The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s Market Commentary, we discuss the Volatility, AAII Sentiment, Recessions and Stock News. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

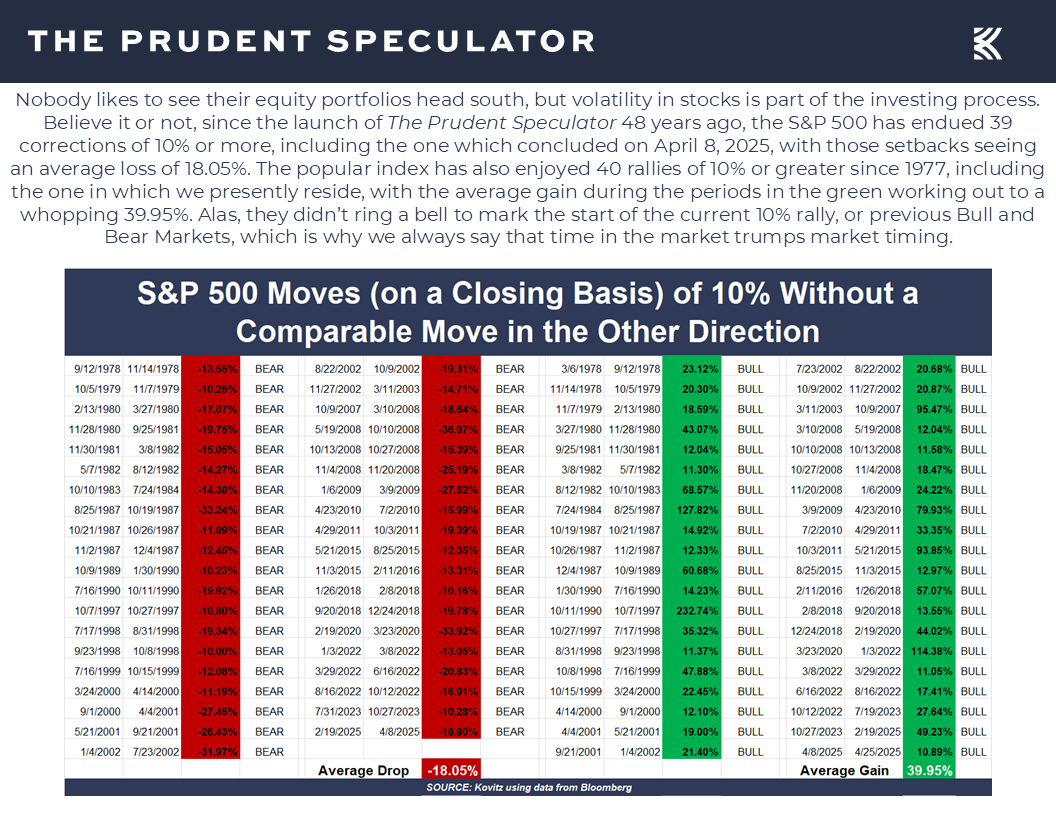

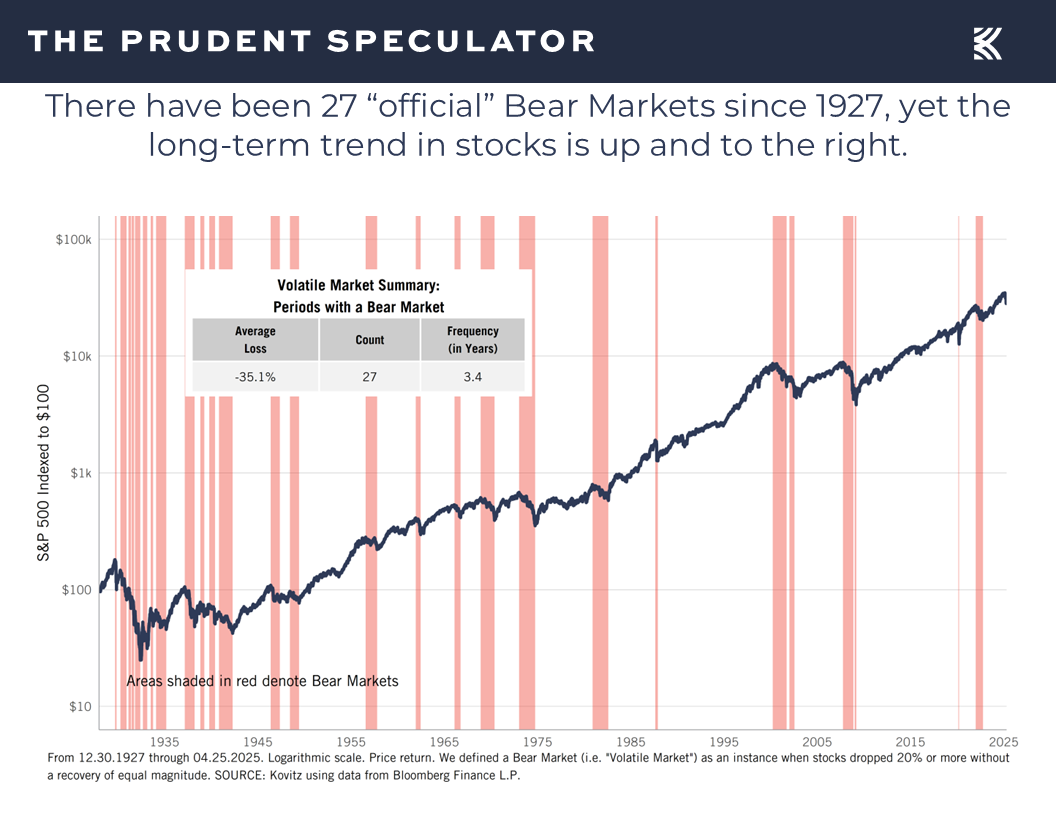

Volatility – 39th Correction since 1977 Officially Ended on Friday

Sentiment – Be Greedy When Others are Fearful

Econ Outlook – Mixed Numbers, But Modest Growth Still Forecast

Recessions – Risk Has Jumped, But History Shows Staying the Course the Right Move Even if a Contraction Were to Occur

Valuations – Ups and Downs Part of the Process, but We Like our Inexpensive Stocks

Stock News – Comments on CMA, ELV, VZ, LMT, COF, NEM, LRCX, WHR, IBM, HAS, CMCSA, INTC, GOOG, GILD & DLR

