The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss stocks, interest rates, Uncle Sam and more Economic News. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

FOMC Meeting – Fed Leaves Interest Rates Unchanged; Higher for Longer?

Week in Review – Bears Maul Goldliocks

Media Flip Flop – Fed Moves Positive One Day and Negative the Next

Econ News – Mixed Set of Numbers Last Week; Solid Q3 Growth Still the Forecast

Interest Rates & Stocks – Rising Fed Funds & 10-Year No Reason to Dump Equities

Valuations – Liking the Metrics Associated with our Portfolios

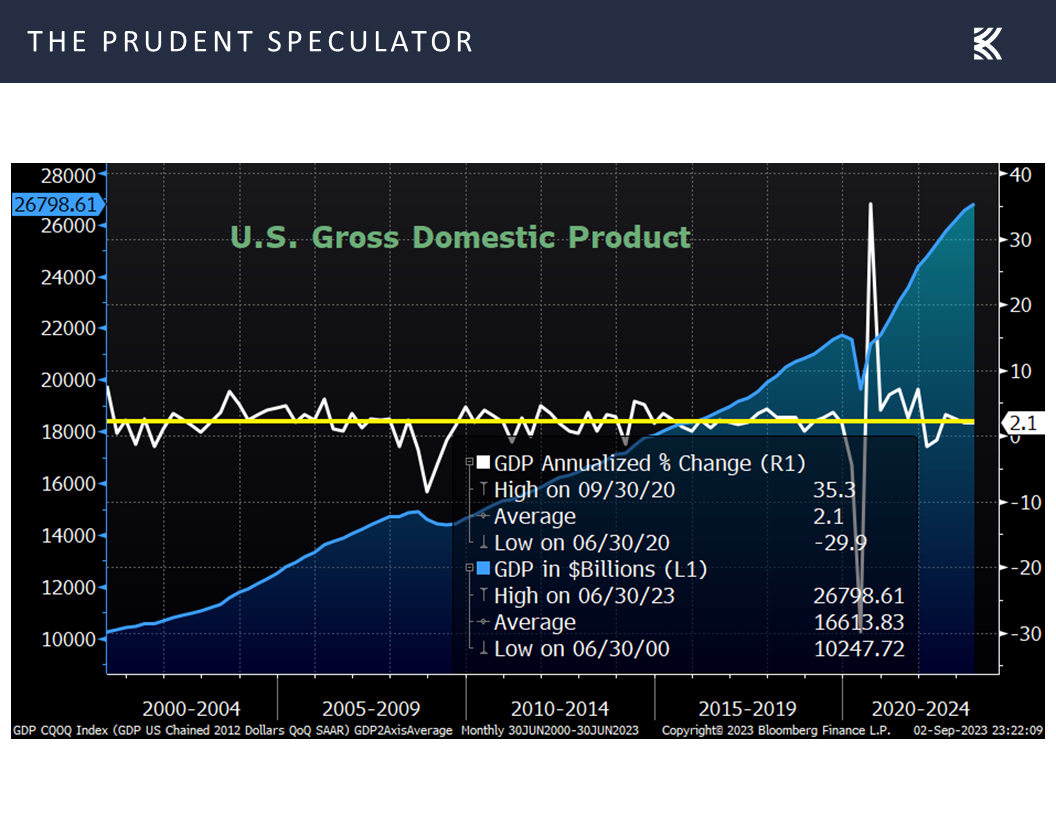

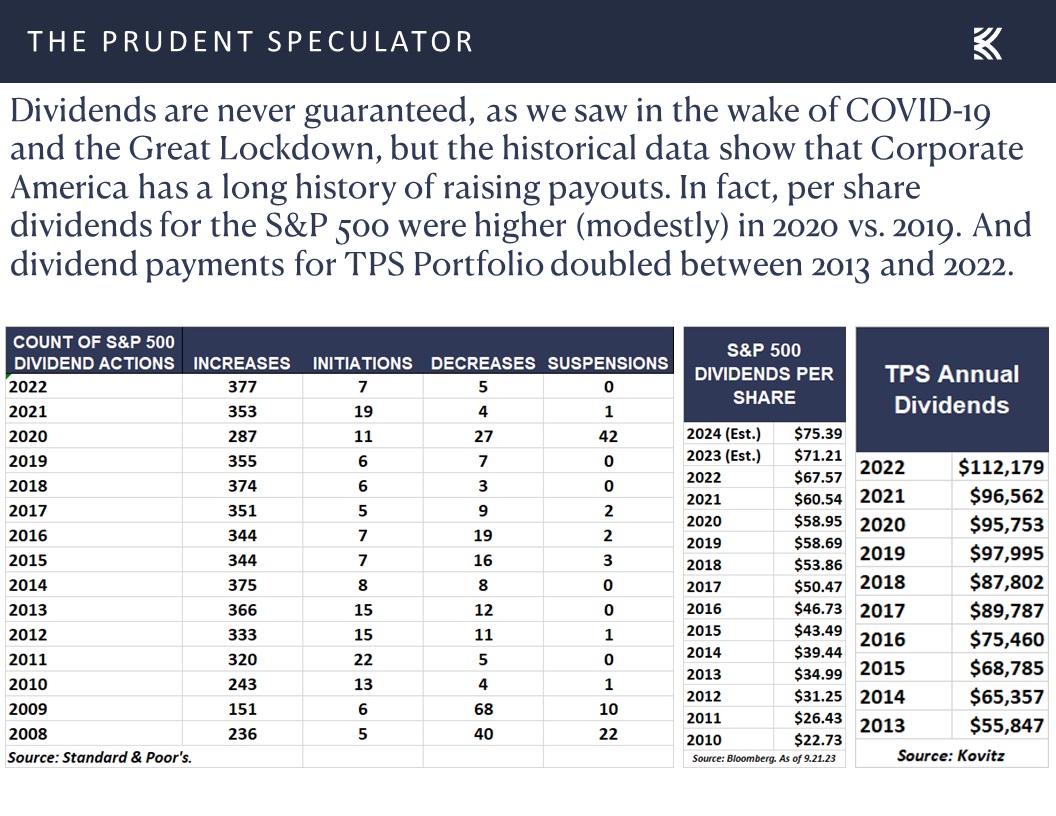

Growth – Corporate Profits, GDP and Dividends Have Increased Over Time

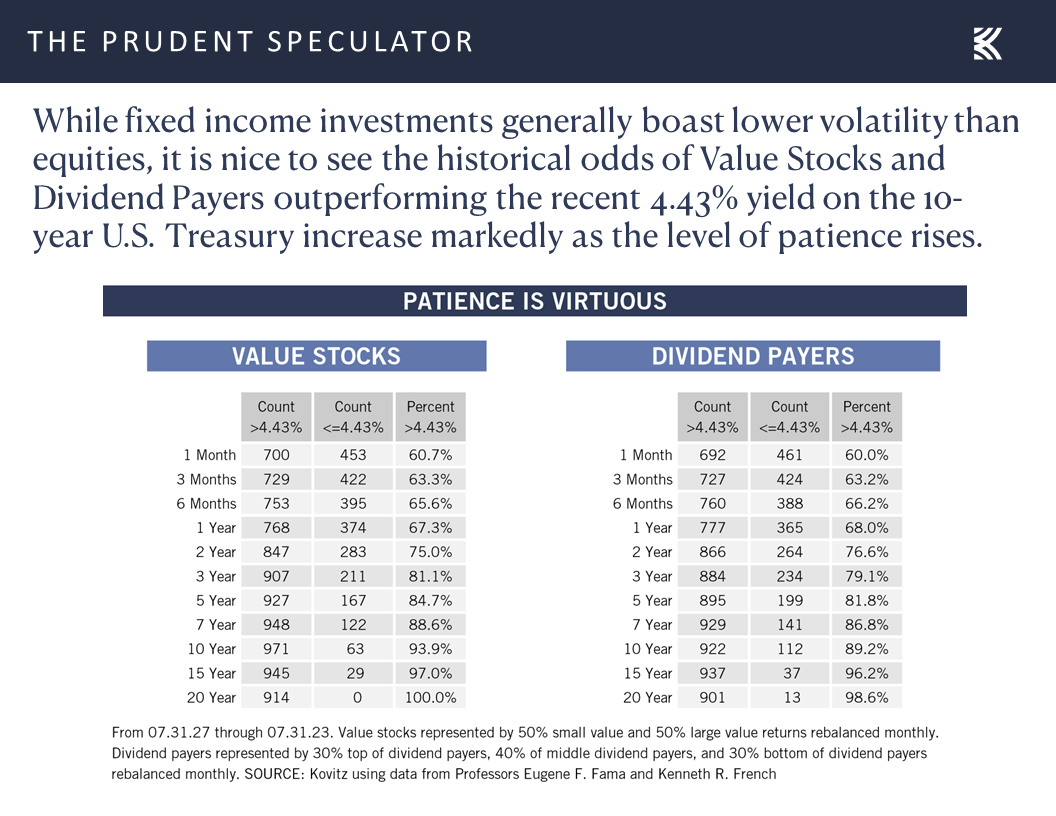

Patience – The Longer the Hold, the Better the Chance of Beating a 4.43% Annualized Return

