The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Volatility, Economic Data, Valuations and more Stock News. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

TPS Webinar – Replay and Slide Deck Available

Newsletter Trades – 7 Buys for 4 Portfolios

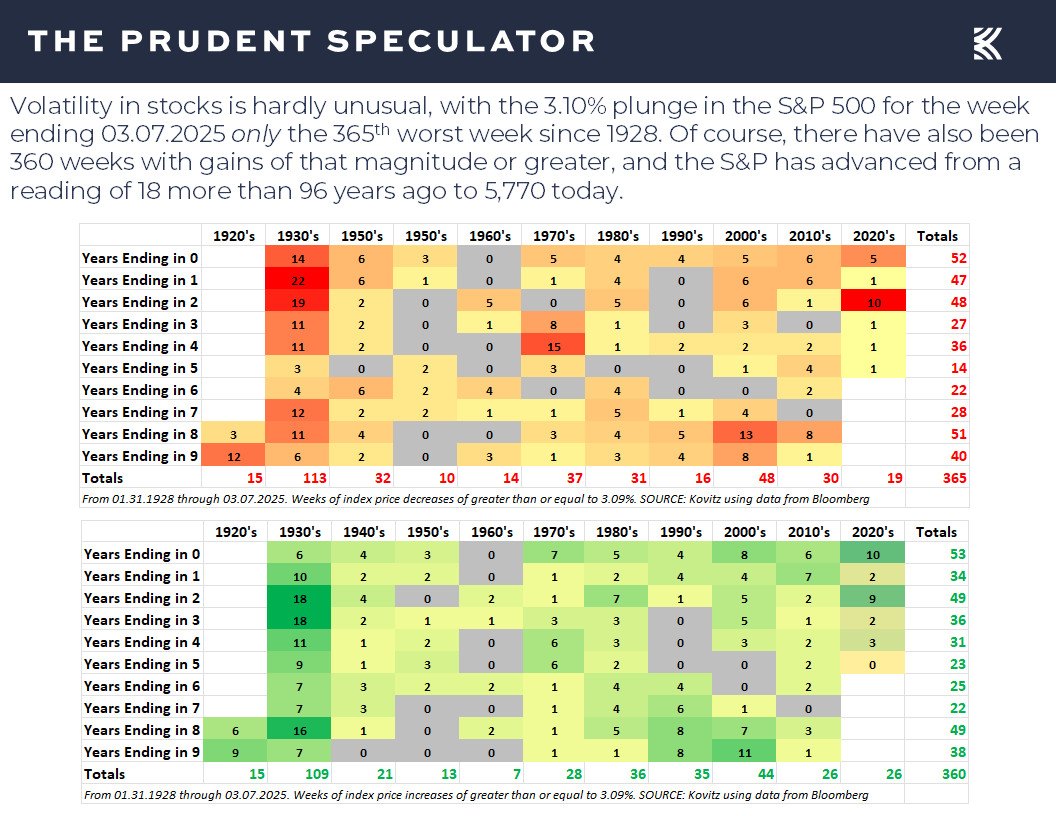

Week – Modest Rebound on Friday, But 365th Worst Five-Day Period Ever

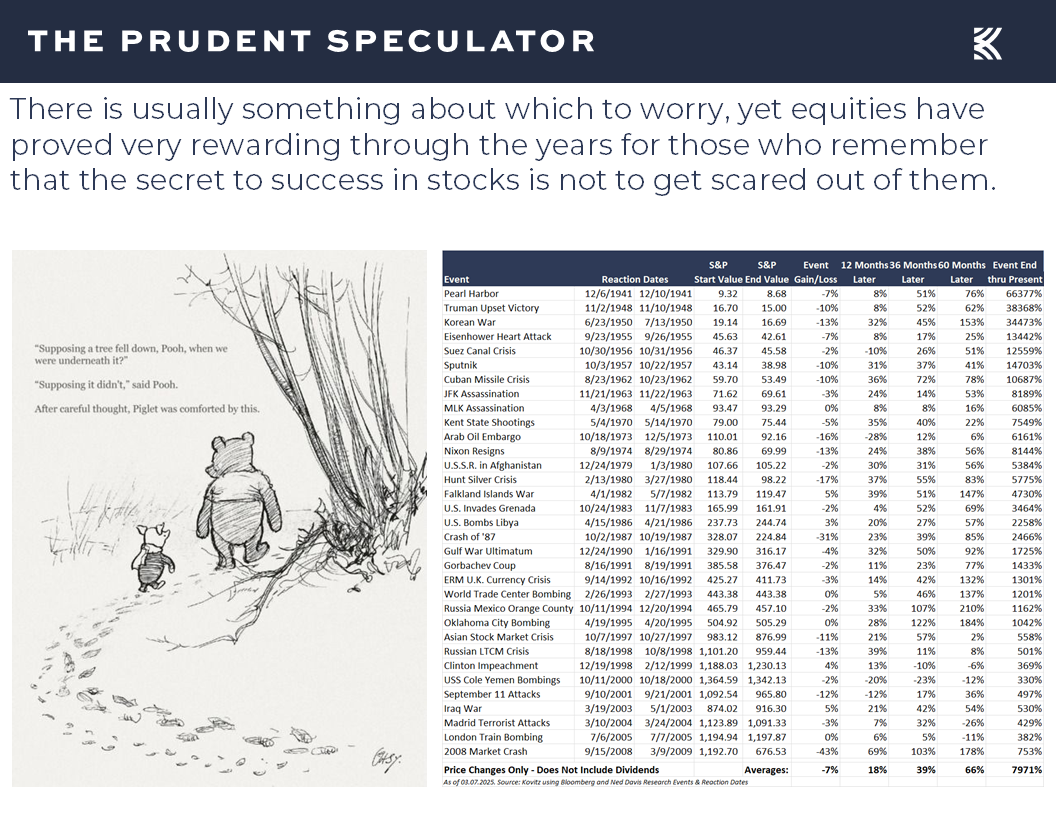

Volatility – Stocks Go Up and Down in the Short Term, But Have Provided Handsome Rewards in the Long-Term

Econ Data – Atlanta Fed Turns Negative on GDP; ISM Says Otherwise

Powell – U.S. Economy in a Good Place

Perspective – Holding Through Recessions & Inflation Fluctuations

Valuations – Liking the Metrics on our Portfolios

Sentiment – Major AAII Contrarian Buy Signal

Stock News – Updates on TGT, BLK, FL, KR, HPE & AVGO

Week – Modest Rebound on Friday, But 365th Worst Five-Day Period Ever

