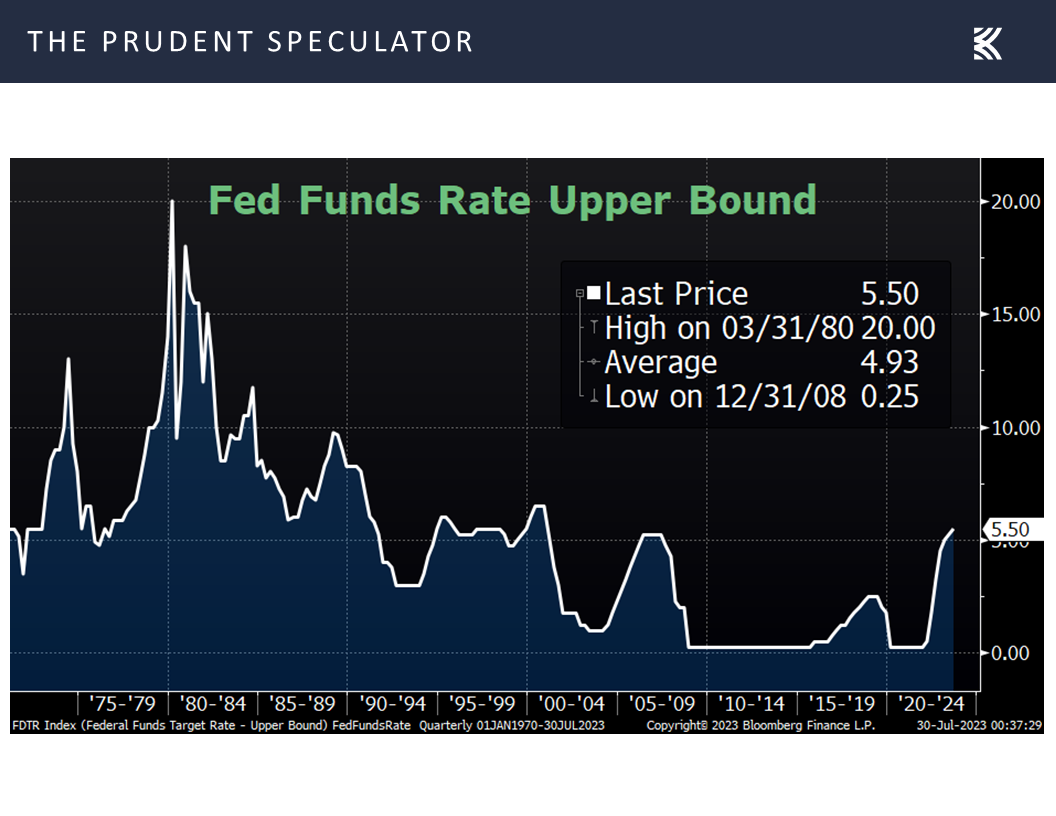

Continuing to target elevated inflation readings, the Fed Chair and his colleagues chose last week to hike the target for the Fed Funds rate by another 25 basis points, raising the benchmark lending rate to 5.5%,

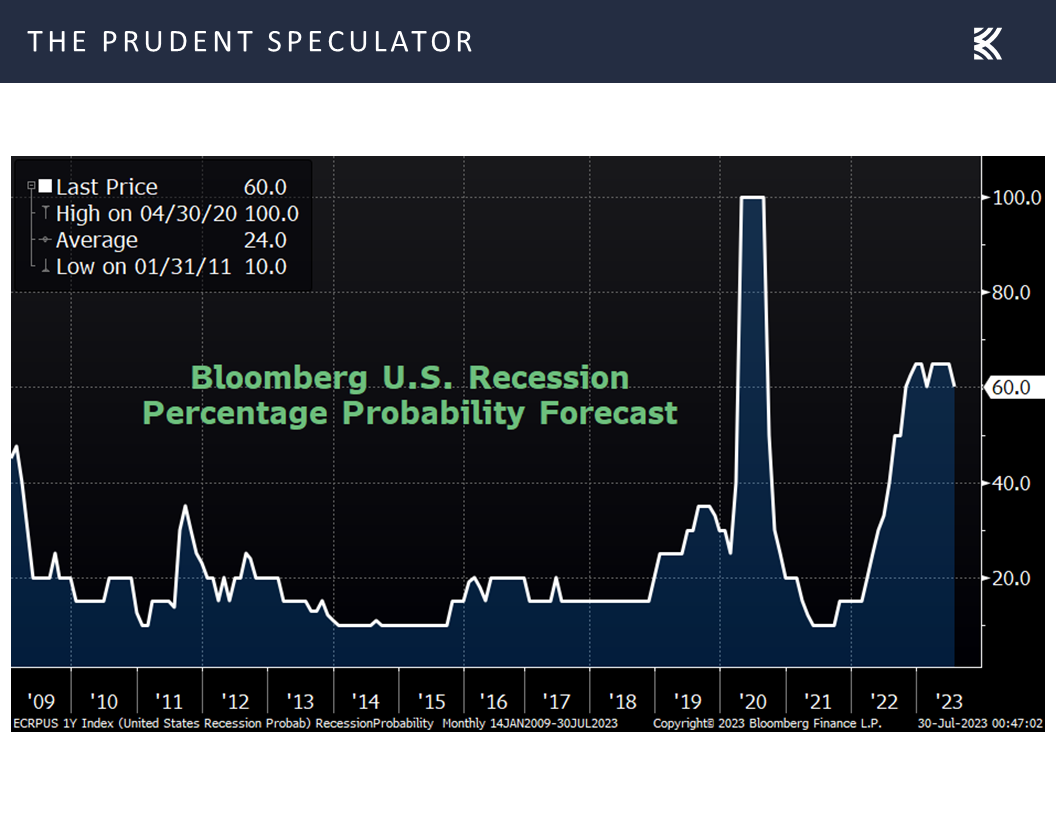

Recession Chances – World Bank and Fed Now Saying No U.S. Contraction This Year

even as the tabulation provided by Bloomberg of the probability of a U.S. recession in the next 12 months stood at 60%.