Volatility – 39th Correction since 1977 Officially Ended on Friday

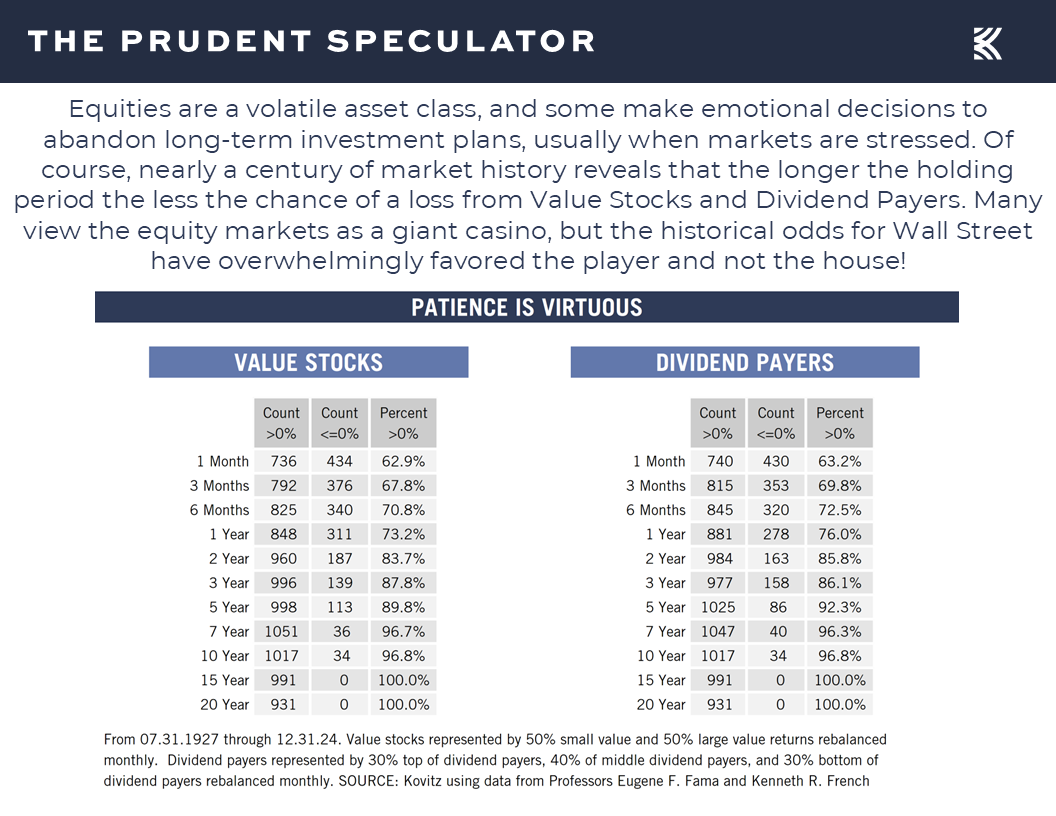

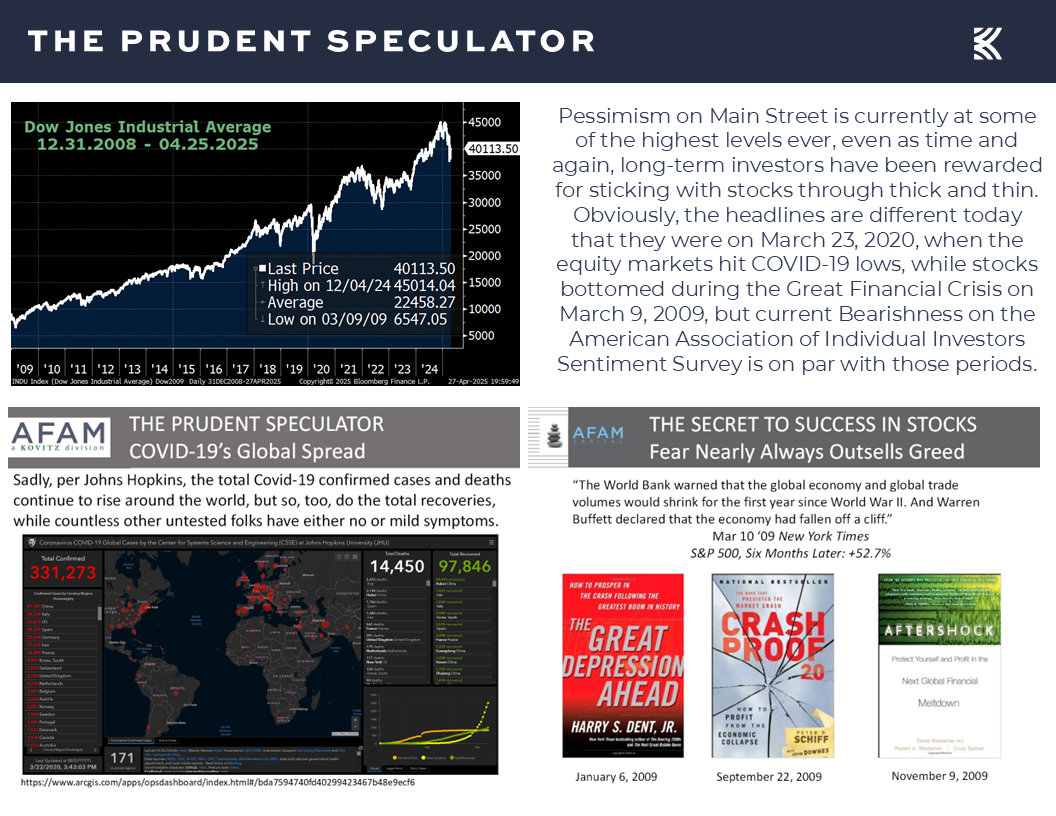

We understand that a social media post from the President, a media headline from a member of his cabinet or a negative response from a foreign government could trigger another big selloff, but the big rebound last week officially ended the 39th correction of 10% in the S&P 500 since the launch of The Prudent Speculator in 1977. Believe it or not, though the popular equity benchmark remains well into the red on the year and the average stock in the broad-based Russell 3000 index is off 11.9% in 2025, we are now in the 40th rally of 10% over the past 48 years,…

providing yet another reminder that while downside volatility is always part of the investment equation, every prior scary event has been overcome in the fullness of time,

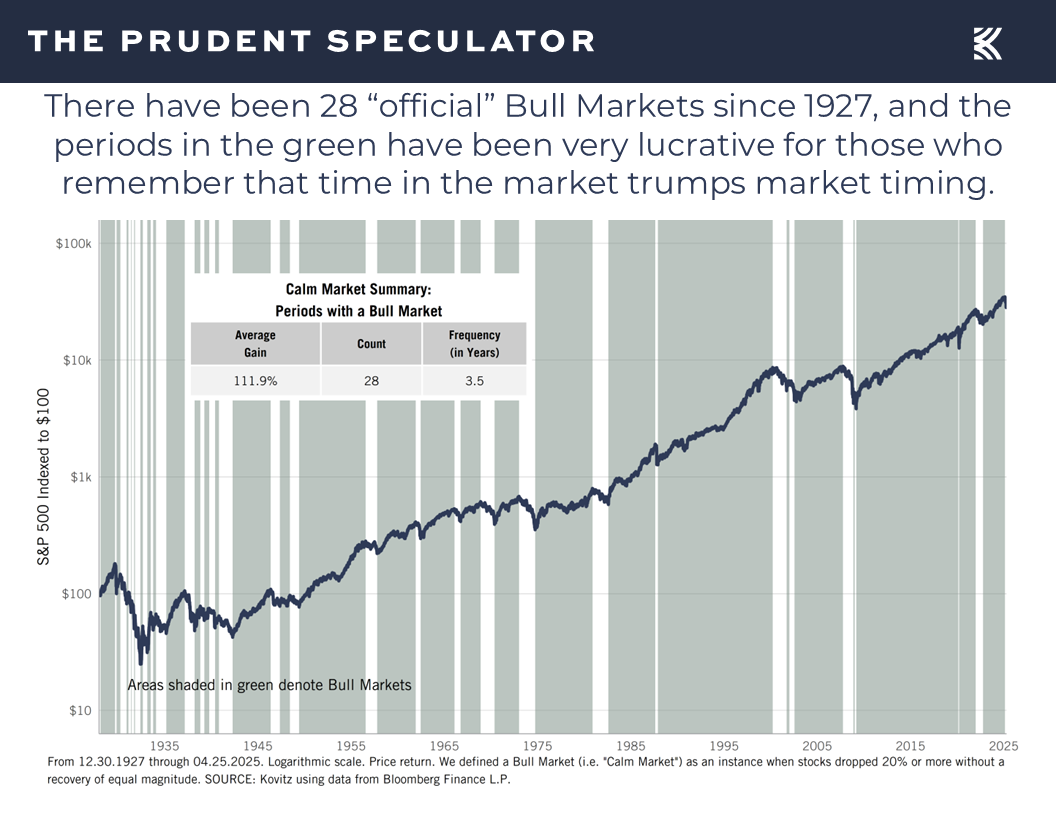

with even Bear Markets having been followed by Bull Markets where gains of far greater magnitude have taken place,

so much so that annualized long-term returns on stocks, led by Value and Dividend Payers, have been in the 9% to 13% range.