You know it was a tough run when it took a late-day rebound on Friday to cut the retreat for the S&P 500 on a price basis for the full five days to 3.10%, which marked the 365th worst trading week in nearly a century. Of course, the statistics show that we have averaged more than three weeks per year of equal or worse magnitude for the popular index, while the same is true for comparable periods to the upside.

Volatility – Stocks Go Up and Down in the Short Term, But Have Provided Handsome Rewards in the Long-Term

Happily, despite inevitable trips south, the gains from times when the markets have headed north have dwarfed the short-term losses, so much so that the long-term returns from equities have been sensational…provided folks stick with stocks through thick and thin.

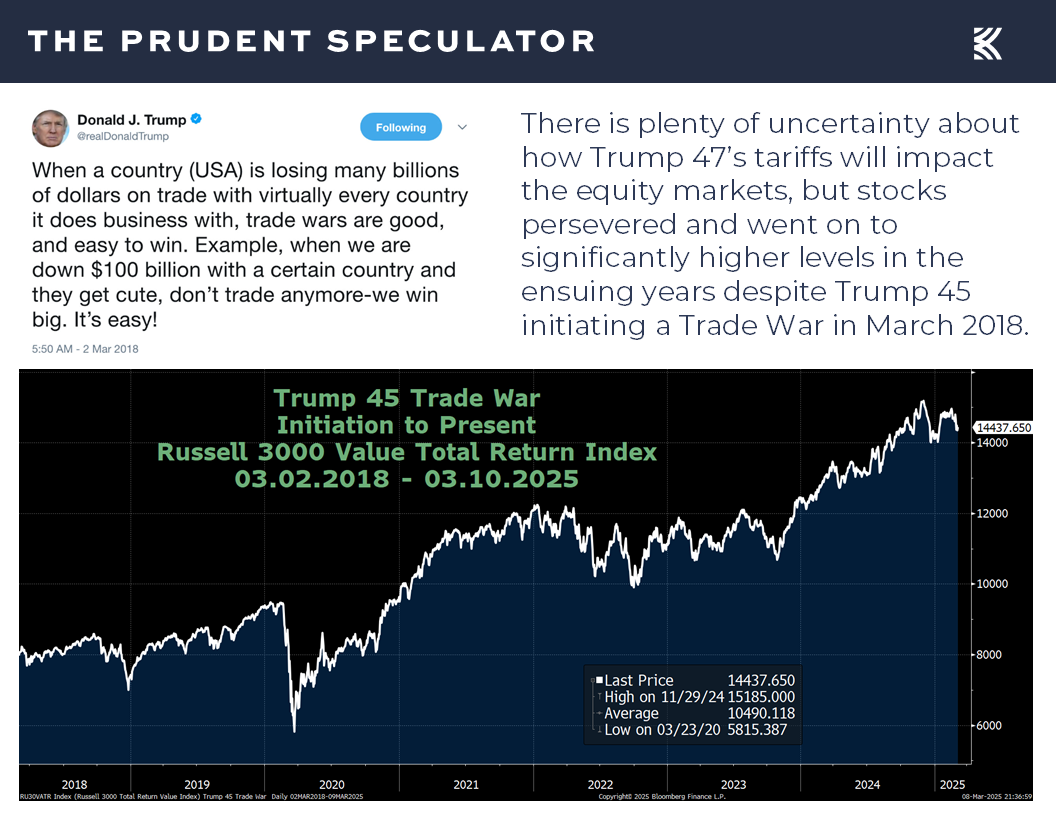

No doubt, the reason for the red ink last week was continued worries about tariffs, even as we have been living with high-profile U.S. tariffs on foreign goods since Trump 45 and carrying through the Biden Administration.

