The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. This week, we cover the late stock market rebound, dividend yields, economic numbers, valuations and earnings, The Prudent Speculator’s 46th Anniversary and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

- Week: Late Rebound…On Soured Sentiment?

- DALBAR QAIB: Stock and Especially Bond Fund Investors are Awful Market Timers

- Patience: The Longer the Hold the Lower the Chance of Loss

- Econ Numbers: Mixed Picture…as is Often the Case

- Fed Rate Hikes: Market Grows More Hawkish

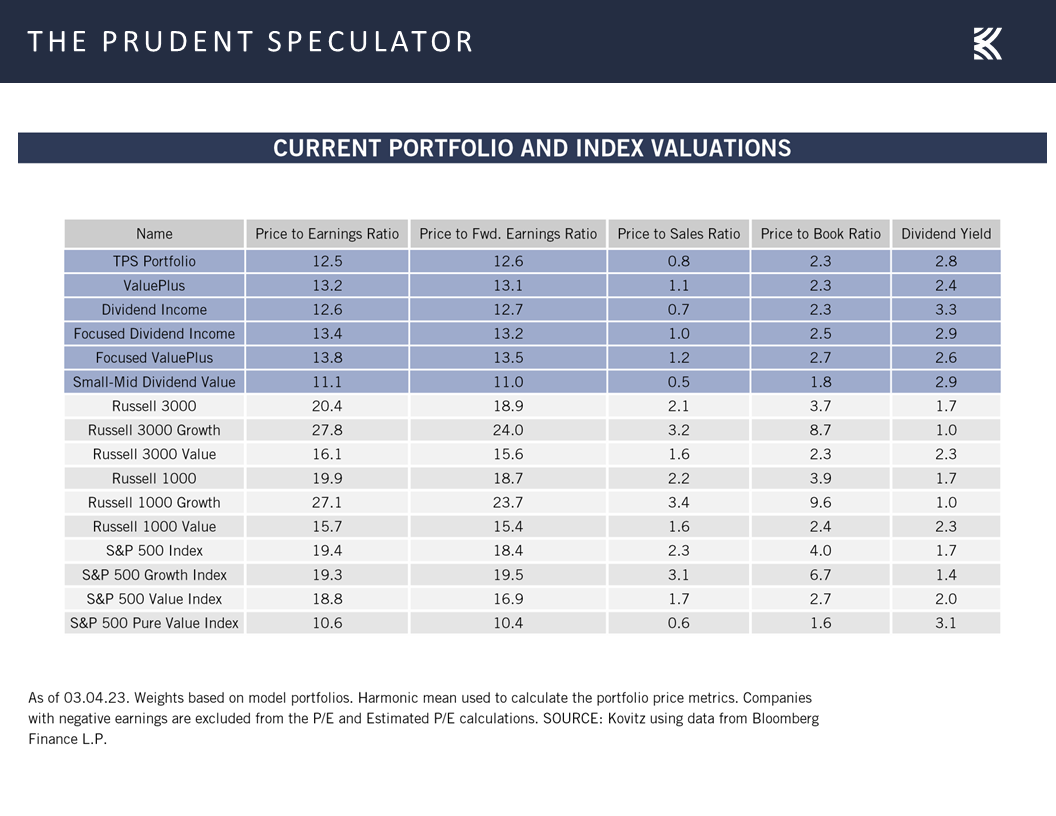

- Valuations: Inexpensive Metrics & Generous Dividend Yield for TPS Portfolio

- 46th Anniversary: Equities Very Rewarding Since the Launch of The Prudent Speculator in 1977

- Corporate Profits: Solid Q4 EPS and Decent Outlook for 2023

- Updates on 10 companies across 7 different sectors

Week In Review:

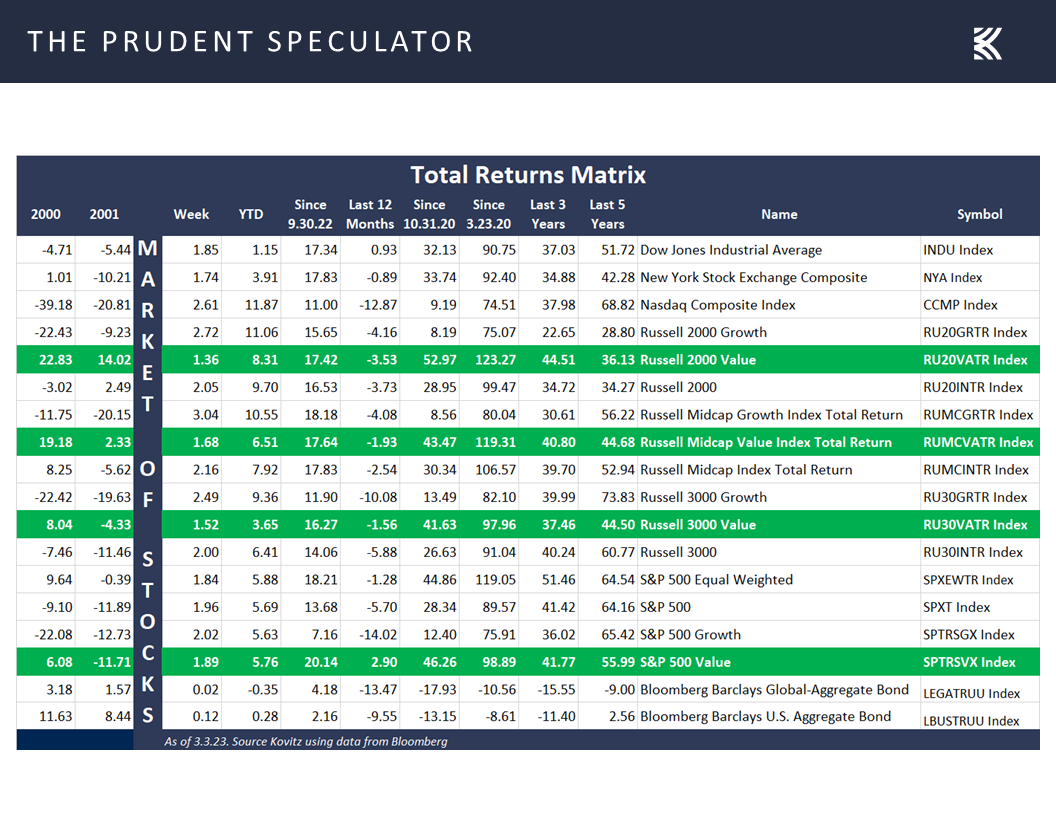

With Growth leading the charge, cutting the deficit against Value since the recent September 30, 2022, market lows, equities enjoyed a terrific last two days of the trading week, which stopped a three-week losing streak and pushed the Dow Jones Industrial Average back into the green for the year.

Interestingly, the rebound came as the good folks at MarketWatch proclaimed, “Data Shows Investors Running Toward Safety of Cash as Stock Market Stumbles, Yields Rise.” In a column called The Tell, MarketWatch explained, “Investors poured $68.1 billion into cash funds in the week to Wednesday as concerns over additional Federal Reserve rate hikes continue to rattle financial markets, according to figures from Bank of America, Goldman Sachs and TD Securities, all citing EPFR data [which also showed that $7.4 billion left stock funds] in their weekly notes.”

