The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss risks of recession, corporate profits, an economic update more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – 8 Stocks for 3 Portfolios

Week In Review – Stocks Pull Back

Long-Term Perspective – Over Time, the Economy, EPS and Dividends Have Grown

Fitch Surprise – What Buffett, Dimon and History Have to Say About the U.S. Credit Rating Downgrade

Econ Update – Mixed ISM and Jobs Numbers

Risk of Recession – Not A Reason to Sell Stocks

Corporate Profits – Excellent Q2 Reports

Valuations – Inexpensive Multiples for our Stocks

Stock News – Updates on twenty stocks across twelve different sectors

Week in Review – Rally Continues

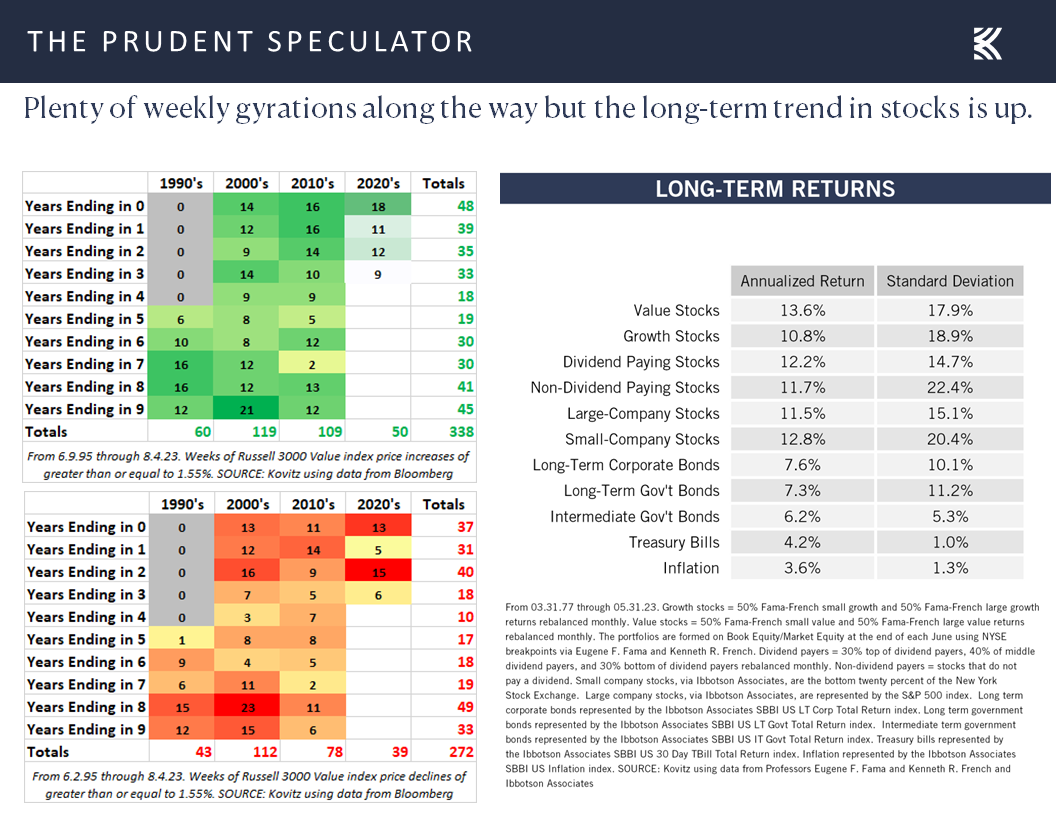

While Value fared better than Growth, with the Russell 3000 Value index losing “only” 1.55% on a price basis, the week just ended provided another reminder that stock prices move in both directions.

Long-Term Perspective – Over Time, the Economy, EPS and Dividends Have Grown

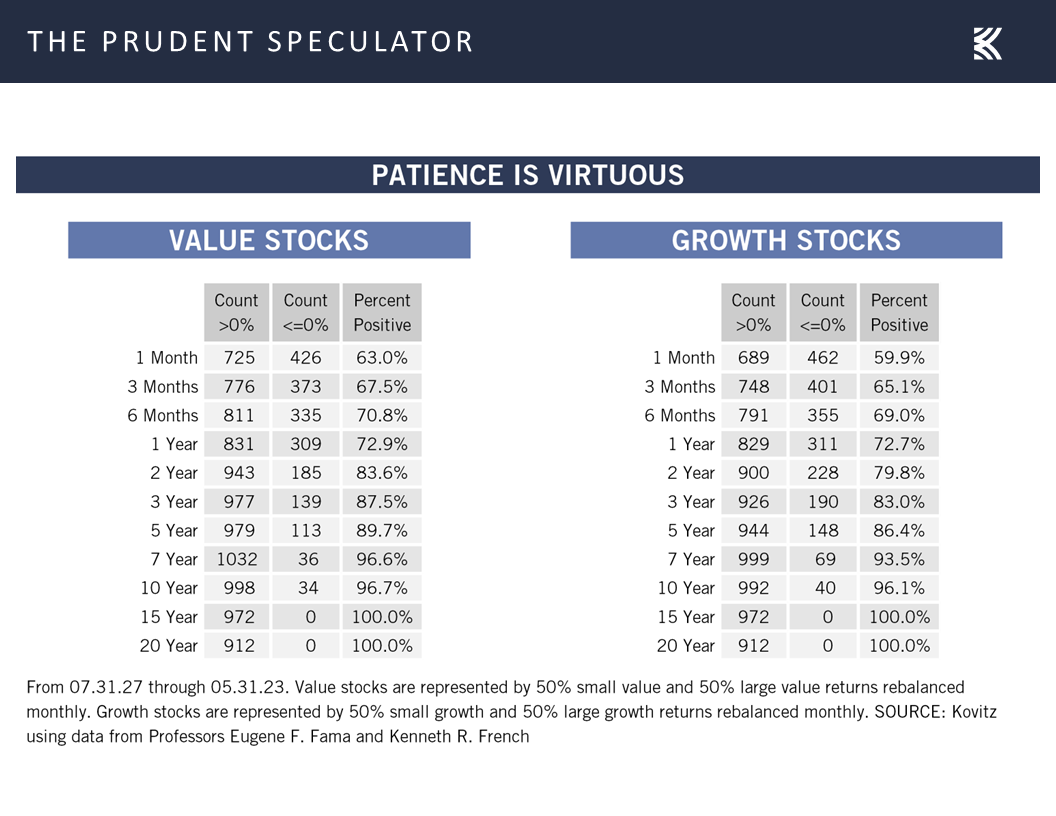

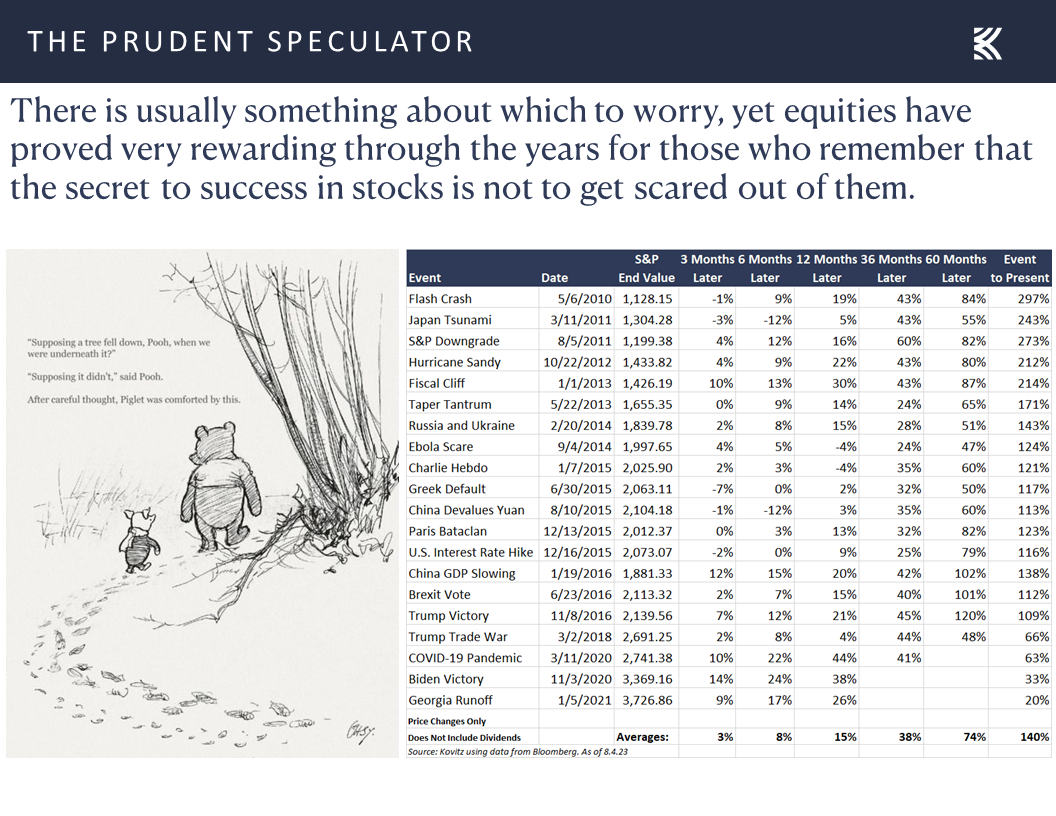

Of course, the chart above shows that there have been more sizable winning weeks than losing ones AND that Value stocks, like those that we have long championed, have enjoyed the best long-term returns. The key has been to stick with undervalued stocks through thick and thin, especially as history shows the odds of losing money in Value have been 37.0% when measured over one month time spans. However, hold for one year and the red-ink probability drops to 27.1% and for five years it declines to 10.3%. Even better, for those of us who truly have a long-term time horizon, there has not been a 15-year period where Value stocks have failed to appreciate.

