The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. This week, we discuss Stock Market Timing, the Shareholder letter from Jamie Dimon, AAII Market Sentiment, Valuations, Earnings and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades: 5 Buys for 3 Portfolios, 1 Buy Still Left to Do

Sentiment: AAII Bulls Jump and Bears Plunge

Market Timing: Only Problem is Getting the Timing Right

Fear Sells: Accentuating the Negative from the Jamie Dimon Shareholder Letter

Opportunities: Dimon Perspective & Historical Evidence

Economic News: Weaker Data; But Monthly Jobs Numbers Impress

Valuations: Still Liking the Metrics for our Portfolios

Earnings: Healthy Corporate Profits in ’23 and ’24 Still the Projection

Stock News: Update on the Energy sector

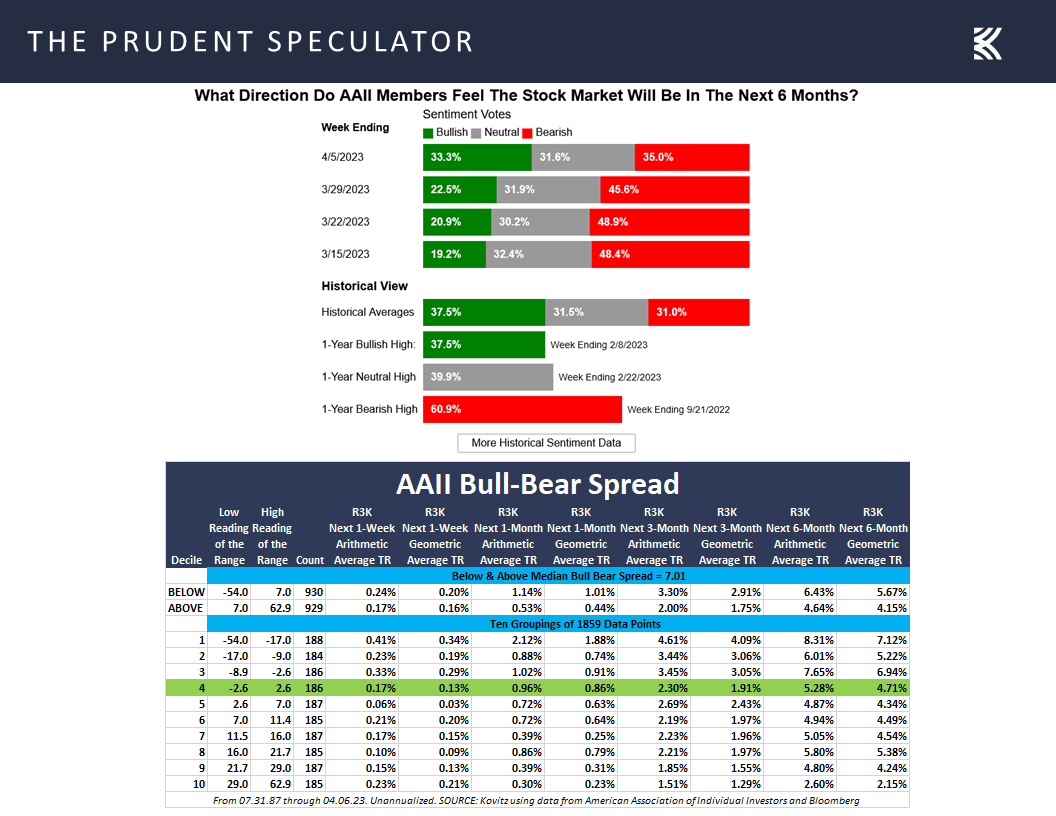

Sentiment – AAII Bulls Jump and Bears Plunge

Perhaps the pullback last week in which the average stock in the Russell 3000 index dropped 2.5% can be blamed on the good folks at the American Association of Individual Investors (AAII). After weeks of significant pessimism on the Sentiment gauge, the sizable equity-market rebound over the last week of March moved a significant number of AAII members out of their negativity. Indeed, the tally of Bears fell by 10.6 percentage points to 35.0% and the count of Bulls rose by 10.8 percentage points to 33.3%, with the Bull-Bear spread rising to -1.7% from -23.1% the week prior.

To be sure, the Bulls are still below the 37.5% average and the Bears are above the 31.0% average, but forward returns historically have been best when the AAII Bull-Bear Spread is tilted heavily toward fear and worst when greed is the dominant emotion. Indeed, investor sentiment is usually a contrarian measure as it is often far better to be greedy when others are fearful and fearful when others are greedy.

Market Timing – Only Problem is Getting the Timing Right

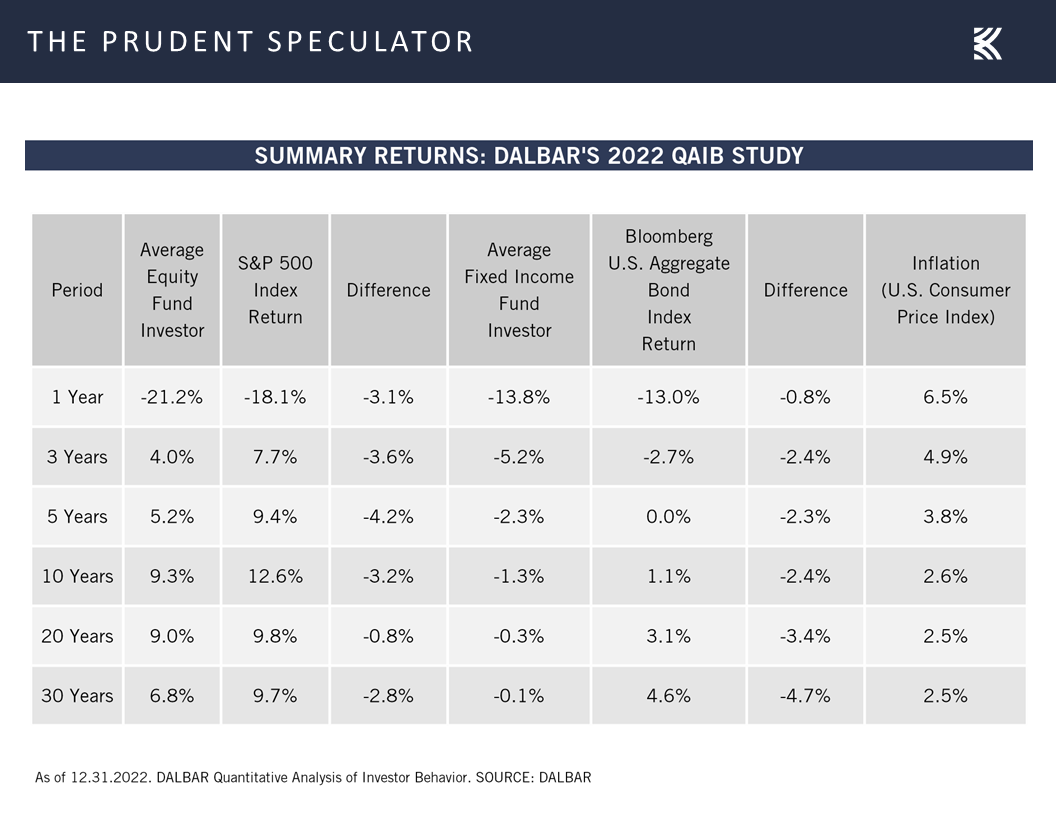

Of course, suppressing emotions is the hardest part of the investment process. Buying and selling is relatively easy – it is the holding that seems to cause the most problems. Unfortunately, far too many zig when they should have zagged, as the latest numbers on investor behavior from DALBAR vividly show that the only problem with market timing is getting the timing right. And, it is fascinating that bond-fund investors are even worse at remembering that time in the market trumps market timing!

Fear Sells – Accentuating the Negative from the Jamie Dimon Shareholder Letter

Of course, suppressing emotions is the hardest part of the investment process. Buying and selling is relatively easy – it is the holding that seems to cause the most problems. Unfortunately, far too many zig when they should have zagged, as the latest numbers on investor behavior from DALBAR vividly show that the only problem with market timing is getting the timing right. And, it is fascinating that bond-fund investors are even worse at remembering that time in the market trumps market timing!

