The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. This week, we cover the Silicon Valley collapse, jobs numbers, interest rates, Fed hikes, unemployment rates, the Great Finacial Crisis and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades: 8 Buys for 4 Portfolios

Silicon Valley Collapse: Uninsured Deposits from Customers in Need of Cash & Long-Dated Un-hedged Assets

Riding to the Rescue: Uncle Sam With a Strong Response

Crisis Events: Keeping the Faith Through Thick and Thin

Interest Rates & Fed Rate Hikes: Market Grows Much More Dovish

Econ News: Jobs Numbers Remain Strong, But Wage Growth Slows

Valuations: Reasonable Metrics for our Portfolios

Corporate Profits: Solid Q4 EPS and Growth Projected for 2023 & 2024

Great Financial Crisis: Words of Wisdom from Warren Buffett in February 2009

Stock News – Updates on Regional Banks

Week In Review:

Silicon Valley Collapse: Uninsured Deposits from Customers in Need of Cash & Long-Dated Un-hedged Assets

One venture capitalist said it was as if someone screamed fire in a crowded theater when there is no fire.

And then when everyone rushes to the door, they knock over the oil lamp and there is a fire and it burns down the building.

And then that same person standing outside says, see I told you so.

While there are plenty of post-mortem details still to emerge, we might argue that the description above courtesy of CNBC.com is a good one to explain the incredible lightning-quick demise of Silicon Valley Bank (SIVB).

Long-time readers of this publication will recall that we had two ownership experiences of the California bank in the past. Happily, the first was in the 1990s and resulted in a 28% annualized return over our seven-year holding period while the second from 2001 to 2003 ended with a 41% annualized return.

Of course, in the 1990s, the bank’s assets were in the $1 billion range and during the early-2000s, they were in the $4 billion range. By December 2022, assets had grown above $200 billion, making Silicon Valley the 16th largest bank in the country, with a roster of clients in technology and life science/healthcare industries, including private equity and venture capital, climate technology, biopharma, enterprise software and fintech.

Per Bloomberg, investors and depositors tried to pull a whopping $42 billion from SIVB on Thursday in a colossal run on the bank, which was triggered by a crisis in confidence after Silicon Valley management on Wednesday disclosed that the company sold $21 billion of available-for-sale securities, realizing a $1.9 billion loss, and announced a proposed public offering of $1.25 billion of common stock and another $500 million of preferred stock.

While Silicon Valley said in a regulatory filing that day…

Our financial position enables us to take these strategic actions, which are intended to further bolster that position now and over the long term.

We are taking these actions because we expect continued higher interest rates, pressured public and private markets, and elevated cash burn levels from our clients as they invest in their businesses.

We are experienced at navigating market cycles and are well positioned to serve our clients through market volatility, with a high-quality, liquid balance sheet and strong capital ratios.

…the communication fell on deaf ears, with prominent venture capitalists instructing the companies they had seeded to pull their money out of the bank.

To be sure, with the benefit of 20-20 hindsight, Silicon Valley was incredibly reckless, given that management poured billions of dollars into long-term mortgage-backed securities and municipal bonds with minimal interest rate hedging as assets literally tripled during the Pandemic. The $91 billion (cost) of securities had an unrealized loss of $15 billion or so at the end of 2022, but regulatory requirements did not necessitate a write down as the assets arguably had minimal credit risk and they were intended to be held to maturity.

As such, there would not have been a liquidity issue if everyone wasn’t pounding on the proverbial doors demanding their money back. And it is highly unlikely that depositors would have been heading for the exits if they had the benefit of FDIC insurance, but sadly $151.5 billion of deposits in U.S. offices exceeded the FDIC insurance limit and $13.9 billion of foreign deposits had no backstopping from Uncle Sam. Total deposits showing on the balance sheet at the end of 2022 were $173.1 billion, meaning that a massive percentage (more than 95%) of the total had plenty of incentive to pull money out of SIVB.

Riding to the Rescue: Uncle Sam With a Strong Response

Happily, few banks in this country look like SIVB and we think the issues in play there are very much isolated. We do not know of any other bank that held the lion’s share of its assets in unhedged 10-year-or-longer-to maturity mortgage-backed securities, while operating with a massively uninsured deposit base made up of a set of customers across the private equity/venture capital landscape with very short-term cash needs at a time when capital committed to the space had dried up.

Contrast this with most regional banks across the country (especially those in our portfolios), whose depositors are typically a highly diverse group of individuals and businesses (the majority of whom tend to be substantially protected by FDIC insurance) and that we expect are unlikely to uproot their day-to-day operating funds.

Despite our arguments that the SIVB situation is idiosyncratic, we realize that the breathtaking run-on-the-bank has led to plenty of consternation for bank-stock investors in particular and the equity markets in general. Naturally, comparisons have been made to the collapse of Lehman Brothers and Washington Mutual during the Great Financial Crisis, but we believe that banks are far better capitalized today. Treasury Secretary Janet Yellen, concurs, saying on Friday, “The U.S. banking system remains resilient.”

Certainly, anything can happen, and there was plenty of chatter over the weekend warning of dire consequences if Washington doesn’t make uninsured SIVB depositors whole, or nearly whole. But we continue to believe that contagion is unlikely, given that few banks have tons of start-up business customers who burn through cash like those of Silicon Valley.

Ms. Yellen responded on Sunday, “Let me be clear that during the financial crisis, there were investors and owners of systemic large banks that were bailed out, and the reforms that have been put in place means that we’re not going to do that again. But we are concerned about depositors and are focused on trying to meet their needs.”

Obviously, we prefer not to have a rerun of the Great Financial Crisis, but that seems very unlikely after the following from the Department of the Treasury, Federal Reserve and FDIC on Sunday afternoon:

Today we are taking decisive actions to protect the U.S. economy by strengthening public confidence in our banking system. This step will ensure that the U.S. banking system continues to perform its vital roles of protecting deposits and providing access to credit to households and businesses in a manner that promotes strong and sustainable economic growth.

After receiving a recommendation from the boards of the FDIC and the Federal Reserve, and consulting with the President, Secretary Yellen approved actions enabling the FDIC to complete its resolution of Silicon Valley Bank, Santa Clara, California, in a manner that fully protects all depositors. Depositors will have access to all of their money starting Monday, March 13. No losses associated with the resolution of Silicon Valley Bank will be borne by the taxpayer.

We are also announcing a similar systemic risk exception for Signature Bank, New York, New York, which was closed today by its state chartering authority. All depositors of this institution will be made whole. As with the resolution of Silicon Valley Bank, no losses will be borne by the taxpayer.

Shareholders and certain unsecured debtholders will not be protected. Senior management has also been removed. Any losses to the Deposit Insurance Fund to support uninsured depositors will be recovered by a special assessment on banks, as required by law.

Finally, the Federal Reserve Board on Sunday announced it will make available additional funding to eligible depository institutions to help assure banks have the ability to meet the needs of all their depositors.

The U.S. banking system remains resilient and on a solid foundation, in large part due to reforms that were made after the financial crisis that ensured better safeguards for the banking industry. Those reforms combined with today’s actions demonstrate our commitment to take the necessary steps to ensure that depositors’ savings remain safe.

Certainly, making all depositors whole at Silicon Valley and Signature, included those who were uninsured, is powerful support against further runs on banks, while the tools provided well-capitalized regional banks allows them to handle sizable near-term deposit outflows.