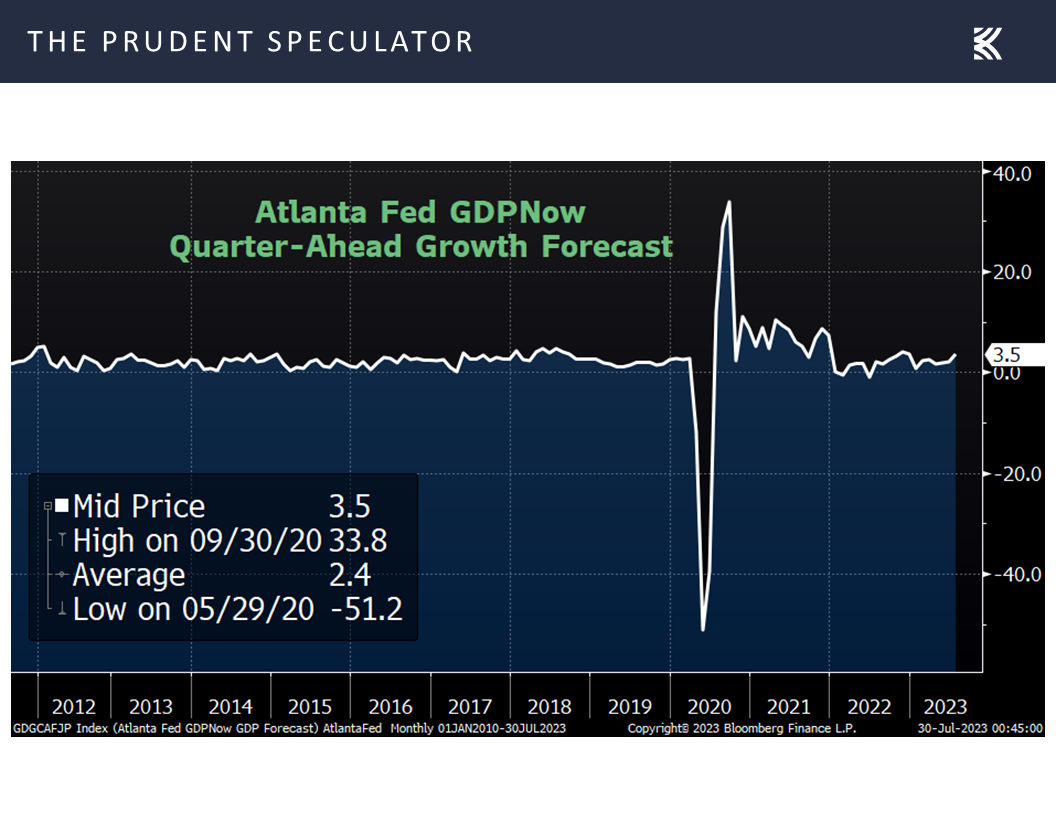

Of course, Chair Powell said in response to a question at the Press Conference, “So, the staff now has a noticeable slowdown in growth starting later this year in the forecast, but given the resilience of the economy recently, they are no longer forecasting a recession,” while the first estimate for Q3 real U.S. GDP growth from the Atlanta Fed was a very robust 3.5%.

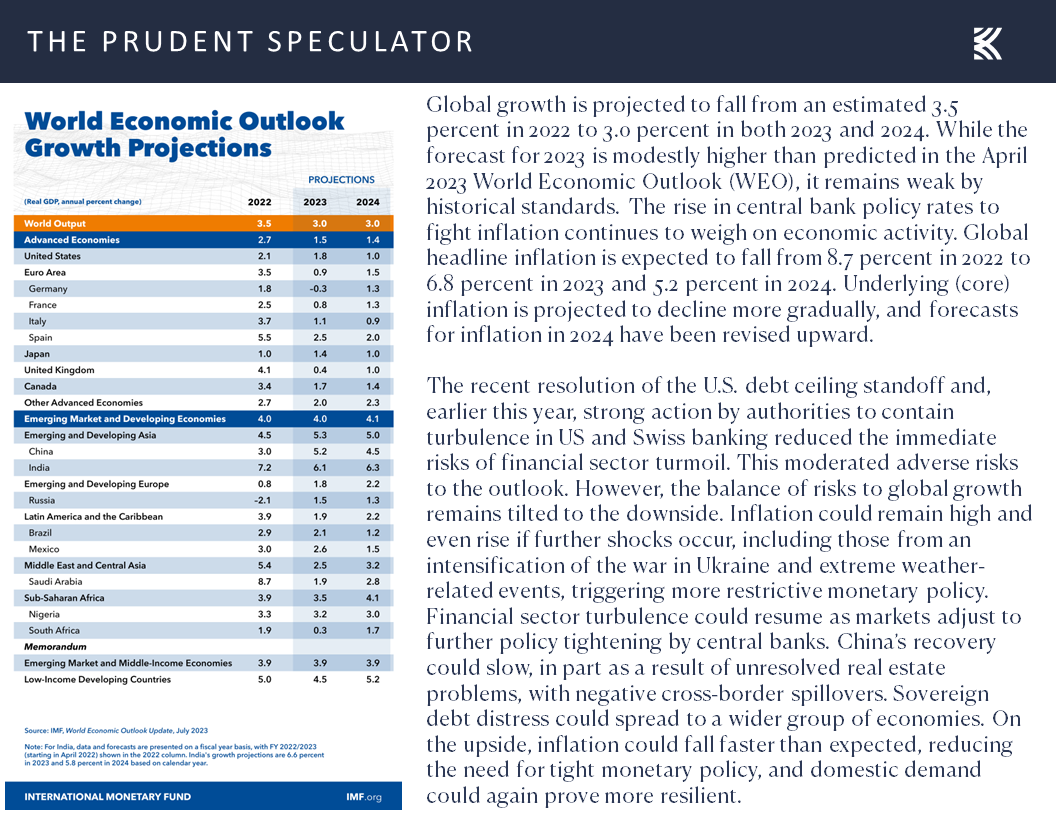

Further, the World Bank last week boosted its estimate for global GDP growth this year to 3.0%, while the group’s current projection for real U.S. growth is 1.8% in 2023 and 1.0% in 2024.