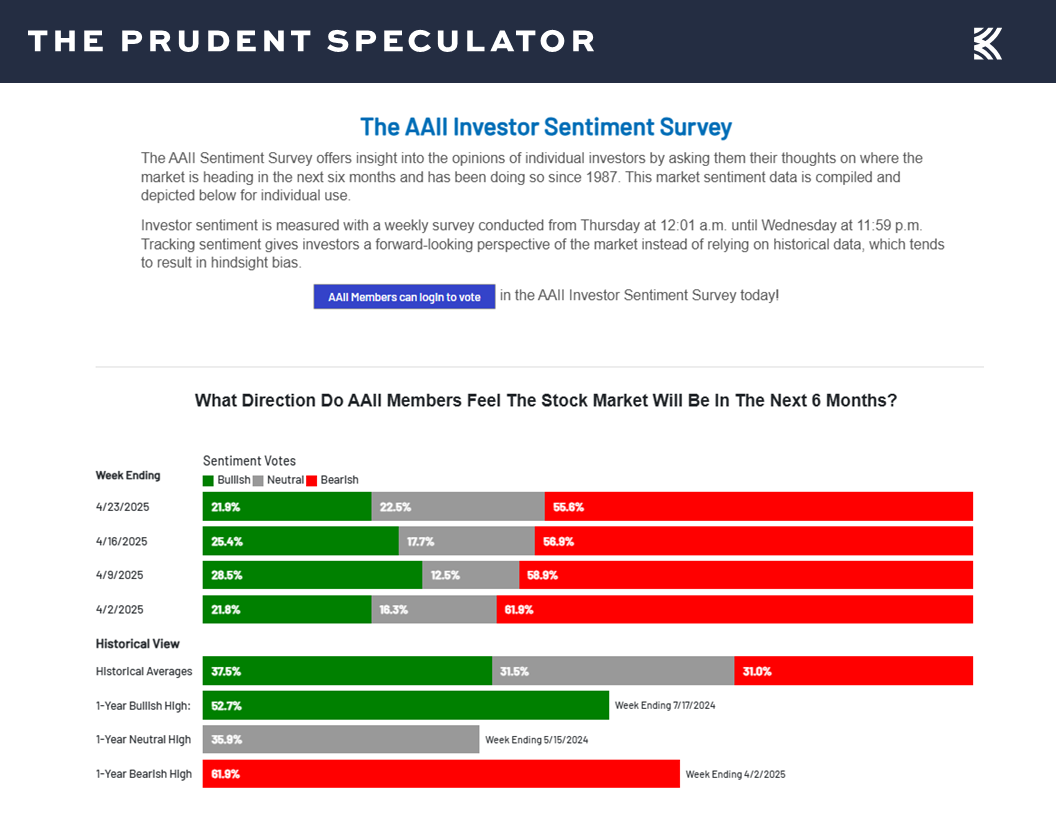

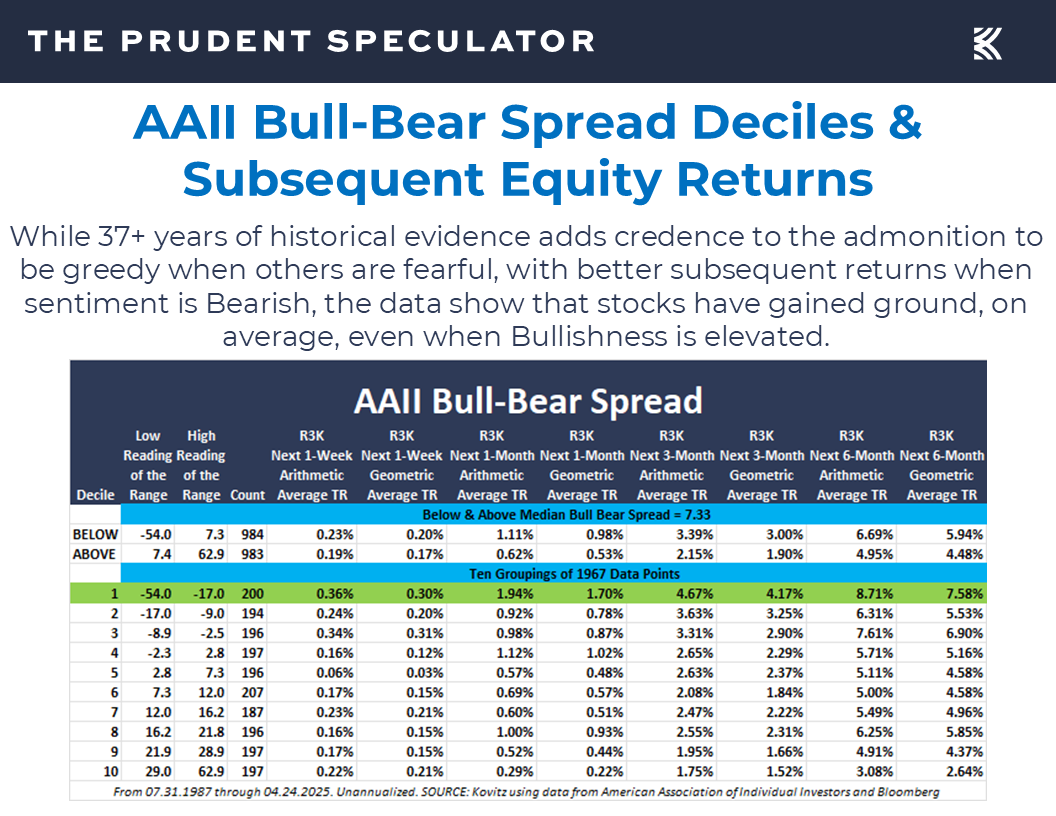

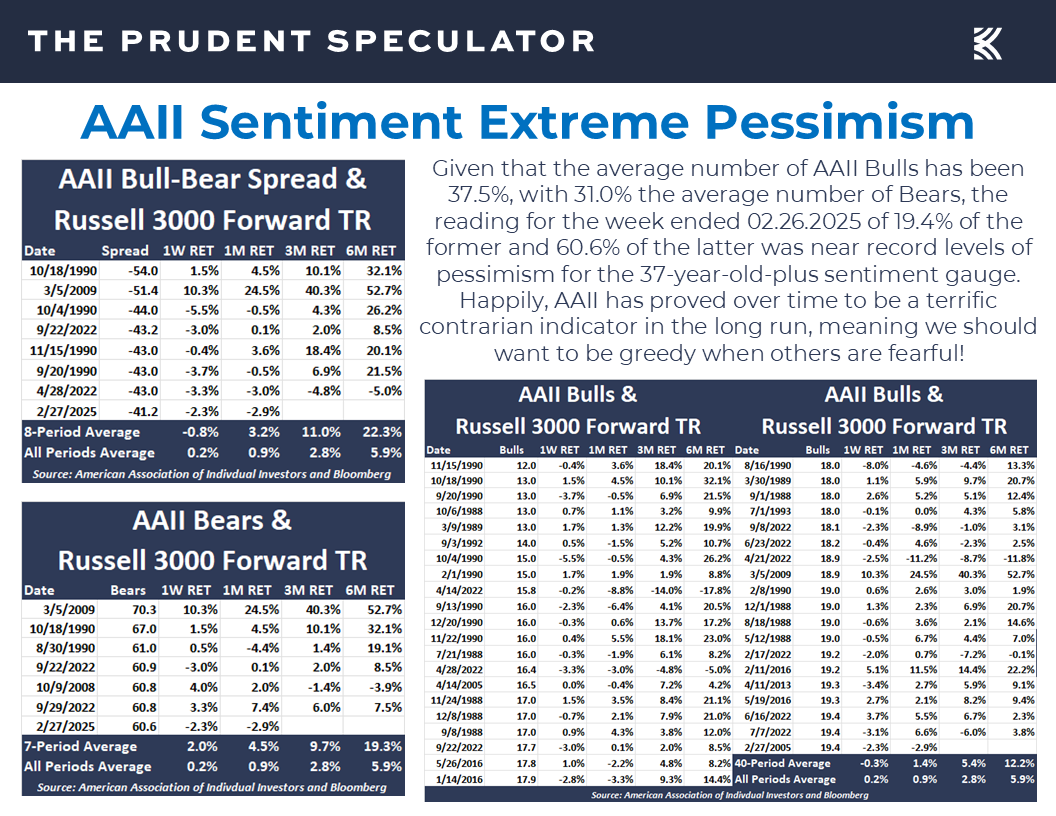

Sentiment – Be Greedy When Others are Fearful

Obviously, there is plenty about which to worry today and folks on Main Street remain overwhelming Bearish, with an extraordinarily elevated level of pessimists on the near-term prospects for equities in recent AAII Sentiment Surveys,

but it is again nice to see that it often pays to be greedy when others are fearful,

and very greedy when others are very fearful.

We are by no means suggesting, “Mission Accomplished,” as the equity futures are pointing south for the opening of trading in the new week and there is still a long way to go just to get back into the green this year, but patience in sticking with stocks through thick and thin has long been a terrific risk-mitigation tool,

while we continue to find it fascinating that many are saying they are as scared today as they were at the market bottoms associated with the Great Financial Crisis and the COVID-19 Pandemic.

Econ Outlook – Mixed Numbers, But Modest Growth Still Forecast

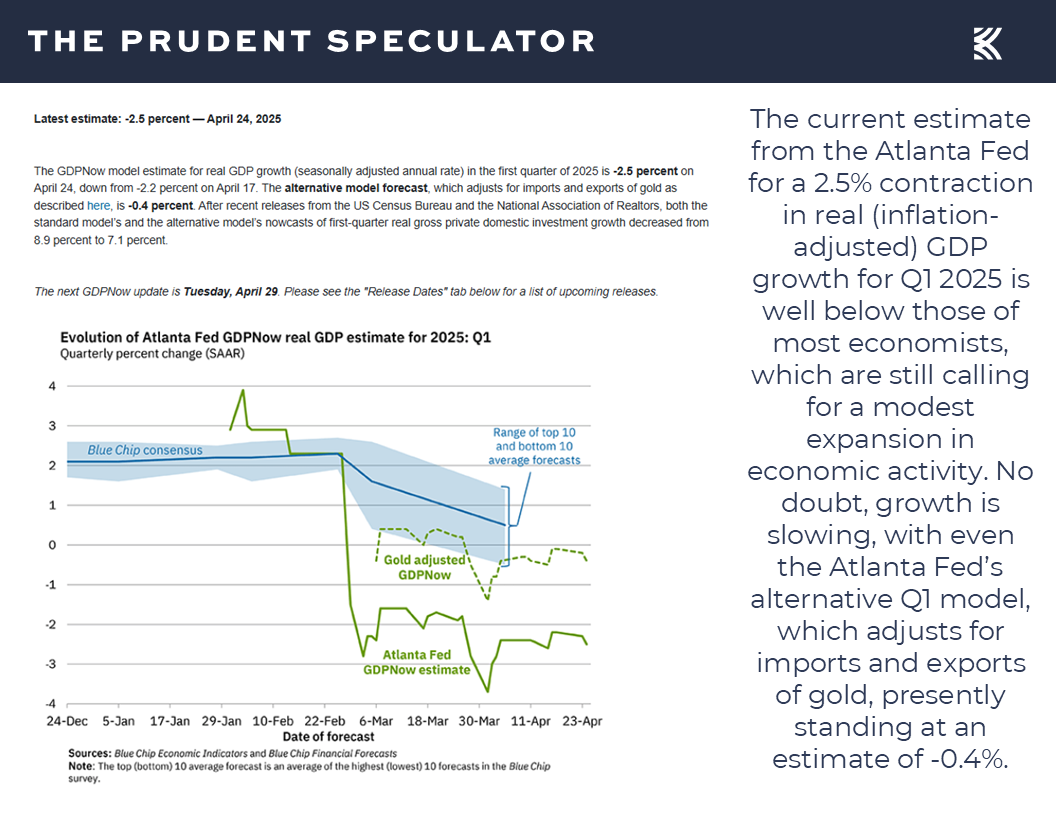

No doubt, all eyes are on tariffs and their impact on the U.S. and global economies, with the Atlanta Fed presently projecting negative real (inflation-adjusted) domestic GDP growth for Q1,

