The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Value Stocks, Historical Events, Volatility and Interest Rates. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

Headlines – Not All the News is Bad

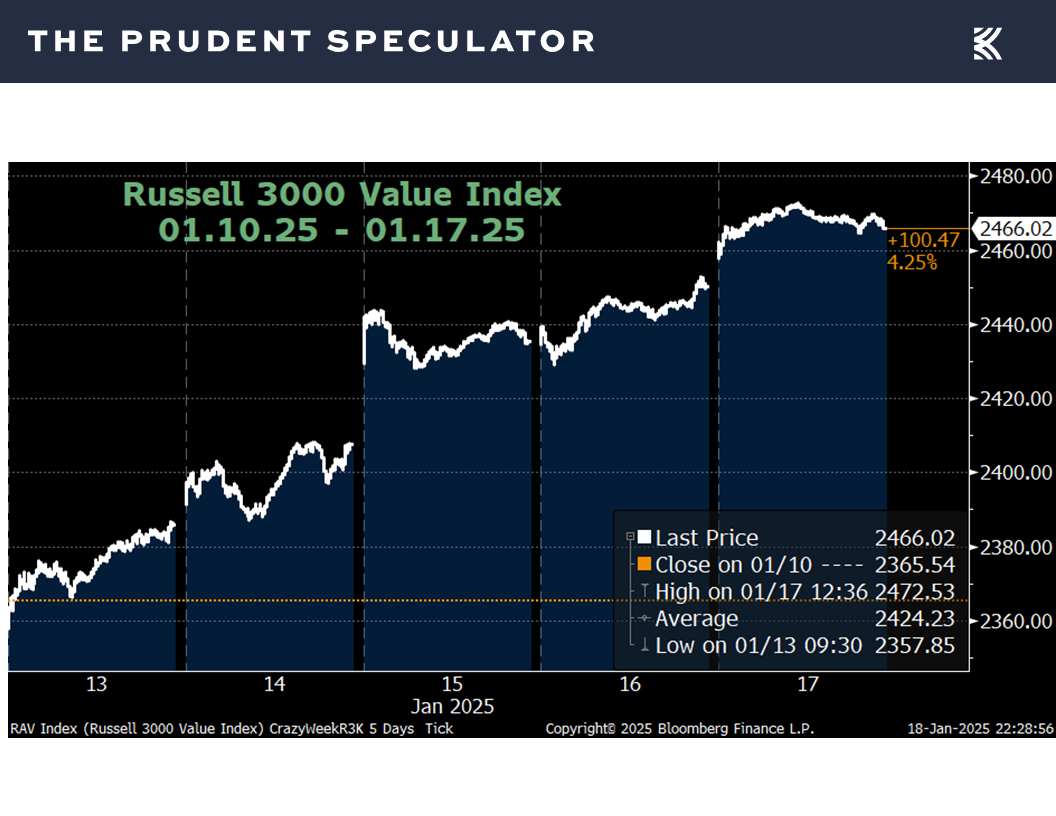

Value – 48th Best Week for R3KV Since 1995

Historical Evidence – Volatility & Disconcerting Events, but Long-Term Trend is Up

Market Timing – Only Problem is Getting the Timing Right

Calendar – First 5 Days, Seasonality, Years Ending in 5 Historical Numbers all Favorable

Corporate Profits – Healthy EPS Growth Still the Forecast

Inflation – Lower-than-Expected PPI & CPI

Interest Rates – Stocks Have Performed Fine, on Average, No Matter the Direction of Rates

Valuations – Value Stocks Remain Reasonably Priced

Stock News – Updates on BLK, BK, JPM, GS, C, PNC, BAC, MS, OZK, TFC & CFG

Headlines – Not All the News is Bad

It wasn’t quite like the weather in Hawaii where a fleeting rainstorm often gives way quickly to more sunshine, but what a difference a week makes! Indeed, after a tough first couple of weeks to the year, with several very disconcerting events,

the news turned positive on several fronts (geopolitics, corporate profits and inflation),

Value – 48th Best Week for R3KV Since 1995

and equities enjoyed a handsome rebound, led by Value stocks, with the Russell 3000 Value index jumping more than 4%,

the 48th best weekly return since that benchmark was launched in 1995.

