The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Value Stocks, Volatility, Inflation and AAII Sentiment. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

TPS Webinar – Join John, Jason & Chris on Thursday, March 6 at 11:00 AM Pacific; 2:00 PM Eastern

Value – Good Week, Year, Decade and Half-Century for Inexpensively Priced Stocks

Headlines – Stocks Have Overcome All Prior Disconcerting Events

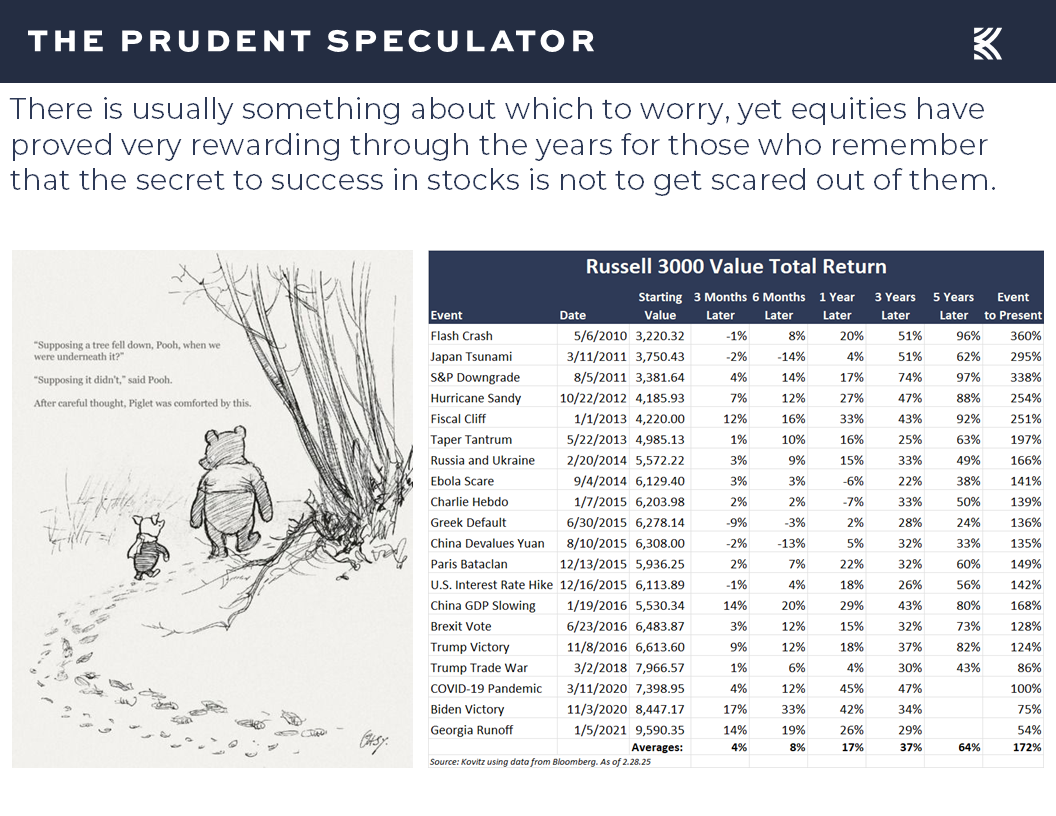

Volatility – Stocks Go Up and Down in the Short Term, But Have Provided Handsome Rewards in the Long-Term

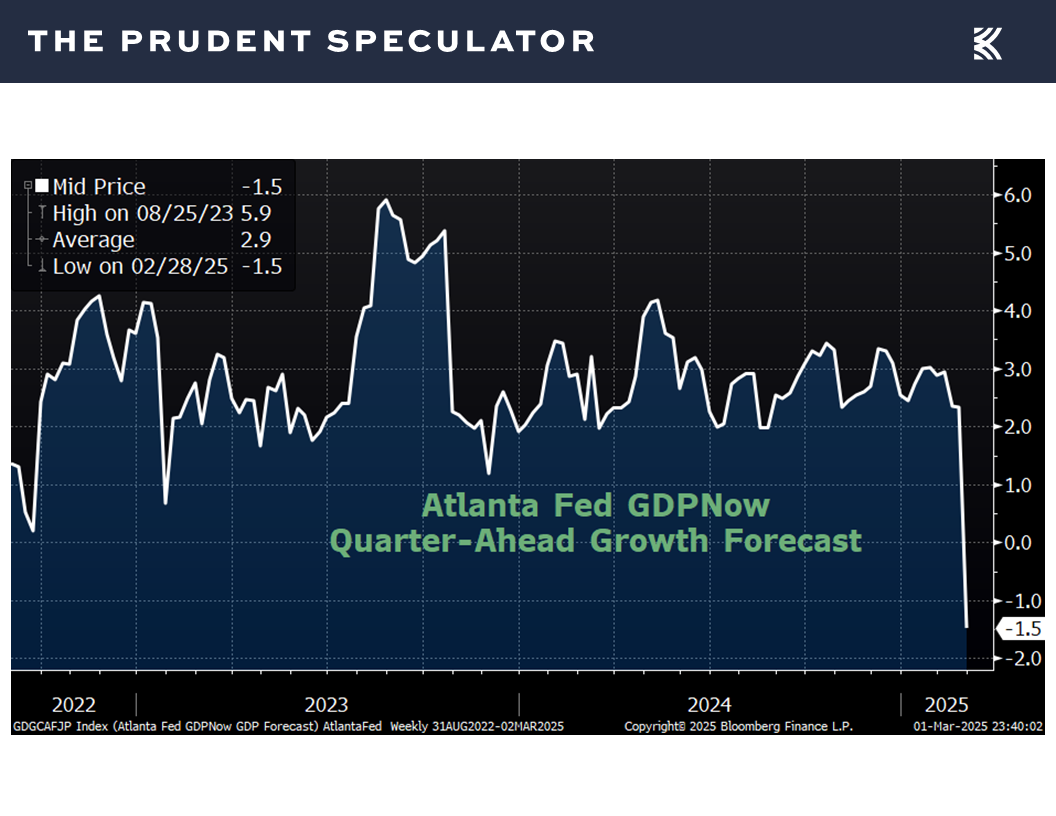

Econ Data – Atlanta Fed Turns Negative on GDP; Weak Stats

Perspective – Holding Through Recessions

Inflation – In Line PCE Numbers; Stocks a Great Hedge

Valuations – Value Stocks Even More Reasonably Priced

Sentiment – Major AAII Contrarian Buy Signal

Stock News – Updates on GM, FDP, AXAHY, CIVI, AMT, SOLV & PNW

TPS Webinar – Join John, Jason & Chris on Thursday, March 6 at 11:00 AM Pacific; 2:00 PM Eastern

Join us for an exclusive webinar where I will cut through the noise and debunk three market myths that are presently circulating in the financial press. We will also hold a live Q&A session where Jason Clark and Chris Quigley will join me so members of the TPS community can ask about anything from value stocks to economic trends to how A.I. is impacting investment decisions.

Mark your calendars for Thursday, March 6 at 11:00 AM PT / 2:00 PM ET. Space is limited, so be sure to sign up here:

https://kovitz.zoom.us/webinar/register/9717297096423/WN_TNkq-QgdQ46lPdWjIh6PwQ

Value – Good Week, Year, Decade and Half-Century for Inexpensively Priced Stocks

Providing yet another reminder that it is very tough to predict short-term gyrations in stocks, news that arguably should have sent the markets higher on Thursday was greeted with a big selloff and headlines that arguably should have pushed equities lower on Friday saw stocks end a volatile session with markedly higher prices.

