The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss stocks, inflation, interest rates, volatility, valuations and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Forbes Cruise – Buckingham in Spain

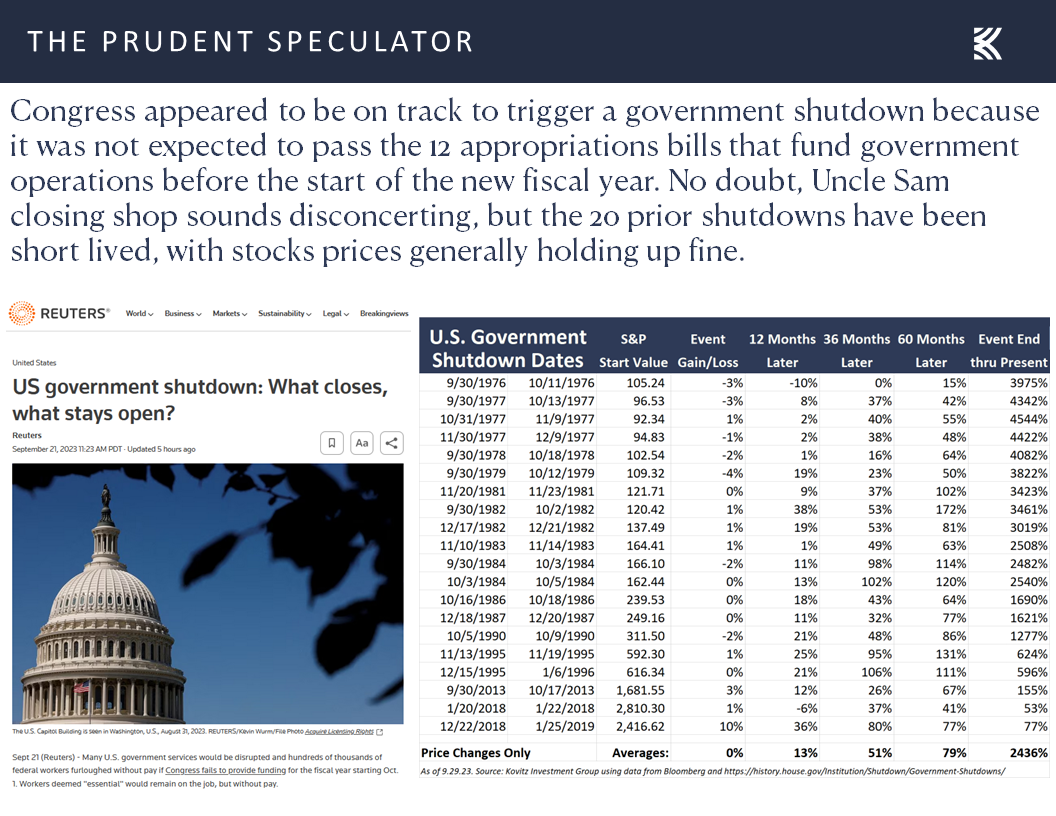

Week in Review – Late Decline Sends Stocks Down Again; Government Shutdowns Historically a Reason to Buy Stocks

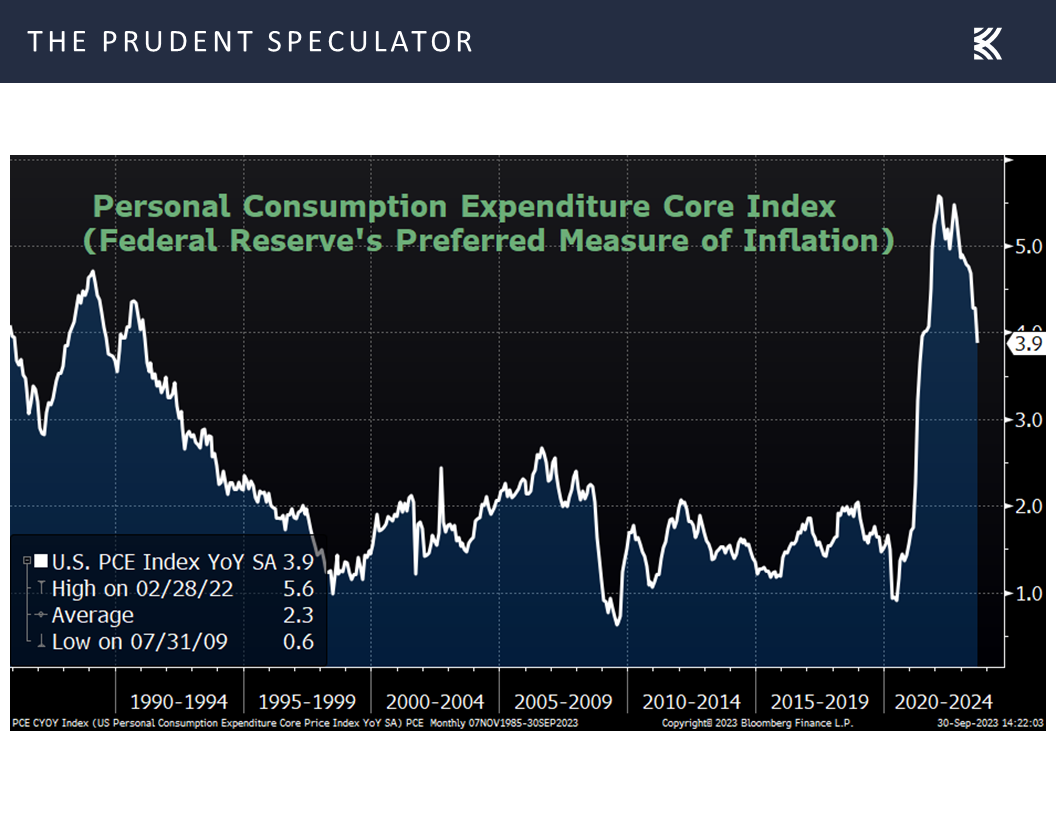

Inflation – Core PCE Rises Less than Expected

Econ News – Mixed Set of Numbers Last Week; Recession Odds Decrease; Strong Q3 Growth Still the Forecast