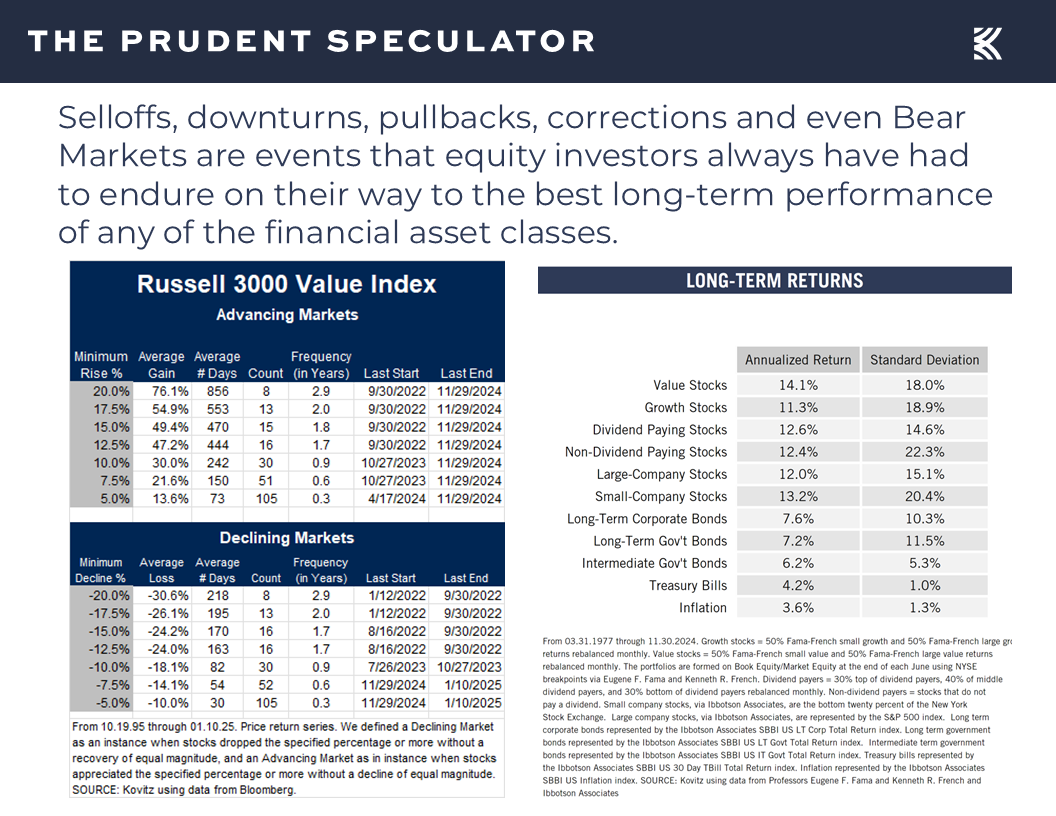

Historical Evidence – Volatility & Disconcerting Events, but Long-Term Trend is Up

