The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s stock market news, we discuss undervalued stocks, higher interest rates, recession, contrarian sentiments and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

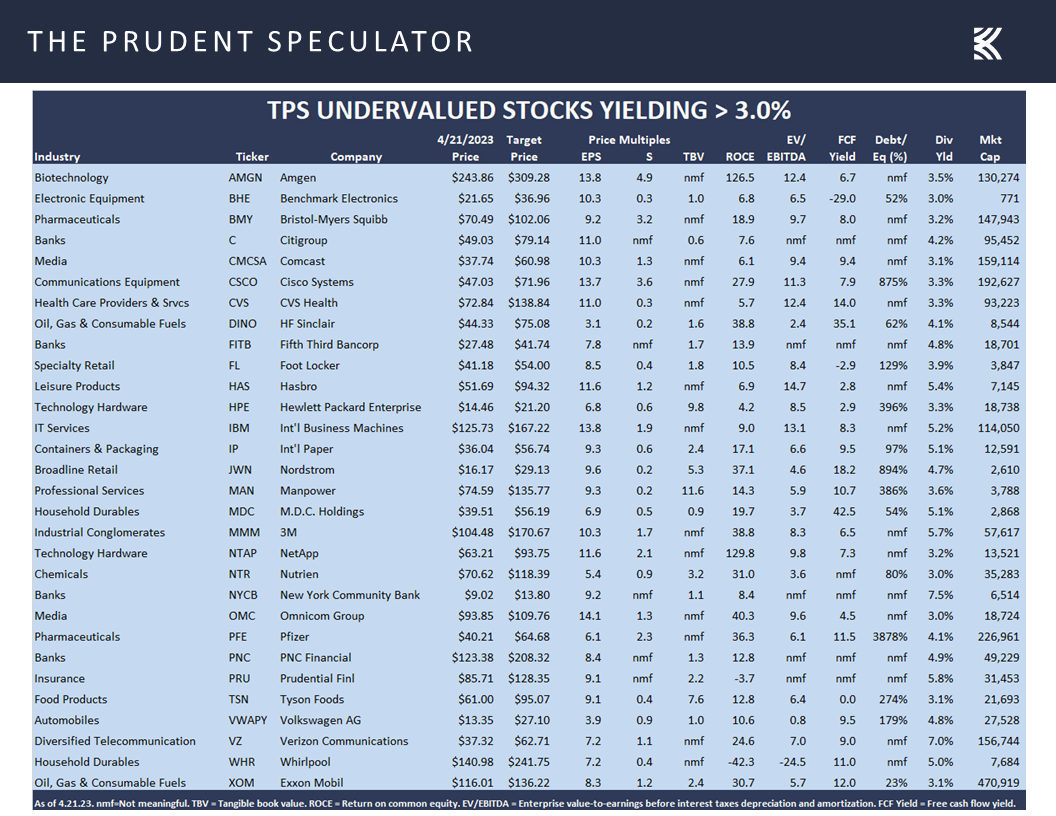

Vegas MoneyShow – 30 Undervalued 3%+ Yielders

Higher Interest Rates – No Reason to Sell Value Stocks or Dividend Payers

Valuations – Value Stocks are Attractive and We Like the Metrics for our Portfolios

Wall of Worry – Stock Have Overcome Plenty of Disconcerting News in the Fullness of Time

Recession? – Mixed Econ Numbers & Historical Equity Return Perspective

Earnings – Healthy Corporate Profits in ’23 and ’24 Still the Projection

Contrarian Sentiment – AAII Still Pessimistic

Stock News – Update on sixteen stocks across eight different sectors

Vegas MoneyShow – 30 Undervalued 3%+ Yielders

Your Editor is off to the MoneyShow Las Vegas later today to give a couple of presentations – The Value of Dividends and Value Investing 101a and 101b. I hope to see some of our readers at the show, but understanding that most won’t be able to attend, we provide a slide from the second talk featuring a 30-stock listing of what we believe to be undervalued stocks, all of which yield at least 3%.

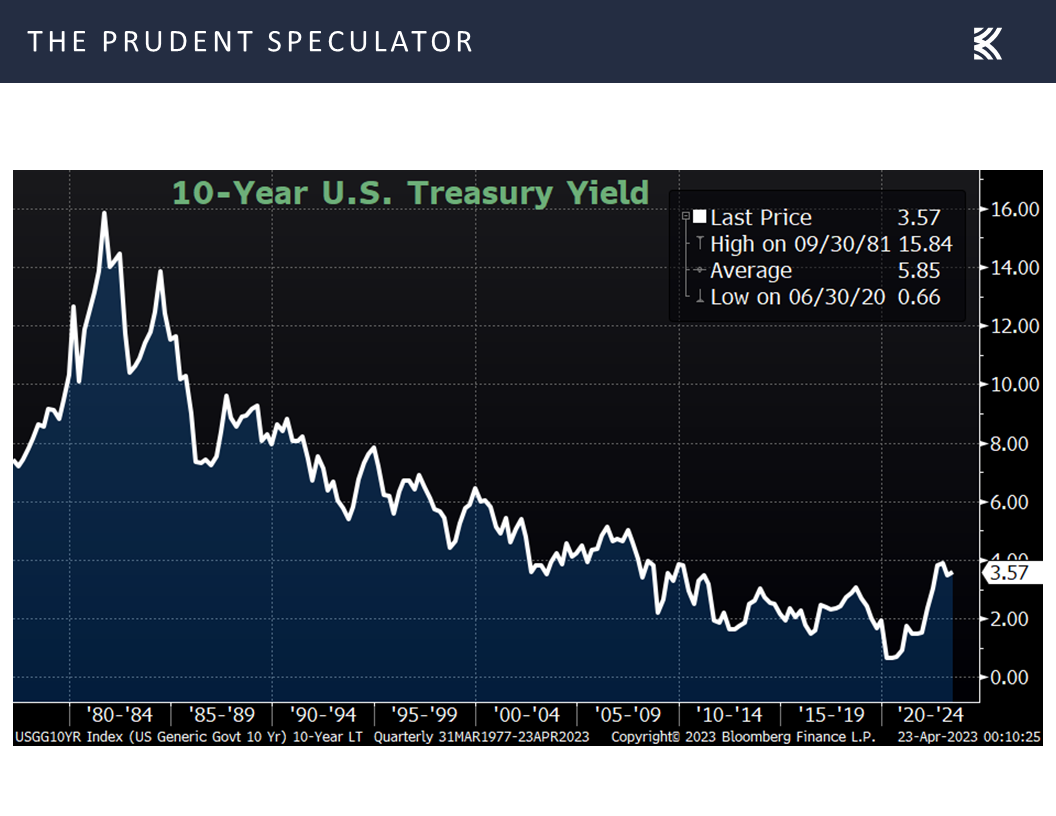

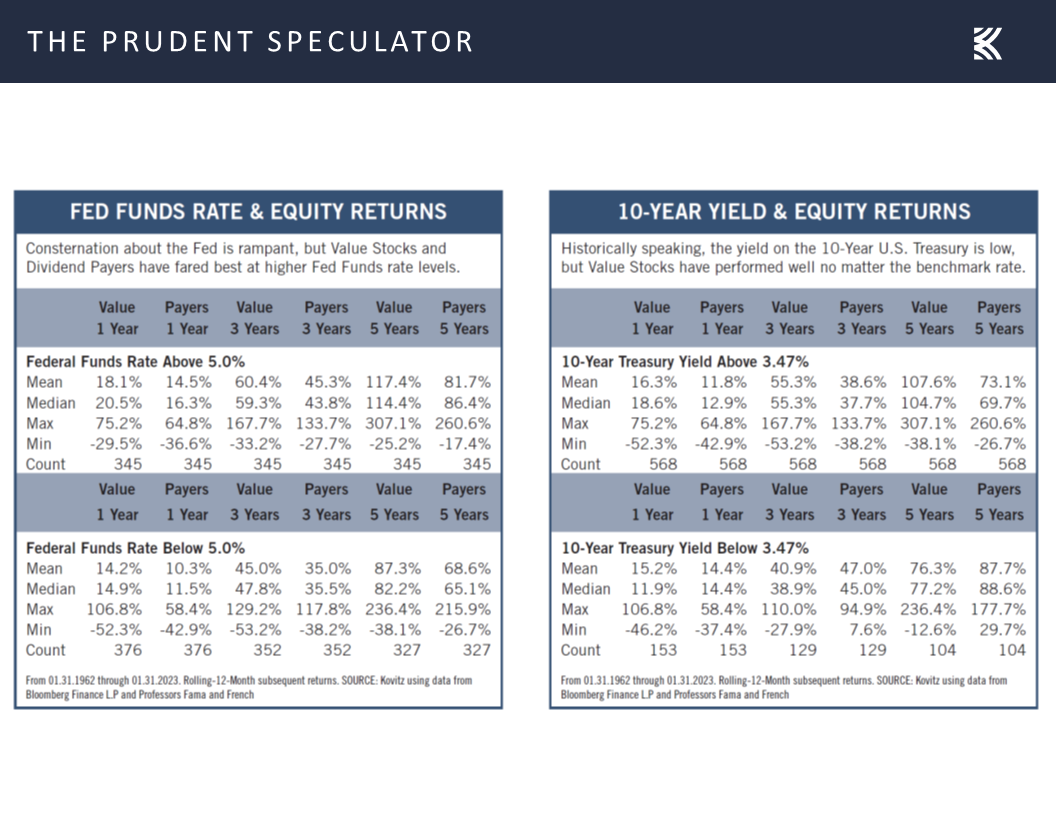

Higher Interest Rates – No Reason to Sell Value Stocks or Dividend Payers

Certainly, we understand that some may not be as enthused about dividend=paying stocks in a higher interest rate environment, but we point out that the 3.57% current yield on the benchmark 10-Year U.S. Treasury is still well below the 5.85% average since the launch of The Prudent Speculator in March 1977,