Obviously, there is a disconnect between market-based recession expectations and those of the World Bank and the Federal Reserve, but a so-called “soft landing” for the U.S. economy is making its way more heavily into the lexicon,

Inflation – PCE Price Growth Slows Markedly, Wage Pressures Ease

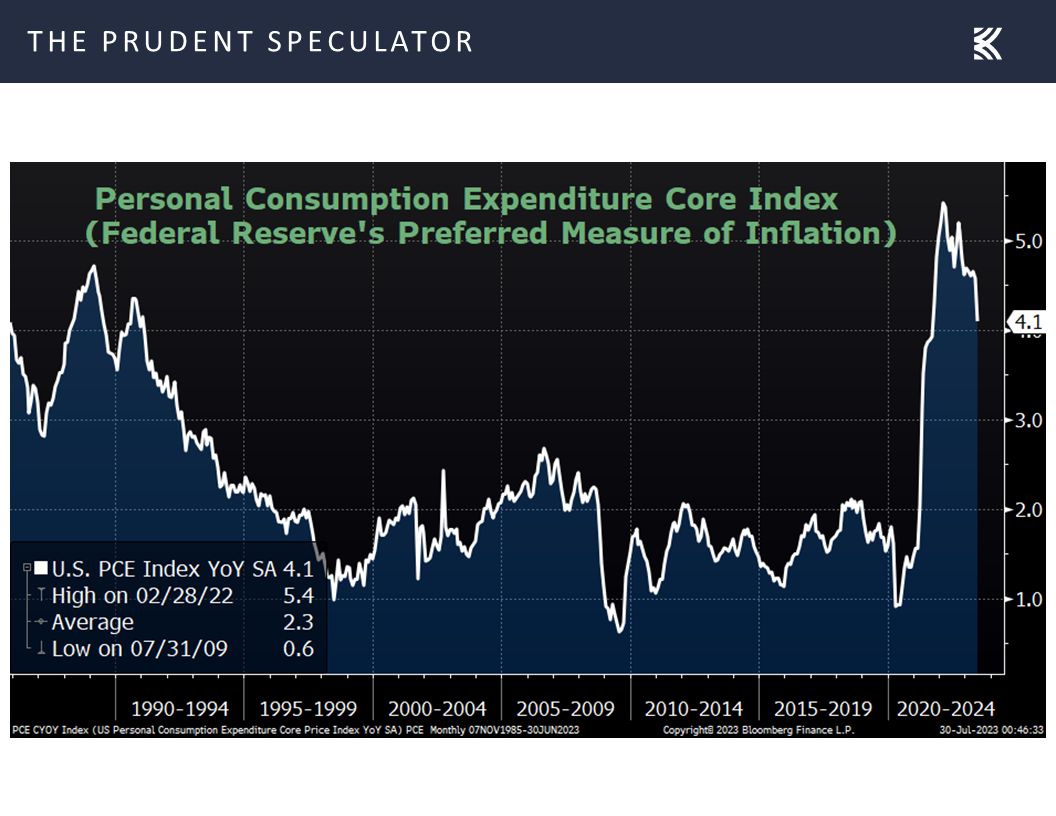

especially after the Bureau of Economic Analysis (BEA) reported on Friday that the Personal Consumption Expenditure (PCE) price index rose by just 3.0% in June, down from a 3.8% increase in May and the smallest advance since October 2021. Even better, the Federal Reserve’s preferred measure of inflation, the Core PCE, saw an increase of 4.1%, down from 4.6% the month prior,

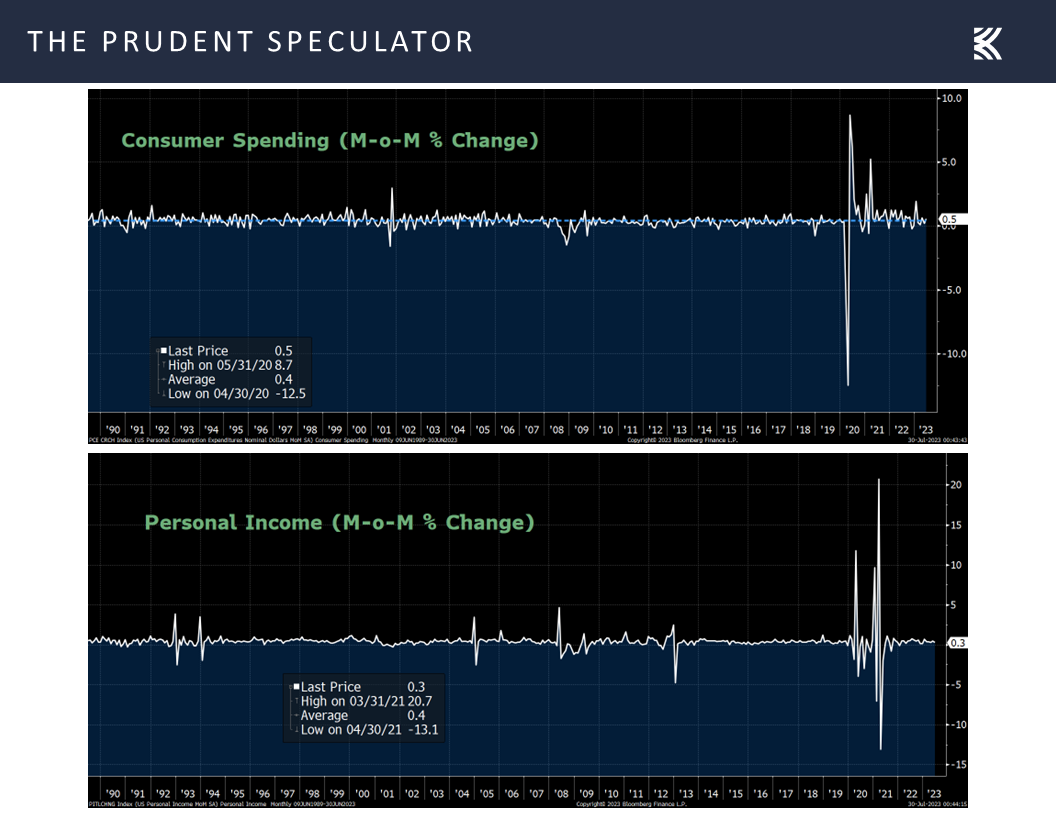

while a separate report out the same day from the Labor Department showed more easing of inflationary pressures as wage growth (personal income) slowed in June, climbing 0.3%, even as consumer spending rose 0.5%.