Headlines – Stocks Have Overcome All Prior Disconcerting Events

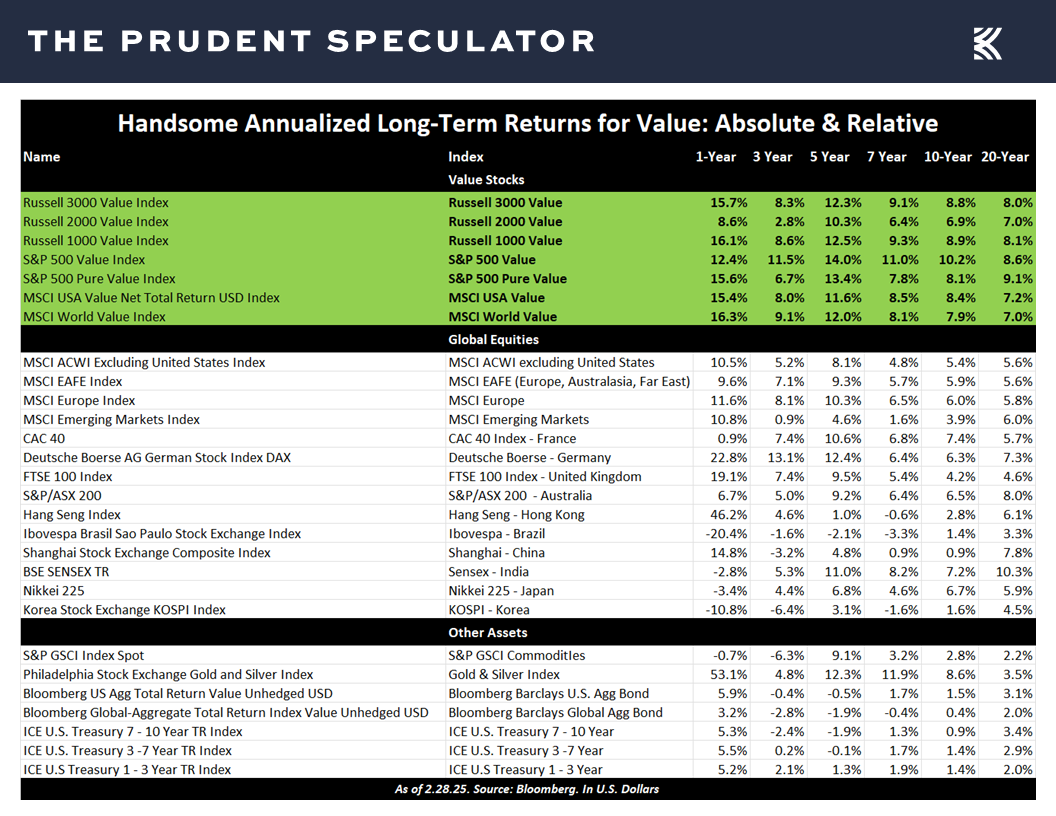

To be sure, it is always a market of stocks and not simply a stock market, as it was an ugly week overall for the Tech sector, with the Nasdaq Composite index off some 3.5% and semiconductor titan Nvidia down more than 7%. Value stocks performed much better, reminding investors that despite inevitable volatility along the way, they have a historical propensity for superior long-term returns,

while they have performed very well over the last two decades relative to international equities, commodities, bonds and U.S. treasuries.

While we often equate ourselves to the turtle in the Tortoise and the Hare fable, as we have always strived to grow wealthy slowly, we don’t mind that the get-rich-quick crowd has discovered some of our holdings. Yes, some of our stocks might today be classified as more Growth than Value, but we have long been eclectic in our approach to buying and harvesting undervalued stocks.

We have never been bound by arbitrary definitions of Value and Growth, so even a high-flyer like Nvidia could be a purchase candidate if it dropped into the double-digits (we offered our take on your Editor’s Forbes Blog last week: https://www.forbes.com/sites/johnbuckingham/2025/02/28/is-3-trillion-nvidia-nvda-a-value-stock/), but the composite valuations on our portfolios always have been deep in the Value camp.

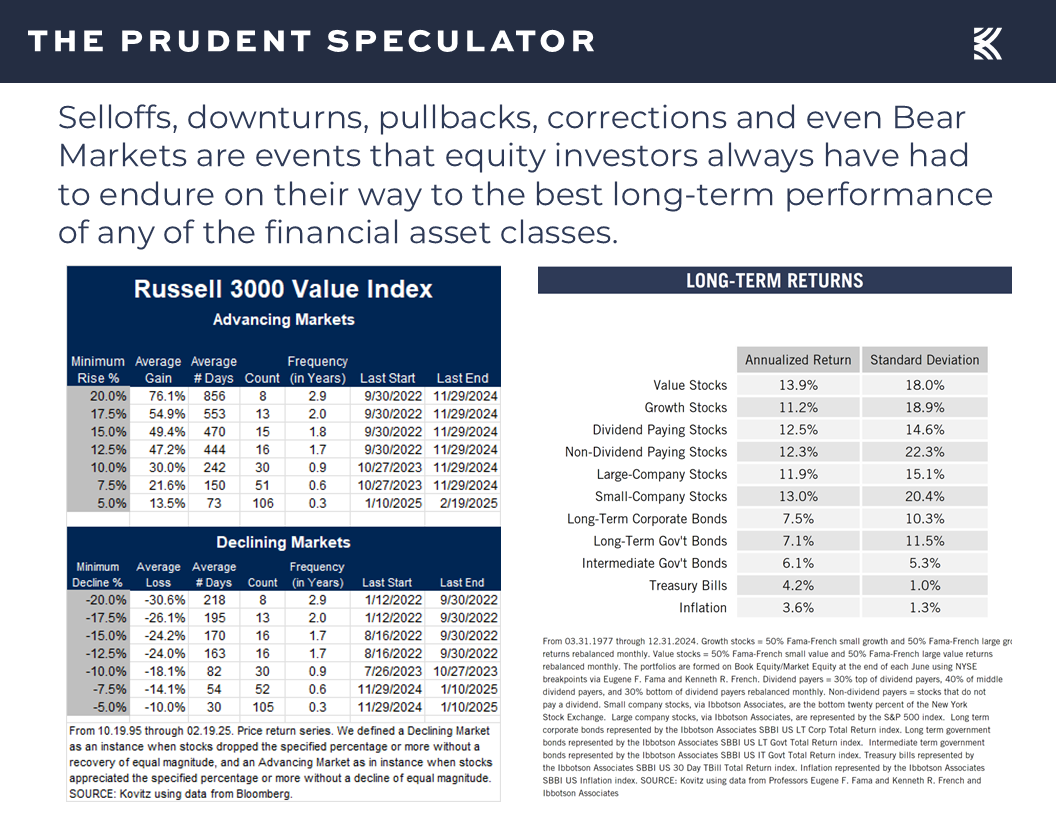

Volatility – Stocks Go Up and Down in the Short Term, But Have Provided Handsome Rewards in the Long-Term

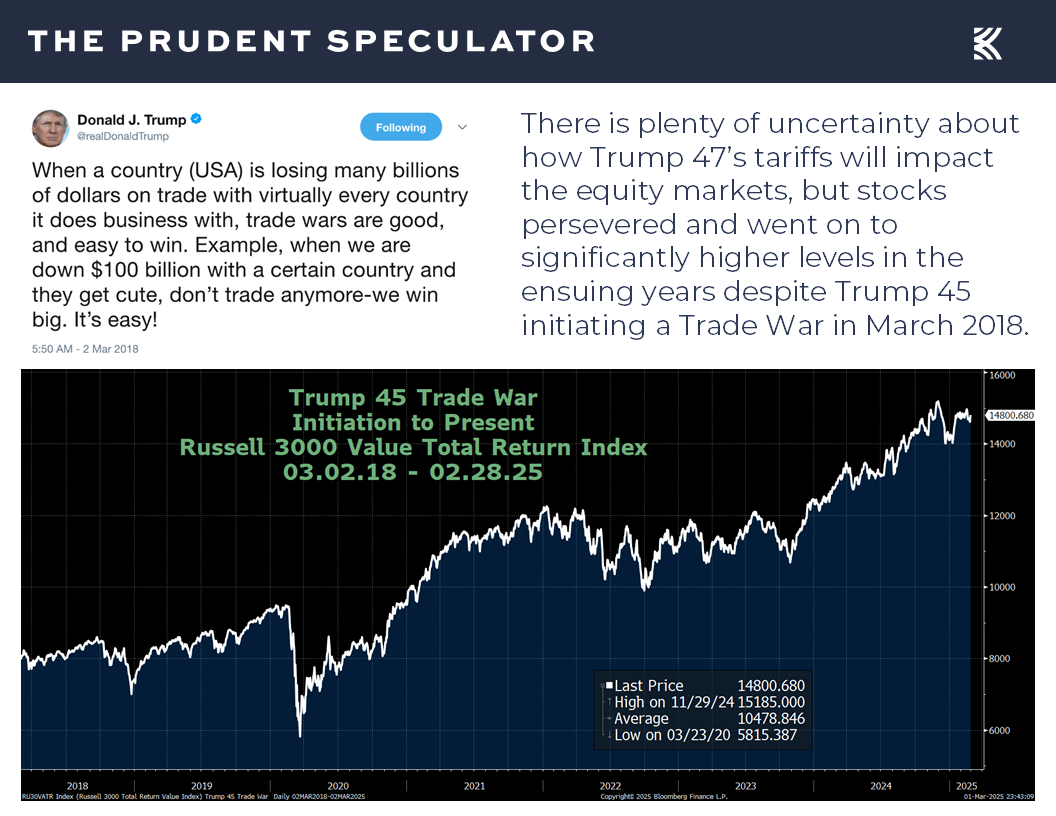

To be sure, there were worries last week as tariff talk again heated up,

and there was heightened drama on the geopolitical stage, but we continued to stay on an even emotional keel, with our patience and discipline always supported by the historical data that shows stocks have overcome every previous disconcerting event in the fullness of time.