Interest Rates & Stocks – Rising 10-Year No Reason to Dump Equities

Valuations – Liking the Metrics Associated with our Portfolios

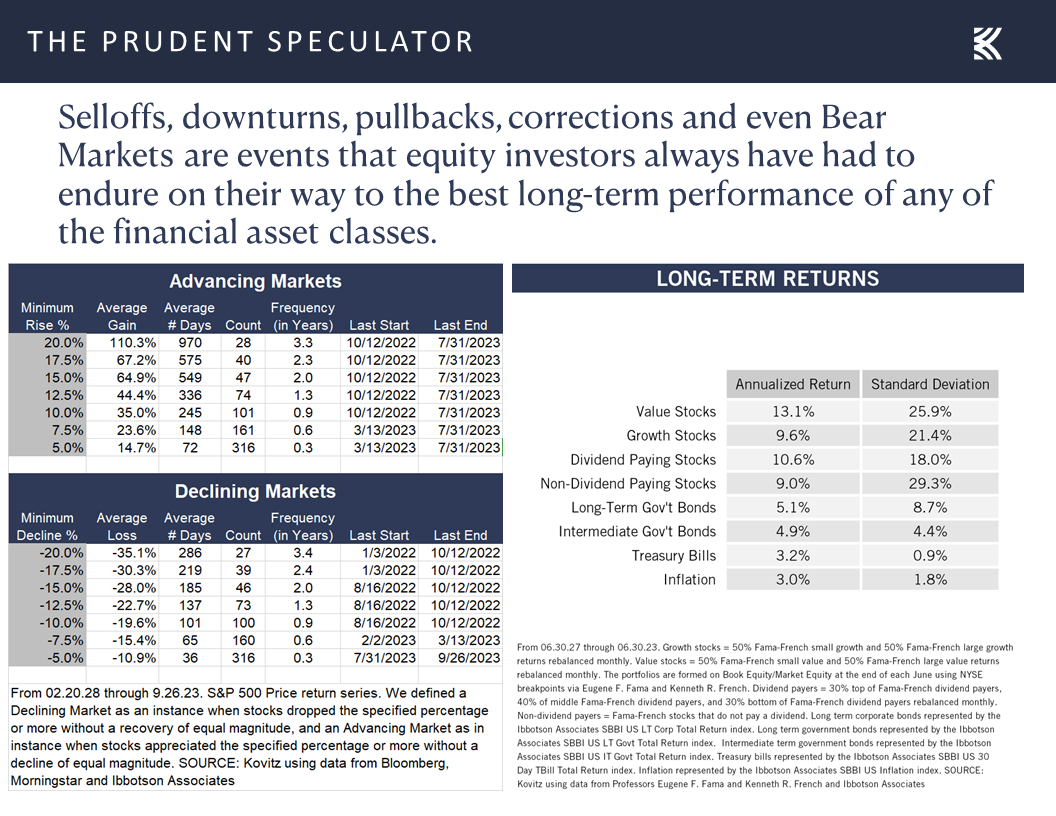

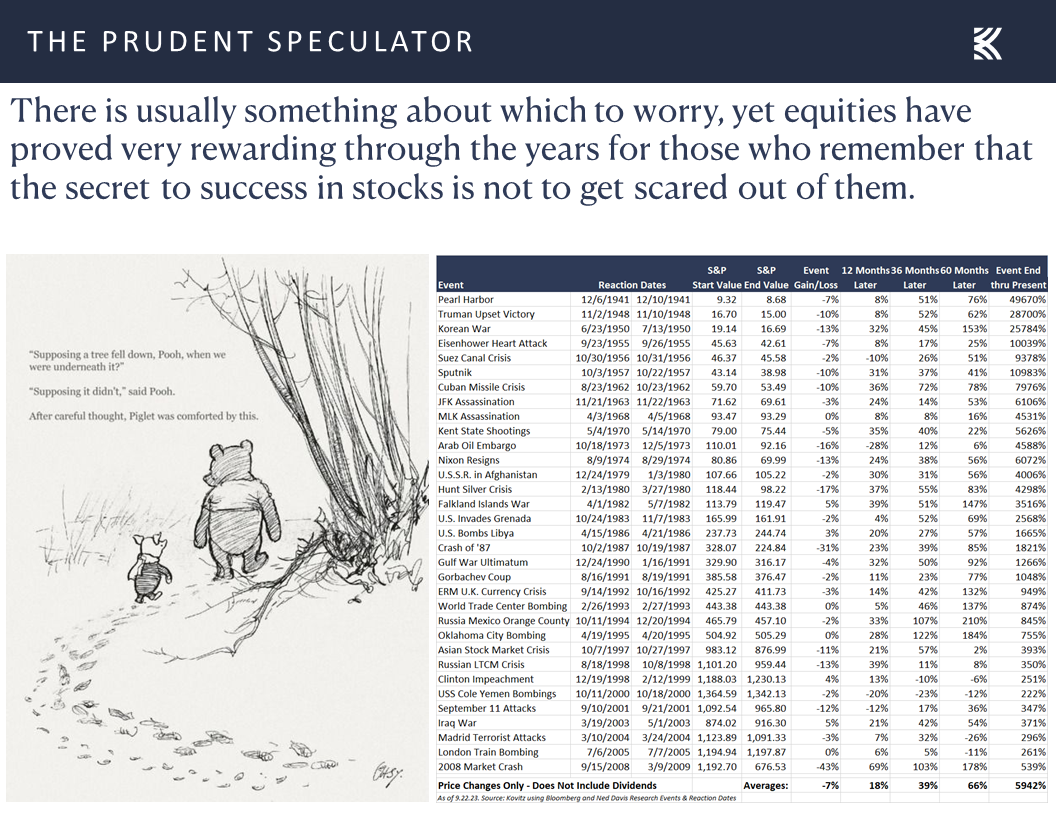

Volatility – Pullbacks are Normal; Stocks Have Provided Handsome Long-Term Rewards

Stock News – Updates on MU & JBL

Forbes Cruise – Buckingham in Spain

Greetings from Cadiz, Spain, where the 40th Forbes Cruise for Investors is now in full swing having set sail from Lisbon, Portugal on Friday evening. Your Editor speaks to the Forbes throng on October 5 and thus far it does not look like any changes are needed to the presentation prepared last weekend.

Week in Review – Late Decline Sends Stocks Down Again; Government Shutdowns Historically a Reason to Buy Stocks

True, stocks endured a volatile trading week, ending with modest losses for the full five trading sessions. It appeared that there might have been green ink for the week, were it not for a late-day selloff on Friday, evidently after worries accelerated about a government shutdown. Of course, if market history is a guide, said concerns seem misplaced, given that such events have been short-lived (a shutdown was averted over the weekend, for 45 days at least) and forward returns one-year hence actually have been better than the norm!

Of course, September lived down to its reputation for red ink since your Editor arrived at The Prudent Speculator more than 36 years ago,

Inflation – Core PCE Rises Less than Expected

but we might have argued that economic news out last week would have led to a rebound in stocks, given that the Federal Reserve’s preferred measure of inflation, the core personal consumption expenditures (PCE) gauge, which excludes volatile food and energy prices, rose a weaker-than-expected 0.1% in August compared to July, with the year-over-year measure holding steady at 3.9%.

Yes, the full PCE jumped 0.4% in August, due to higher energy prices, with the overall rate of annualized inflation rising to 3.5% from 3.4%, but the Fed Funds futures market decided that the probabilities of additional rate hikes from Jerome H. Powell & Co. were slightly lower at the end of this week than they were at the end of the week prior.

