The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Value Stocks, Federal Reserve Projections, Earnings and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Market Breadth – A Handful of Mega Caps Up but Most Stocks Down Last Week; Average Stock Down on the Year

Value – Tech Bubble History Lesson; R3K Value Index Very Inexpensive Relative to R3K Growth

Inflation – Lower-than-Expected CPI & PPI

Fed Econ Projections – 1 Rate Cut This Year; 4 Cuts Next Year

Interest Rates – Lower 10-Year Yield & Lower Expected Year-End Fed Funds Rate vs. the Prior Week

Econ News – Mixed Data; Fed & World Bank Each Projecting Decent U.S. Growth for ’24 and ’25

Earnings – Solid Growth Estimated in ’24 & ’25

Volatility – Scary Headlines & Plenty of Gyrations Along the Way but Long-Term Trend is Up

Stock News – Updates on AAPL, ORCL, AVGO, GM & ZBH

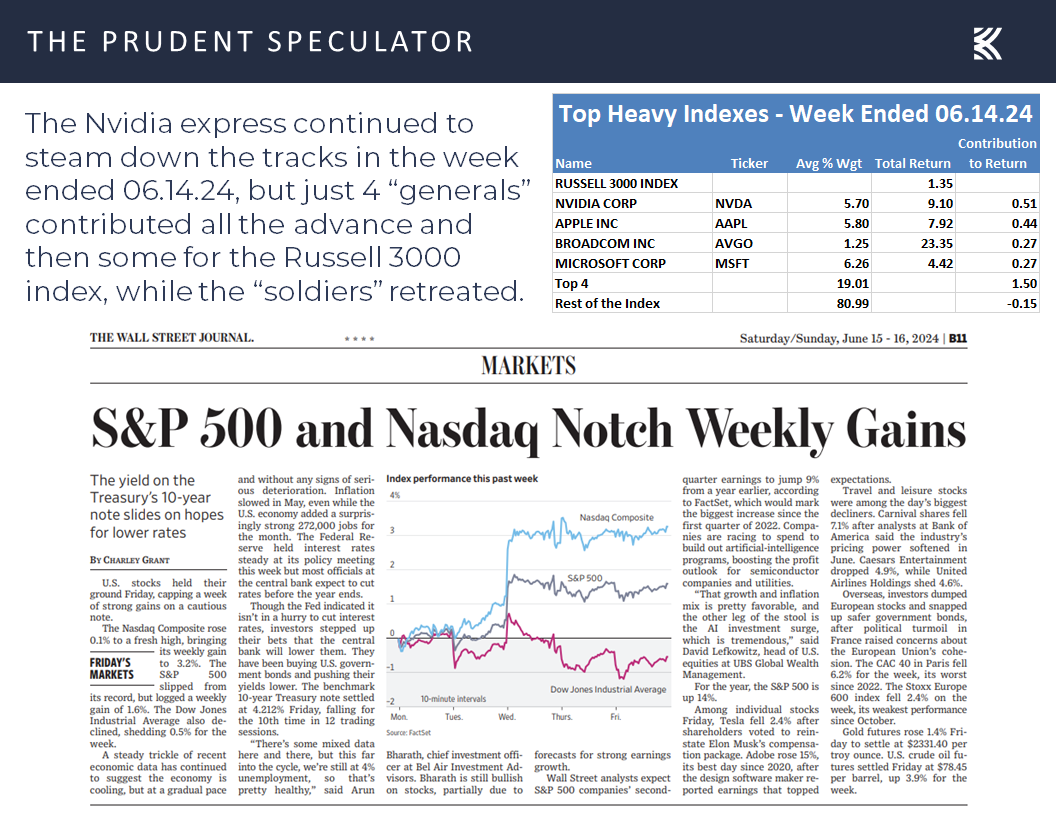

Market Breadth – A Handful of Mega Caps Up but Most Stocks Down Last Week; Average Stock Down on the Year

The average member of the Russell 3000 index lost 1.26% last week, the New York Composite index declined 0.86%, the S&P 500 Equal Weight index dropped 0.52% and the Dow Jones Industrial Average retreated 0.51%, so it was not a grand week for the market of stocks, even as the financial press argued that the stock market had a good five days.

Of course, lousy market breadth is nothing new as the average stock in the Russell 3000, believe it or not, has had a negative total return for the year, with the average-stock losses even extending to the supposedly high-flying Russell 3000 Growth index.