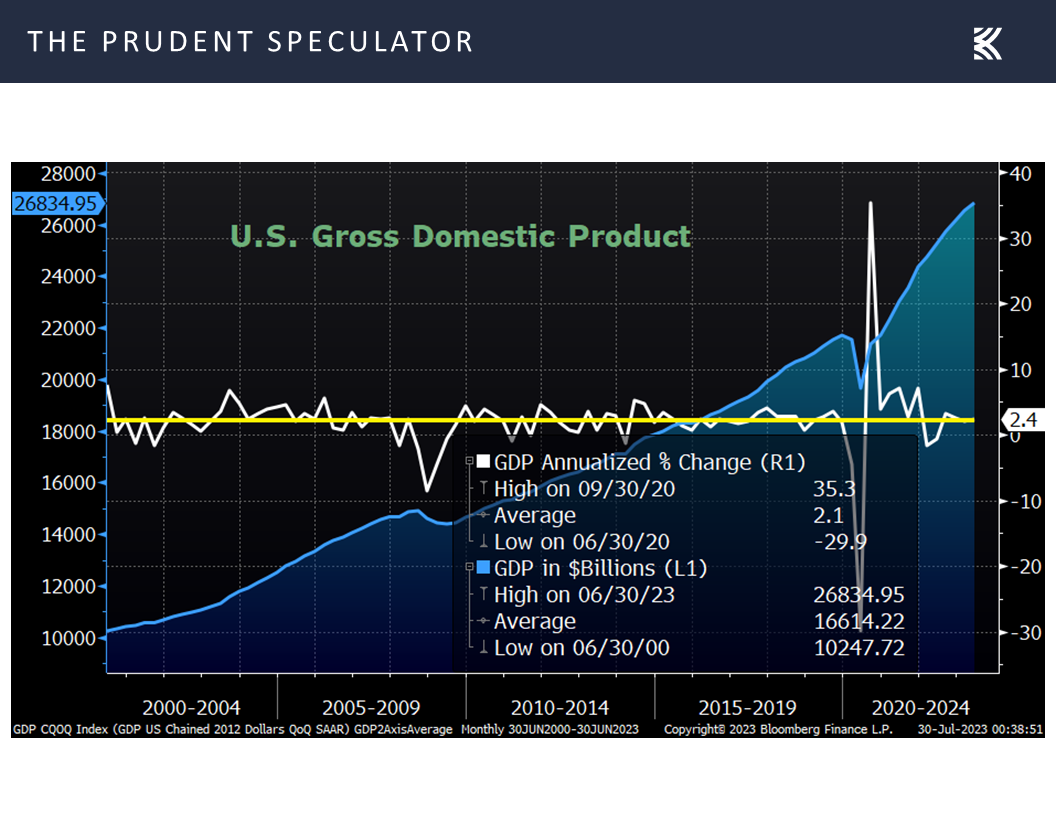

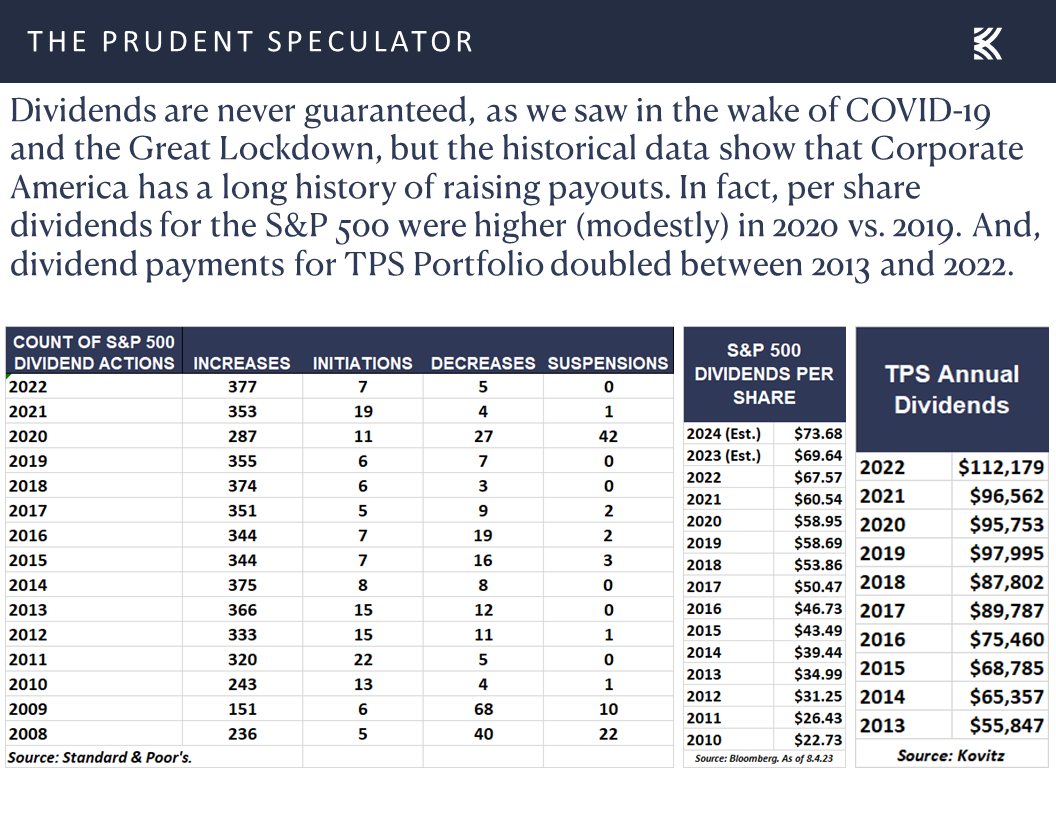

The reason for equity success over the years is relatively straightforward. Over time, the economy has expanded considerably,

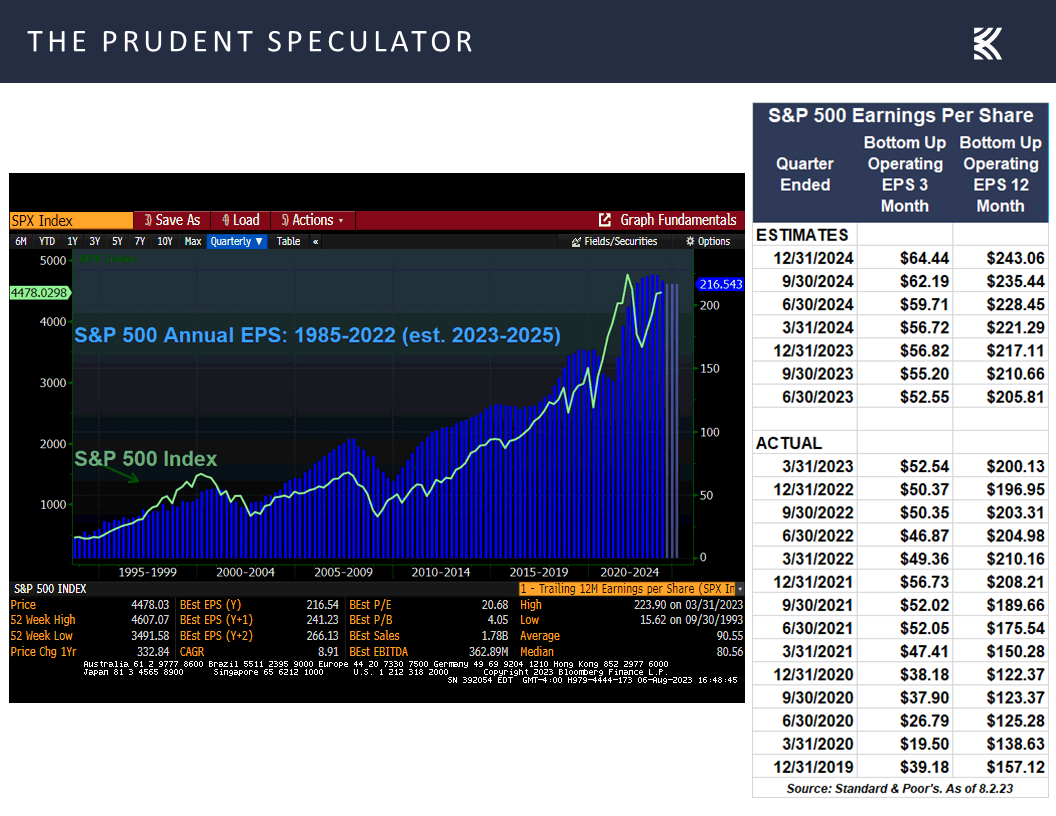

helping to fuel handsome growth in corporate profits,

which affords Corporate America the wherewithal to return capital to shareholders via stock repurchases and rising dividend payouts.