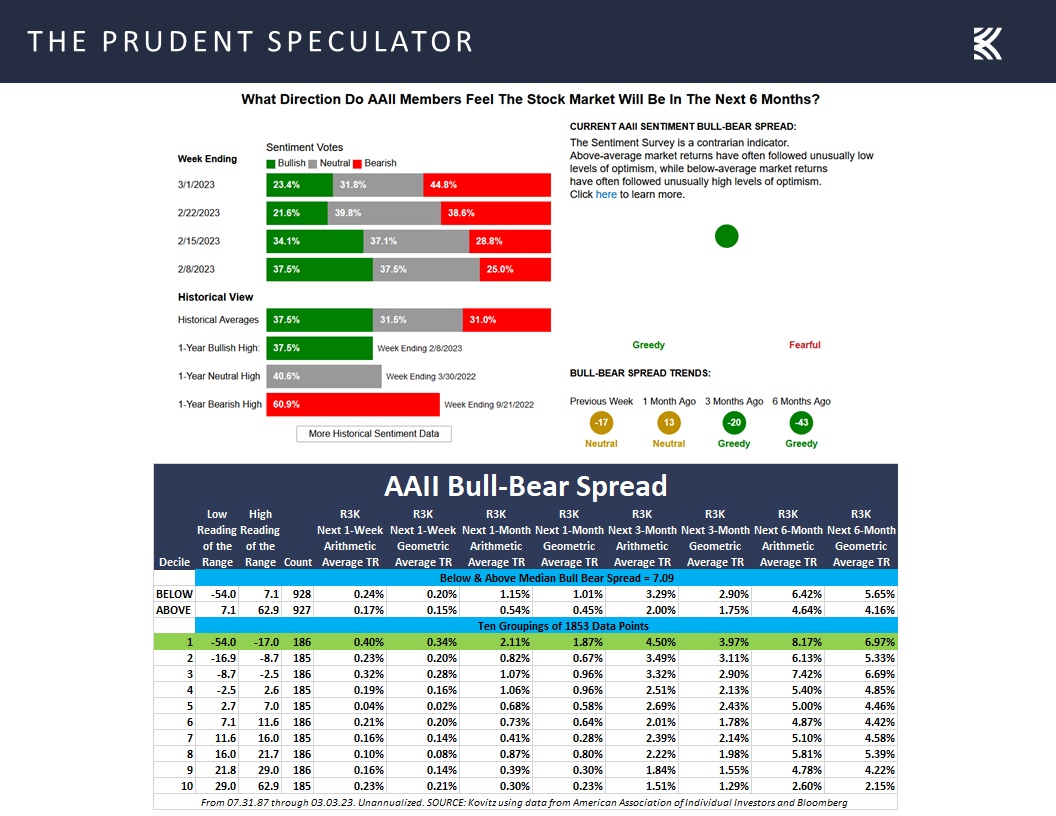

A couple of days does not a trend make but zigging when they should have zagged is not an unusual occurrence, with data from the American Association of Individual Investors (AAII) vividly illustrating the point. The latest AAII weekly sentiment gauge saw a big jump to 44.8% in the number of respondents who say they are Bearish on the prospects for stocks over the next six months, with their lead over those who say they are Bullish widening to 21.4 percentage points and putting the Bull-Bear spread in the lowest decile of all the readings dating back to 1987. Incredibly, 1-week, 1-month, 3-month, and 6-month forward returns are best when the folks on Main Street are very pessimistic…like they are today.

DALBAR QAIB: Stock and Especially Bond Fund Investors are Awful Market Timers

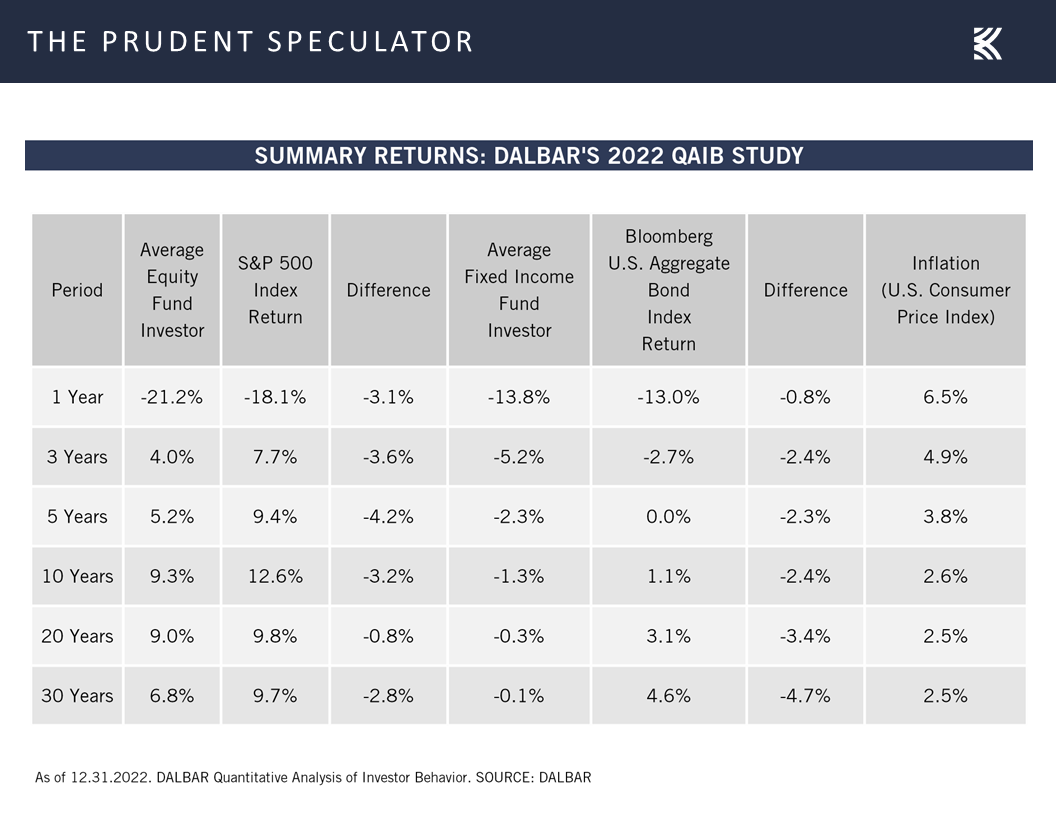

We have long admonished that the only problem with market timing is getting the timing right, and numbers further confirming this view arrived this week as the 2022 DALBAR Quantitative Analysis of Investor Behavior returns were released. The data provider’s calculations show just how bad the average stock fund investor has performed, with the 3% or so deficit versus the S&P 500’s return last year in line with the dismal returns endured over the past three decades.

And if you think the 6.8% annualized return over the last 30 years for the average equity fund investor versus the 9.7% return for the S&P 500 is bad, take a gander at the average fixed income investor. Believe it or not, DALBAR calculates that folks actually have lost money on average in bond funds over the past 30 years! And stocks are supposed to be the risky asset class?