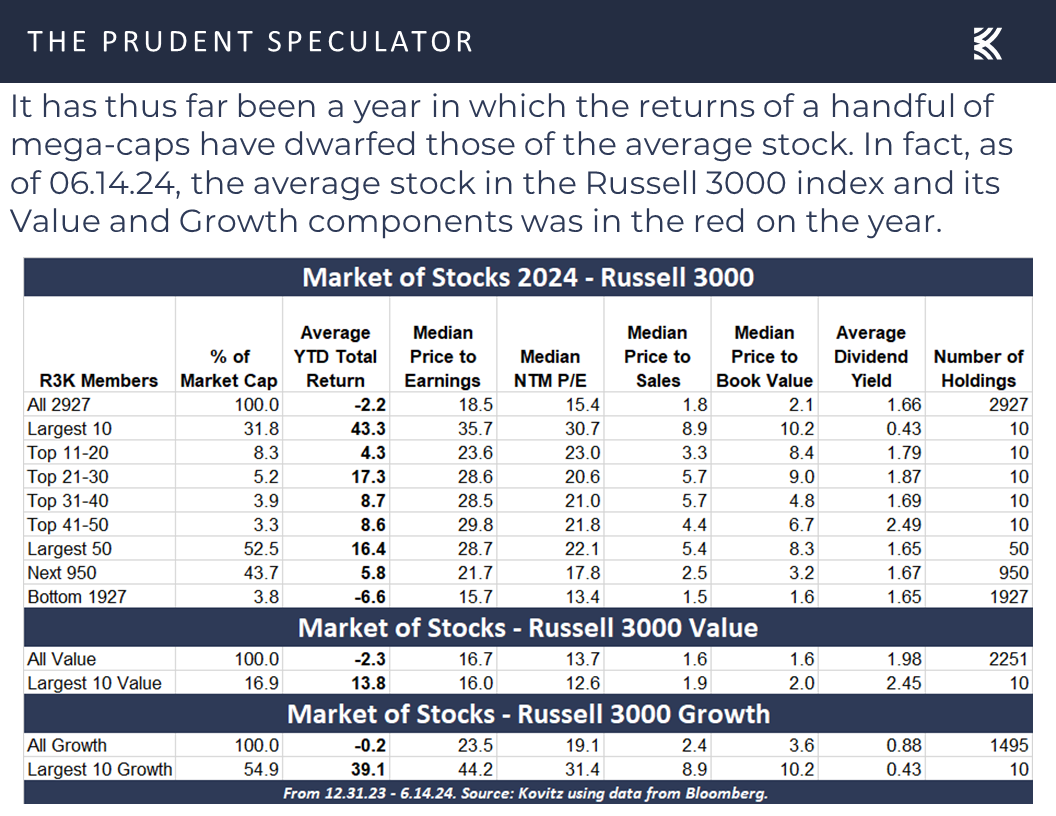

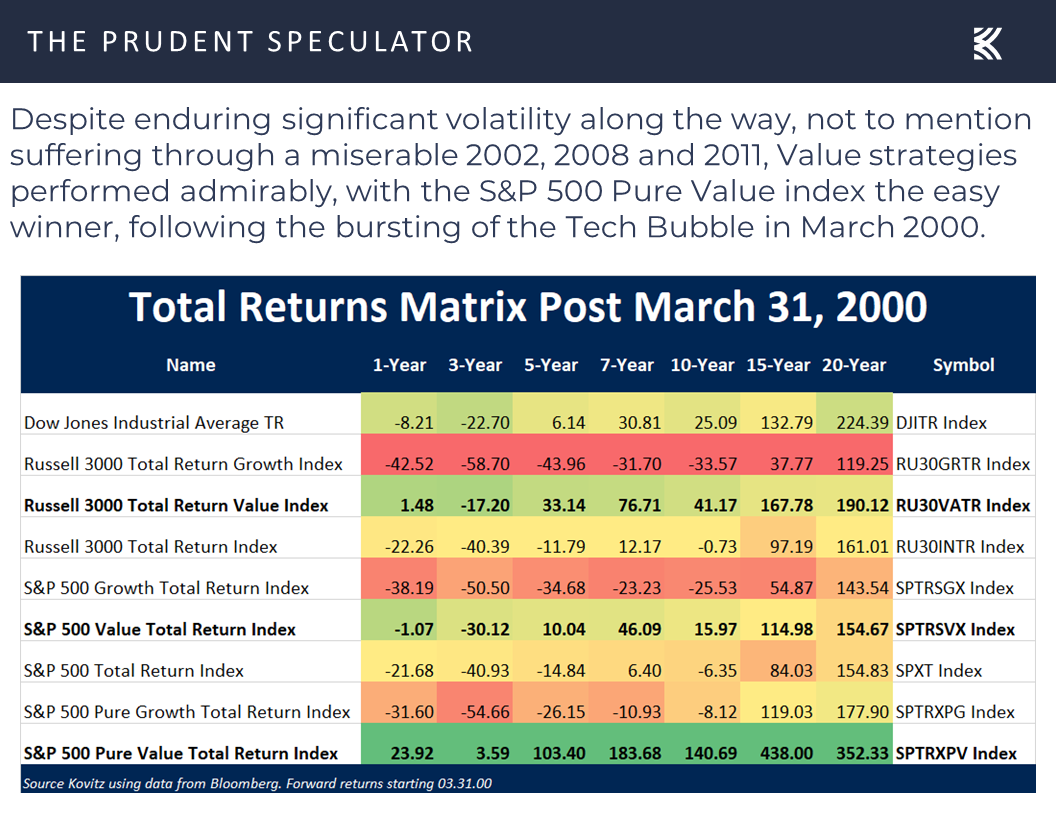

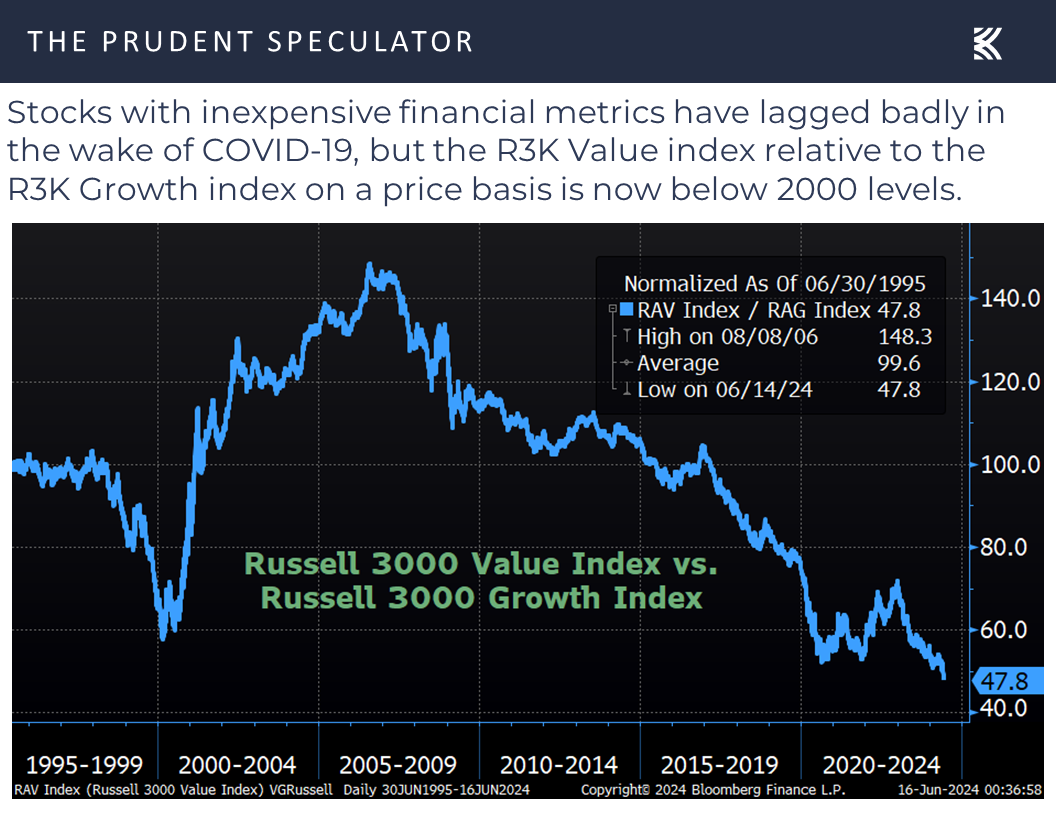

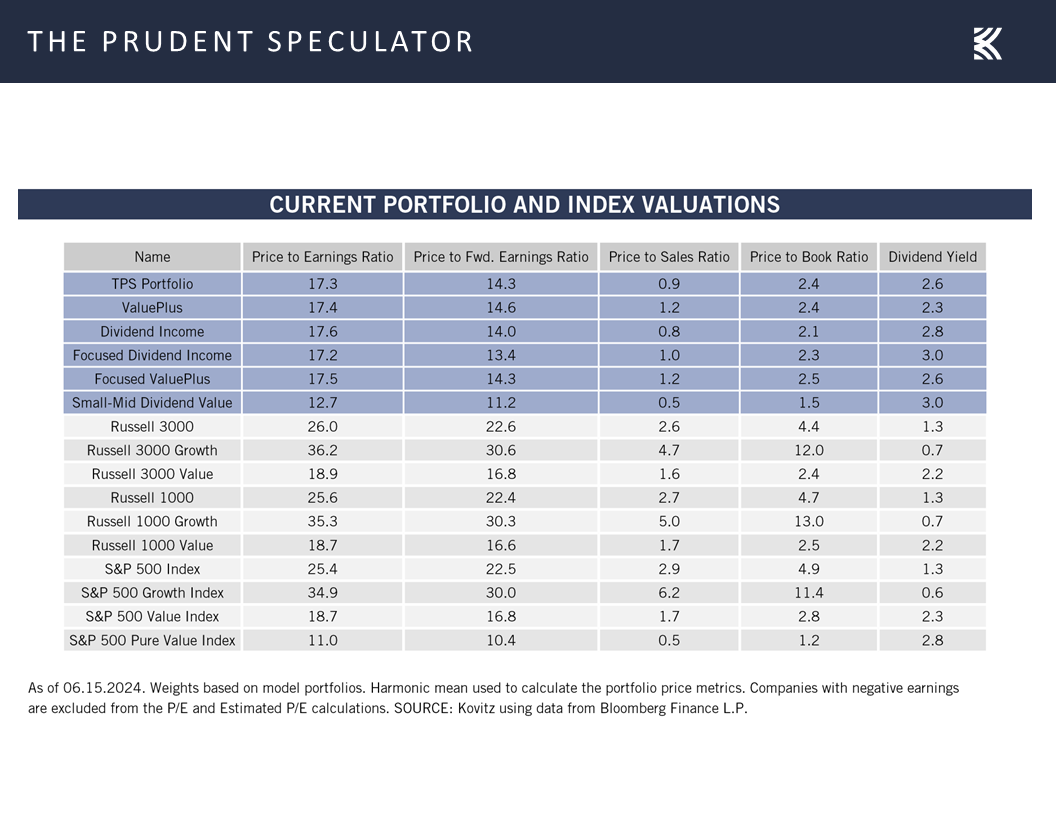

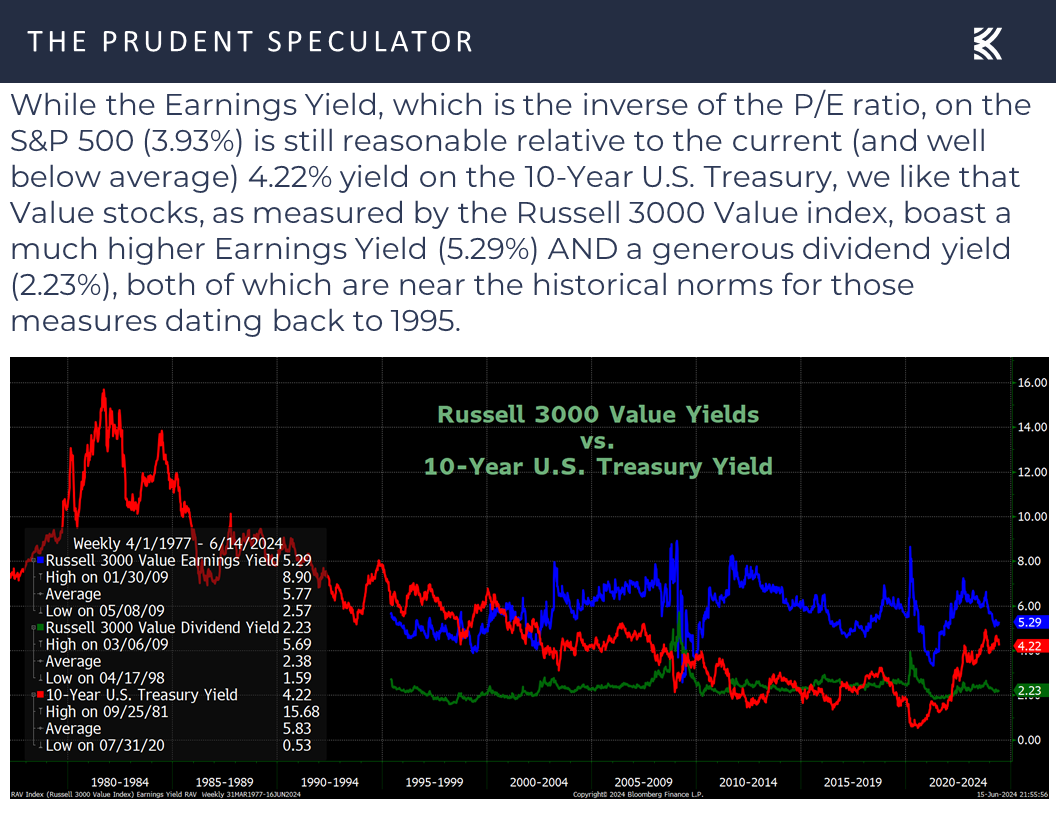

Value – Tech Bubble History Lesson; R3K Value Index Very Inexpensive Relative to R3K Growth

There are plenty of opinions about what the broad divergence might mean for stocks going forward, but students of market history might consider what transpired (Value was very much the place to be!) following the bursting of the Tech Bubble back in 2000,

especially considering that the Value indexes are even more attractively priced relative to growth today than they were 24 years ago.

History doesn’t always repeat, but it often rhymes, so we continue to sleep well at night, given the inexpensive metrics and generous dividend yields on our broadly diversified portfolios of what we believe to be undervalued stocks. Happily, even as we own three of last week’s four big Russell 3000 winners (our initial newsletter recommendations came years ago: Apple: 10.06.00 at $0.40; Broadcom: 10.31.19 at $292.85; Microsoft: 02.28.05 at $25.16), the price ratios in the table below generally are less expensive than those of the Russell 3000 Value index, while our dividend yields are higher.