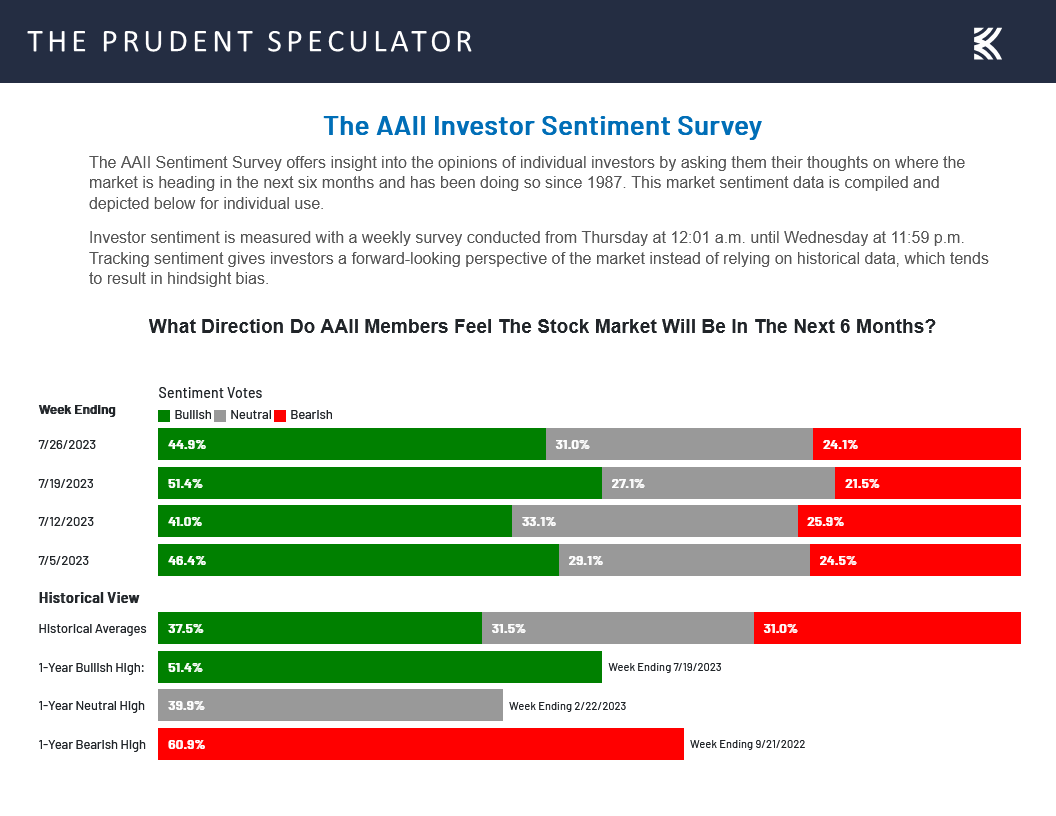

Sentiment – AAII Bullishness Moderates Somewhat

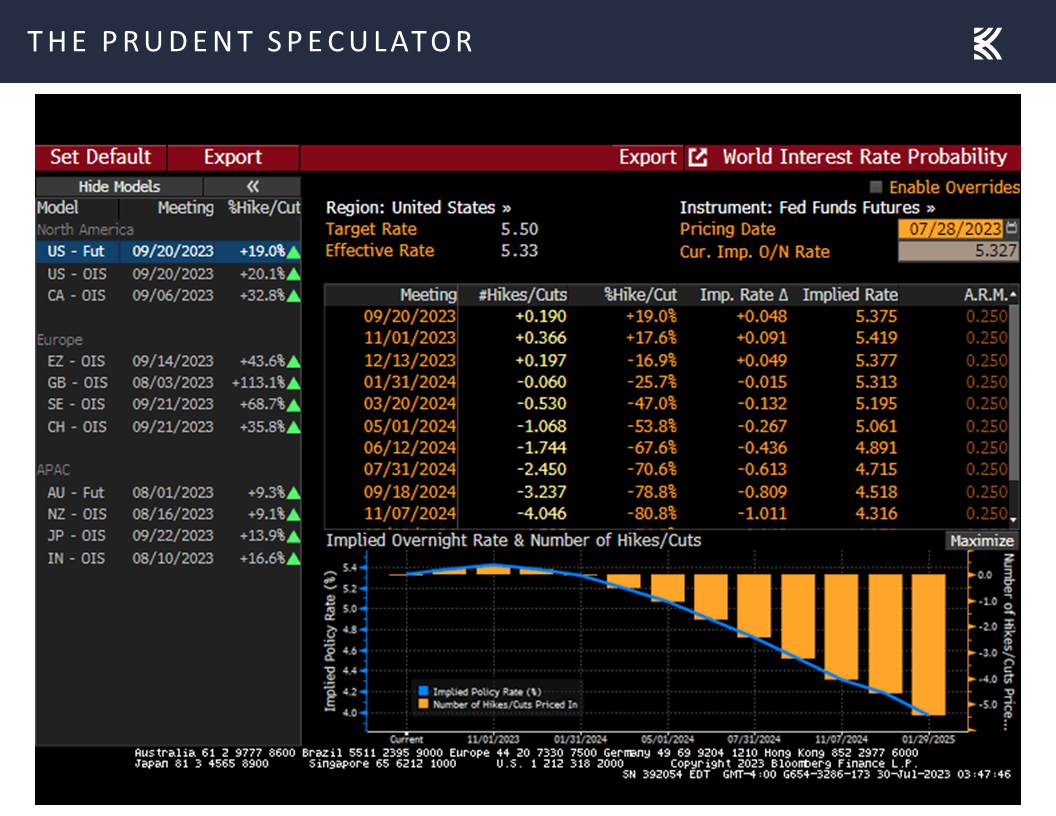

No doubt, plenty of uncertainty remains about the health of the U.S. economy and the potential for additional Fed rate hikes, but the Fed Funds futures market suggests that Jerome Powell & Co. are about at the end of their tightening cycle,