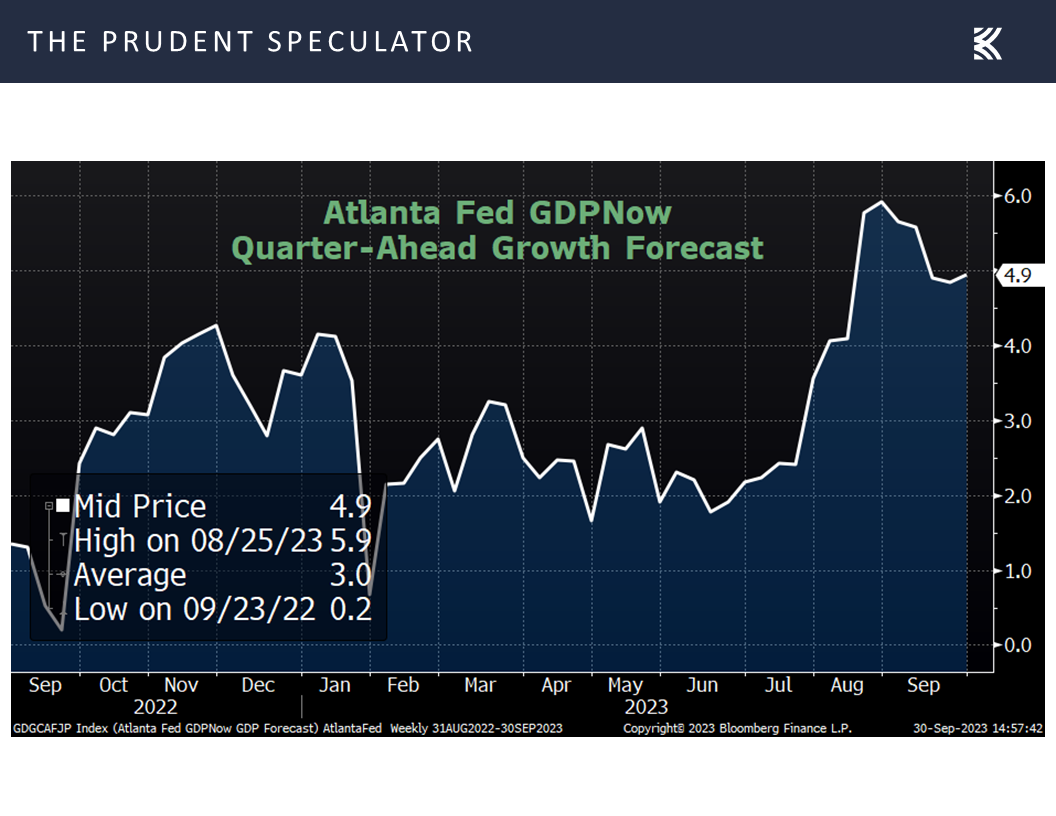

On the growth side of the economic equation, the outlook for Q3 GDP, per calculations from the Atlanta Fed, remained at a very robust real (inflation-adjusted) expansion of 4.9%,

Econ News – Mixed Set of Numbers Last Week; Recession Odds Decrease; Strong Q3 Growth Still the Forecast

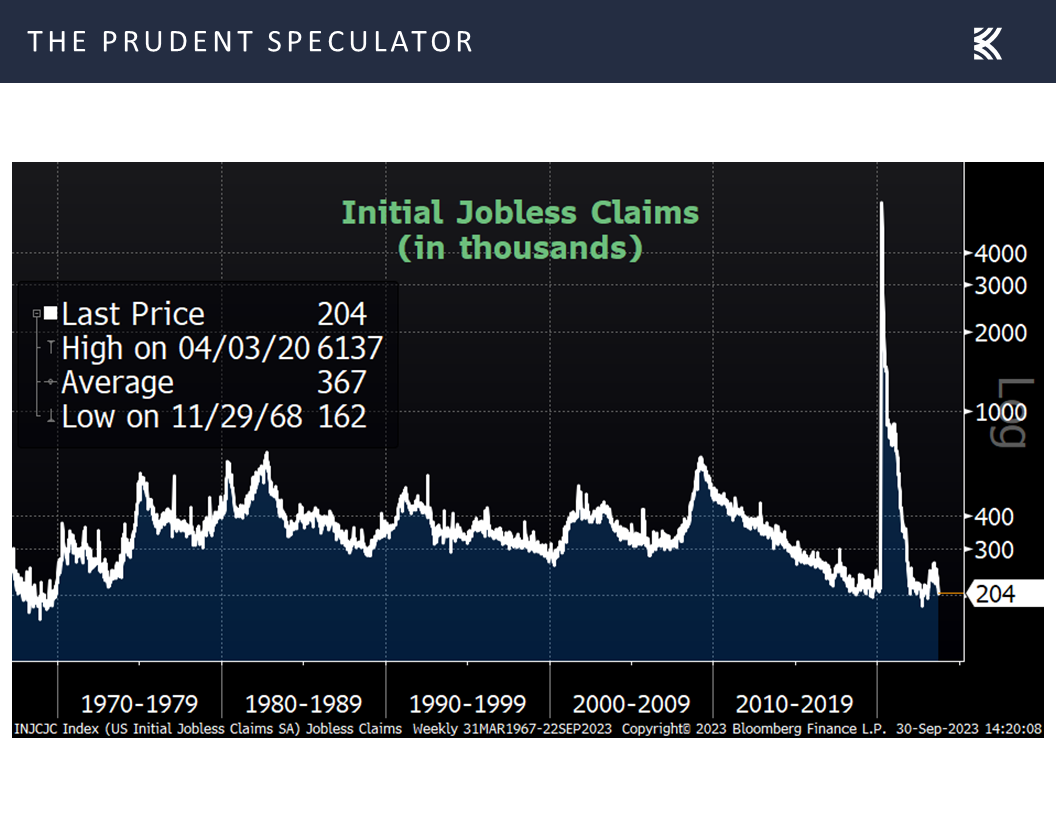

as the labor market continues to be very healthy, with extraordinarily low levels of first-time filings for unemployment benefits,