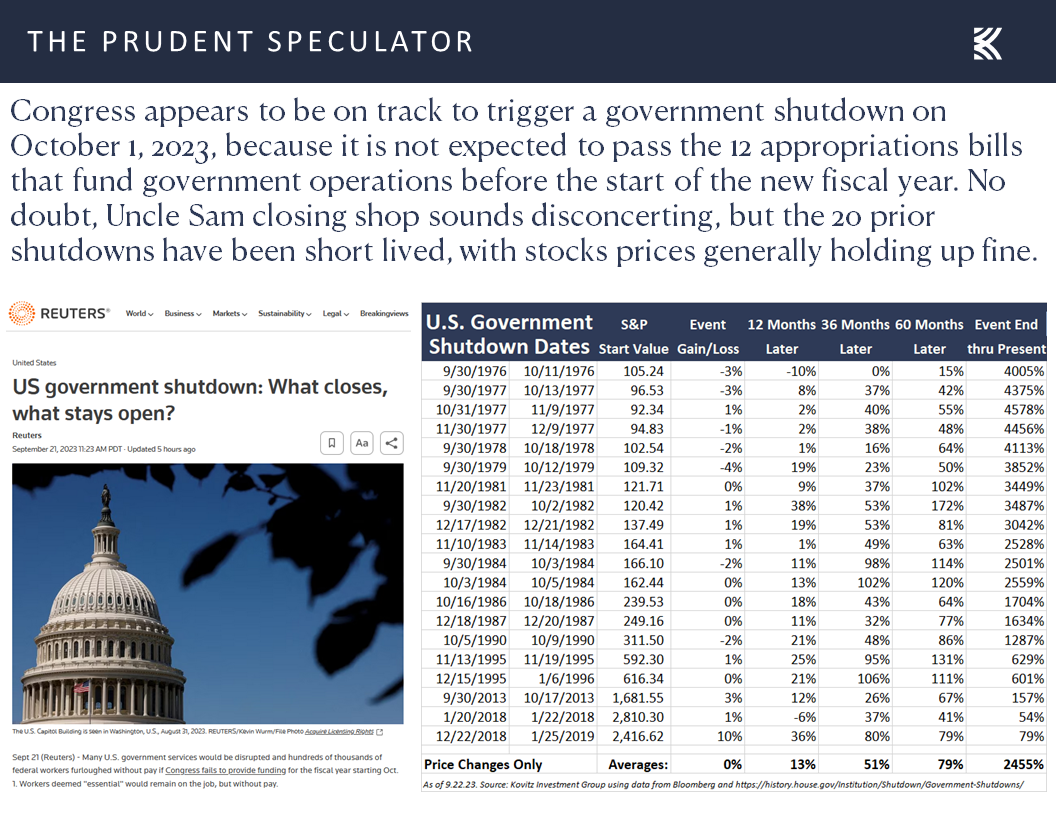

Uncle Sam – Government Shutdowns Historically a Reason to Buy Stocks

Stock News – Updates on seven stocks across eight different sectors

FOMC Meeting – Fed Leaves Interest Rates Unchanged; Higher for Longer?

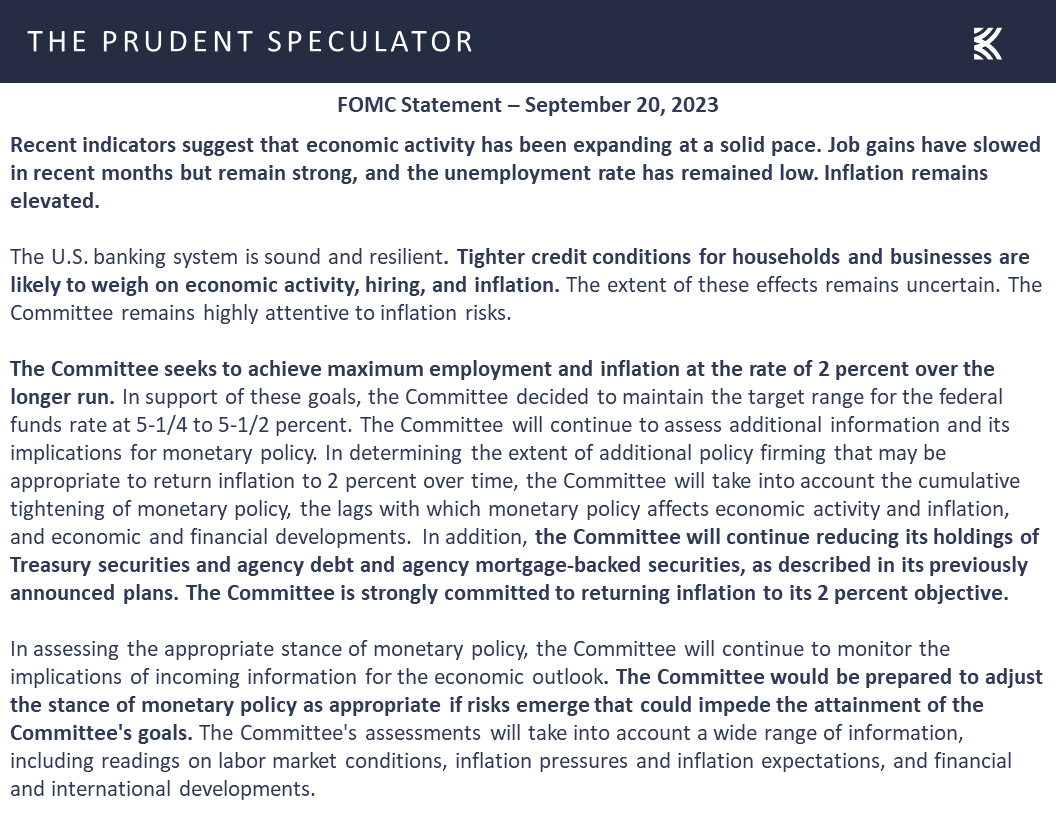

The financial markets are often more volatile than usual during Fed Week, and the aftermath of the September FOMC Meeting continued that trend. Jerome H. Powell & Co. chose to leave their Target for the Fed Funds rate unchanged at a range of 5.25% to 5.50%,

while the Fed Chair offered a relatively upbeat assessment of the economy:

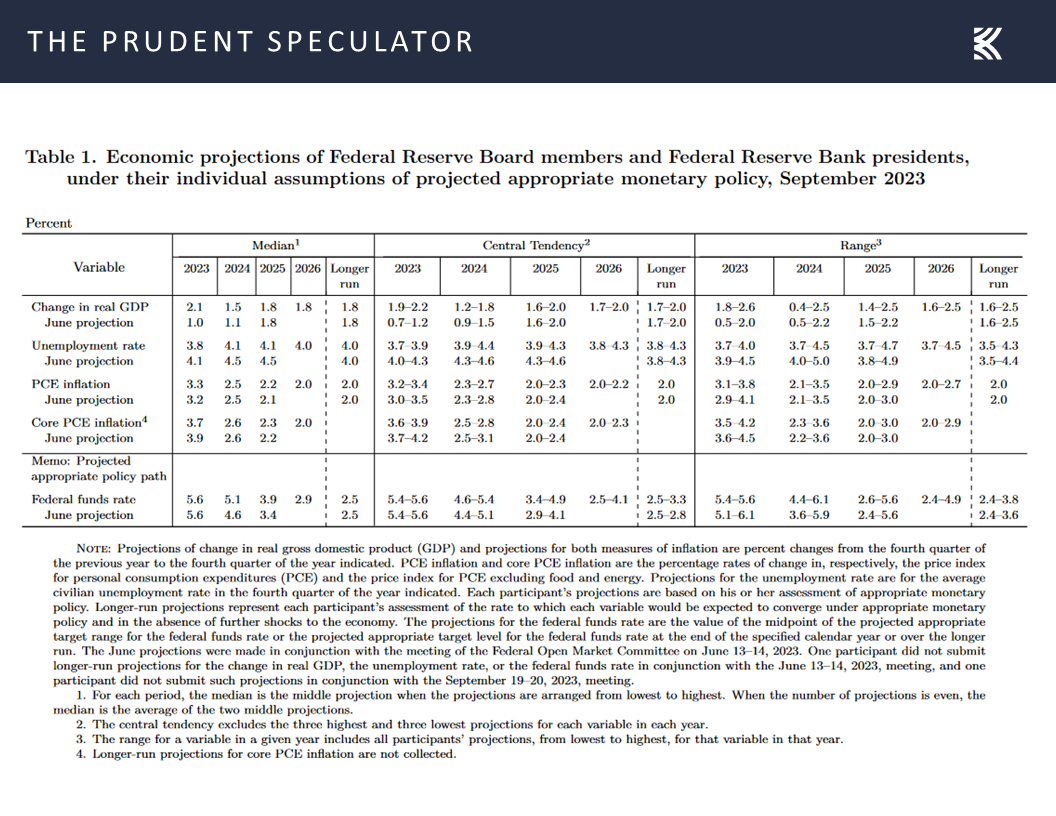

Recent indicators suggest that economic activity has been expanding at a solid pace, and so far this year, growth in real GDP has come in above expectations. Recent readings on consumer spending have been particularly robust. Activity in the housing sector has picked up somewhat, though it remains well below levels of a year ago, largely reflecting higher mortgage rates. Higher interest rates also appear to be weighing on business fixed investment. In our Summary of Economic Projections, or SEP, Committee participants revised up their assessments of real GDP growth, with the median for this year now at 2.1 percent. Participants expect growth to cool, with the median projection falling to 1.5 percent next year.

The latest projections from the Federal Reserve Board members and Federal Reserve Board Bank presidents were an improvement from those offered in June, in which respective real GDP growth this year and next was estimated to be 1.0% and 1.1%.

Interestingly, the lead Fed watcher for The New York Times offered the following positive spin in Thursday’s edition of the newspaper:

Taken together, the projections painted a sunny picture, one in which a robust economy is managing to digest higher borrowing costs without tipping into — or even getting close to — a recession. At the same time, inflation is steadily fading from its rapid pace last year. The combination is giving Fed officials the breathing room they need to be patient, and it is increasing the odds that they might be able to wrangle price increases without inflicting a lot of economic pain.

“It does read very much like a Goldilocks,” said Blerina Uruci, chief U.S. economist at T. Rowe Price. “We’re basically getting a deceleration in inflation with less pain on the economic front.”