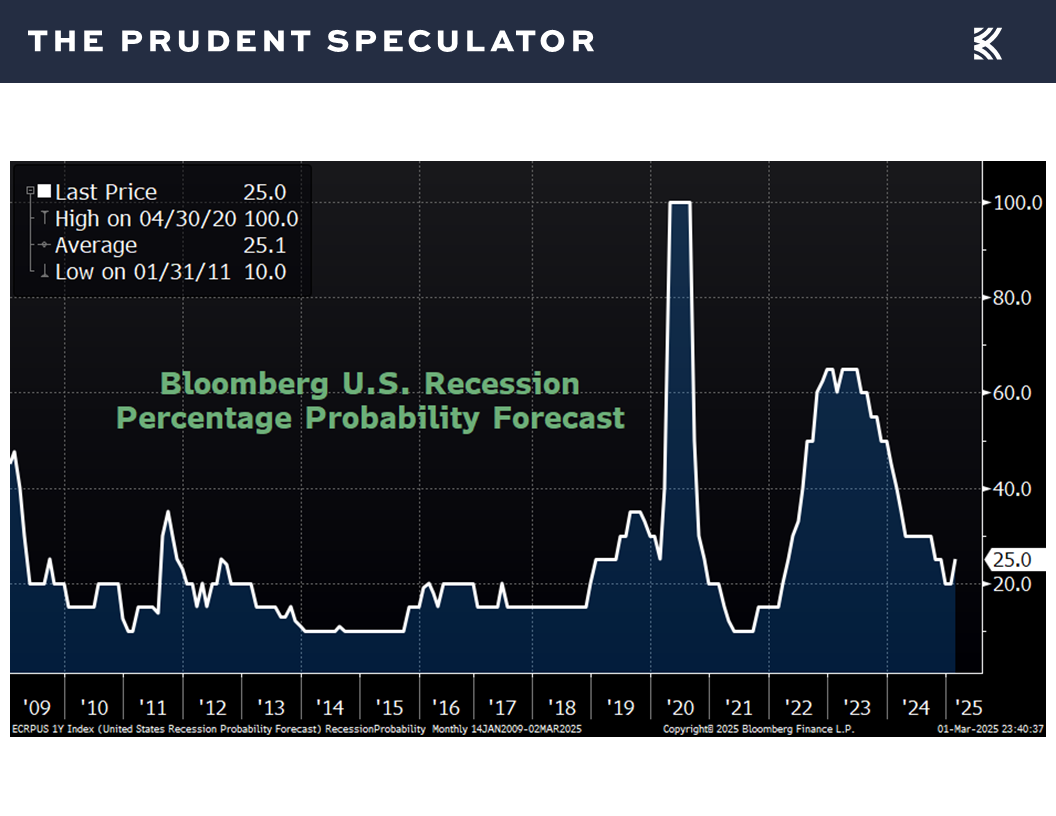

No doubt, it is different this time, just as it has been different every time, and a new bogeyman emerged last week as the latest estimate for real (inflation-adjusted) U.S. GDP growth in the current quarter from the Atlanta Fed was slashed to negative 1.5% on Friday from positive 2.3% earlier in the week,

and the odds of recession, as tabulated by Bloomberg, rose to 25%, up from 20% the week prior.

Econ Data – Atlanta Fed Turns Negative on GDP; Weak Stats

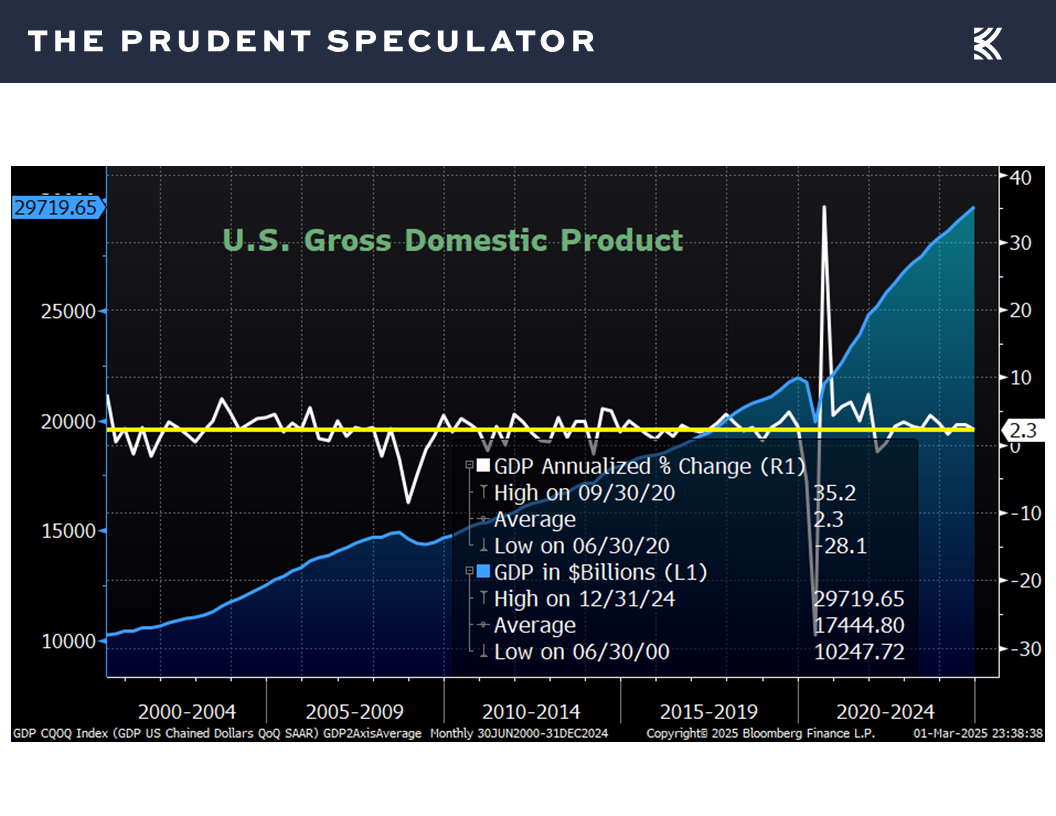

The latest batch of economic numbers was the culprit, even as the second estimate out last week from Uncle Sam for real Q4 2024 GDP growth held steady at positive 2.3%, with the nominal level of domestic output climbing to nearly $30 trillion.

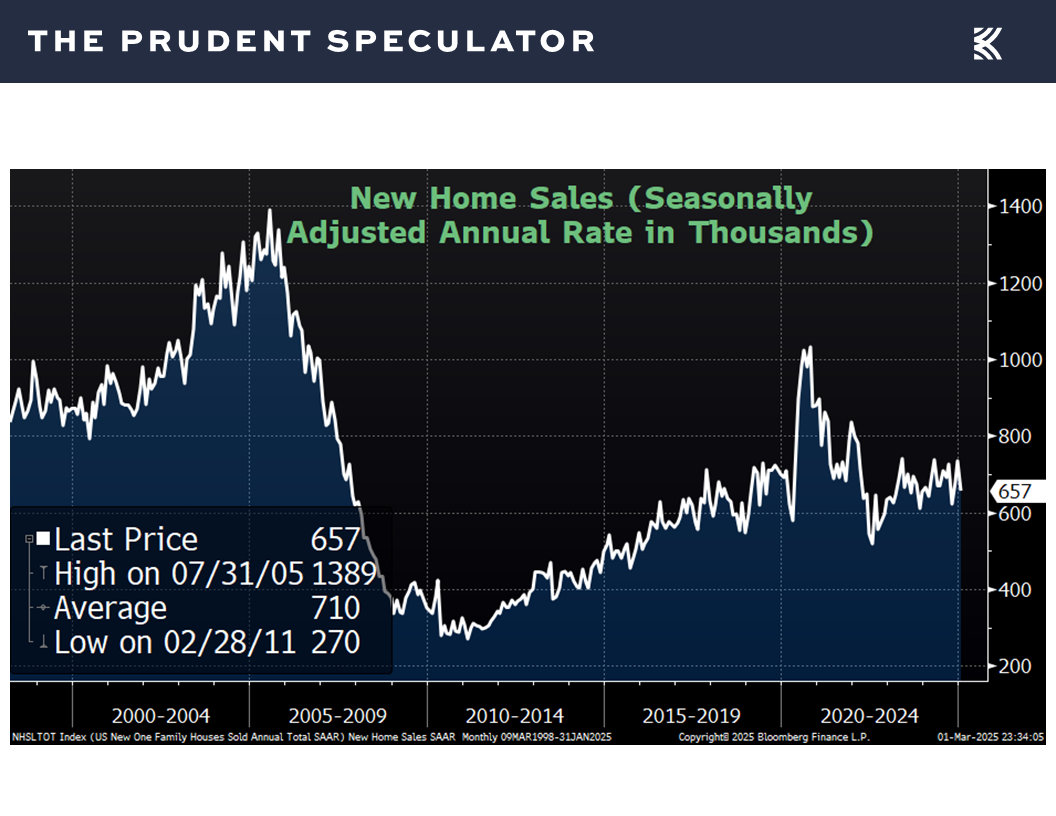

Certainly, the current quarter’s GDP figures aren’t helped by a weaker-than-expected drop in new home sales for January,

