The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Federal Reserve, Earnings, Valuations and more Stock News. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Week in Review – Stocks Retreat Again but Value Crushes Growth

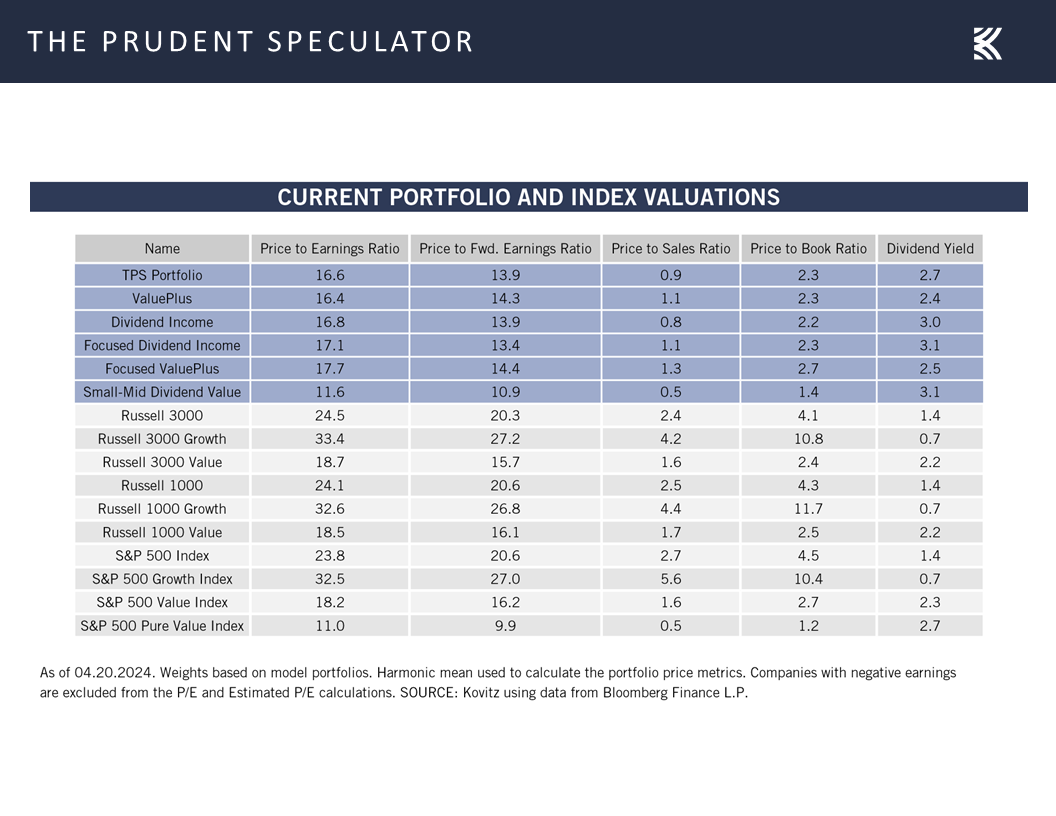

Valuations – Value Reasonably Priced

Sentiment – Bullishness Falls; Bearishness Rises

Headlines – Favorable Economic News; Growth Outlook Improves

Fed Speak – Seemingly Longer Before Rate Cuts

Earnings – Solid Growth Estimated in ’24 & ’25

History – Stocks Haven’t Minded Rising Inflation or Interest Rates, on Average

Stock News – Updates on seventeen stocks across nine different sectors

Week in Review – Stocks Retreat Again but Value Crushes Growth

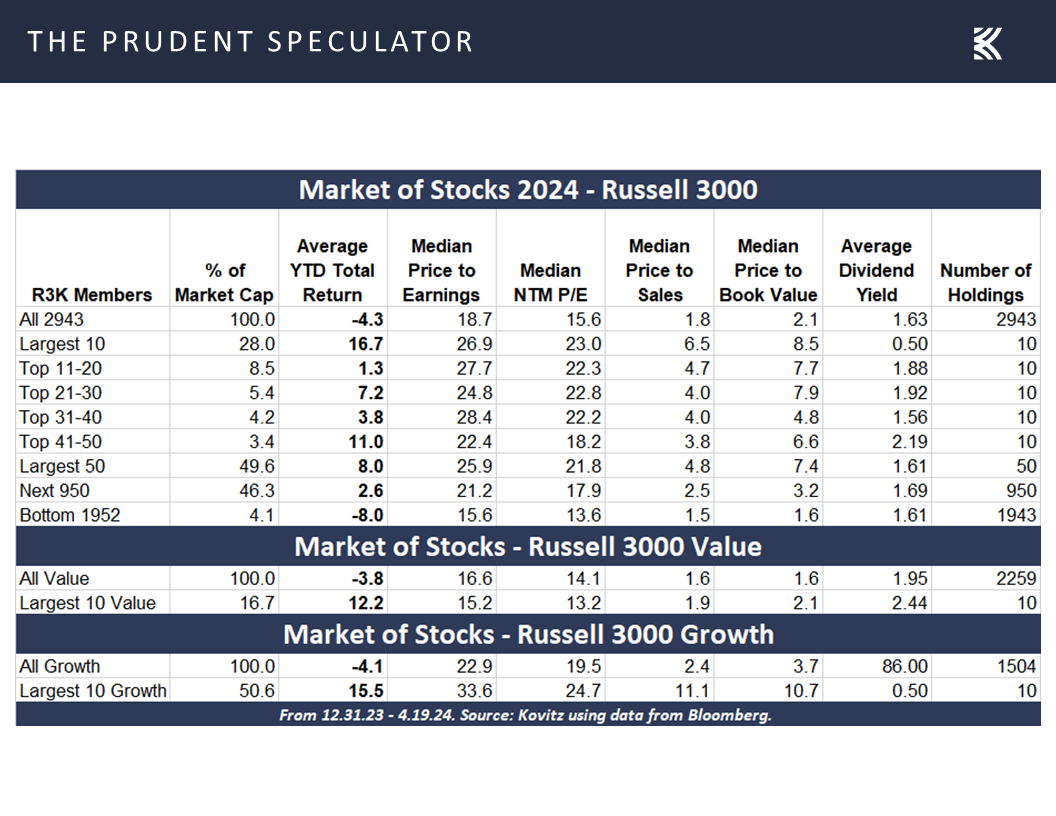

It is difficult to find a lot of cheer in the equity markets over the last five days, given that the average stock in the Russell 3000 index posted a negative total return of 2.4%, pushing the average-stock-return calculation to negative 4.3% for the year.

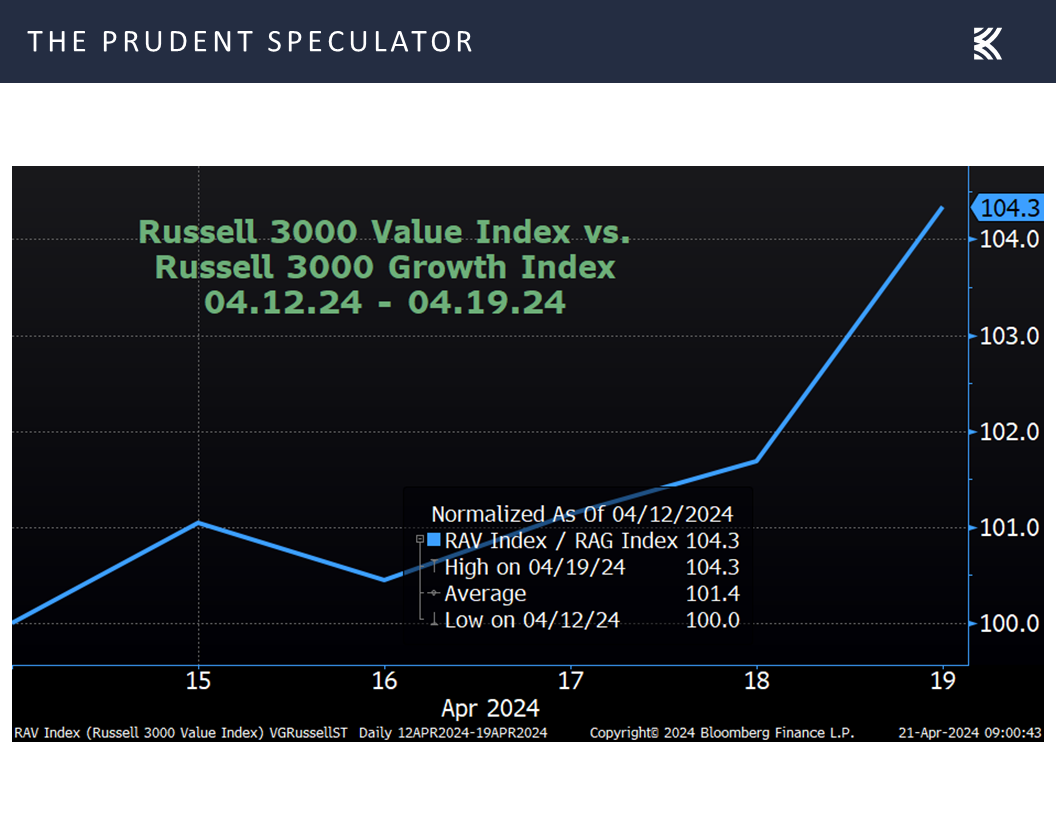

However, we were very happy with how the week ended for Value, especially given where the stock futures were residing on Thursday evening following reports of an Israeli “attack” or “retaliatory strike” (depending on the media outlet) on Iran. True, Value stocks were still in the red for the week, but Friday saw a massive performance advantage for the Russell 3000 Value index over the Russell 3000 Growth index, with the former topping the latter by more than 400 basis points for the full week.