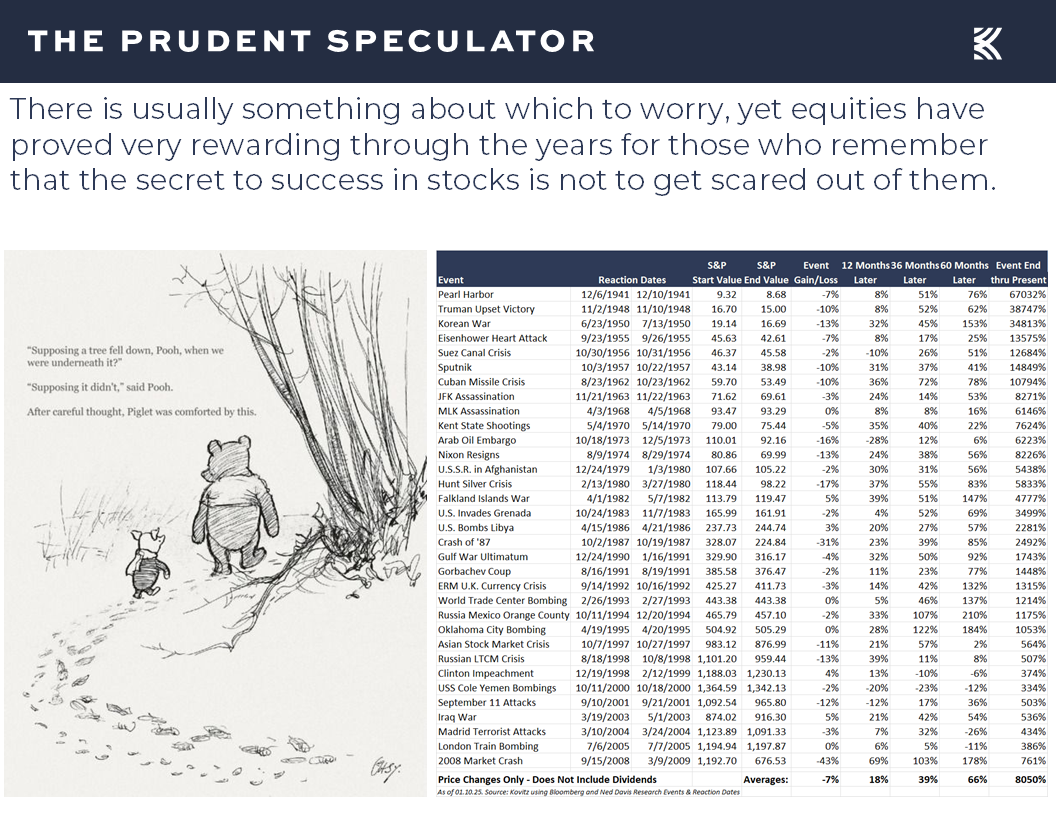

Certainly, stocks could head south as volatility is always part of the investment equation, but the long-term trend in equities historically always has been higher,

with frightening headlines always overcome in the fullness of time,

Market Timing – Only Problem is Getting the Timing Right

and those who think they can outguess market gyrations often shooting themselves in the foot,

as evidenced yet again by the preponderance of pessimism (more Bears than Bulls in the American Association of Individual Investors weekly Investor Sentiment Survey) on Main Street heading into last week’s big rally.

Calendar – First 5 Days, Seasonality, Years Ending in 5 Historical Numbers all Favorable

To be sure, we had no crystal ball that told us stocks would soar last week, but the odds tell us that the longer we hold Value Stocks and Dividend Payers, the greater the likelihood that we will make money,

while the first five days of January being positive (as they were this time around) historically bodes well for the rest of the year.

January is part of the seasonally more favorable six months of the year.

and years ending in 5 heretofore have enjoyed sensational returns, on average.

Corporate Profits – Healthy EPS Growth Still the Forecast

True, many would question the statistical significance of the last three charts. More importantly, we know that stock prices over time have tracked corporate profits, with sustained downturns coinciding with an earnings contraction. Happily, EPS have shown significant growth over the long term, and a sizable increase in earnings is the current forecast for 2025,

…given a very low probability of an economic recession,

with the latest estimate for Q4 2024 GDP growth from the Atlanta Fed moving up last week to 3.0% from 2.7% the week prior,

and the Federal Reserve Board members and Federal Reserve Bank presidents projecting 2.1% real (inflation-adjusted) GDP growth for 2025.