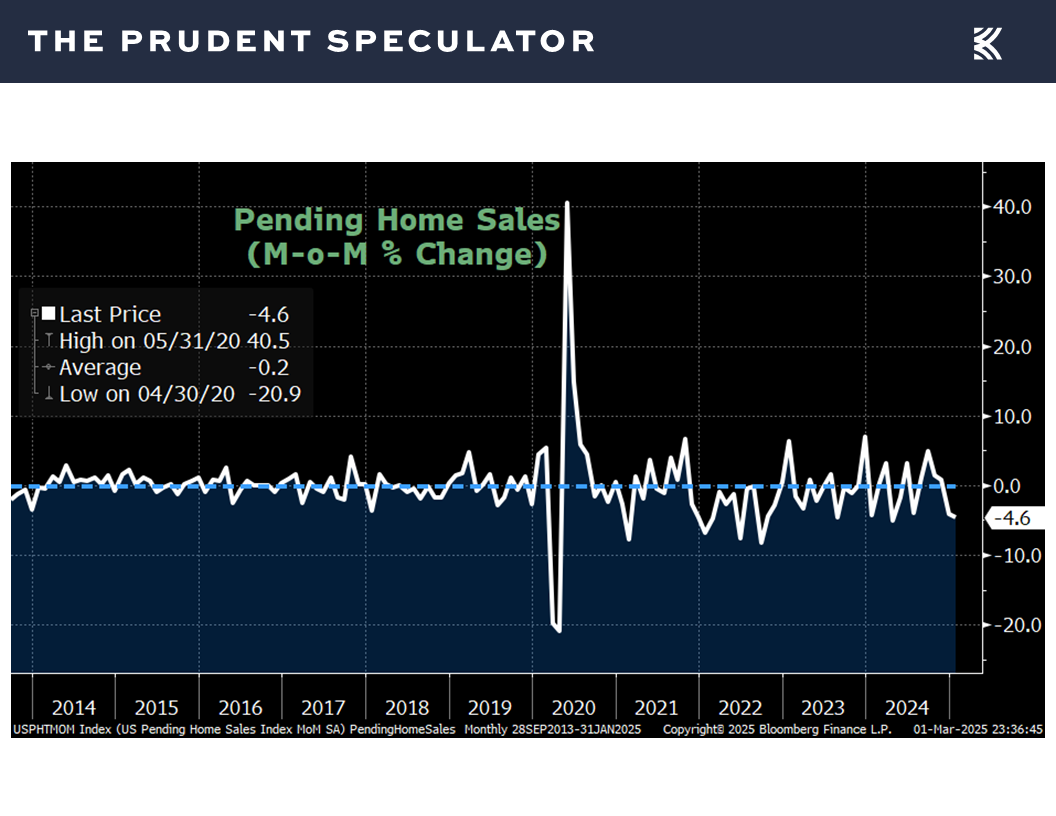

a much-worse-than-forecast 4.6% skid in pending home sales for January,

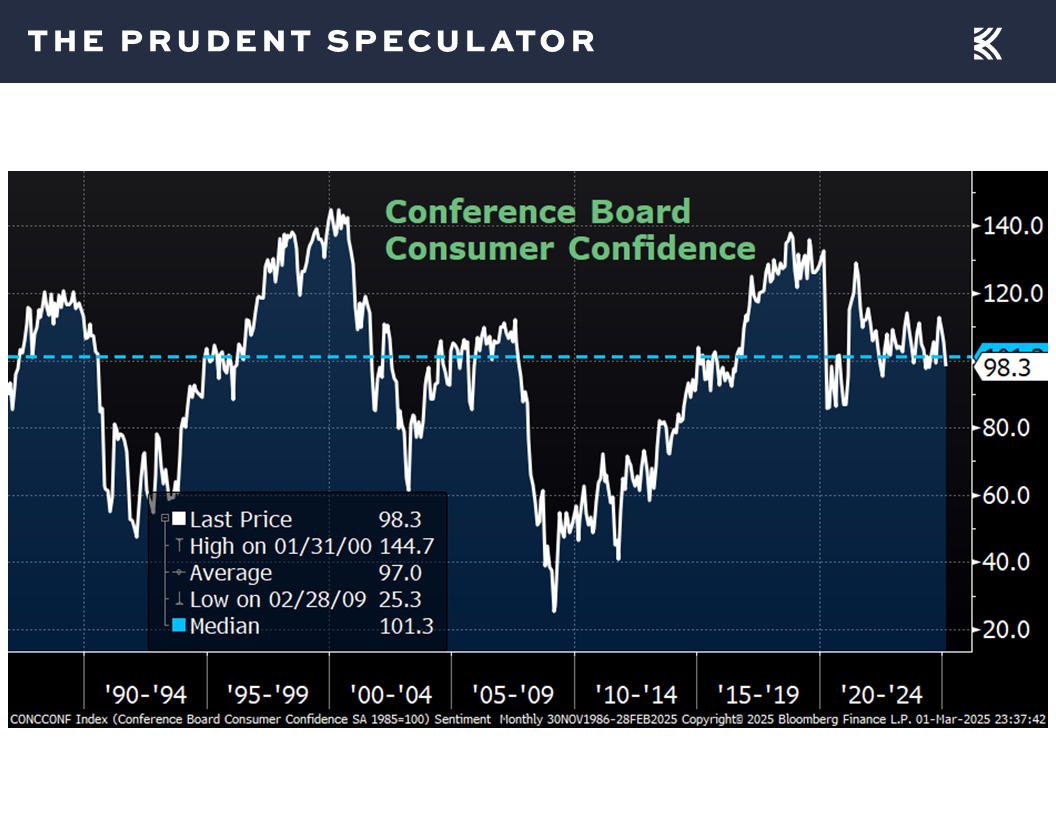

a decline in the Conference Board’s measure of consumer confidence for February to 98.3, down from January’s revised figure of 105.3 and the consensus projection of 102.5,

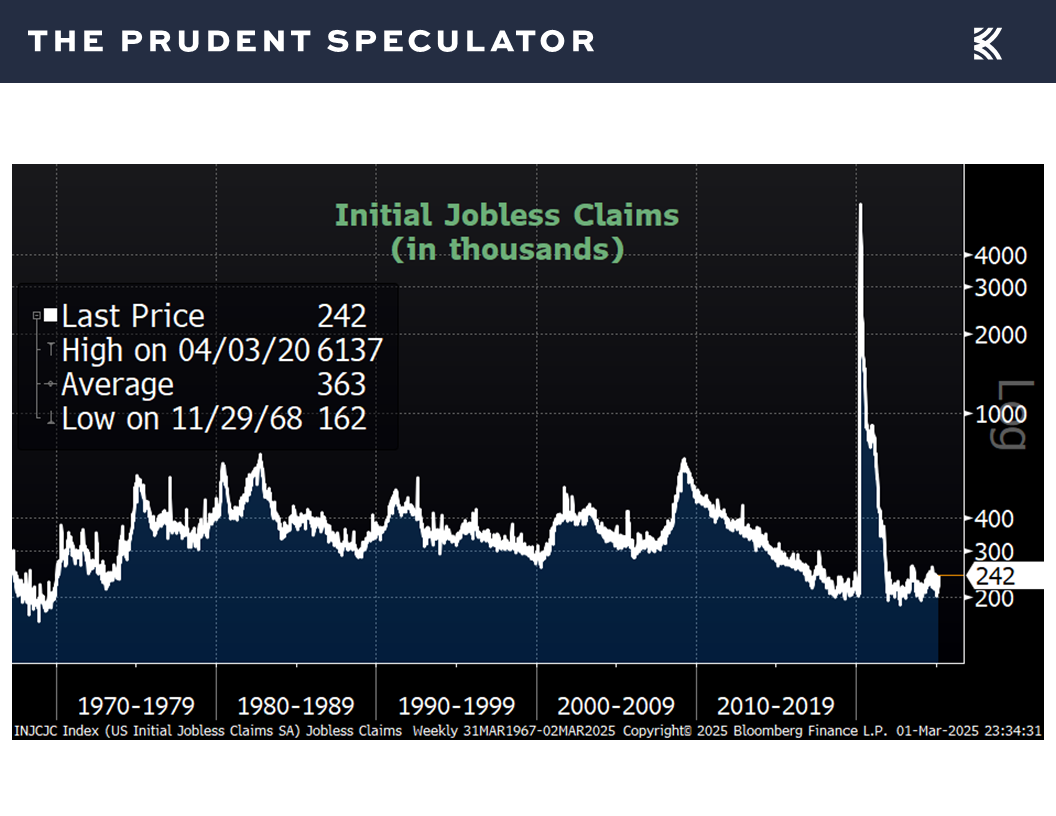

and a jump in first-time filings for unemployment benefits in the latest week to 242,000, versus 219,000 for the week prior.