Opportunities – Dimon Perspective & Historical Evidence

Alas, fear sells much better than greed and financial television, web sites and newspapers are in the business of attracting eyeballs, which often has little to do with helping those focused on multi-year time horizons achieve their long-term investment goals. A good example were headlines last week like, Jamie Dimon Says Effects of Banking Crisis Will Be Felt for “Years to Come” in conjunction with the release of the 2022 Annual Report letter from the JPMorgan Chase (JPM – $127.47) CEO.

Certainly, we do not mean to suggest that Mr. Dimon offered unicorns and rainbows as he wrote:

We are prepared for potentially higher interest rates, and we may have higher inflation for longer.

If we have higher inflation for longer, the Fed may be forced to increase rates higher than people expect despite the recent bank crisis. Also, QT may have ongoing impacts that might, over time, be another force, pushing longer-term rates higher than currently envisioned. This may occur even if we have a mild – or not-so-mild – recession, as we saw in the 1970s and 1980s.

Today’s inverted yield curve implies that we are going into a recession. As someone once said, an inverted yield curve like this is “eight for eight” in predicting a recession in the next 12 months. However, it may not be true this time because of the enormous effect of QT. As previously stated, longer-term rates are not necessarily controlled by central banks, and it is possible that the inversion we see today is still driven by prior QE and not the dramatic change in supply and demand that is going to take place in the future.

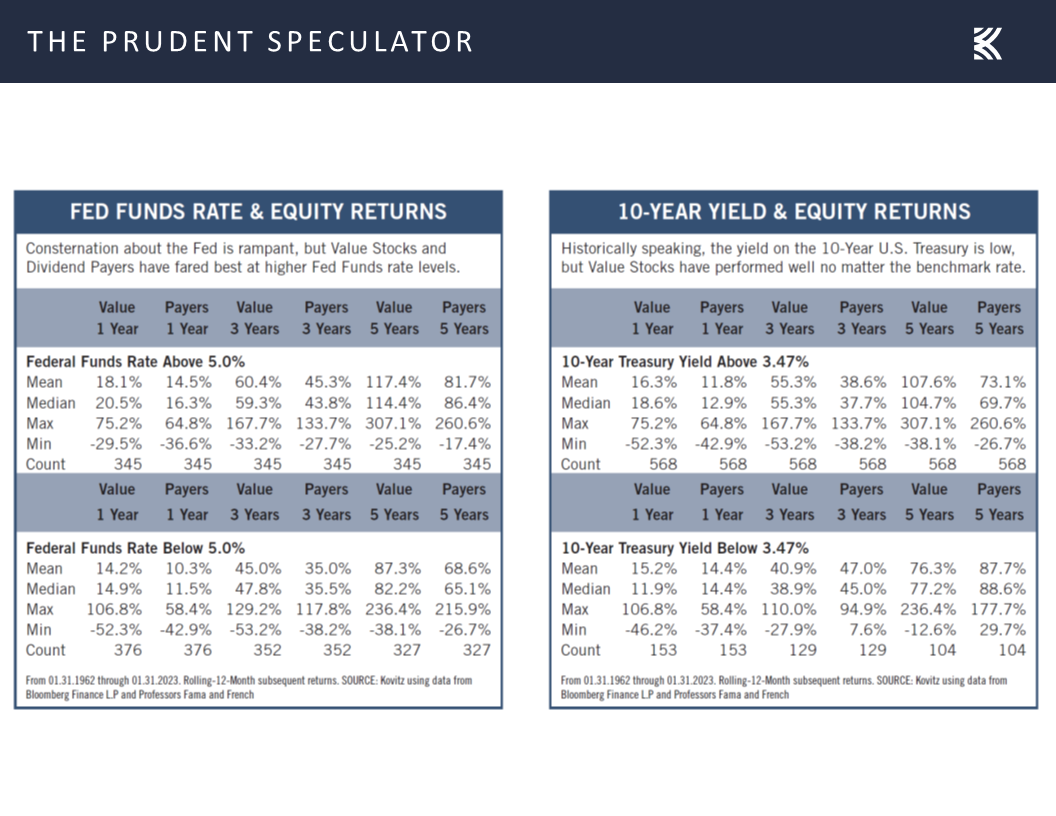

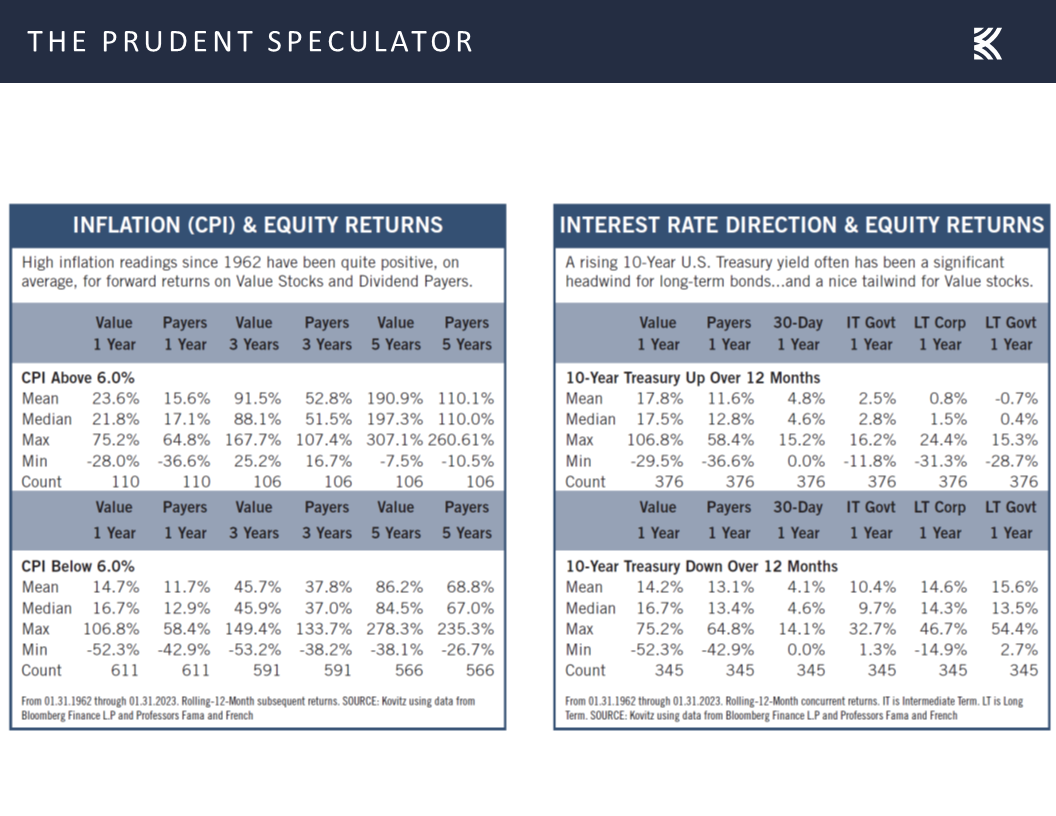

However, there was little mention in the press that, historically speaking, Value Stocks and Dividend Payers, like those that we have long championed, have performed well no matter where the Fed Funds rate and benchmark 10-Year Treasury yield reside.

The same can be said for inflation levels and when interest rates are moving higher or lower. Believe it or not, Value Stocks have performed very well, on average, over the ensuing one, three and five years when the consumer price index is at the current 6.0% level or higher, while the only thing that can be said with certainty when interest rates are rising is that long-term bonds do not perform well.

The same can be said for inflation levels and when interest rates are moving higher or lower. Believe it or not, Value Stocks have performed very well, on average, over the ensuing one, three and five years when the consumer price index is at the current 6.0% level or higher, while the only thing that can be said with certainty when interest rates are rising is that long-term bonds do not perform well.