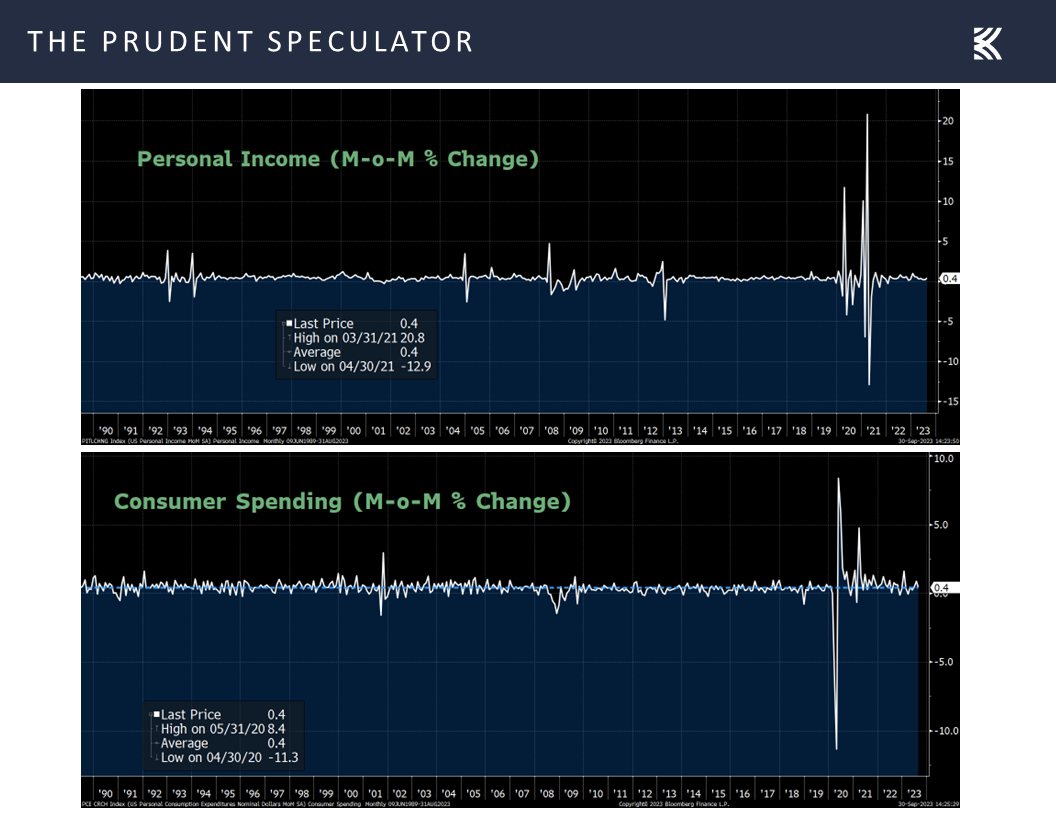

and personal incomes and consumer spending rising faster than the rate of inflation.

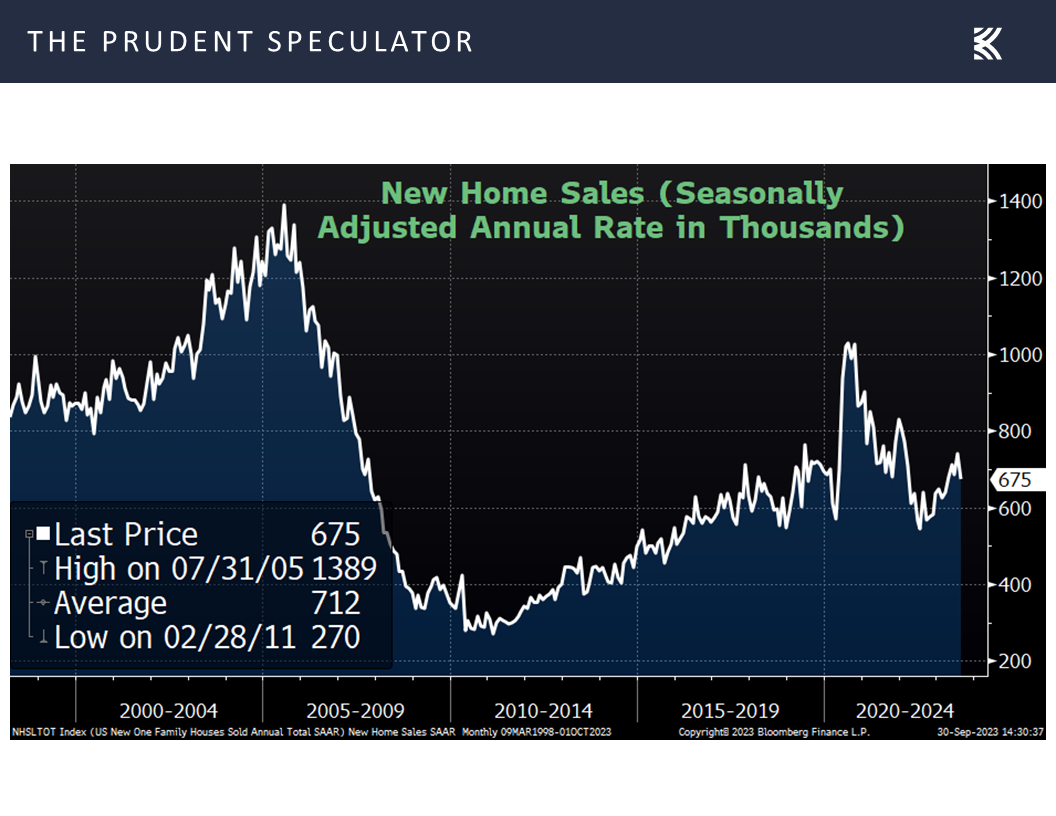

We concede that other economic data out last week was not so grand, with new home sales for August of 675,000 coming in below expectations and down from July’s 739,000 annualized rate,

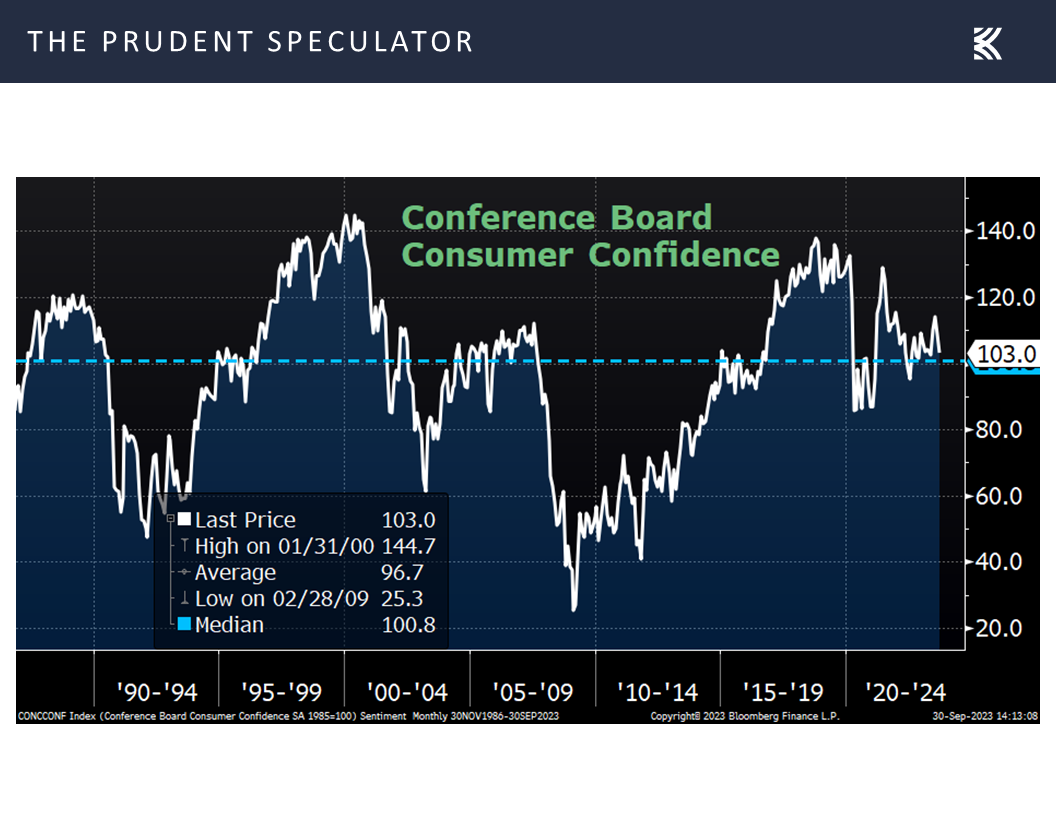

and consumer confidence for September, per the Conference Board, retreated to a four-month low at 103.0, down from a reading of 108.7 in August.