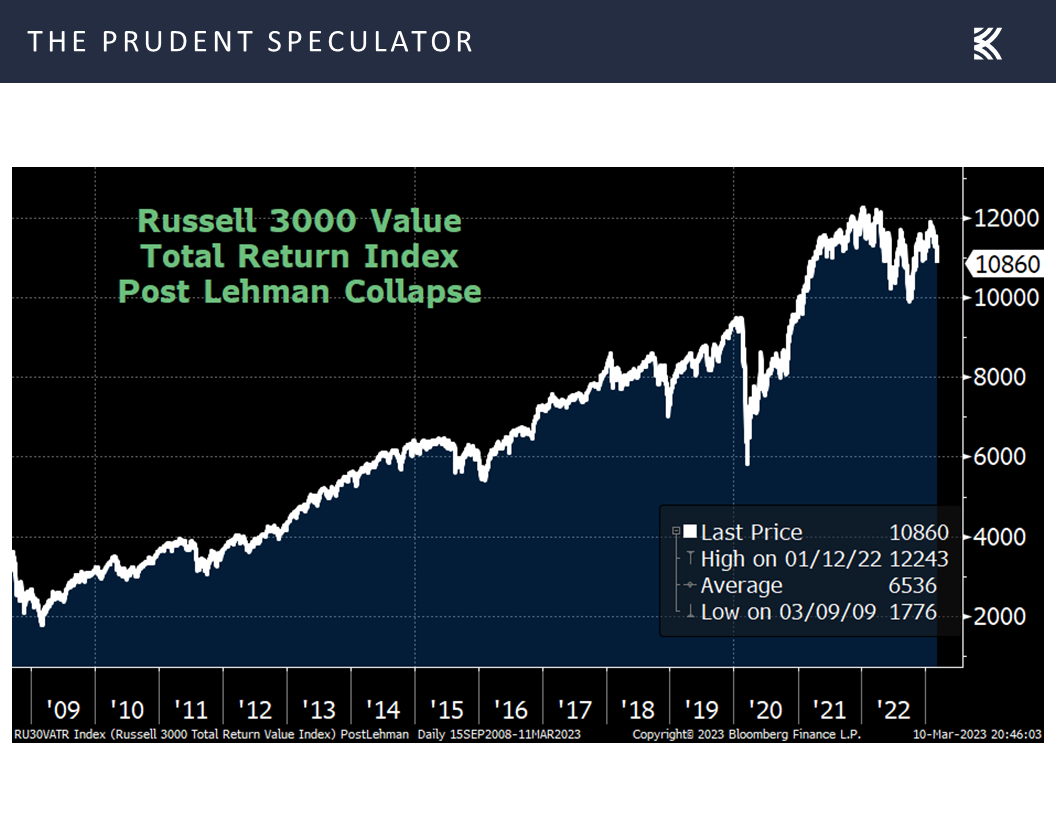

So, it would seem that a financial crisis has been averted. Still, we offer the reminder that through Friday, the Russell 3000 Value index had returned 225% since the collapse of Lehman Brothers in September 2008.

Crisis Events: Keeping the Faith Through Thick and Thin

True, the markets didn’t bottom for six months after Lehman, but we continue to think that no matter the near-term hurdles, time in the market trumps market timing, as the chart below illustrates the handsome gains enjoyed by equity holders who keep the faith to stick in times of turmoil.

True, the markets didn’t bottom for six months after Lehman, but we continue to think that no matter the near-term hurdles, time in the market trumps market timing, as the chart below illustrates the handsome gains enjoyed by equity holders who keep the faith to stick in times of turmoil.

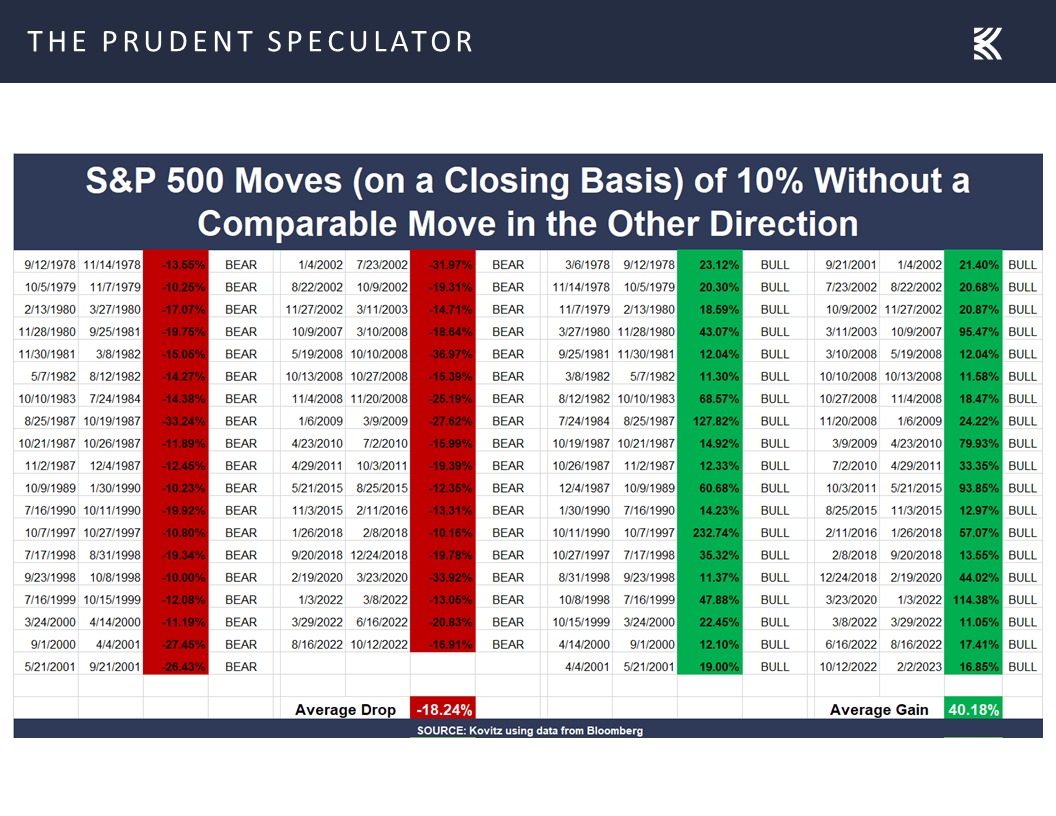

Illustrating why we like to say that the only problem with market timing is getting the timing right, we suspect that few who managed to exit their equity holdings prior to the Lehman collapse were able to get back into stocks at an opportune time. After all, there were three rebounds of 10% or greater for the S&P 500 just from October 2008 to January 2009, before stocks ultimately hit their lows in March 2009.

Given that there have been 10 downturns and 11 upturns of that same 10% or greater magnitude in the 14 years since March 2009, volatility is very much a normal part of the investment process. Yes, it would be nice to avoid the inevitable trips south, and the current downturn has not yet made its way on to the 10% table above, but as Bernard Baruch states, “Only liars manage to always be out during bad times and in during good times.”

Given that there have been 10 downturns and 11 upturns of that same 10% or greater magnitude in the 14 years since March 2009, volatility is very much a normal part of the investment process. Yes, it would be nice to avoid the inevitable trips south, and the current downturn has not yet made its way on to the 10% table above, but as Bernard Baruch states, “Only liars manage to always be out during bad times and in during good times.”