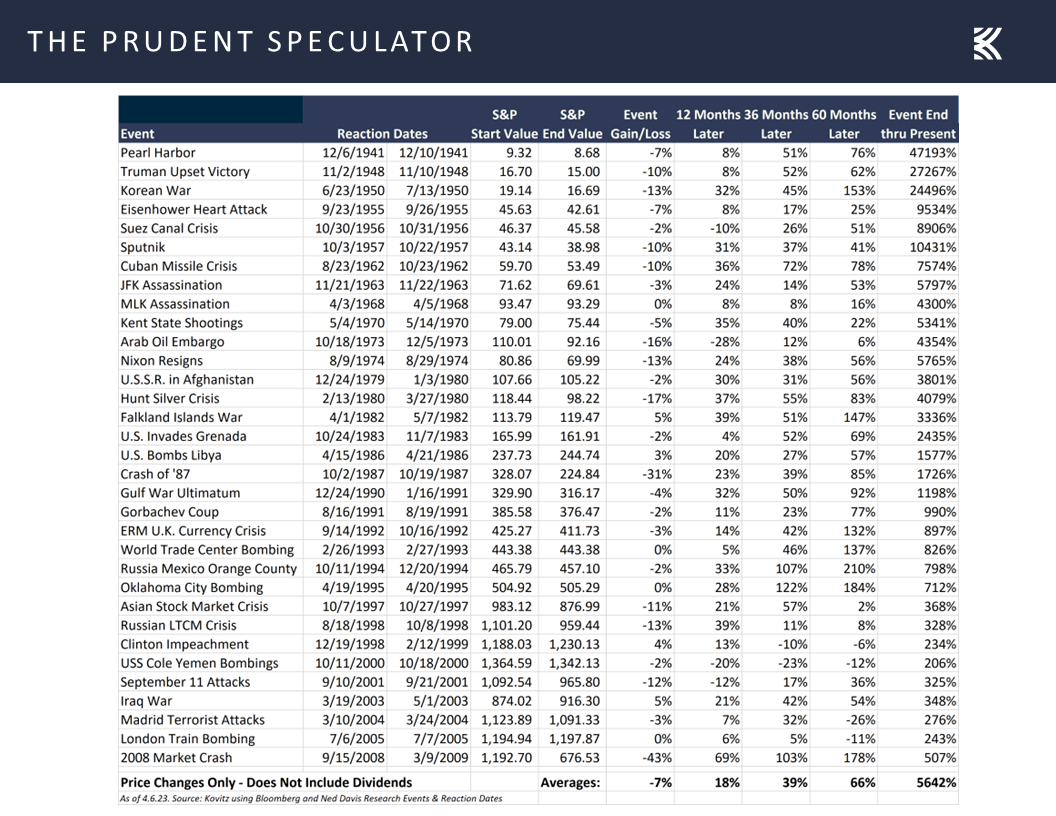

We realize that past performance is never a guarantee of future results, but we think the plunge in the prices of many stocks over the last year or so discounts a significant amount of bad news that may or may not materialize.

We realize that past performance is never a guarantee of future results, but we think the plunge in the prices of many stocks over the last year or so discounts a significant amount of bad news that may or may not materialize.

Further, as Mr. Dimon stated, “While focusing on the risks, it’s also important not to forget the opportunities. The transition to a green economy will eventually require $4 trillion a year in capital expenditures. The IRA, CHIPS Act and Bipartisan Infrastructure Law combined will create huge opportunities for companies, investors and entrepreneurs across virtually every industry group in the United States. You can rest assured that our company is organizing to help clients make the most of these opportunities.”

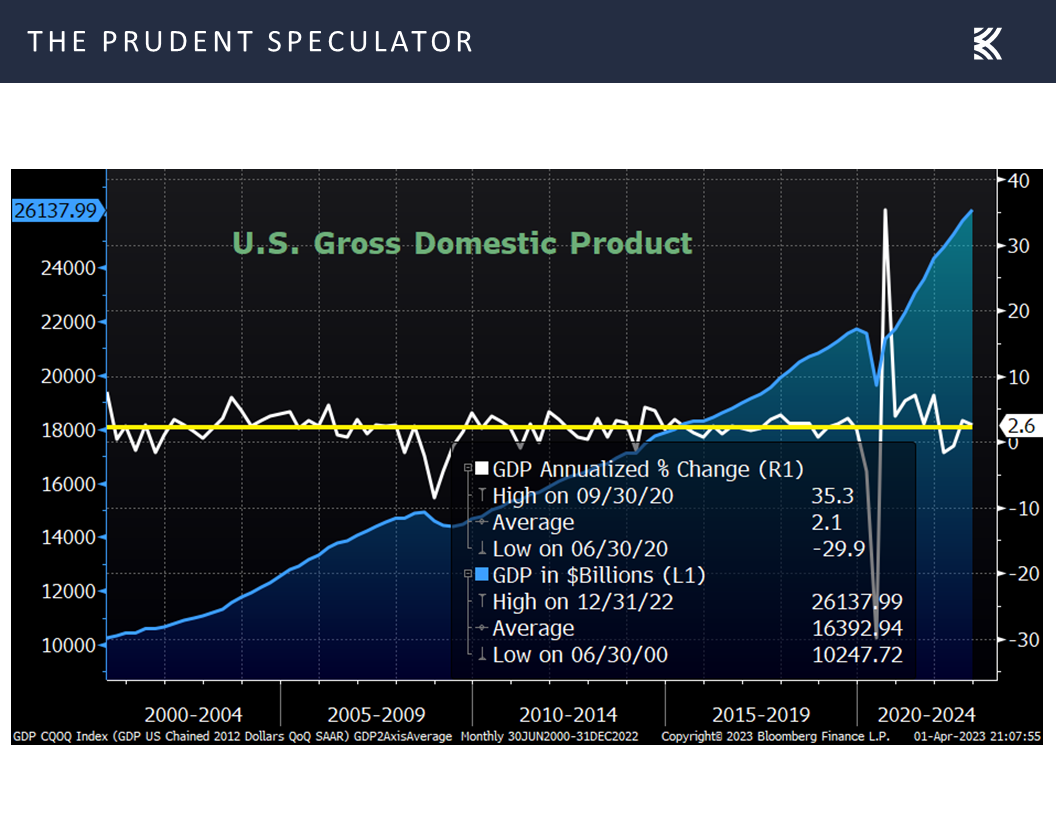

He concluded, “Finally, when one talks about risk for too long, it begins to cloud your judgment. Looking ahead, the positives are huge. However events play out, it is likely that 20 years from now, America’s GDP will be more than twice the size it is today, and hundreds of millions of people around the world will have been lifted out of poverty.”

Economic News – Weaker Data; But Monthly Jobs Numbers Impress

While the long-term trend in GDP growth is significantly higher, we realize that short-term equity market movements will be heavily influenced by the constant stream of economic statistics. Last week’s figures generally were pointing to a weaker near-term economic outlook as the number of job openings in February came in lower than expected, while the count of first-time filings for unemployment benefits in the most recent week hit 228,000, above levels we had been seeing in prior weeks.