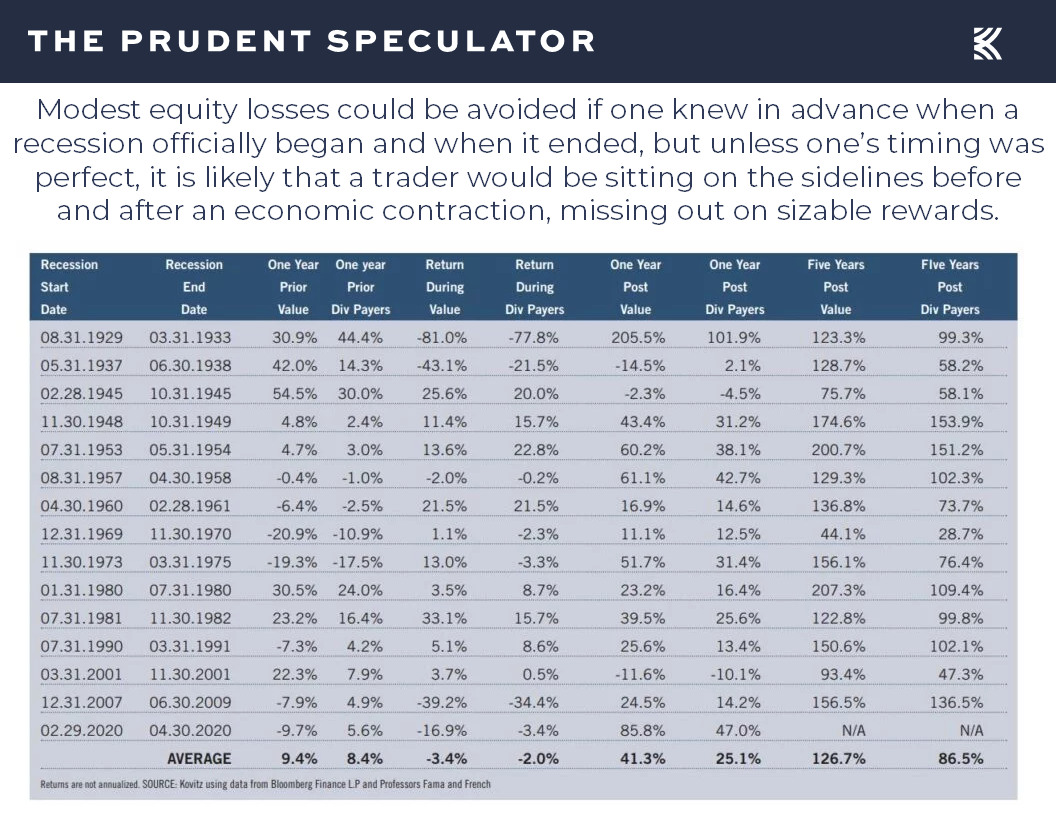

Perspective – Holding Through Recessions

While the odds of recession (two quarters of negative GDP growth) remain low, the question investors who are concerned about an economic downturn should be asking is how have stocks performed before, during and after prior periods of “official” contraction?

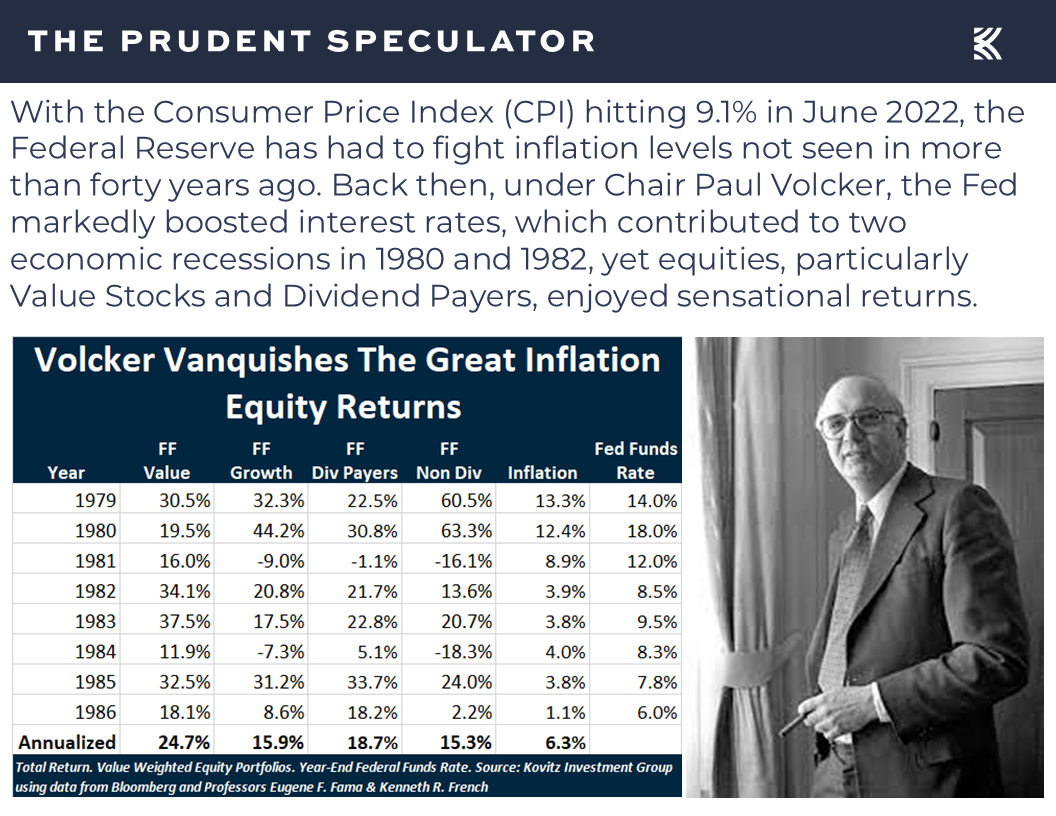

As the chart above illustrates, getting the timing right is the only problem with engaging in market timing around prior economic downturns, as it isn’t easy to know when a recession begins and ends. These days, we might argue that the most relevant prior period would be the Great Inflation of the early-1980’s, which included two recessions…and fantastic returns for stocks, led by Value and Dividend Payers.