Fitch Surprise – What Buffett, Dimon and History Have to Say About the U.S. Credit Rating Downgrade

No doubt, there are numerous disconcerting events that must be navigated to achieve long-term rewards in stocks,

with the broad-based equity market advance since the end of May stopped in its tracks for the time being due to a downgrade of the U.S. credit rating to “AA+” from “AAA” this past Tuesday by Fitch Ratings.

Fitch said, “The rating downgrade of the United States reflects the expected fiscal deterioration over the next three years, a high and growing general government debt burden, and the erosion of governance relative to ‘AA’ and ‘AAA’ rated peers over the last two decades that has manifested in repeated debt limit standoffs and last-minute resolutions.”

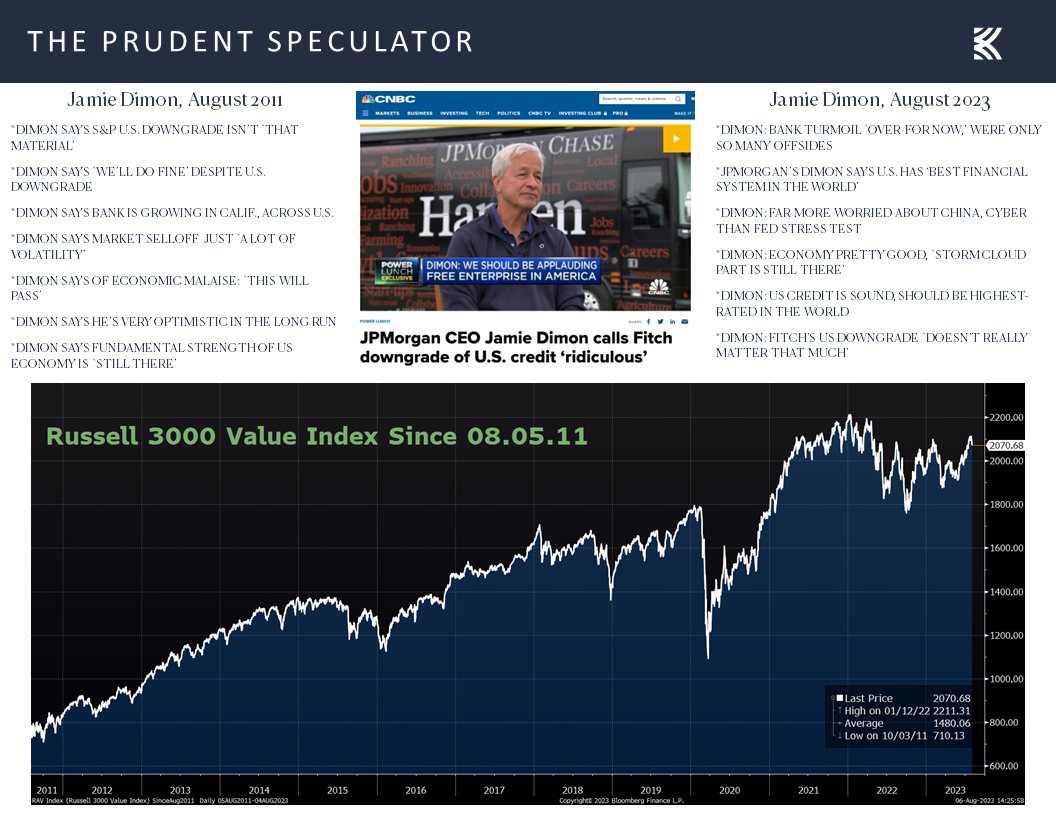

Not surprisingly, given that the move came a dozen years after Standard & Poor’s did the same thing, following arguably the most acrimonious debt-ceiling squabble in Washington history, most were quick to dismiss the Fitch move.

None other than Warren Buffett proclaimed, “There are some things people shouldn’t worry about. This is one.” The Oracle of Omaha added, “Berkshire bought $10 billion in U.S. Treasurys last Monday. We bought $10 billion in Treasurys this Monday. And the only question for next Monday is whether we will buy $10 billion in 3-month or 6-month T-bills.”

And Jamie Dimon was equally dismissive, with his comments last week on the right in the chart below. As students of market history, we also offer the JPMorgan Chase (JPM – $156.02) CEO’s remarks following the S&P downgrade of Uncle Sam’s credit back in 2011…along with a chart showing that the impact of that event was little more than a blip on the long-term uptrend of the Russell 3000 Value index.

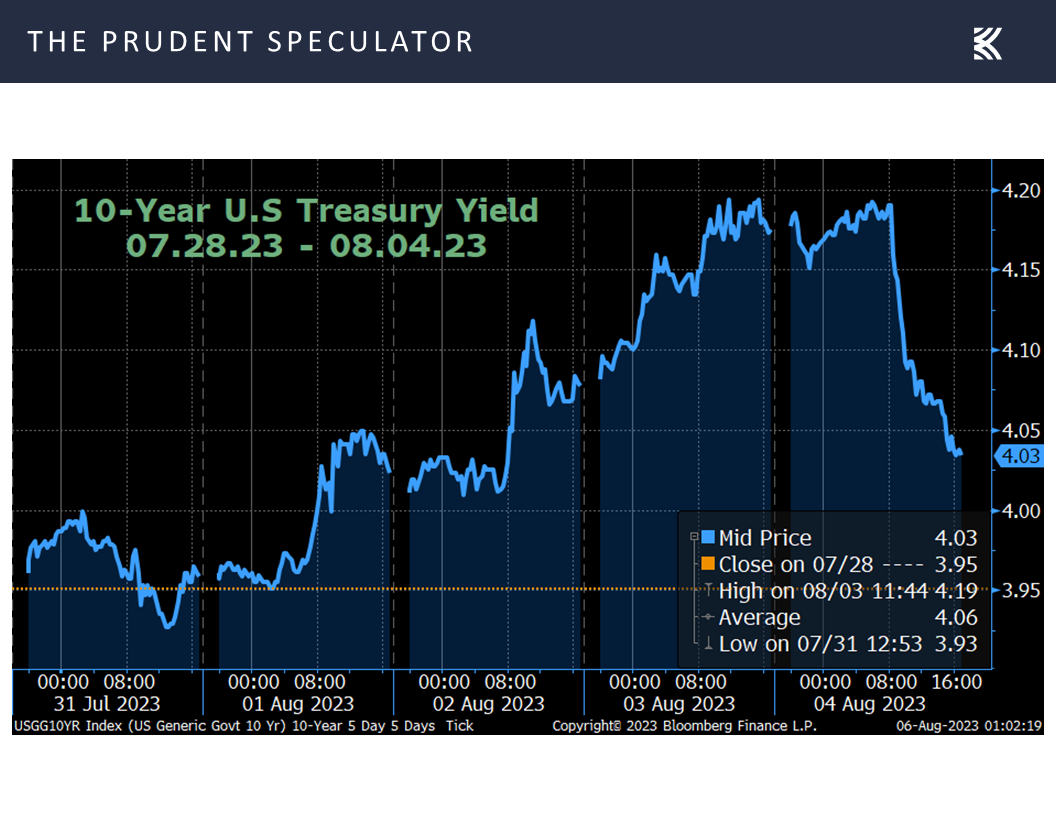

To be sure, the issues raised by Fitch are real, given the dysfunction in Washington and the $32.6 trillion in national debt, and the benchmark U.S. Treasury yield moved above 4.0% last week

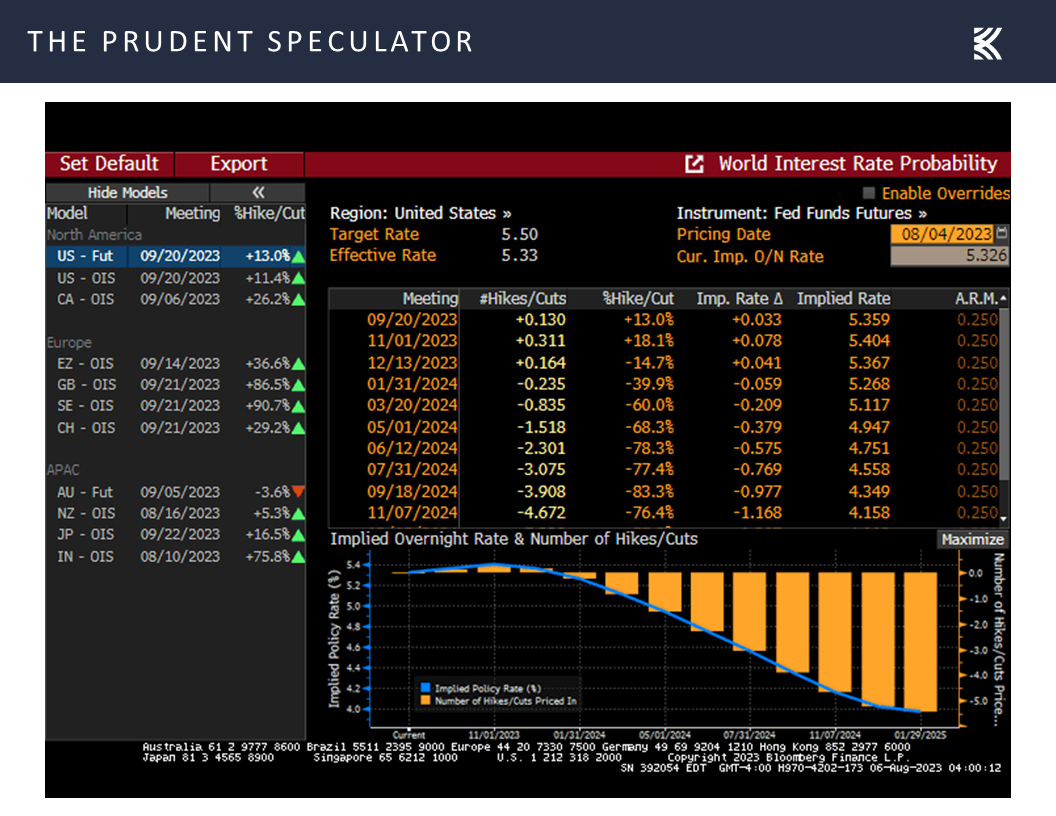

even as the market outlook for further interest rate hikes from the Federal Reserve did not show much change from the week prior, with the Fed Funds futures betting that there will be a series of rate cuts in 2024.