while history shows that Payers have performed well, on average, whether interest rates are high or low, and they actually have done better on a go-forward basis when the Fed Funds rate is above the current 5.0% level.

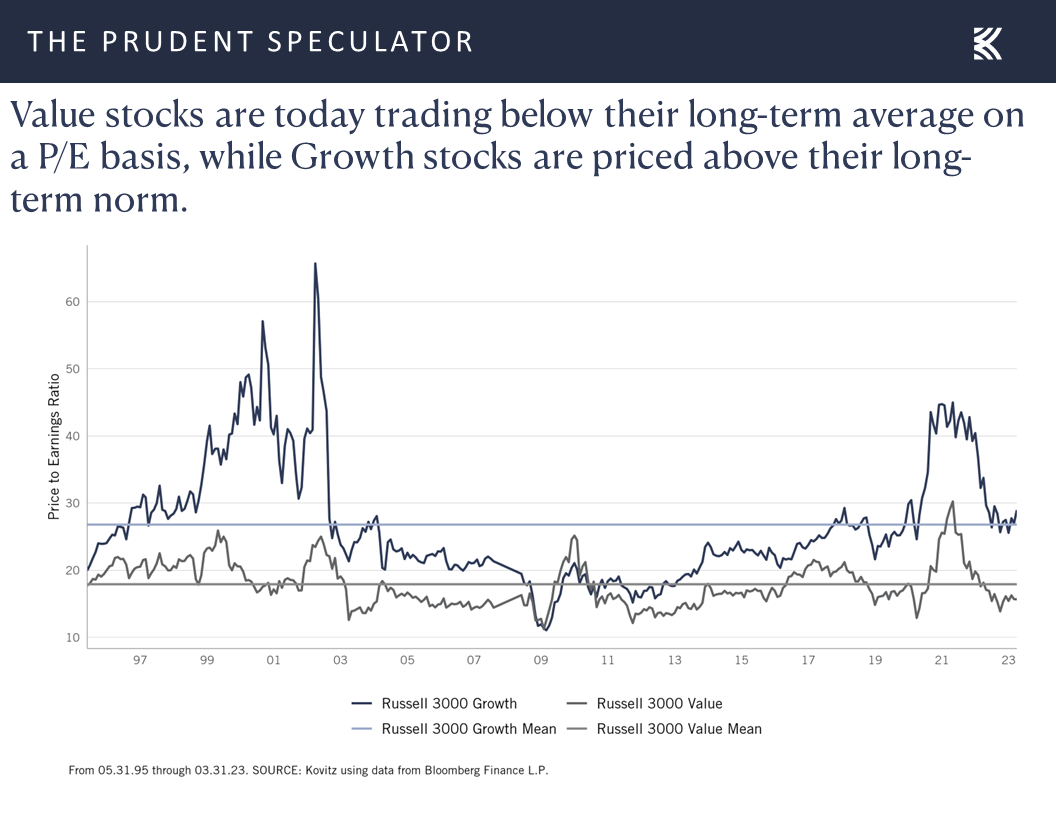

We also note, given concerns some have about equity valuations, that Value Stocks are today priced below their average since 1995, which is the date that numbers are available for the Russell 3000 Value and Growth indexes,