Patience: The Longer the Hold the Lower the Chance of Loss

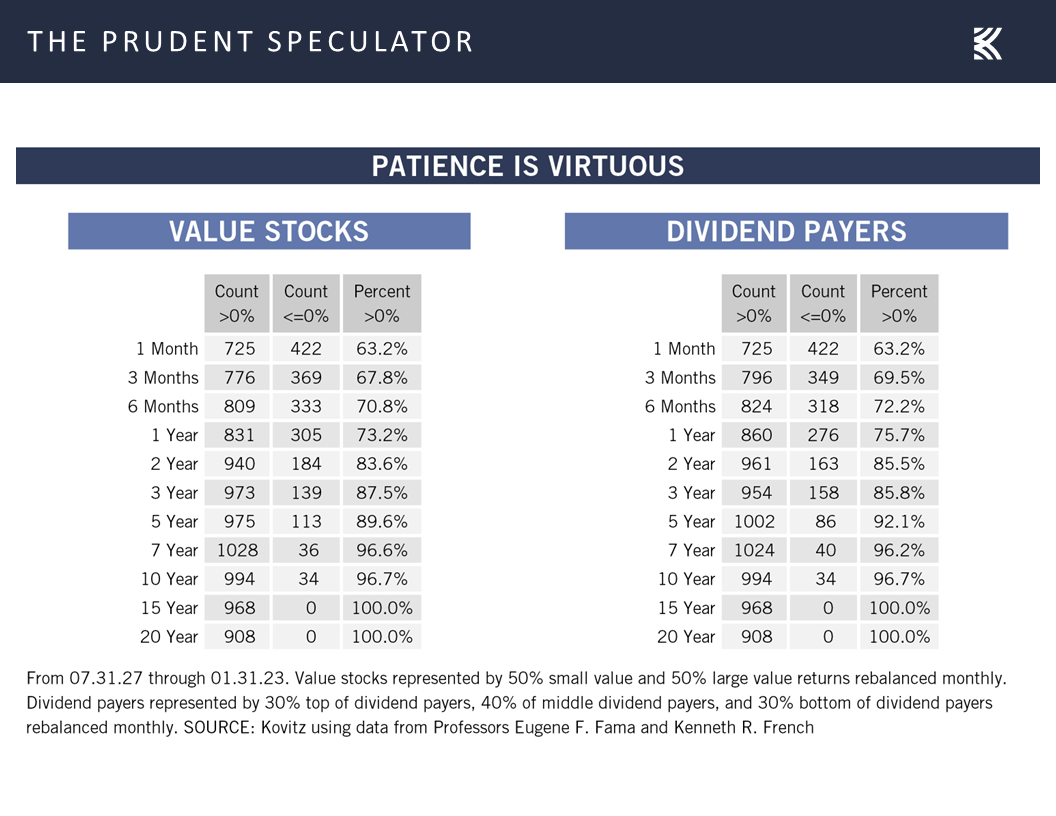

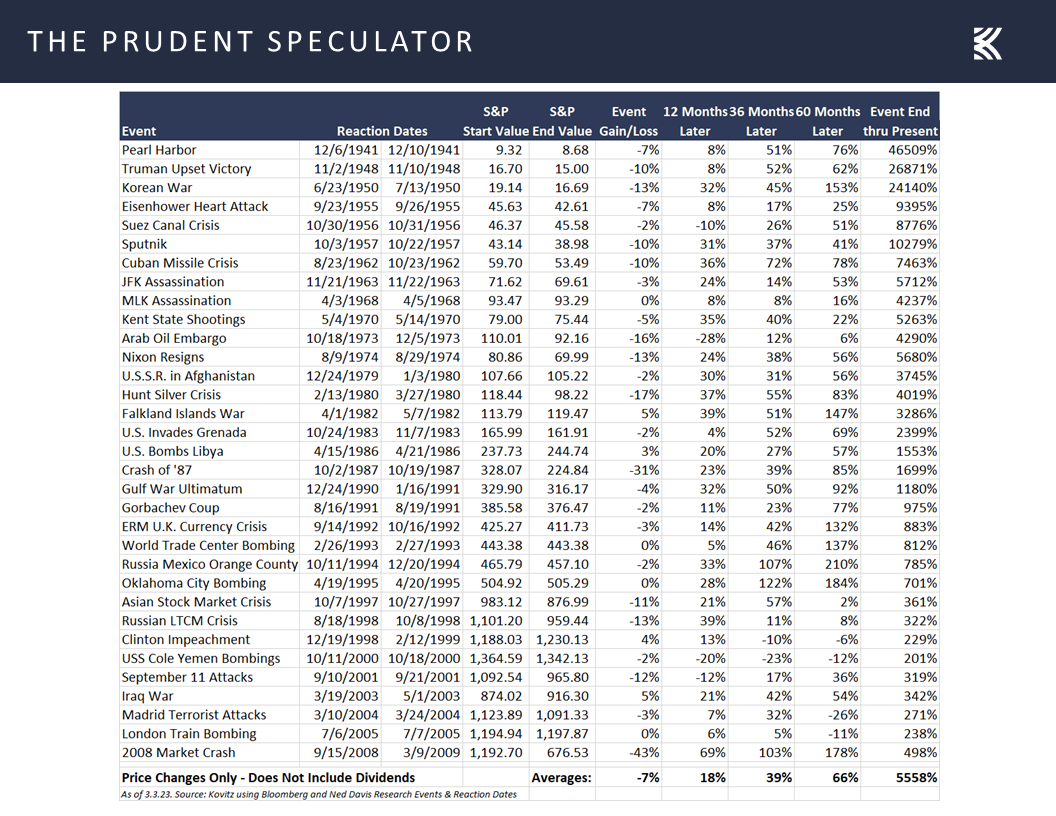

Certainly, bond prices are less volatile than stock prices, but given that the average fixed income investor lost money in every period DALBAR studied, we remain puzzled that so many continue to think about risk in terms of volatility of one-month returns. This is especially true in that most are investing for long-term objectives. We know that we won’t win any Stocks are not as Risky as Bonds debates, and there is no assurance that past is prologue, but we can’t help but point out that there has not been a 15-year or 20-year period in which Value Stocks or Dividend Payers lost money, provided those who owned them did not stray from their course along the way.

No doubt, keeping the faith through thick and thin is not easy, with the significant downturn endured in 2022 fresh on investor minds. Certainly, we do not wish to downplay the war in Ukraine, supply-chain issues, inflation, high interest rates, Federal Reserve tightening, a slowing economy and other headwinds, but there have been more than a few frightening events throughout history, yet stocks have still managed to move substantially higher in the fullness of time.

No doubt, keeping the faith through thick and thin is not easy, with the significant downturn endured in 2022 fresh on investor minds. Certainly, we do not wish to downplay the war in Ukraine, supply-chain issues, inflation, high interest rates, Federal Reserve tightening, a slowing economy and other headwinds, but there have been more than a few frightening events throughout history, yet stocks have still managed to move substantially higher in the fullness of time.