Econ Update – Mixed ISM and Jobs Numbers

Further, Fitch reminded, “Exceptional Strengths Support Ratings: Several structural strengths underpin the United States’ ratings. These include its large, advanced, well-diversified and high-income economy, supported by a dynamic business environment. Critically, the U.S. dollar is the world’s preeminent reserve currency, which gives the government extraordinary financing flexibility.”

Of course, Fitch also believes the U.S. economy will soon slip into recession: “Tighter credit conditions, weakening business investment, and a slowdown in consumption will push the U.S. economy into a mild recession in 4Q23 and 1Q24, according to Fitch projections. The agency sees U.S. annual real GDP growth slowing to 1.2% this year from 2.1% in 2022 and overall growth of just 0.5% in 2024. Job vacancies remain higher and the labor participation rate is still lower (by 1 pp) than pre-pandemic levels, which could negatively affect medium-term potential growth.”

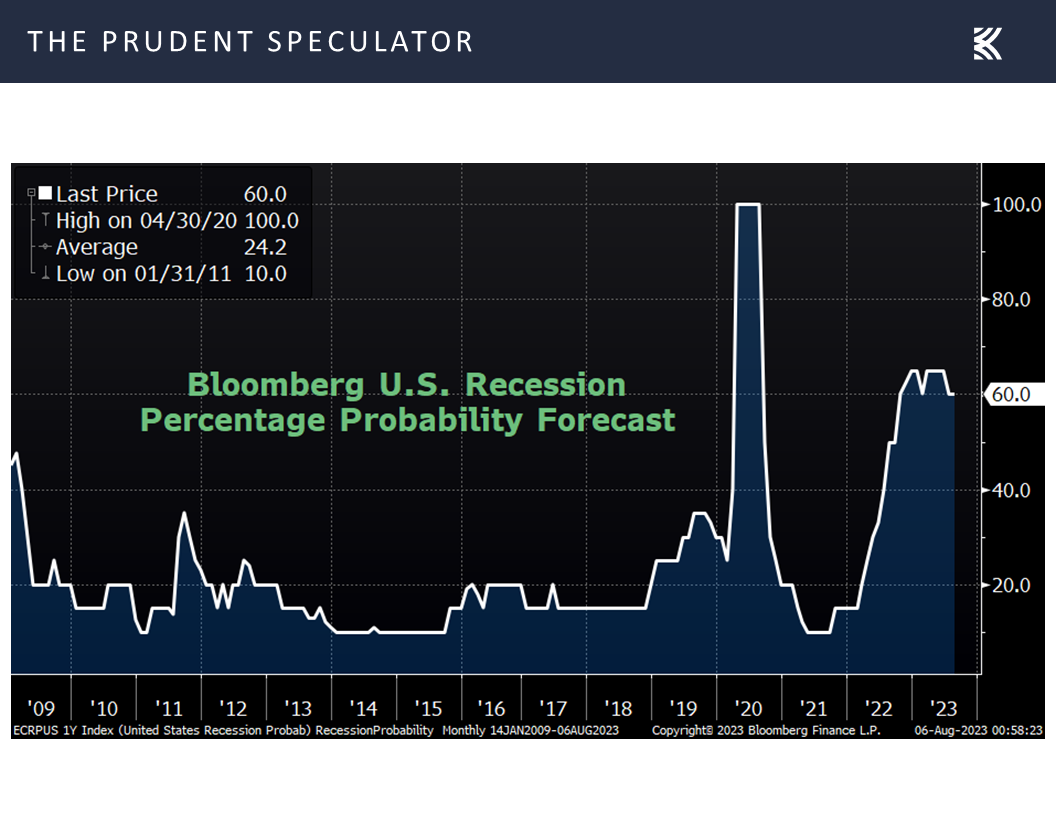

However, the jury is very much out on the economic contraction call, with several prominent forecasters now predicting a so-called soft landing and the latest odds of recession as tabulated by Bloomberg standing at 60%, down from 65% a few weeks ago.

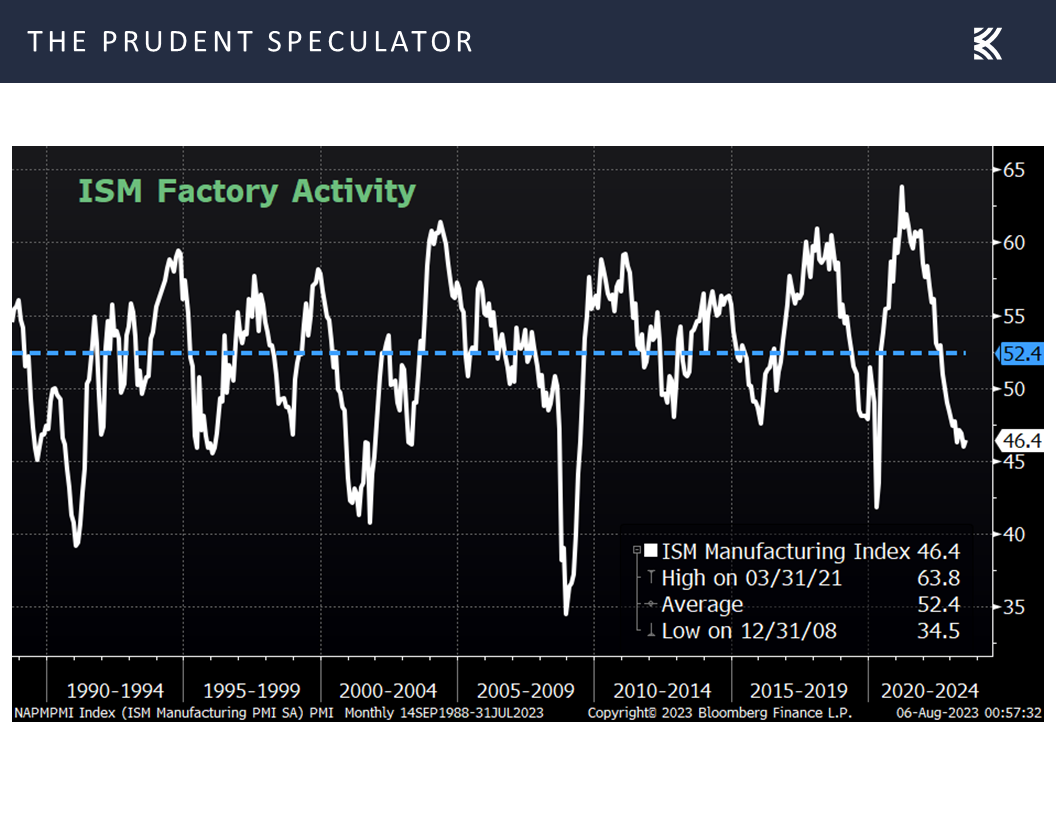

Obviously, a 60% chance of recession is an elevated percentage, but we heard from the Institute for Supply Management (ISM) last week, with the Manufacturing Survey for July inching up to 46.4 from 46.0 the month prior. ISM said, “A Manufacturing PMI® above 48.7 percent, over a period of time, generally indicates an expansion of the overall economy. Therefore, the July Manufacturing PMI® indicates the overall economy contracted for an eighth consecutive month after 30 straight months of expansion. The past relationship between the Manufacturing PMI® and the overall economy indicates that the July reading (46.4 percent) corresponds to a change of minus-0.8 percent in real gross domestic product (GDP) on an annualized basis.”