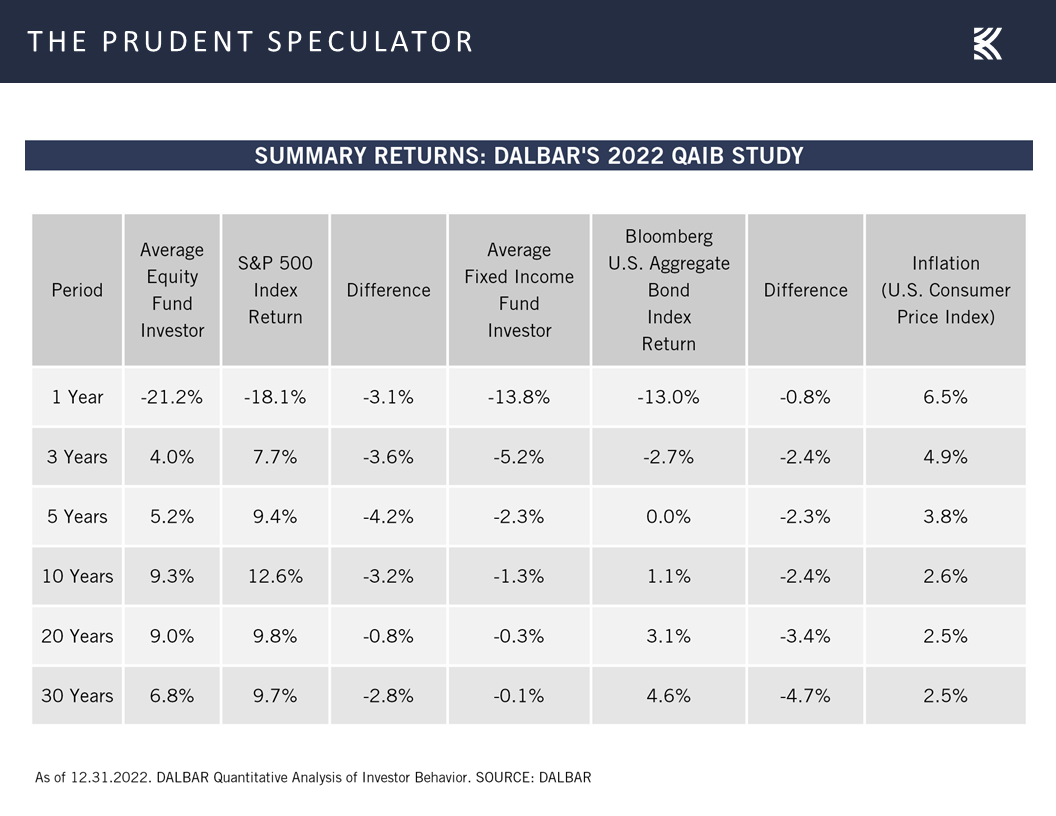

And history suggests that those who try to get in and out end up with miserable long-term returns, as the latest study from data provider DALBAR detailing average equity and fixed income fund investor returns over the last three decades vividly shows. While the 2.8%-per-annum lag in performance for stock fund investors is bad enough, we are shaking our heads that the average bond fund investor evidently has lost money for 30 years.

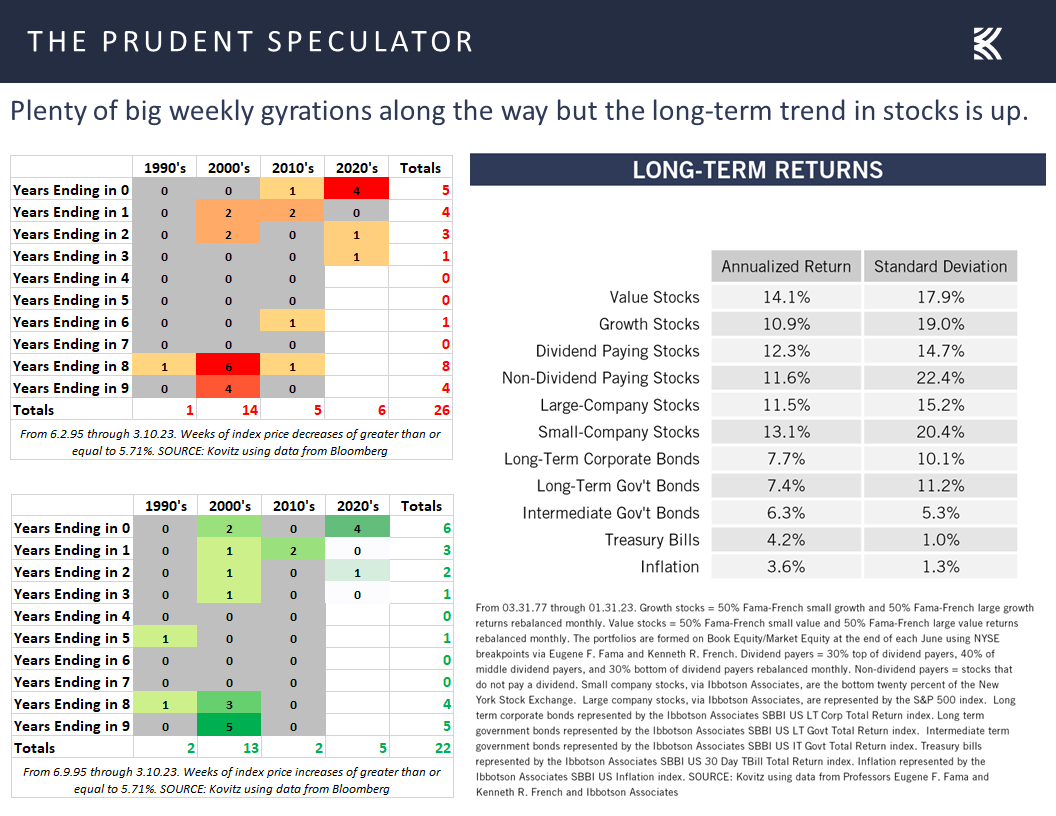

None of this is to suggest that the week just ended was not painful. Indeed, rare is a sizable one-week plunge of 5% or greater for the Russell 3000 Value index, but the benchmark skidded 5.71% on a price-return basis over the last five trading days, the 26th-worst weekly showing since the index was established in 1995. Of course, there have also been 22 weeks with gains of similar or greater magnitude, while the historical evidence shows that Value Stocks have enjoyed the best long-term returns – 14.1% per annum since the launch of The Prudent Speculator in 1977 through January 2023!

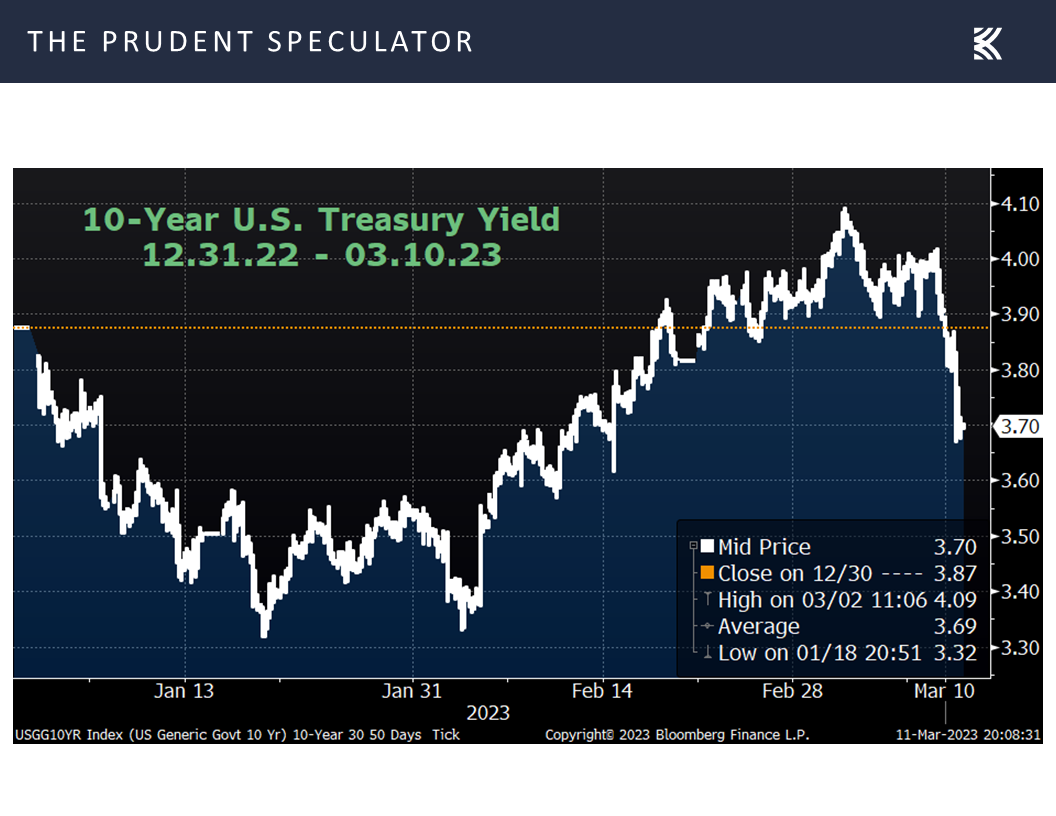

A byproduct of the Silicon Valley bust was that interest rates cratered, with a massive flight to safety into U.S. Treasuries, sending the yield on the benchmark 10-Year bond down to 3.70%, compared to the 3.87% at which it began the year, 3.95% a week ago and 4.09% midweek.