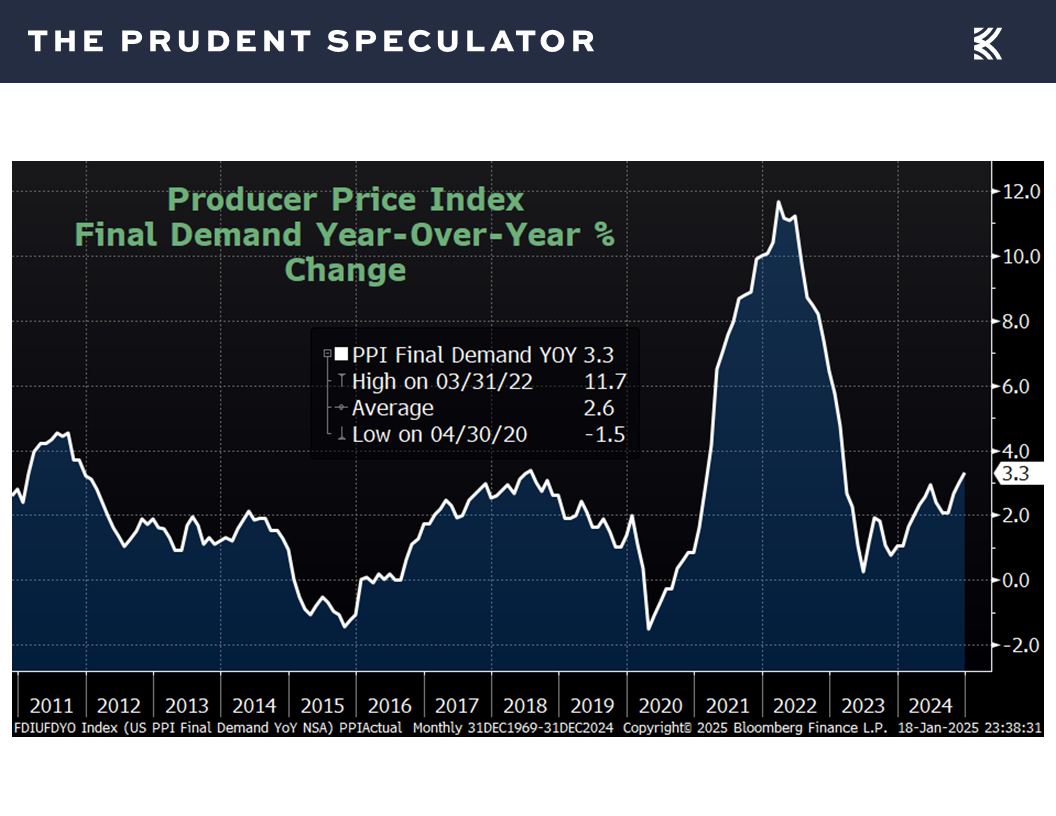

Inflation – Lower-than-Expected PPI & CPI

And speaking of inflation, what really ignited the equity advance last week was a lower-than-expected year-over-year increase in prices at the wholesale level of 3.3% last month vs. the forecasted rise in the producer price index of 3.5%,

…and the even-more-important consumer price index (CPI) for December climbing 2.9%, in line with estimates,

but the so-called core CPI, which excludes volatile food and energy prices, advancing “only” 3.2%, less than the 3.3% consensus projection.

Though years of evidence show that stocks don’t mind if the Federal Reserve is easing or tightening monetary policy,

or if government bond yields are rising or falling,

Interest Rates – Stocks Have Performed Fine, on Average, No Matter the Direction of Rates

traders were buoyed last week by a drop in the expected 2025 year-end Fed Funds rate betting to a rate of 3.95% from 4.04% the week prior,

…and a dip in the yield on the 10-Year U.S. Treasury to 4.63%, down from 4.76% at the end of the preceding week.