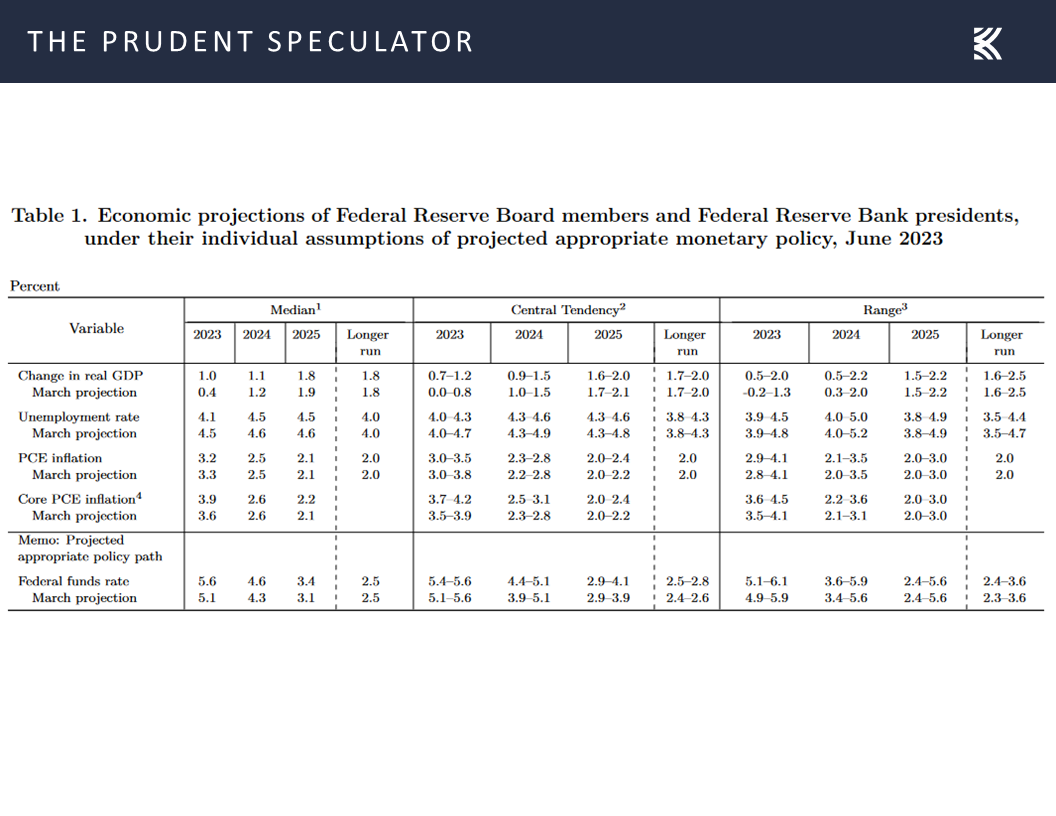

which is in keeping with what the Federal Reserve Board members and Federal Reserve Bank presidents estimated (5.6% year-end Fed Funds rate) in June.

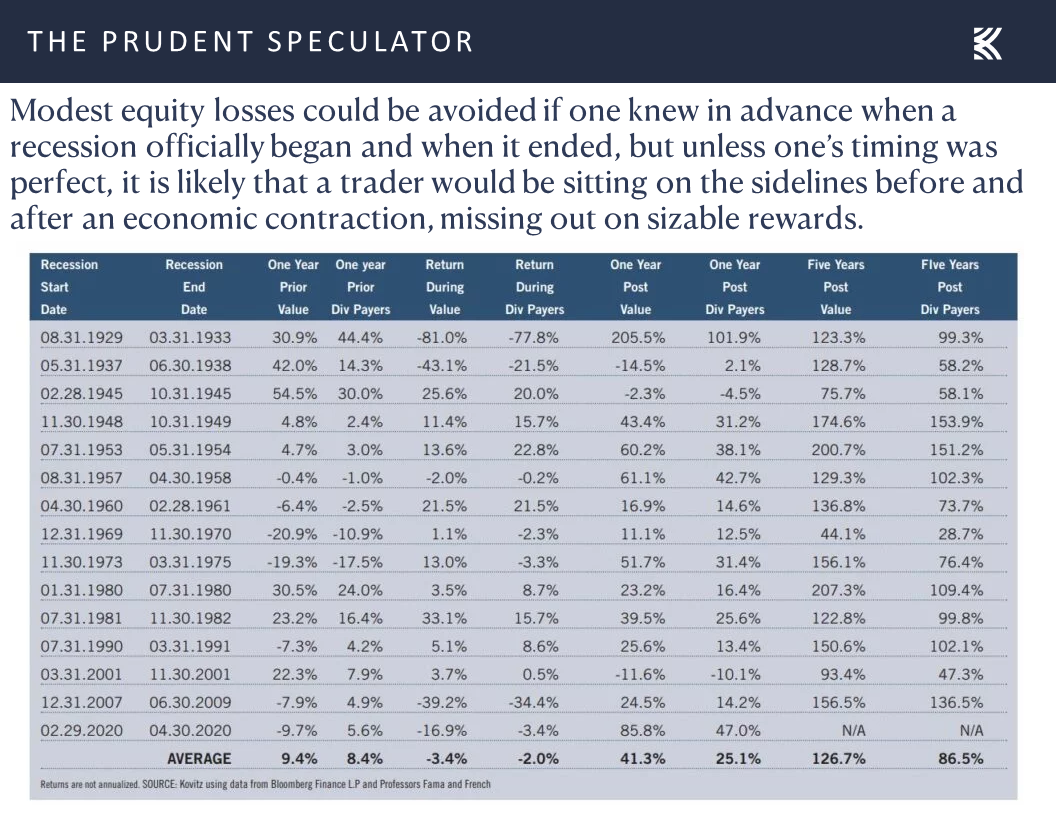

And even if the economy were to endure a recession, we continue to believe that the right course of action is to stick with Value and Dividend Paying stocks like those that we have long favored, given what has transpired before, during and especially after economic contractions.