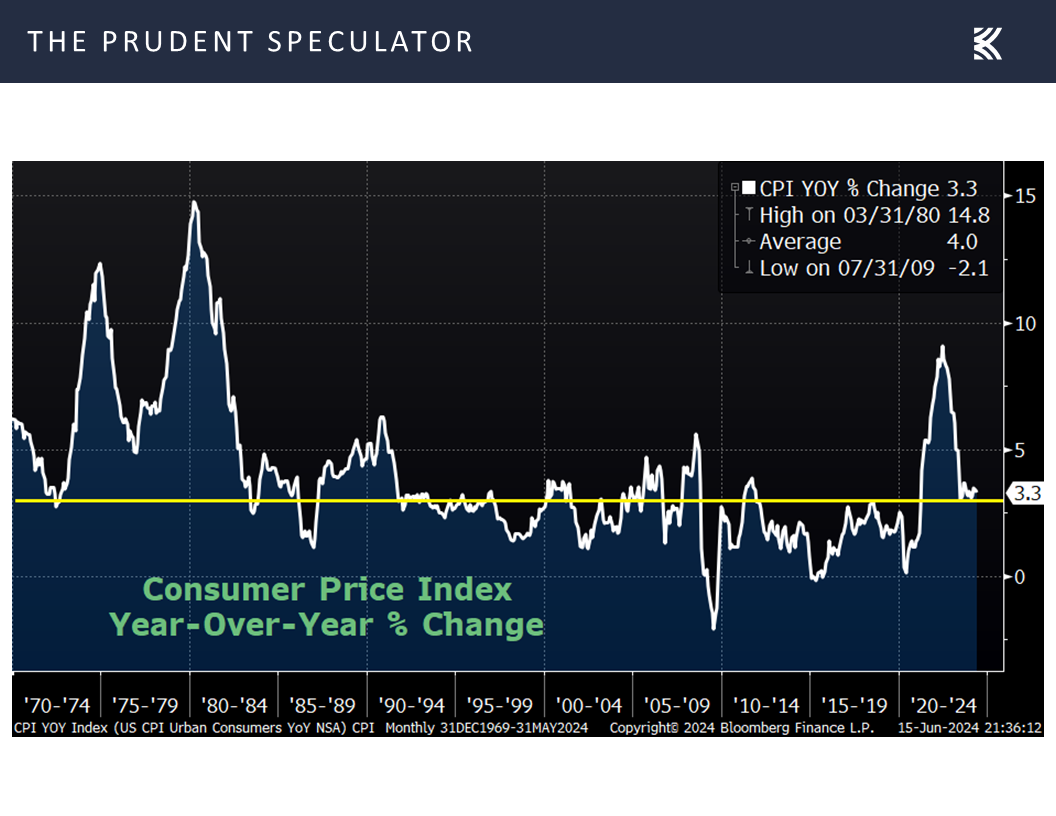

Inflation – Lower-than-Expected CPI & PPI

Developments last week did nothing to alter our optimism about the prospects for our stocks going forward, even as others evidently did not share our enthusiasm. Inflation at the consumer level (Consumer Price Index – CPI) in May came in slightly lower than expected with a 3.3% increase (vs. 3.4% est.),

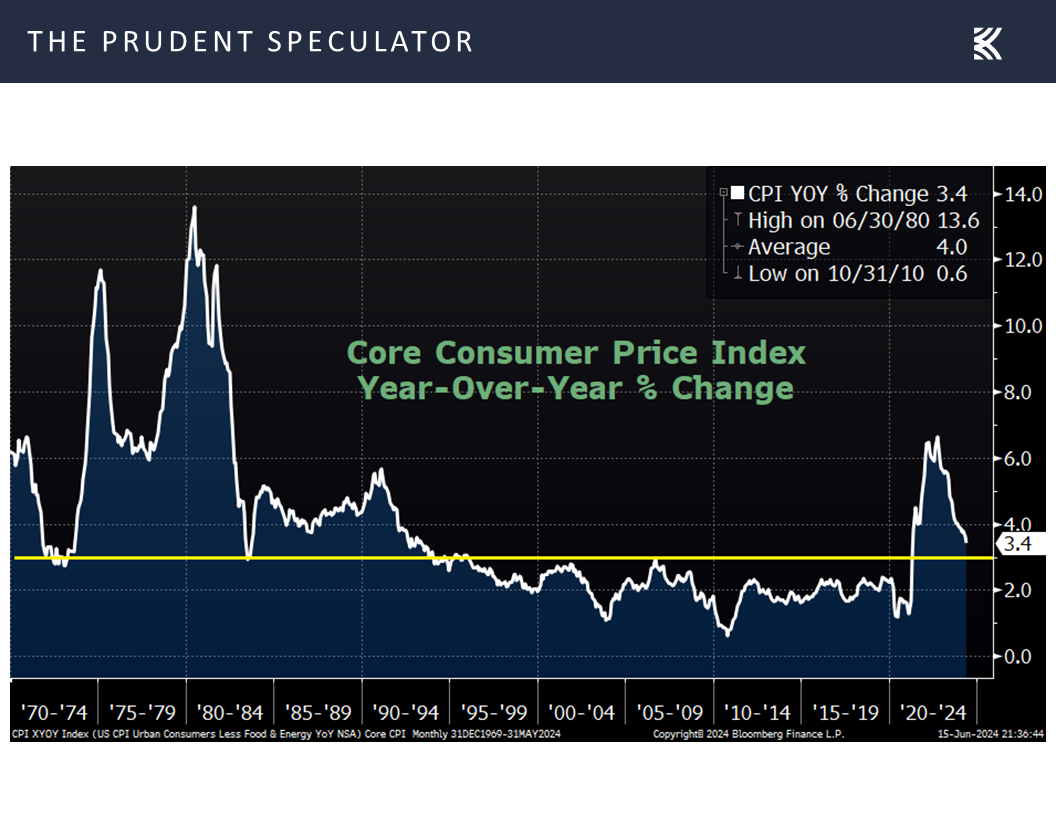

with the core CPI’s (excludes volatile food and energy) year-over-year rise of 3.4% also beating the 3.5% projection.

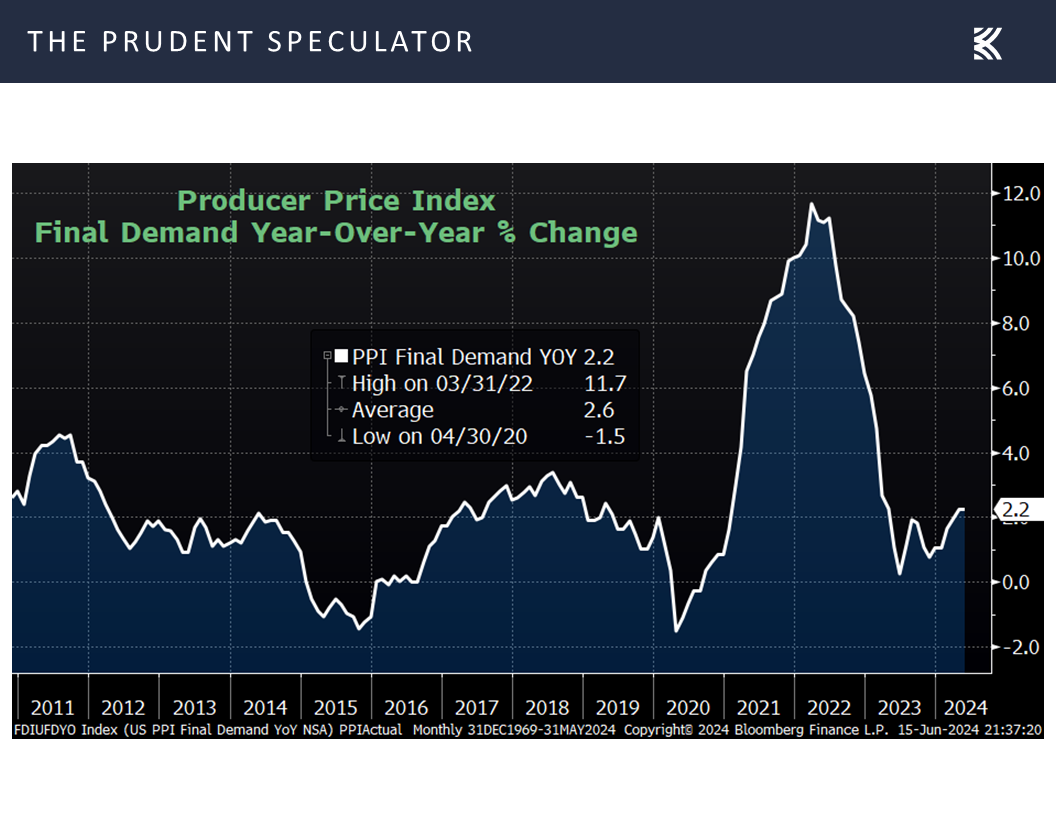

It was a similar story for inflation at the wholesale level as the Producer Price Index’s advance of 2.2% for May was below forecasts for a 2.5% gain.