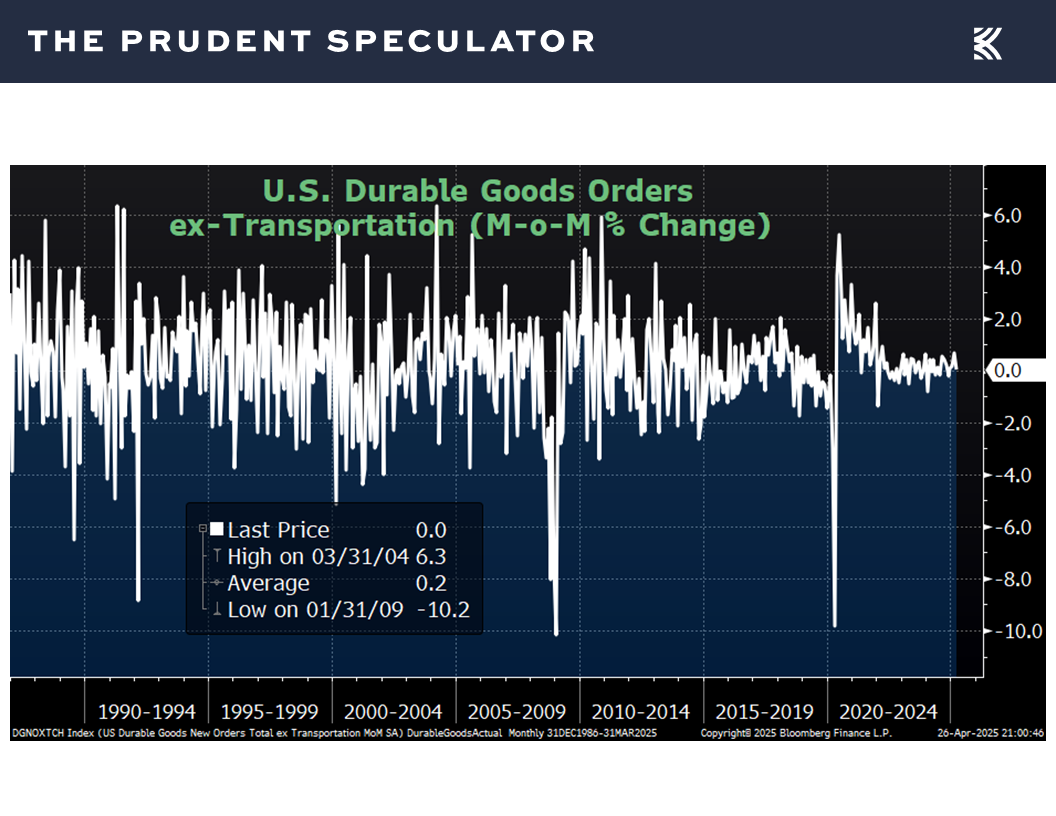

as durable goods orders excluding the volatile transportation sector were flat in March, below estimates of a 0.3% increase,

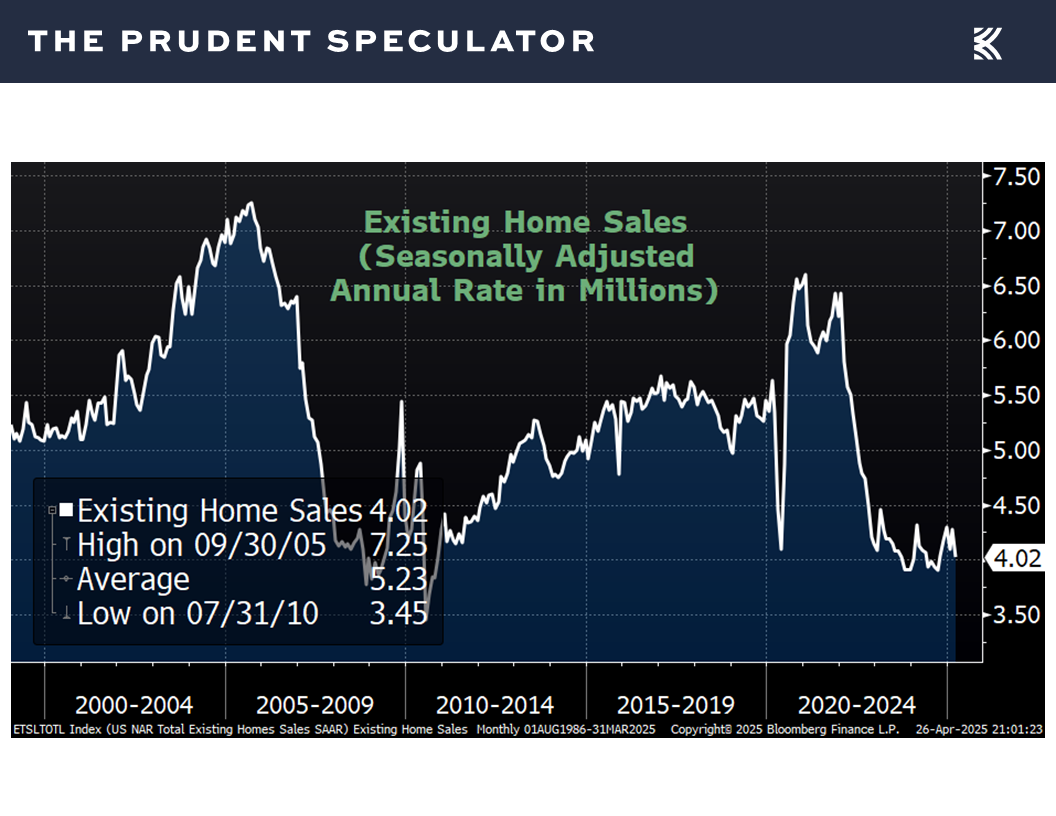

and existing home sales skidded 5.9% in March to a seasonally adjusted annual rate of 4.02 million, the lowest sales pace for that month since 2009…right when stocks bottomed during the Great Financial Crisis.

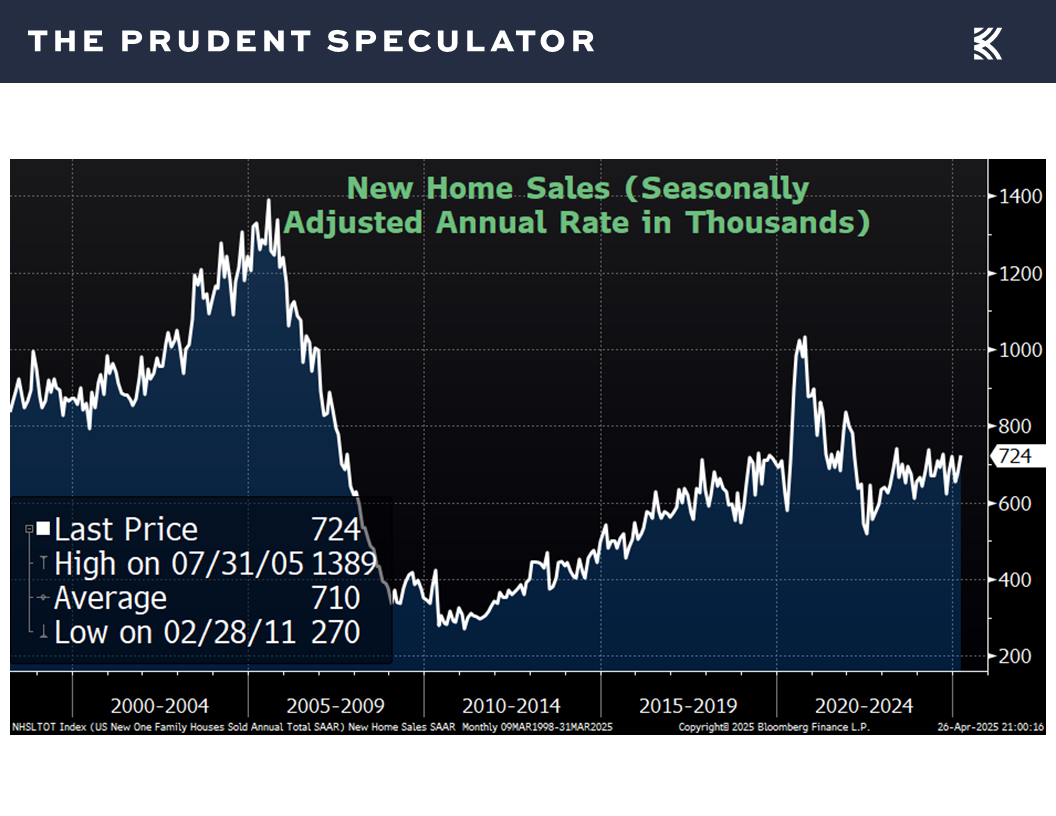

True, new home sales in March of 724,000 exceeded expectations of 685,000 and rebounded from a revised rate of 674,000 in February,