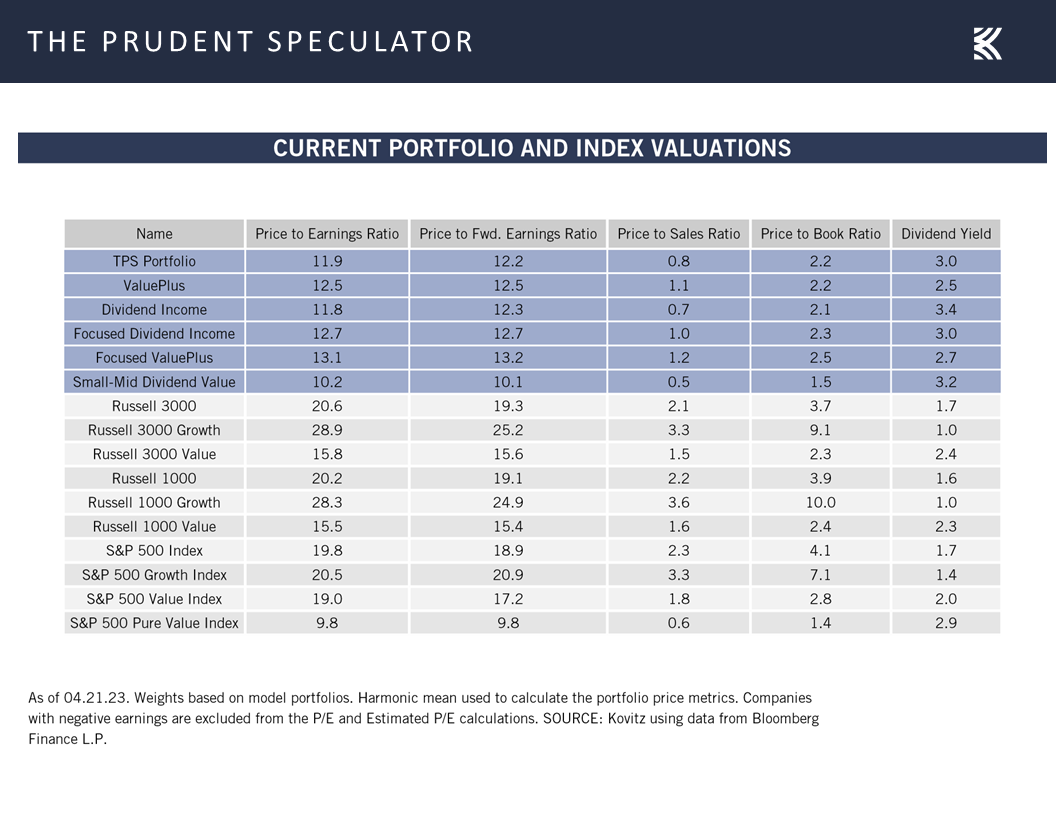

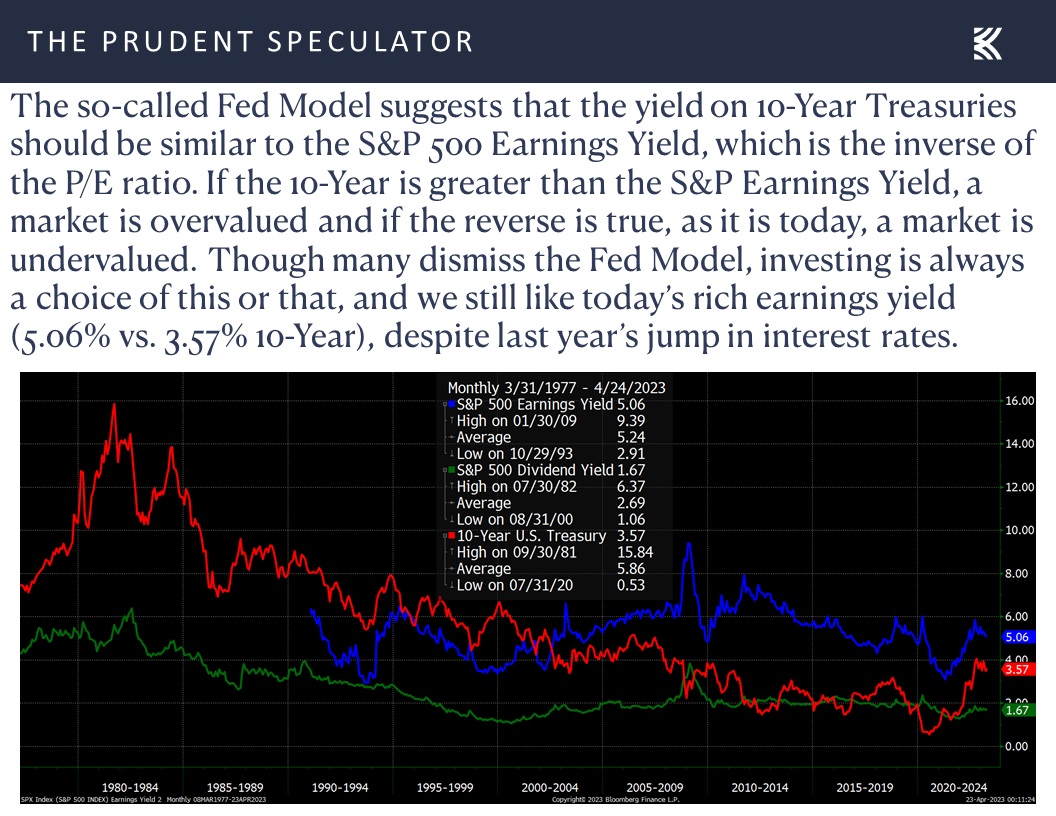

Valuations – Value Stocks are Attractive and We Like the Metrics for our Portfolios.

while we continue to sleep well at night with the reasonable valuations on our broadly diversified portfolios.

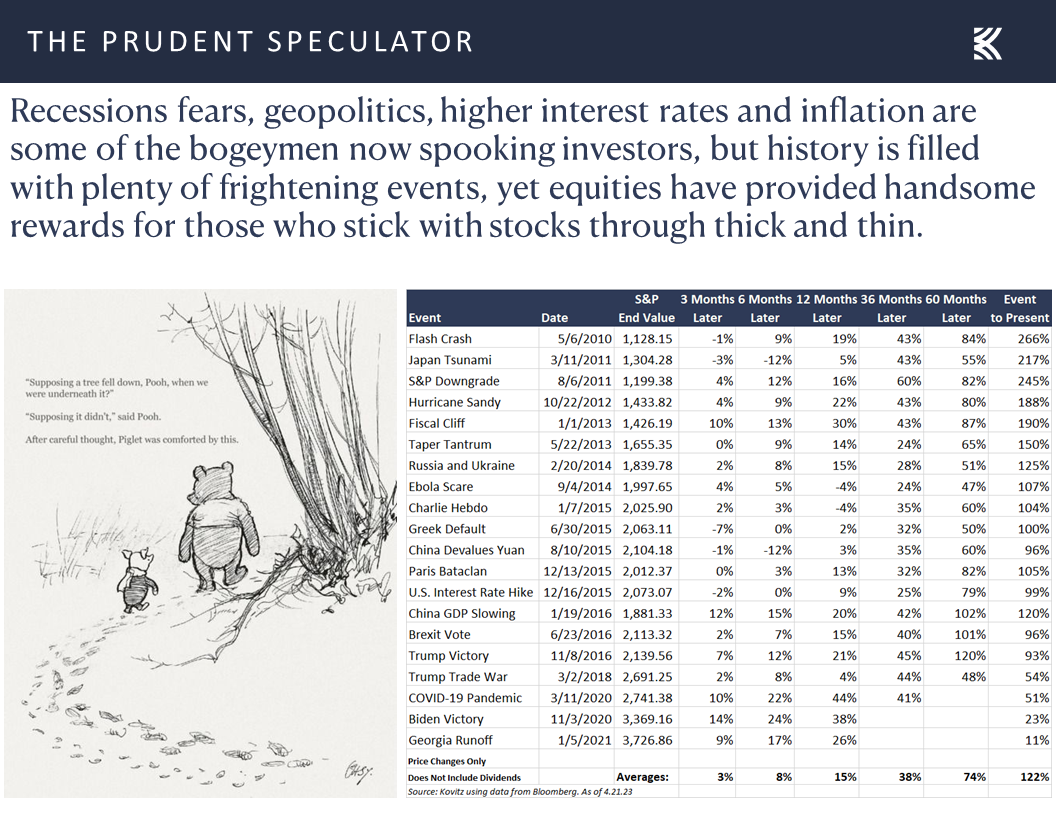

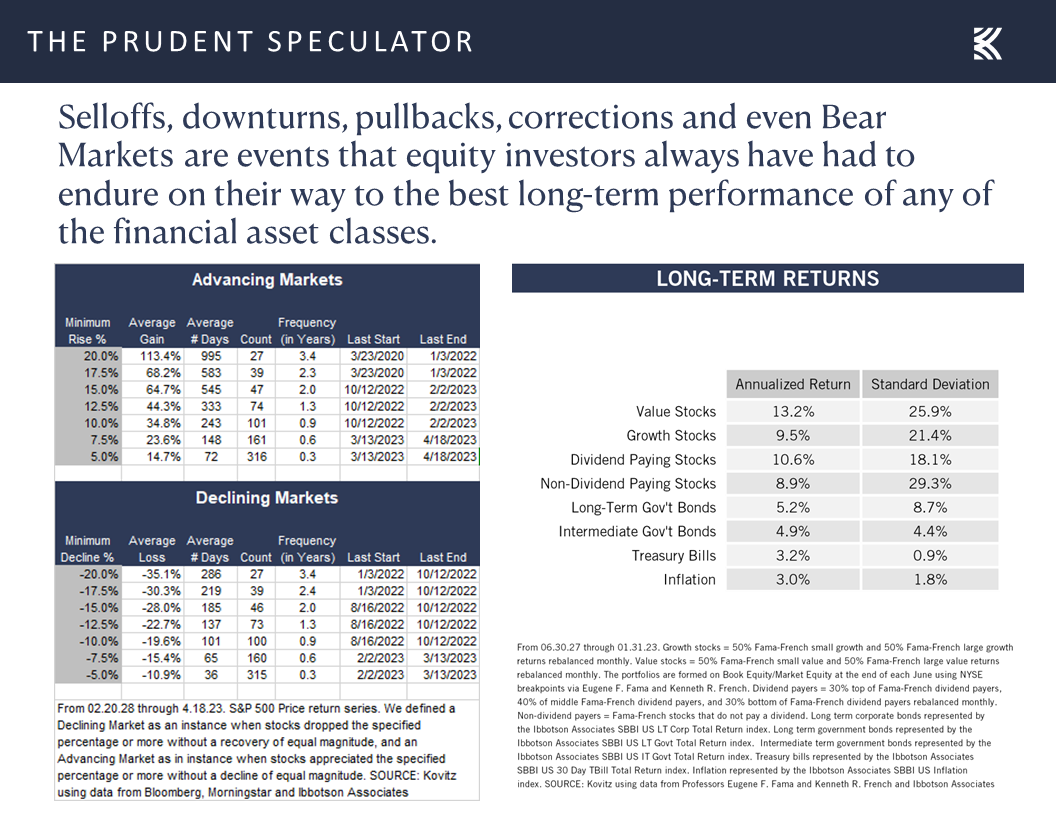

Wall of Worry – Stocks Have Overcome Plenty of Disconcerting News in the Fullness of Time

Equity investors have plenty about which to be concerned these days, which if we study market history is no different than usual, but stocks have long climbed a wall of worry.

Equity investors have plenty about which to be concerned these days, which if we study market history is no different than usual, but stocks have long climbed a wall of worry.