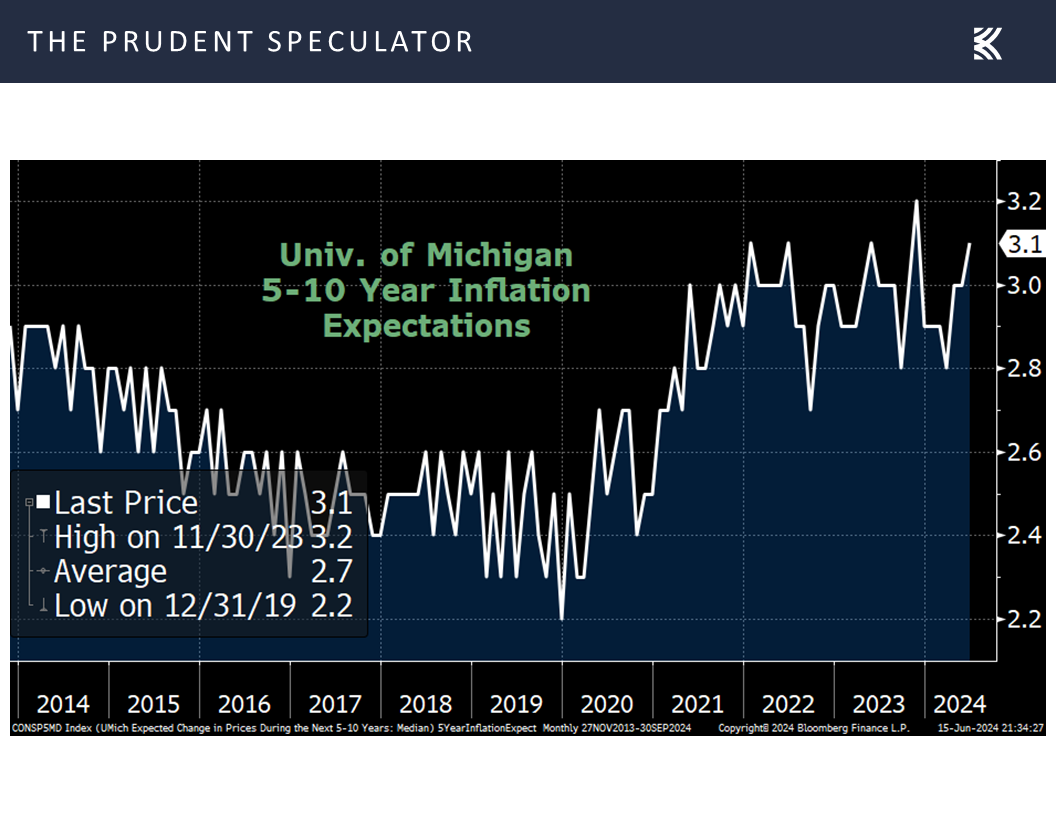

True, longer-term inflation expectations ticked up a notch this month to a 3.1% rate, per the Univ. of Michigan,