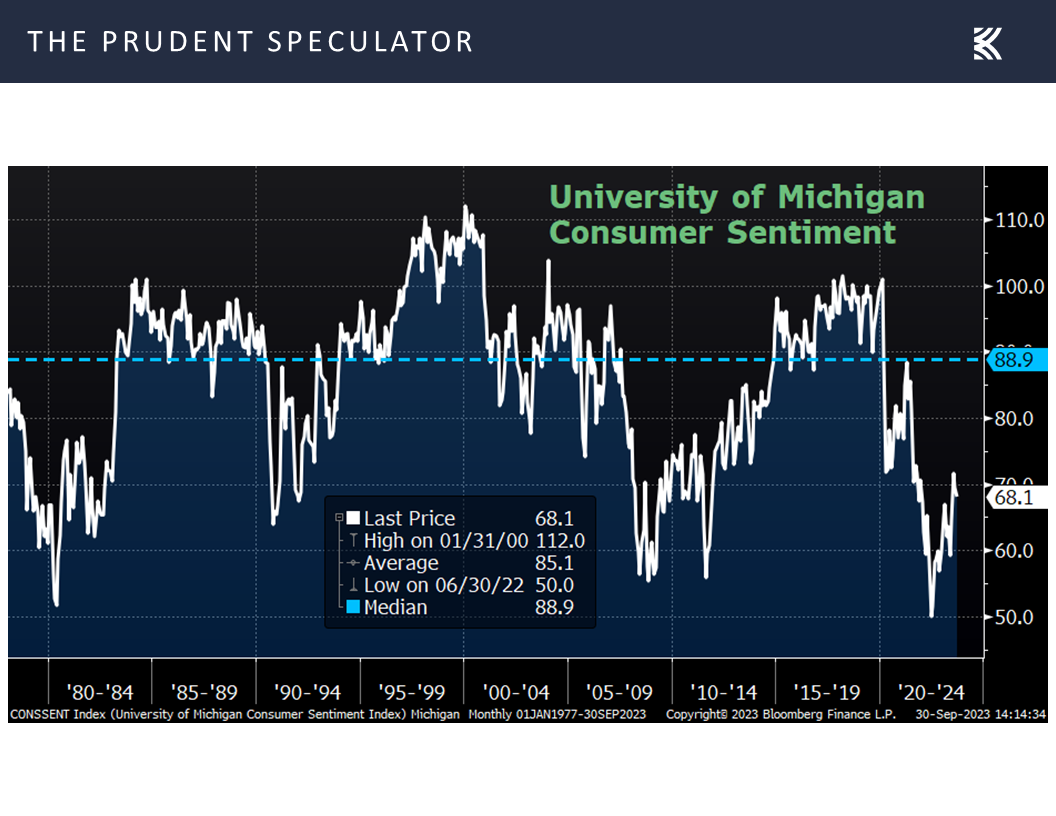

However, the gauge of consumer sentiment from the Univ. of Michigan for September of 68.1 modestly exceeded forecasts,

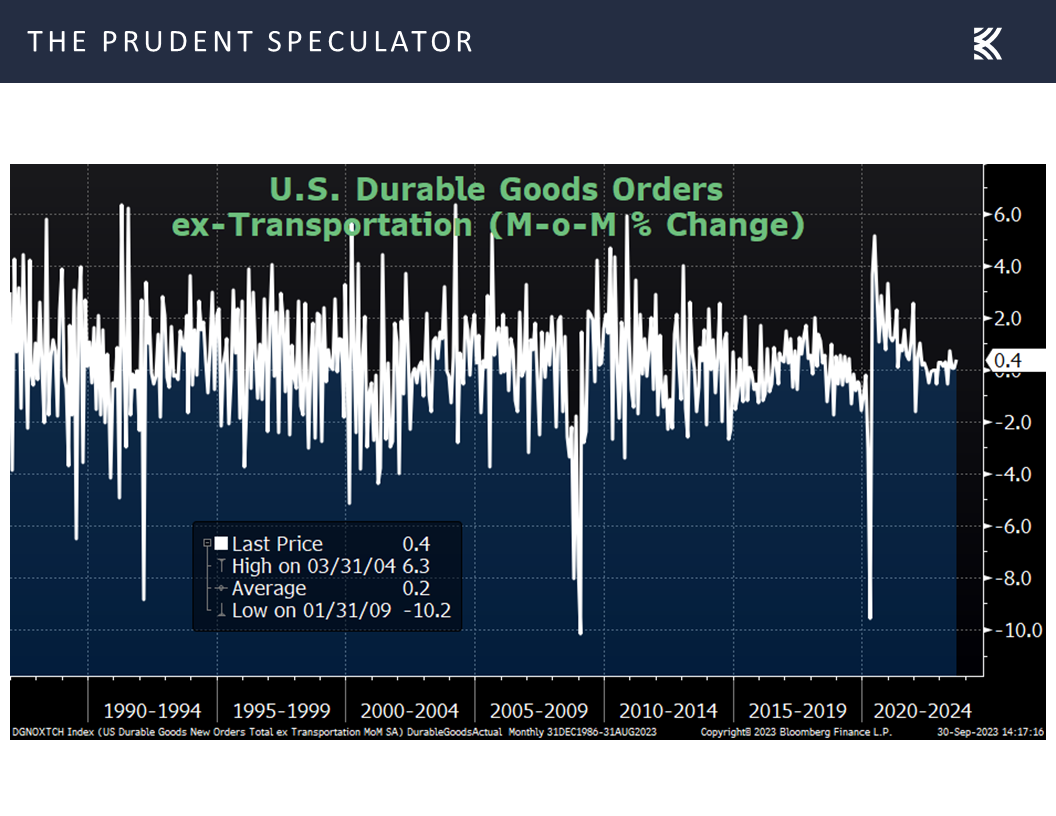

while orders for durable goods excluding the volatile transportation sector climbed 0.4% in August.