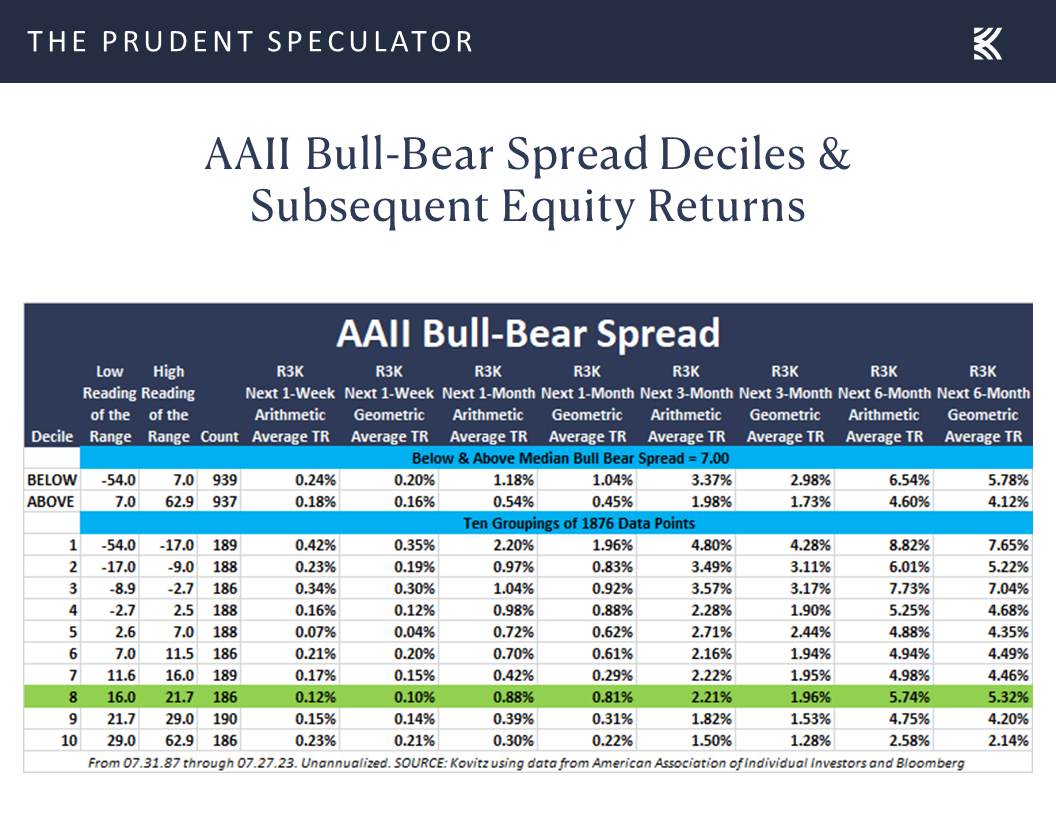

As always, we are braced for downside volatility, especially after the big run-up over the last two months, but we note that enthusiasm on Main Street pulled back last week with the Bull-Bear spread on the Sentiment Survey from the American Association of Individual Investors (AAII) shrinking to 20.8, down from an unusually high reading of 29.9 the week prior.

The AAII gauge is generally perceived as a contrarian indicator, but dividing up the Bull-Bear spreads into deciles shows that while average short-term returns are better when folks are pessimistic, they are still positive no matter the grouping, with decile 8 (where the current number resides) seeing surprisingly strong forward six-month performance.