Of course, there is a long way to go (which should excite buyers and owners of inexpensively priced stocks),

and there will be plenty of ups and downs before Value reasserts its historical propensity for outperformance,

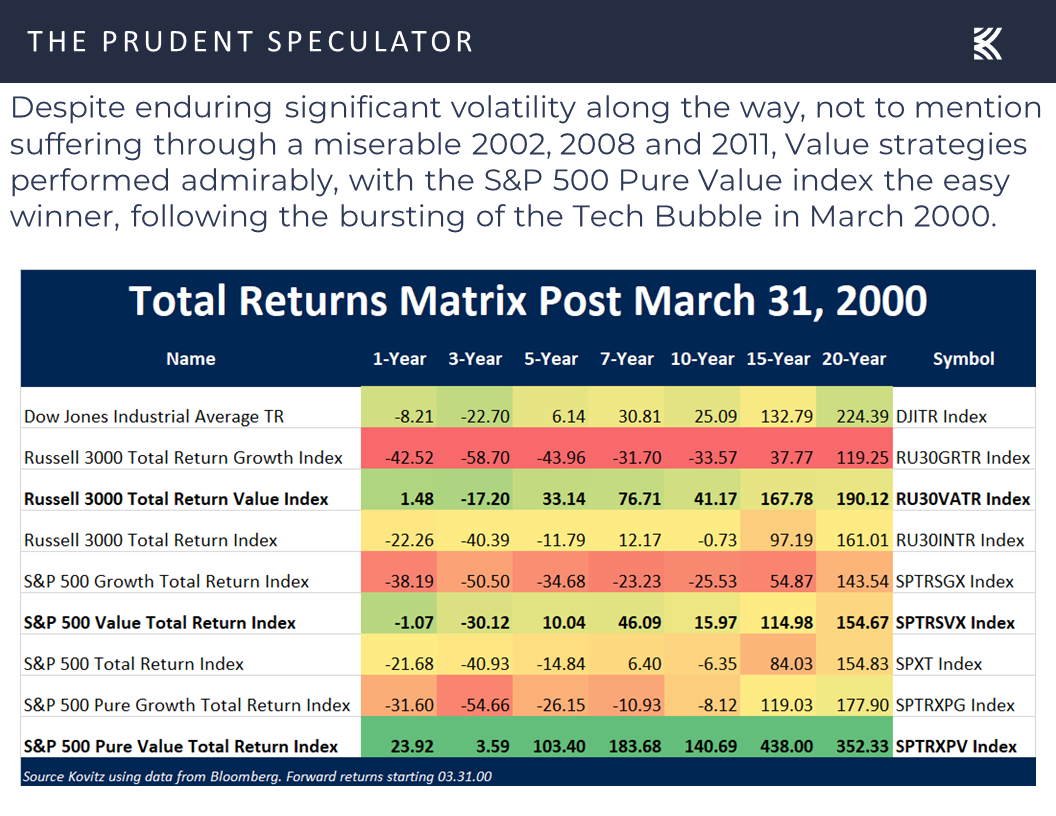

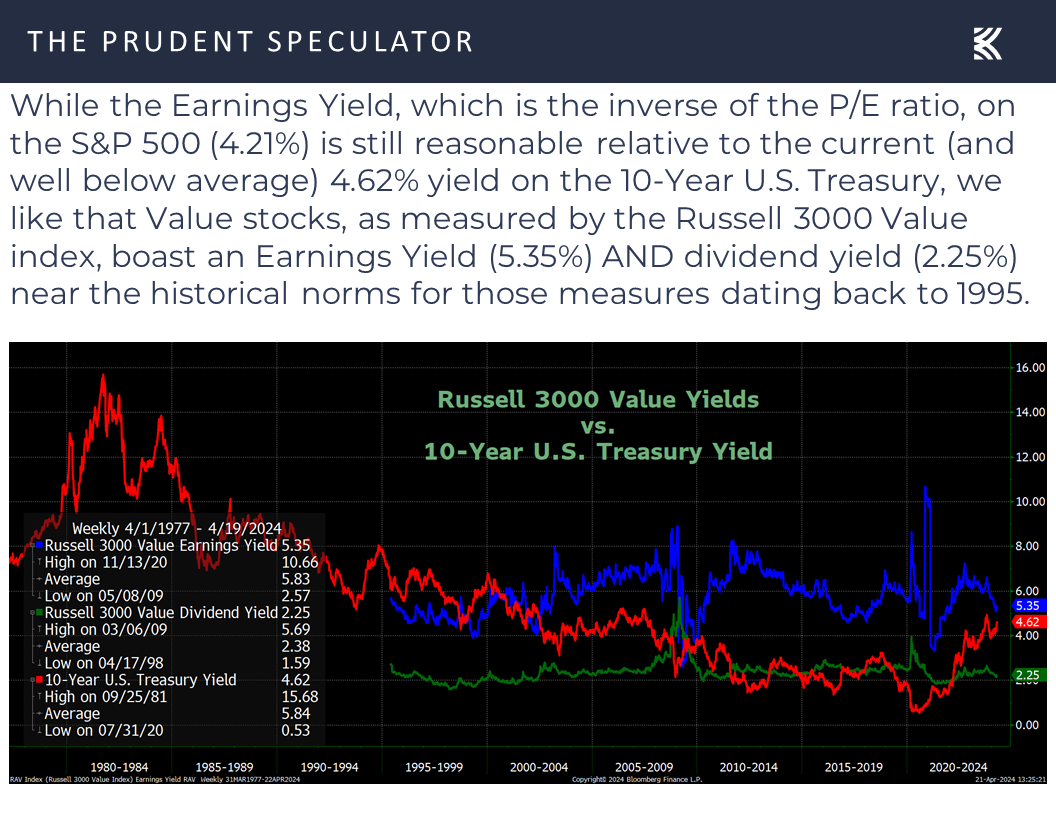

Valuations – Value Reasonably Priced

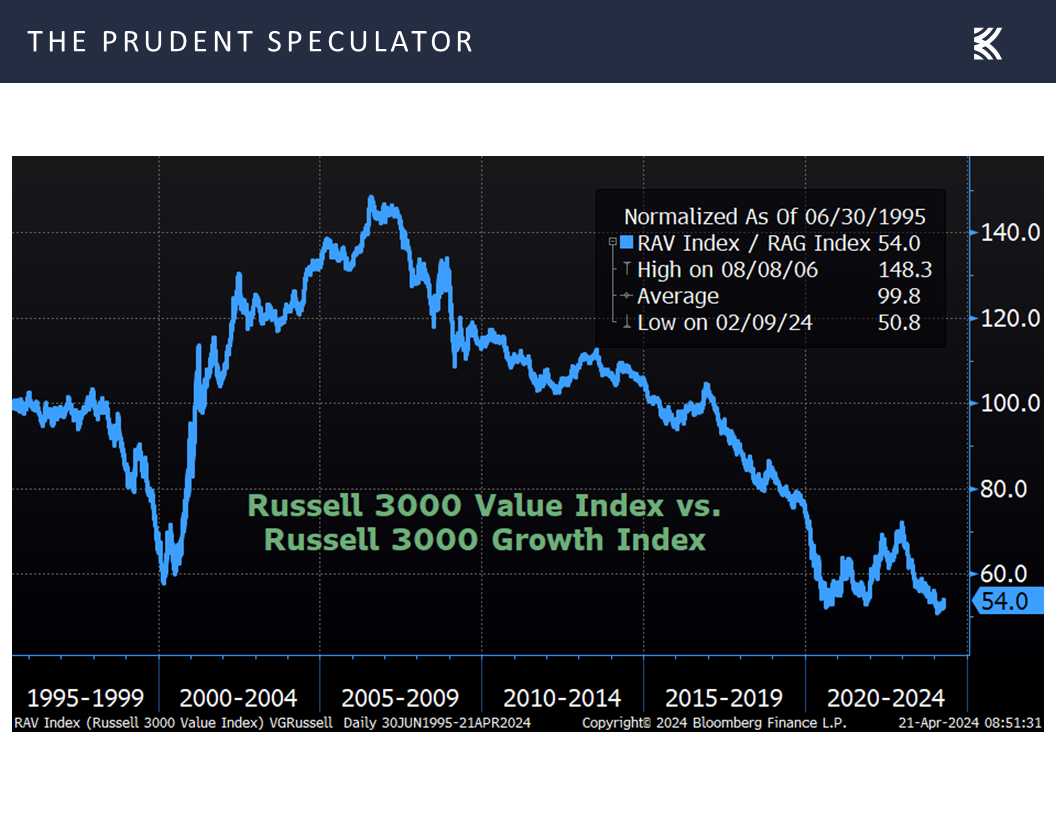

but there is historical precedent for more days like Friday in which Value stocks gain ground, Growth stocks plunge and the major capitalization-weighted market averages are in the red.