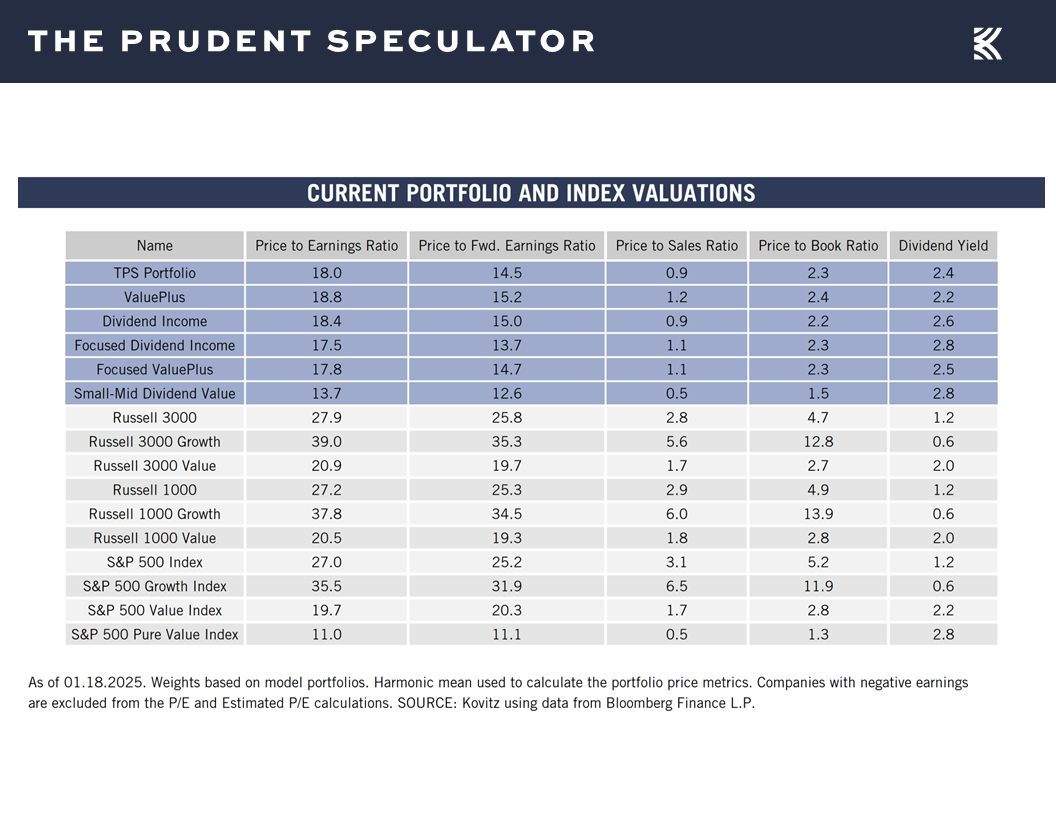

Valuations – Value Stocks Remain Reasonably Priced

No doubt, we liked what we saw last week with Value stocks leading the equity charge, especially as there is a very long way to go for inexpensively priced companies to catch up with their Growth peers, much less reassert their long-term propensity to outperform,

while we still think the Russell 3000 Value index is attractively priced,

even as it and its fellow Value gauges have turned in strong returns relative to international stocks, commodities and bonds for much of the past two decades.

We are always braced for moves to the downside, but we continue to sleep very well at night given the valuation metrics on our broadly diversified portfolios of what we believe are undervalued stocks.

Stock News – Updates on eleven stocks in the financial sector

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Value Stocks, Historical Events, Volatility and Interest Rates

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Value Stocks, Historical Events, Volatility and Interest Rates. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

Headlines – Not All the News is Bad

Value – 48th Best Week for R3KV Since 1995

Historical Evidence – Volatility & Disconcerting Events, but Long-Term Trend is Up

Market Timing – Only Problem is Getting the Timing Right

Calendar – First 5 Days, Seasonality, Years Ending in 5 Historical Numbers all Favorable

Corporate Profits – Healthy EPS Growth Still the Forecast

Inflation – Lower-than-Expected PPI & CPI

Interest Rates – Stocks Have Performed Fine, on Average, No Matter the Direction of Rates