Week in Review – Bears Maul Goldliocks

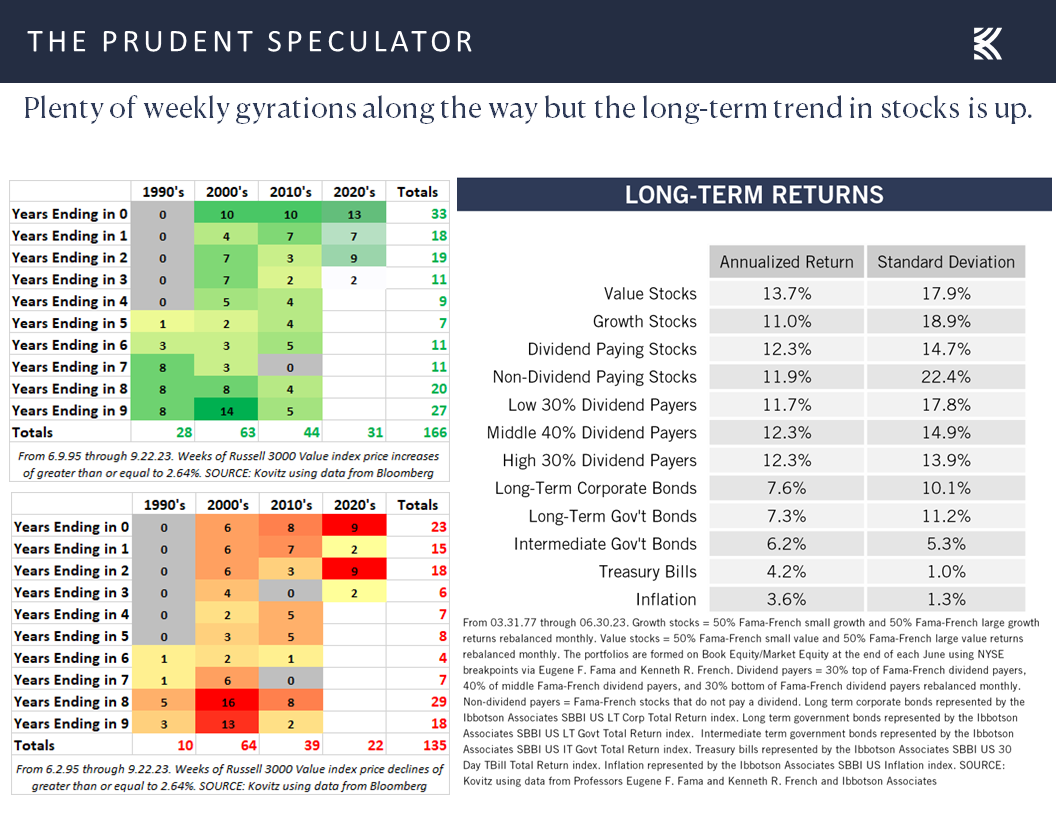

Alas, Goldilocks was seemingly consumed by the Three Bears on Thursday and Friday as stocks endured one of the worst weeks of the year, with the Russell 3000 Value index shedding 2.64% on a price basis, its 135th biggest weekly loss since the inception of that benchmark in 1995.

Media Flip Flop – Fed Moves Positive One Day and Negative the Next

The big selloff in equities prompted a radically different and negative take from the same New York Times columnist in the Friday edition:

The era of ultralow interest rates may be over. At the very least, policymakers don’t expect the type of low borrowing costs that prevailed before the pandemic to return anytime soon.

The Federal Reserve decided this week to leave interest rates unchanged at their highest level in two decades, and left the door open to raising rates again before the end of the year. But an even more significant if subtle change lurked in its freshly released economic projections.

Fed officials do not expect rates to go much higher — the next quarter-point increase is likely to be the last, if they make even that. But they do expect borrowing costs to stay elevated for years to come. Policymakers expect their benchmark short-term interest rate to stay above 5 percent next year, and to end 2025 at nearly 4 percent, the estimates showed. That would be roughly double where they were at the end of 2019.

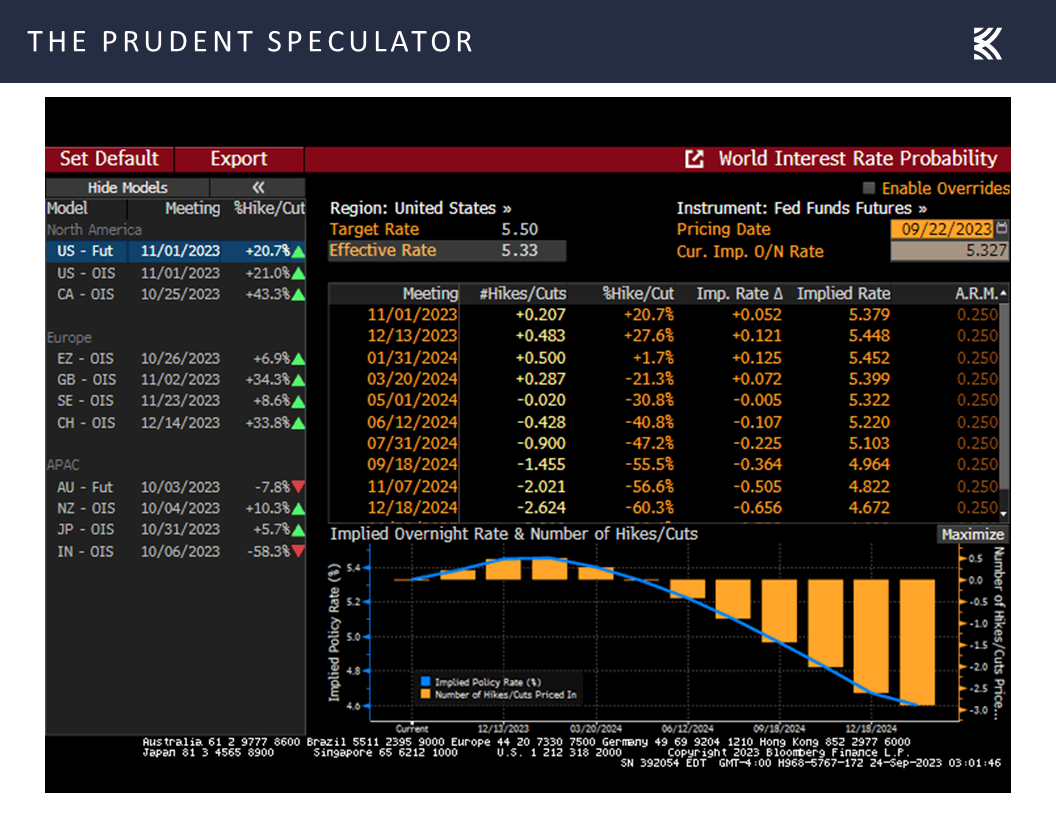

It was the “higher for longer” view that seemed to cause consternation, as the expectations of the futures market for the year-end 2023 and 2024 Fed Funds rates ticked up last week,

Econ News – Mixed Set of Numbers Last Week; Solid Q3 Growth Still the Forecast

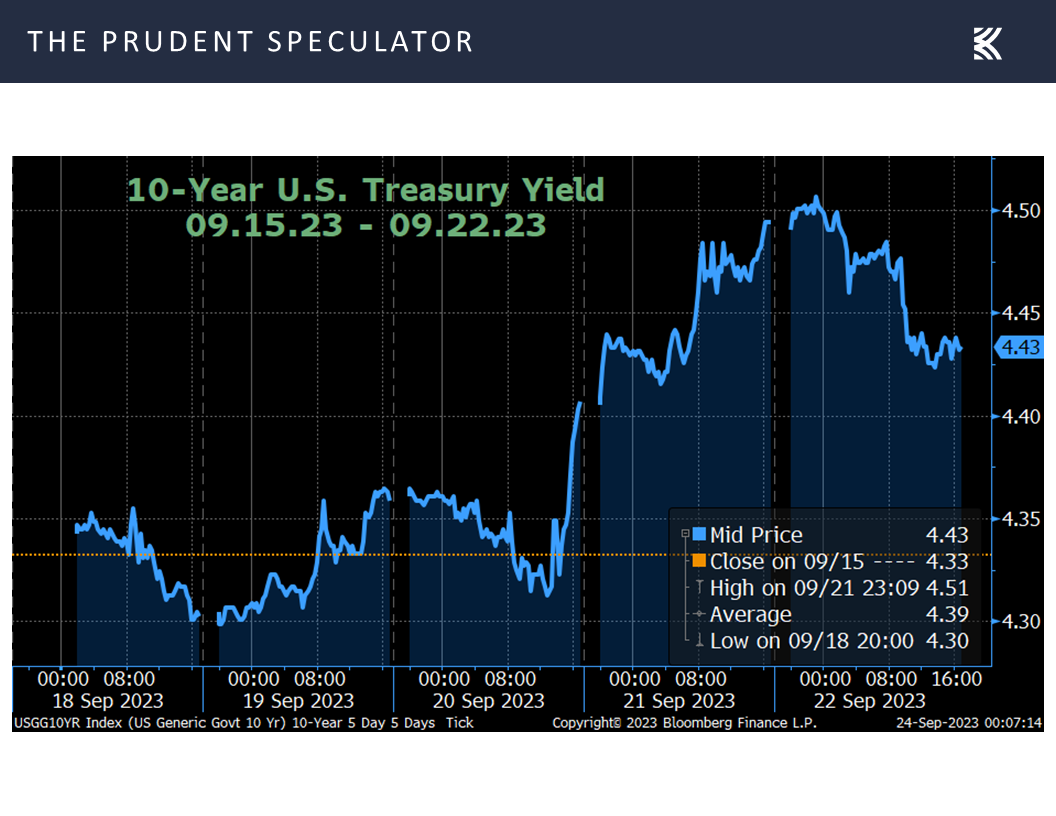

The knee-jerk reaction for fixed-income traders was to dump longer-term government bonds following the FOMC’s decision on interest rates,