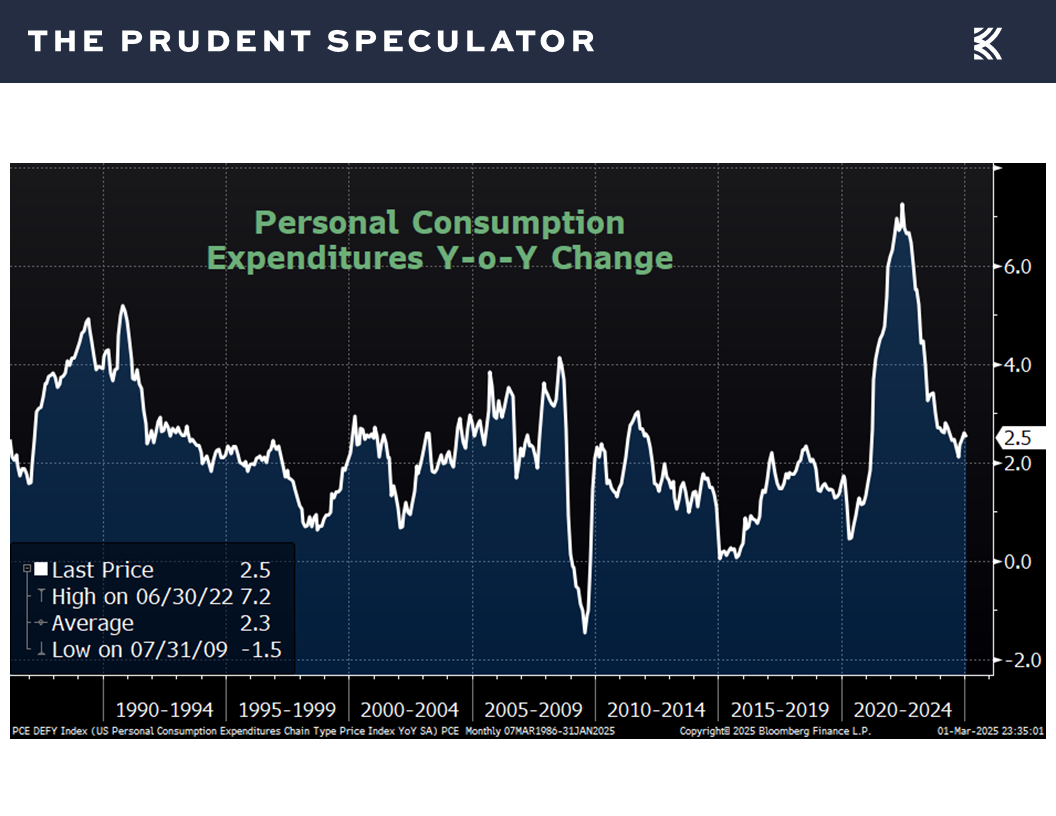

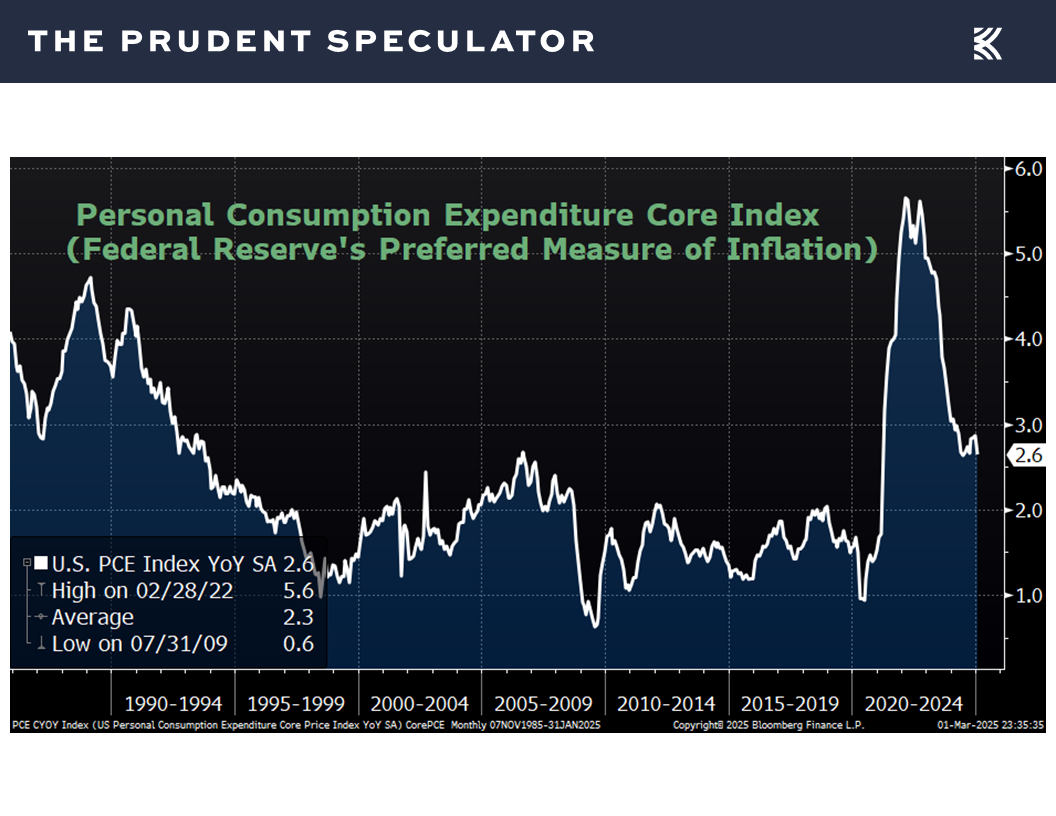

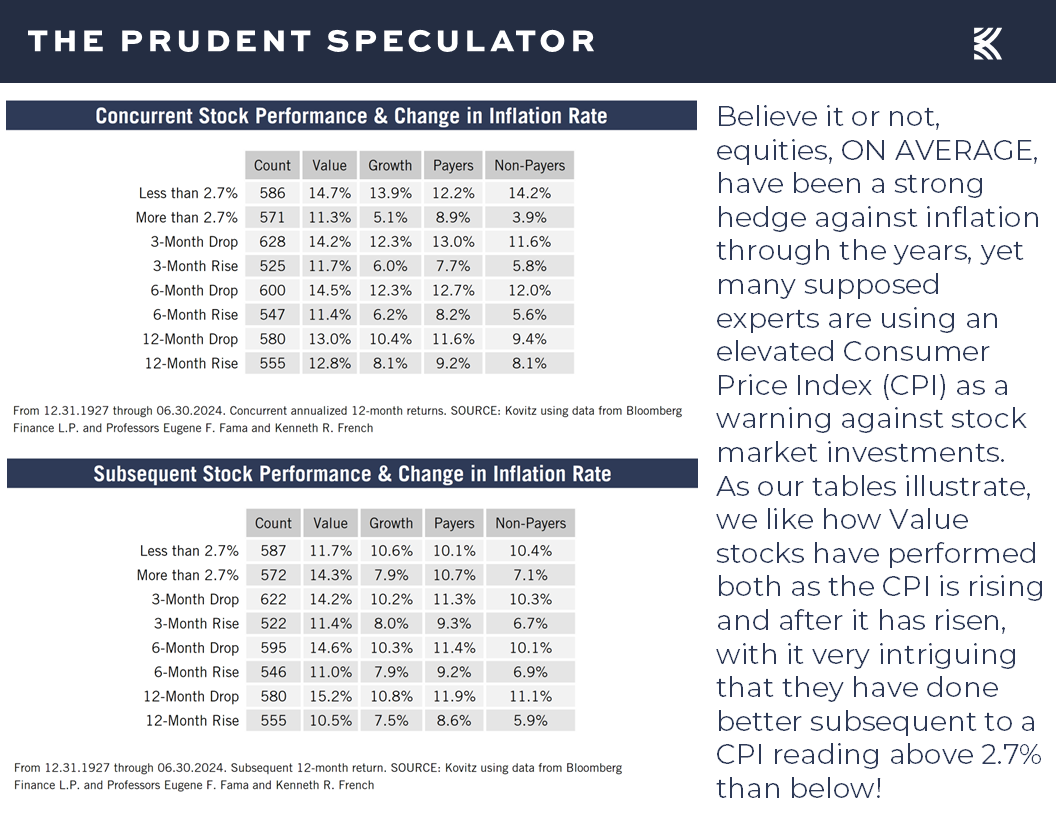

Inflation – In Line PCE Numbers; Stocks a Great Hedge

And, speaking of inflation, a reason that stocks caught a bid on Friday was that the Federal Reserve’s preferred measure of price pressures, the personal consumption expenditure (PCE), came in as expected in January with a 2.5% increase, down from 2.6% in December,

with the core PCE’s (excludes volatile food and energy prices) 2.6% year-over-year increase for January also matching forecasts and dropping from a revised advance of 2.9% in December.

Of course, the historical evidence show that stocks have been a great hedge against inflation, on average, no matter if it is rising or falling,