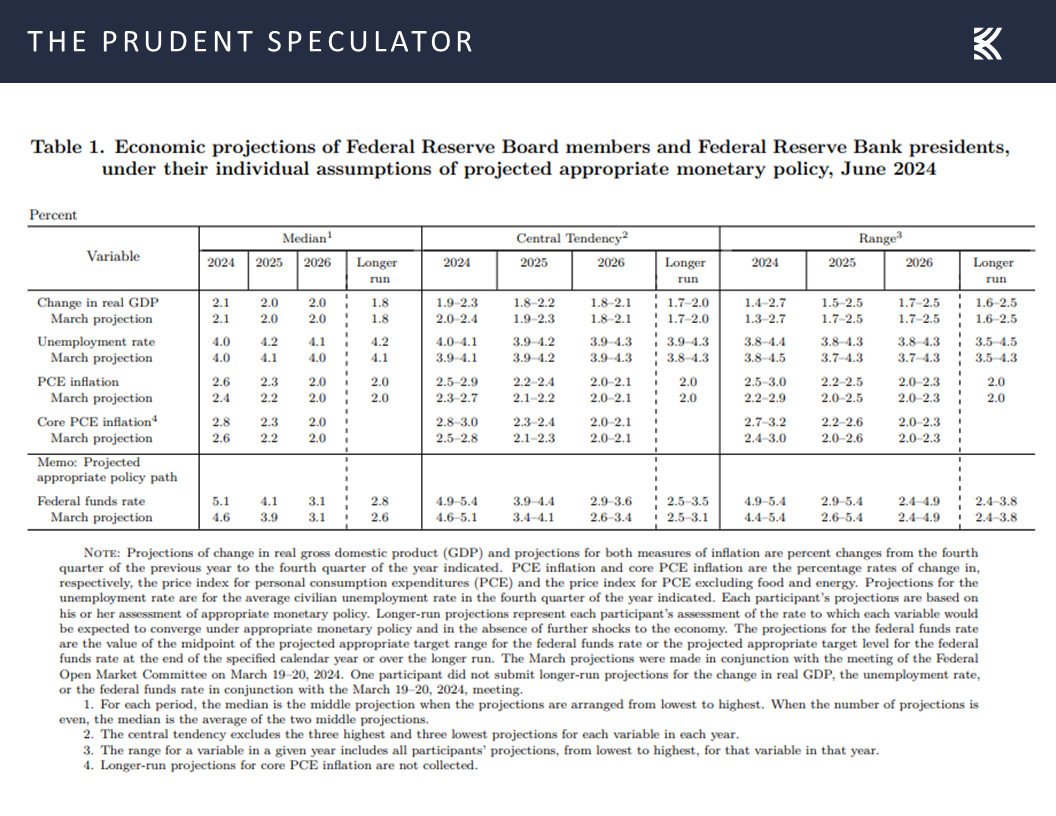

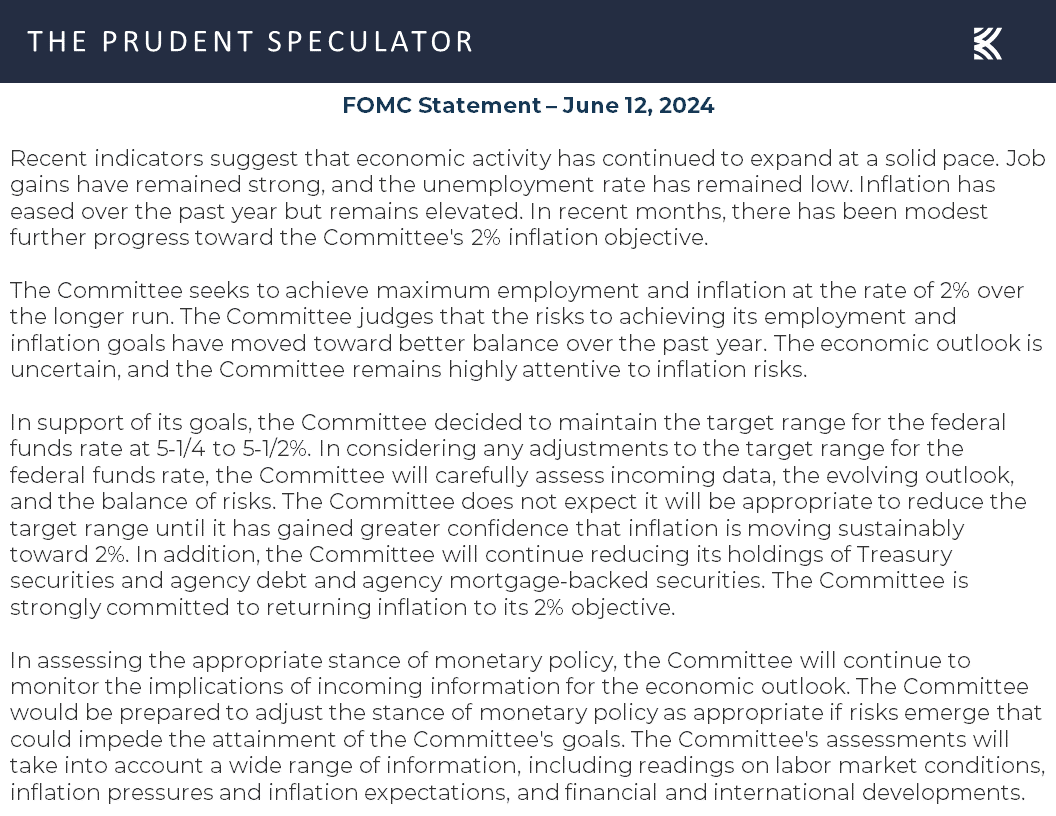

Fed Econ Projections – 1 Rate Cut This Year; 4 Cuts Next Year

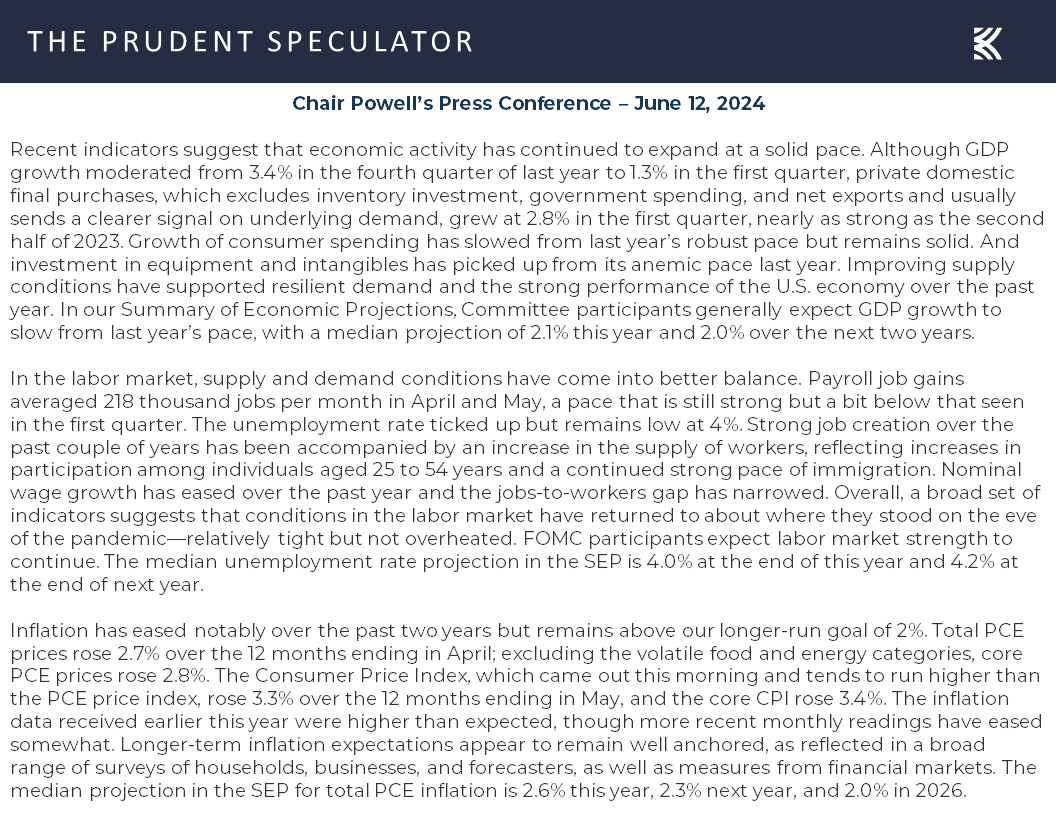

while projections released on Wednesday from Federal Reserve Board members and Federal Reserve Bank presidents showed that inflation is likely to be slightly stickier this year and next than was thought three months ago.

Still, Jerome H. Powell had the following to say at his Press Conference on Wednesday,…

There are fewer rate cuts in the median this year, but there’s one more next year. So, you really, if you look at year-end 2025 and 26, you’re almost exactly where you would have been, just it’s moved later because of that progress. Now, you get different data today. So, we’ll have to see where the data light the way, you know, where the economy has, you know, repeatedly surprised forecasters in both directions, and today was certainly a better inflation report than almost anybody expected. And we’ll just have to see what the incoming data flow brings and how that affects the outlook in the balance of risks.

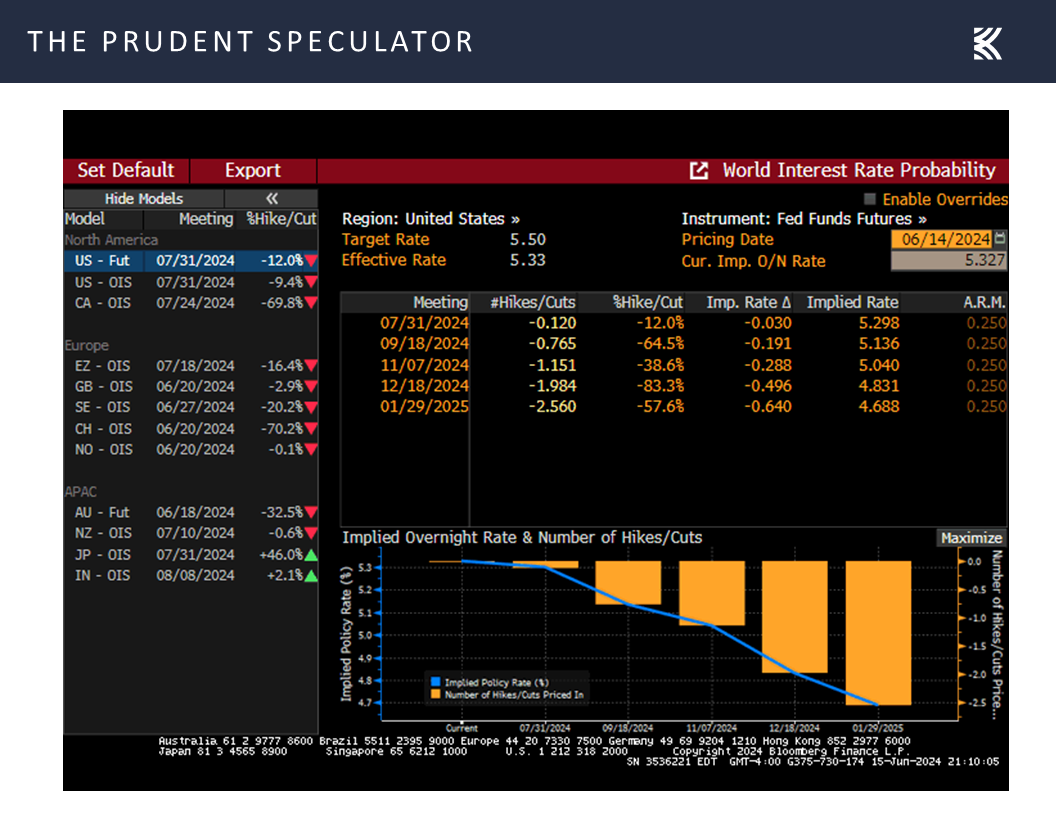

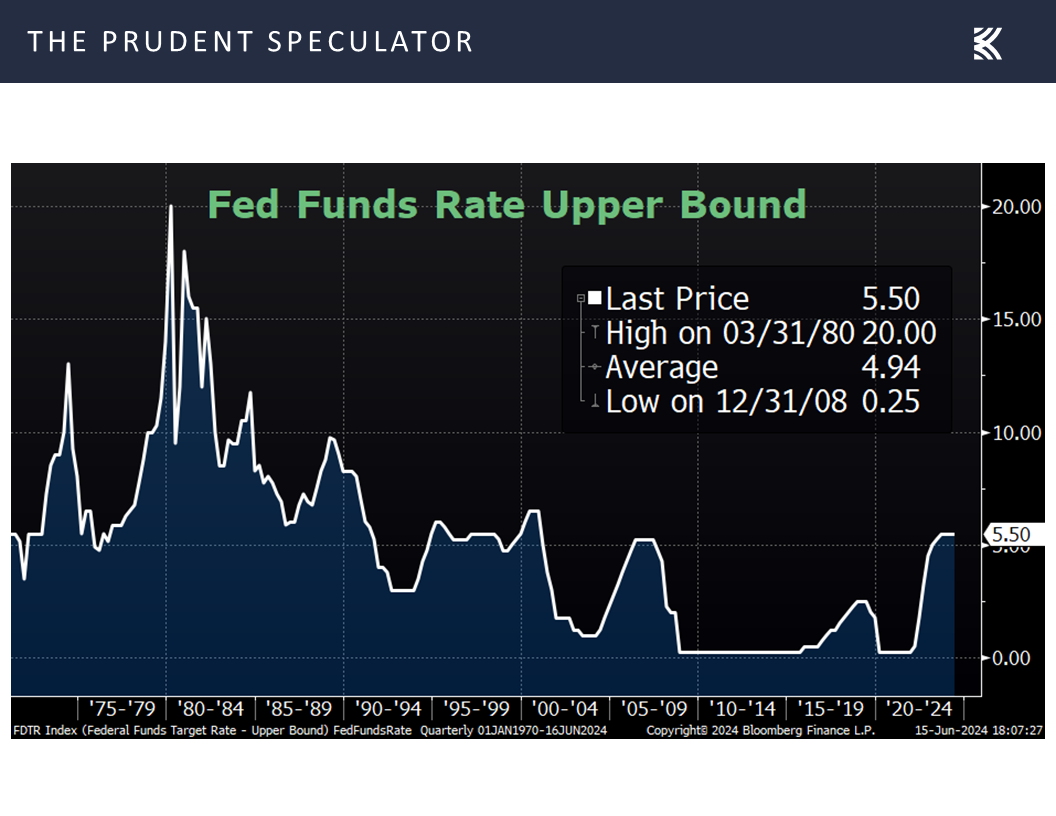

…which contributed to a reduction in market forecasts for the year-end Fed Funds rate to 4.83%, down from 4.96% a week ago,…

Interest Rates – Lower 10-Year Yield & Lower Expected Year-End Fed Funds Rate vs. the Prior Week

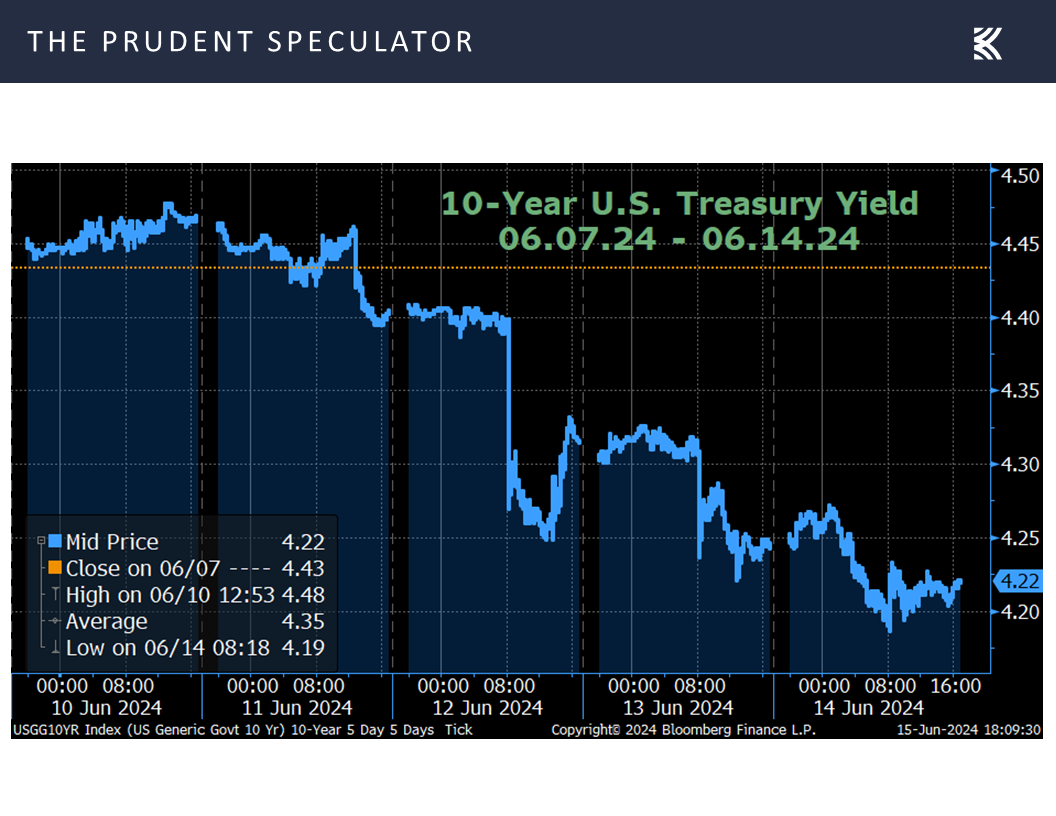

…and a sizable drop in the yield on the benchmark government bond to the lowest level since March 28.