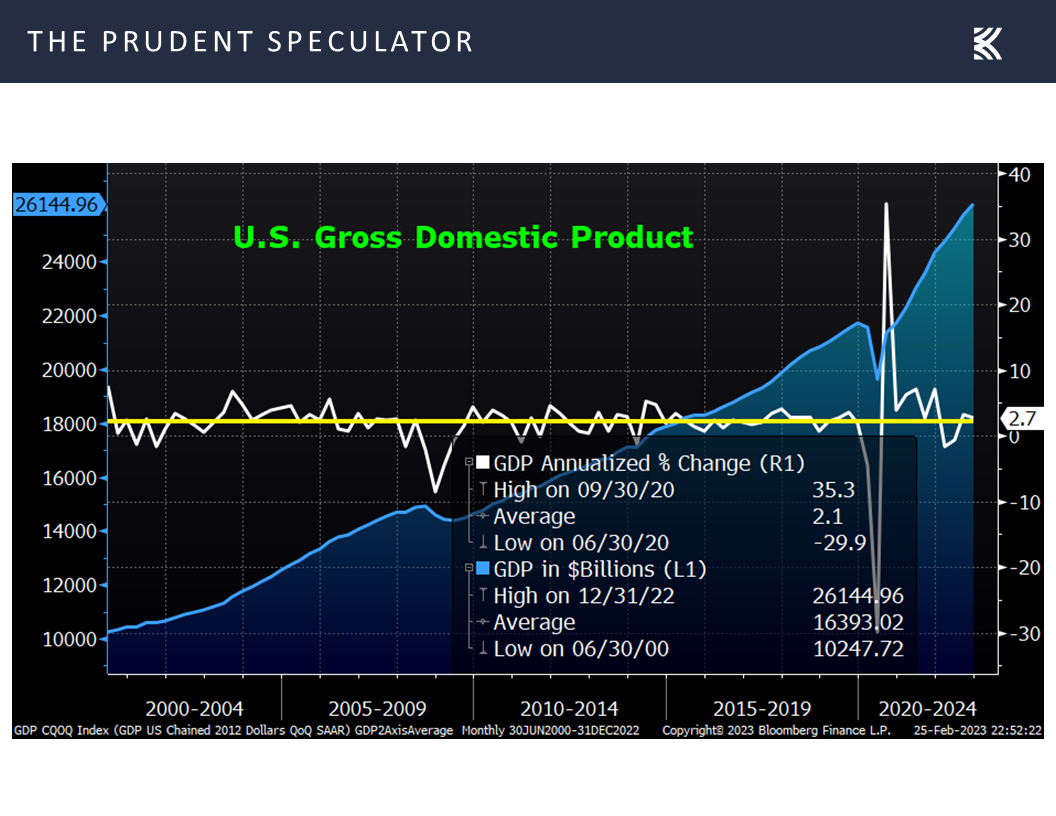

Econ Numbers: Mixed Picture…as is Often the Case

While the long-term trend has been up, many think they can bail out and avoid the inevitable trips south and somehow get back into stocks before the next upswing. Alas, the path stock prices traverse will always be bumpy and there is no way that anyone can predict with any certainty the short-term direction.

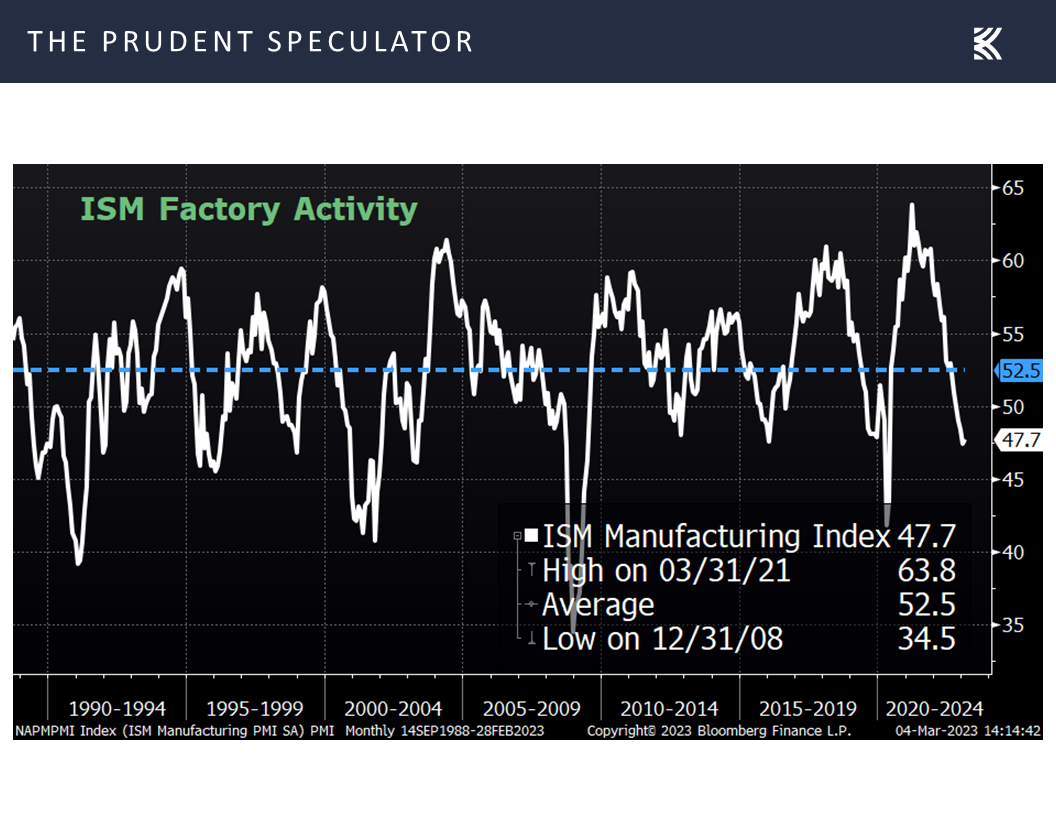

After all, consider that stocks were moving lower last week, with The Wall Street Journal’s Market’s column on Thursday morning explaining, “S&P Ticks Down as Data Point to Factory Rebound.” We are not sure that that is what the factory data showed as the ISM Manufacturing Index that the WSJ was referencing did come in better than expected at a tally of 47.7, but such a reading historically has suggested a 0.3% contraction in real U.S. GDP on an annual basis.