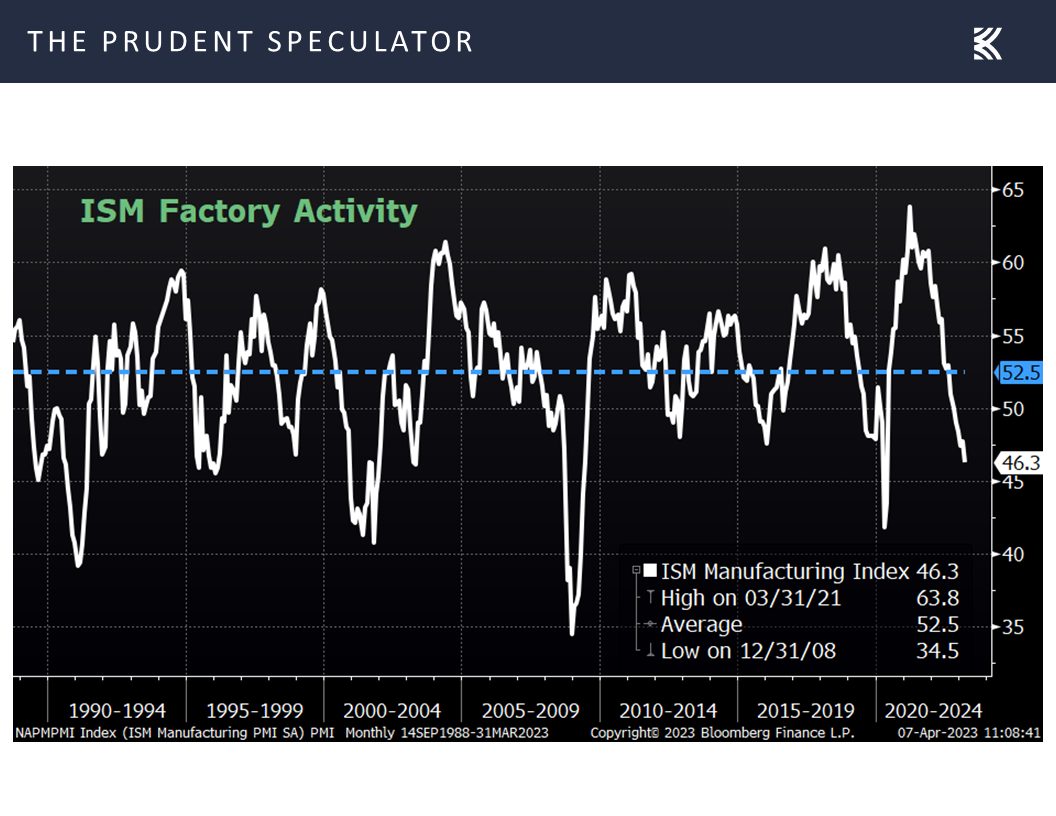

In addition, the important March read on the health of the factory sector from the Institute of Supply Management (ISM) was weaker than expected at 46.3, down from 47.7 in February. ISM stated, “The past relationship between the Manufacturing PMI® and the overall economy indicates that the March reading (46.3 percent) corresponds to a change of minus-0.9 percent in real gross domestic product (GDP) on an annualized basis.”

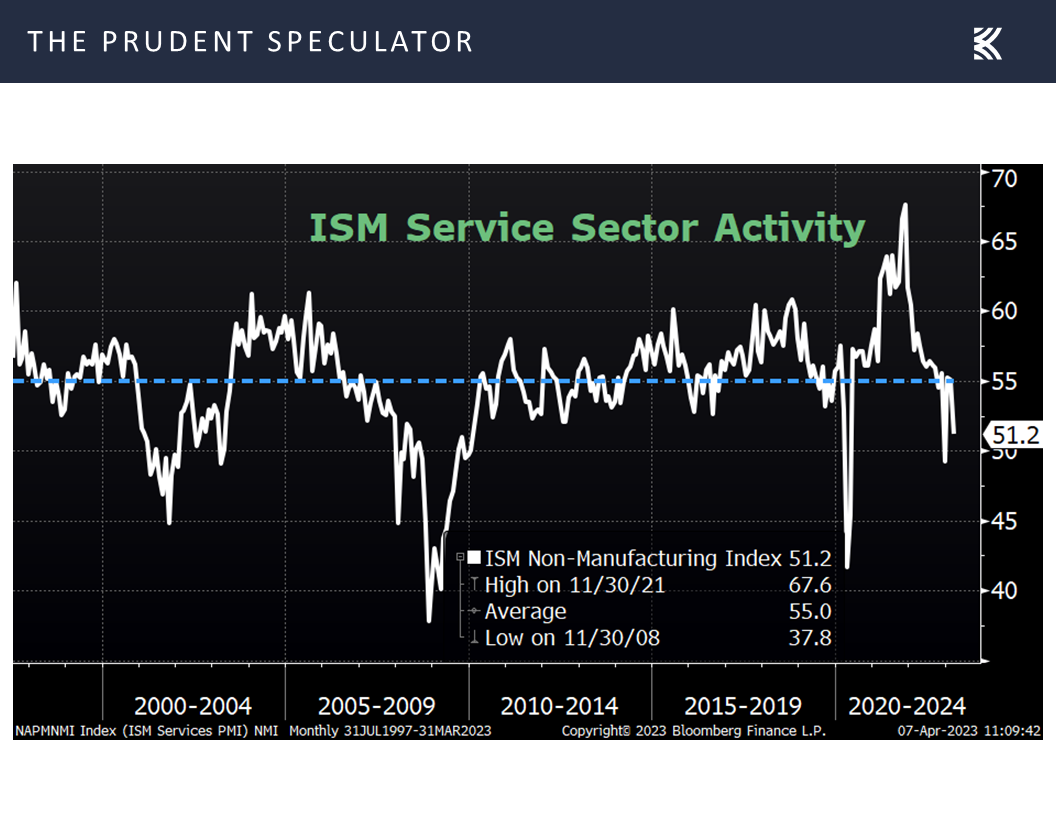

The ISM gauge on the health of the even-more-important services sector also was below projections, falling to 51.2 in March, down from 55.1 the month prior. Of course, ISM said, “The past relationship between the Services PMI® and the overall economy indicates that the Services PMI® for March (51.2 percent) corresponds to a 0.5-percent increase in real gross domestic product (GDP) on an annualized basis.”

The ISM gauge on the health of the even-more-important services sector also was below projections, falling to 51.2 in March, down from 55.1 the month prior. Of course, ISM said, “The past relationship between the Services PMI® and the overall economy indicates that the Services PMI® for March (51.2 percent) corresponds to a 0.5-percent increase in real gross domestic product (GDP) on an annualized basis.”

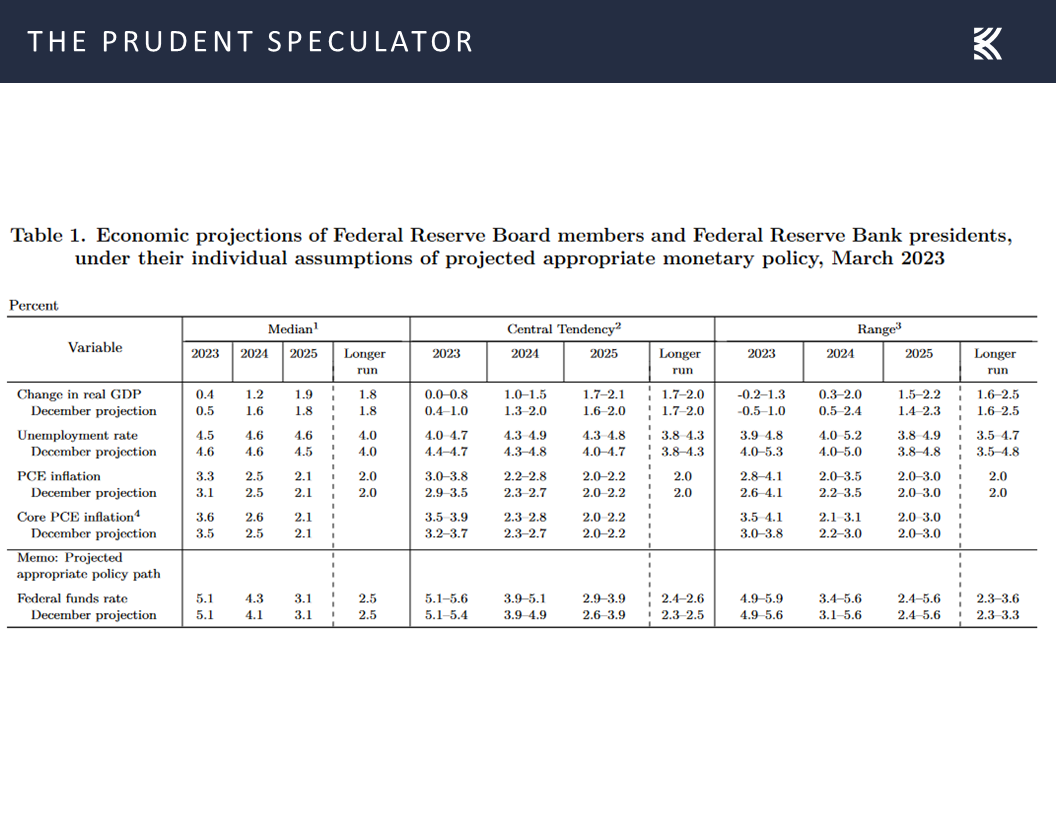

Interestingly, that 0.5% increase in GDP is in line with the most recent full-year 2023 U.S. growth projection from the Federal Reserve,