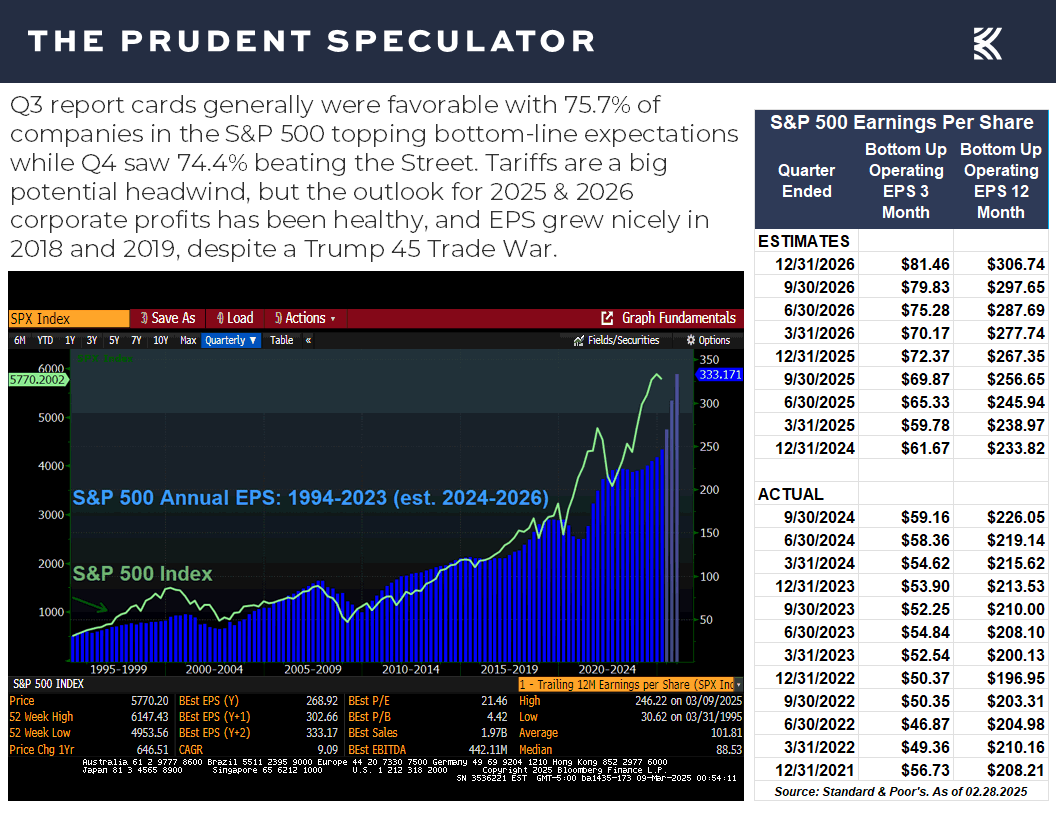

True, part of the near-term problem for stocks is uncertainty given that tariffs were lifted on American carmakers producing in Canada and Mexico early last week, and then later postponed again on virtually all imports to the U.S., even as they were maintained on goods from China. Though President Trump proclaimed that plans for broader “reciprocal” tariffs will go into effect on April 2, it is impossible to know if, when and what impact they will have, so we must take current estimates for handsome corporate profit growth this year and next with more than the usual grain of salt.