Interest Rates & Fed Rate Hikes: Market Grows Much More Dovish

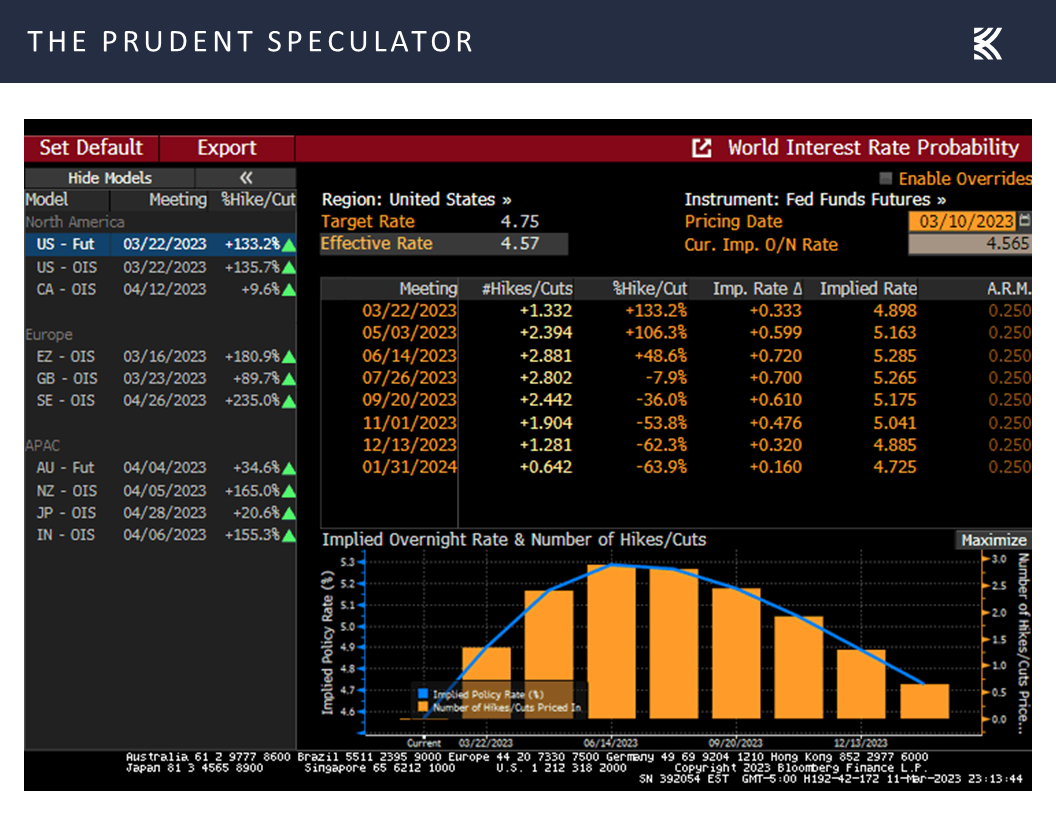

The futures markets also saw a huge reduction in the peak level for the Federal Funds rate, with the current high of 5.29% in June down sharply from last week’s 5.44% high in September. In addition, the end-of-year level for the Fed Funds rate fell markedly to 4.89%, down from 5.31% a week ago.

Believe it or not, the tilt toward a dovish view of the Fed was a complete reversal from where things stood mid-week. In fact, the markets were starting to price in a 50-basis-point hike in the Fed Funds rate at the upcoming Federal Open Market Committee (FOMC) meeting.

Such a stance arguably was not misguided after Fed Chair Jerome H. Powell said on Capitol Hill on Tuesday, “The latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated. If the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes.”

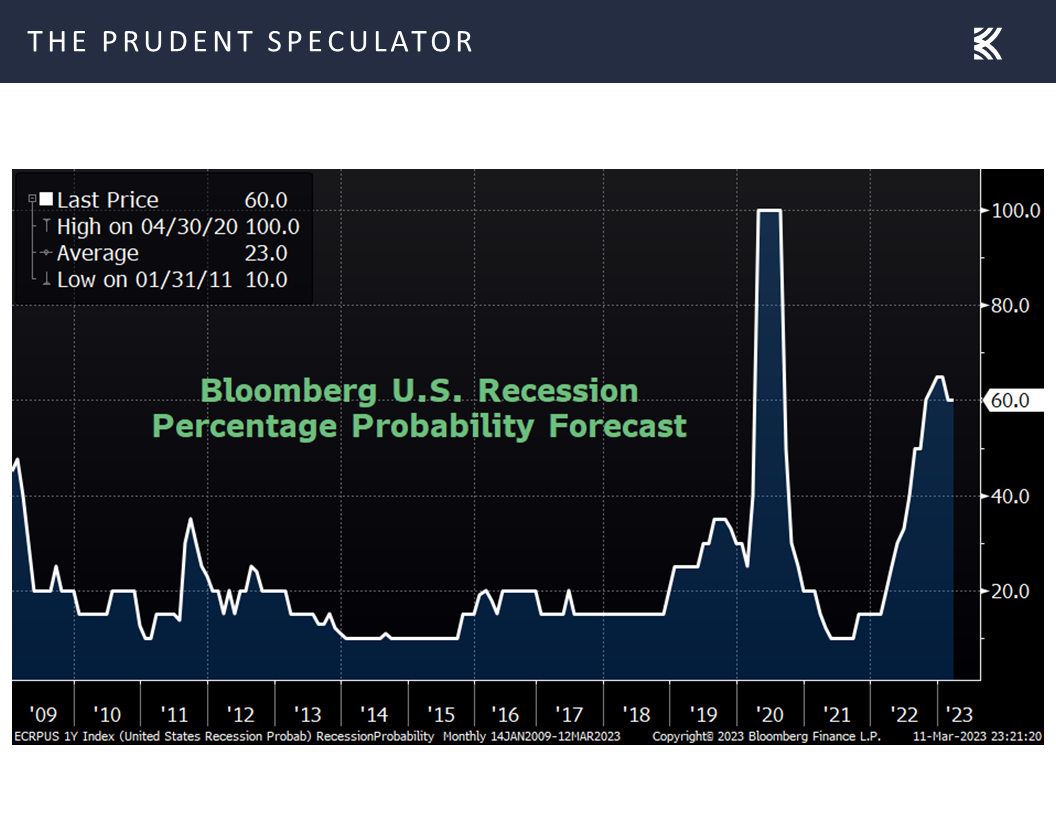

It does seem strange that the Fed would be worried about too-strong economic numbers when Bloomberg calculations suggest the odds of recession over the next 12 months stand at 60%,