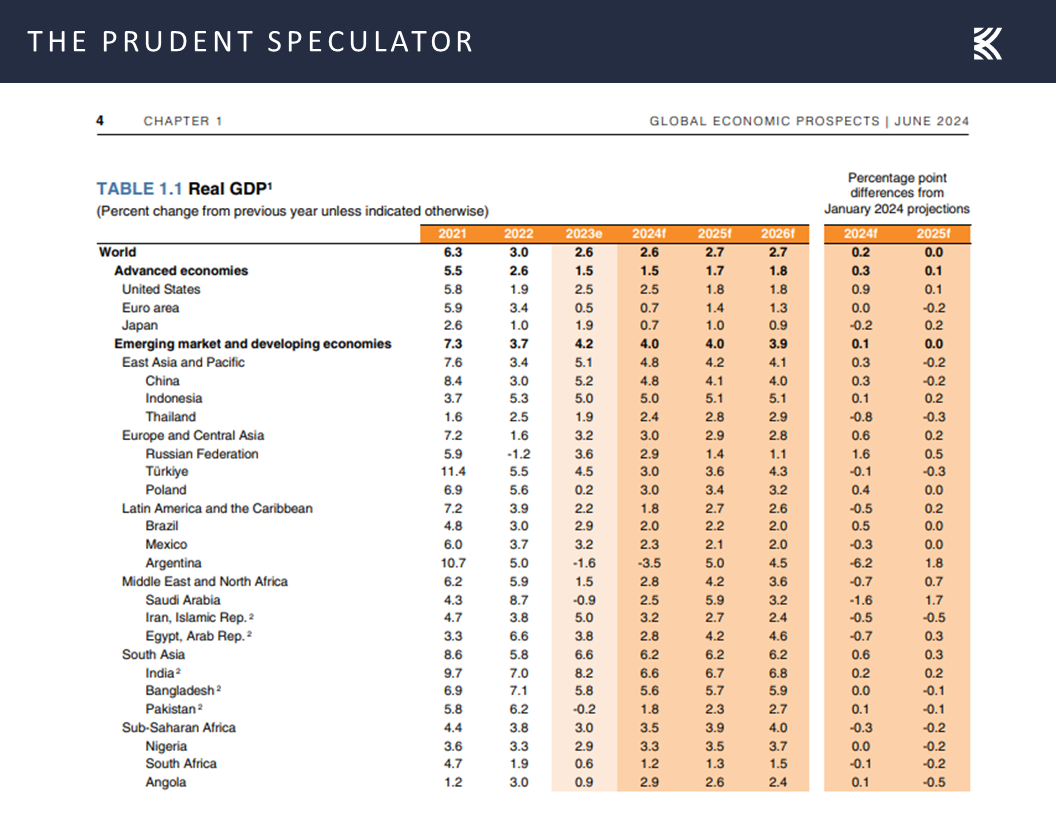

Econ News – Mixed Data; Fed & World Bank Each Projecting Decent U.S. Growth for ’24 and ’25

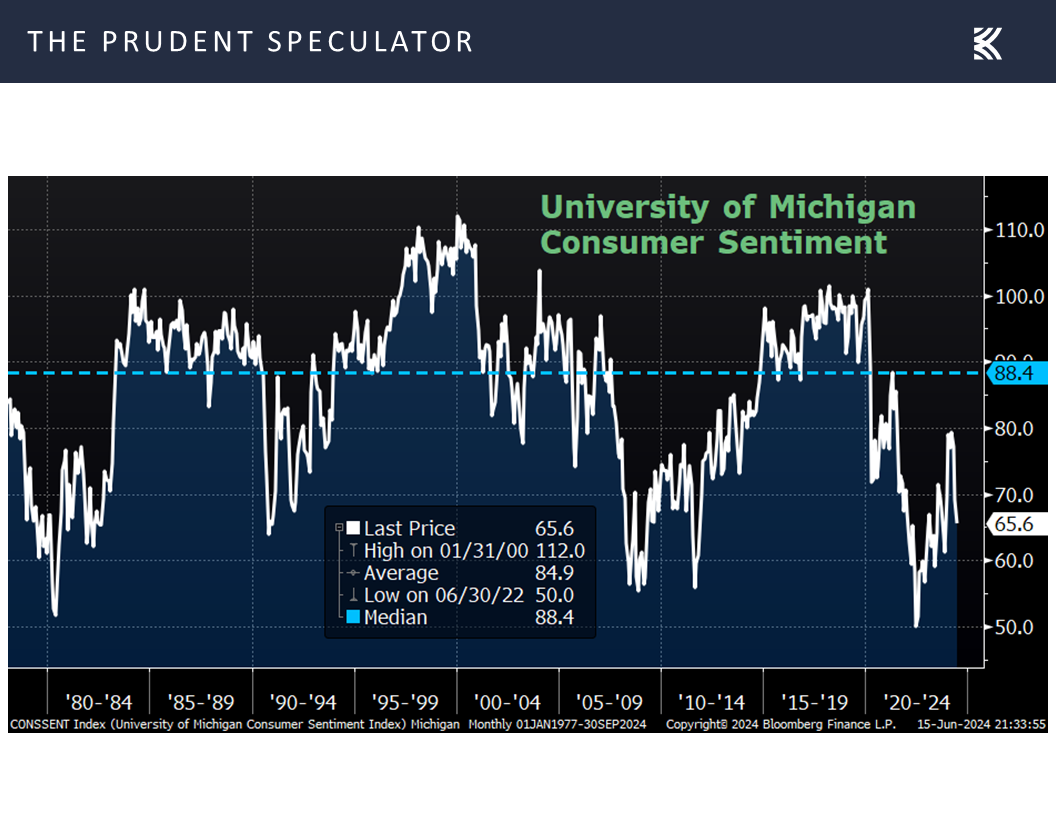

Some will argue that weaker economic data, like declining consumer sentiment for June,

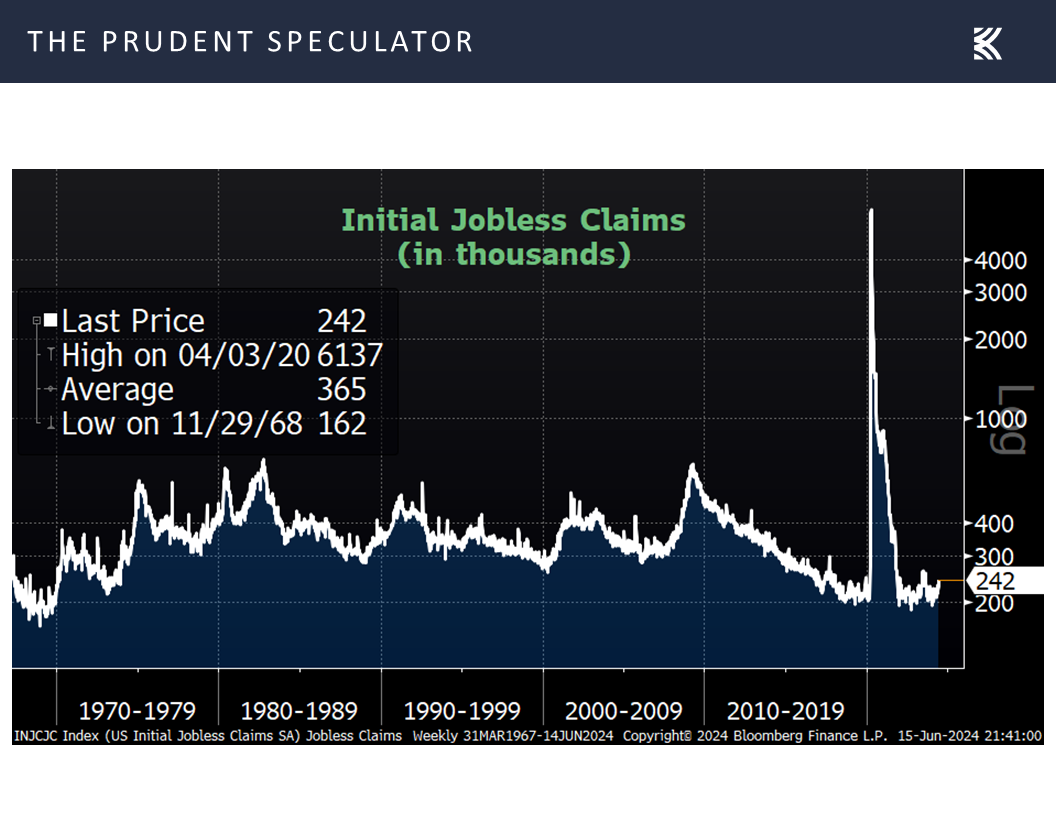

and more first-time filings for unemployment benefits than expected in the latest week, also contributed to the reduction in interest rates,