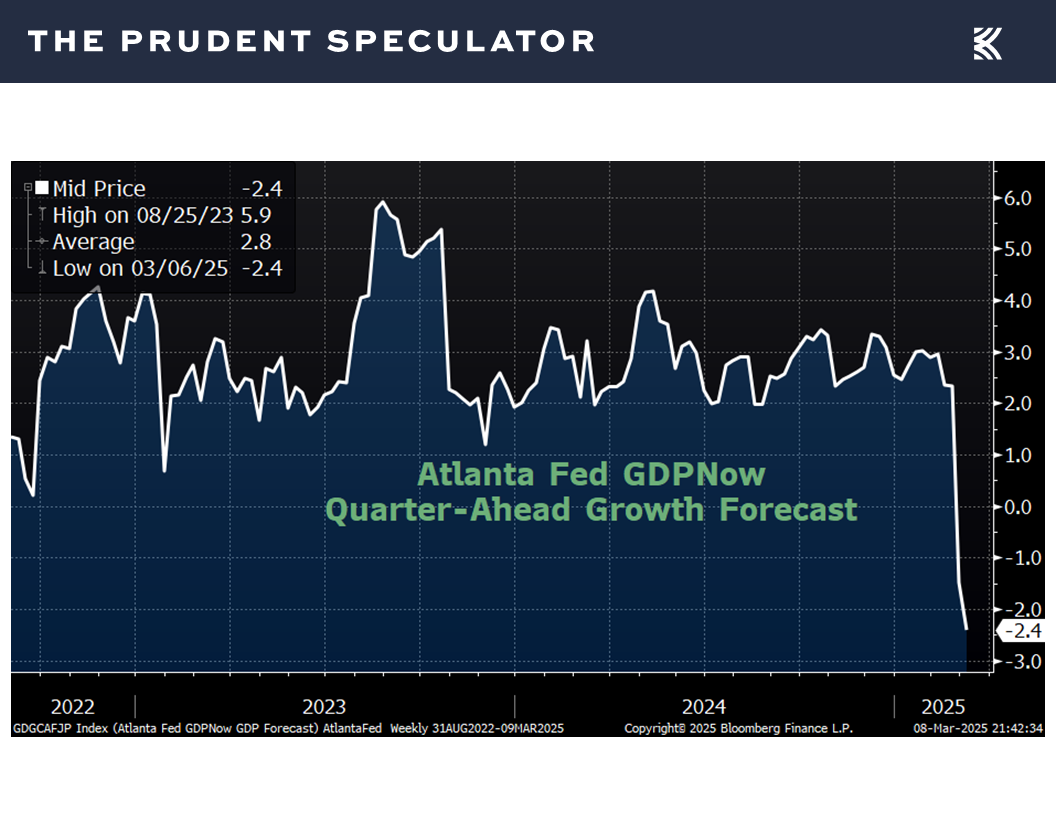

Econ Data – Atlanta Fed Turns Negative on GDP; ISM Says Otherwise

Certainly, there are question marks about the health of the U.S. economy as the latest estimate for real (inflation-adjusted) Q1 GDP from the Atlanta Fed stood at a contraction of 2.4%,

even as that is not the conclusion that would be drawn from the latest readings from the Institute for Supply Management (ISM) for the domestic manufacturing and non-manufacturing sectors.

Indeed, though the ISM factory gauge for February trailed expectations with a dip to 50.3, down from 50.9 in January, ISM states, “A Manufacturing PMI® above 42.3 percent, over a period of time, generally indicates an expansion of the overall economy. Therefore, the February Manufacturing PMI® indicates the overall economy grew for the 58th straight month after last contracting in April 2020. The past relationship between the Manufacturing PMI® and the overall economy indicates that the February reading (50.3 percent) corresponds to a change of plus-2.2 percent in real gross domestic product (GDP) on an annualized basis.”

It is an even more interesting story for the ISM Services measure, as the tally for February of 53.5 topped estimates of 52.5 and rose from the 52.8 tabulation for January. ISM states, “A Services PMI® above 48.6 percent, over time, generally indicates an expansion of the overall economy. Therefore, the February Services PMI® indicates the overall economy is expanding for the 57th straight month. The past relationship between the Services PMI® and the overall economy indicates that the Services PMI® for February (53.5 percent) corresponds to a 1.6-percentage point increase in real gross domestic product (GDP) on an annualized basis.”

Powell – U.S. Economy in a Good Place

We do not mean to suggest that the economy will boom in the short run, though we might expect extra activity as corporations work to get ahead of possible tariffs, but we can’t ignore comments from Jerome H. Powell on Friday afternoon. In a planned speech in New York, the Fed Chair led off with, “Despite elevated levels of uncertainty, the U.S. economy continues to be in a good place. The labor market is solid, and inflation has moved closer to our 2 percent longer-run goal,” and provided additional color to support his always-data-dependent viewpoint.