Econ News: Jobs Numbers Remain Strong, But Wage Growth Slows

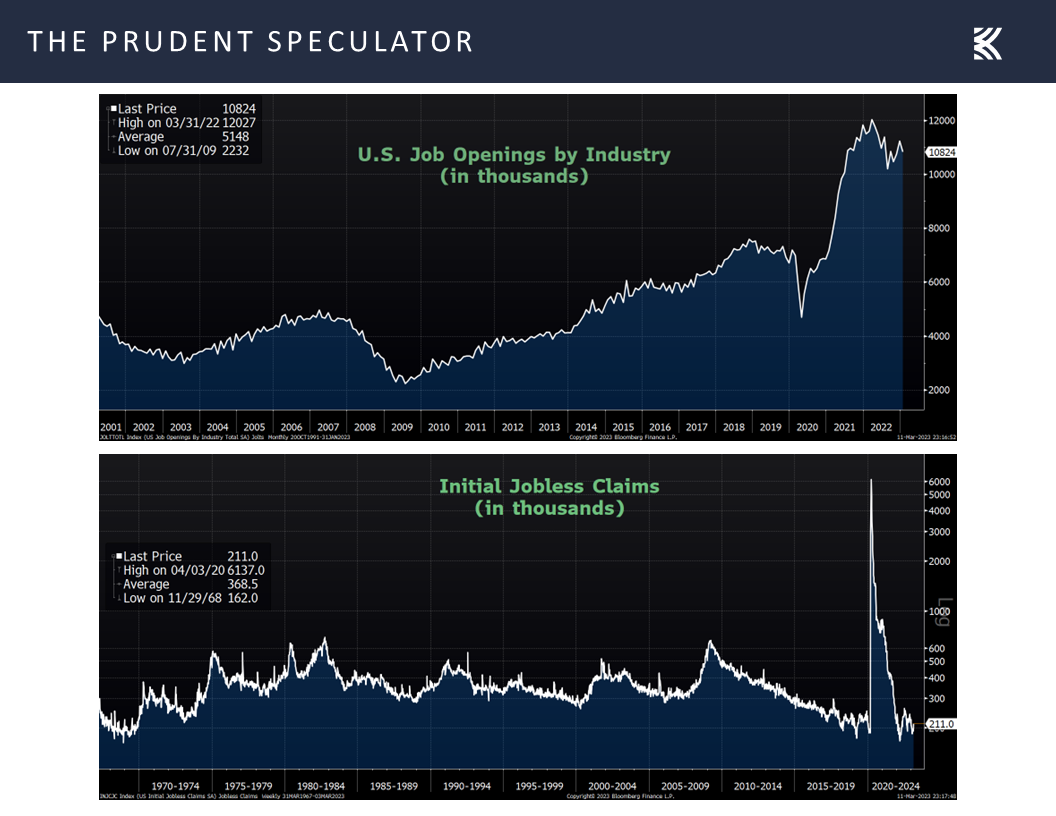

but job openings in January came in better-than-expected at 10.8 million, though that tally was down from 11.2 million in December, and first-time filings for jobless benefits remain unusually low, despite a tick up in the latest week to 211,000…

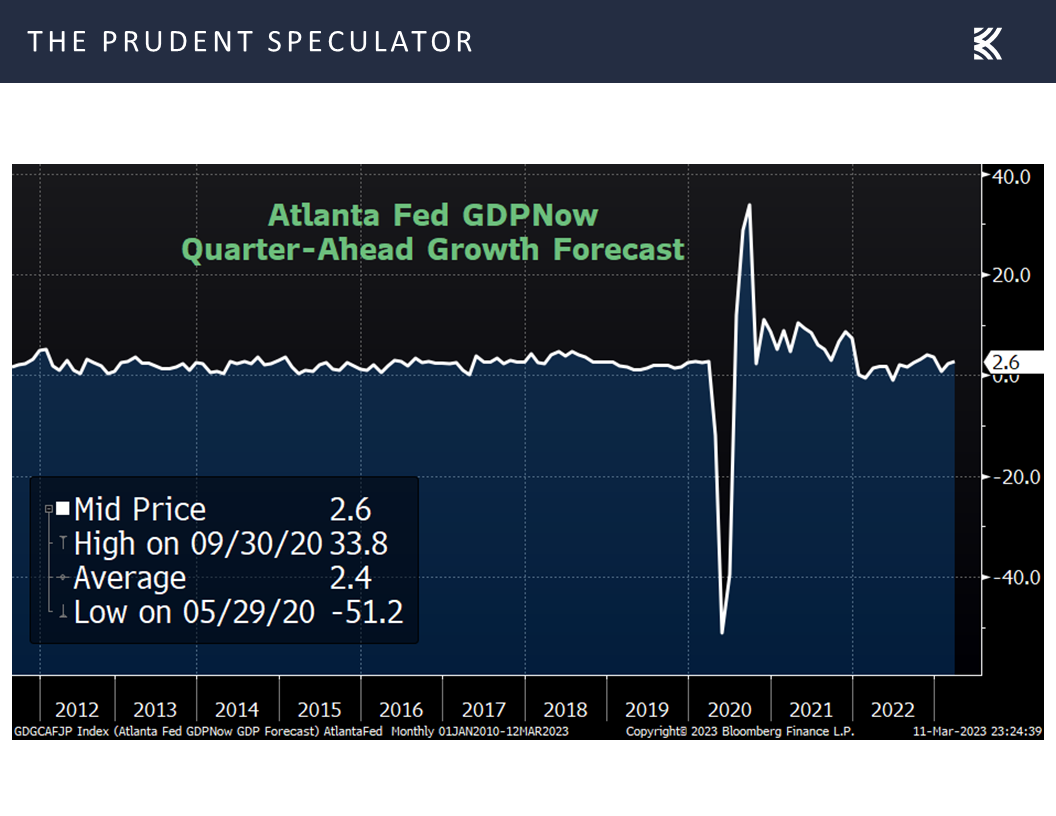

while the most recent Q1 inflation-adjusted U.S. GDP growth estimate from the Atlanta Fed increased last week to 2.6%.

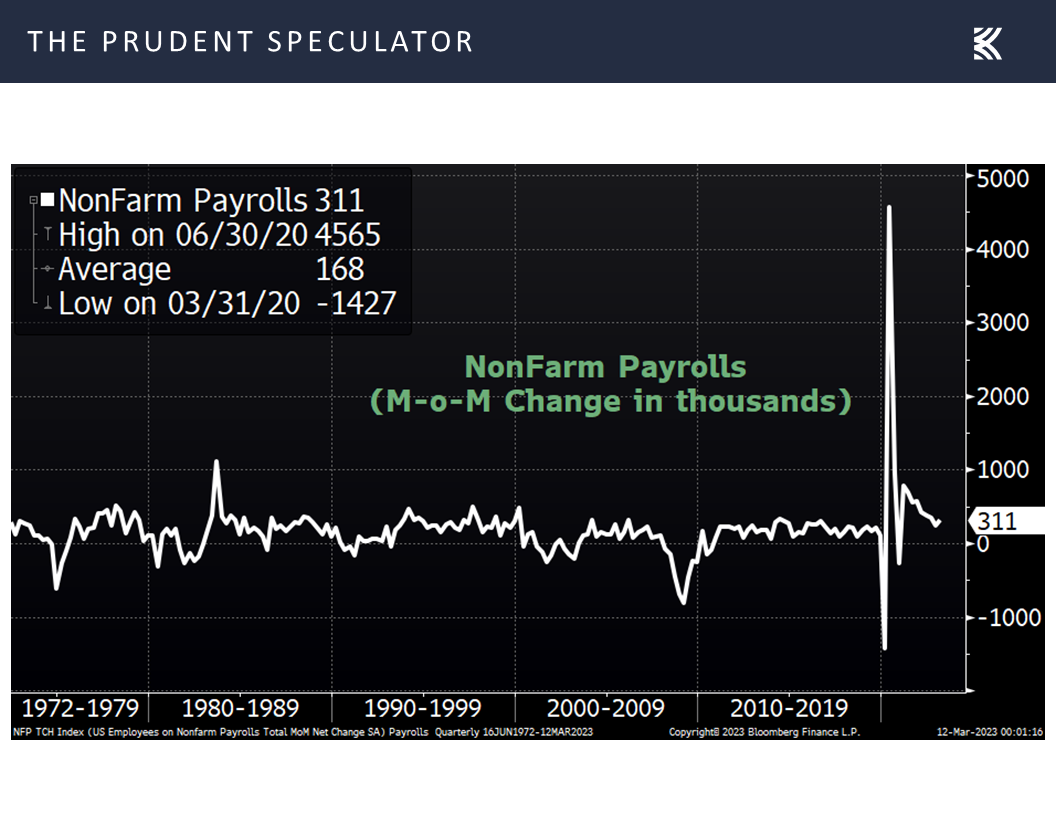

Also, the all-important monthly labor situation report arrived on Friday morning, with the number of non-farm payrolls created in February exceeding expectations by a wide margin with a gain of 311,000.