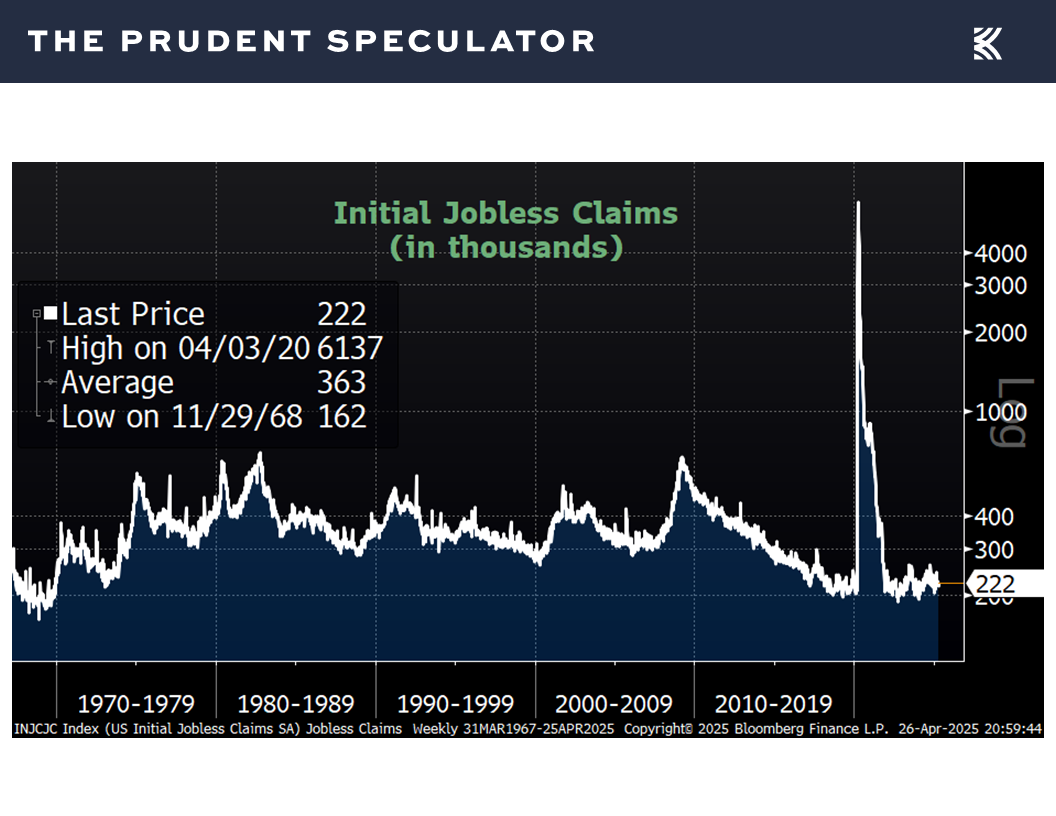

while first-time filings for unemployment benefits of 222,000 for the week ended April 19 continued to reside near multi-generational lows,

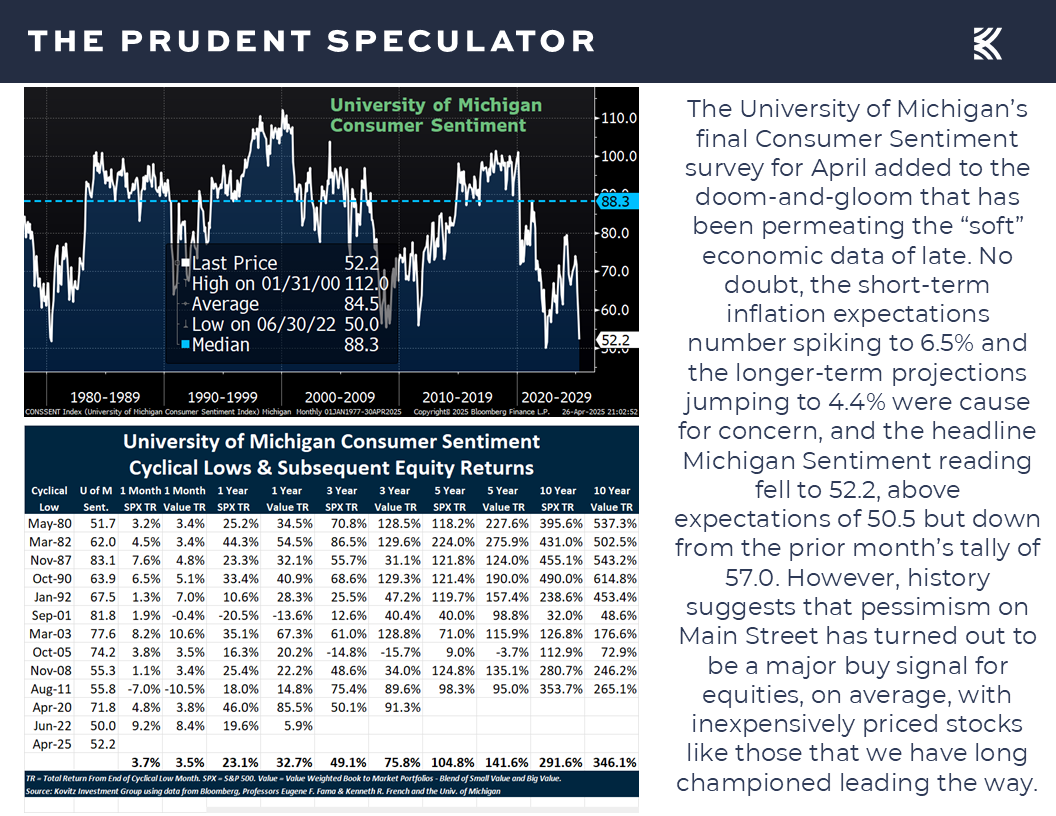

but the final read on Consumer Sentiment in April from the Univ. of Michigan of 52.2 marked a new cyclical low (which, historically has been a major buy signal)

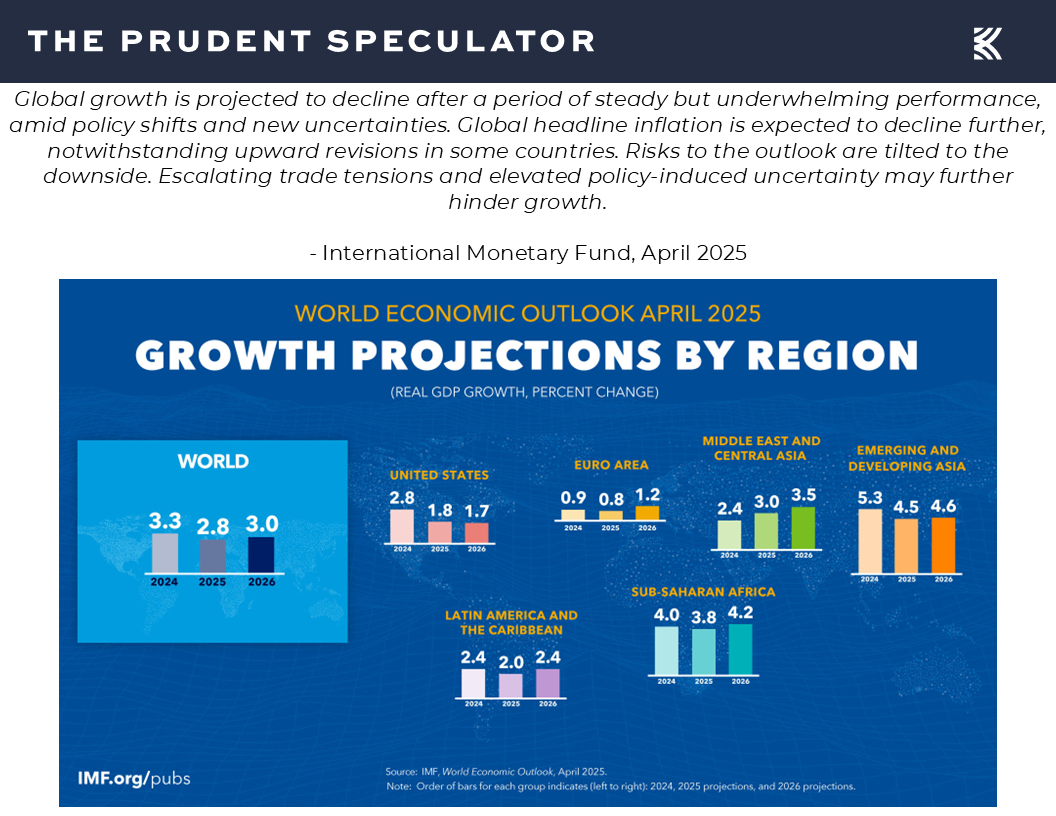

the International Monetary Fund (IMF) last week lowered its outlook for global and U.S. real (inflation-adjusted) GDP growth for 2025 and 2026,