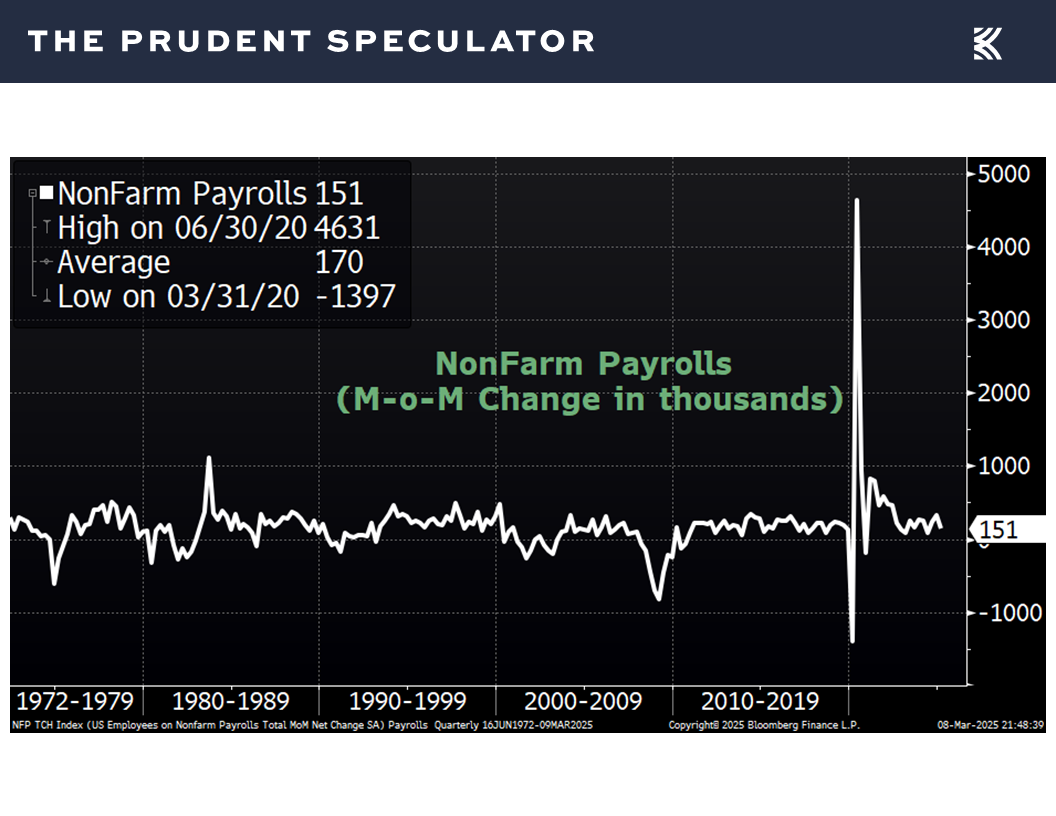

His less pessimistic outlook than that of many market watchers received some support from the employment statistics out last week, as the number of net new jobs created during February of 151,000 was up from a revised 125,000 in January and was not too far below projections.

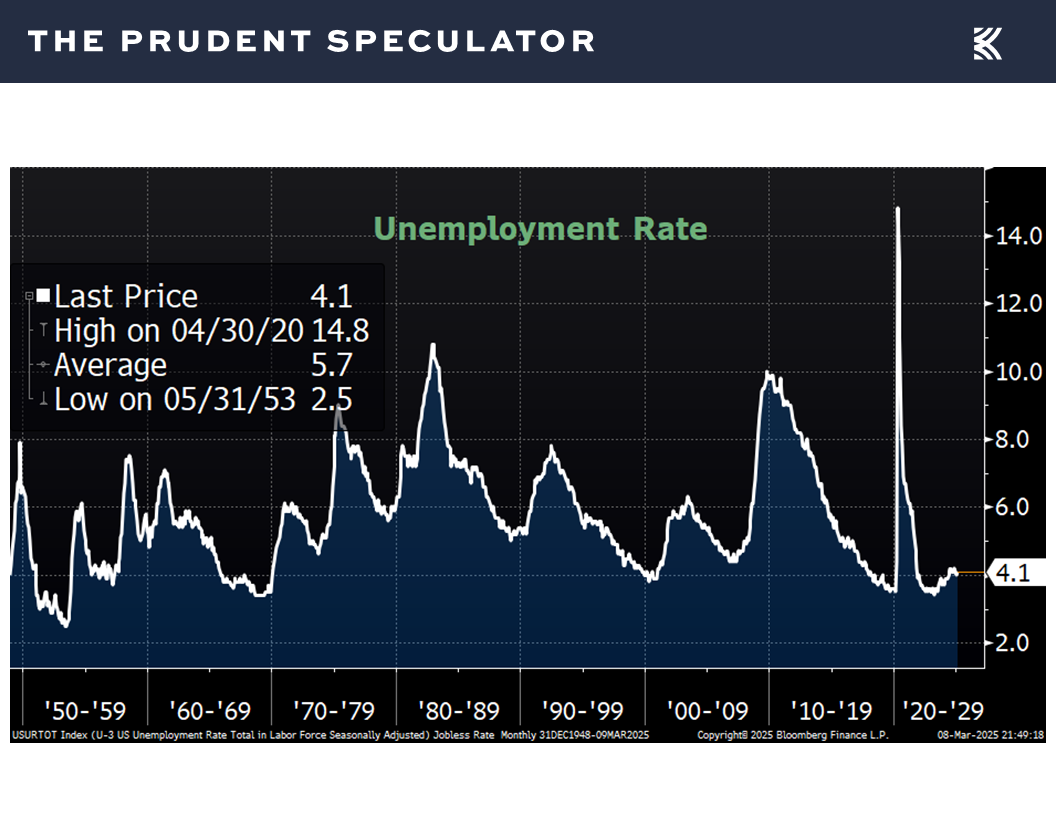

The unemployment rate for February ticked up to 4.1%, which is still well below the historical average,