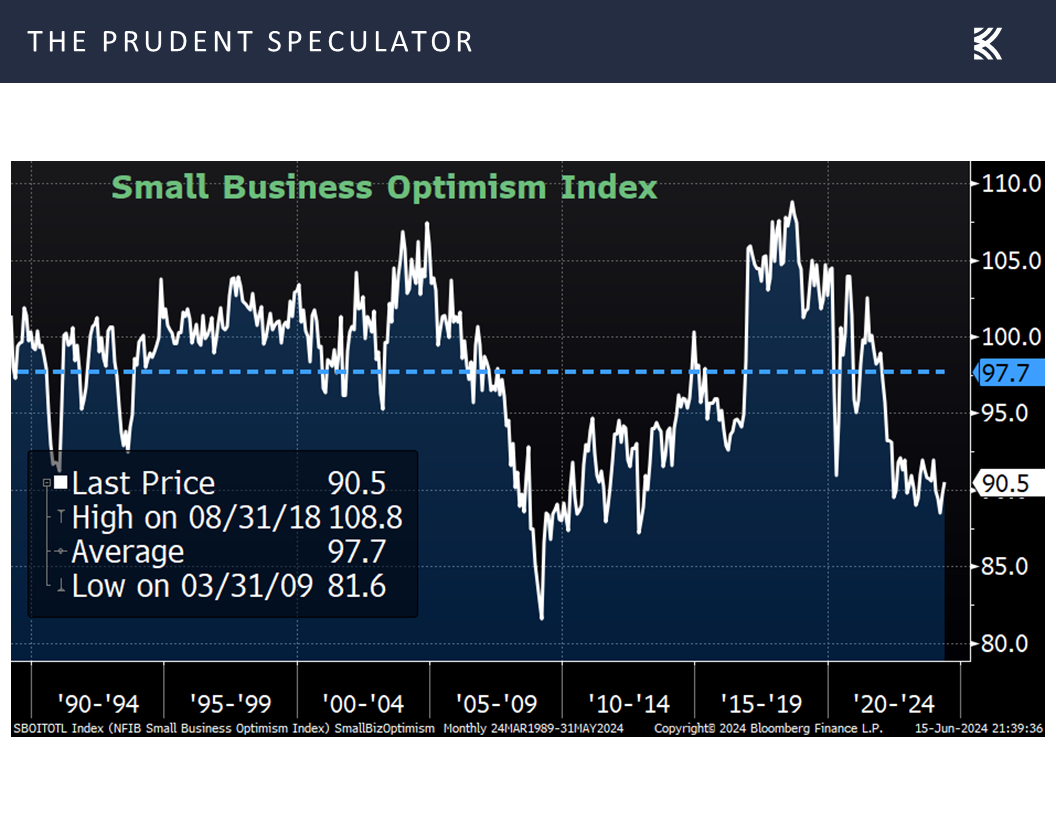

but Small Business Optimism for May exceeded estimates,

and the Fed Chair reminded that the Summary of Economic Projections shows an outlook for real (inflation-adjusted) GDP growth this year of 2.1% and 2.0% for 2025,

while the World Bank last week modestly upgraded its outlook for global GDP growth, stating: “The global economy is stabilizing, following several years of overlapping negative shocks. Despite elevated financing costs and heightened geopolitical tensions, global activity firmed in early 2024. Global growth is envisaged to reach a slightly faster pace this year than previously expected, due mainly to the continued solid expansion of the U.S. economy. However, the extent of expected declines in global interest rates has moderated amid lingering inflation pressures in key economies. By historical standards, the global outlook remains subdued: both advanced economies and emerging market and developing economies (EMDEs) are set to grow at a slower pace over 2024-26 than in the decade preceding the pandemic.”

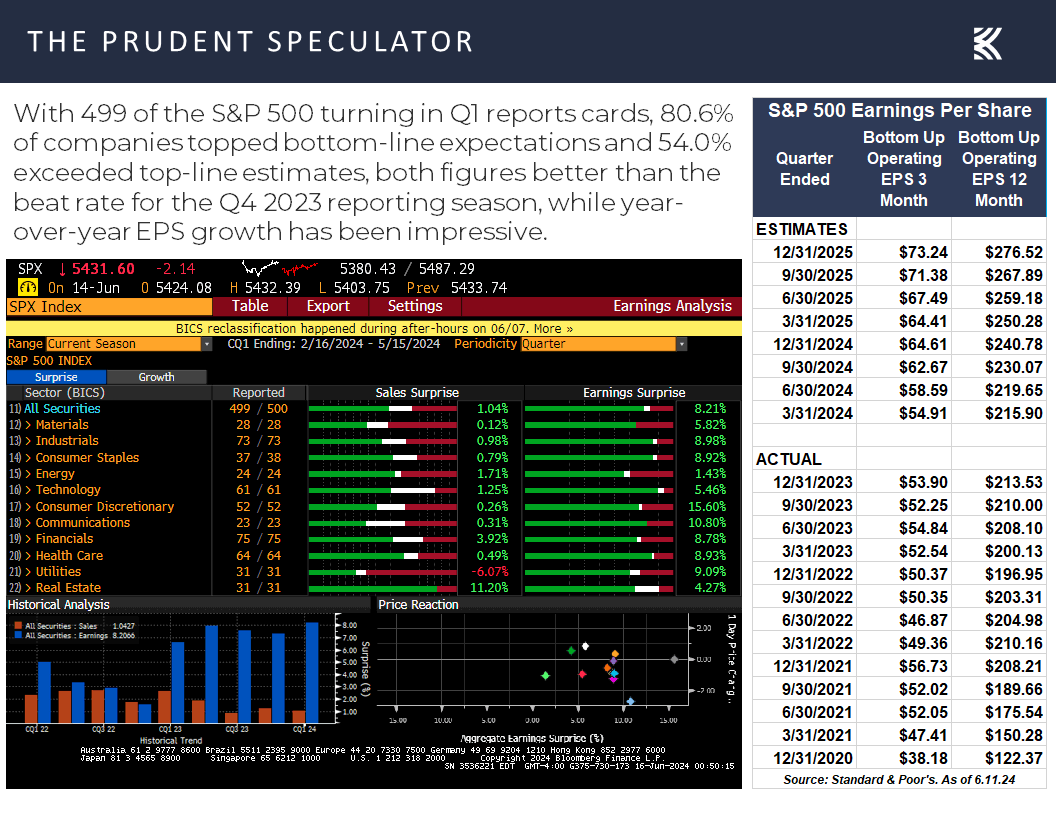

Earnings – Solid Growth Estimated in ’24 & ’25

We realize that many were disappointed that the FOMC Statement issued on Wednesday,

did not suggest that a cut in the target for the Fed Funds rate was imminent,

but we think the current interest rate environment should not be a headwind for the kind of stocks that we have long championed,

especially as we think corporate profits, the E in the Earnings Yield (E/P) ratio, should continue to grow this year and next.