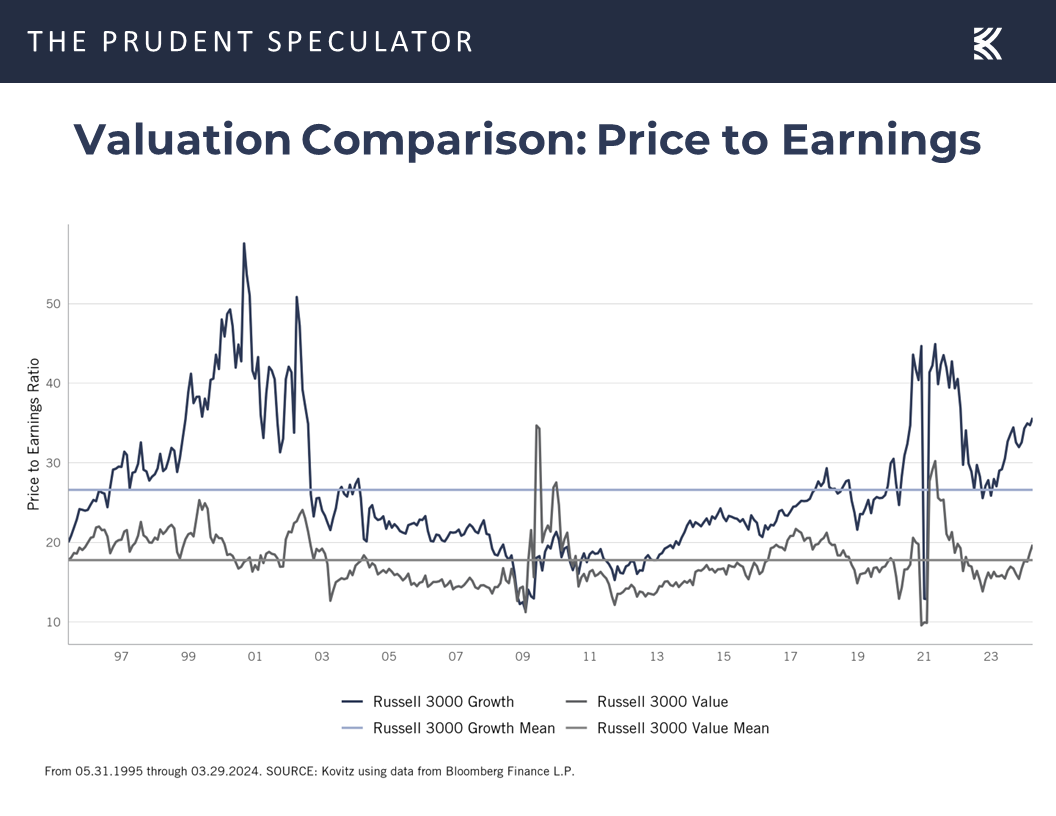

To be sure, today is nothing like the Tech Bubble in terms of ridiculous valuations for many stocks, and we own more than a few reasonably priced companies that reside in the Russell 3000 Growth index, but we note that Value stocks are much closer than Growth to their historical means on a P/E basis,

and we sleep very well at night with the inexpensive price metrics and generous dividend yields on our broadly diversified portfolios of what we believe are undervalued stocks.