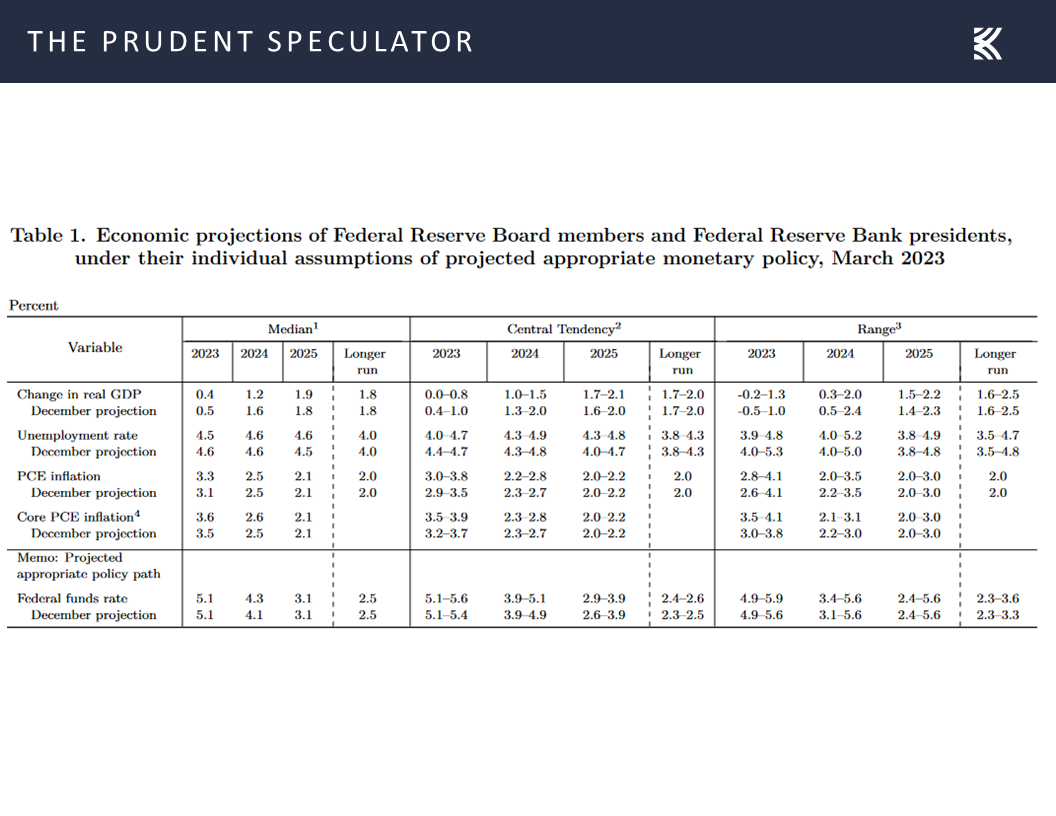

and the latest projections from the Federal Reserve call for real (inflation-adjusted) GDP to grow 0.4% this year and 1.2% in 2024.

and the latest projections from the Federal Reserve call for real (inflation-adjusted) GDP to grow 0.4% this year and 1.2% in 2024.

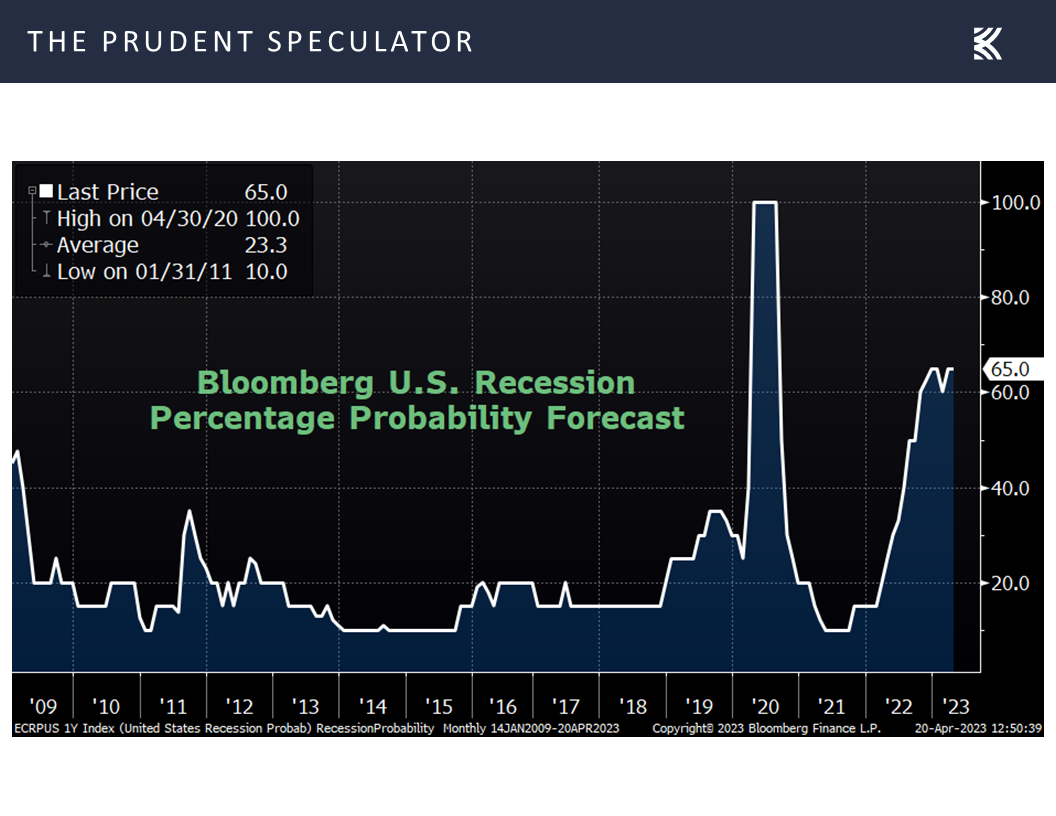

Recession? – Mixed Econ Numbers & Historical Equity Return Perspective

To be sure, the Bloomberg recession estimate now stands at 65%,

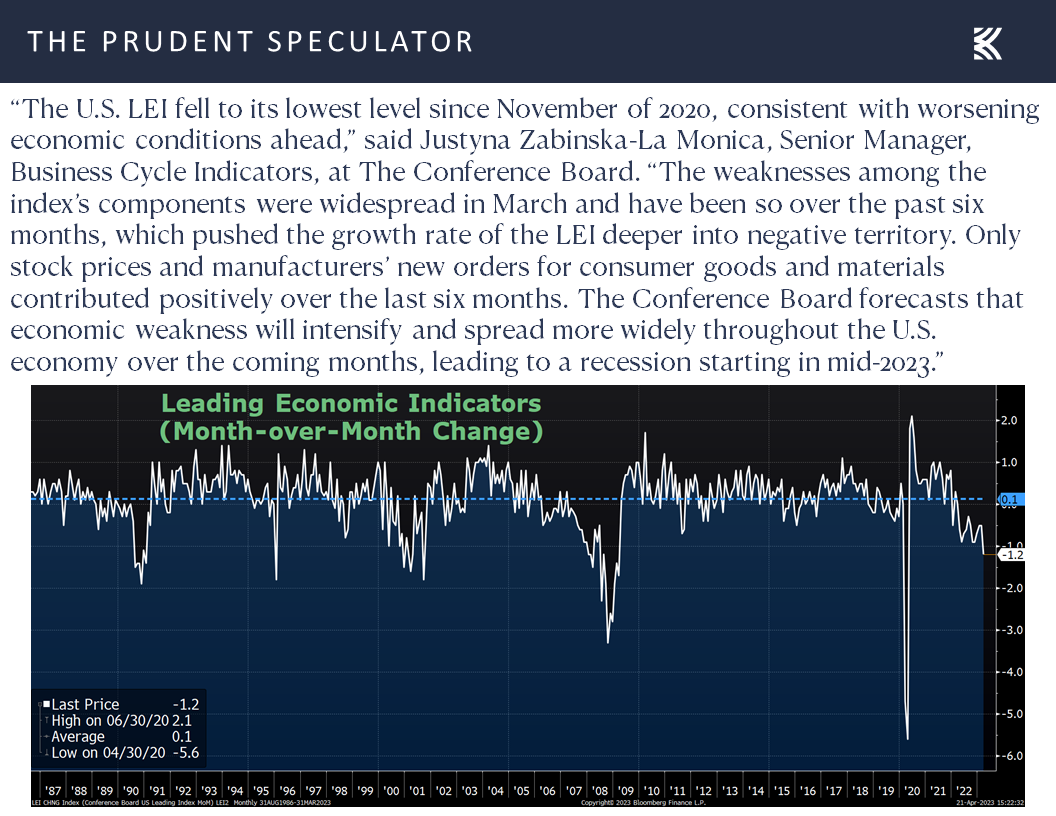

while the latest read on the forward-looking Leading Economic Index (LEI) fell by 1.2% in March. The keeper of that gauge, The Conference Board, asserted, “The U.S. LEI fell to its lowest level since November of 2020, consistent with worsening economic conditions ahead. The weaknesses among the index’s components were widespread in March and have been so over the past six months, which pushed the growth rate of the LEI deeper into negative territory. Only stock prices and manufacturers’ new orders for consumer goods and materials contributed positively over the last six months. The Conference Board forecasts that economic weakness will intensify and spread more widely throughout the US economy over the coming months, leading to a recession starting in mid-2023.”

while the latest read on the forward-looking Leading Economic Index (LEI) fell by 1.2% in March. The keeper of that gauge, The Conference Board, asserted, “The U.S. LEI fell to its lowest level since November of 2020, consistent with worsening economic conditions ahead. The weaknesses among the index’s components were widespread in March and have been so over the past six months, which pushed the growth rate of the LEI deeper into negative territory. Only stock prices and manufacturers’ new orders for consumer goods and materials contributed positively over the last six months. The Conference Board forecasts that economic weakness will intensify and spread more widely throughout the US economy over the coming months, leading to a recession starting in mid-2023.”