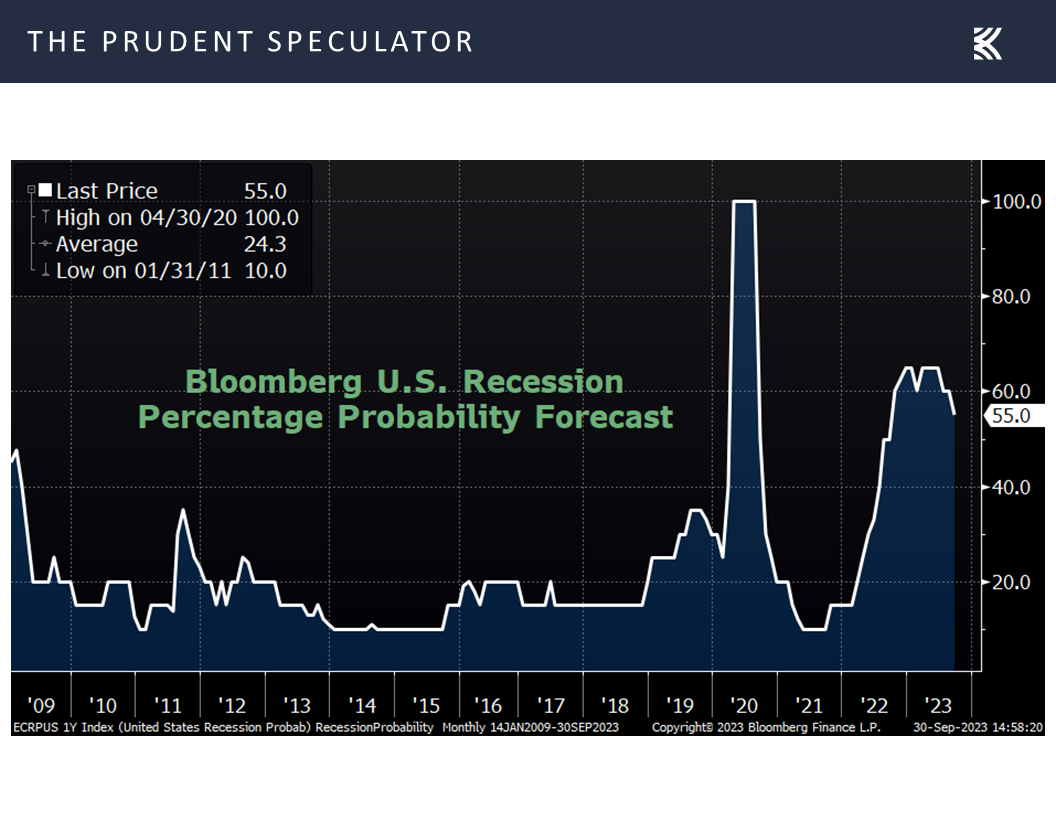

When all was said and done last week, the odds of recession, as calculated by Bloomberg, fell to 55%, down from the 60% level at which they have resided for the last few months.