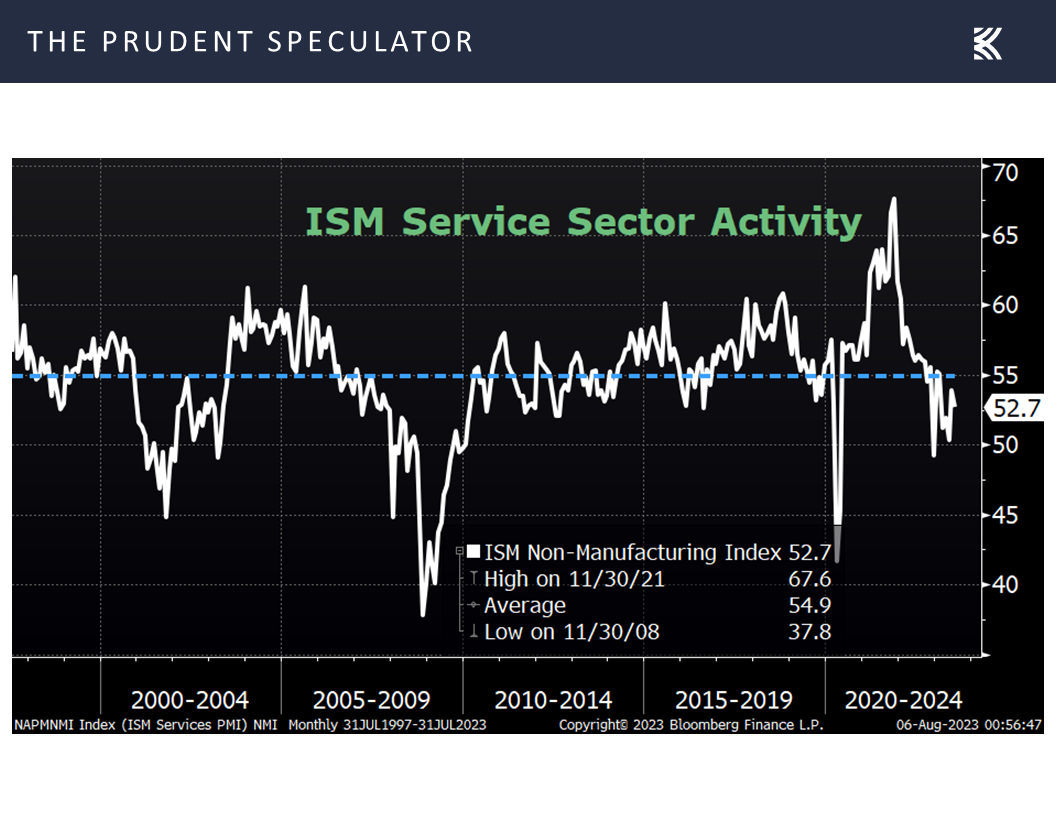

The ISM Non-Manufacturing index for July retreated to 52.7, down from 53.9 in June. However, ISM stated, “A Services PMI® above 49.9 percent, over time, generally indicates an expansion of the overall economy. Therefore, the July Services PMI® indicates the overall economy is growing for the seventh consecutive month after one month of contraction in December. The past relationship between the Services PMI® and the overall economy indicates that the Services PMI® for July (52.7 percent) corresponds to a 1-percent increase in real gross domestic product (GDP) on an annualized basis.”

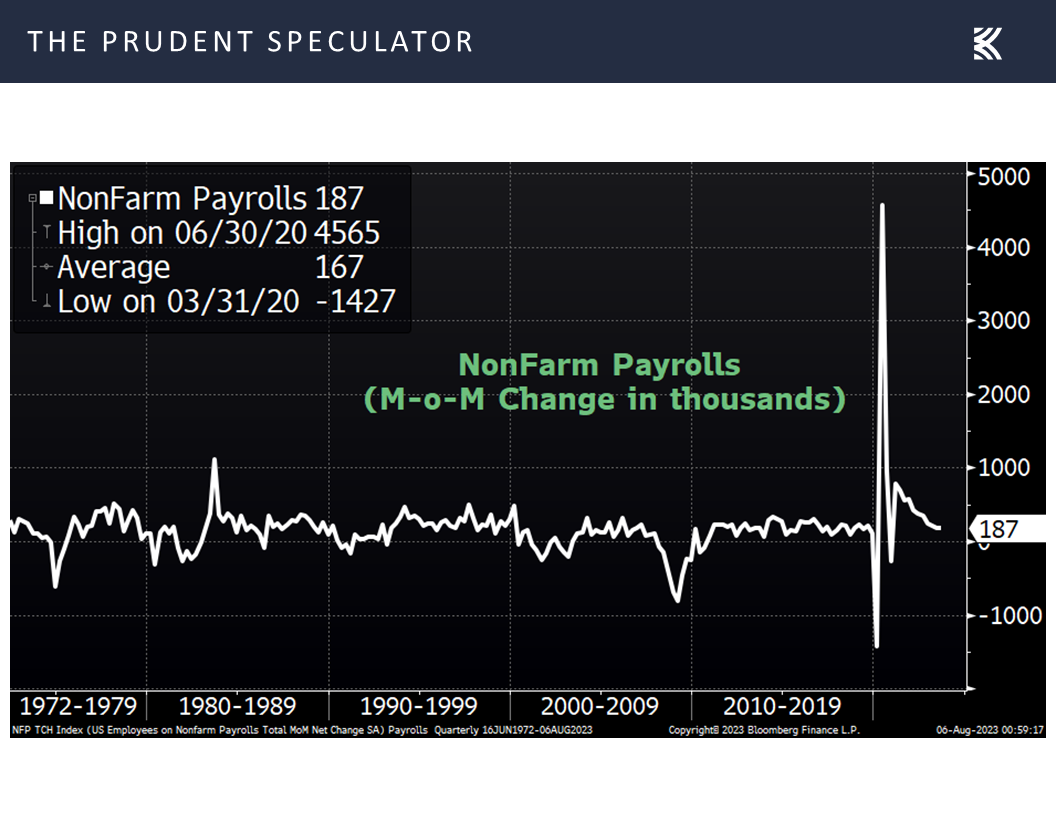

So, based on the ISM figures, the economy will either contract or expand…while we also might argue that the important monthly jobs numbers out on Friday were equally confusing. On the one hand, the economy added 187,000 new payrolls in July, but the tally was below expectations, while the May and June calculations were revised lower by a combined 49,000.