That sounds ominous, but we note that famed American Economist Paul Samuelson years ago joked, “Economists have predicted nine of the last five recessions,” and forecasting today remains as fraught with peril as ever. For example, we recently heard from two executives of prominent American financial institutions with conflicting views.

Bank of America (BAC – $29.87) CEO Brian Moynihan said inflation is showing signs of cooling, but the U.S. economy will still face a recession. Nevertheless, on BAC’s quarterly conference call, Mr. Moynihan hedged when he said, “Everything points to a relatively mild recession given the amount of stimulus that was paid to people and the money they have left over.”

On the other hand, BlackRock (BLK – $680.94) CEO Larry Fink cited stimulus from the Infrastructure Bill, the Chips and Science Act, and the Inflation Reduction Act as reason to think a U.S. recession won’t occur. In a television interview, Mr. Fink elaborated, “Those three bills are a trillion dollars of stimulus over the next few years. Think about how many jobs infrastructure creates. Think about the demand for commodities as we build infrastructure.”

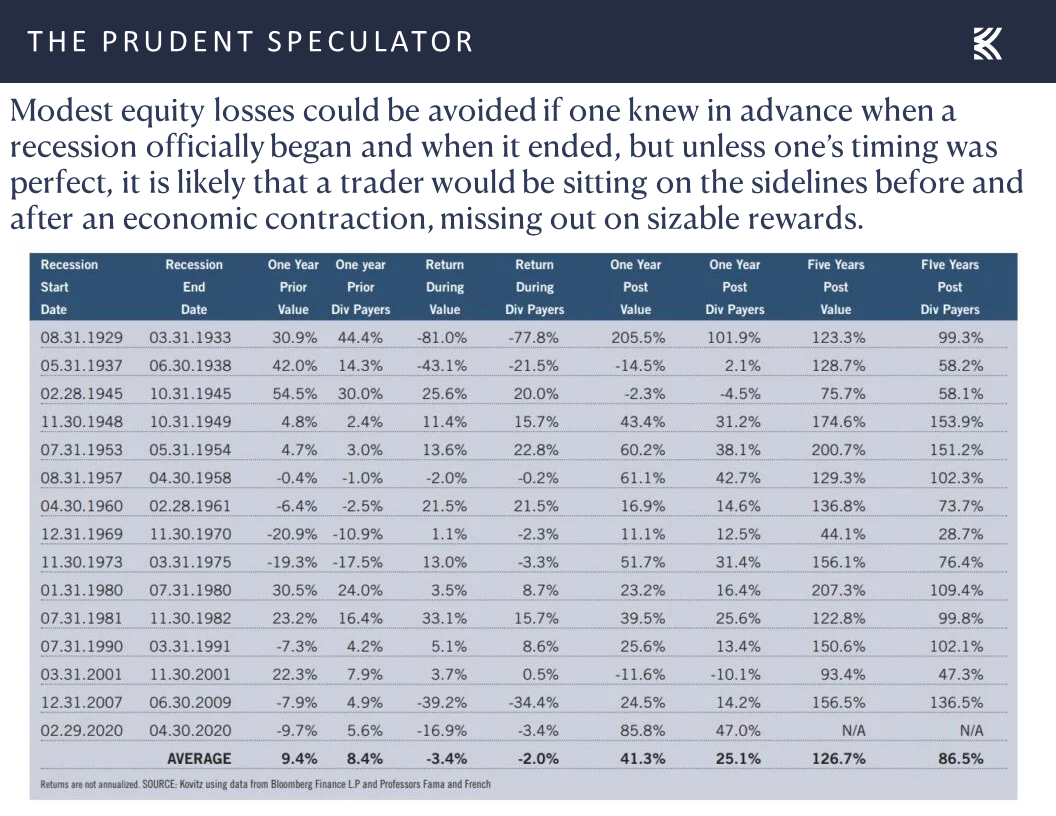

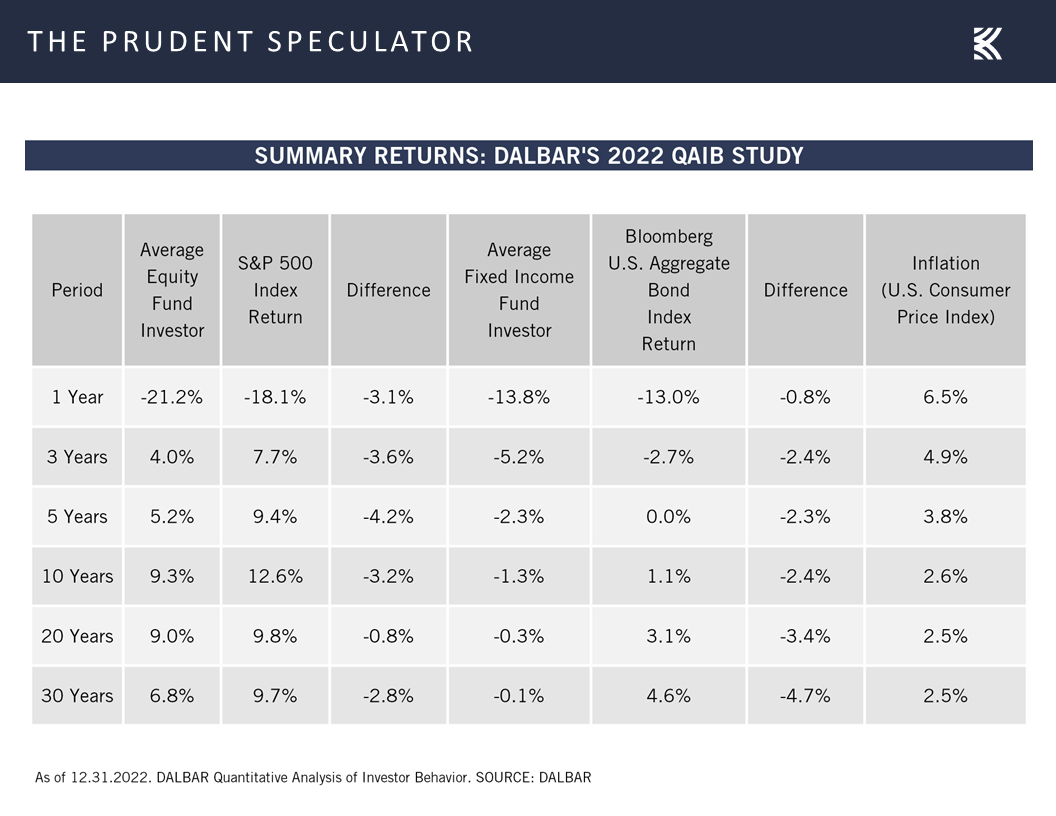

Needless to say, the economic crystal ball is cloudy, with many investors likely sitting on the sidelines, even as crunching nearly a century of data on recessions and stock returns supports the view that the time in the market trumps market timing.