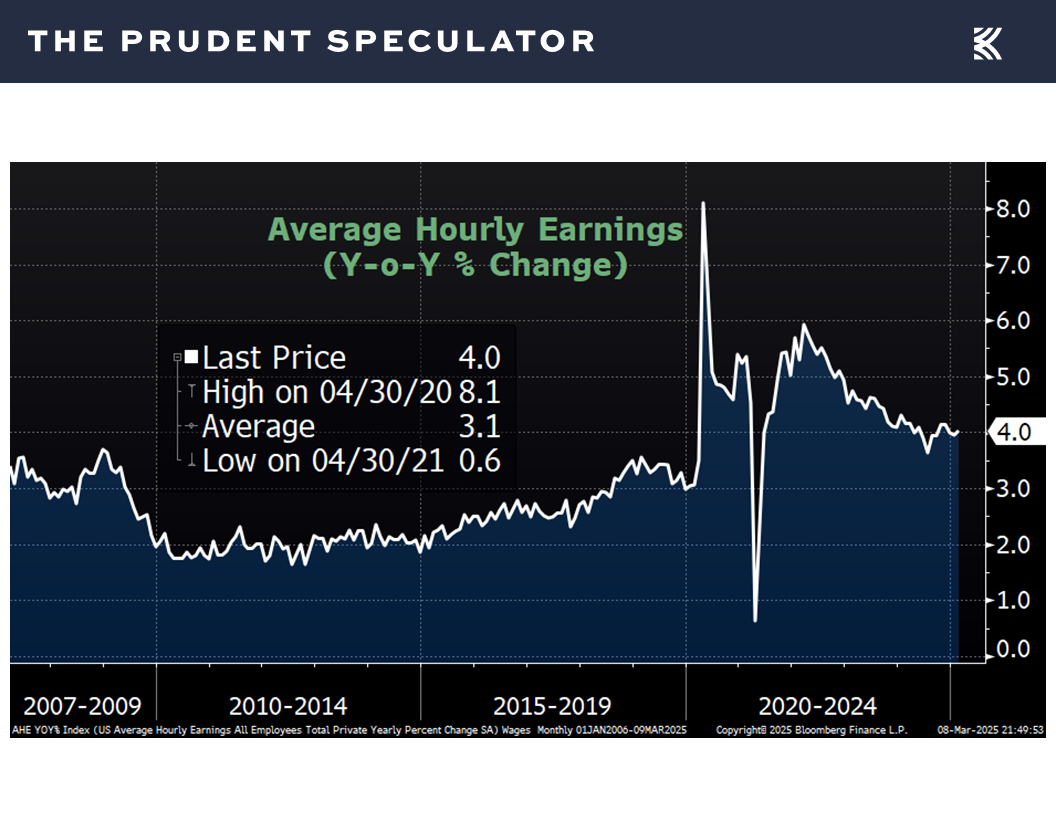

average hourly earnings rose 4.0% last month, a smidge better than the January number of 3.9%,