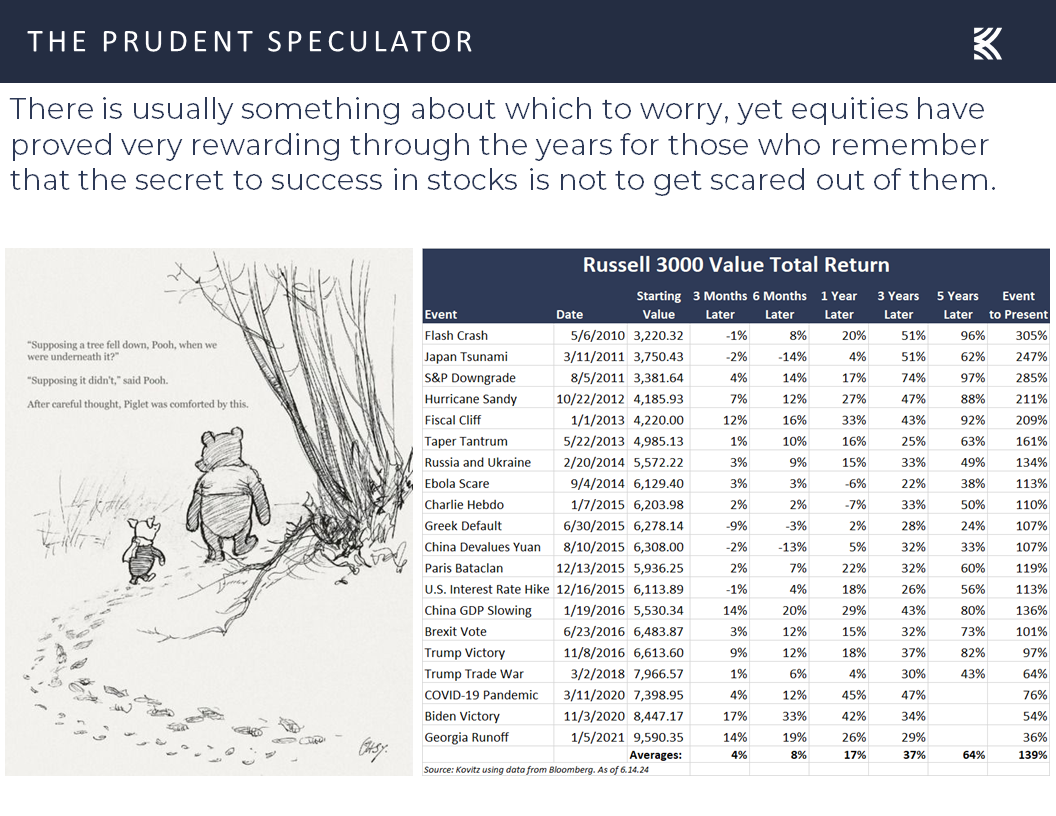

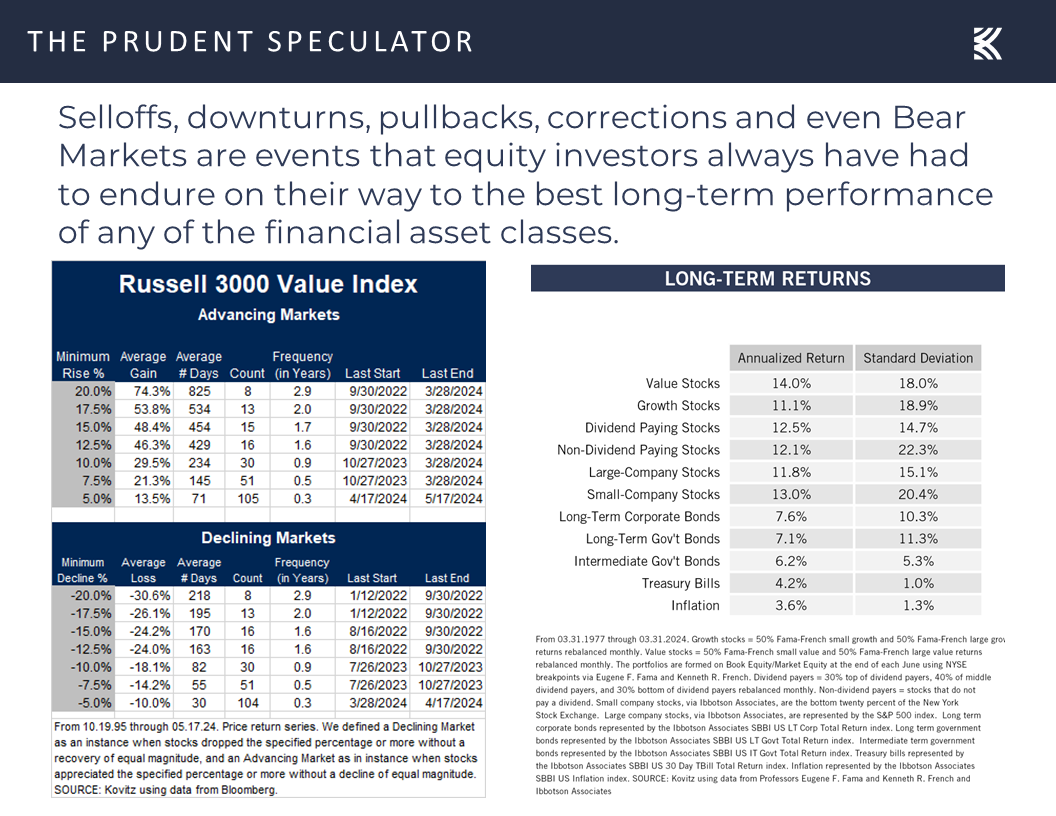

Volatility – Scary Headlines & Plenty of Gyrations Along the Way but Long-Term Trend is Up

None of the above is meant to suggest that the sailing will be smooth going forward, and we know that there will be disconcerting headlines in our future,

not to mention sometimes-scary volatility, but Value stocks always have proved very rewarding in the fullness of time.

Stock News – Updates on five stocks across four different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Value Stocks, Federal Reserve Projections, Earnings and More

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Value Stocks, Federal Reserve Projections, Earnings and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Market Breadth – A Handful of Mega Caps Up but Most Stocks Down Last Week; Average Stock Down on the Year

Value – Tech Bubble History Lesson; R3K Value Index Very Inexpensive Relative to R3K Growth

Inflation – Lower-than-Expected CPI & PPI

Fed Econ Projections – 1 Rate Cut This Year; 4 Cuts Next Year

Interest Rates – Lower 10-Year Yield & Lower Expected Year-End Fed Funds Rate vs. the Prior Week

Econ News – Mixed Data; Fed & World Bank Each Projecting Decent U.S. Growth for ’24 and ’25

Earnings – Solid Growth Estimated in ’24 & ’25

Volatility – Scary Headlines & Plenty of Gyrations Along the Way but Long-Term Trend is Up

Stock News – Updates on AAPL, ORCL, AVGO, GM & ZBH

Market Breadth – A Handful of Mega Caps Up but Most Stocks Down Last Week; Average Stock Down on the Year

The average member of the Russell 3000 index lost 1.26% last week, the New York Composite index declined 0.86%, the S&P 500 Equal Weight index dropped 0.52% and the Dow Jones Industrial Average retreated 0.51%, so it was not a grand week for the market of stocks, even as the financial press argued that the stock market had a good five days.

Of course, lousy market breadth is nothing new as the average stock in the Russell 3000, believe it or not, has had a negative total return for the year, with the average-stock losses even extending to the supposedly high-flying Russell 3000 Growth index.

Value – Tech Bubble History Lesson; R3K Value Index Very Inexpensive Relative to R3K Growth

There are plenty of opinions about what the broad divergence might mean for stocks going forward, but students of market history might consider what transpired (Value was very much the place to be!) following the bursting of the Tech Bubble back in 2000,

especially considering that the Value indexes are even more attractively priced relative to growth today than they were 24 years ago.

History doesn’t always repeat, but it often rhymes, so we continue to sleep well at night, given the inexpensive metrics and generous dividend yields on our broadly diversified portfolios of what we believe to be undervalued stocks. Happily, even as we own three of last week’s four big Russell 3000 winners (our initial newsletter recommendations came years ago: Apple: 10.06.00 at $0.40; Broadcom: 10.31.19 at $292.85; Microsoft: 02.28.05 at $25.16), the price ratios in the table below generally are less expensive than those of the Russell 3000 Value index, while our dividend yields are higher.

Inflation – Lower-than-Expected CPI & PPI

Developments last week did nothing to alter our optimism about the prospects for our stocks going forward, even as others evidently did not share our enthusiasm. Inflation at the consumer level (Consumer Price Index – CPI) in May came in slightly lower than expected with a 3.3% increase (vs. 3.4% est.),

with the core CPI’s (excludes volatile food and energy) year-over-year rise of 3.4% also beating the 3.5% projection.

It was a similar story for inflation at the wholesale level as the Producer Price Index’s advance of 2.2% for May was below forecasts for a 2.5% gain.

True, longer-term inflation expectations ticked up a notch this month to a 3.1% rate, per the Univ. of Michigan,

Fed Econ Projections – 1 Rate Cut This Year; 4 Cuts Next Year

while projections released on Wednesday from Federal Reserve Board members and Federal Reserve Bank presidents showed that inflation is likely to be slightly stickier this year and next than was thought three months ago.

Still, Jerome H. Powell had the following to say at his Press Conference on Wednesday,…

There are fewer rate cuts in the median this year, but there’s one more next year. So, you really, if you look at year-end 2025 and 26, you’re almost exactly where you would have been, just it’s moved later because of that progress. Now, you get different data today. So, we’ll have to see where the data light the way, you know, where the economy has, you know, repeatedly surprised forecasters in both directions, and today was certainly a better inflation report than almost anybody expected. And we’ll just have to see what the incoming data flow brings and how that affects the outlook in the balance of risks.

…which contributed to a reduction in market forecasts for the year-end Fed Funds rate to 4.83%, down from 4.96% a week ago,…

Interest Rates – Lower 10-Year Yield & Lower Expected Year-End Fed Funds Rate vs. the Prior Week

…and a sizable drop in the yield on the benchmark government bond to the lowest level since March 28.

Econ News – Mixed Data; Fed & World Bank Each Projecting Decent U.S. Growth for ’24 and ’25

Some will argue that weaker economic data, like declining consumer sentiment for June,

and more first-time filings for unemployment benefits than expected in the latest week, also contributed to the reduction in interest rates,

but Small Business Optimism for May exceeded estimates,

and the Fed Chair reminded that the Summary of Economic Projections shows an outlook for real (inflation-adjusted) GDP growth this year of 2.1% and 2.0% for 2025,

while the World Bank last week modestly upgraded its outlook for global GDP growth, stating: “The global economy is stabilizing, following several years of overlapping negative shocks. Despite elevated financing costs and heightened geopolitical tensions, global activity firmed in early 2024. Global growth is envisaged to reach a slightly faster pace this year than previously expected, due mainly to the continued solid expansion of the U.S. economy. However, the extent of expected declines in global interest rates has moderated amid lingering inflation pressures in key economies. By historical standards, the global outlook remains subdued: both advanced economies and emerging market and developing economies (EMDEs) are set to grow at a slower pace over 2024-26 than in the decade preceding the pandemic.”

Earnings – Solid Growth Estimated in ’24 & ’25

We realize that many were disappointed that the FOMC Statement issued on Wednesday,

did not suggest that a cut in the target for the Fed Funds rate was imminent,

but we think the current interest rate environment should not be a headwind for the kind of stocks that we have long championed,

especially as we think corporate profits, the E in the Earnings Yield (E/P) ratio, should continue to grow this year and next.

Volatility – Scary Headlines & Plenty of Gyrations Along the Way but Long-Term Trend is Up

None of the above is meant to suggest that the sailing will be smooth going forward, and we know that there will be disconcerting headlines in our future,

not to mention sometimes-scary volatility, but Value stocks always have proved very rewarding in the fullness of time.

Stock News – Updates on five stocks across four different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.