Interestingly, that 0.5% increase in GDP is in line with the most recent full-year 2023 U.S. growth projection from the Federal Reserve,

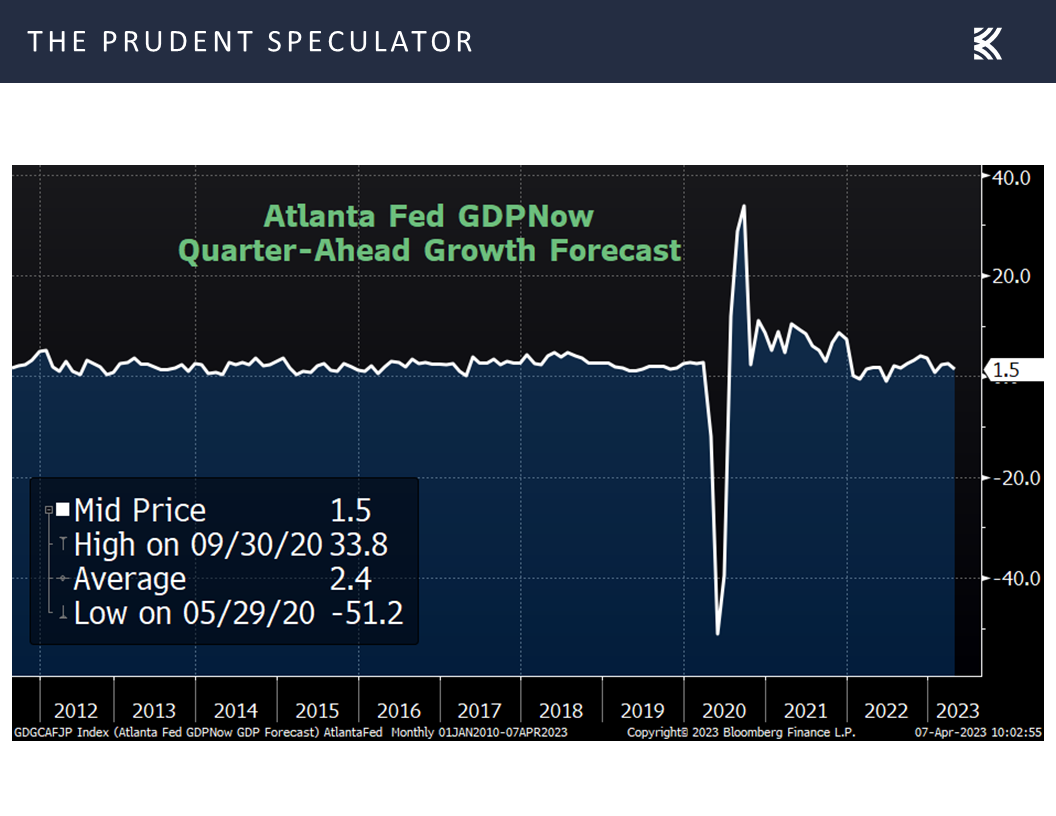

while the current estimate for Q1 GDP growth from the Atlanta Fed is 1.5%.

while the current estimate for Q1 GDP growth from the Atlanta Fed is 1.5%.

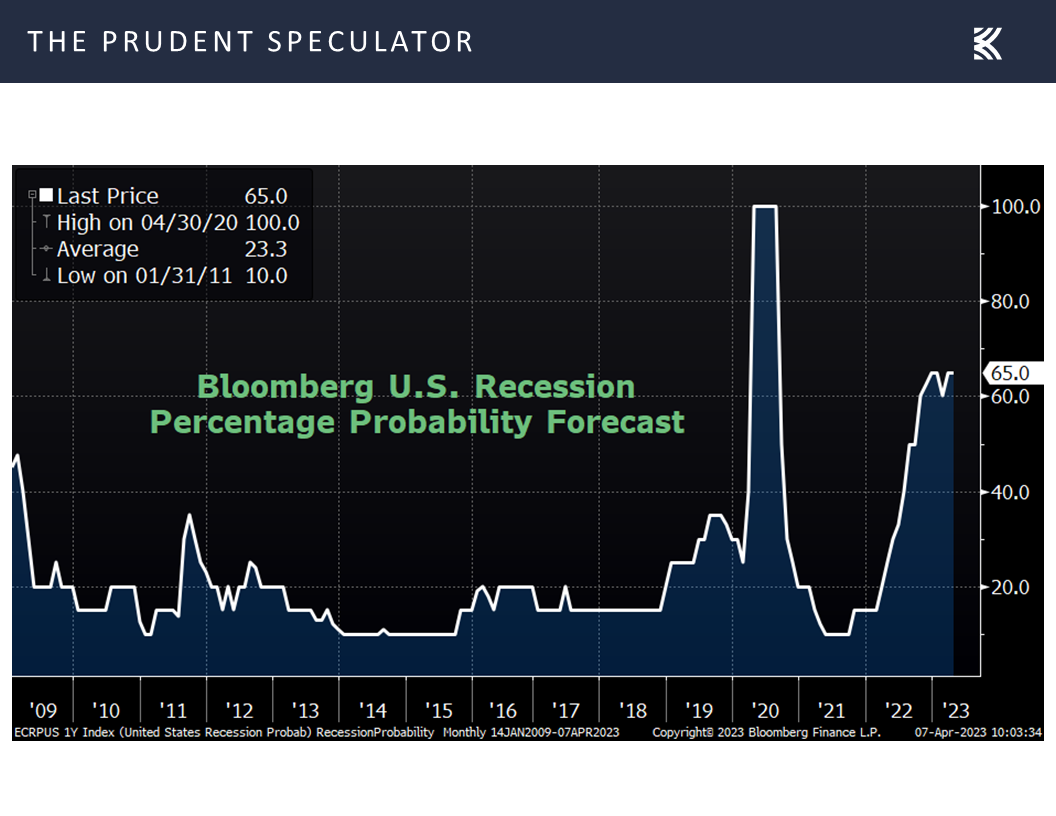

Those positive GDP figures would seem to be optimistic, if the latest calculation from Bloomberg of a 65% probability of a recession in the next 12 months is to believed,