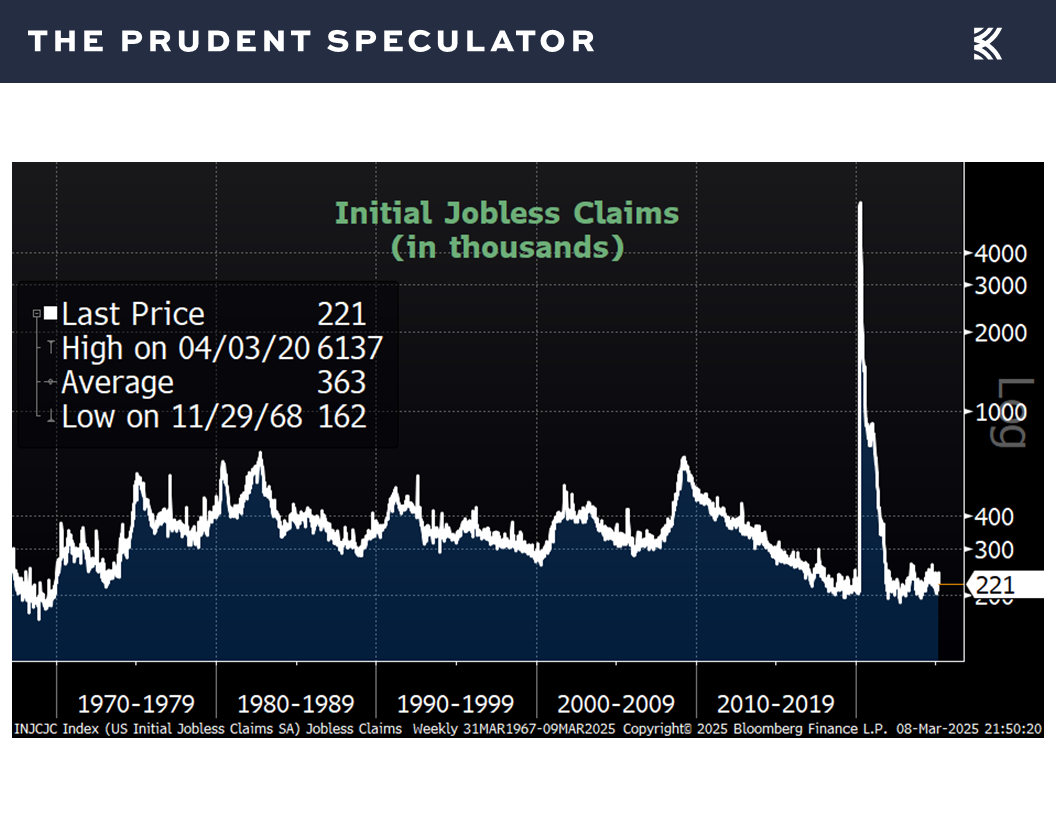

and first-time filings for unemployment benefits in the latest week dropped to 221,000, down from 242,000 the week prior.

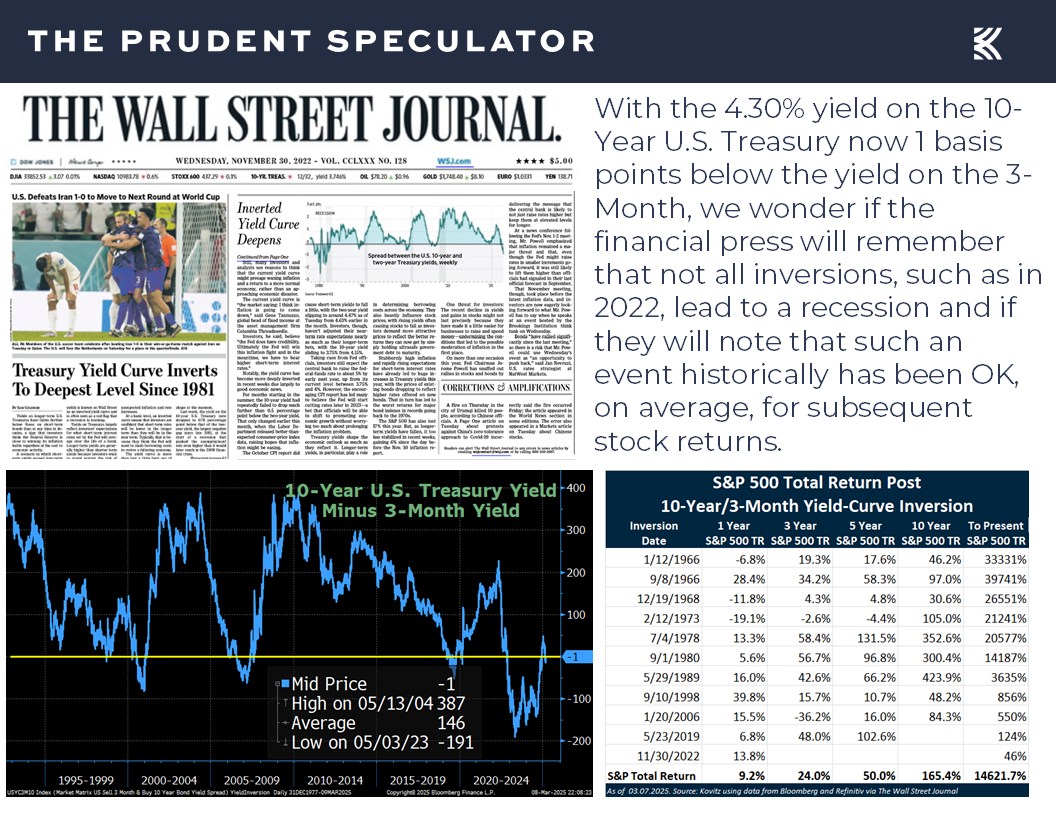

To be sure, an economic slowdown is a very real possibility, and we realize that the latest yield-curve inversion where the yield on the short-term 3-month U.S. Treasury went above that of the long-term 10-Year Treasury has some arguing a recession is in the cards.