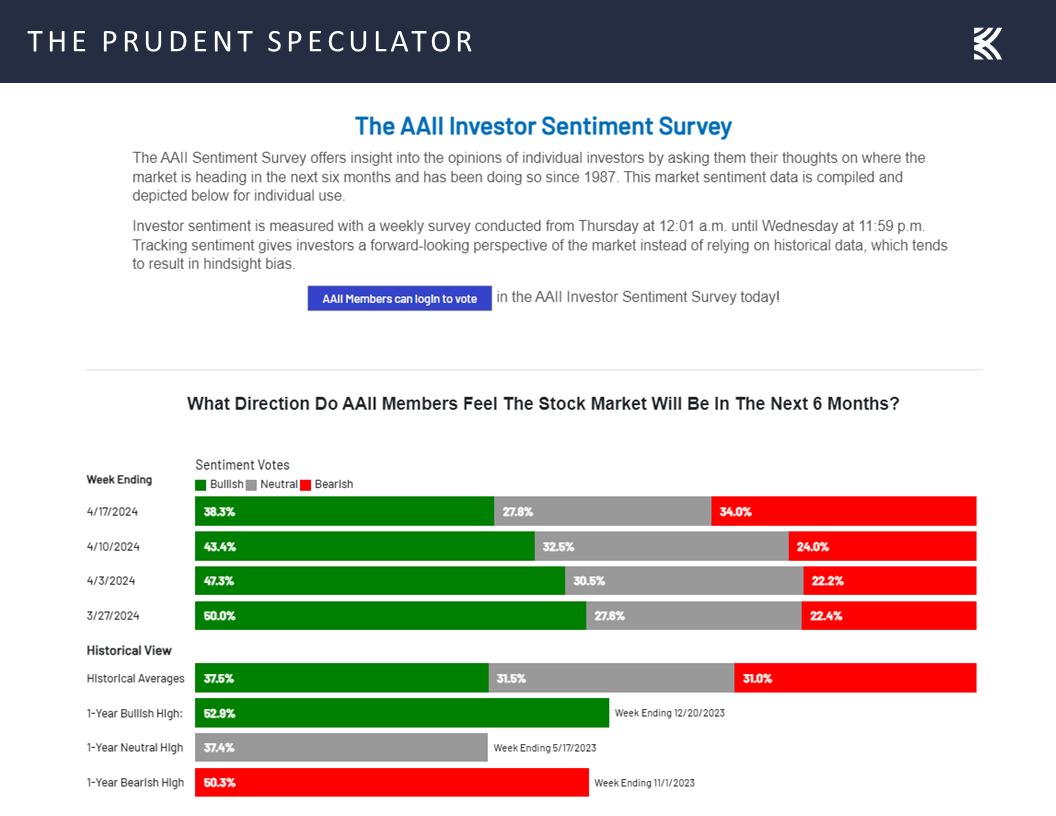

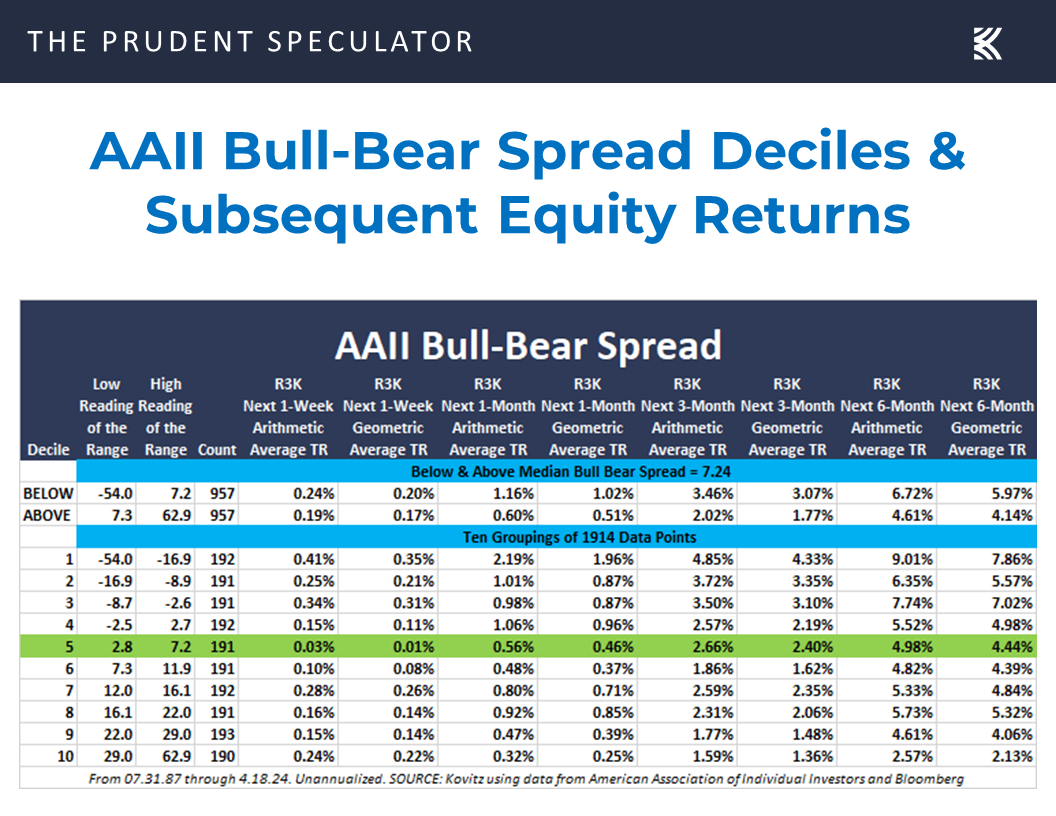

Sentiment – Bullishness Falls; Bearishness Rises

Aside from the modestly lower prices for many of our stocks today versus a week ago and a significant drop in Bullishness and rise in Bearishness from the American Association of Individual Investors (AAII),

which generally is a contrarian positive,

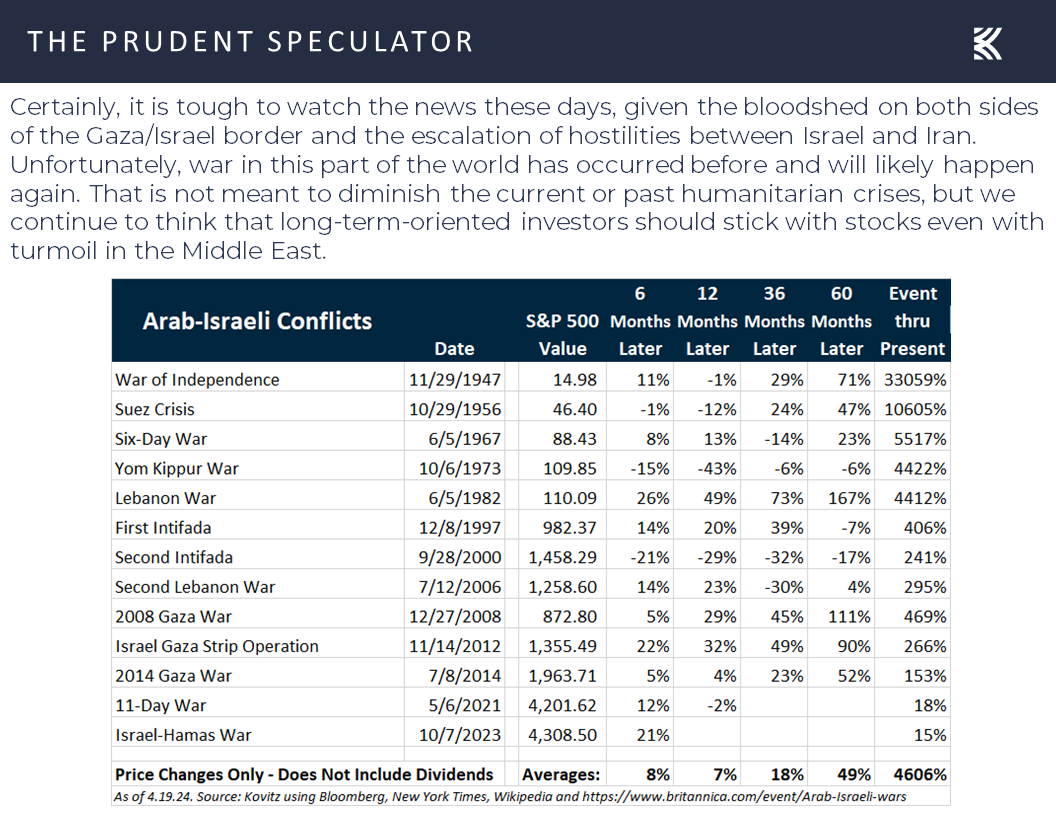

Headlines – Favorable Economic News; Growth Outlook Improves

we might argue that we should be even more optimistic about the long-term prospects for equities. The Middle East seems to have escaped a major escalation cycle for the moment at least,

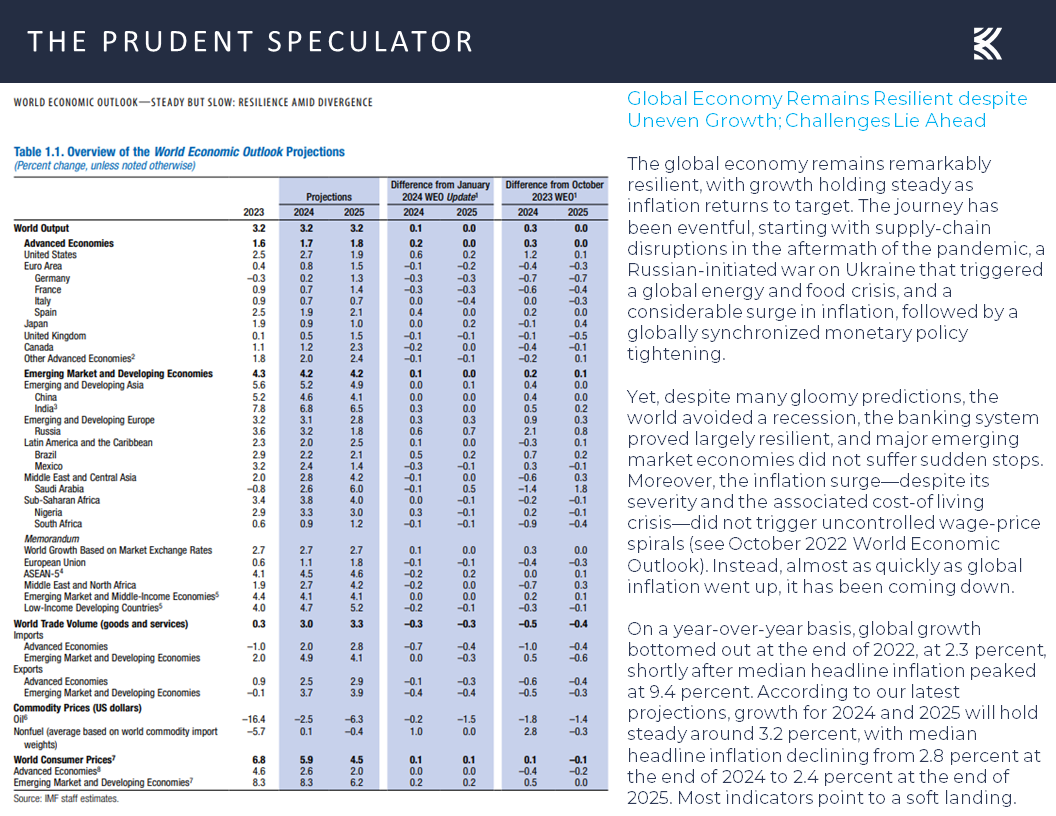

and the economic headlines globally and domestically last week were favorable,

with the International Monetary Fund (IMF) boosting its outlook for U.S. GDP Growth since its January World Economic Outlook by six-tenths of a percent this year and two-tenths of a percent for 2025.