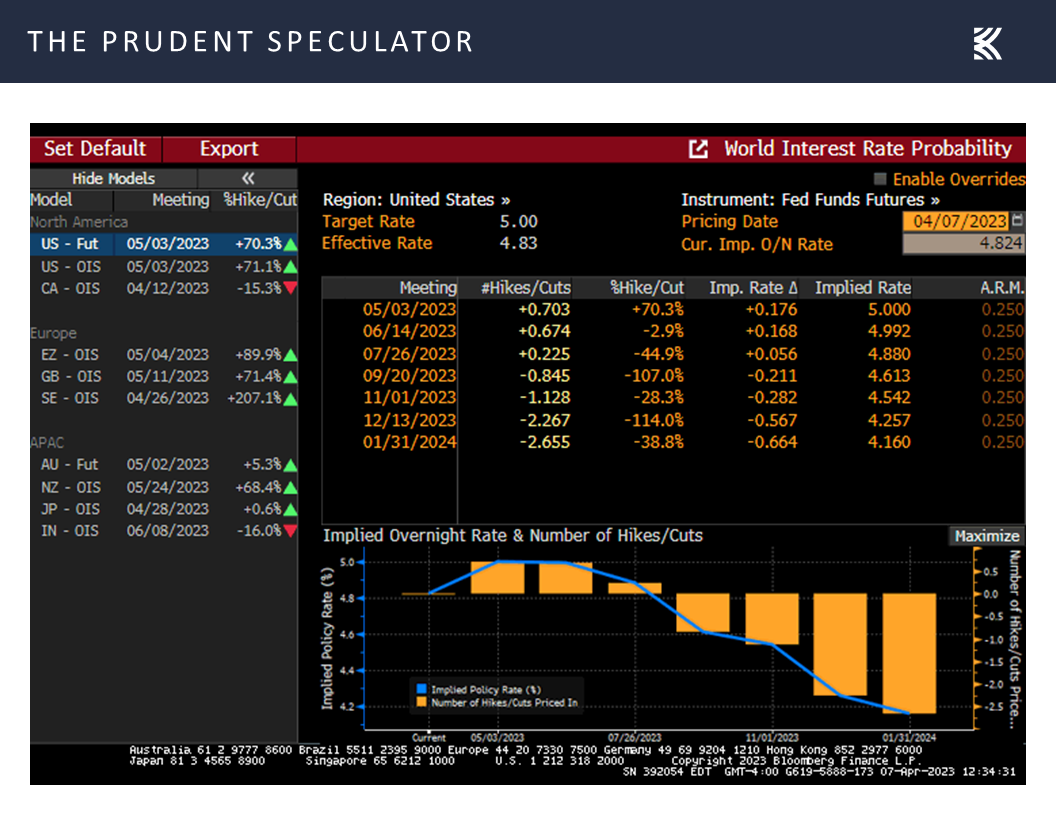

while the Fed Funds futures market is projecting a much-less-hawkish Federal Reserve going forward, given a current view of a 4.26% year-end rate, down from the current target rate of 5.0%.

while the Fed Funds futures market is projecting a much-less-hawkish Federal Reserve going forward, given a current view of a 4.26% year-end rate, down from the current target rate of 5.0%.

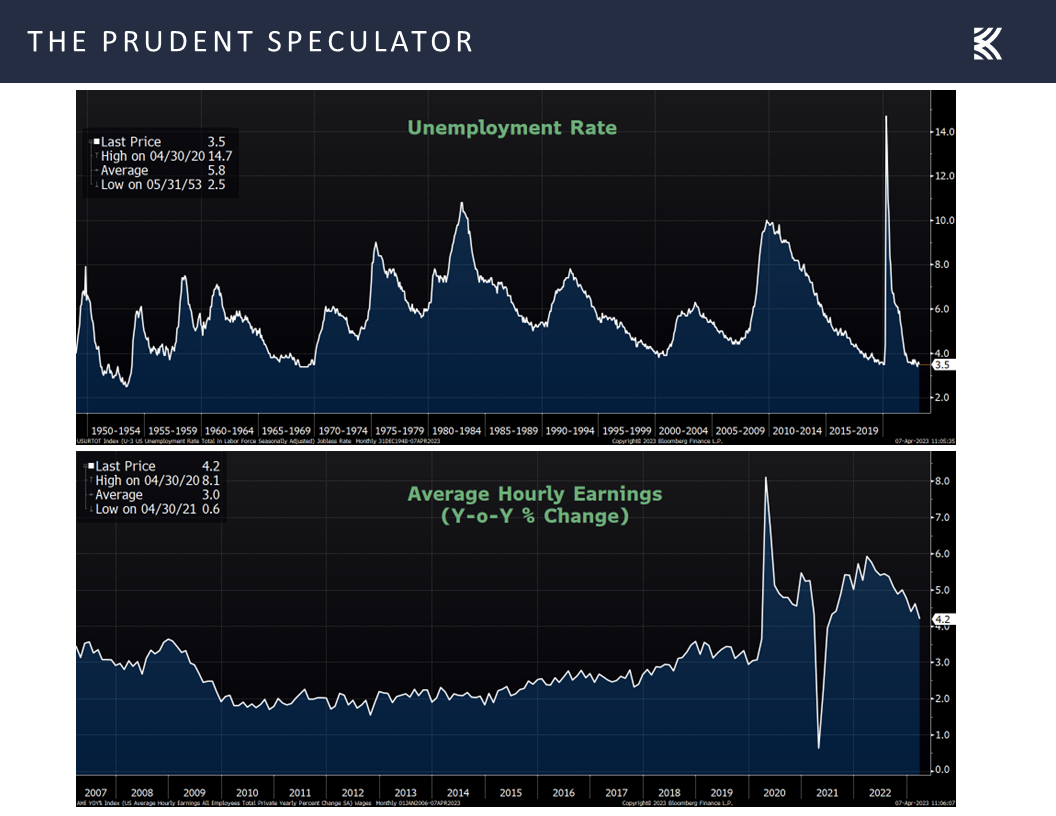

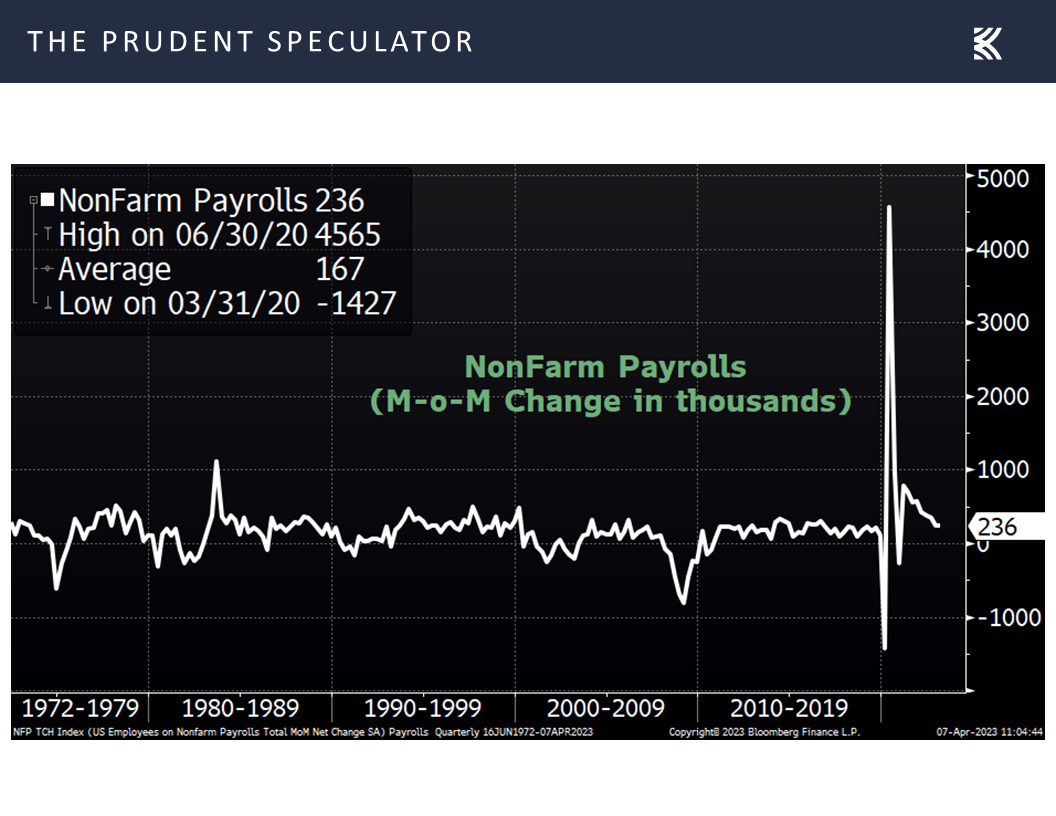

Lest anyone think the economy is falling off a cliff, Friday’s jobs report was of the Goldilocks variety (not-too-hot and not-too-cold) as a solid and roughly in-line-with-estimates 236,000 new payrolls were created,

while the unemployment rate edged down to 3.5%, but average hourly earnings rose “only” 4.2% on a year-over-year basis, with wage pressures falling to a nearly two-year low and dropping from 4.6% in February.