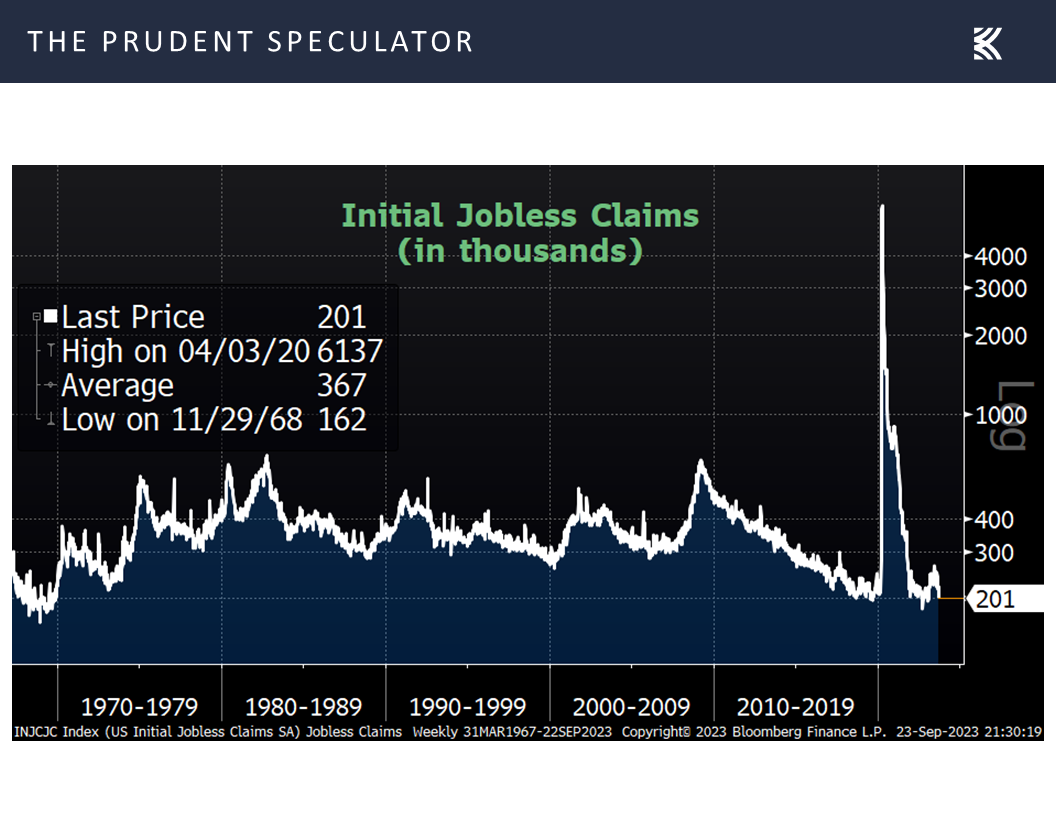

with Thursday’s much lower-than-expected weekly tally of 201,000 first-time filings for unemployment benefits adding to worries that the economy might be too strong for the Fed’s taste.

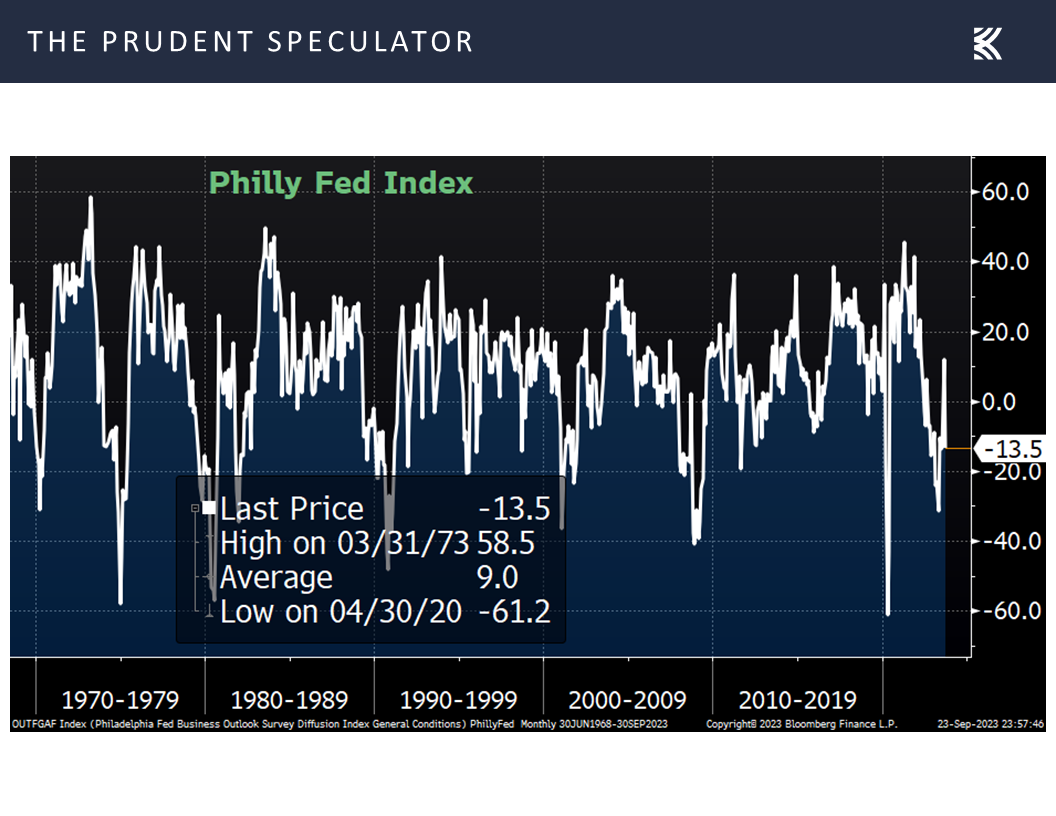

Of course, other economic data out last week was not exactly stellar, with a weaker-than-expected reading on manufacturing in the Philadelphia region,

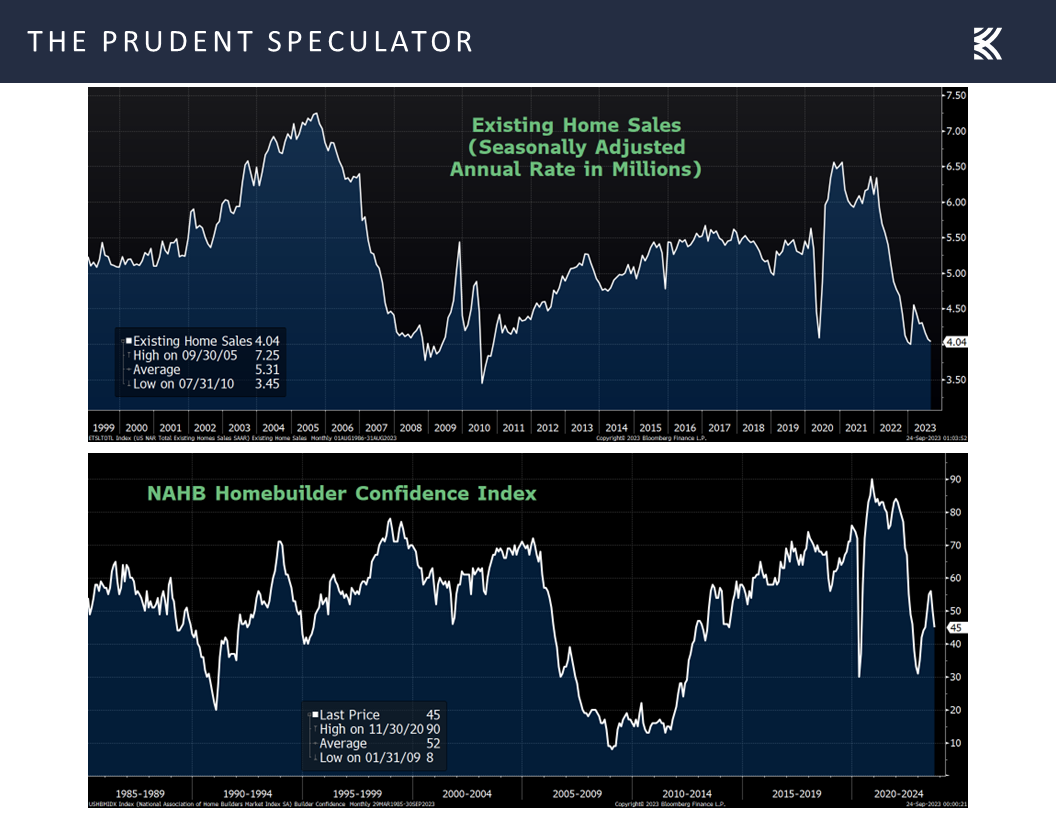

and disappointing numbers on the state of the housing market,

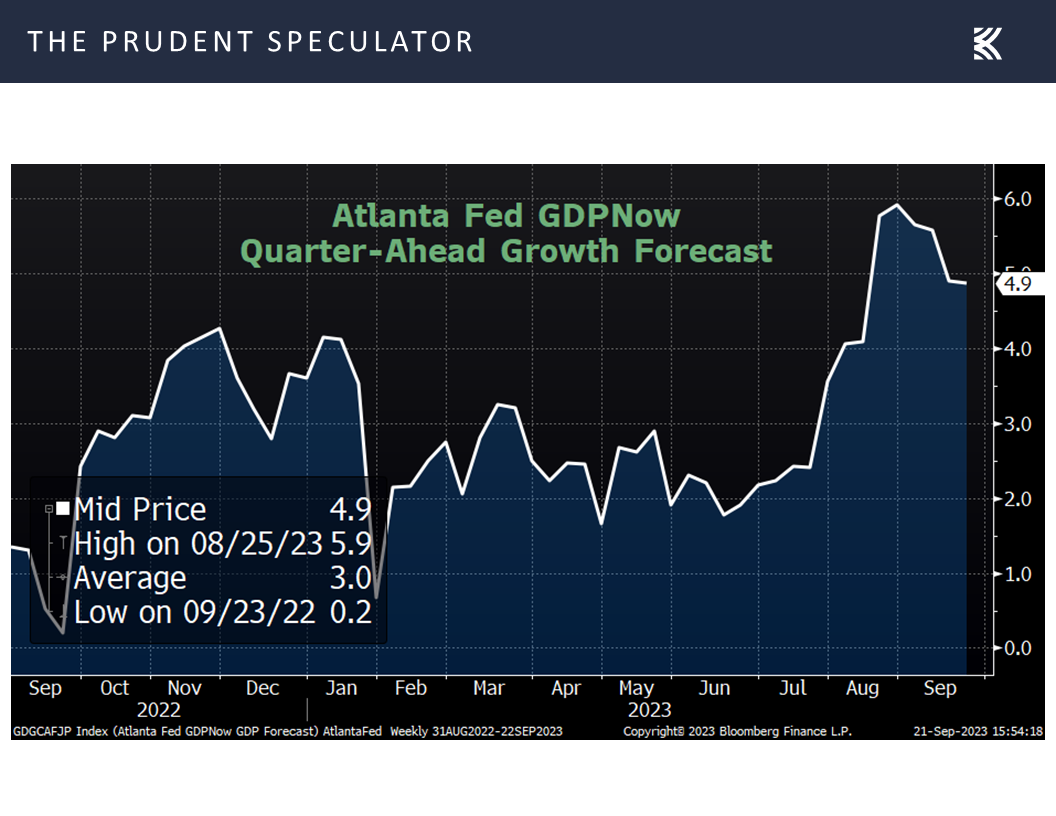

but the latest projection for real (inflation-adjusted) GDP growth from the Atlanta Fed remained at a very robust 4.9%.