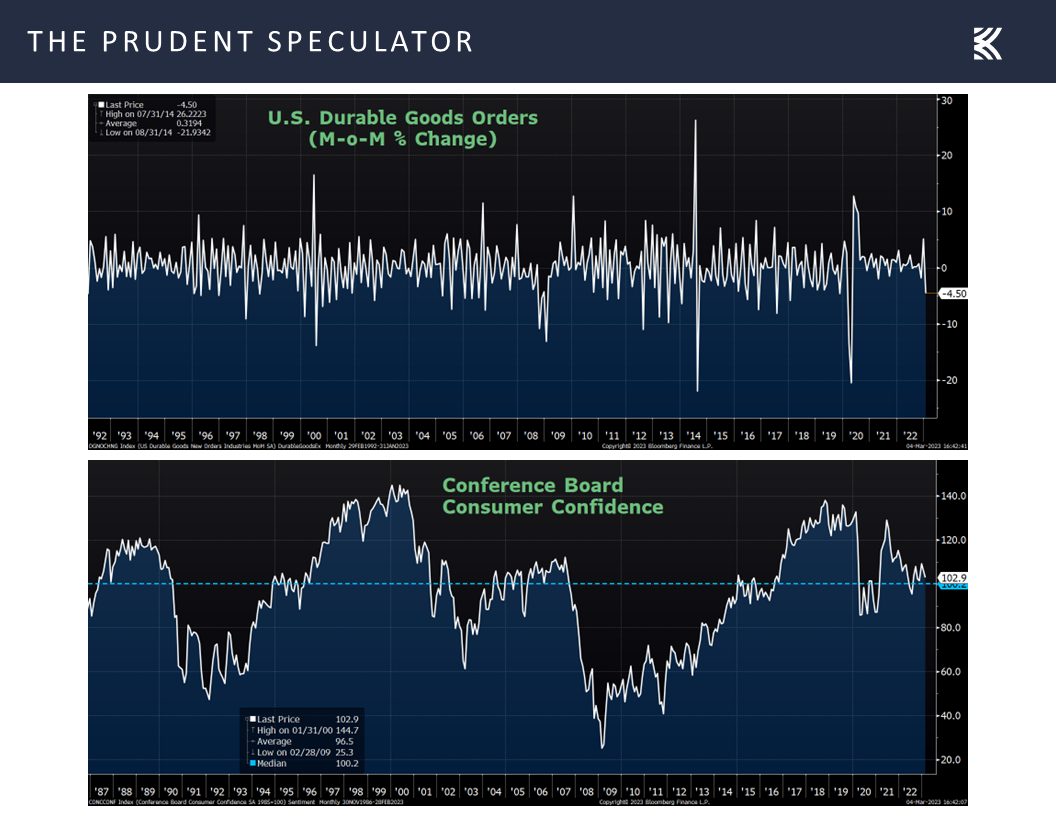

Considering that there were weaker-than-expected numbers on durable goods orders and consumer confidence out earlier in the week, we might argue that stocks were pulling back on concerns about the health of the economy, rather than on worries that strong economic data would compel the Federal Reserve to be more aggressive in hiking interest rates.