Also, the all-important monthly labor situation report arrived on Friday morning, with the number of non-farm payrolls created in February exceeding expectations by a wide margin with a gain of 311,000.

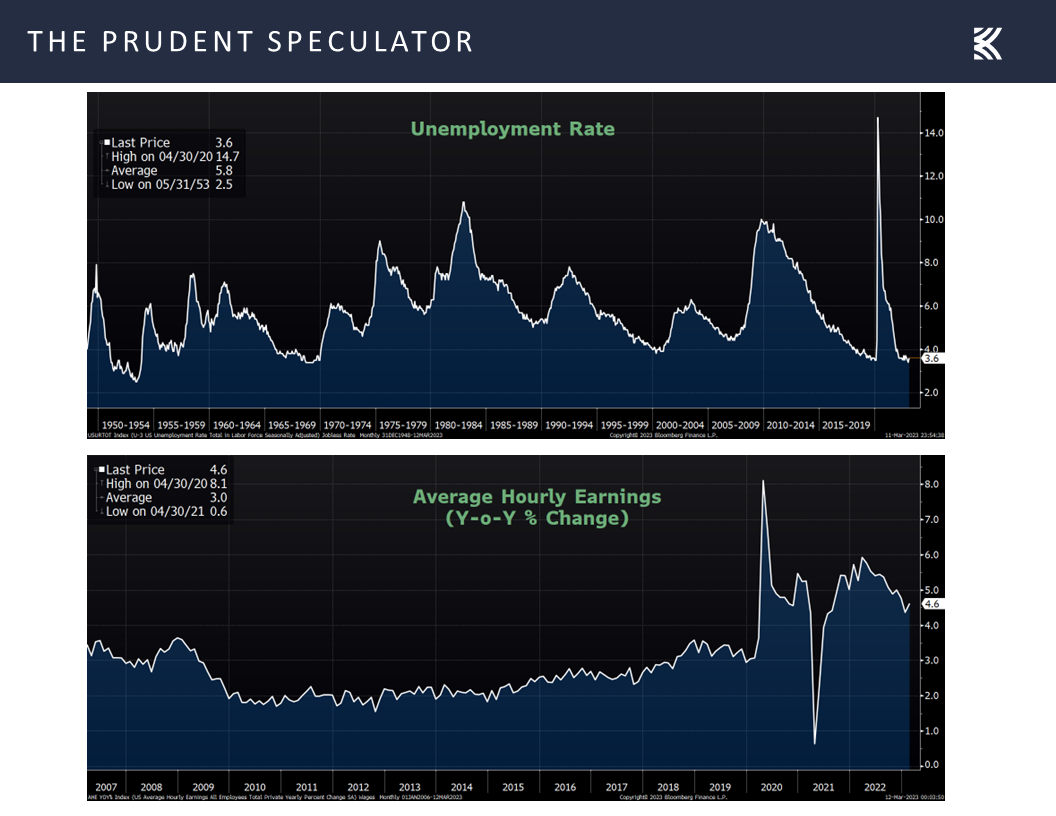

The jobs numbers, however, had a bit of Goldilocks to them in that the unemployment rate edged up to 3.6% and the crucial wage component rose just 0.2%, the smallest increase in a year, with the year-over-year gain of 4.6% trailing forecasts of a 4.8% advance, a positive sign in the Fed’s fight against inflation.

The jobs numbers, however, had a bit of Goldilocks to them in that the unemployment rate edged up to 3.6% and the crucial wage component rose just 0.2%, the smallest increase in a year, with the year-over-year gain of 4.6% trailing forecasts of a 4.8% advance, a positive sign in the Fed’s fight against inflation.

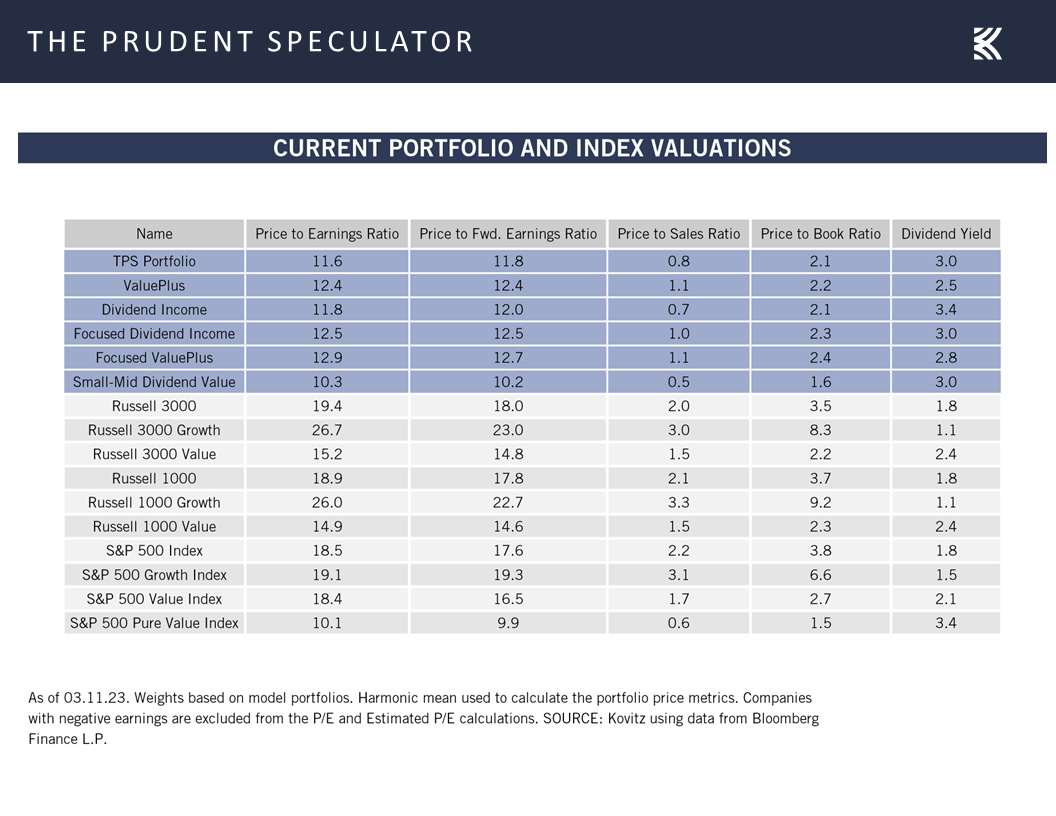

Valuations: Reasonable Metrics for our Portfolios

No doubt, the markets are in for significant near-term volatility, even as the rally in bonds arguably reduces the pressure on bank assets, but we remain comfortable with our broadly diversified portfolios of what we believe to be undervalued stocks,