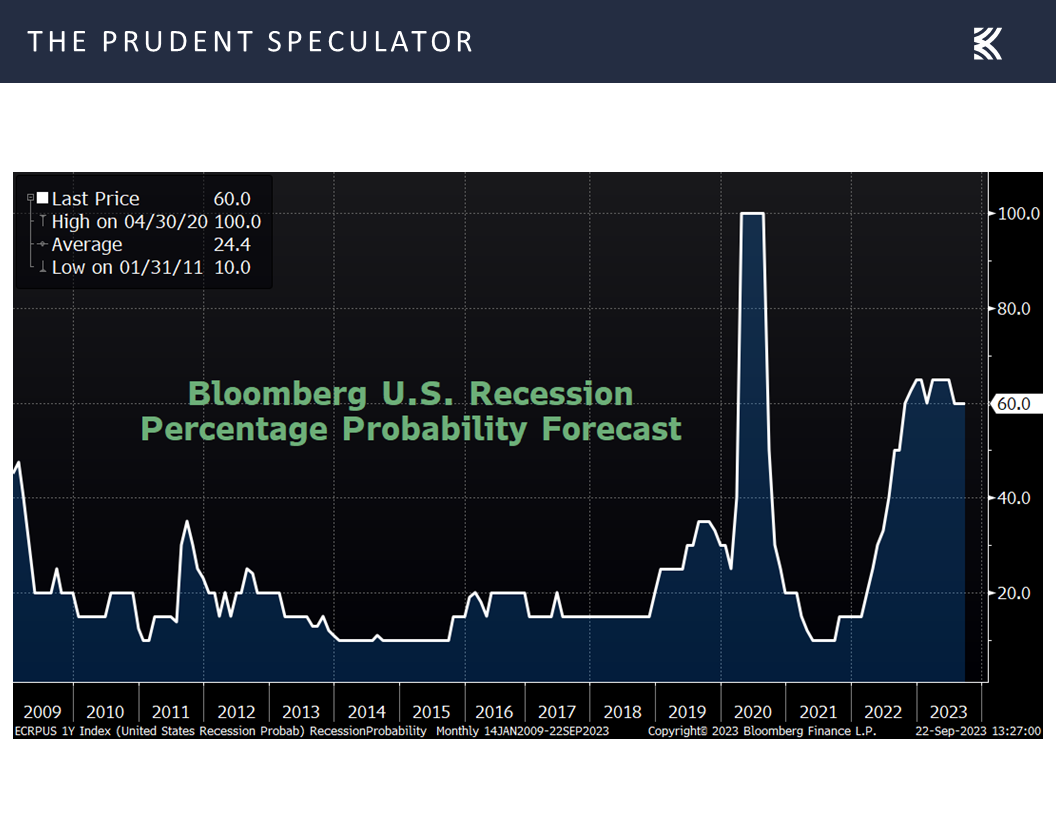

Lest there be worry that folks are starting to see the economic glass as half full, the odds of recession in the next 12 months, as tabulated by Bloomberg, continued to reside at 60%,

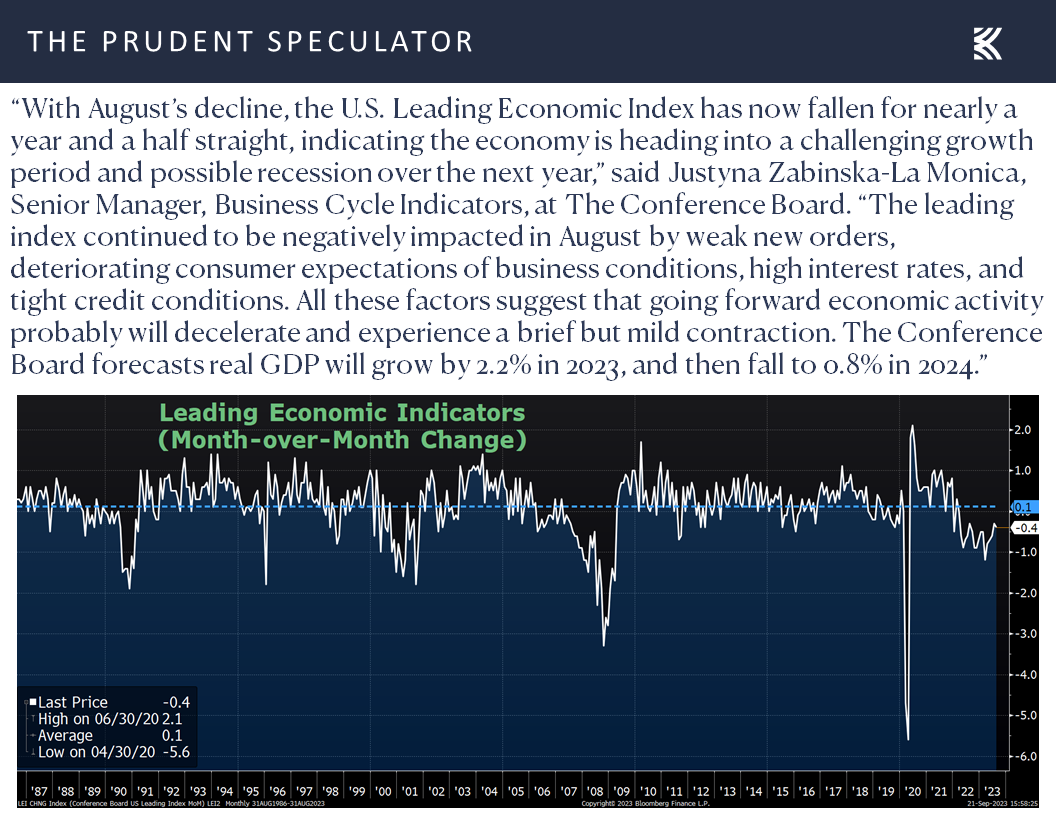

while the widely watched Leading Economic Index dropped by 0.4% last month, with the keeper of that metric, The Conference Board, continuing to predict a contraction next year, though their pessimism did diminish somewhat in the group’s latest commentary with the suggestion that the expected recession will be “brief” and “mild.”