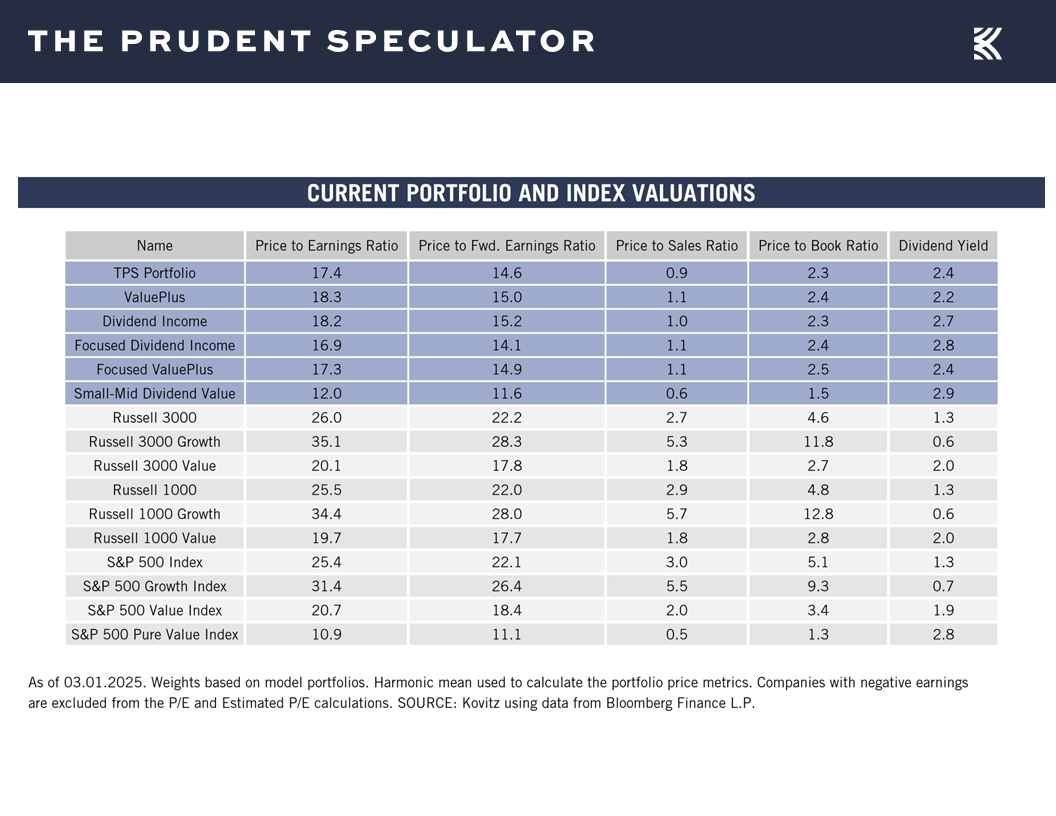

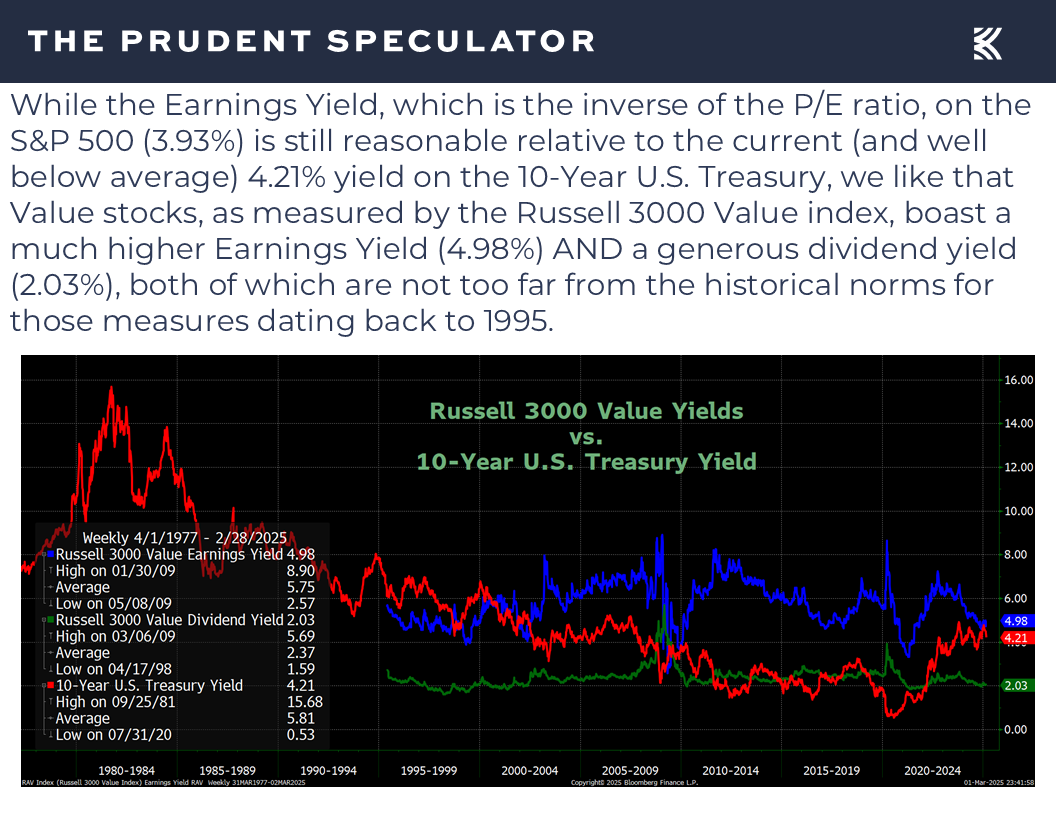

Valuations – Value Stocks Even More Reasonably Priced

while the economic weakness last week led to a drop in interest rates, which should make equities, especially those of the Value variety, even more attractive,

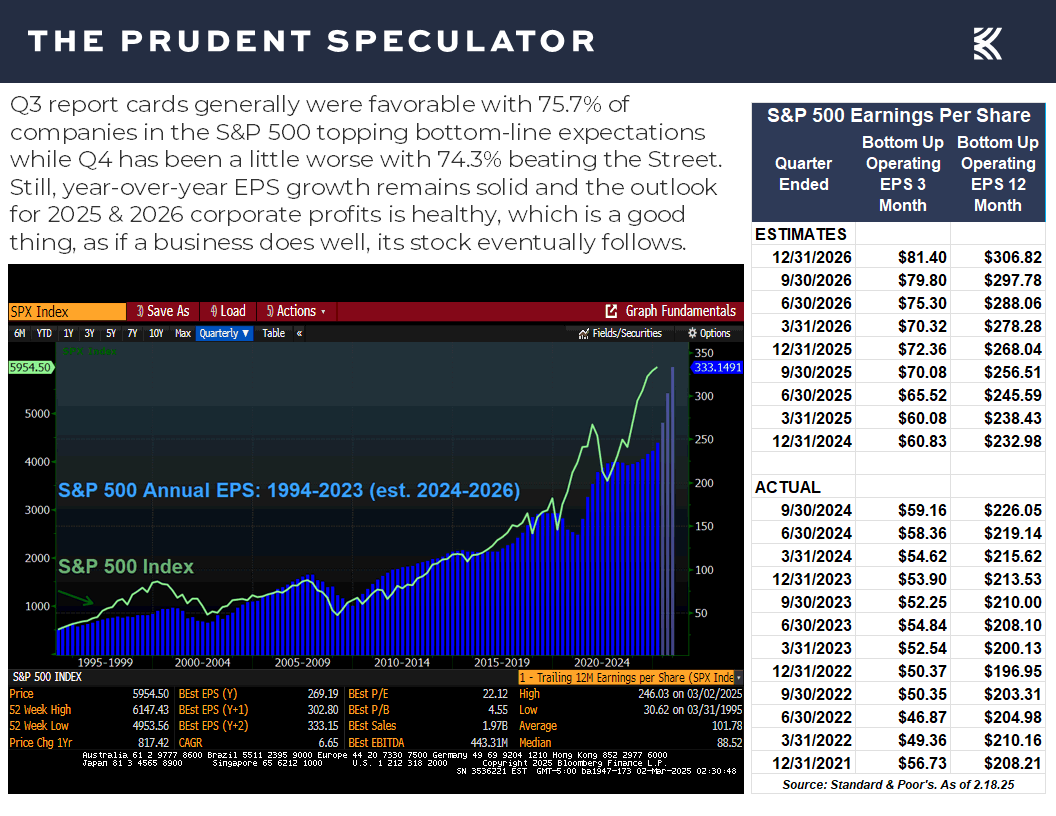

especially as the earnings yield increased and corporate profits are likely to show solid growth this year and next.