Yes, the IMF was quick to add, “The forecast for global growth five years from now—at 3.1 percent—is at its lowest in decades,” but the group also stated, “Global inflation is forecast to decline steadily, from 6.8 percent in 2023 to 5.9 percent in 2024 and 4.5 percent in 2025, with advanced economies returning to their inflation targets sooner than emerging market and developing economies.”

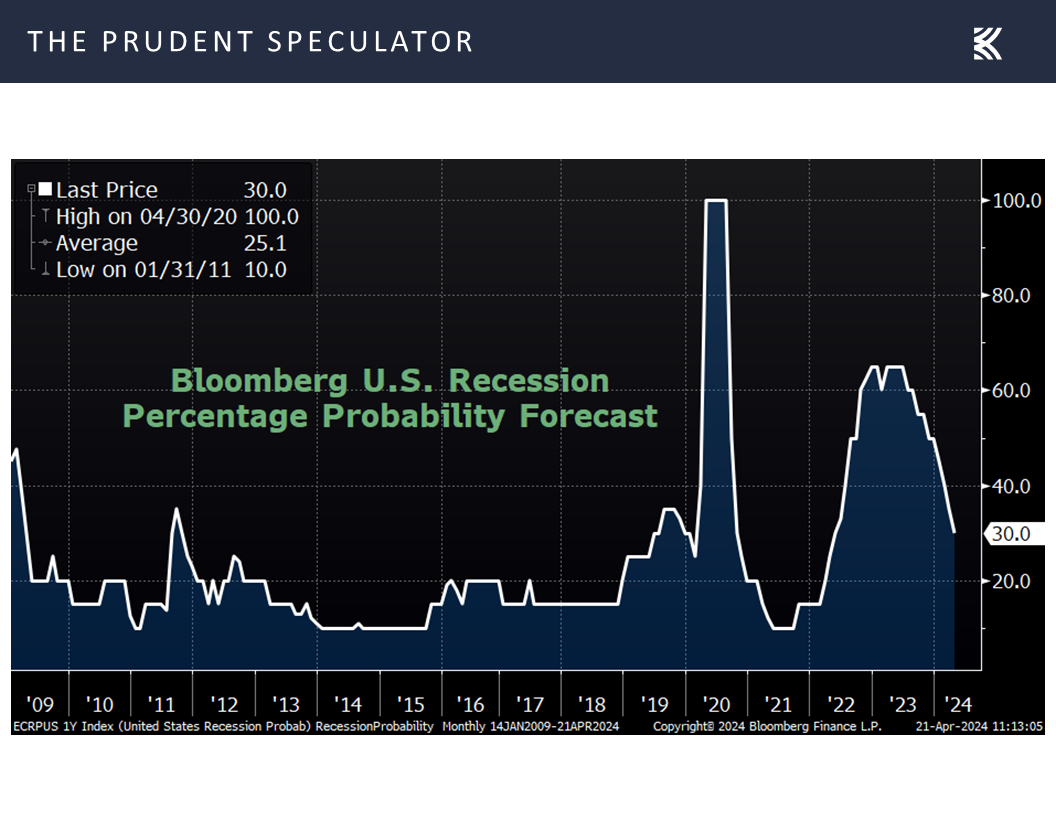

And here at home, the latest estimate for Q1 real (inflation-adjusted) U.S. GDP growth from the Atlanta Fed rose to 2.9% last week, up from 2.4% the week prior,

while the odds of recession in the next 12 months declined to 30% as compared to 35% a week ago, per calculations from data provider Bloomberg.

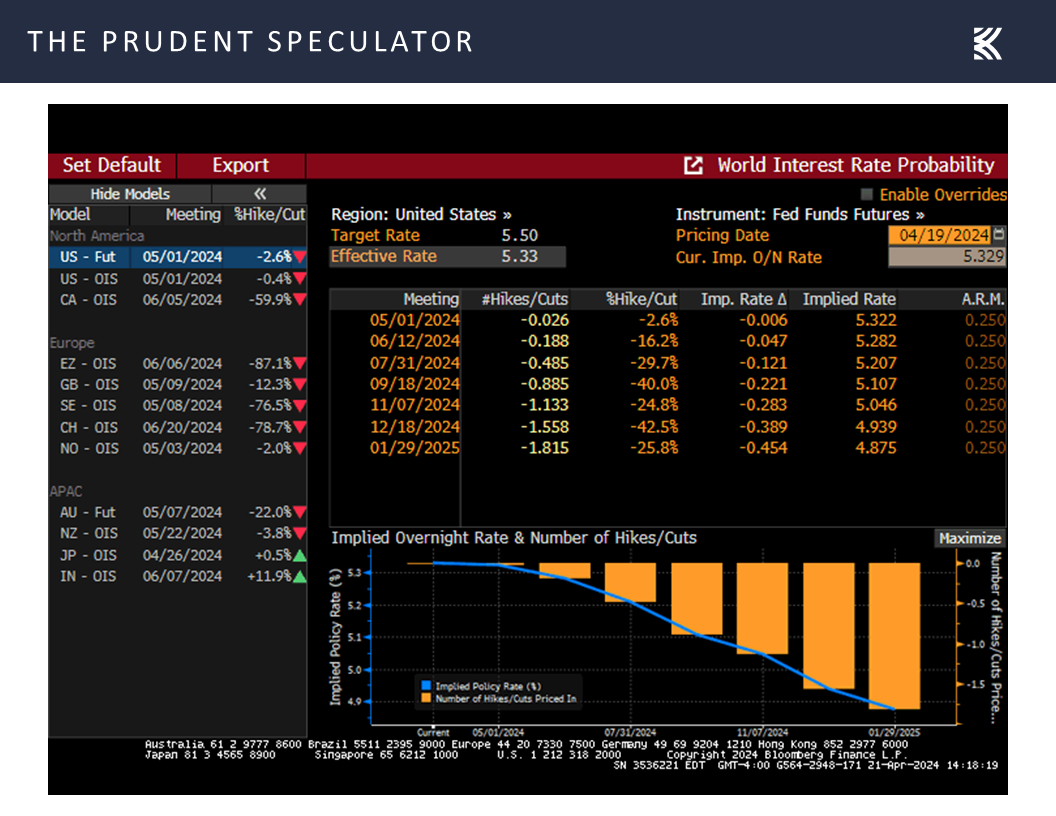

Fed Speak – Seemingly Longer Before Rate Cuts

We realize that some traders view good economic news as bad news, given that it might mean that Federal Reserve Chair Jerome H. Powell and his colleagues will be less likely to cut interest rates in the near term, with The Associated Press reporting last week,

Mr. Powell said at an event on Tuesday that the central bank has been waiting to cut its main interest rate, which is at the highest level since 2001, because it first needs more confidence that inflation is heading sustainably down to its 2 percent target.

The recent data have clearly not given us great confidence and instead indicate that it’s likely to take longer than expected to achieve that confidence,” he said, referring to a string of reports this year that showed inflation remaining hotter than forecast.

He suggested that if higher inflation does persist, the Fed will hold rates steady “for as long as needed.” But he also acknowledged that the Fed could cut rates if the job market unexpectedly weakens.