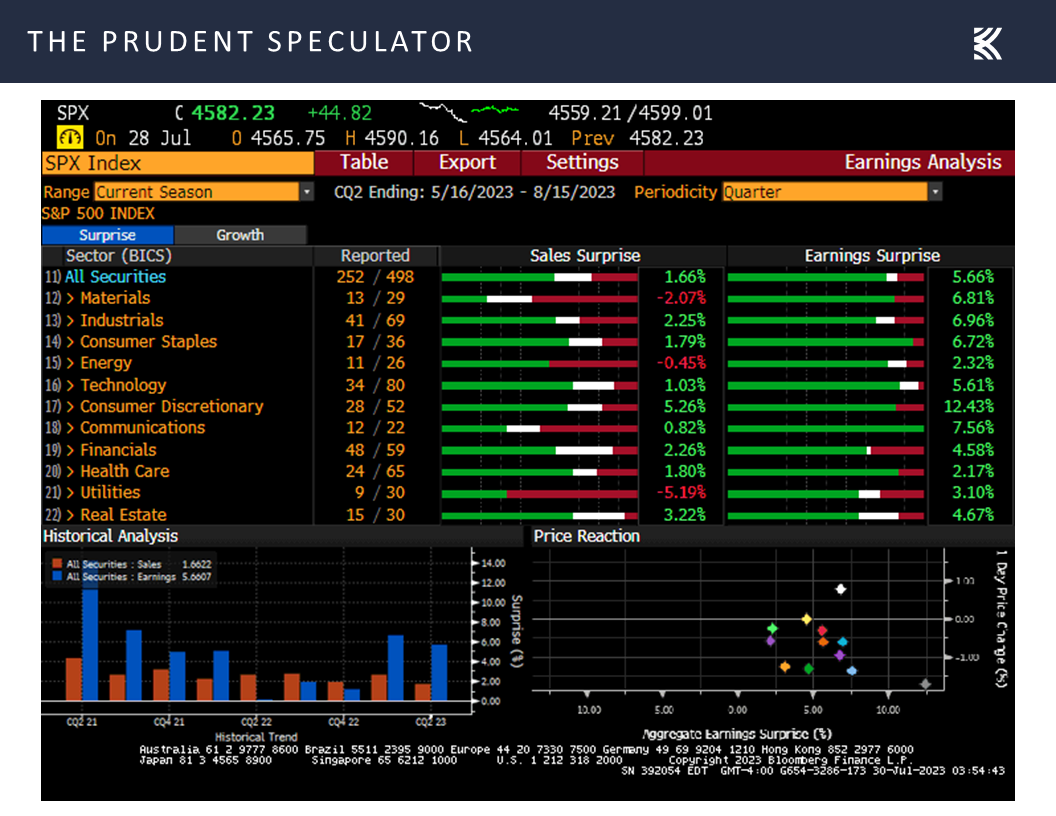

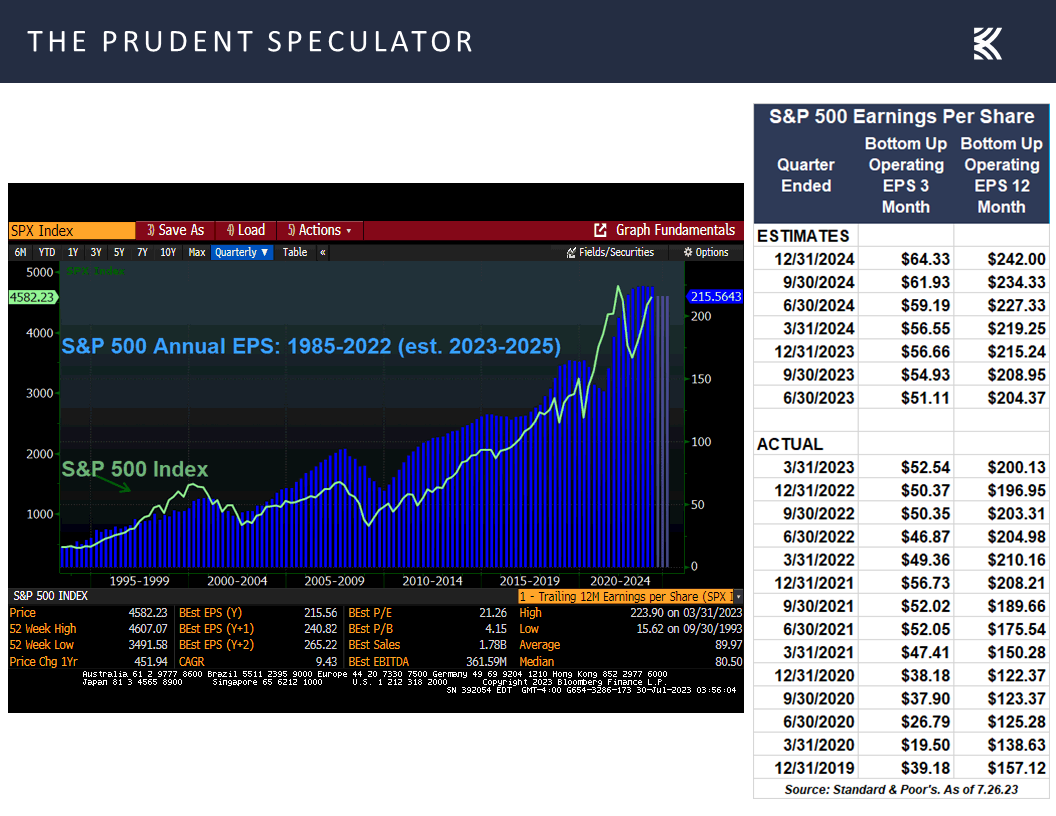

Earnings – Strong Q2 Results; Growth Still the Forecast This Year and in 2024

More importantly, and the primary reason for our continued optimism for stocks, Q2 corporate profits have been coming in much better than expected, with a whopping 80.9% of the 252 S&P 500 constituents to have reported thus far beating bottom-line estimates and 57.8% exceeding top-line forecasts.

Further, the outlook from both Bloomberg and Standard & Poor’s over the balance of the year and 2024 is for solid EPS growth,

which would boost the E in the Earnings to Price ratio, adding to the attractiveness of equities in general,

Valuations – Inexpensive Multiples for our Stocks

and our broadly diversified portfolios of what we believe to be undervalued stocks in particular.

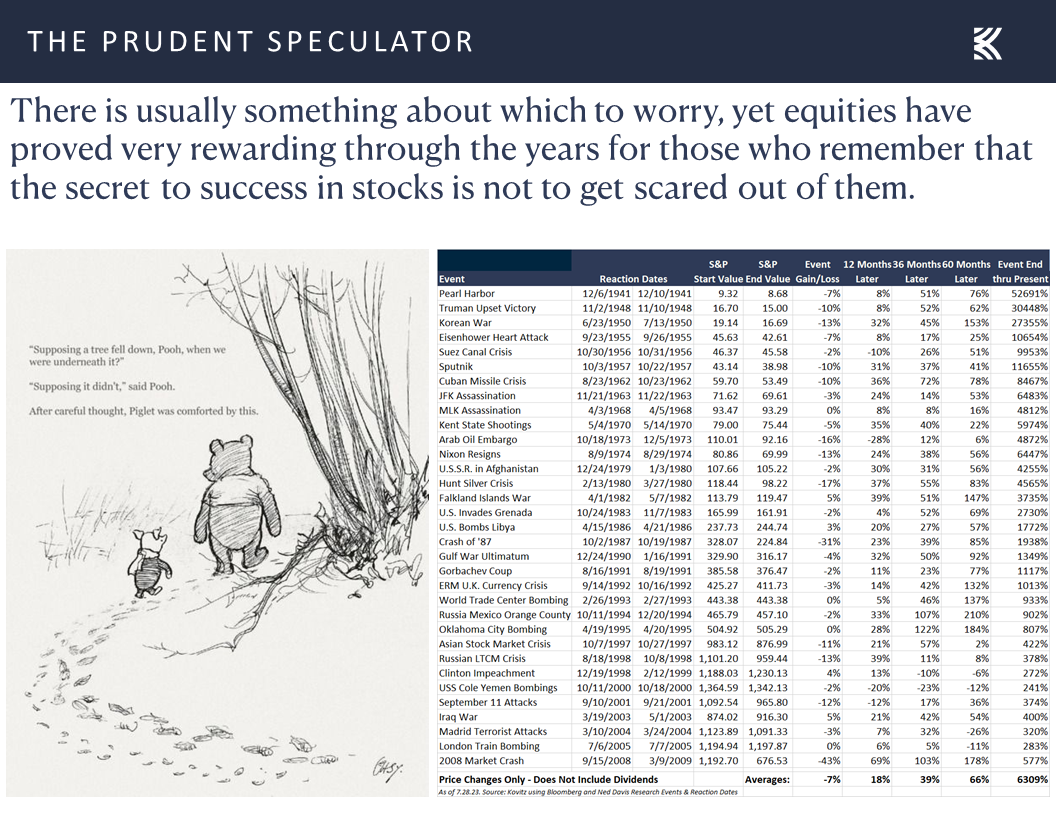

True, there are numerous issues about which to be concerned, so we know the sailing ahead will be far from smooth, but this is usually the case and we continue to argue that the secret to success in stocks is not to get scared out of them.

Stock News – Updates on fifteen stocks across ninedifferent sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Recession Chances, Earnings, Inflation, FOMC Decision and Economic News

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Recession Chances, Earnings, Inflation, FOMC Decision more Economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Week in Review – Rally Continues

Econ News – Favorable Numbers

FOMC Decision – As Expected, Fed Raises Rates 25 Basis Points

Recession Chances – World Bank and Fed Now Saying No U.S. Contraction This Year

Inflation – PCE Price Growth Slows Markedly, Wage Pressures Ease

Sentiment – AAII Bullishness Moderates Somewhat

Earnings – Strong Q2 Results; Growth Still the Forecast This Year and in 2024

Valuations – Inexpensive Multiples for our Stocks

Stock News – Updates on GOOG, MSFT, META, LRCX, GLW, INTC, GD, MDC, CMCSA, SNY, DLR, BMY, ONB, NYCB & MMM

Week in Review – Rally Continues

Although the winning streak for the Dow Jones Industrial Average came to an end after 13 days and the average stock did not perform nearly as well as the price- and market-capitalization- weighted indexes, it was another positive week for equity prices. The sizable advance, especially with market breadth broadening considerably since the end of May, provides more support for the assertion that time in the market trumps market timing,

even as our oft-stated admonition often falls on deaf ears, as evidenced by the miserable long-term returns put up by mutual fund investors in both stocks and bonds, per analytics from data-provider DALBAR.