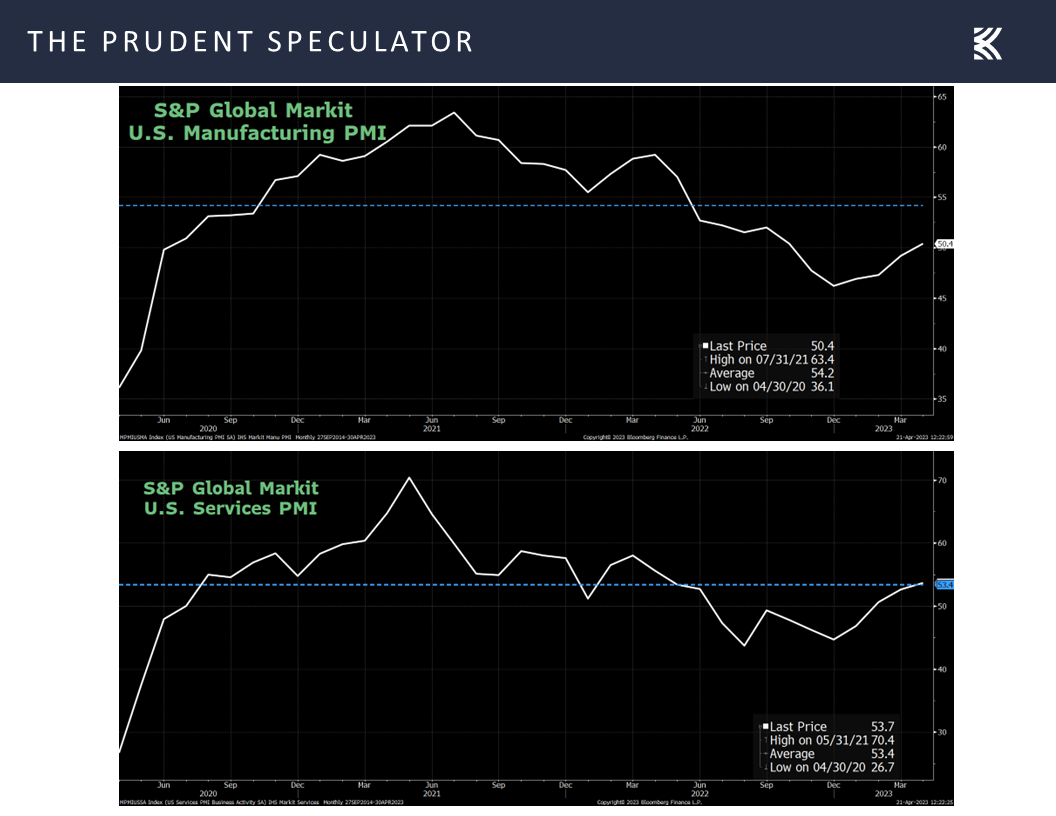

We might also point out that the first economic numbers for April from S&P Global showed stronger figures than expected on the outlook for the factory and services sectors, with both gauges hitting their highest levels in nearly a year,

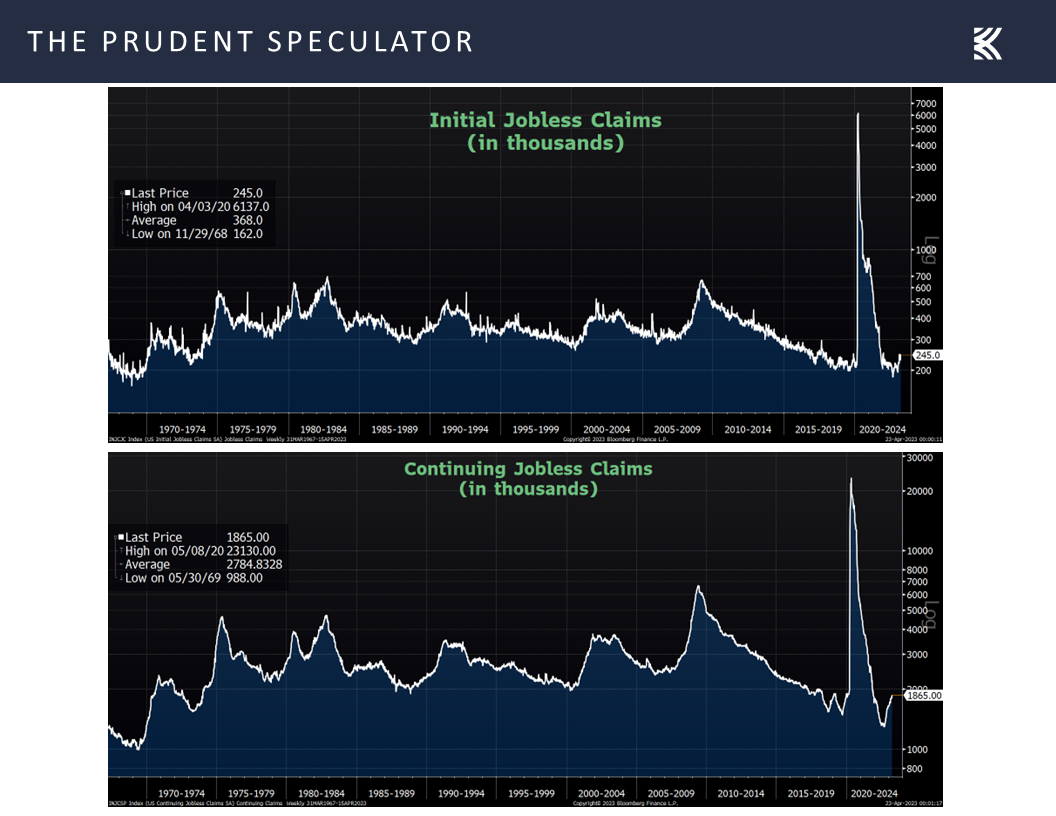

and the labor picture remains remarkably robust, even as weekly initial filings for jobless benefits have ticked up from half-century lows.

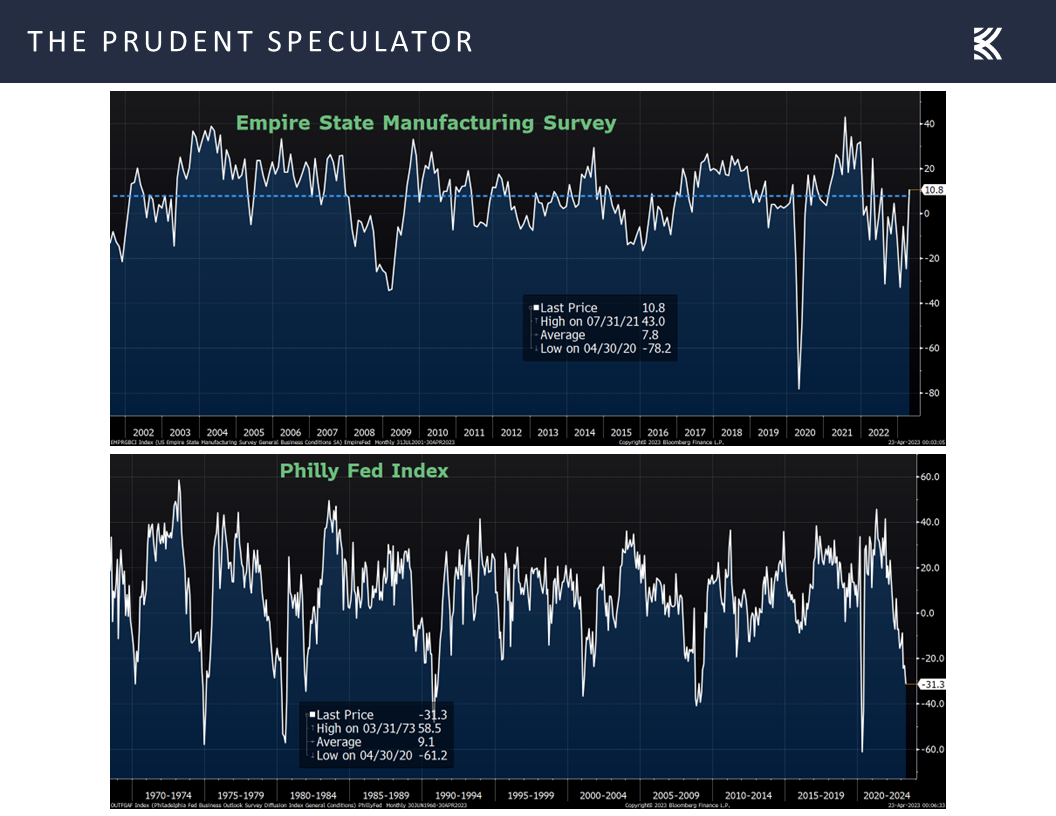

Other economic data points out last week were mixed. On the positive side, the Empire State manufacturing index for April rocketed up more than 35 points to a much-stronger-than-expected of 10.8, a tally better than the average over the past two decades. Countering that bit of good news, the more-important Philadelphia Fed factory survey dropped 8 points to a worse-than-expected minus 31.3. Of course, the last two times that Philly Fed figure was lower was April 2020 and February 2009, both fantastic times for investors to be buying stocks.