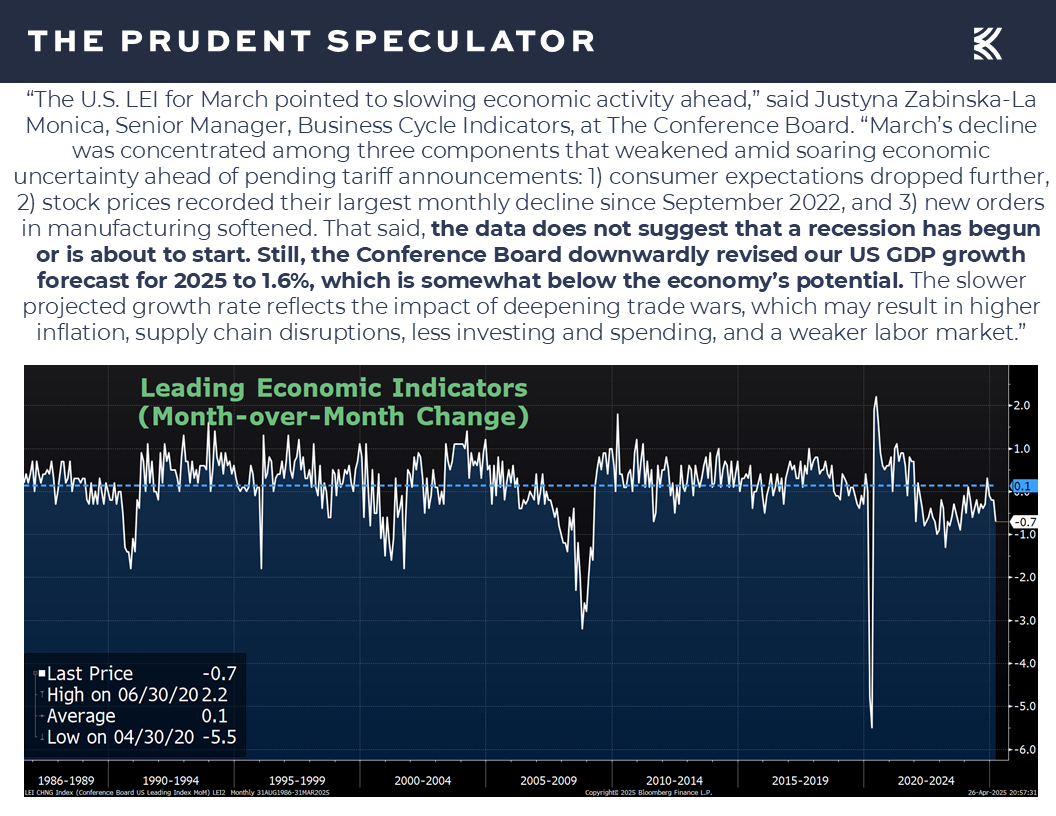

and the forward-looking Leading Economic Index from the Conference Board came in below expectations with a 0.7% decline for April.

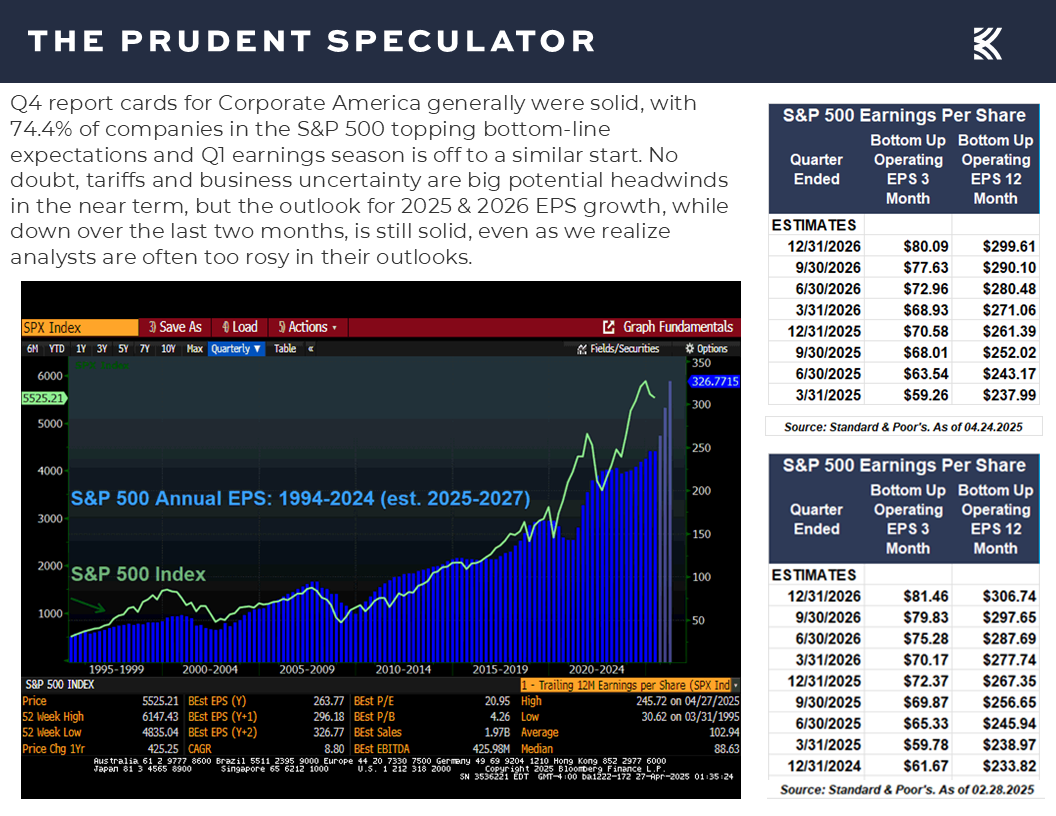

Of course, both the IMF and the Conference Board were still projecting positive real GDP growth this year, which would support current projections for solid growth of corporate profits,