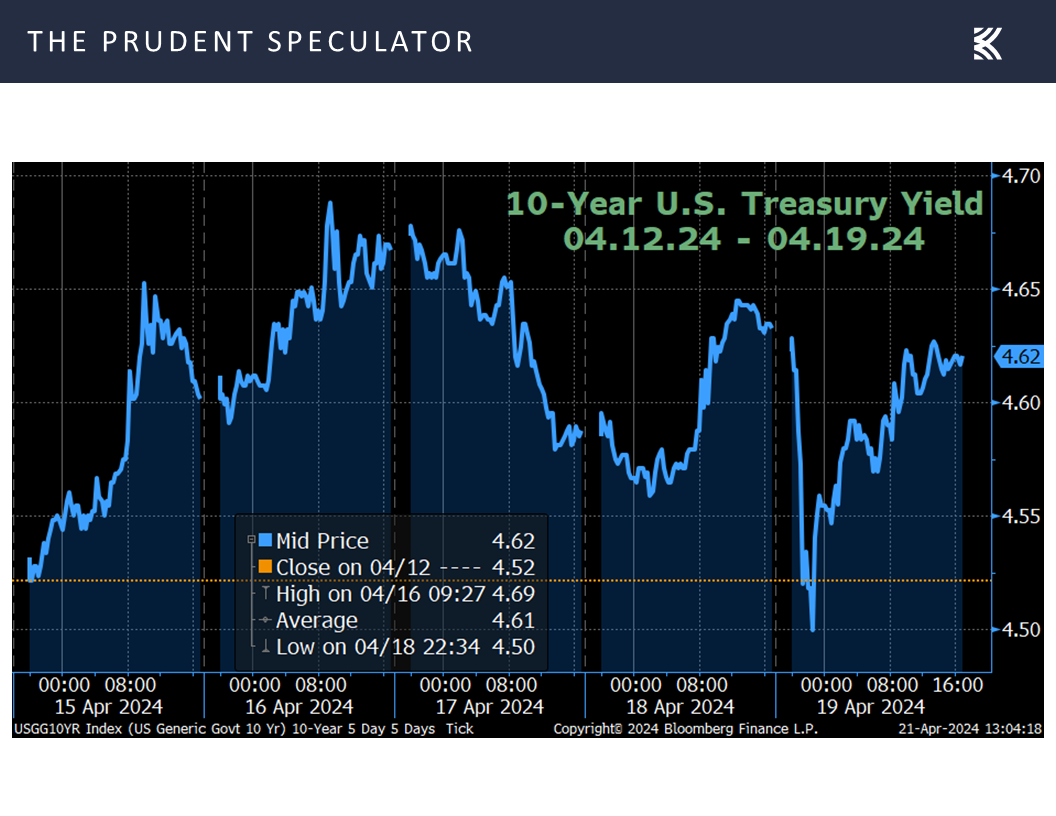

True, Mr. Powell concluded, “Right now, given the strength of the labor market and progress on inflation so far, it’s appropriate to allow restrictive policy further time to work and let the data and evolving outlook guide us,” which compelled bettors in the futures market to raise their wagers last week for the year-end Fed Funds rate to 4.94%, up from 4.86% seven days earlier,

and pushed the yield on the benchmark U.S. government bond up to 4.62% from 4.52%.

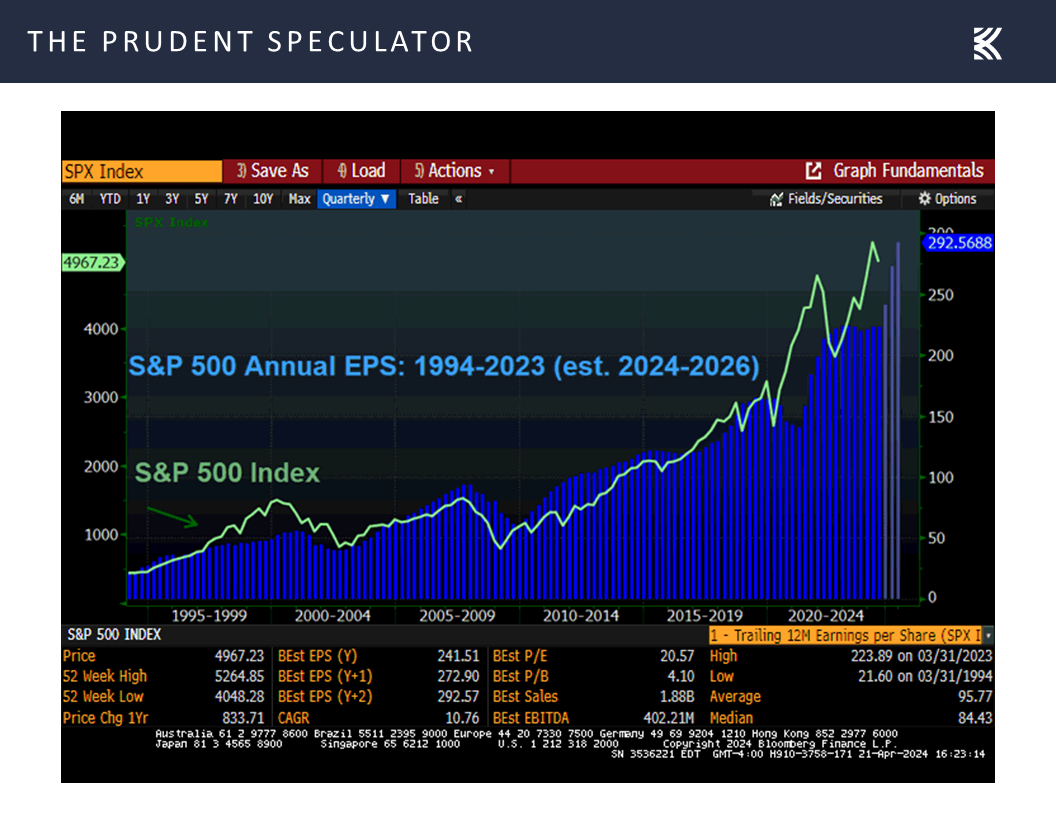

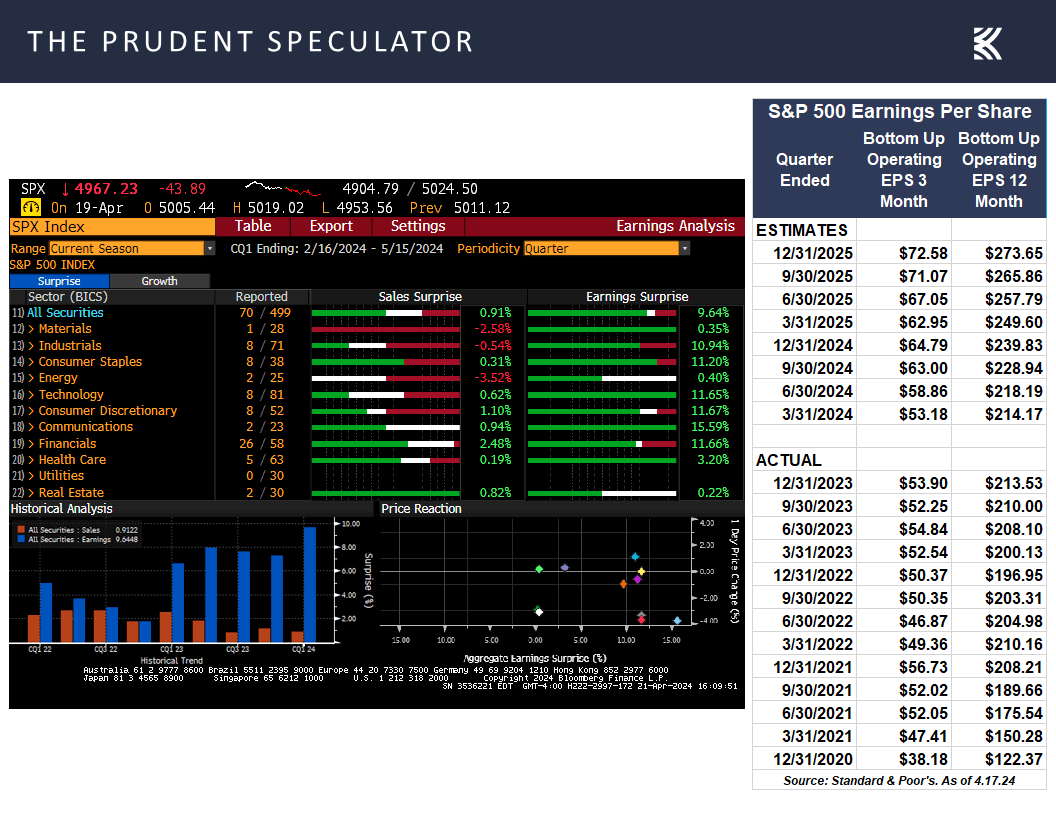

Earnings – Solid Growth Estimated in ’24 & ’25

but we prefer a solid economic backdrop rather than one in need of Fed support. After all, stock prices historically have followed earnings,

and we are investing in businesses that we expect to grow their bottom lines over time,

so even if the reasonable P/E ratio (or in the chart below, the Earnings to Price ratio) today for the kind of stocks we have long advocated does not rise (decline), the growth in profits over time mathematically would have to lead to higher stock prices.