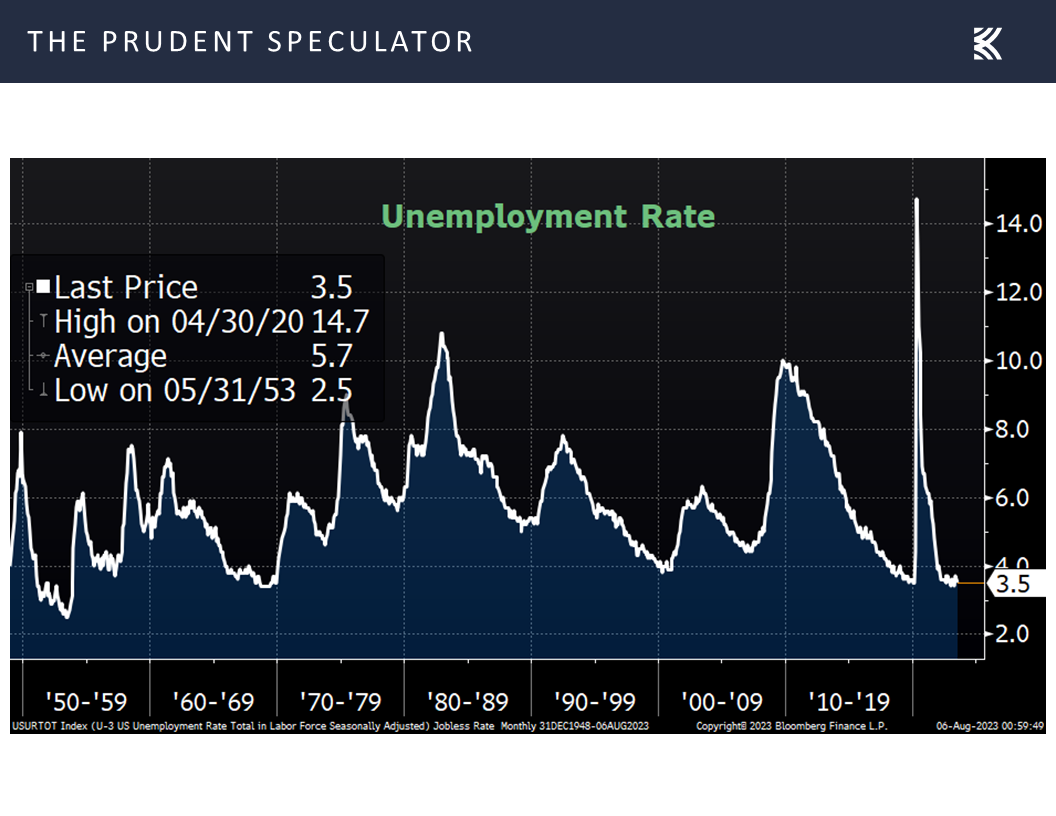

On the other hand, the unemployment rate fell to 3.5%,

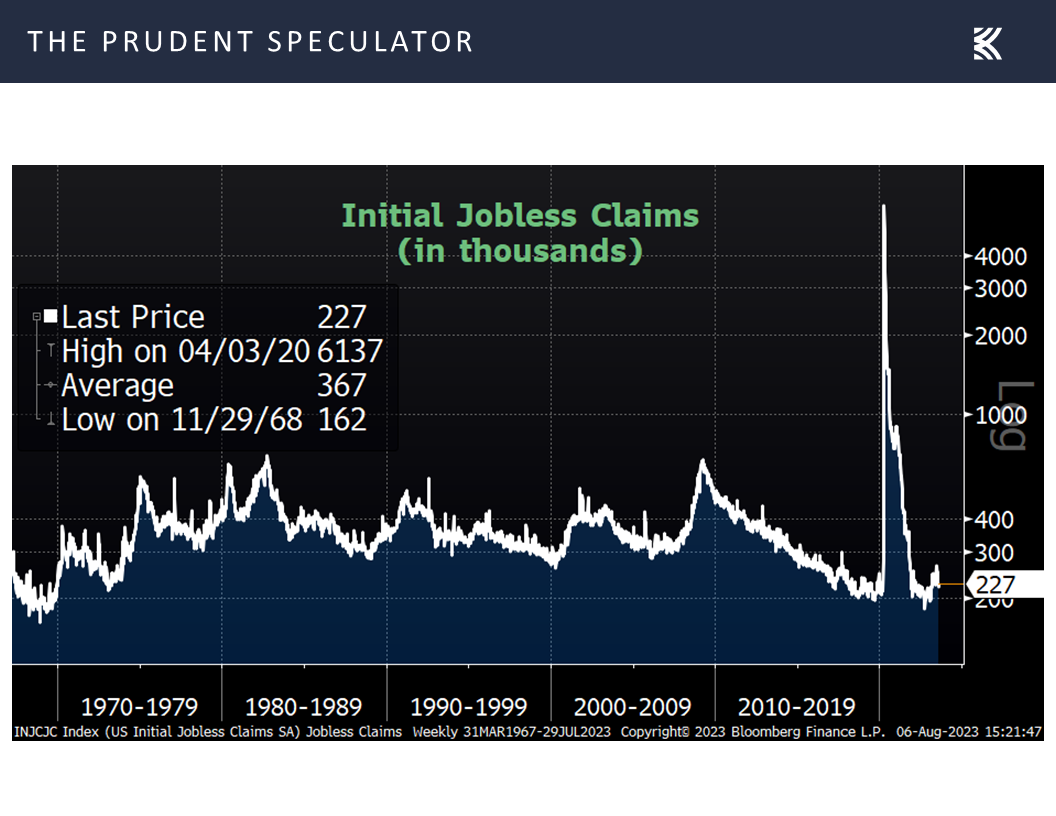

and the latest weekly count of first-time filings for unemployment benefits out the day before came in at a very low 227,000.

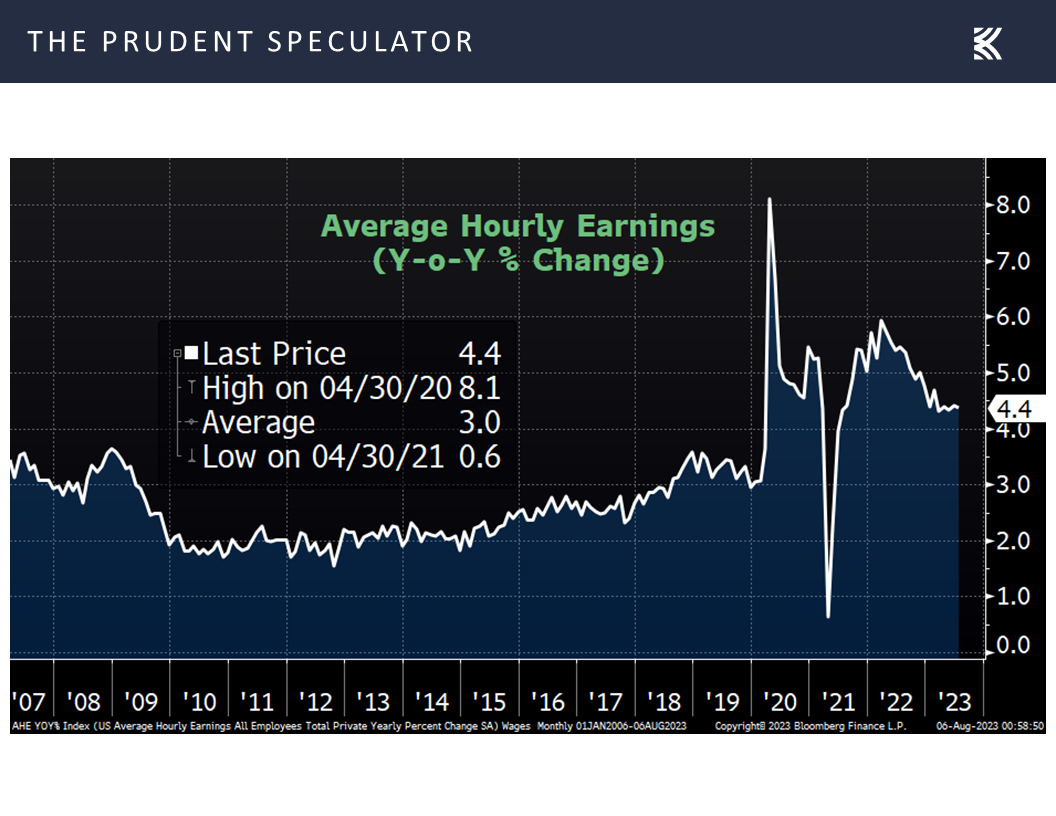

On the third hand, wage growth remained elevated, rising 4.4% in July, well above pre-pandemic levels and perhaps not falling as fast as the Federal Reserve might like,

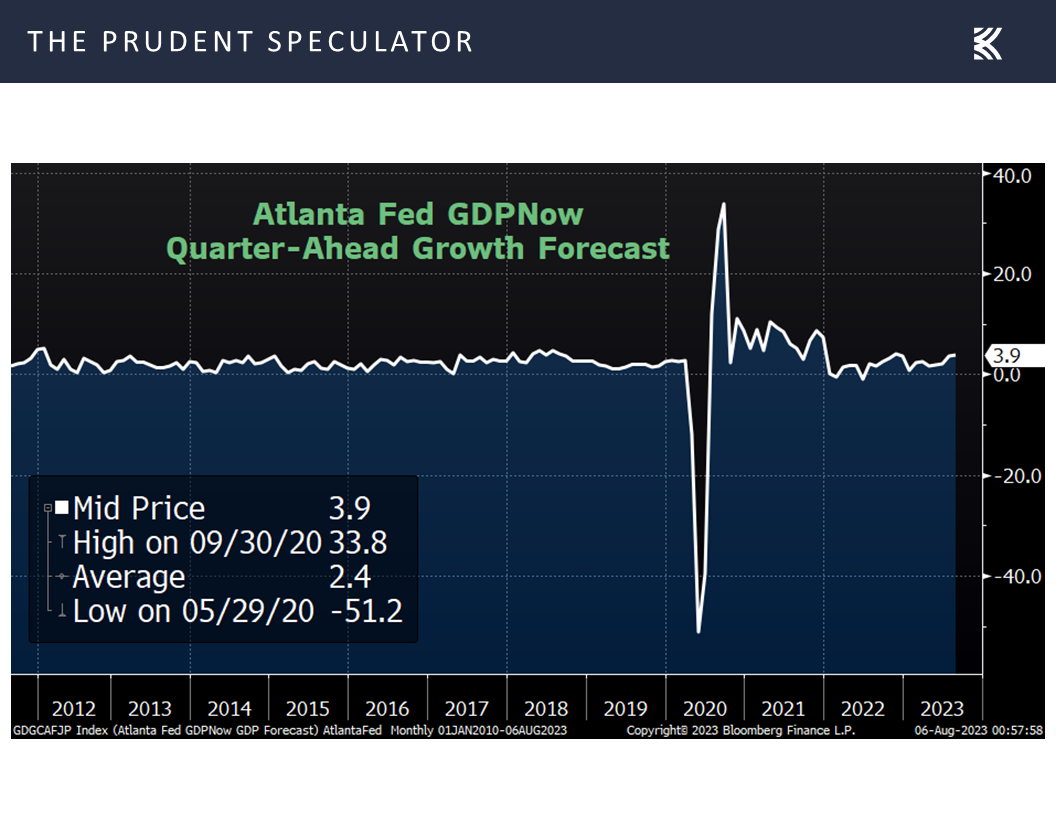

but the latest estimate from the Atlanta Fed for real (inflation adjusted) Q3 U.S. GDP growth hit 3.9% last week.