Econ News – Favorable Numbers

No doubt, the gains last week were fueled by favorable economic statistics, with the first estimate of second quarter real (inflation-adjusted) GDP growth coming in at 2.4%, above expectations in the 1.8% to 2.0% range

the number of initial filings for unemployment benefits in the latest week dropping to a lower-than-projected 221,000

and the Conference Board’s measure of Consumer Confidence jumping to a two-year high in July and rising to 117.0, well above the long-term average of 96.7.

Other economic numbers were mixed as orders for durable goods bounded 4.7% higher in June, led by aircraft contracts, but new home sales last month fell short of estimates, falling 2.5% from the month prior’s revised figure to a seasonally adjusted annual rate of 697,000

while the University of Michigan’s final Consumer Sentiment gauge reading for July hit 71.6, down from a preliminary figure of 72.6 and well-below the historical norm, even as it was up sharply from June’s tally of 64.4.

FOMC Decision – As Expected, Fed Raises Rates 25 Basis Points

Not surprisingly, given that the Federal Reserve has long stated that it is data-dependent, Jerome H. Powell was relatively upbeat in his economic assessment featured in his opening remarks for his Press Conference this past Wednesday following the decision on interest rates.

Recent indicators suggest that economic activity has been expanding at a moderate pace. Growth in consumer spending appears to have slowed from earlier in the year. Although activity in the housing sector has picked up somewhat, it remains well below levels of a year ago, largely reflecting higher mortgage rates. And higher interest rates and slower output growth also appear to be weighing on business fixed investment.

The labor market remains very tight. Over the past three months, job gains averaged 244 thousand jobs per month, a pace below that seen earlier in the year but still a strong pace. The unemployment rate remains low, at 3.6 percent. There are some continuing signs that supply and demand in the labor market are coming into better balance. The labor force participation rate has moved up since last year, particularly for individuals aged 25 to 54 years.

Nominal wage growth has shown some signs of easing, and job vacancies have declined so far this year. While the jobs-to-workers gap has narrowed, labor demand still substantially exceeds the supply of available workers.

Continuing to target elevated inflation readings, the Fed Chair and his colleagues chose last week to hike the target for the Fed Funds rate by another 25 basis points, raising the benchmark lending rate to 5.5%,

Recession Chances – World Bank and Fed Now Saying No U.S. Contraction This Year

even as the tabulation provided by Bloomberg of the probability of a U.S. recession in the next 12 months stood at 60%.

Of course, Chair Powell said in response to a question at the Press Conference, “So, the staff now has a noticeable slowdown in growth starting later this year in the forecast, but given the resilience of the economy recently, they are no longer forecasting a recession,” while the first estimate for Q3 real U.S. GDP growth from the Atlanta Fed was a very robust 3.5%.

Further, the World Bank last week boosted its estimate for global GDP growth this year to 3.0%, while the group’s current projection for real U.S. growth is 1.8% in 2023 and 1.0% in 2024.

Obviously, there is a disconnect between market-based recession expectations and those of the World Bank and the Federal Reserve, but a so-called “soft landing” for the U.S. economy is making its way more heavily into the lexicon,

Inflation – PCE Price Growth Slows Markedly, Wage Pressures Ease

especially after the Bureau of Economic Analysis (BEA) reported on Friday that the Personal Consumption Expenditure (PCE) price index rose by just 3.0% in June, down from a 3.8% increase in May and the smallest advance since October 2021. Even better, the Federal Reserve’s preferred measure of inflation, the Core PCE, saw an increase of 4.1%, down from 4.6% the month prior,

while a separate report out the same day from the Labor Department showed more easing of inflationary pressures as wage growth (personal income) slowed in June, climbing 0.3%, even as consumer spending rose 0.5%.

Sentiment – AAII Bullishness Moderates Somewhat

No doubt, plenty of uncertainty remains about the health of the U.S. economy and the potential for additional Fed rate hikes, but the Fed Funds futures market suggests that Jerome Powell & Co. are about at the end of their tightening cycle,

which is in keeping with what the Federal Reserve Board members and Federal Reserve Bank presidents estimated (5.6% year-end Fed Funds rate) in June.

And even if the economy were to endure a recession, we continue to believe that the right course of action is to stick with Value and Dividend Paying stocks like those that we have long favored, given what has transpired before, during and especially after economic contractions.

As always, we are braced for downside volatility, especially after the big run-up over the last two months, but we note that enthusiasm on Main Street pulled back last week with the Bull-Bear spread on the Sentiment Survey from the American Association of Individual Investors (AAII) shrinking to 20.8, down from an unusually high reading of 29.9 the week prior.

The AAII gauge is generally perceived as a contrarian indicator, but dividing up the Bull-Bear spreads into deciles shows that while average short-term returns are better when folks are pessimistic, they are still positive no matter the grouping, with decile 8 (where the current number resides) seeing surprisingly strong forward six-month performance.

Earnings – Strong Q2 Results; Growth Still the Forecast This Year and in 2024

More importantly, and the primary reason for our continued optimism for stocks, Q2 corporate profits have been coming in much better than expected, with a whopping 80.9% of the 252 S&P 500 constituents to have reported thus far beating bottom-line estimates and 57.8% exceeding top-line forecasts.

Further, the outlook from both Bloomberg and Standard & Poor’s over the balance of the year and 2024 is for solid EPS growth,

which would boost the E in the Earnings to Price ratio, adding to the attractiveness of equities in general,

Valuations – Inexpensive Multiples for our Stocks

and our broadly diversified portfolios of what we believe to be undervalued stocks in particular.

True, there are numerous issues about which to be concerned, so we know the sailing ahead will be far from smooth, but this is usually the case and we continue to argue that the secret to success in stocks is not to get scared out of them.

Stock News – Updates on fifteen stocks across ninedifferent sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.