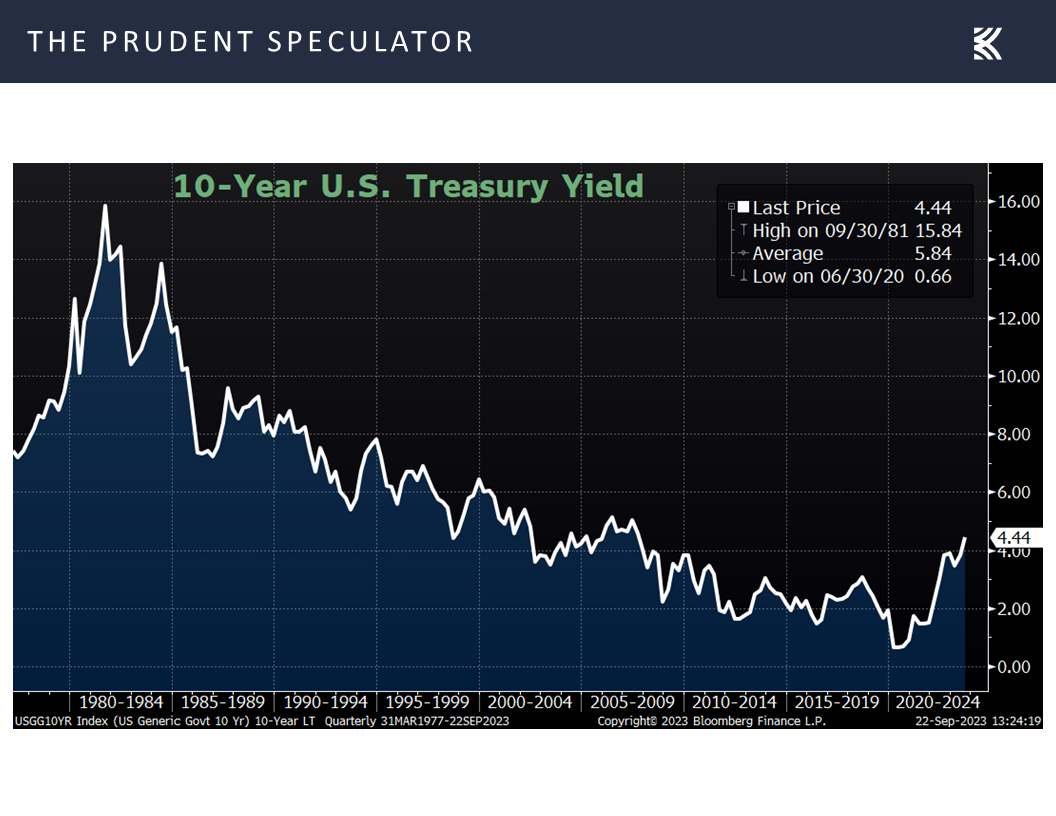

Interest Rates & Stocks – Rising Fed Funds & 10-Year No Reason to Dump Equities

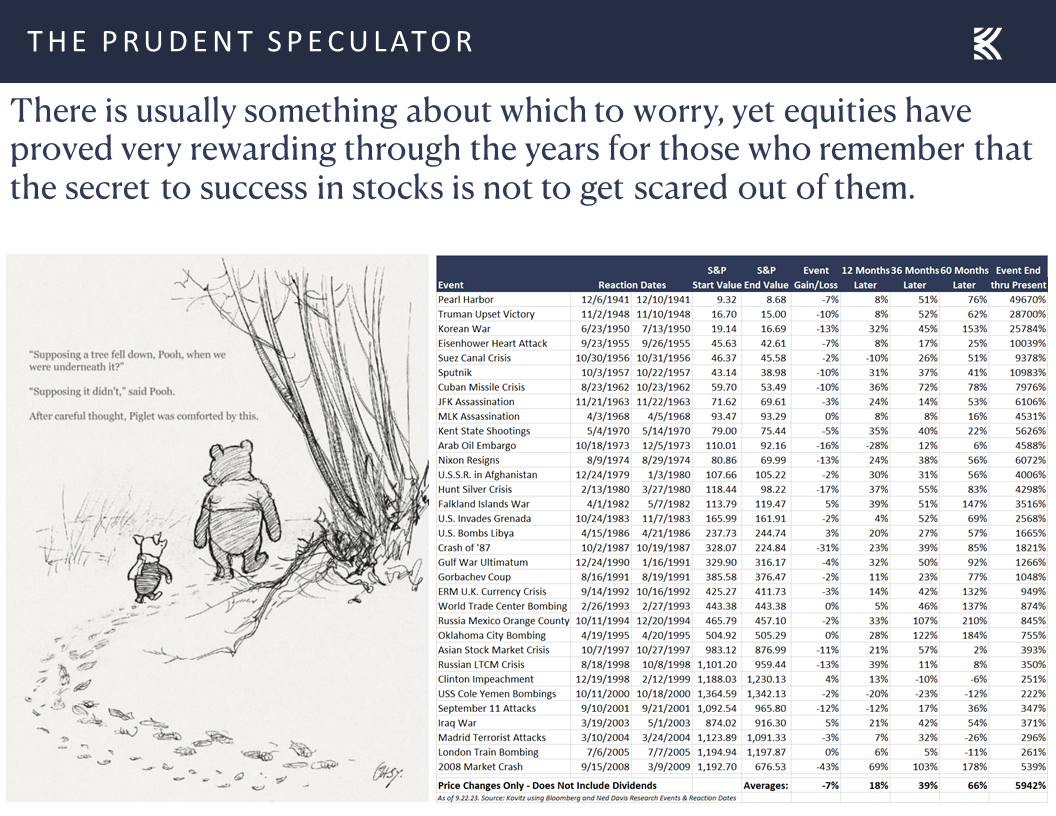

As is always the case, we remain braced for additional equity market downside, especially as there are still five-plus trading weeks to go in the seasonally less-favorable time of the year,

but we offer the friendly reminder that stocks have overcome plenty of disconcerting events over the years to go on to post terrific long-term returns.

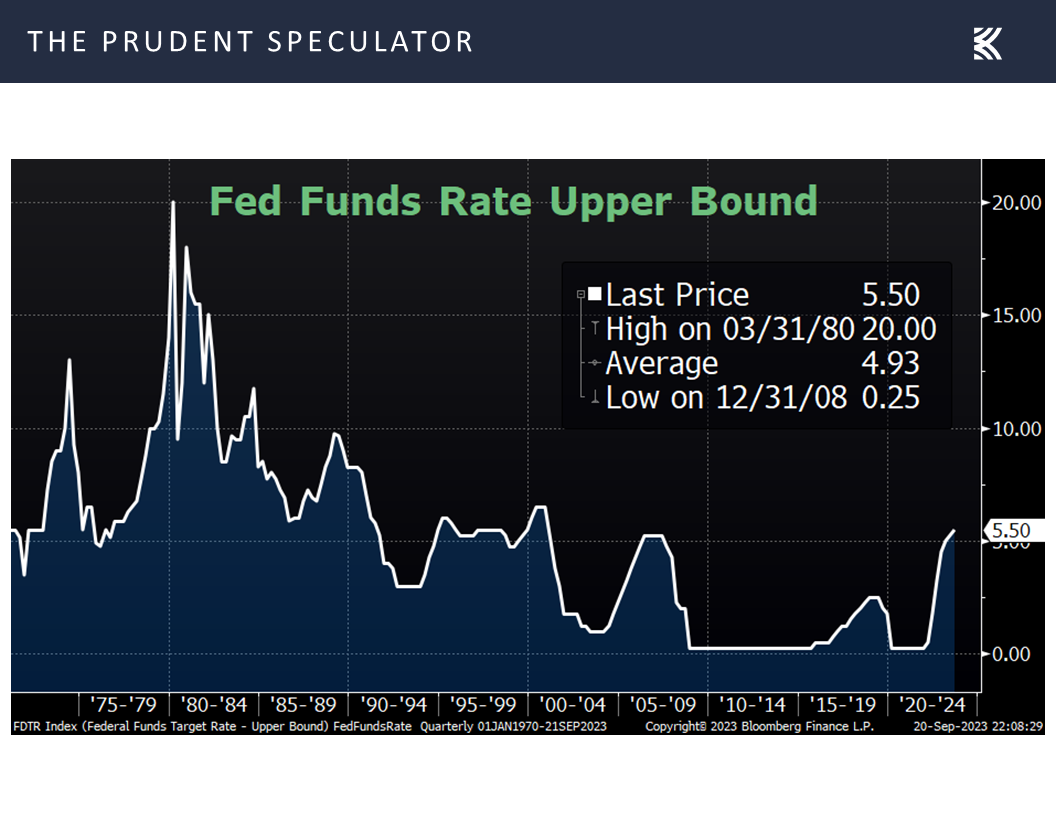

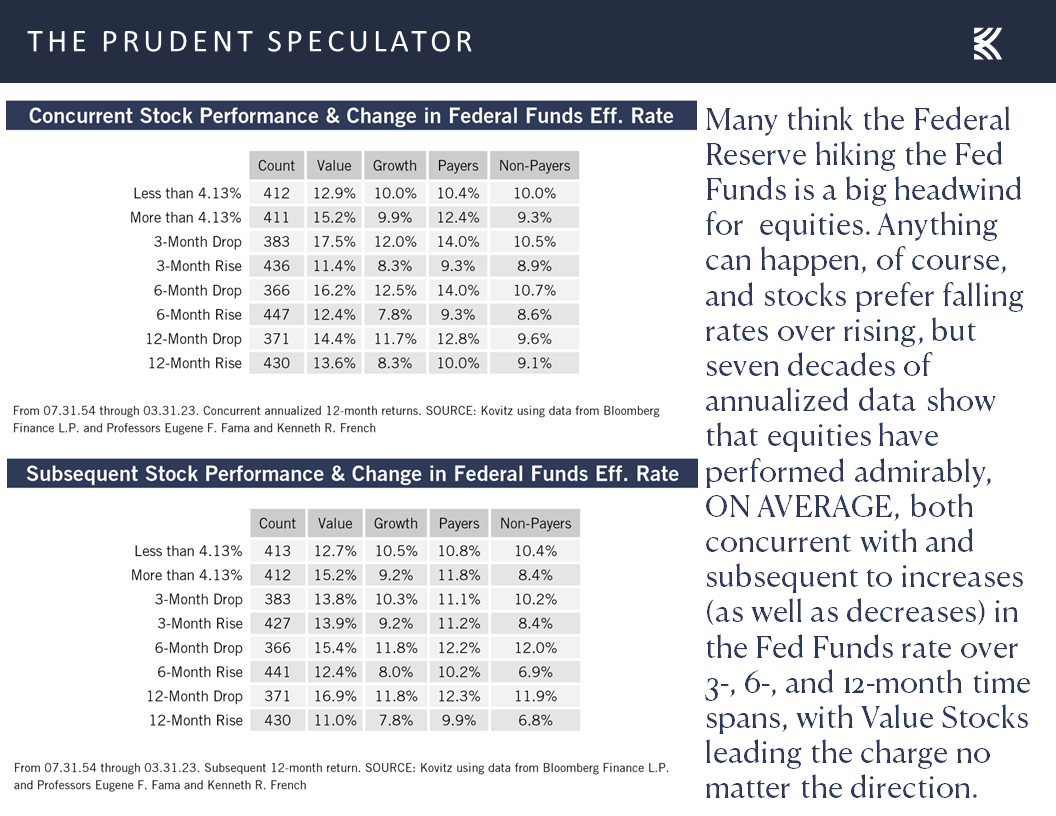

We also note that though the Fed Funds upper bound at 5.5% is modestly above the long-term norm,

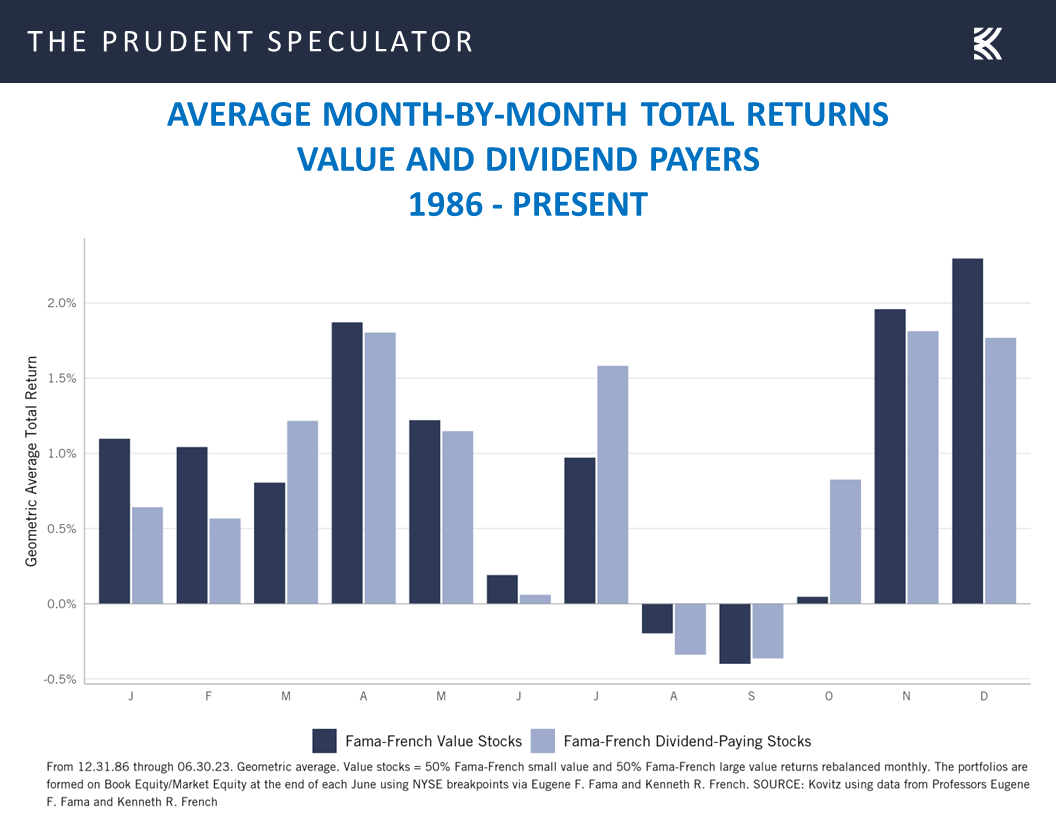

equities have performed well, on average, whether the benchmark is rising or falling. Even more interesting, Value Stocks have actually done better when the Fed Funds rate is above the long-term median than when it is below.