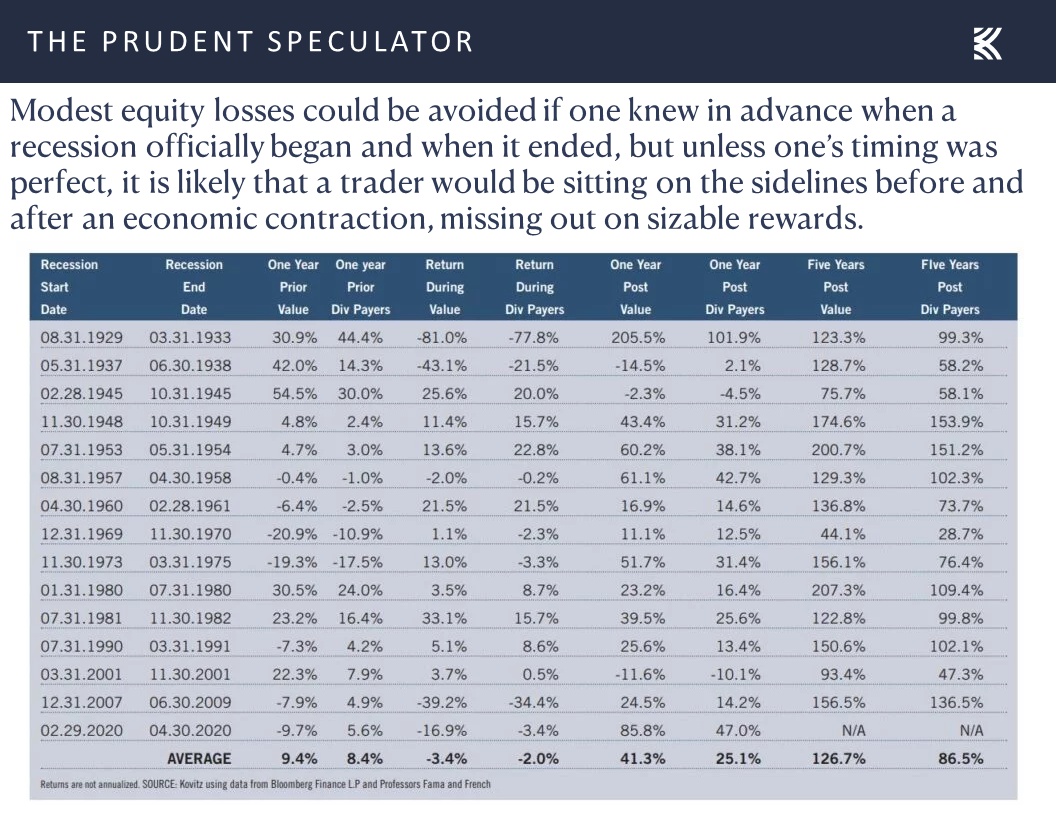

Obviously, the economic crystal ball is cloudy, and there very well could be a recession in the cards. So, in the April edition of The Prudent Speculator, we looked at all of the National Bureau of Economic Research’s (NBER) declared recessions since 1929 and calculated returns for Value Stocks and Dividend Payers preceding, during and following each economic contraction.

Equity returns in the lead-up to the recessions are generally good (averaging 9%) and we think one wouldn’t want to miss out on those gains. Not owning stocks during recessions would spare modest losses, but the NBER doesn’t determine recessions in real time, meaning the recording lag significantly complicates timing this type of trade. And, the performance numbers have been stellar, on average, coming out of recessions!

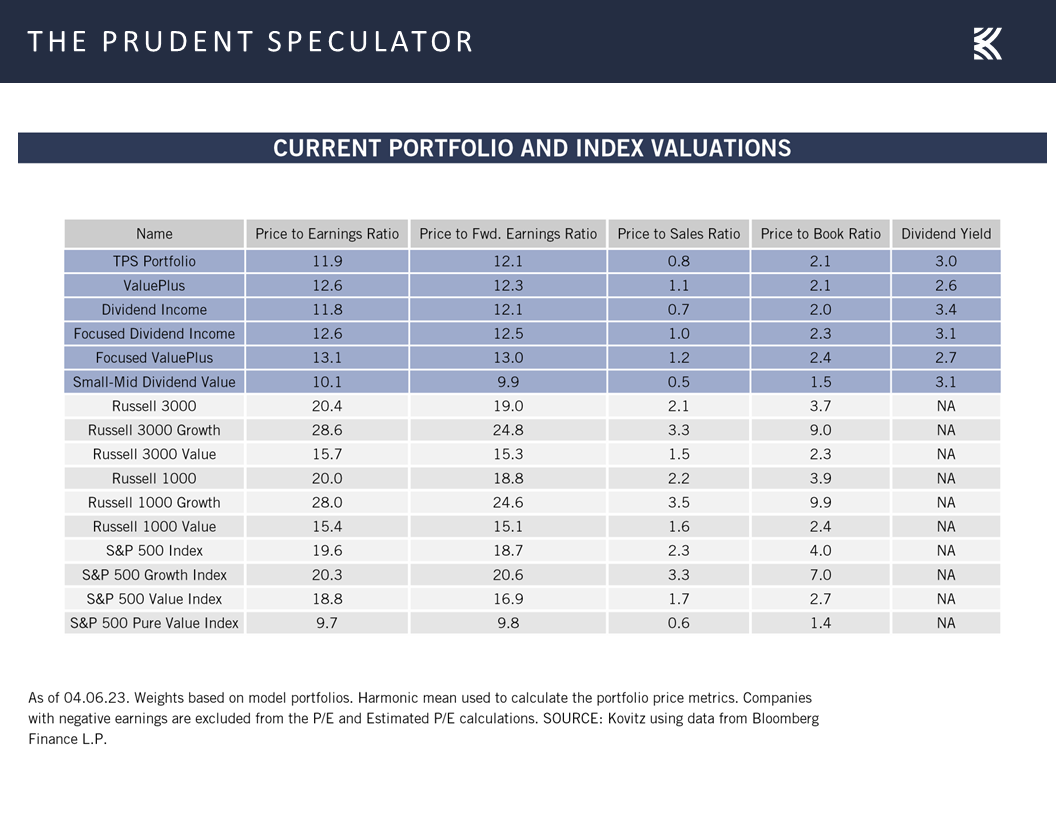

Valuations: Still Liking the Metrics for our Portfolios

Not surprisingly, though we always are braced for near-term downside volatility, we see little reason to alter our enthusiasm for the long-term prospects of our broadly diversified portfolios of what we believe to be undervalued stocks,

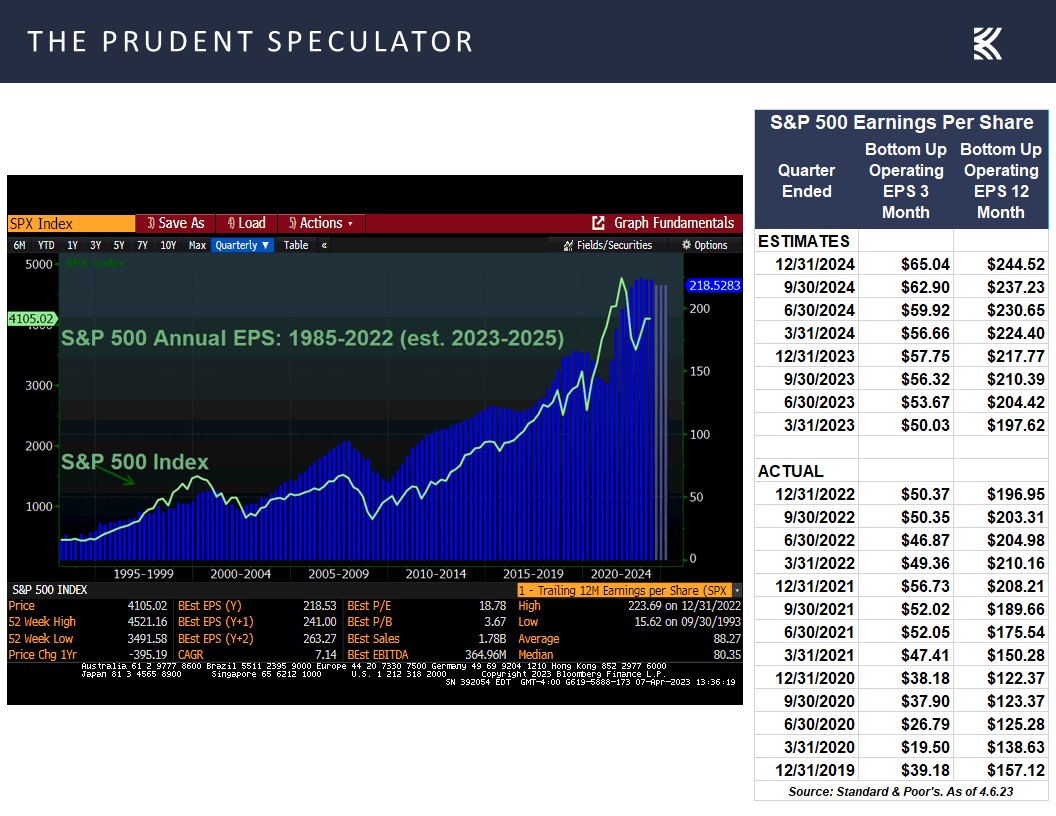

Earnings: Solid Growth This Year and Next Still the Forecast

Especially as corporate profits still are expected to remain healthy even with the economic headwinds.