Earnings – Healthy Corporate Profits in ’23 and ’24 Still the Projection

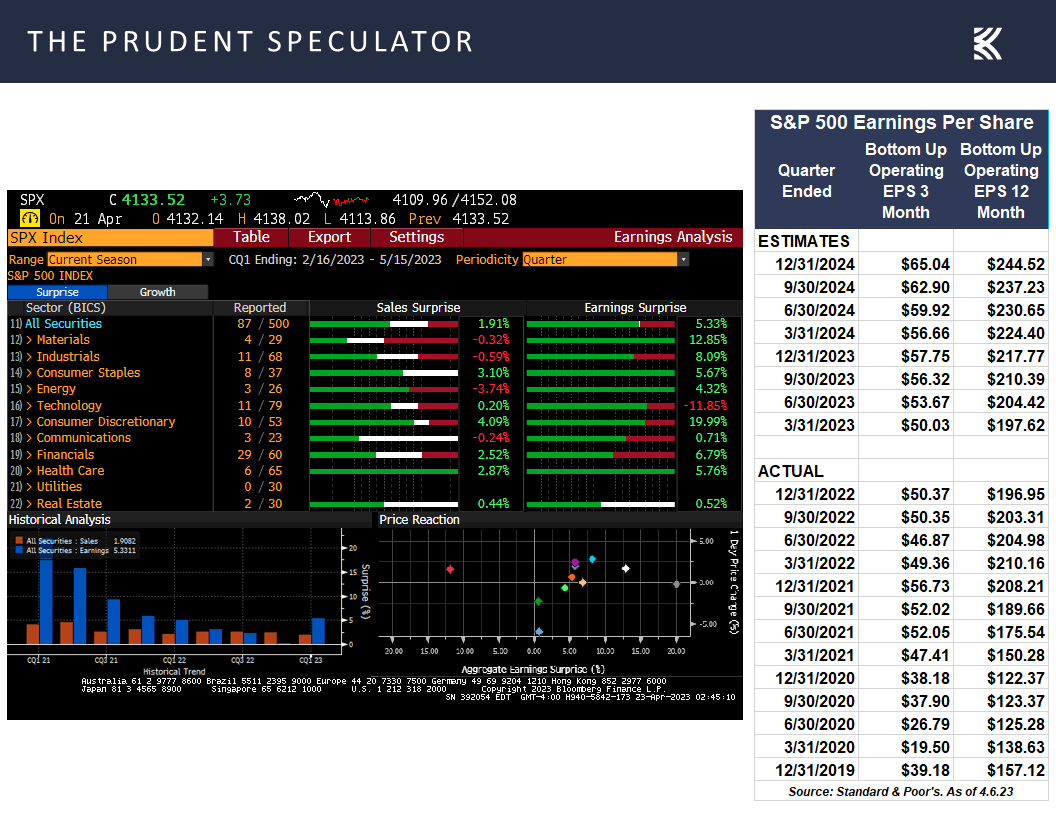

In addition, Q1 report cards from Corporate America generally have come in better-than-pessimistic forecasts thus far, with a greater-than-usual 75.9% of companies beating estimates on the bottom line. True, forward guidance has been guarded, as has been the case for quite some time, and analysts are often overly optimistic in their outlooks, but earnings are still expected to show solid growth this year and next.

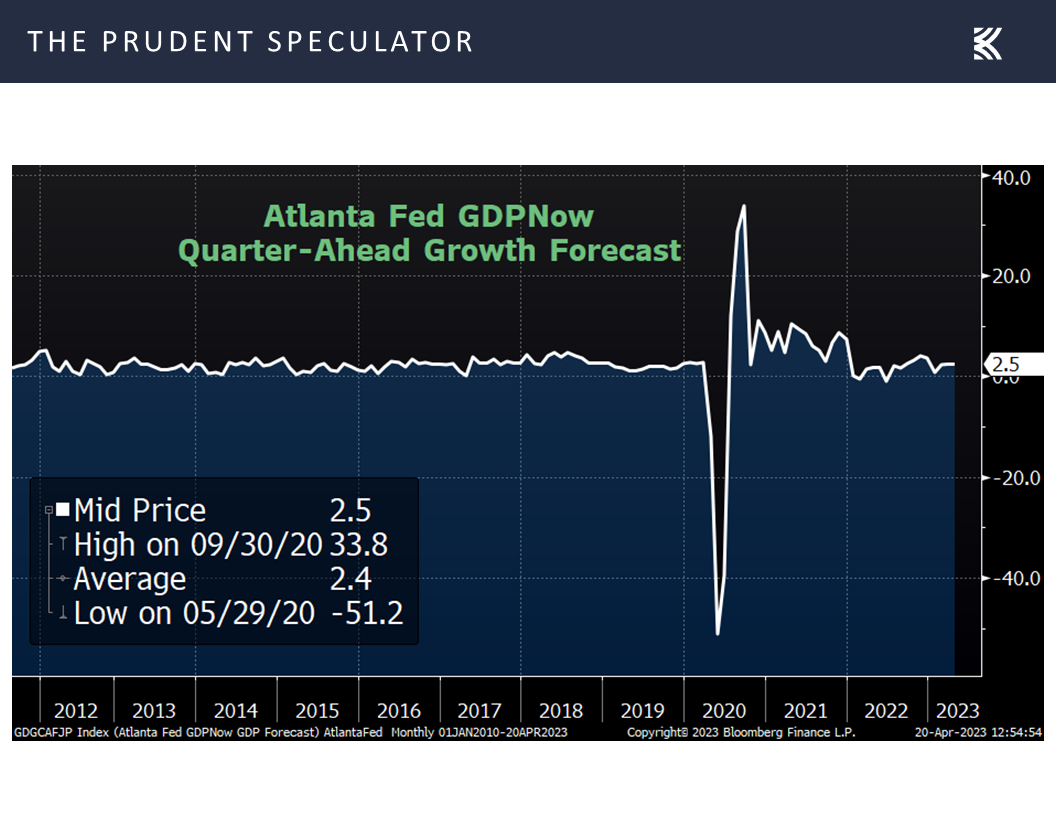

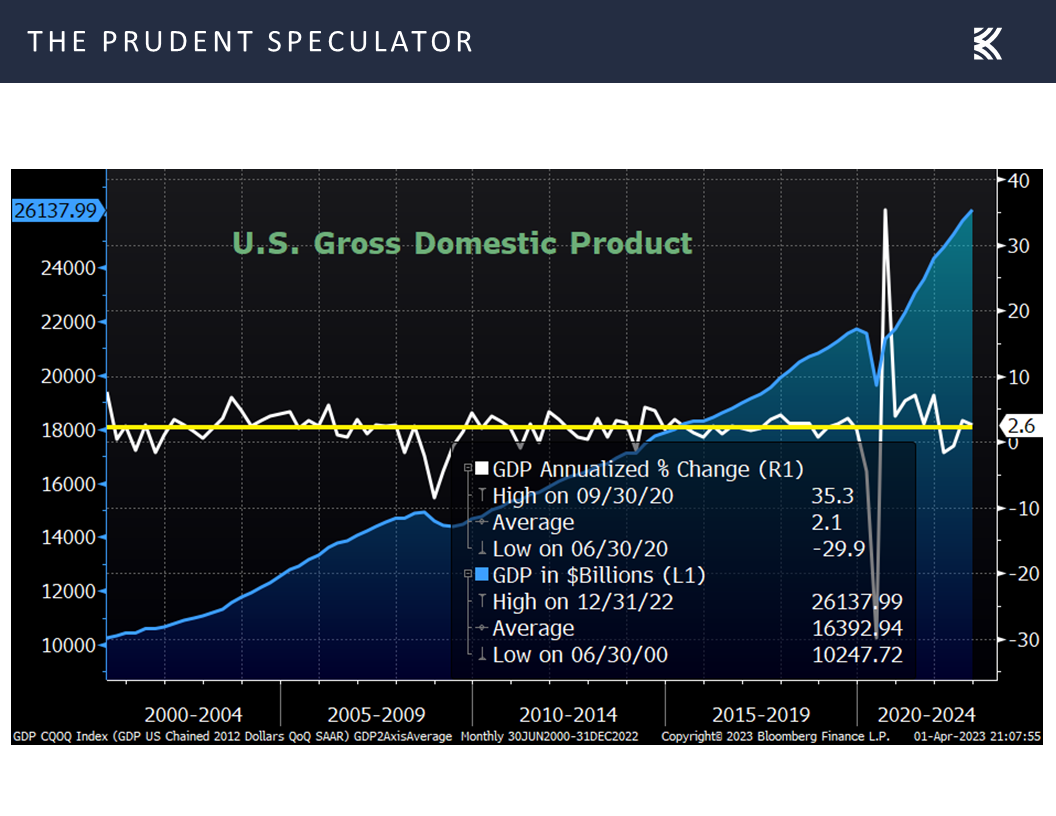

We might argue that this is due to the fact that while many are fixated on real (inflation-adjusted) GDP numbers, sales and profits, as well as stock prices, are measured in nominal (actual) dollars. As the chart below illustrates, the long-term and near-term trends in nominal GDP growth have been higher.