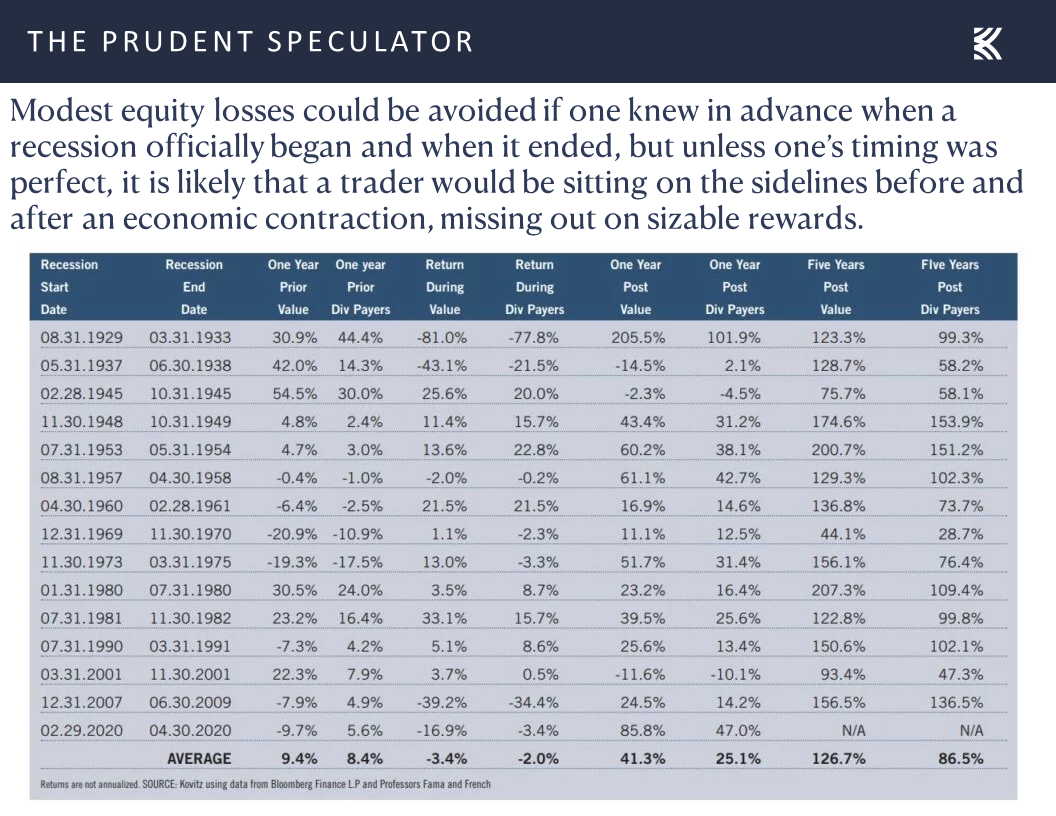

Risk of Recession – Not A Reason to Sell Stocks

Needless to say, the economic outlook is as clear as mud, so we’ll continue to lose little sleep over the prospects for a recession, especially given how difficult they have been to predict as well as what history has to say about the periods before, during and, importantly, after prior contractions have occurred.

Corporate Profits – Excellent Q2 Reports

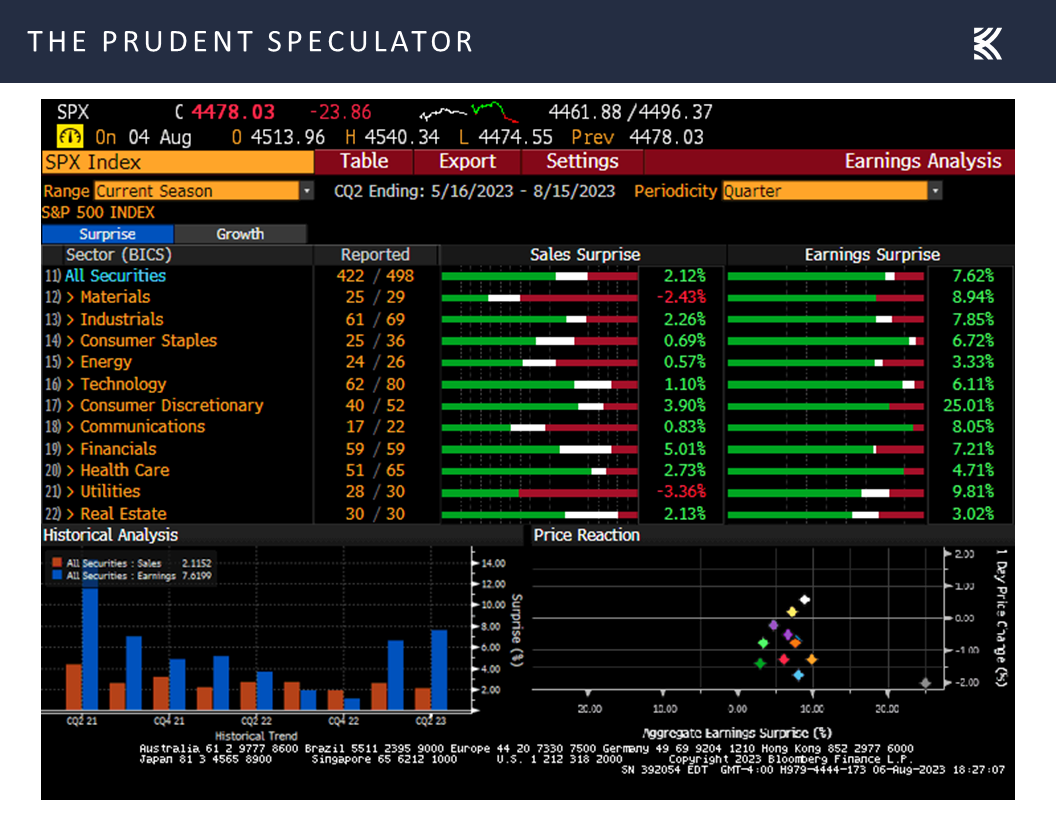

We also like what we have been seeing from Q2 earnings reports, with 80.0% of S&P 500 companies topping EPS expectations, a much better beat-rate than usual, and 58.7% exceeding top-line projections.

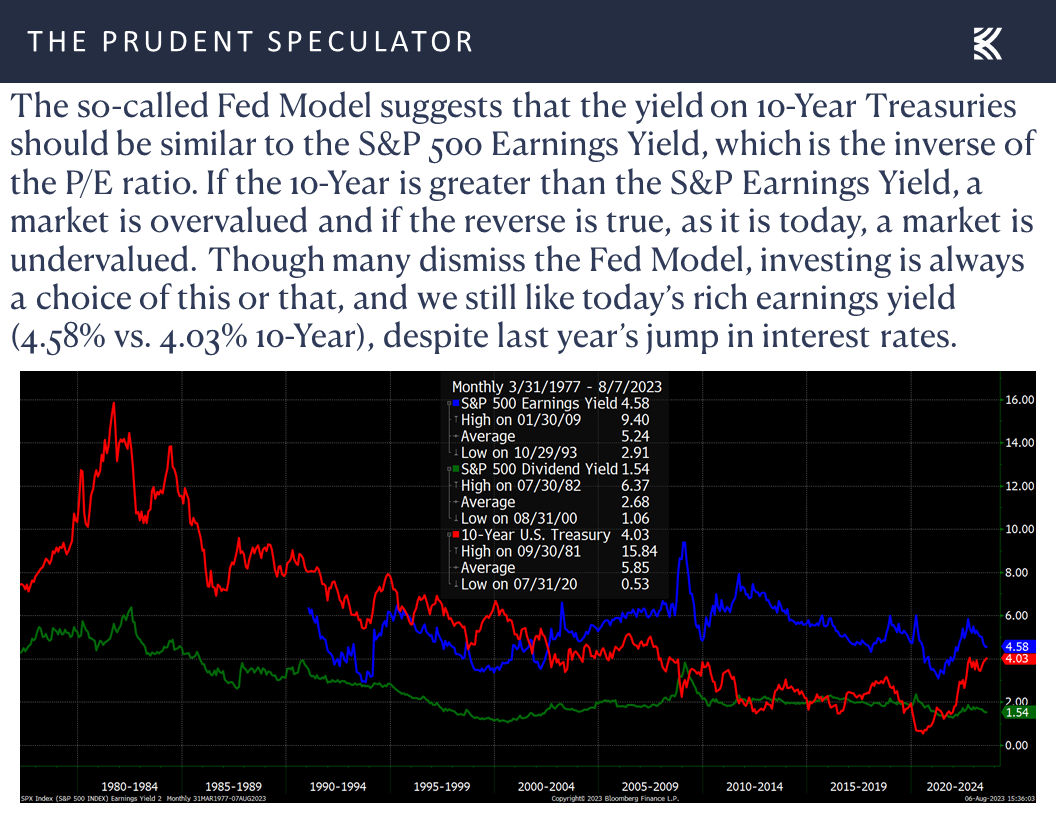

True, we have to expect more turbulence in the near term, especially as the 4%-yield mark on the 10-Year U.S. Treasury seems to be an important level for traders. Still, we note that the average yield for the government bond benchmark since the launch of The Prudent Speculator in March 1977 has been 5.85%, while we still think stocks in general are reasonably priced,