Stock Market News: Updates on five stocks across

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Stock Market Timing, Jamie Dimon’s Shareholder Letter and Historical Evidence for Equity Returns

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. This week, we discuss Stock Market Timing, the Shareholder letter from Jamie Dimon, AAII Market Sentiment, Valuations, Earnings and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades: 5 Buys for 3 Portfolios, 1 Buy Still Left to Do

Sentiment: AAII Bulls Jump and Bears Plunge

Market Timing: Only Problem is Getting the Timing Right

Fear Sells: Accentuating the Negative from the Jamie Dimon Shareholder Letter

Opportunities: Dimon Perspective & Historical Evidence

Economic News: Weaker Data; But Monthly Jobs Numbers Impress

Valuations: Still Liking the Metrics for our Portfolios

Earnings: Healthy Corporate Profits in ’23 and ’24 Still the Projection

Stock News: Update on the Energy sector

Sentiment – AAII Bulls Jump and Bears Plunge

Perhaps the pullback last week in which the average stock in the Russell 3000 index dropped 2.5% can be blamed on the good folks at the American Association of Individual Investors (AAII). After weeks of significant pessimism on the Sentiment gauge, the sizable equity-market rebound over the last week of March moved a significant number of AAII members out of their negativity. Indeed, the tally of Bears fell by 10.6 percentage points to 35.0% and the count of Bulls rose by 10.8 percentage points to 33.3%, with the Bull-Bear spread rising to -1.7% from -23.1% the week prior.

To be sure, the Bulls are still below the 37.5% average and the Bears are above the 31.0% average, but forward returns historically have been best when the AAII Bull-Bear Spread is tilted heavily toward fear and worst when greed is the dominant emotion. Indeed, investor sentiment is usually a contrarian measure as it is often far better to be greedy when others are fearful and fearful when others are greedy.

Market Timing – Only Problem is Getting the Timing Right

Of course, suppressing emotions is the hardest part of the investment process. Buying and selling is relatively easy – it is the holding that seems to cause the most problems. Unfortunately, far too many zig when they should have zagged, as the latest numbers on investor behavior from DALBAR vividly show that the only problem with market timing is getting the timing right. And, it is fascinating that bond-fund investors are even worse at remembering that time in the market trumps market timing!

Fear Sells – Accentuating the Negative from the Jamie Dimon Shareholder Letter

Of course, suppressing emotions is the hardest part of the investment process. Buying and selling is relatively easy – it is the holding that seems to cause the most problems. Unfortunately, far too many zig when they should have zagged, as the latest numbers on investor behavior from DALBAR vividly show that the only problem with market timing is getting the timing right. And, it is fascinating that bond-fund investors are even worse at remembering that time in the market trumps market timing!

Opportunities – Dimon Perspective & Historical Evidence

Alas, fear sells much better than greed and financial television, web sites and newspapers are in the business of attracting eyeballs, which often has little to do with helping those focused on multi-year time horizons achieve their long-term investment goals. A good example were headlines last week like, Jamie Dimon Says Effects of Banking Crisis Will Be Felt for “Years to Come” in conjunction with the release of the 2022 Annual Report letter from the JPMorgan Chase (JPM – $127.47) CEO.

Certainly, we do not mean to suggest that Mr. Dimon offered unicorns and rainbows as he wrote:

We are prepared for potentially higher interest rates, and we may have higher inflation for longer.

If we have higher inflation for longer, the Fed may be forced to increase rates higher than people expect despite the recent bank crisis. Also, QT may have ongoing impacts that might, over time, be another force, pushing longer-term rates higher than currently envisioned. This may occur even if we have a mild – or not-so-mild – recession, as we saw in the 1970s and 1980s.

Today’s inverted yield curve implies that we are going into a recession. As someone once said, an inverted yield curve like this is “eight for eight” in predicting a recession in the next 12 months. However, it may not be true this time because of the enormous effect of QT. As previously stated, longer-term rates are not necessarily controlled by central banks, and it is possible that the inversion we see today is still driven by prior QE and not the dramatic change in supply and demand that is going to take place in the future.

However, there was little mention in the press that, historically speaking, Value Stocks and Dividend Payers, like those that we have long championed, have performed well no matter where the Fed Funds rate and benchmark 10-Year Treasury yield reside.

Further, as Mr. Dimon stated, “While focusing on the risks, it’s also important not to forget the opportunities. The transition to a green economy will eventually require $4 trillion a year in capital expenditures. The IRA, CHIPS Act and Bipartisan Infrastructure Law combined will create huge opportunities for companies, investors and entrepreneurs across virtually every industry group in the United States. You can rest assured that our company is organizing to help clients make the most of these opportunities.”

He concluded, “Finally, when one talks about risk for too long, it begins to cloud your judgment. Looking ahead, the positives are huge. However events play out, it is likely that 20 years from now, America’s GDP will be more than twice the size it is today, and hundreds of millions of people around the world will have been lifted out of poverty.”

Economic News – Weaker Data; But Monthly Jobs Numbers Impress

While the long-term trend in GDP growth is significantly higher, we realize that short-term equity market movements will be heavily influenced by the constant stream of economic statistics. Last week’s figures generally were pointing to a weaker near-term economic outlook as the number of job openings in February came in lower than expected, while the count of first-time filings for unemployment benefits in the most recent week hit 228,000, above levels we had been seeing in prior weeks.

In addition, the important March read on the health of the factory sector from the Institute of Supply Management (ISM) was weaker than expected at 46.3, down from 47.7 in February. ISM stated, “The past relationship between the Manufacturing PMI® and the overall economy indicates that the March reading (46.3 percent) corresponds to a change of minus-0.9 percent in real gross domestic product (GDP) on an annualized basis.”

Those positive GDP figures would seem to be optimistic, if the latest calculation from Bloomberg of a 65% probability of a recession in the next 12 months is to believed,

Lest anyone think the economy is falling off a cliff, Friday’s jobs report was of the Goldilocks variety (not-too-hot and not-too-cold) as a solid and roughly in-line-with-estimates 236,000 new payrolls were created,

while the unemployment rate edged down to 3.5%, but average hourly earnings rose “only” 4.2% on a year-over-year basis, with wage pressures falling to a nearly two-year low and dropping from 4.6% in February.

Obviously, the economic crystal ball is cloudy, and there very well could be a recession in the cards. So, in the April edition of The Prudent Speculator, we looked at all of the National Bureau of Economic Research’s (NBER) declared recessions since 1929 and calculated returns for Value Stocks and Dividend Payers preceding, during and following each economic contraction.

Equity returns in the lead-up to the recessions are generally good (averaging 9%) and we think one wouldn’t want to miss out on those gains. Not owning stocks during recessions would spare modest losses, but the NBER doesn’t determine recessions in real time, meaning the recording lag significantly complicates timing this type of trade. And, the performance numbers have been stellar, on average, coming out of recessions!

Valuations: Still Liking the Metrics for our Portfolios

Not surprisingly, though we always are braced for near-term downside volatility, we see little reason to alter our enthusiasm for the long-term prospects of our broadly diversified portfolios of what we believe to be undervalued stocks,

Earnings: Solid Growth This Year and Next Still the Forecast

Especially as corporate profits still are expected to remain healthy even with the economic headwinds.

Stock Market News: Updates on five stocks across

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.