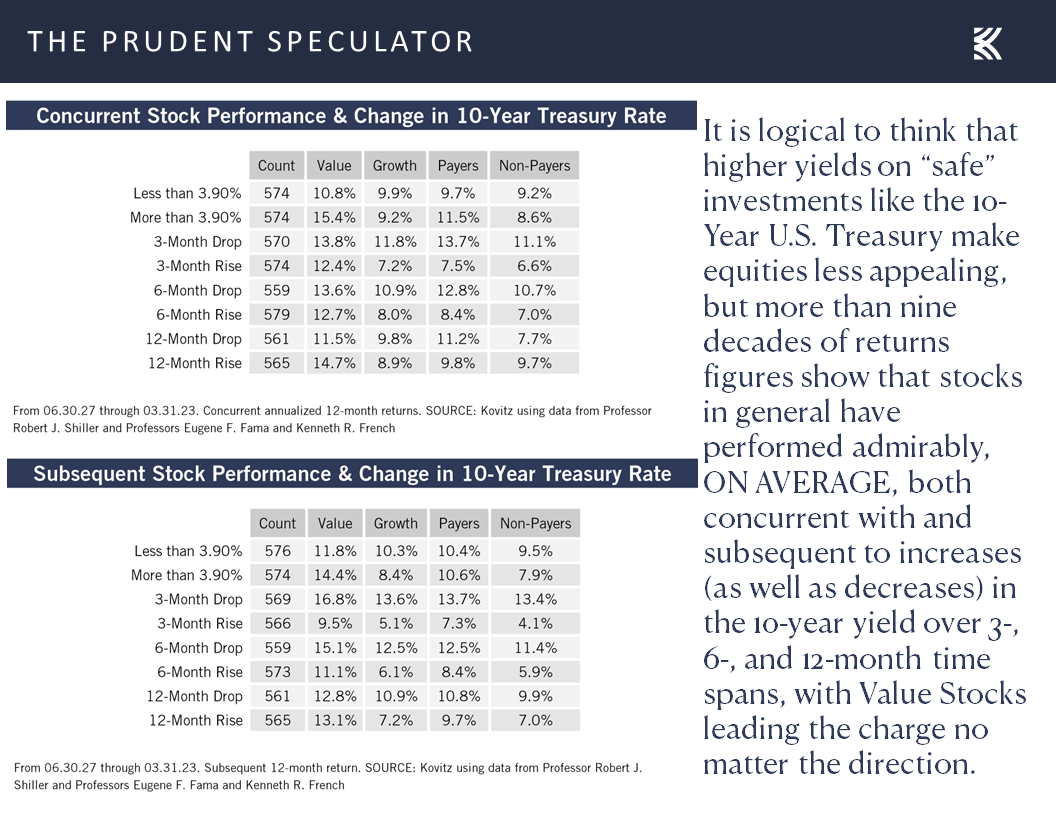

It is a similar story with the yield on the 10-Year U.S. Treasury, with Value not complaining much, on average, about higher government bond rates,

and we note that the current 4.44% yield is not high, believe it or not, relative to the historical average since the launch of The Prudent Speculator in March 1977,

which, in our view, puts the current valuation for Value stocks in the attractive range,

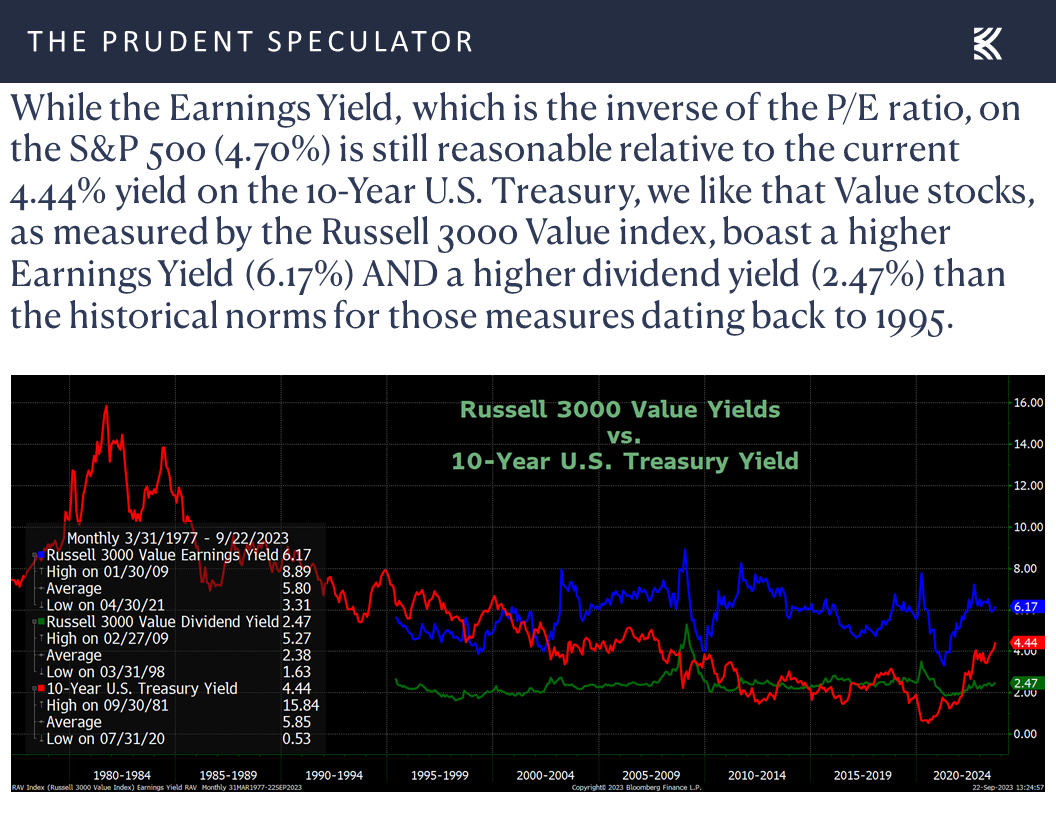

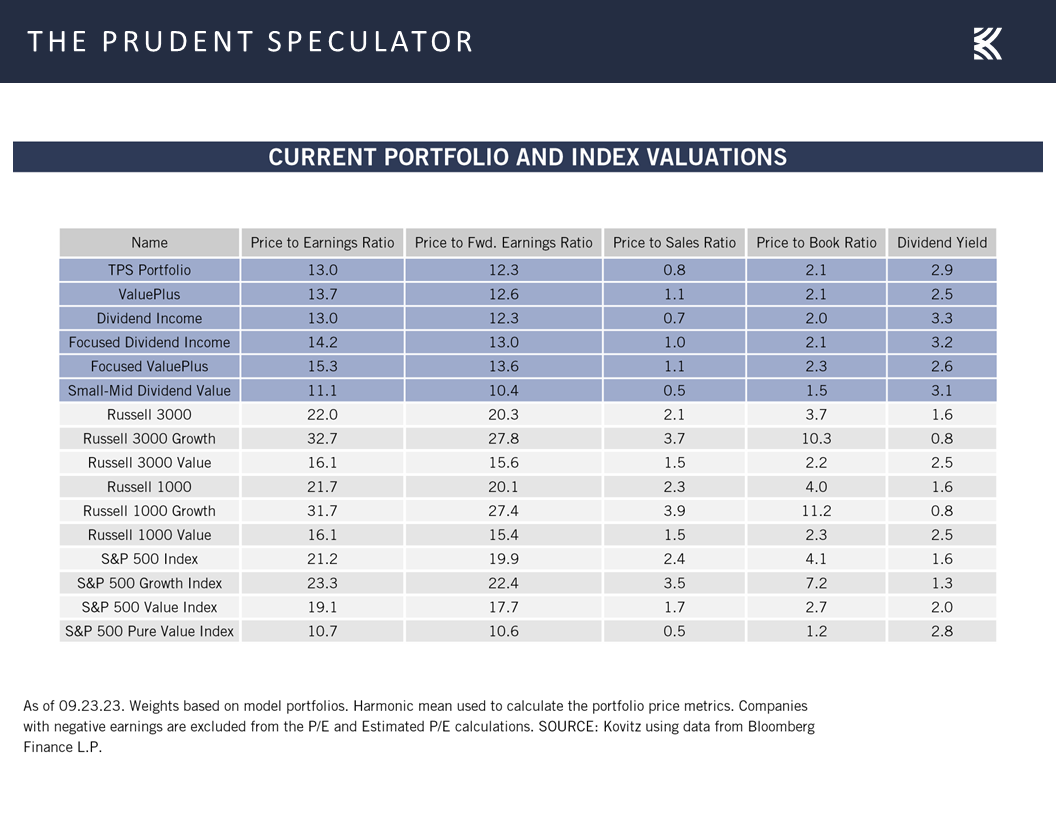

Valuations – Liking the Metrics Associated with our Portfolios

and adds to our enthusiasm for the even-less-expensive price metrics and more-generous dividend yields of our broadly diversified portfolios of what we believe to be undervalued stocks.