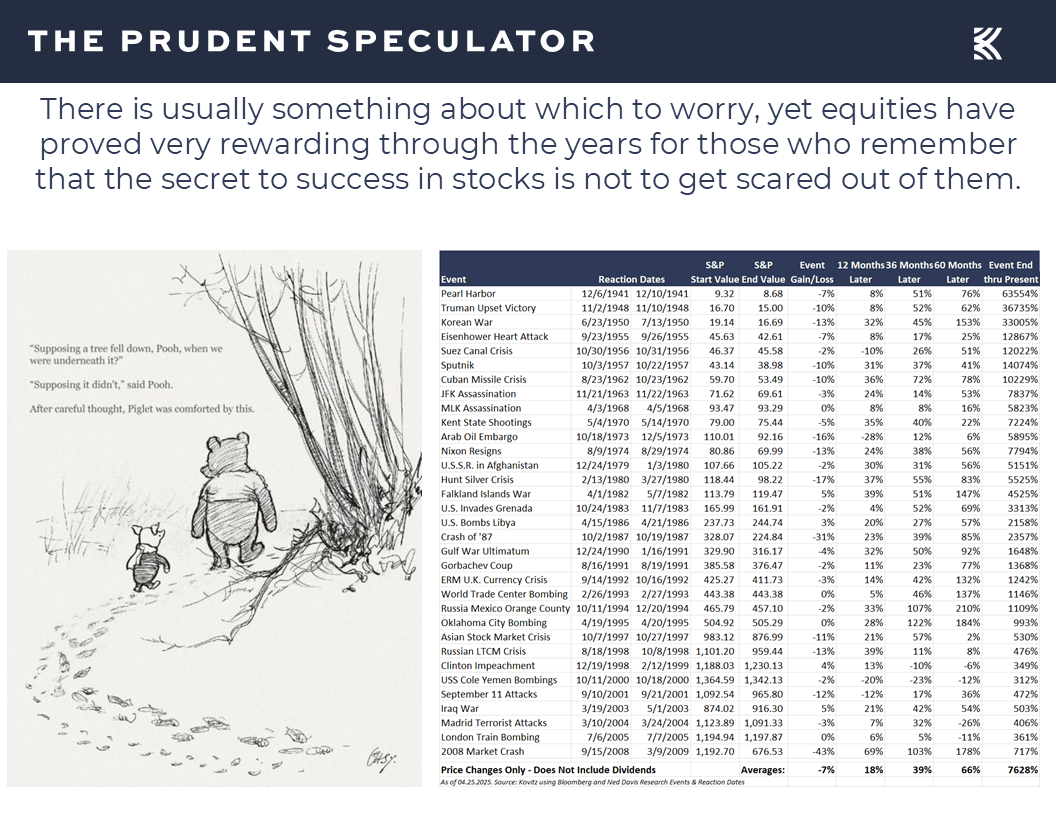

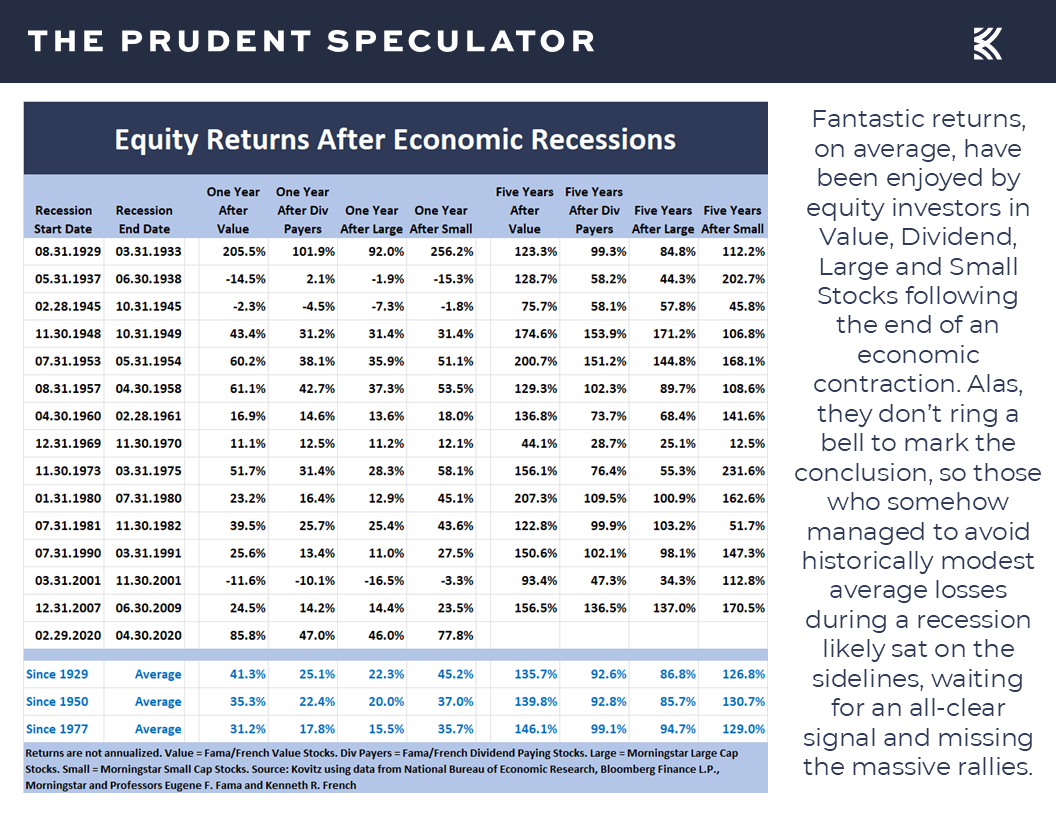

Recessions – Risk Has Jumped, But History Shows Staying the Course the Right Move Even if a Contraction Were to Occur

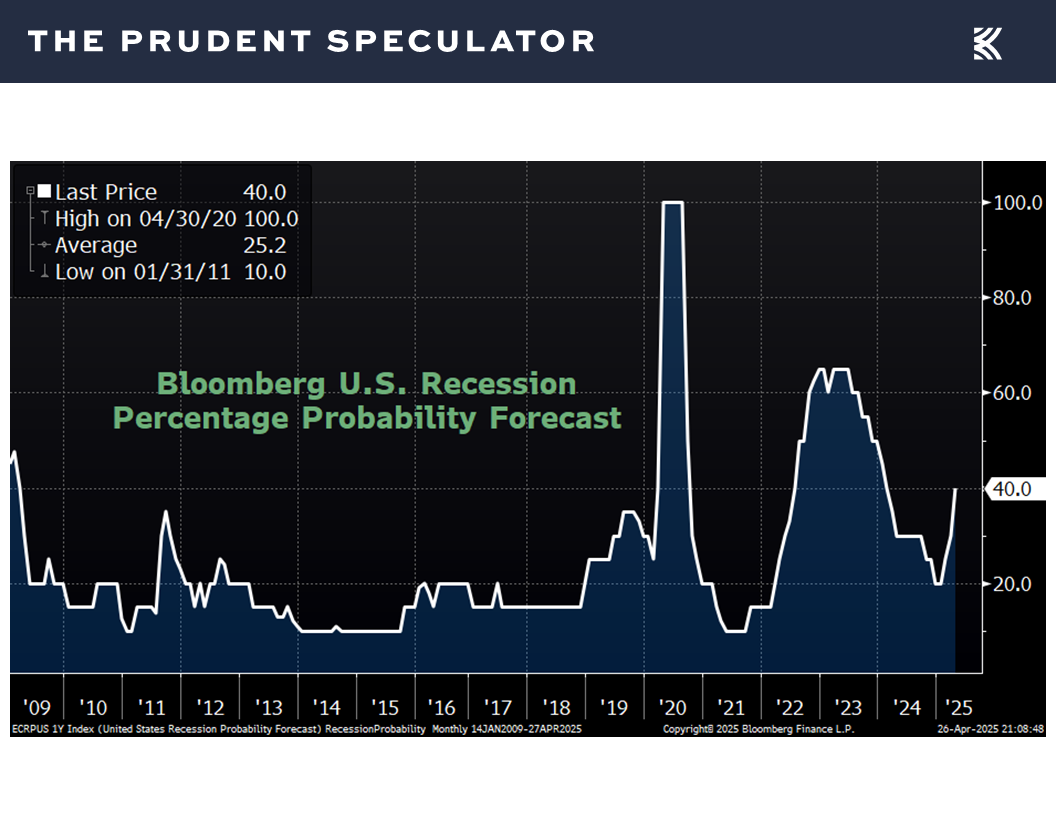

but we respect that the odds of recession (which Bloomberg now tabulates at 40%) have risen sharply,

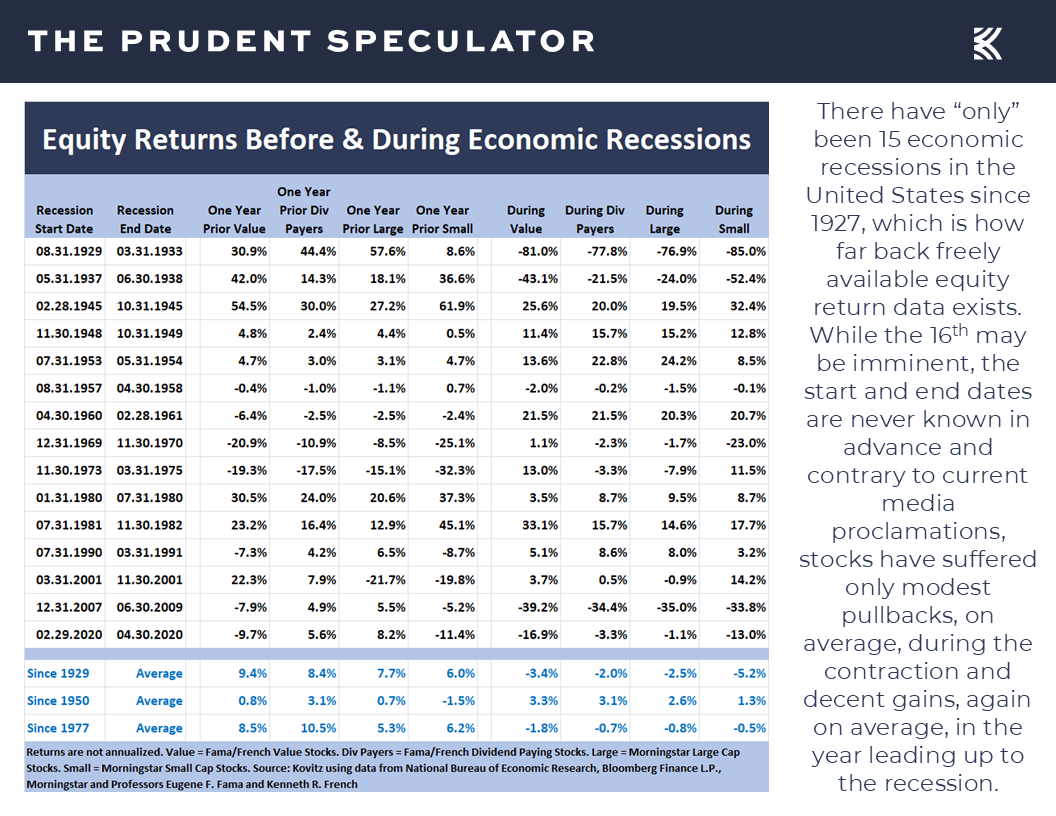

so we offer the reminder that stocks, even with the recent bounce, have already lost more than has been the norm during prior economic contractions,

while the rewards coming out of recessions, on average, have been sensational, providing investors have maintained their allocations to equities.

Come what may, and we continue to be braced for additional downside, especially as it was just two-plus weeks ago that CNBC Television was proclaiming that we had entered a Bear Market,

which if the then-level had persisted into that day’s close would have marked the 28th official drop of 20% or more, despite massive equity-market appreciation over the last century,