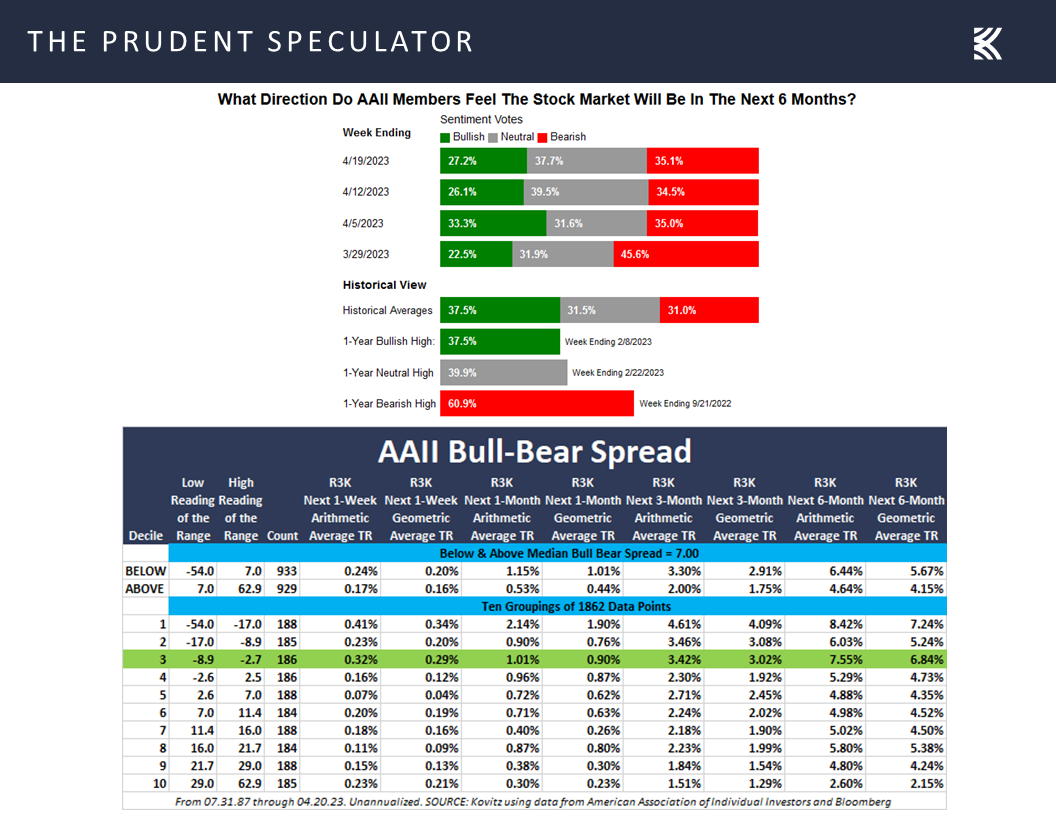

Contrarian Sentiment – AAII Still Pessimistic

We continue to be braced for downside volatility (the equity futures are pointing to a poor start to the week) as it is a the price that investors must pay to achieve handsome long-term gains,

while the weight of the historical evidence shows that those who attempt to sidestep the trips south usually end up with lousy returns in the process.

With the latest measure of Main Street investor sentiment (the contrarian AAII Bull-Bear Survey showing 27.2% Bulls and 35.1% Bears) continuing to be skewed in favor of the pessimists.

and stocks in general remaining attractively valued,

we see no reason to alter our enthusiasm for the long-term prospects for equities.

Stock Market News: Updates on sixteen stocks across eight different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Stock Market News, Higher Interest Rates, Recession? Contrarian Sentiment and more

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s stock market news, we discuss undervalued stocks, higher interest rates, recession, contrarian sentiments and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Vegas MoneyShow – 30 Undervalued 3%+ Yielders

Higher Interest Rates – No Reason to Sell Value Stocks or Dividend Payers

Valuations – Value Stocks are Attractive and We Like the Metrics for our Portfolios

Wall of Worry – Stock Have Overcome Plenty of Disconcerting News in the Fullness of Time

Recession? – Mixed Econ Numbers & Historical Equity Return Perspective

Earnings – Healthy Corporate Profits in ’23 and ’24 Still the Projection

Contrarian Sentiment – AAII Still Pessimistic

Stock News – Update on sixteen stocks across eight different sectors

Vegas MoneyShow – 30 Undervalued 3%+ Yielders

Your Editor is off to the MoneyShow Las Vegas later today to give a couple of presentations – The Value of Dividends and Value Investing 101a and 101b. I hope to see some of our readers at the show, but understanding that most won’t be able to attend, we provide a slide from the second talk featuring a 30-stock listing of what we believe to be undervalued stocks, all of which yield at least 3%.

Higher Interest Rates – No Reason to Sell Value Stocks or Dividend Payers

Certainly, we understand that some may not be as enthused about dividend=paying stocks in a higher interest rate environment, but we point out that the 3.57% current yield on the benchmark 10-Year U.S. Treasury is still well below the 5.85% average since the launch of The Prudent Speculator in March 1977,

while history shows that Payers have performed well, on average, whether interest rates are high or low, and they actually have done better on a go-forward basis when the Fed Funds rate is above the current 5.0% level.

We also note, given concerns some have about equity valuations, that Value Stocks are today priced below their average since 1995, which is the date that numbers are available for the Russell 3000 Value and Growth indexes,

Valuations – Value Stocks are Attractive and We Like the Metrics for our Portfolios.

while we continue to sleep well at night with the reasonable valuations on our broadly diversified portfolios.

Wall of Worry – Stocks Have Overcome Plenty of Disconcerting News in the Fullness of Time

Equity investors have plenty about which to be concerned these days, which if we study market history is no different than usual, but stocks have long climbed a wall of worry.

Equity investors have plenty about which to be concerned these days, which if we study market history is no different than usual, but stocks have long climbed a wall of worry.

and the latest projections from the Federal Reserve call for real (inflation-adjusted) GDP to grow 0.4% this year and 1.2% in 2024.

and the latest projections from the Federal Reserve call for real (inflation-adjusted) GDP to grow 0.4% this year and 1.2% in 2024.

Recession? – Mixed Econ Numbers & Historical Equity Return Perspective

To be sure, the Bloomberg recession estimate now stands at 65%,

That sounds ominous, but we note that famed American Economist Paul Samuelson years ago joked, “Economists have predicted nine of the last five recessions,” and forecasting today remains as fraught with peril as ever. For example, we recently heard from two executives of prominent American financial institutions with conflicting views.

Bank of America (BAC – $29.87) CEO Brian Moynihan said inflation is showing signs of cooling, but the U.S. economy will still face a recession. Nevertheless, on BAC’s quarterly conference call, Mr. Moynihan hedged when he said, “Everything points to a relatively mild recession given the amount of stimulus that was paid to people and the money they have left over.”

On the other hand, BlackRock (BLK – $680.94) CEO Larry Fink cited stimulus from the Infrastructure Bill, the Chips and Science Act, and the Inflation Reduction Act as reason to think a U.S. recession won’t occur. In a television interview, Mr. Fink elaborated, “Those three bills are a trillion dollars of stimulus over the next few years. Think about how many jobs infrastructure creates. Think about the demand for commodities as we build infrastructure.”

Needless to say, the economic crystal ball is cloudy, with many investors likely sitting on the sidelines, even as crunching nearly a century of data on recessions and stock returns supports the view that the time in the market trumps market timing.

We might also point out that the first economic numbers for April from S&P Global showed stronger figures than expected on the outlook for the factory and services sectors, with both gauges hitting their highest levels in nearly a year,

and the labor picture remains remarkably robust, even as weekly initial filings for jobless benefits have ticked up from half-century lows.

Other economic data points out last week were mixed. On the positive side, the Empire State manufacturing index for April rocketed up more than 35 points to a much-stronger-than-expected of 10.8, a tally better than the average over the past two decades. Countering that bit of good news, the more-important Philadelphia Fed factory survey dropped 8 points to a worse-than-expected minus 31.3. Of course, the last two times that Philly Fed figure was lower was April 2020 and February 2009, both fantastic times for investors to be buying stocks.

Earnings – Healthy Corporate Profits in ’23 and ’24 Still the Projection

In addition, Q1 report cards from Corporate America generally have come in better-than-pessimistic forecasts thus far, with a greater-than-usual 75.9% of companies beating estimates on the bottom line. True, forward guidance has been guarded, as has been the case for quite some time, and analysts are often overly optimistic in their outlooks, but earnings are still expected to show solid growth this year and next.

We might argue that this is due to the fact that while many are fixated on real (inflation-adjusted) GDP numbers, sales and profits, as well as stock prices, are measured in nominal (actual) dollars. As the chart below illustrates, the long-term and near-term trends in nominal GDP growth have been higher.

Contrarian Sentiment – AAII Still Pessimistic

We continue to be braced for downside volatility (the equity futures are pointing to a poor start to the week) as it is a the price that investors must pay to achieve handsome long-term gains,

while the weight of the historical evidence shows that those who attempt to sidestep the trips south usually end up with lousy returns in the process.

With the latest measure of Main Street investor sentiment (the contrarian AAII Bull-Bear Survey showing 27.2% Bulls and 35.1% Bears) continuing to be skewed in favor of the pessimists.

and stocks in general remaining attractively valued,

we see no reason to alter our enthusiasm for the long-term prospects for equities.

Stock Market News: Updates on sixteen stocks across eight different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.