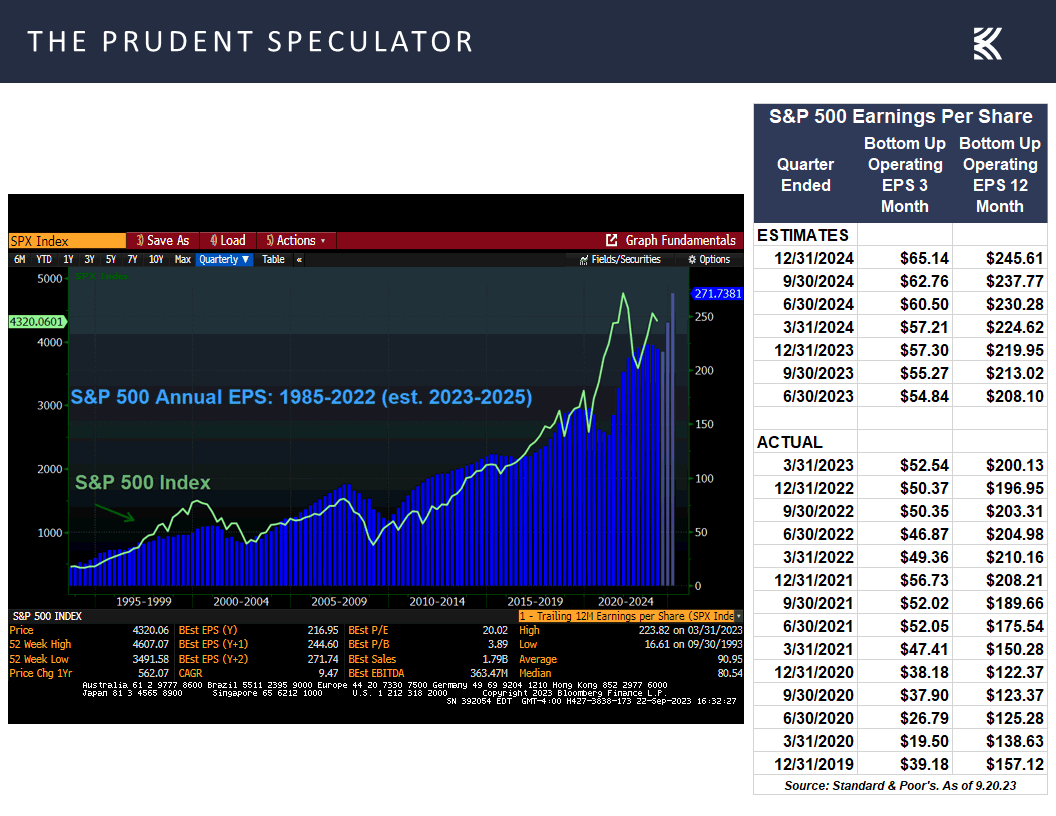

Growth – Corporate Profits, GDP and Dividends Have Increased Over Time

This is especially true, as corporate profits on a bottom-up operating basis are likely to continue to show solid growth this year and next,

given that GDP is still likely to expand nicely on a nominal basis, even if the inflation-adjusted tally eventually suffers a modest contraction.

Patience – The Longer the Hold, the Better the Chance of Beating a 4.43% Annualized Return

And for those who argue that the yield on Treasuries today offers too much competition for stocks, the historical performance numbers show that the odds heavily favor long-term-oriented (and even short-term-focused) investors enjoying a better annualized return on equities,

while those worried about our dividend yields residing only in the 2.5% to 3.3% range can take heart that our experience has been that those payouts have risen year after year.

Uncle Sam – Government Shutdowns Historically a Reason to Buy Stocks

To be sure, anything can happen in the short run and there is plenty about which to be worried, but we’ll close this missive with historical evidence on the latest bogeyman scaring investors: the looming government shutdown. Stocks, as measured by the S&P 500, actually have performed much better than usual, on average, in the 12 months following the prior 20 times Uncle Sam closed for business!

Stock News – Updates on eight stocks across seven different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Stocks, Interest Rates, Uncle Sam and More Economic News

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss stocks, interest rates, Uncle Sam and more Economic News. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

FOMC Meeting – Fed Leaves Interest Rates Unchanged; Higher for Longer?

Week in Review – Bears Maul Goldliocks

Media Flip Flop – Fed Moves Positive One Day and Negative the Next

Econ News – Mixed Set of Numbers Last Week; Solid Q3 Growth Still the Forecast

Interest Rates & Stocks – Rising Fed Funds & 10-Year No Reason to Dump Equities

Valuations – Liking the Metrics Associated with our Portfolios

Growth – Corporate Profits, GDP and Dividends Have Increased Over Time

Patience – The Longer the Hold, the Better the Chance of Beating a 4.43% Annualized Return

Uncle Sam – Government Shutdowns Historically a Reason to Buy Stocks

Stock News – Updates on seven stocks across eight different sectors

FOMC Meeting – Fed Leaves Interest Rates Unchanged; Higher for Longer?

The financial markets are often more volatile than usual during Fed Week, and the aftermath of the September FOMC Meeting continued that trend. Jerome H. Powell & Co. chose to leave their Target for the Fed Funds rate unchanged at a range of 5.25% to 5.50%,

while the Fed Chair offered a relatively upbeat assessment of the economy:

Recent indicators suggest that economic activity has been expanding at a solid pace, and so far this year, growth in real GDP has come in above expectations. Recent readings on consumer spending have been particularly robust. Activity in the housing sector has picked up somewhat, though it remains well below levels of a year ago, largely reflecting higher mortgage rates. Higher interest rates also appear to be weighing on business fixed investment. In our Summary of Economic Projections, or SEP, Committee participants revised up their assessments of real GDP growth, with the median for this year now at 2.1 percent. Participants expect growth to cool, with the median projection falling to 1.5 percent next year.

The latest projections from the Federal Reserve Board members and Federal Reserve Board Bank presidents were an improvement from those offered in June, in which respective real GDP growth this year and next was estimated to be 1.0% and 1.1%.

Interestingly, the lead Fed watcher for The New York Times offered the following positive spin in Thursday’s edition of the newspaper:

Taken together, the projections painted a sunny picture, one in which a robust economy is managing to digest higher borrowing costs without tipping into — or even getting close to — a recession. At the same time, inflation is steadily fading from its rapid pace last year. The combination is giving Fed officials the breathing room they need to be patient, and it is increasing the odds that they might be able to wrangle price increases without inflicting a lot of economic pain.

“It does read very much like a Goldilocks,” said Blerina Uruci, chief U.S. economist at T. Rowe Price. “We’re basically getting a deceleration in inflation with less pain on the economic front.”

Week in Review – Bears Maul Goldliocks

Alas, Goldilocks was seemingly consumed by the Three Bears on Thursday and Friday as stocks endured one of the worst weeks of the year, with the Russell 3000 Value index shedding 2.64% on a price basis, its 135th biggest weekly loss since the inception of that benchmark in 1995.

Media Flip Flop – Fed Moves Positive One Day and Negative the Next

The big selloff in equities prompted a radically different and negative take from the same New York Times columnist in the Friday edition:

The era of ultralow interest rates may be over. At the very least, policymakers don’t expect the type of low borrowing costs that prevailed before the pandemic to return anytime soon.

The Federal Reserve decided this week to leave interest rates unchanged at their highest level in two decades, and left the door open to raising rates again before the end of the year. But an even more significant if subtle change lurked in its freshly released economic projections.

Fed officials do not expect rates to go much higher — the next quarter-point increase is likely to be the last, if they make even that. But they do expect borrowing costs to stay elevated for years to come. Policymakers expect their benchmark short-term interest rate to stay above 5 percent next year, and to end 2025 at nearly 4 percent, the estimates showed. That would be roughly double where they were at the end of 2019.

It was the “higher for longer” view that seemed to cause consternation, as the expectations of the futures market for the year-end 2023 and 2024 Fed Funds rates ticked up last week,

Econ News – Mixed Set of Numbers Last Week; Solid Q3 Growth Still the Forecast

The knee-jerk reaction for fixed-income traders was to dump longer-term government bonds following the FOMC’s decision on interest rates,

with Thursday’s much lower-than-expected weekly tally of 201,000 first-time filings for unemployment benefits adding to worries that the economy might be too strong for the Fed’s taste.

Of course, other economic data out last week was not exactly stellar, with a weaker-than-expected reading on manufacturing in the Philadelphia region,

and disappointing numbers on the state of the housing market,

but the latest projection for real (inflation-adjusted) GDP growth from the Atlanta Fed remained at a very robust 4.9%.

Lest there be worry that folks are starting to see the economic glass as half full, the odds of recession in the next 12 months, as tabulated by Bloomberg, continued to reside at 60%,

while the widely watched Leading Economic Index dropped by 0.4% last month, with the keeper of that metric, The Conference Board, continuing to predict a contraction next year, though their pessimism did diminish somewhat in the group’s latest commentary with the suggestion that the expected recession will be “brief” and “mild.”

Interest Rates & Stocks – Rising Fed Funds & 10-Year No Reason to Dump Equities

As is always the case, we remain braced for additional equity market downside, especially as there are still five-plus trading weeks to go in the seasonally less-favorable time of the year,

but we offer the friendly reminder that stocks have overcome plenty of disconcerting events over the years to go on to post terrific long-term returns.

We also note that though the Fed Funds upper bound at 5.5% is modestly above the long-term norm,

equities have performed well, on average, whether the benchmark is rising or falling. Even more interesting, Value Stocks have actually done better when the Fed Funds rate is above the long-term median than when it is below.

It is a similar story with the yield on the 10-Year U.S. Treasury, with Value not complaining much, on average, about higher government bond rates,

and we note that the current 4.44% yield is not high, believe it or not, relative to the historical average since the launch of The Prudent Speculator in March 1977,

which, in our view, puts the current valuation for Value stocks in the attractive range,

Valuations – Liking the Metrics Associated with our Portfolios

and adds to our enthusiasm for the even-less-expensive price metrics and more-generous dividend yields of our broadly diversified portfolios of what we believe to be undervalued stocks.

Growth – Corporate Profits, GDP and Dividends Have Increased Over Time

This is especially true, as corporate profits on a bottom-up operating basis are likely to continue to show solid growth this year and next,

given that GDP is still likely to expand nicely on a nominal basis, even if the inflation-adjusted tally eventually suffers a modest contraction.

Patience – The Longer the Hold, the Better the Chance of Beating a 4.43% Annualized Return

And for those who argue that the yield on Treasuries today offers too much competition for stocks, the historical performance numbers show that the odds heavily favor long-term-oriented (and even short-term-focused) investors enjoying a better annualized return on equities,

while those worried about our dividend yields residing only in the 2.5% to 3.3% range can take heart that our experience has been that those payouts have risen year after year.

Uncle Sam – Government Shutdowns Historically a Reason to Buy Stocks

To be sure, anything can happen in the short run and there is plenty about which to be worried, but we’ll close this missive with historical evidence on the latest bogeyman scaring investors: the looming government shutdown. Stocks, as measured by the S&P 500, actually have performed much better than usual, on average, in the 12 months following the prior 20 times Uncle Sam closed for business!

Stock News – Updates on eight stocks across seven different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.