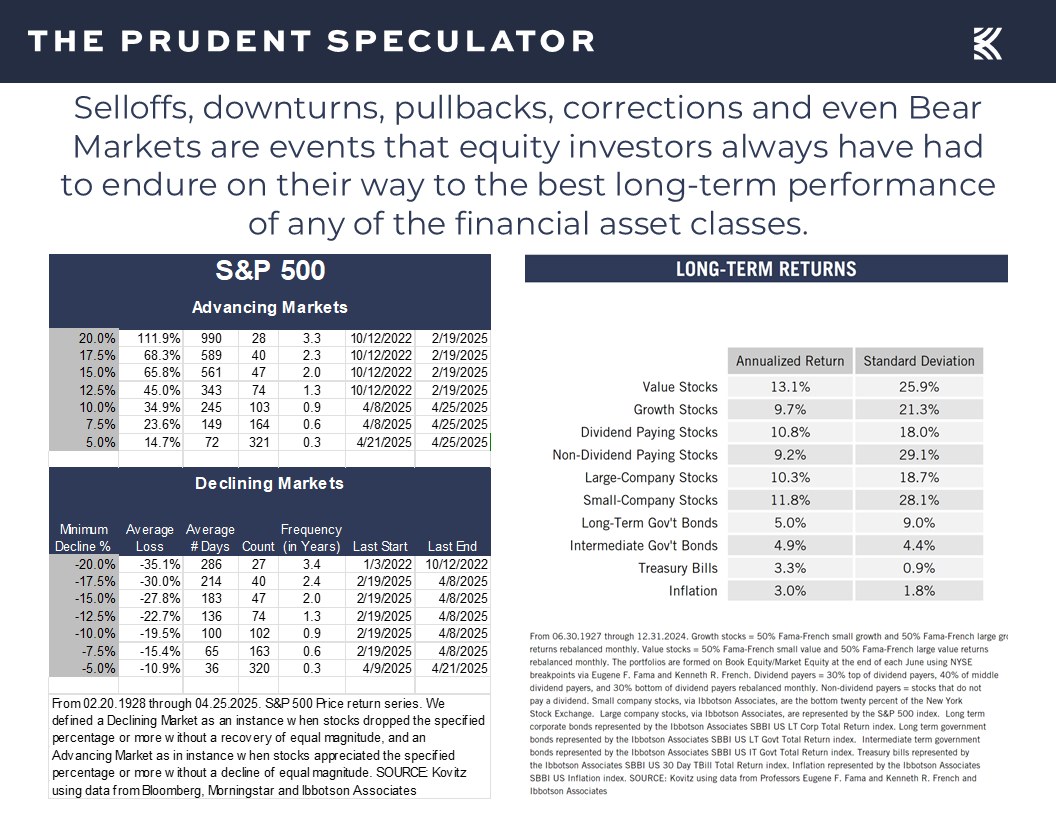

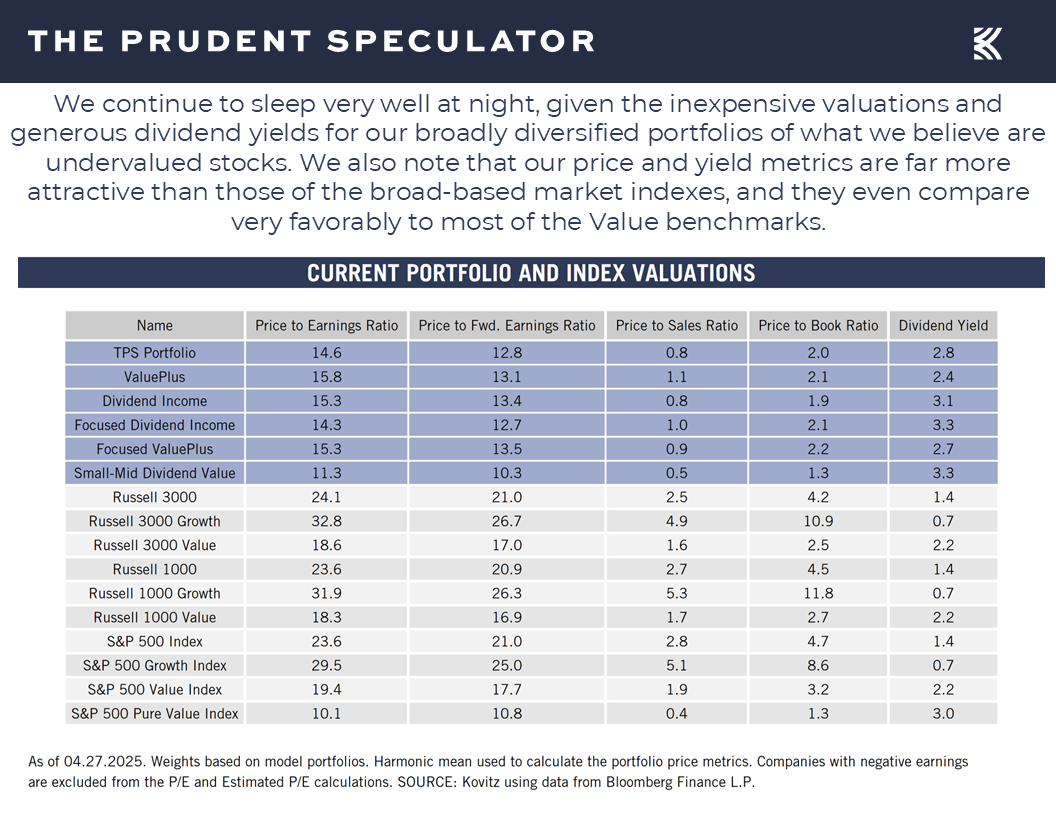

Valuations – Ups and Downs Part of the Process, but We Like our Inexpensive Stocks

but we see no reason to alter our favorable view for the long-term prospects of our broadly diversified portfolios of what we believe are undervalued stocks.

Stock News – Updates on fifteen stocks across nine different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Volatility, AAII Sentiment, Recessions and Stock News

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s Market Commentary, we discuss the Volatility, AAII Sentiment, Recessions and Stock News. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

Volatility – 39th Correction since 1977 Officially Ended on Friday

Sentiment – Be Greedy When Others are Fearful

Econ Outlook – Mixed Numbers, But Modest Growth Still Forecast

Recessions – Risk Has Jumped, But History Shows Staying the Course the Right Move Even if a Contraction Were to Occur

Valuations – Ups and Downs Part of the Process, but We Like our Inexpensive Stocks

Stock News – Comments on CMA, ELV, VZ, LMT, COF, NEM, LRCX, WHR, IBM, HAS, CMCSA, INTC, GOOG, GILD & DLR

Volatility – 39th Correction since 1977 Officially Ended on Friday

We understand that a social media post from the President, a media headline from a member of his cabinet or a negative response from a foreign government could trigger another big selloff, but the big rebound last week officially ended the 39th correction of 10% in the S&P 500 since the launch of The Prudent Speculator in 1977. Believe it or not, though the popular equity benchmark remains well into the red on the year and the average stock in the broad-based Russell 3000 index is off 11.9% in 2025, we are now in the 40th rally of 10% over the past 48 years,…

providing yet another reminder that while downside volatility is always part of the investment equation, every prior scary event has been overcome in the fullness of time,

with even Bear Markets having been followed by Bull Markets where gains of far greater magnitude have taken place,

so much so that annualized long-term returns on stocks, led by Value and Dividend Payers, have been in the 9% to 13% range.

Sentiment – Be Greedy When Others are Fearful

Obviously, there is plenty about which to worry today and folks on Main Street remain overwhelming Bearish, with an extraordinarily elevated level of pessimists on the near-term prospects for equities in recent AAII Sentiment Surveys,

but it is again nice to see that it often pays to be greedy when others are fearful,

and very greedy when others are very fearful.

We are by no means suggesting, “Mission Accomplished,” as the equity futures are pointing south for the opening of trading in the new week and there is still a long way to go just to get back into the green this year, but patience in sticking with stocks through thick and thin has long been a terrific risk-mitigation tool,

while we continue to find it fascinating that many are saying they are as scared today as they were at the market bottoms associated with the Great Financial Crisis and the COVID-19 Pandemic.

Econ Outlook – Mixed Numbers, But Modest Growth Still Forecast

No doubt, all eyes are on tariffs and their impact on the U.S. and global economies, with the Atlanta Fed presently projecting negative real (inflation-adjusted) domestic GDP growth for Q1,

as durable goods orders excluding the volatile transportation sector were flat in March, below estimates of a 0.3% increase,

and existing home sales skidded 5.9% in March to a seasonally adjusted annual rate of 4.02 million, the lowest sales pace for that month since 2009…right when stocks bottomed during the Great Financial Crisis.

True, new home sales in March of 724,000 exceeded expectations of 685,000 and rebounded from a revised rate of 674,000 in February,

while first-time filings for unemployment benefits of 222,000 for the week ended April 19 continued to reside near multi-generational lows,

but the final read on Consumer Sentiment in April from the Univ. of Michigan of 52.2 marked a new cyclical low (which, historically has been a major buy signal)

the International Monetary Fund (IMF) last week lowered its outlook for global and U.S. real (inflation-adjusted) GDP growth for 2025 and 2026,

and the forward-looking Leading Economic Index from the Conference Board came in below expectations with a 0.7% decline for April.

Of course, both the IMF and the Conference Board were still projecting positive real GDP growth this year, which would support current projections for solid growth of corporate profits,

Recessions – Risk Has Jumped, But History Shows Staying the Course the Right Move Even if a Contraction Were to Occur

but we respect that the odds of recession (which Bloomberg now tabulates at 40%) have risen sharply,

so we offer the reminder that stocks, even with the recent bounce, have already lost more than has been the norm during prior economic contractions,

while the rewards coming out of recessions, on average, have been sensational, providing investors have maintained their allocations to equities.

Come what may, and we continue to be braced for additional downside, especially as it was just two-plus weeks ago that CNBC Television was proclaiming that we had entered a Bear Market,

which if the then-level had persisted into that day’s close would have marked the 28th official drop of 20% or more, despite massive equity-market appreciation over the last century,

Valuations – Ups and Downs Part of the Process, but We Like our Inexpensive Stocks

but we see no reason to alter our favorable view for the long-term prospects of our broadly diversified portfolios of what we believe are undervalued stocks.

Stock News – Updates on fifteen stocks across nine different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.