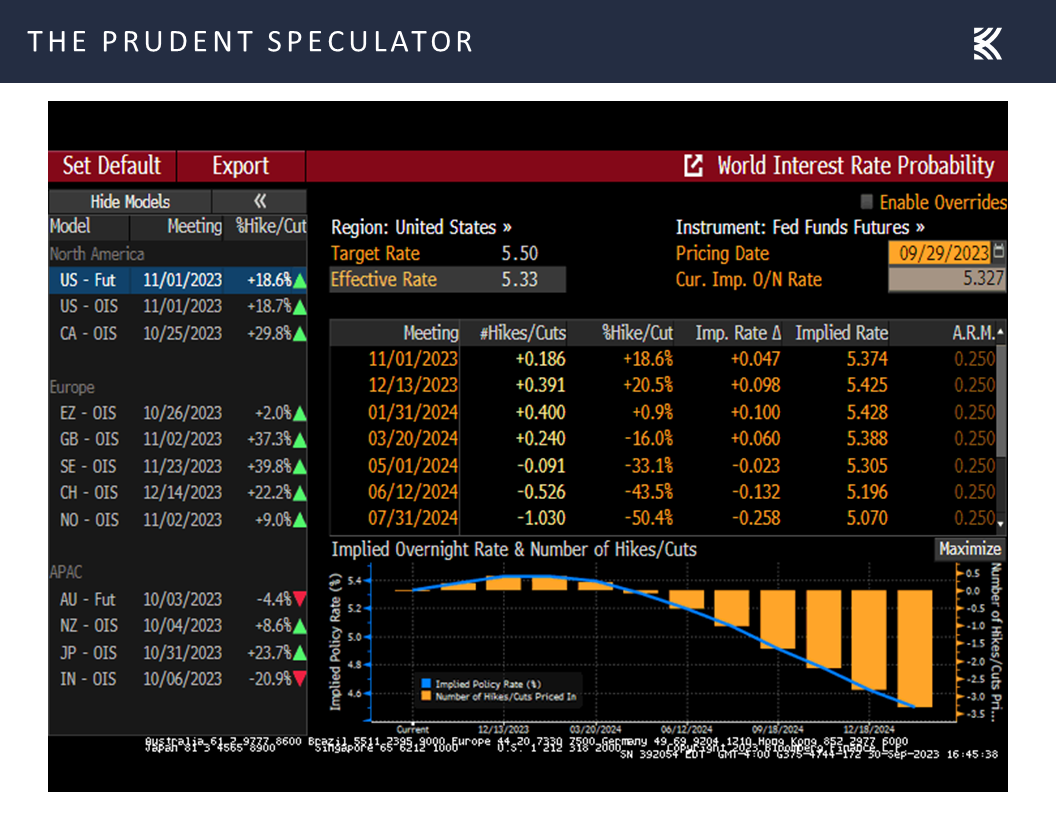

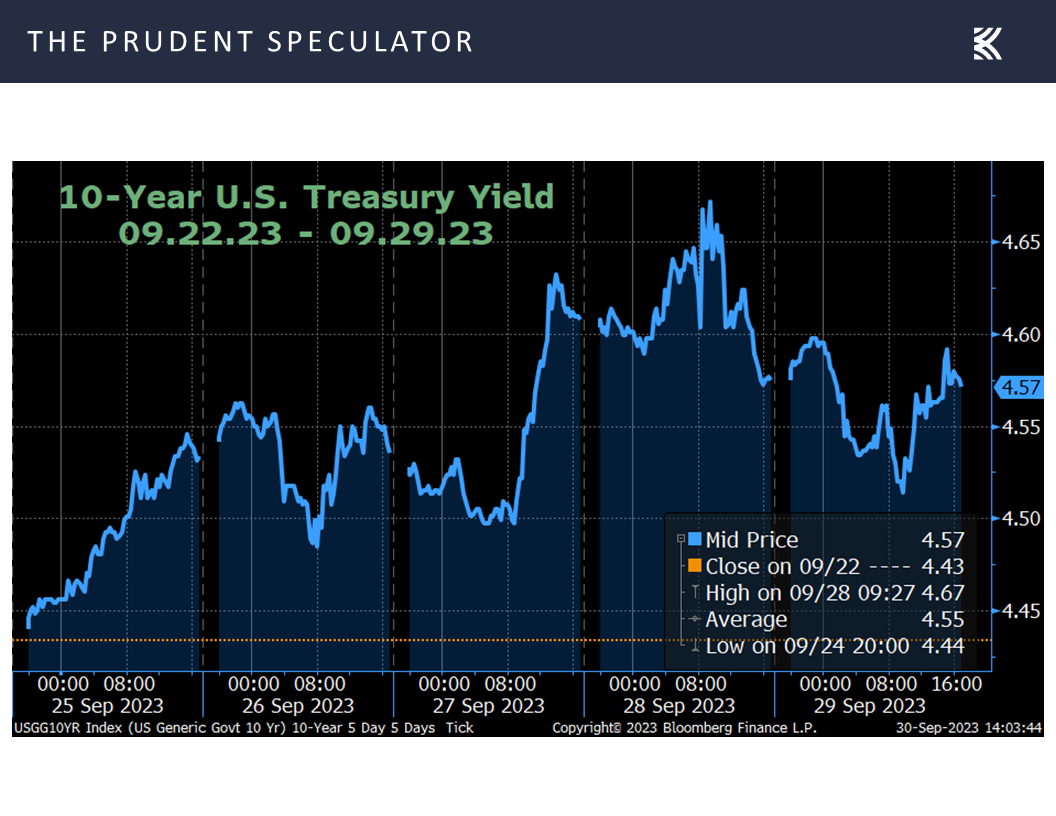

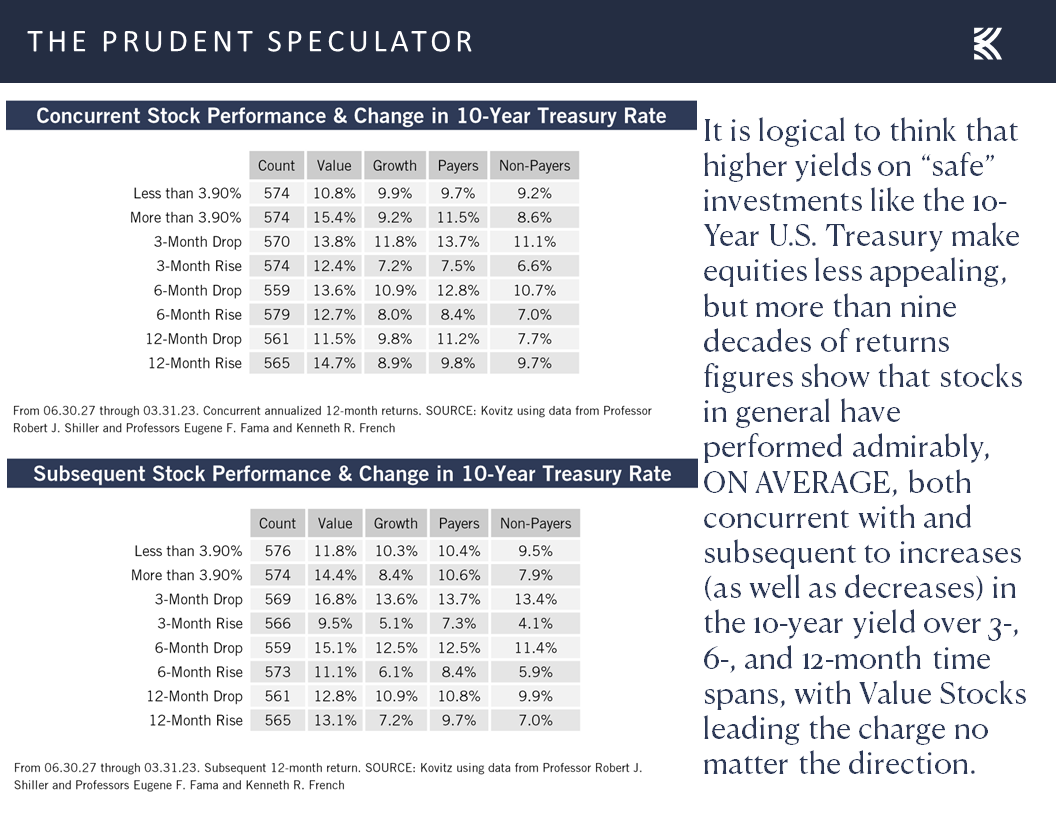

Interest Rates & Stocks – Rising 10-Year No Reason to Dump Equities

We realize that interest rates rose again last week, as government bond prices fell anew,

but history shows that a rising 10-Year U.S. Treasury yield has not been reason in the past to sell stocks, especially those of the Value variety,

while we continue to think that Value stocks in general remain inexpensively priced,