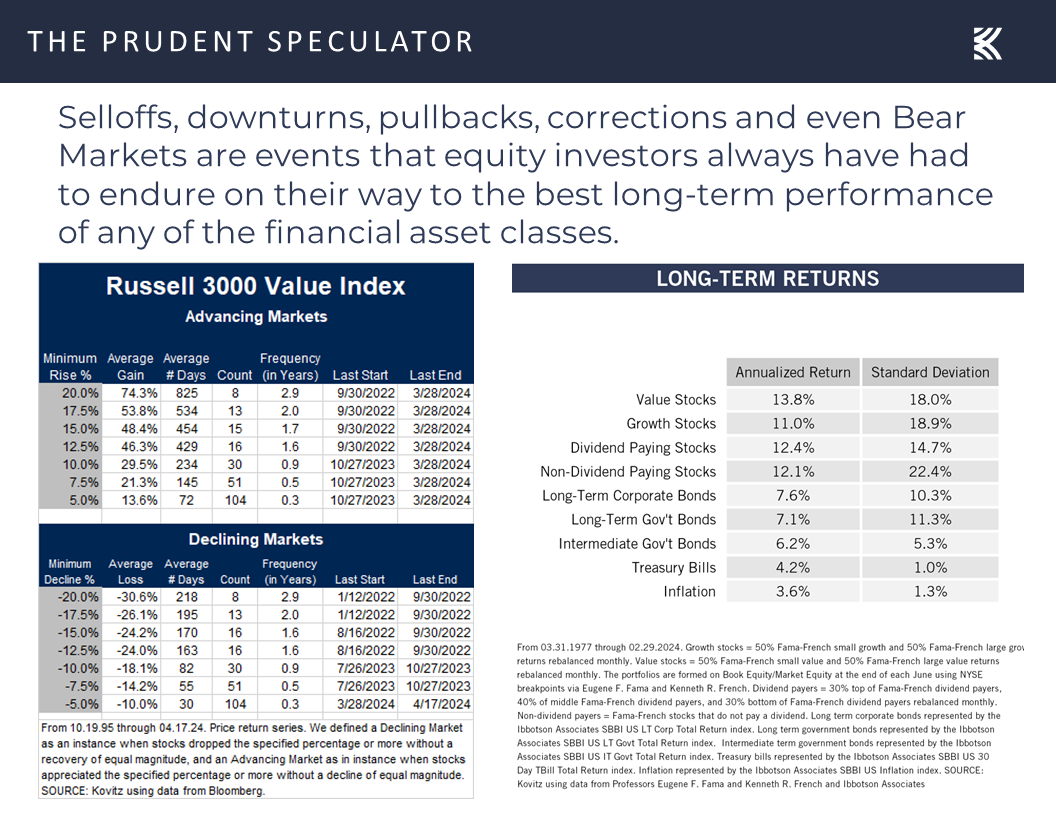

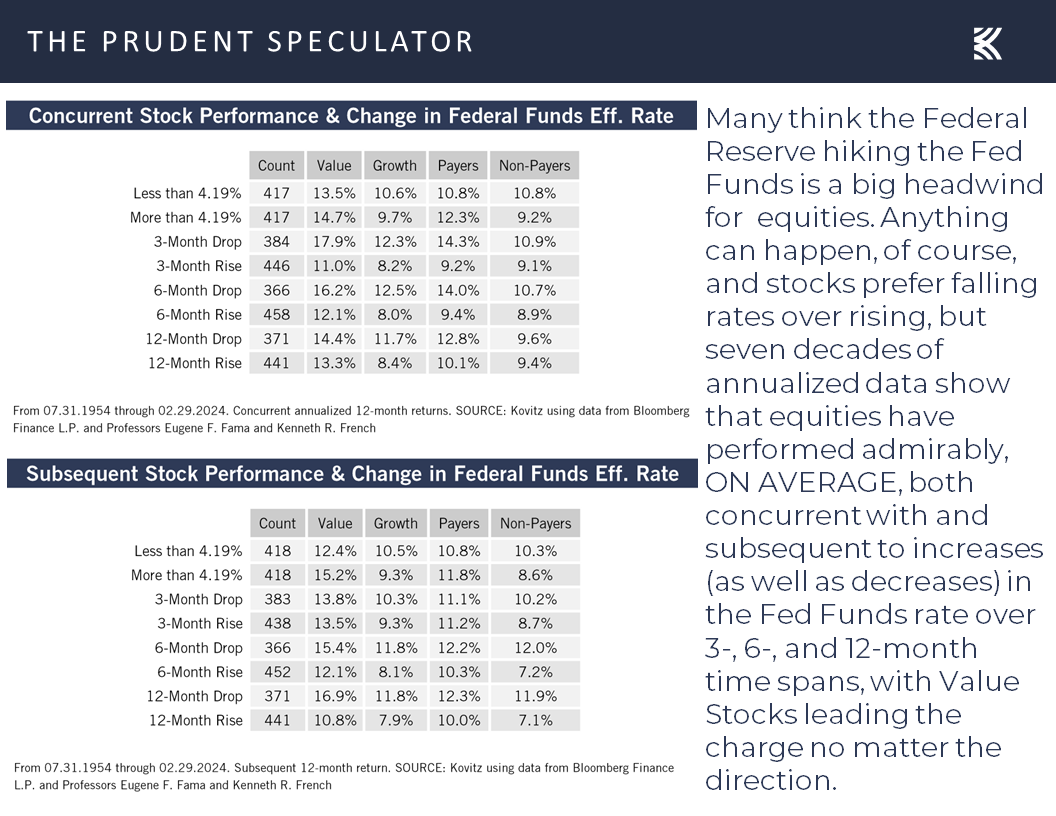

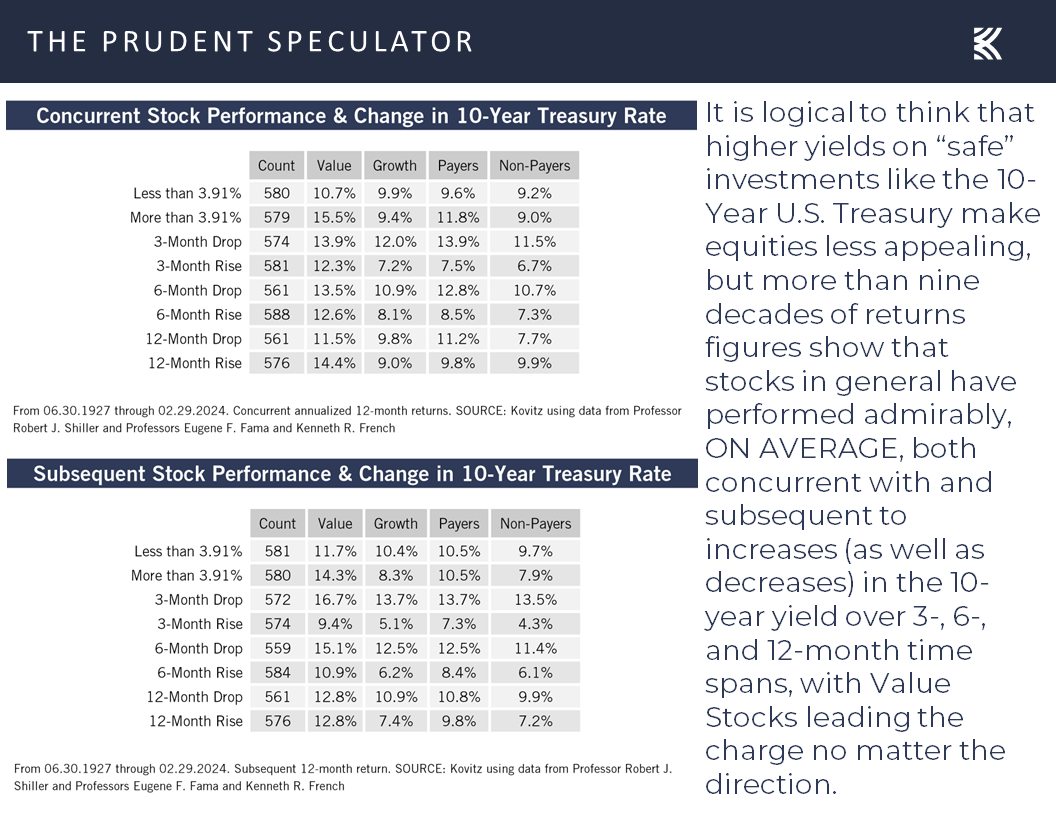

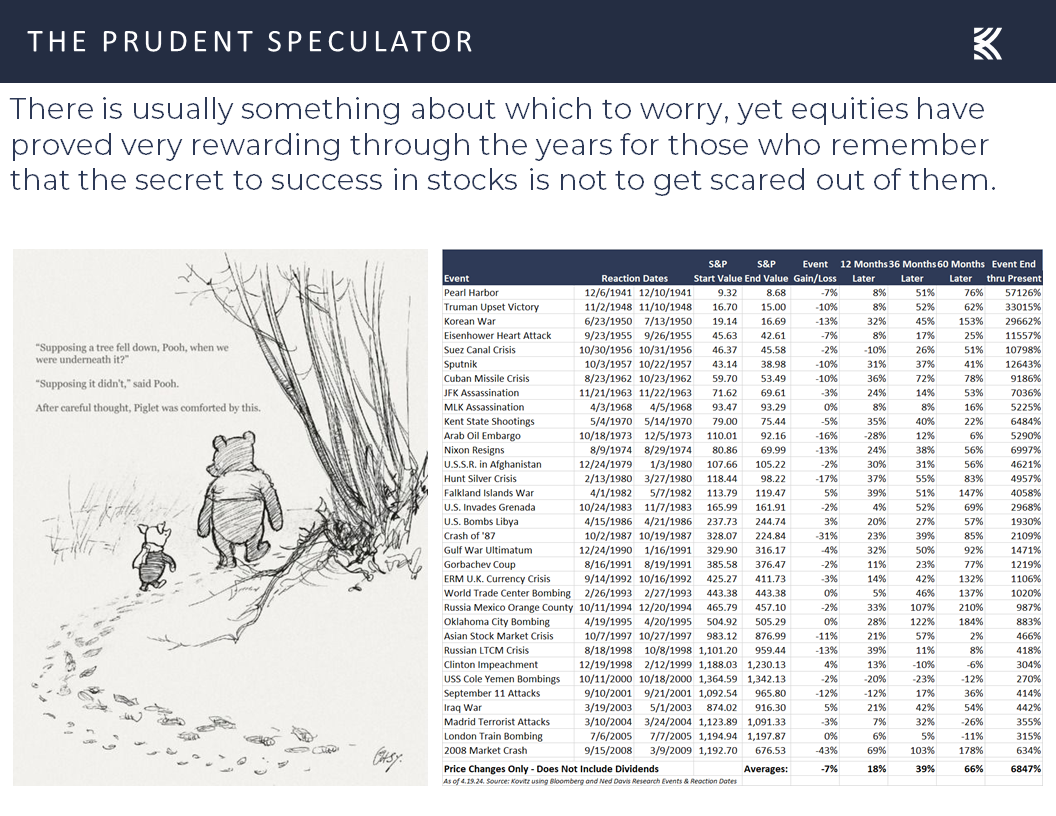

History – Stocks Haven’t Minded Rising Inflation or Interest Rates, on Average

Further, we offer the reminder that stocks have, on average, performed fine whether the Fed Funds rate is rising or falling, or whether it is high or low, with Value Stocks winning all the returns races,

with the same also true whether the yield on the 10-Year U.S. Treasury is moving up or down, or whether that yield is above or below the historical median.

with the same also true whether the yield on the 10-Year U.S. Treasury is moving up or down, or whether that yield is above or below the historical median.

Stock News – Updates on seventeen stocks across nine different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

The Federal Reserve, Earnings, Valuations and more Stock News

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Federal Reserve, Earnings, Valuations and more Stock News. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Week in Review – Stocks Retreat Again but Value Crushes Growth

Valuations – Value Reasonably Priced

Sentiment – Bullishness Falls; Bearishness Rises

Headlines – Favorable Economic News; Growth Outlook Improves

Fed Speak – Seemingly Longer Before Rate Cuts

Earnings – Solid Growth Estimated in ’24 & ’25

History – Stocks Haven’t Minded Rising Inflation or Interest Rates, on Average

Stock News – Updates on seventeen stocks across nine different sectors

Week in Review – Stocks Retreat Again but Value Crushes Growth

It is difficult to find a lot of cheer in the equity markets over the last five days, given that the average stock in the Russell 3000 index posted a negative total return of 2.4%, pushing the average-stock-return calculation to negative 4.3% for the year.

However, we were very happy with how the week ended for Value, especially given where the stock futures were residing on Thursday evening following reports of an Israeli “attack” or “retaliatory strike” (depending on the media outlet) on Iran. True, Value stocks were still in the red for the week, but Friday saw a massive performance advantage for the Russell 3000 Value index over the Russell 3000 Growth index, with the former topping the latter by more than 400 basis points for the full week.

Of course, there is a long way to go (which should excite buyers and owners of inexpensively priced stocks),

and there will be plenty of ups and downs before Value reasserts its historical propensity for outperformance,

Valuations – Value Reasonably Priced

but there is historical precedent for more days like Friday in which Value stocks gain ground, Growth stocks plunge and the major capitalization-weighted market averages are in the red.

To be sure, today is nothing like the Tech Bubble in terms of ridiculous valuations for many stocks, and we own more than a few reasonably priced companies that reside in the Russell 3000 Growth index, but we note that Value stocks are much closer than Growth to their historical means on a P/E basis,

and we sleep very well at night with the inexpensive price metrics and generous dividend yields on our broadly diversified portfolios of what we believe are undervalued stocks.

Sentiment – Bullishness Falls; Bearishness Rises

Aside from the modestly lower prices for many of our stocks today versus a week ago and a significant drop in Bullishness and rise in Bearishness from the American Association of Individual Investors (AAII),

which generally is a contrarian positive,

Headlines – Favorable Economic News; Growth Outlook Improves

we might argue that we should be even more optimistic about the long-term prospects for equities. The Middle East seems to have escaped a major escalation cycle for the moment at least,