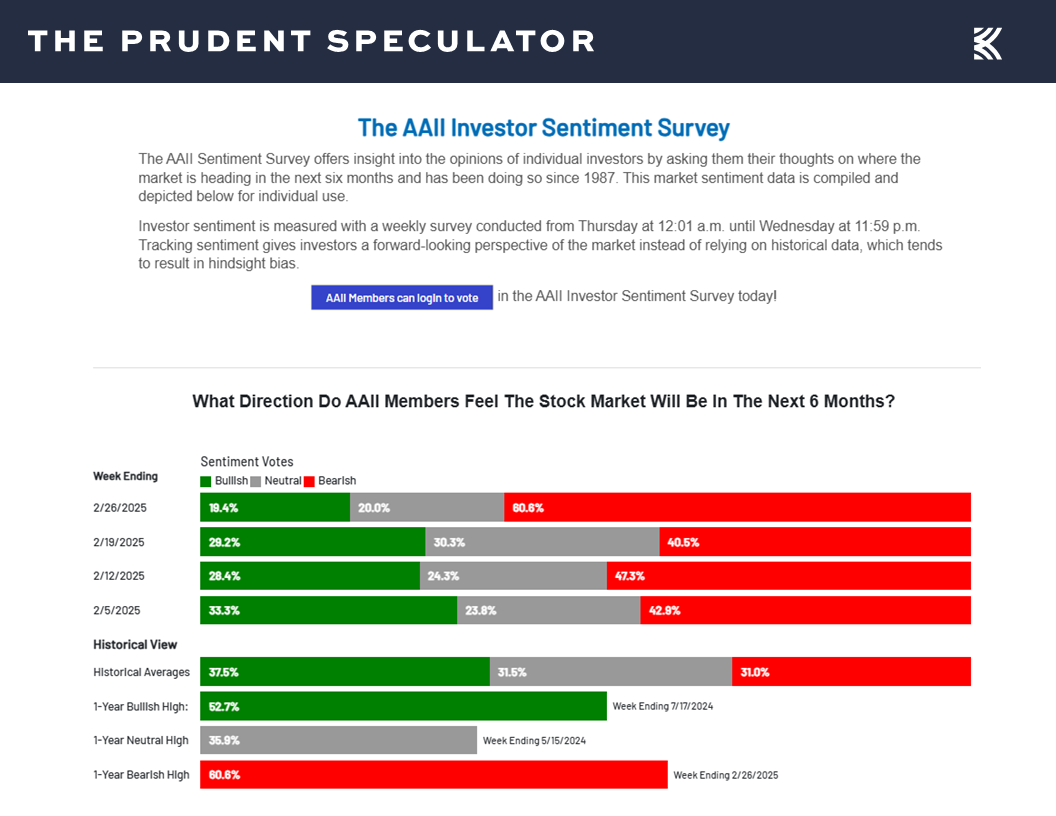

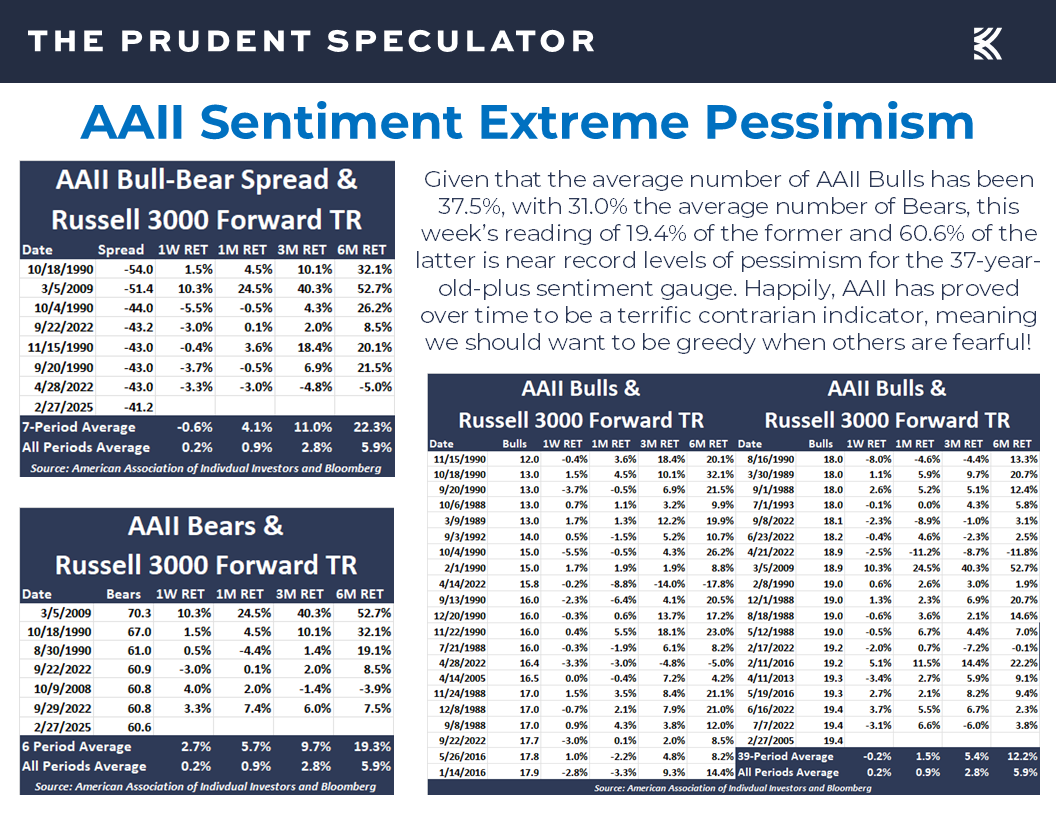

Sentiment – Major AAII Contrarian Buy Signal

As always, we are braced for more equity market turbulence, but contrarian investors received a major dose of good news on Thursday, courtesy of the American Association of Individual Investors Sentiment Survey (AAII). For the latest week, the number of optimists plunged to 19.4% while the number of pessimists ballooned to 60.6%, putting the Bull-Bear spread at -41.2, the eighth-most-Bearish reading in the 37-plus-year history of the weekly gauge.

Not surprisingly, given that it has long paid to be very greedy when others are very fearful, the respective near-term subsequent return figures, on average, have been sensational over the ensuing one, three and six months for the 7 times the AAII Bull-Bear Spread has been lower than -41.2, the 6 times the number of AAII Bears has been greater than 60.6 and the 39 times the number of AAII Bulls has been fewer than 19.4!

Stock News – Updates on eight stocks seven different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Value Stocks, Volatility, Inflation and AAII Sentiment

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Value Stocks, Volatility, Inflation and AAII Sentiment. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

TPS Webinar – Join John, Jason & Chris on Thursday, March 6 at 11:00 AM Pacific; 2:00 PM Eastern

Value – Good Week, Year, Decade and Half-Century for Inexpensively Priced Stocks

Headlines – Stocks Have Overcome All Prior Disconcerting Events

Volatility – Stocks Go Up and Down in the Short Term, But Have Provided Handsome Rewards in the Long-Term

Econ Data – Atlanta Fed Turns Negative on GDP; Weak Stats

Perspective – Holding Through Recessions

Inflation – In Line PCE Numbers; Stocks a Great Hedge

Valuations – Value Stocks Even More Reasonably Priced

Sentiment – Major AAII Contrarian Buy Signal

Stock News – Updates on GM, FDP, AXAHY, CIVI, AMT, SOLV & PNW

TPS Webinar – Join John, Jason & Chris on Thursday, March 6 at 11:00 AM Pacific; 2:00 PM Eastern

Join us for an exclusive webinar where I will cut through the noise and debunk three market myths that are presently circulating in the financial press. We will also hold a live Q&A session where Jason Clark and Chris Quigley will join me so members of the TPS community can ask about anything from value stocks to economic trends to how A.I. is impacting investment decisions.

Mark your calendars for Thursday, March 6 at 11:00 AM PT / 2:00 PM ET. Space is limited, so be sure to sign up here:

https://kovitz.zoom.us/webinar/register/9717297096423/WN_TNkq-QgdQ46lPdWjIh6PwQ

Value – Good Week, Year, Decade and Half-Century for Inexpensively Priced Stocks

Providing yet another reminder that it is very tough to predict short-term gyrations in stocks, news that arguably should have sent the markets higher on Thursday was greeted with a big selloff and headlines that arguably should have pushed equities lower on Friday saw stocks end a volatile session with markedly higher prices.

Headlines – Stocks Have Overcome All Prior Disconcerting Events

To be sure, it is always a market of stocks and not simply a stock market, as it was an ugly week overall for the Tech sector, with the Nasdaq Composite index off some 3.5% and semiconductor titan Nvidia down more than 7%. Value stocks performed much better, reminding investors that despite inevitable volatility along the way, they have a historical propensity for superior long-term returns,

while they have performed very well over the last two decades relative to international equities, commodities, bonds and U.S. treasuries.

While we often equate ourselves to the turtle in the Tortoise and the Hare fable, as we have always strived to grow wealthy slowly, we don’t mind that the get-rich-quick crowd has discovered some of our holdings. Yes, some of our stocks might today be classified as more Growth than Value, but we have long been eclectic in our approach to buying and harvesting undervalued stocks.

We have never been bound by arbitrary definitions of Value and Growth, so even a high-flyer like Nvidia could be a purchase candidate if it dropped into the double-digits (we offered our take on your Editor’s Forbes Blog last week: https://www.forbes.com/sites/johnbuckingham/2025/02/28/is-3-trillion-nvidia-nvda-a-value-stock/), but the composite valuations on our portfolios always have been deep in the Value camp.

Volatility – Stocks Go Up and Down in the Short Term, But Have Provided Handsome Rewards in the Long-Term

To be sure, there were worries last week as tariff talk again heated up,

and there was heightened drama on the geopolitical stage, but we continued to stay on an even emotional keel, with our patience and discipline always supported by the historical data that shows stocks have overcome every previous disconcerting event in the fullness of time.

No doubt, it is different this time, just as it has been different every time, and a new bogeyman emerged last week as the latest estimate for real (inflation-adjusted) U.S. GDP growth in the current quarter from the Atlanta Fed was slashed to negative 1.5% on Friday from positive 2.3% earlier in the week,

and the odds of recession, as tabulated by Bloomberg, rose to 25%, up from 20% the week prior.

Econ Data – Atlanta Fed Turns Negative on GDP; Weak Stats

The latest batch of economic numbers was the culprit, even as the second estimate out last week from Uncle Sam for real Q4 2024 GDP growth held steady at positive 2.3%, with the nominal level of domestic output climbing to nearly $30 trillion.

Certainly, the current quarter’s GDP figures aren’t helped by a weaker-than-expected drop in new home sales for January,

a much-worse-than-forecast 4.6% skid in pending home sales for January,

a decline in the Conference Board’s measure of consumer confidence for February to 98.3, down from January’s revised figure of 105.3 and the consensus projection of 102.5,

and a jump in first-time filings for unemployment benefits in the latest week to 242,000, versus 219,000 for the week prior.

Perspective – Holding Through Recessions

While the odds of recession (two quarters of negative GDP growth) remain low, the question investors who are concerned about an economic downturn should be asking is how have stocks performed before, during and after prior periods of “official” contraction?

As the chart above illustrates, getting the timing right is the only problem with engaging in market timing around prior economic downturns, as it isn’t easy to know when a recession begins and ends. These days, we might argue that the most relevant prior period would be the Great Inflation of the early-1980’s, which included two recessions…and fantastic returns for stocks, led by Value and Dividend Payers.

Inflation – In Line PCE Numbers; Stocks a Great Hedge

And, speaking of inflation, a reason that stocks caught a bid on Friday was that the Federal Reserve’s preferred measure of price pressures, the personal consumption expenditure (PCE), came in as expected in January with a 2.5% increase, down from 2.6% in December,

with the core PCE’s (excludes volatile food and energy prices) 2.6% year-over-year increase for January also matching forecasts and dropping from a revised advance of 2.9% in December.

Of course, the historical evidence show that stocks have been a great hedge against inflation, on average, no matter if it is rising or falling,

Valuations – Value Stocks Even More Reasonably Priced

while the economic weakness last week led to a drop in interest rates, which should make equities, especially those of the Value variety, even more attractive,

especially as the earnings yield increased and corporate profits are likely to show solid growth this year and next.

Sentiment – Major AAII Contrarian Buy Signal

As always, we are braced for more equity market turbulence, but contrarian investors received a major dose of good news on Thursday, courtesy of the American Association of Individual Investors Sentiment Survey (AAII). For the latest week, the number of optimists plunged to 19.4% while the number of pessimists ballooned to 60.6%, putting the Bull-Bear spread at -41.2, the eighth-most-Bearish reading in the 37-plus-year history of the weekly gauge.

Not surprisingly, given that it has long paid to be very greedy when others are very fearful, the respective near-term subsequent return figures, on average, have been sensational over the ensuing one, three and six months for the 7 times the AAII Bull-Bear Spread has been lower than -41.2, the 6 times the number of AAII Bears has been greater than 60.6 and the 39 times the number of AAII Bulls has been fewer than 19.4!

Stock News – Updates on eight stocks seven different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.