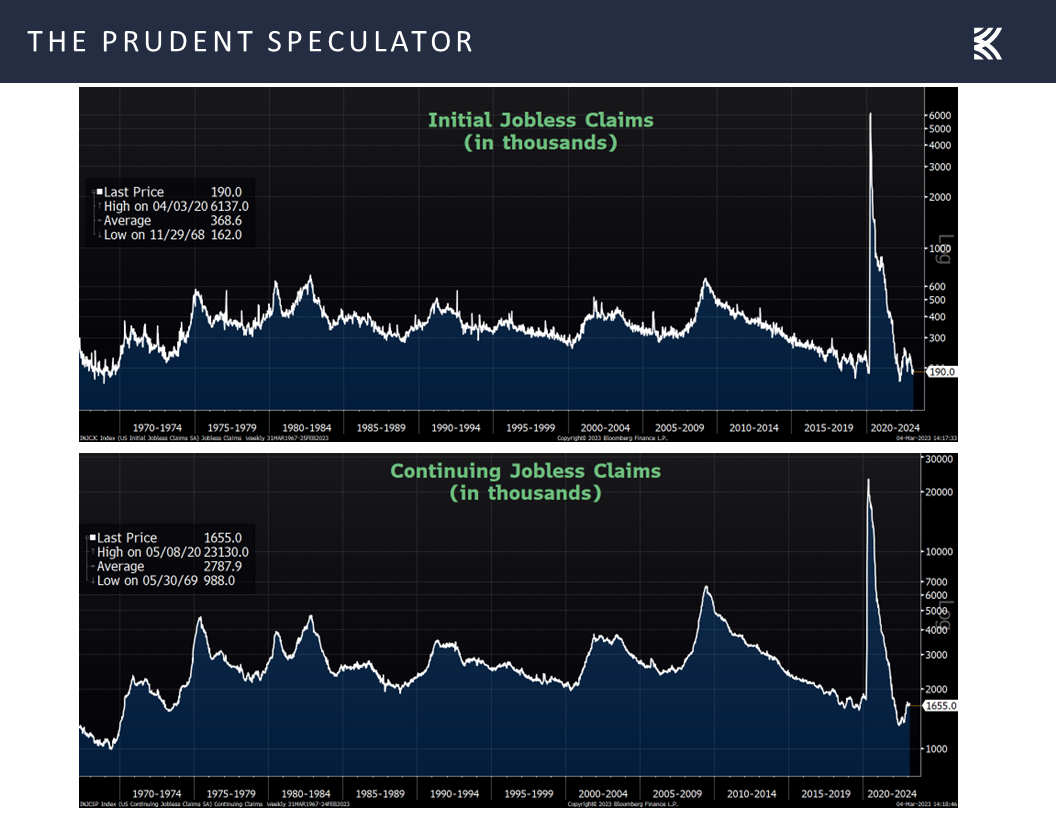

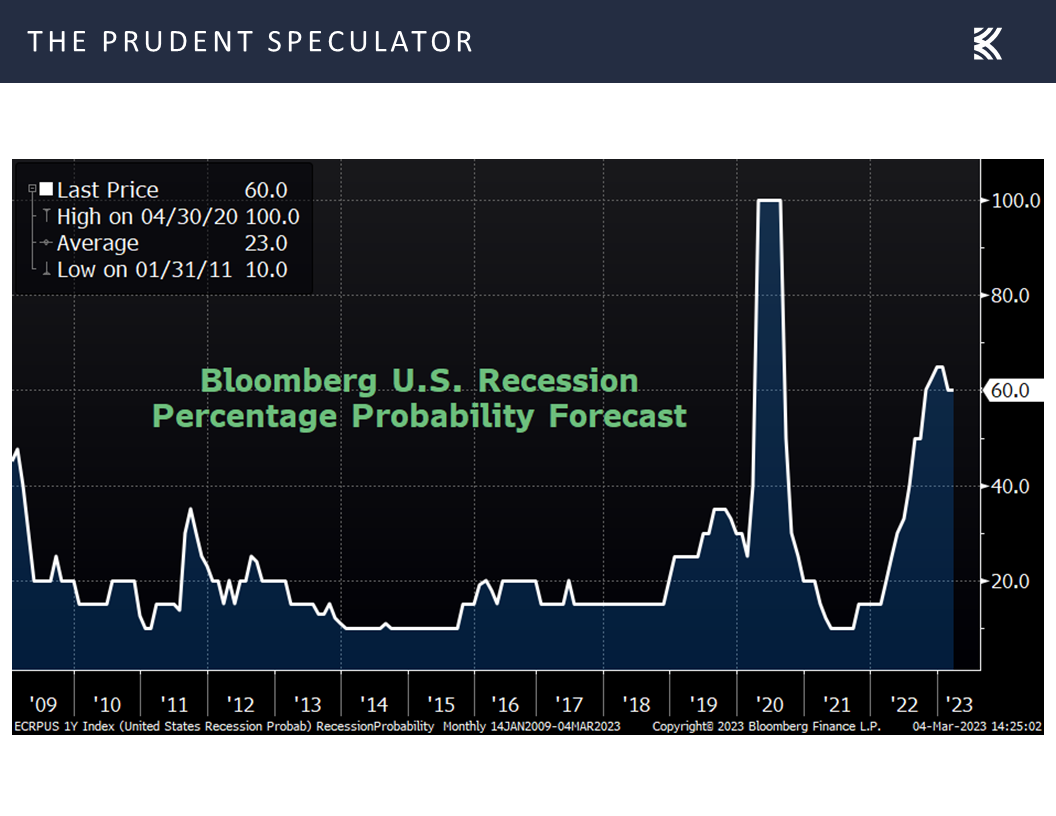

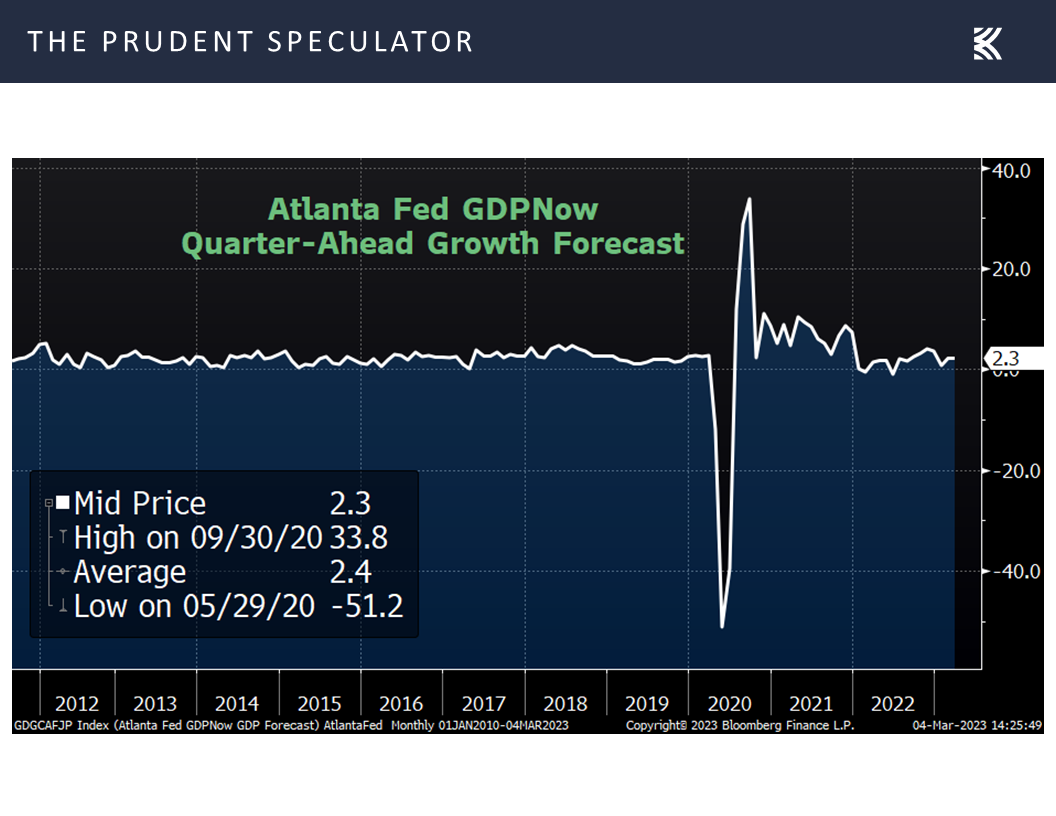

However, the latter seemed to be a better explanation as stocks again headed lower in trading on Thursday morning after yet another robust report on weekly jobless claims. Indeed, the number of first-time filings came in at 190,000, remaining near five-decade-plus lows, and confounding the doom-and-gloom crowd who have been of the mind that a recession must be in the near-term cards. Though down from a 2023 high of 67.5%, the odds of an economic contraction, per Bloomberg, now stand at 60%, which is interesting in that the latest projection for Q1 real (inflation-adjusted) GDP growth from the Atlanta Fed resided at a solid 2.3%.

Fed Rate Hikes: Market Grows More Hawkish

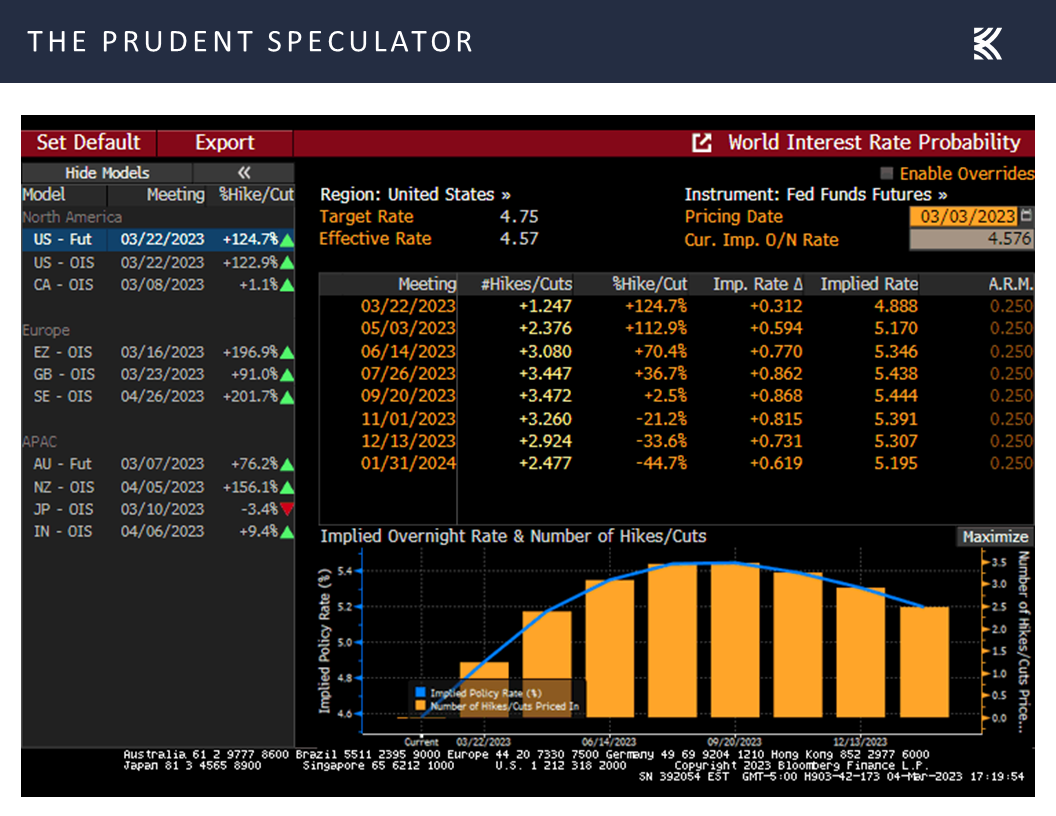

The economic outlook evidently is clear as mud, with the same seemingly to be said for the path of future Federal Reserve interest rate hikes. While some had begun to price in a 50-basis-point boost to the Fed Funds rate at this month’s FOMC meeting, equities staged a big rebound later on Thursday when Atlanta Fed President Raphael Bostic said that he supports a 25-basis-point increase, adding that there is a “plausible case” that prior hikes would still slow the economy.