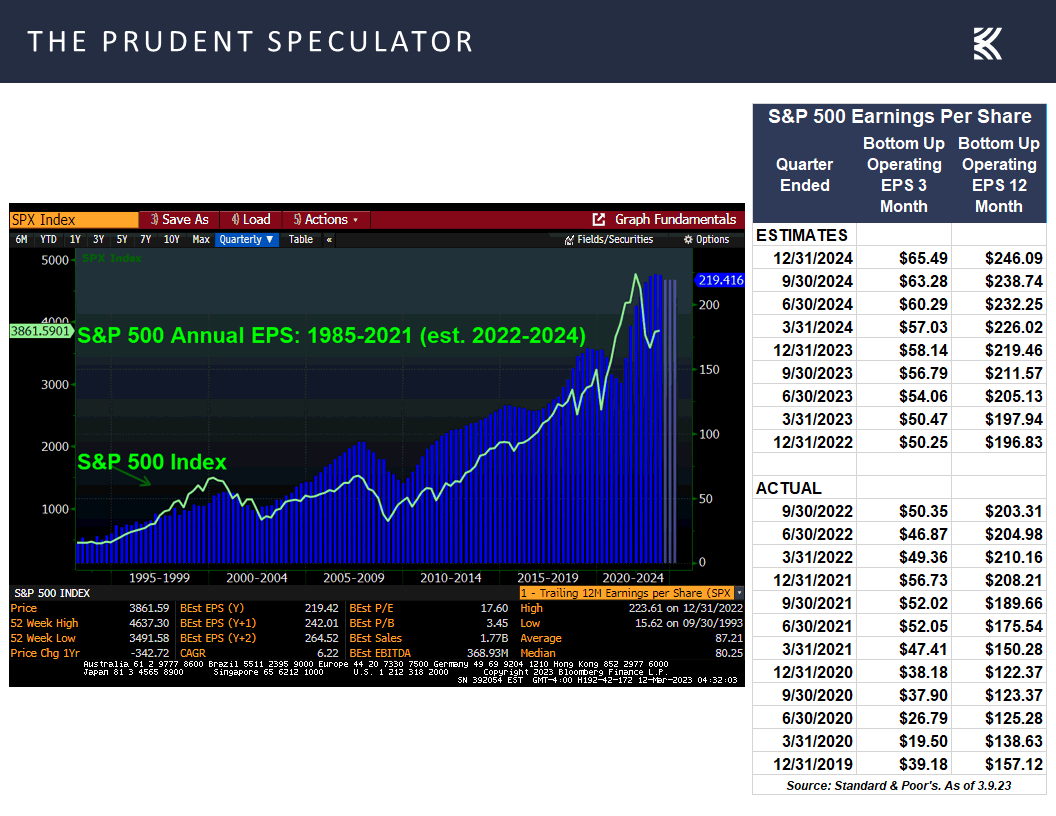

Corporate Profits: Solid Q4 EPS and Growth Projected for 2023 & 2024

and we think corporate profits are still likely to hold up well, with the latest EPS estimates from Standard & Poor’s calling for significant growth this year and in 2024.

Great Financial Crisis: Words of Wisdom from Warren Buffett in February 2009

Though we are braced for a roller-coaster ride as trading resumes this week (the equity futures are up sharply as this update goes to press), we’ll close this missive with comments Warren Buffett penned in February 2009, noting that equities put in their Great Financial Crisis bottom a couple of weeks later.

Never forget that our country has faced far worse travails in the past. In the 20th Century alone, we dealt with two great wars (one of which we initially appeared to be losing); a dozen or so panics and recessions; virulent inflation that led to a 21 1⁄2 % prime rate in 1980; and the Great Depression of the 1930s, when unemployment ranged between 15% and 25% for many years. America has had no shortage of challenges.

Without fail, however, we’ve overcome them. In the face of those obstacles – and many others – the real standard of living for Americans improved nearly seven-fold during the 1900s, while the Dow Jones Industrials rose from 66 to 11,497. Compare the record of this period with the dozens of centuries during which humans secured only tiny gains, if any, in how they lived. Though the path has not been smooth, our economic system has worked extraordinarily well over time. It has unleashed human potential as no other system has, and it will continue to do so. America’s best days lie ahead.

Stock News & Earnings – Updates on Regional Banks

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Silicon Valley Collapse, Stock Market Grows Much More Dovish and more Economic News

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. This week, we cover the Silicon Valley collapse, jobs numbers, interest rates, Fed hikes, unemployment rates, the Great Finacial Crisis and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades: 8 Buys for 4 Portfolios

Silicon Valley Collapse: Uninsured Deposits from Customers in Need of Cash & Long-Dated Un-hedged Assets

Riding to the Rescue: Uncle Sam With a Strong Response

Crisis Events: Keeping the Faith Through Thick and Thin

Interest Rates & Fed Rate Hikes: Market Grows Much More Dovish

Econ News: Jobs Numbers Remain Strong, But Wage Growth Slows

Valuations: Reasonable Metrics for our Portfolios

Corporate Profits: Solid Q4 EPS and Growth Projected for 2023 & 2024

Great Financial Crisis: Words of Wisdom from Warren Buffett in February 2009

Stock News – Updates on Regional Banks

Week In Review:

Silicon Valley Collapse: Uninsured Deposits from Customers in Need of Cash & Long-Dated Un-hedged Assets

Long-time readers of this publication will recall that we had two ownership experiences of the California bank in the past. Happily, the first was in the 1990s and resulted in a 28% annualized return over our seven-year holding period while the second from 2001 to 2003 ended with a 41% annualized return.

Of course, in the 1990s, the bank’s assets were in the $1 billion range and during the early-2000s, they were in the $4 billion range. By December 2022, assets had grown above $200 billion, making Silicon Valley the 16th largest bank in the country, with a roster of clients in technology and life science/healthcare industries, including private equity and venture capital, climate technology, biopharma, enterprise software and fintech.

Per Bloomberg, investors and depositors tried to pull a whopping $42 billion from SIVB on Thursday in a colossal run on the bank, which was triggered by a crisis in confidence after Silicon Valley management on Wednesday disclosed that the company sold $21 billion of available-for-sale securities, realizing a $1.9 billion loss, and announced a proposed public offering of $1.25 billion of common stock and another $500 million of preferred stock.

While Silicon Valley said in a regulatory filing that day…

Our financial position enables us to take these strategic actions, which are intended to further bolster that position now and over the long term.

We are taking these actions because we expect continued higher interest rates, pressured public and private markets, and elevated cash burn levels from our clients as they invest in their businesses.

We are experienced at navigating market cycles and are well positioned to serve our clients through market volatility, with a high-quality, liquid balance sheet and strong capital ratios.

…the communication fell on deaf ears, with prominent venture capitalists instructing the companies they had seeded to pull their money out of the bank.

To be sure, with the benefit of 20-20 hindsight, Silicon Valley was incredibly reckless, given that management poured billions of dollars into long-term mortgage-backed securities and municipal bonds with minimal interest rate hedging as assets literally tripled during the Pandemic. The $91 billion (cost) of securities had an unrealized loss of $15 billion or so at the end of 2022, but regulatory requirements did not necessitate a write down as the assets arguably had minimal credit risk and they were intended to be held to maturity.

As such, there would not have been a liquidity issue if everyone wasn’t pounding on the proverbial doors demanding their money back. And it is highly unlikely that depositors would have been heading for the exits if they had the benefit of FDIC insurance, but sadly $151.5 billion of deposits in U.S. offices exceeded the FDIC insurance limit and $13.9 billion of foreign deposits had no backstopping from Uncle Sam. Total deposits showing on the balance sheet at the end of 2022 were $173.1 billion, meaning that a massive percentage (more than 95%) of the total had plenty of incentive to pull money out of SIVB.

Riding to the Rescue: Uncle Sam With a Strong Response

Happily, few banks in this country look like SIVB and we think the issues in play there are very much isolated. We do not know of any other bank that held the lion’s share of its assets in unhedged 10-year-or-longer-to maturity mortgage-backed securities, while operating with a massively uninsured deposit base made up of a set of customers across the private equity/venture capital landscape with very short-term cash needs at a time when capital committed to the space had dried up.