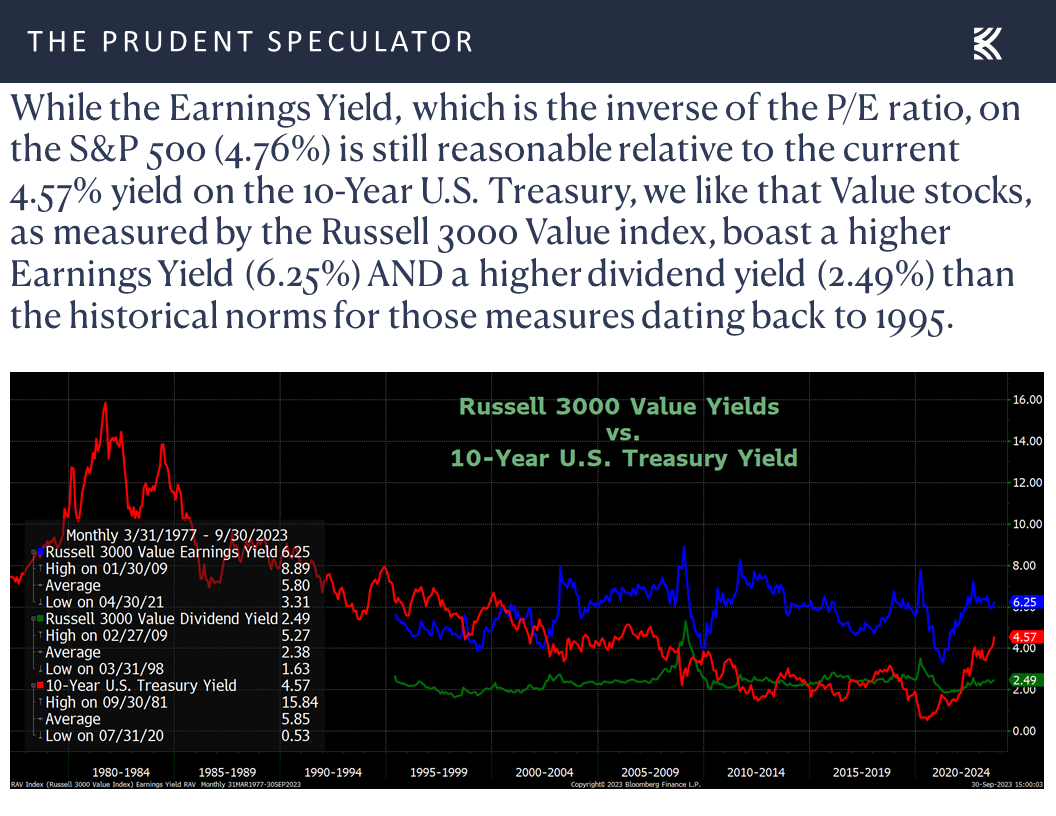

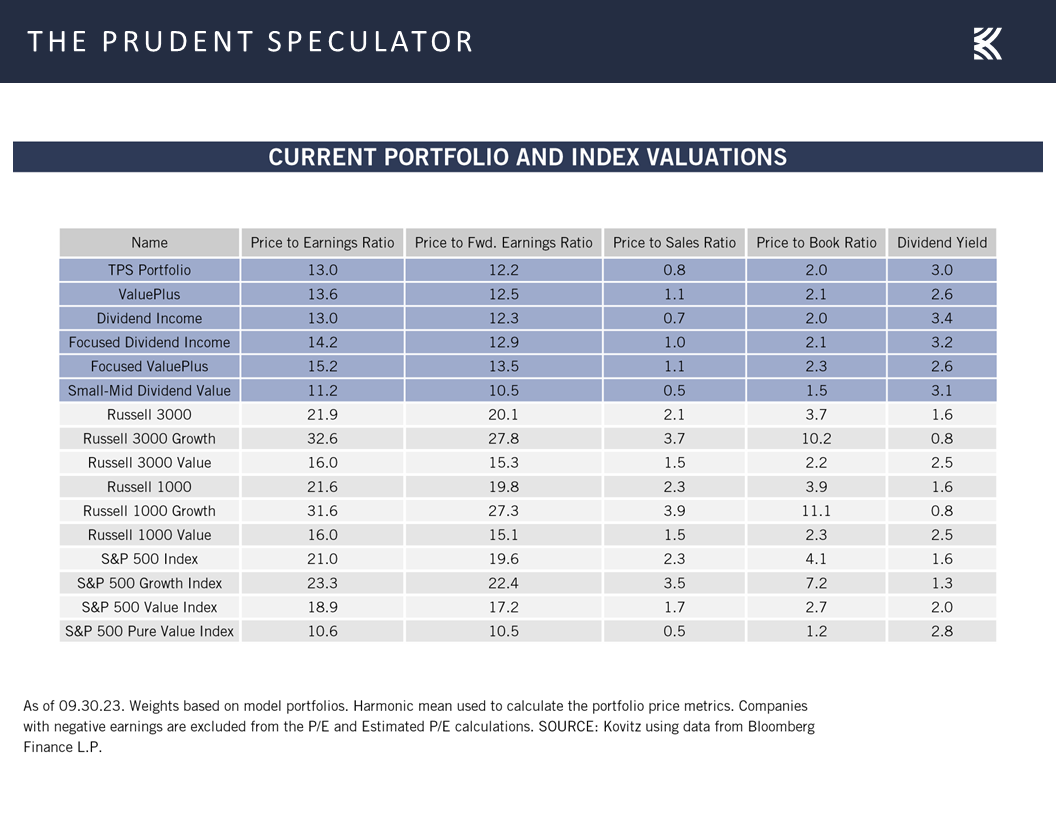

Valuations – Liking the Metrics Associated with our Portfolios

and that our portfolios in particular boast very attractive valuation metrics.

Volatility – Pullbacks are Normal; Stocks Have Provided Handsome Long-Term Rewards

Certainly, we must be braced for additional downside volatility, as we are now in a 5%+ pullback (which has happened more than 3 times per year, on average), but we continue to believe that handsome long-term rewards will accrue,

to those who remember that time in the market trumps market timing.

Stock News – Updates on two stocks across two different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Stocks, Inflation, Interest Rates, Volatility, Valuations and More

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss stocks, inflation, interest rates, volatility, valuations and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Forbes Cruise – Buckingham in Spain

Week in Review – Late Decline Sends Stocks Down Again; Government Shutdowns Historically a Reason to Buy Stocks

Inflation – Core PCE Rises Less than Expected

Econ News – Mixed Set of Numbers Last Week; Recession Odds Decrease; Strong Q3 Growth Still the Forecast

Interest Rates & Stocks – Rising 10-Year No Reason to Dump Equities

Valuations – Liking the Metrics Associated with our Portfolios

Volatility – Pullbacks are Normal; Stocks Have Provided Handsome Long-Term Rewards

Stock News – Updates on MU & JBL

Forbes Cruise – Buckingham in Spain

Greetings from Cadiz, Spain, where the 40th Forbes Cruise for Investors is now in full swing having set sail from Lisbon, Portugal on Friday evening. Your Editor speaks to the Forbes throng on October 5 and thus far it does not look like any changes are needed to the presentation prepared last weekend.

Week in Review – Late Decline Sends Stocks Down Again; Government Shutdowns Historically a Reason to Buy Stocks

True, stocks endured a volatile trading week, ending with modest losses for the full five trading sessions. It appeared that there might have been green ink for the week, were it not for a late-day selloff on Friday, evidently after worries accelerated about a government shutdown. Of course, if market history is a guide, said concerns seem misplaced, given that such events have been short-lived (a shutdown was averted over the weekend, for 45 days at least) and forward returns one-year hence actually have been better than the norm!

Of course, September lived down to its reputation for red ink since your Editor arrived at The Prudent Speculator more than 36 years ago,

Inflation – Core PCE Rises Less than Expected

but we might have argued that economic news out last week would have led to a rebound in stocks, given that the Federal Reserve’s preferred measure of inflation, the core personal consumption expenditures (PCE) gauge, which excludes volatile food and energy prices, rose a weaker-than-expected 0.1% in August compared to July, with the year-over-year measure holding steady at 3.9%.

Yes, the full PCE jumped 0.4% in August, due to higher energy prices, with the overall rate of annualized inflation rising to 3.5% from 3.4%, but the Fed Funds futures market decided that the probabilities of additional rate hikes from Jerome H. Powell & Co. were slightly lower at the end of this week than they were at the end of the week prior.

On the growth side of the economic equation, the outlook for Q3 GDP, per calculations from the Atlanta Fed, remained at a very robust real (inflation-adjusted) expansion of 4.9%,

Econ News – Mixed Set of Numbers Last Week; Recession Odds Decrease; Strong Q3 Growth Still the Forecast

as the labor market continues to be very healthy, with extraordinarily low levels of first-time filings for unemployment benefits,

and personal incomes and consumer spending rising faster than the rate of inflation.

We concede that other economic data out last week was not so grand, with new home sales for August of 675,000 coming in below expectations and down from July’s 739,000 annualized rate,

and consumer confidence for September, per the Conference Board, retreated to a four-month low at 103.0, down from a reading of 108.7 in August.

However, the gauge of consumer sentiment from the Univ. of Michigan for September of 68.1 modestly exceeded forecasts,

while orders for durable goods excluding the volatile transportation sector climbed 0.4% in August.

When all was said and done last week, the odds of recession, as calculated by Bloomberg, fell to 55%, down from the 60% level at which they have resided for the last few months.

Interest Rates & Stocks – Rising 10-Year No Reason to Dump Equities

We realize that interest rates rose again last week, as government bond prices fell anew,

but history shows that a rising 10-Year U.S. Treasury yield has not been reason in the past to sell stocks, especially those of the Value variety,

while we continue to think that Value stocks in general remain inexpensively priced,

Valuations – Liking the Metrics Associated with our Portfolios

and that our portfolios in particular boast very attractive valuation metrics.

Volatility – Pullbacks are Normal; Stocks Have Provided Handsome Long-Term Rewards

Certainly, we must be braced for additional downside volatility, as we are now in a 5%+ pullback (which has happened more than 3 times per year, on average), but we continue to believe that handsome long-term rewards will accrue,

to those who remember that time in the market trumps market timing.

Stock News – Updates on two stocks across two different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.