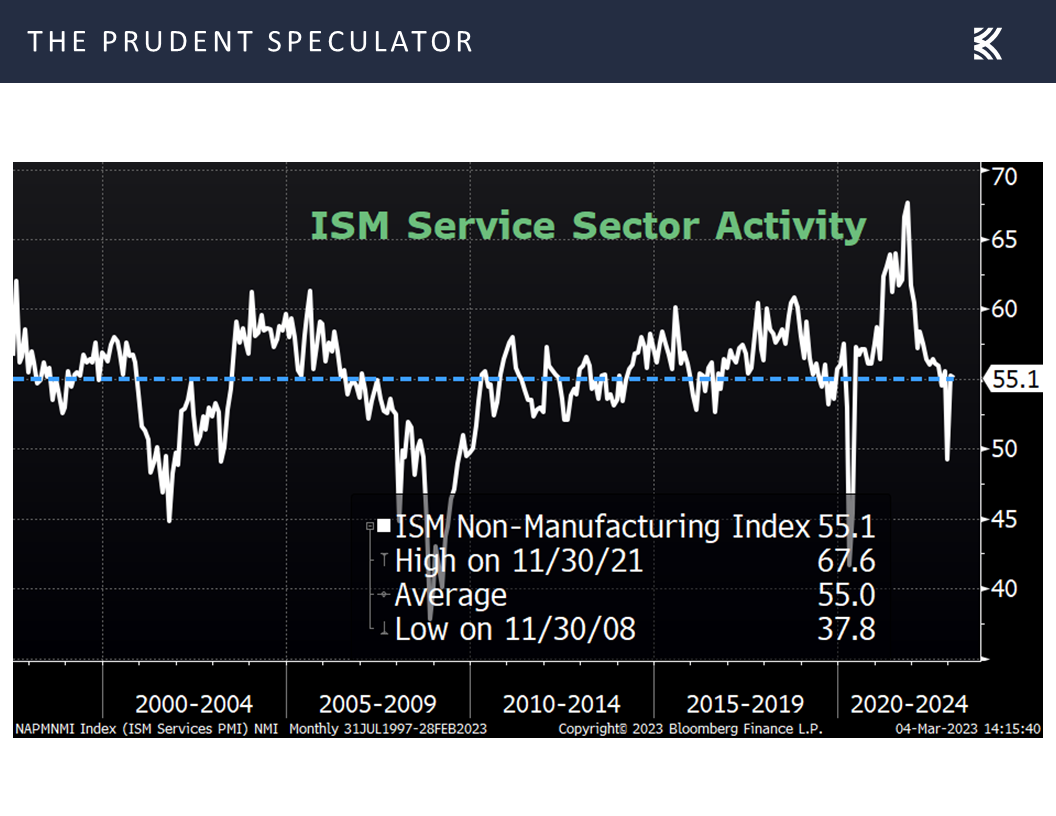

That rally gained steam on Friday, even as the important ISM Services index beat Wall Street forecasts in scoring 55.1 in February, a number that coincides with a decent 1.8% increase in real GDP growth on an annual basis, and the futures market ended the week with a more hawkish view of the peak (now 5.44%) in the Fed Funds rate as well as the year-end level than at the end of the prior week.

Valuations: Inexpensive Metrics & Generous Dividend Yield for TPS Portfolio

As more or less has been the case for our entire 46-year history of publishing The Prudent Speculator, we believe that time in the market trumps market timing and we see no reason to alter our optimism for the long-term prospects of our broadly diversified portfolios of what we believe to be undervalued stocks.

46th Anniversary: Equities Very Rewarding Since the Launch of The Prudent Speculator in 1977

That does not mean that there won’t be downside volatility with which to contend and we concede that we have managed to avoid precisely zero of the 37 corrections of 10% or more that have taken place since the inaugural edition of our publication in March 1977. However, every one of those downturns was followed by a rebound of far greater magnitude, so much so that returns on equities, especially Value Stocks and Dividend Payers have been fantastic over the past nearly 46 years.

However, every one of those downturns was followed by a rebound of far greater magnitude, so much so that returns on equities, especially Value Stocks and Dividend Payers have been fantastic over the past nearly 46 years.

We would also add that even if we could somehow predict when a recession would begin and end, history suggests that on average anyone with a long-term time horizon would want to maintain their equity exposure.

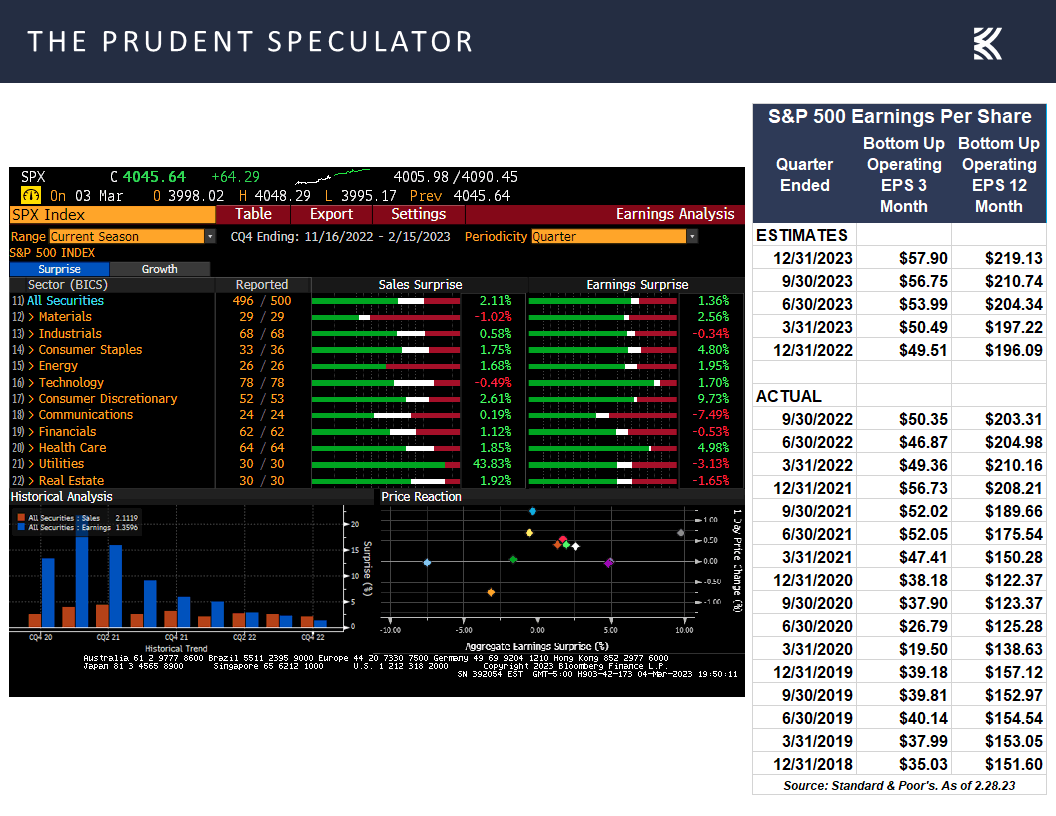

Corporate Profits: Solid Q4 EPS and Decent Outlook for 2023

This would seem to go double for the current environment as nominal GDP is likely to show a healthy advance, even if inflation-adjusted growth suffers the modest retreat that so many have been projecting with a relatively favorable economic environment continuing to provide a solid backdrop for corporate profits, which are still expected to show a sizable increase in 2023.