Contrast this with most regional banks across the country (especially those in our portfolios), whose depositors are typically a highly diverse group of individuals and businesses (the majority of whom tend to be substantially protected by FDIC insurance) and that we expect are unlikely to uproot their day-to-day operating funds.

Despite our arguments that the SIVB situation is idiosyncratic, we realize that the breathtaking run-on-the-bank has led to plenty of consternation for bank-stock investors in particular and the equity markets in general. Naturally, comparisons have been made to the collapse of Lehman Brothers and Washington Mutual during the Great Financial Crisis, but we believe that banks are far better capitalized today. Treasury Secretary Janet Yellen, concurs, saying on Friday, “The U.S. banking system remains resilient.”

Certainly, anything can happen, and there was plenty of chatter over the weekend warning of dire consequences if Washington doesn’t make uninsured SIVB depositors whole, or nearly whole. But we continue to believe that contagion is unlikely, given that few banks have tons of start-up business customers who burn through cash like those of Silicon Valley.

Ms. Yellen responded on Sunday, “Let me be clear that during the financial crisis, there were investors and owners of systemic large banks that were bailed out, and the reforms that have been put in place means that we’re not going to do that again. But we are concerned about depositors and are focused on trying to meet their needs.”

Obviously, we prefer not to have a rerun of the Great Financial Crisis, but that seems very unlikely after the following from the Department of the Treasury, Federal Reserve and FDIC on Sunday afternoon:

Today we are taking decisive actions to protect the U.S. economy by strengthening public confidence in our banking system. This step will ensure that the U.S. banking system continues to perform its vital roles of protecting deposits and providing access to credit to households and businesses in a manner that promotes strong and sustainable economic growth.

After receiving a recommendation from the boards of the FDIC and the Federal Reserve, and consulting with the President, Secretary Yellen approved actions enabling the FDIC to complete its resolution of Silicon Valley Bank, Santa Clara, California, in a manner that fully protects all depositors. Depositors will have access to all of their money starting Monday, March 13. No losses associated with the resolution of Silicon Valley Bank will be borne by the taxpayer.

We are also announcing a similar systemic risk exception for Signature Bank, New York, New York, which was closed today by its state chartering authority. All depositors of this institution will be made whole. As with the resolution of Silicon Valley Bank, no losses will be borne by the taxpayer.

Shareholders and certain unsecured debtholders will not be protected. Senior management has also been removed. Any losses to the Deposit Insurance Fund to support uninsured depositors will be recovered by a special assessment on banks, as required by law.

Finally, the Federal Reserve Board on Sunday announced it will make available additional funding to eligible depository institutions to help assure banks have the ability to meet the needs of all their depositors.

The U.S. banking system remains resilient and on a solid foundation, in large part due to reforms that were made after the financial crisis that ensured better safeguards for the banking industry. Those reforms combined with today’s actions demonstrate our commitment to take the necessary steps to ensure that depositors’ savings remain safe.

Certainly, making all depositors whole at Silicon Valley and Signature, included those who were uninsured, is powerful support against further runs on banks, while the tools provided well-capitalized regional banks allows them to handle sizable near-term deposit outflows.

So, it would seem that a financial crisis has been averted. Still, we offer the reminder that through Friday, the Russell 3000 Value index had returned 225% since the collapse of Lehman Brothers in September 2008.

Crisis Events: Keeping the Faith Through Thick and Thin

Illustrating why we like to say that the only problem with market timing is getting the timing right, we suspect that few who managed to exit their equity holdings prior to the Lehman collapse were able to get back into stocks at an opportune time. After all, there were three rebounds of 10% or greater for the S&P 500 just from October 2008 to January 2009, before stocks ultimately hit their lows in March 2009.

And history suggests that those who try to get in and out end up with miserable long-term returns, as the latest study from data provider DALBAR detailing average equity and fixed income fund investor returns over the last three decades vividly shows. While the 2.8%-per-annum lag in performance for stock fund investors is bad enough, we are shaking our heads that the average bond fund investor evidently has lost money for 30 years.

None of this is to suggest that the week just ended was not painful. Indeed, rare is a sizable one-week plunge of 5% or greater for the Russell 3000 Value index, but the benchmark skidded 5.71% on a price-return basis over the last five trading days, the 26th-worst weekly showing since the index was established in 1995. Of course, there have also been 22 weeks with gains of similar or greater magnitude, while the historical evidence shows that Value Stocks have enjoyed the best long-term returns – 14.1% per annum since the launch of The Prudent Speculator in 1977 through January 2023!

A byproduct of the Silicon Valley bust was that interest rates cratered, with a massive flight to safety into U.S. Treasuries, sending the yield on the benchmark 10-Year bond down to 3.70%, compared to the 3.87% at which it began the year, 3.95% a week ago and 4.09% midweek.

Interest Rates & Fed Rate Hikes: Market Grows Much More Dovish

The futures markets also saw a huge reduction in the peak level for the Federal Funds rate, with the current high of 5.29% in June down sharply from last week’s 5.44% high in September. In addition, the end-of-year level for the Fed Funds rate fell markedly to 4.89%, down from 5.31% a week ago.

Believe it or not, the tilt toward a dovish view of the Fed was a complete reversal from where things stood mid-week. In fact, the markets were starting to price in a 50-basis-point hike in the Fed Funds rate at the upcoming Federal Open Market Committee (FOMC) meeting.

Such a stance arguably was not misguided after Fed Chair Jerome H. Powell said on Capitol Hill on Tuesday, “The latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated. If the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes.”

It does seem strange that the Fed would be worried about too-strong economic numbers when Bloomberg calculations suggest the odds of recession over the next 12 months stand at 60%,

Econ News: Jobs Numbers Remain Strong, But Wage Growth Slows

but job openings in January came in better-than-expected at 10.8 million, though that tally was down from 11.2 million in December, and first-time filings for jobless benefits remain unusually low, despite a tick up in the latest week to 211,000…

while the most recent Q1 inflation-adjusted U.S. GDP growth estimate from the Atlanta Fed increased last week to 2.6%.

Valuations: Reasonable Metrics for our Portfolios

No doubt, the markets are in for significant near-term volatility, even as the rally in bonds arguably reduces the pressure on bank assets, but we remain comfortable with our broadly diversified portfolios of what we believe to be undervalued stocks,

Corporate Profits: Solid Q4 EPS and Growth Projected for 2023 & 2024

and we think corporate profits are still likely to hold up well, with the latest EPS estimates from Standard & Poor’s calling for significant growth this year and in 2024.

Great Financial Crisis: Words of Wisdom from Warren Buffett in February 2009

Though we are braced for a roller-coaster ride as trading resumes this week (the equity futures are up sharply as this update goes to press), we’ll close this missive with comments Warren Buffett penned in February 2009, noting that equities put in their Great Financial Crisis bottom a couple of weeks later.

Never forget that our country has faced far worse travails in the past. In the 20th Century alone, we dealt with two great wars (one of which we initially appeared to be losing); a dozen or so panics and recessions; virulent inflation that led to a 21 1⁄2 % prime rate in 1980; and the Great Depression of the 1930s, when unemployment ranged between 15% and 25% for many years. America has had no shortage of challenges.

Without fail, however, we’ve overcome them. In the face of those obstacles – and many others – the real standard of living for Americans improved nearly seven-fold during the 1900s, while the Dow Jones Industrials rose from 66 to 11,497. Compare the record of this period with the dozens of centuries during which humans secured only tiny gains, if any, in how they lived. Though the path has not been smooth, our economic system has worked extraordinarily well over time. It has unleashed human potential as no other system has, and it will continue to do so. America’s best days lie ahead.

Stock News & Earnings – Updates on Regional Banks

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.