Valuations – Value Stocks Remain Reasonably Priced

Stock News – Updates on BLK, BK, JPM, GS, C, PNC, BAC, MS, OZK, TFC & CFG

Headlines – Not All the News is Bad

It wasn’t quite like the weather in Hawaii where a fleeting rainstorm often gives way quickly to more sunshine, but what a difference a week makes! Indeed, after a tough first couple of weeks to the year, with several very disconcerting events,

the news turned positive on several fronts (geopolitics, corporate profits and inflation),

Value – 48th Best Week for R3KV Since 1995

and equities enjoyed a handsome rebound, led by Value stocks, with the Russell 3000 Value index jumping more than 4%,

the 48th best weekly return since that benchmark was launched in 1995.

Historical Evidence – Volatility & Disconcerting Events, but Long-Term Trend is Up

Certainly, stocks could head south as volatility is always part of the investment equation, but the long-term trend in equities historically always has been higher,

with frightening headlines always overcome in the fullness of time,

Market Timing – Only Problem is Getting the Timing Right

and those who think they can outguess market gyrations often shooting themselves in the foot,

as evidenced yet again by the preponderance of pessimism (more Bears than Bulls in the American Association of Individual Investors weekly Investor Sentiment Survey) on Main Street heading into last week’s big rally.

Calendar – First 5 Days, Seasonality, Years Ending in 5 Historical Numbers all Favorable

To be sure, we had no crystal ball that told us stocks would soar last week, but the odds tell us that the longer we hold Value Stocks and Dividend Payers, the greater the likelihood that we will make money,

while the first five days of January being positive (as they were this time around) historically bodes well for the rest of the year.

January is part of the seasonally more favorable six months of the year.

and years ending in 5 heretofore have enjoyed sensational returns, on average.

Corporate Profits – Healthy EPS Growth Still the Forecast

True, many would question the statistical significance of the last three charts. More importantly, we know that stock prices over time have tracked corporate profits, with sustained downturns coinciding with an earnings contraction. Happily, EPS have shown significant growth over the long term, and a sizable increase in earnings is the current forecast for 2025,

…given a very low probability of an economic recession,

with the latest estimate for Q4 2024 GDP growth from the Atlanta Fed moving up last week to 3.0% from 2.7% the week prior,

and the Federal Reserve Board members and Federal Reserve Bank presidents projecting 2.1% real (inflation-adjusted) GDP growth for 2025.

Inflation – Lower-than-Expected PPI & CPI

And speaking of inflation, what really ignited the equity advance last week was a lower-than-expected year-over-year increase in prices at the wholesale level of 3.3% last month vs. the forecasted rise in the producer price index of 3.5%,

…and the even-more-important consumer price index (CPI) for December climbing 2.9%, in line with estimates,

but the so-called core CPI, which excludes volatile food and energy prices, advancing “only” 3.2%, less than the 3.3% consensus projection.

Though years of evidence show that stocks don’t mind if the Federal Reserve is easing or tightening monetary policy,

or if government bond yields are rising or falling,

Interest Rates – Stocks Have Performed Fine, on Average, No Matter the Direction of Rates

traders were buoyed last week by a drop in the expected 2025 year-end Fed Funds rate betting to a rate of 3.95% from 4.04% the week prior,

…and a dip in the yield on the 10-Year U.S. Treasury to 4.63%, down from 4.76% at the end of the preceding week.

Valuations – Value Stocks Remain Reasonably Priced

No doubt, we liked what we saw last week with Value stocks leading the equity charge, especially as there is a very long way to go for inexpensively priced companies to catch up with their Growth peers, much less reassert their long-term propensity to outperform,

while we still think the Russell 3000 Value index is attractively priced,

even as it and its fellow Value gauges have turned in strong returns relative to international stocks, commodities and bonds for much of the past two decades.

We are always braced for moves to the downside, but we continue to sleep very well at night given the valuation metrics on our broadly diversified portfolios of what we believe are undervalued stocks.

Stock News – Updates on eleven stocks in the financial sector

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.