Stock News & Earnings – Updates on 10 stocks across 7 sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Stock Market Grows Hawkish plus Equities Very Rewarding Since the Launch of The Prudent Speculator in 1977

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. This week, we cover the late stock market rebound, dividend yields, economic numbers, valuations and earnings, The Prudent Speculator’s 46th Anniversary and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Week In Review:

With Growth leading the charge, cutting the deficit against Value since the recent September 30, 2022, market lows, equities enjoyed a terrific last two days of the trading week, which stopped a three-week losing streak and pushed the Dow Jones Industrial Average back into the green for the year.

Interestingly, the rebound came as the good folks at MarketWatch proclaimed, “Data Shows Investors Running Toward Safety of Cash as Stock Market Stumbles, Yields Rise.” In a column called The Tell, MarketWatch explained, “Investors poured $68.1 billion into cash funds in the week to Wednesday as concerns over additional Federal Reserve rate hikes continue to rattle financial markets, according to figures from Bank of America, Goldman Sachs and TD Securities, all citing EPFR data [which also showed that $7.4 billion left stock funds] in their weekly notes.”

A couple of days does not a trend make but zigging when they should have zagged is not an unusual occurrence, with data from the American Association of Individual Investors (AAII) vividly illustrating the point. The latest AAII weekly sentiment gauge saw a big jump to 44.8% in the number of respondents who say they are Bearish on the prospects for stocks over the next six months, with their lead over those who say they are Bullish widening to 21.4 percentage points and putting the Bull-Bear spread in the lowest decile of all the readings dating back to 1987. Incredibly, 1-week, 1-month, 3-month, and 6-month forward returns are best when the folks on Main Street are very pessimistic…like they are today.

DALBAR QAIB: Stock and Especially Bond Fund Investors are Awful Market Timers

We have long admonished that the only problem with market timing is getting the timing right, and numbers further confirming this view arrived this week as the 2022 DALBAR Quantitative Analysis of Investor Behavior returns were released. The data provider’s calculations show just how bad the average stock fund investor has performed, with the 3% or so deficit versus the S&P 500’s return last year in line with the dismal returns endured over the past three decades.

And if you think the 6.8% annualized return over the last 30 years for the average equity fund investor versus the 9.7% return for the S&P 500 is bad, take a gander at the average fixed income investor. Believe it or not, DALBAR calculates that folks actually have lost money on average in bond funds over the past 30 years! And stocks are supposed to be the risky asset class?

Patience: The Longer the Hold the Lower the Chance of Loss

Certainly, bond prices are less volatile than stock prices, but given that the average fixed income investor lost money in every period DALBAR studied, we remain puzzled that so many continue to think about risk in terms of volatility of one-month returns. This is especially true in that most are investing for long-term objectives. We know that we won’t win any Stocks are not as Risky as Bonds debates, and there is no assurance that past is prologue, but we can’t help but point out that there has not been a 15-year or 20-year period in which Value Stocks or Dividend Payers lost money, provided those who owned them did not stray from their course along the way.

Econ Numbers: Mixed Picture…as is Often the Case

While the long-term trend has been up, many think they can bail out and avoid the inevitable trips south and somehow get back into stocks before the next upswing. Alas, the path stock prices traverse will always be bumpy and there is no way that anyone can predict with any certainty the short-term direction.

After all, consider that stocks were moving lower last week, with The Wall Street Journal’s Market’s column on Thursday morning explaining, “S&P Ticks Down as Data Point to Factory Rebound.” We are not sure that that is what the factory data showed as the ISM Manufacturing Index that the WSJ was referencing did come in better than expected at a tally of 47.7, but such a reading historically has suggested a 0.3% contraction in real U.S. GDP on an annual basis.

Considering that there were weaker-than-expected numbers on durable goods orders and consumer confidence out earlier in the week, we might argue that stocks were pulling back on concerns about the health of the economy, rather than on worries that strong economic data would compel the Federal Reserve to be more aggressive in hiking interest rates.

However, the latter seemed to be a better explanation as stocks again headed lower in trading on Thursday morning after yet another robust report on weekly jobless claims. Indeed, the number of first-time filings came in at 190,000, remaining near five-decade-plus lows, and confounding the doom-and-gloom crowd who have been of the mind that a recession must be in the near-term cards. Though down from a 2023 high of 67.5%, the odds of an economic contraction, per Bloomberg, now stand at 60%, which is interesting in that the latest projection for Q1 real (inflation-adjusted) GDP growth from the Atlanta Fed resided at a solid 2.3%.

Fed Rate Hikes: Market Grows More Hawkish

The economic outlook evidently is clear as mud, with the same seemingly to be said for the path of future Federal Reserve interest rate hikes. While some had begun to price in a 50-basis-point boost to the Fed Funds rate at this month’s FOMC meeting, equities staged a big rebound later on Thursday when Atlanta Fed President Raphael Bostic said that he supports a 25-basis-point increase, adding that there is a “plausible case” that prior hikes would still slow the economy.

That rally gained steam on Friday, even as the important ISM Services index beat Wall Street forecasts in scoring 55.1 in February, a number that coincides with a decent 1.8% increase in real GDP growth on an annual basis, and the futures market ended the week with a more hawkish view of the peak (now 5.44%) in the Fed Funds rate as well as the year-end level than at the end of the prior week.

Valuations: Inexpensive Metrics & Generous Dividend Yield for TPS Portfolio

As more or less has been the case for our entire 46-year history of publishing The Prudent Speculator, we believe that time in the market trumps market timing and we see no reason to alter our optimism for the long-term prospects of our broadly diversified portfolios of what we believe to be undervalued stocks.

46th Anniversary: Equities Very Rewarding Since the Launch of The Prudent Speculator in 1977

That does not mean that there won’t be downside volatility with which to contend and we concede that we have managed to avoid precisely zero of the 37 corrections of 10% or more that have taken place since the inaugural edition of our publication in March 1977. However, every one of those downturns was followed by a rebound of far greater magnitude, so much so that returns on equities, especially Value Stocks and Dividend Payers have been fantastic over the past nearly 46 years.

However, every one of those downturns was followed by a rebound of far greater magnitude, so much so that returns on equities, especially Value Stocks and Dividend Payers have been fantastic over the past nearly 46 years.

We would also add that even if we could somehow predict when a recession would begin and end, history suggests that on average anyone with a long-term time horizon would want to maintain their equity exposure.

Corporate Profits: Solid Q4 EPS and Decent Outlook for 2023

This would seem to go double for the current environment as nominal GDP is likely to show a healthy advance, even if inflation-adjusted growth suffers the modest retreat that so many have been projecting with a relatively favorable economic environment continuing to provide a solid backdrop for corporate profits, which are still expected to show a sizable increase in 2023.

Stock News & Earnings – Updates on 10 stocks across 7 sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.