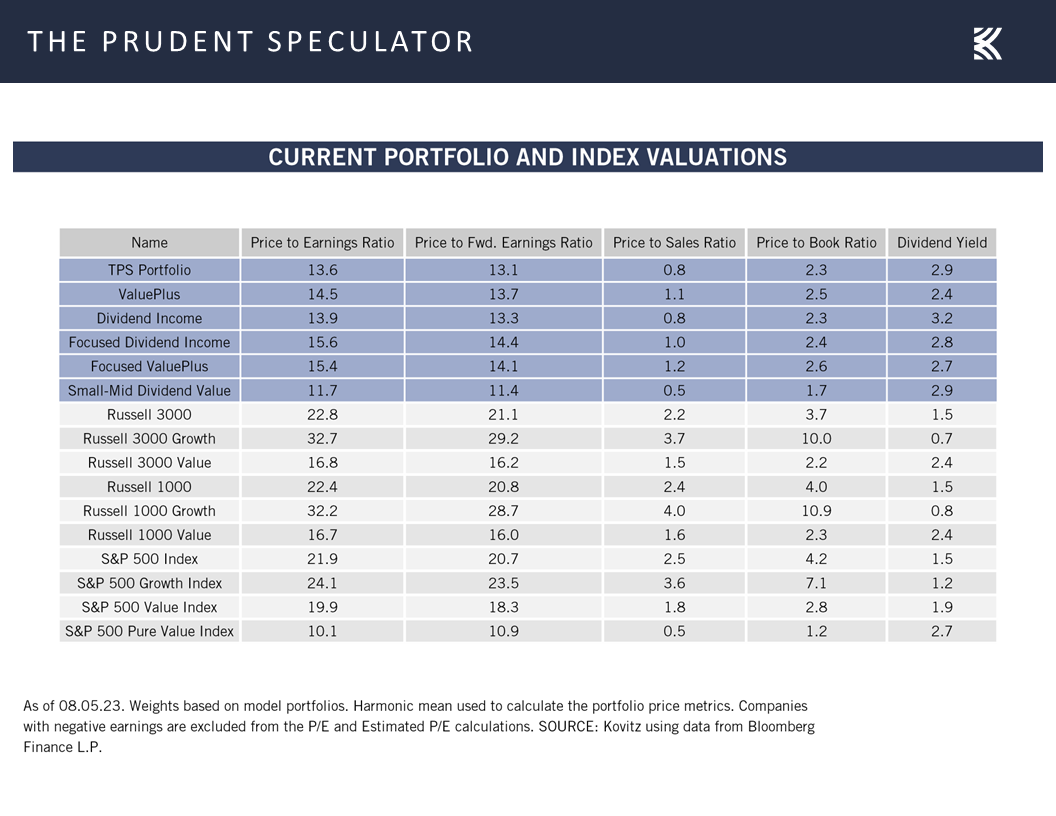

Valuations – Inexpensive Multiples for our Stocks

with the valuation metrics and dividend yields for our broadly diversified portfolios of what we believe to be undervalued stocks remaining very attractive.

Stock News – Updates on twenty stocks across twelve different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Risk of Recession, Corporate Profits, Economic Update and more

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss risks of recession, corporate profits, an economic update more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – 8 Stocks for 3 Portfolios

Week In Review – Stocks Pull Back

Long-Term Perspective – Over Time, the Economy, EPS and Dividends Have Grown

Fitch Surprise – What Buffett, Dimon and History Have to Say About the U.S. Credit Rating Downgrade

Econ Update – Mixed ISM and Jobs Numbers

Risk of Recession – Not A Reason to Sell Stocks

Corporate Profits – Excellent Q2 Reports

Valuations – Inexpensive Multiples for our Stocks

Stock News – Updates on twenty stocks across twelve different sectors

Week in Review – Rally Continues

While Value fared better than Growth, with the Russell 3000 Value index losing “only” 1.55% on a price basis, the week just ended provided another reminder that stock prices move in both directions.

Long-Term Perspective – Over Time, the Economy, EPS and Dividends Have Grown

Of course, the chart above shows that there have been more sizable winning weeks than losing ones AND that Value stocks, like those that we have long championed, have enjoyed the best long-term returns. The key has been to stick with undervalued stocks through thick and thin, especially as history shows the odds of losing money in Value have been 37.0% when measured over one month time spans. However, hold for one year and the red-ink probability drops to 27.1% and for five years it declines to 10.3%. Even better, for those of us who truly have a long-term time horizon, there has not been a 15-year period where Value stocks have failed to appreciate.

The reason for equity success over the years is relatively straightforward. Over time, the economy has expanded considerably,

helping to fuel handsome growth in corporate profits,

which affords Corporate America the wherewithal to return capital to shareholders via stock repurchases and rising dividend payouts.

Fitch Surprise – What Buffett, Dimon and History Have to Say About the U.S. Credit Rating Downgrade

No doubt, there are numerous disconcerting events that must be navigated to achieve long-term rewards in stocks,

with the broad-based equity market advance since the end of May stopped in its tracks for the time being due to a downgrade of the U.S. credit rating to “AA+” from “AAA” this past Tuesday by Fitch Ratings.

Fitch said, “The rating downgrade of the United States reflects the expected fiscal deterioration over the next three years, a high and growing general government debt burden, and the erosion of governance relative to ‘AA’ and ‘AAA’ rated peers over the last two decades that has manifested in repeated debt limit standoffs and last-minute resolutions.”

Not surprisingly, given that the move came a dozen years after Standard & Poor’s did the same thing, following arguably the most acrimonious debt-ceiling squabble in Washington history, most were quick to dismiss the Fitch move.

None other than Warren Buffett proclaimed, “There are some things people shouldn’t worry about. This is one.” The Oracle of Omaha added, “Berkshire bought $10 billion in U.S. Treasurys last Monday. We bought $10 billion in Treasurys this Monday. And the only question for next Monday is whether we will buy $10 billion in 3-month or 6-month T-bills.”

And Jamie Dimon was equally dismissive, with his comments last week on the right in the chart below. As students of market history, we also offer the JPMorgan Chase (JPM – $156.02) CEO’s remarks following the S&P downgrade of Uncle Sam’s credit back in 2011…along with a chart showing that the impact of that event was little more than a blip on the long-term uptrend of the Russell 3000 Value index.

To be sure, the issues raised by Fitch are real, given the dysfunction in Washington and the $32.6 trillion in national debt, and the benchmark U.S. Treasury yield moved above 4.0% last week

even as the market outlook for further interest rate hikes from the Federal Reserve did not show much change from the week prior, with the Fed Funds futures betting that there will be a series of rate cuts in 2024.

Econ Update – Mixed ISM and Jobs Numbers

Further, Fitch reminded, “Exceptional Strengths Support Ratings: Several structural strengths underpin the United States’ ratings. These include its large, advanced, well-diversified and high-income economy, supported by a dynamic business environment. Critically, the U.S. dollar is the world’s preeminent reserve currency, which gives the government extraordinary financing flexibility.”

Of course, Fitch also believes the U.S. economy will soon slip into recession: “Tighter credit conditions, weakening business investment, and a slowdown in consumption will push the U.S. economy into a mild recession in 4Q23 and 1Q24, according to Fitch projections. The agency sees U.S. annual real GDP growth slowing to 1.2% this year from 2.1% in 2022 and overall growth of just 0.5% in 2024. Job vacancies remain higher and the labor participation rate is still lower (by 1 pp) than pre-pandemic levels, which could negatively affect medium-term potential growth.”

However, the jury is very much out on the economic contraction call, with several prominent forecasters now predicting a so-called soft landing and the latest odds of recession as tabulated by Bloomberg standing at 60%, down from 65% a few weeks ago.

Obviously, a 60% chance of recession is an elevated percentage, but we heard from the Institute for Supply Management (ISM) last week, with the Manufacturing Survey for July inching up to 46.4 from 46.0 the month prior. ISM said, “A Manufacturing PMI® above 48.7 percent, over a period of time, generally indicates an expansion of the overall economy. Therefore, the July Manufacturing PMI® indicates the overall economy contracted for an eighth consecutive month after 30 straight months of expansion. The past relationship between the Manufacturing PMI® and the overall economy indicates that the July reading (46.4 percent) corresponds to a change of minus-0.8 percent in real gross domestic product (GDP) on an annualized basis.”

The ISM Non-Manufacturing index for July retreated to 52.7, down from 53.9 in June. However, ISM stated, “A Services PMI® above 49.9 percent, over time, generally indicates an expansion of the overall economy. Therefore, the July Services PMI® indicates the overall economy is growing for the seventh consecutive month after one month of contraction in December. The past relationship between the Services PMI® and the overall economy indicates that the Services PMI® for July (52.7 percent) corresponds to a 1-percent increase in real gross domestic product (GDP) on an annualized basis.”

So, based on the ISM figures, the economy will either contract or expand…while we also might argue that the important monthly jobs numbers out on Friday were equally confusing. On the one hand, the economy added 187,000 new payrolls in July, but the tally was below expectations, while the May and June calculations were revised lower by a combined 49,000.

On the other hand, the unemployment rate fell to 3.5%,

and the latest weekly count of first-time filings for unemployment benefits out the day before came in at a very low 227,000.

On the third hand, wage growth remained elevated, rising 4.4% in July, well above pre-pandemic levels and perhaps not falling as fast as the Federal Reserve might like,

but the latest estimate from the Atlanta Fed for real (inflation adjusted) Q3 U.S. GDP growth hit 3.9% last week.

Risk of Recession – Not A Reason to Sell Stocks

Needless to say, the economic outlook is as clear as mud, so we’ll continue to lose little sleep over the prospects for a recession, especially given how difficult they have been to predict as well as what history has to say about the periods before, during and, importantly, after prior contractions have occurred.

Corporate Profits – Excellent Q2 Reports

We also like what we have been seeing from Q2 earnings reports, with 80.0% of S&P 500 companies topping EPS expectations, a much better beat-rate than usual, and 58.7% exceeding top-line projections.

True, we have to expect more turbulence in the near term, especially as the 4%-yield mark on the 10-Year U.S. Treasury seems to be an important level for traders. Still, we note that the average yield for the government bond benchmark since the launch of The Prudent Speculator in March 1977 has been 5.85%, while we still think stocks in general are reasonably priced,

Valuations – Inexpensive Multiples for our Stocks

with the valuation metrics and dividend yields for our broadly diversified portfolios of what we believe to be undervalued stocks remaining very attractive.

Stock News – Updates on twenty stocks across twelve different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.