and the economic headlines globally and domestically last week were favorable,

with the International Monetary Fund (IMF) boosting its outlook for U.S. GDP Growth since its January World Economic Outlook by six-tenths of a percent this year and two-tenths of a percent for 2025.

Yes, the IMF was quick to add, “The forecast for global growth five years from now—at 3.1 percent—is at its lowest in decades,” but the group also stated, “Global inflation is forecast to decline steadily, from 6.8 percent in 2023 to 5.9 percent in 2024 and 4.5 percent in 2025, with advanced economies returning to their inflation targets sooner than emerging market and developing economies.”

And here at home, the latest estimate for Q1 real (inflation-adjusted) U.S. GDP growth from the Atlanta Fed rose to 2.9% last week, up from 2.4% the week prior,

while the odds of recession in the next 12 months declined to 30% as compared to 35% a week ago, per calculations from data provider Bloomberg.

Fed Speak – Seemingly Longer Before Rate Cuts

We realize that some traders view good economic news as bad news, given that it might mean that Federal Reserve Chair Jerome H. Powell and his colleagues will be less likely to cut interest rates in the near term, with The Associated Press reporting last week,

Mr. Powell said at an event on Tuesday that the central bank has been waiting to cut its main interest rate, which is at the highest level since 2001, because it first needs more confidence that inflation is heading sustainably down to its 2 percent target.

The recent data have clearly not given us great confidence and instead indicate that it’s likely to take longer than expected to achieve that confidence,” he said, referring to a string of reports this year that showed inflation remaining hotter than forecast.

He suggested that if higher inflation does persist, the Fed will hold rates steady “for as long as needed.” But he also acknowledged that the Fed could cut rates if the job market unexpectedly weakens.

True, Mr. Powell concluded, “Right now, given the strength of the labor market and progress on inflation so far, it’s appropriate to allow restrictive policy further time to work and let the data and evolving outlook guide us,” which compelled bettors in the futures market to raise their wagers last week for the year-end Fed Funds rate to 4.94%, up from 4.86% seven days earlier,

and pushed the yield on the benchmark U.S. government bond up to 4.62% from 4.52%.

Earnings – Solid Growth Estimated in ’24 & ’25

but we prefer a solid economic backdrop rather than one in need of Fed support. After all, stock prices historically have followed earnings,

and we are investing in businesses that we expect to grow their bottom lines over time,

so even if the reasonable P/E ratio (or in the chart below, the Earnings to Price ratio) today for the kind of stocks we have long advocated does not rise (decline), the growth in profits over time mathematically would have to lead to higher stock prices.

History – Stocks Haven’t Minded Rising Inflation or Interest Rates, on Average

Further, we offer the reminder that stocks have, on average, performed fine whether the Fed Funds rate is rising or falling, or whether it is high or low, with Value Stocks winning all the returns races,

with the same also true whether the yield on the 10-Year U.S. Treasury is moving up or down, or whether that yield is above or below the historical median.

with the same also true whether the yield on the 10-Year U.S. Treasury is moving up or down, or whether that yield is above or below the historical median.

Stock News – Updates on seventeen stocks across nine different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.