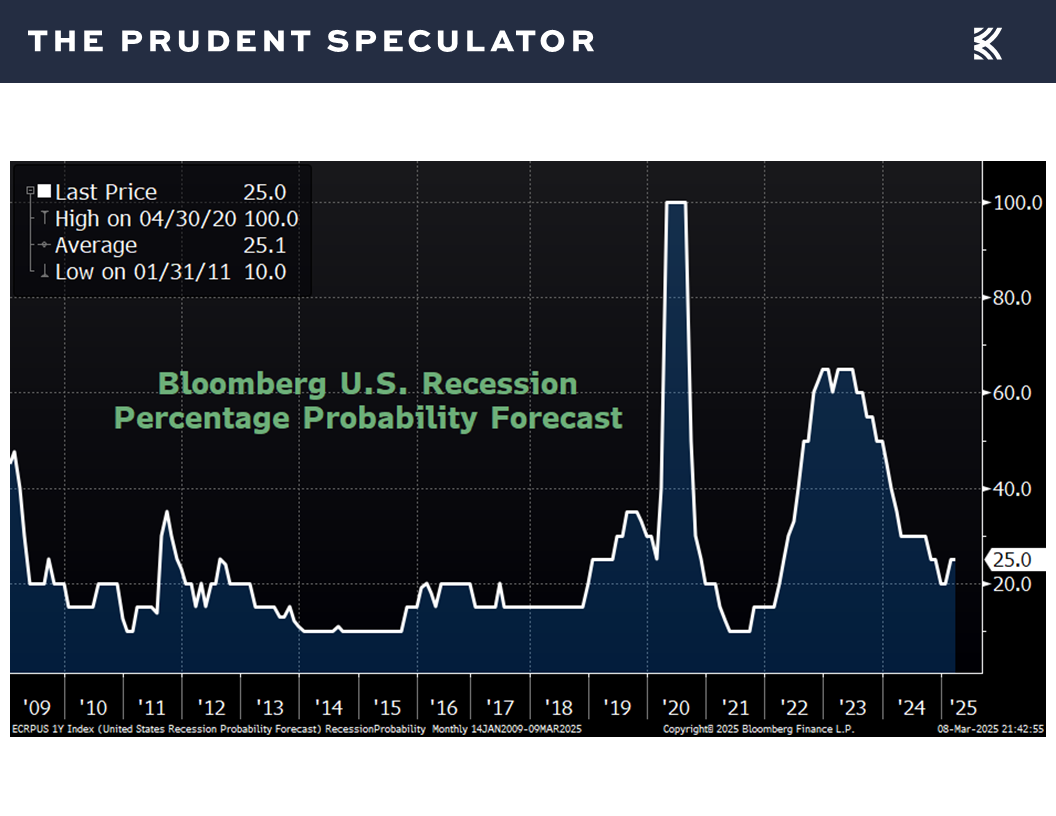

An inversion has not had a foolproof forecasting record, while history shows we wouldn’t have wanted to sell stocks, given the favorable forward average returns detailed in the chart above. Further, the present odds of recession at 25%, as tabulated by Bloomberg, remain very low.

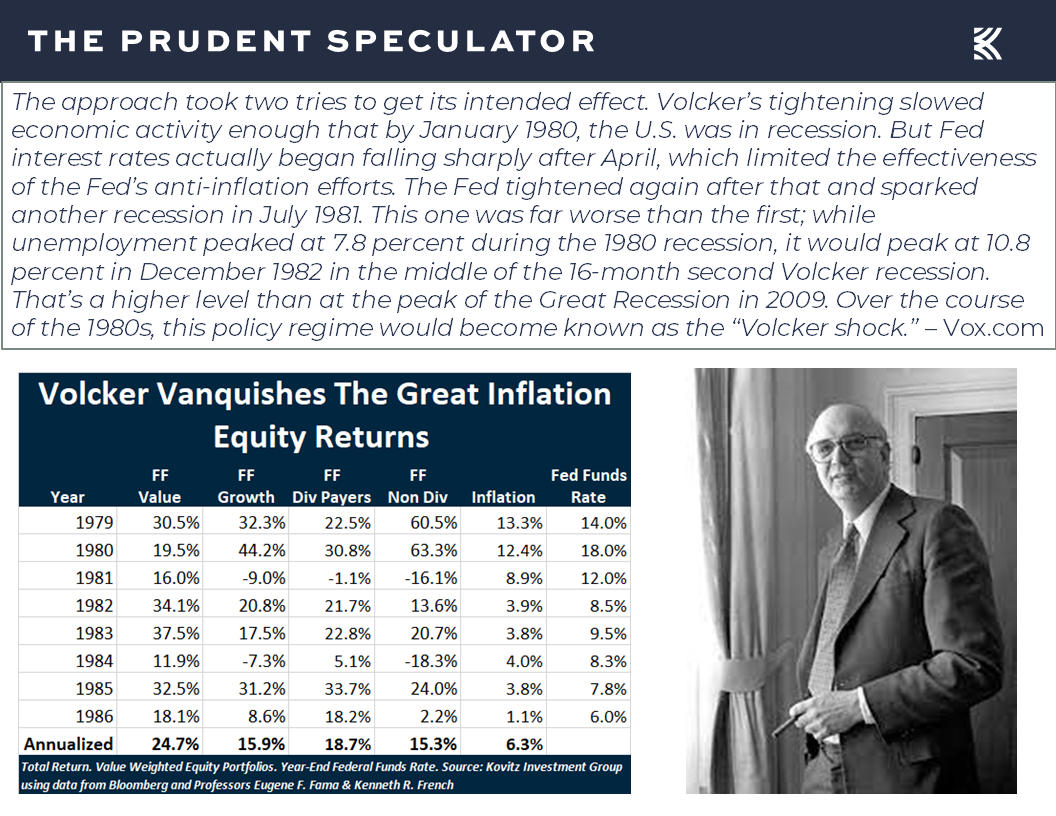

Perspective – Holding Through Recessions & Inflation Fluctuations

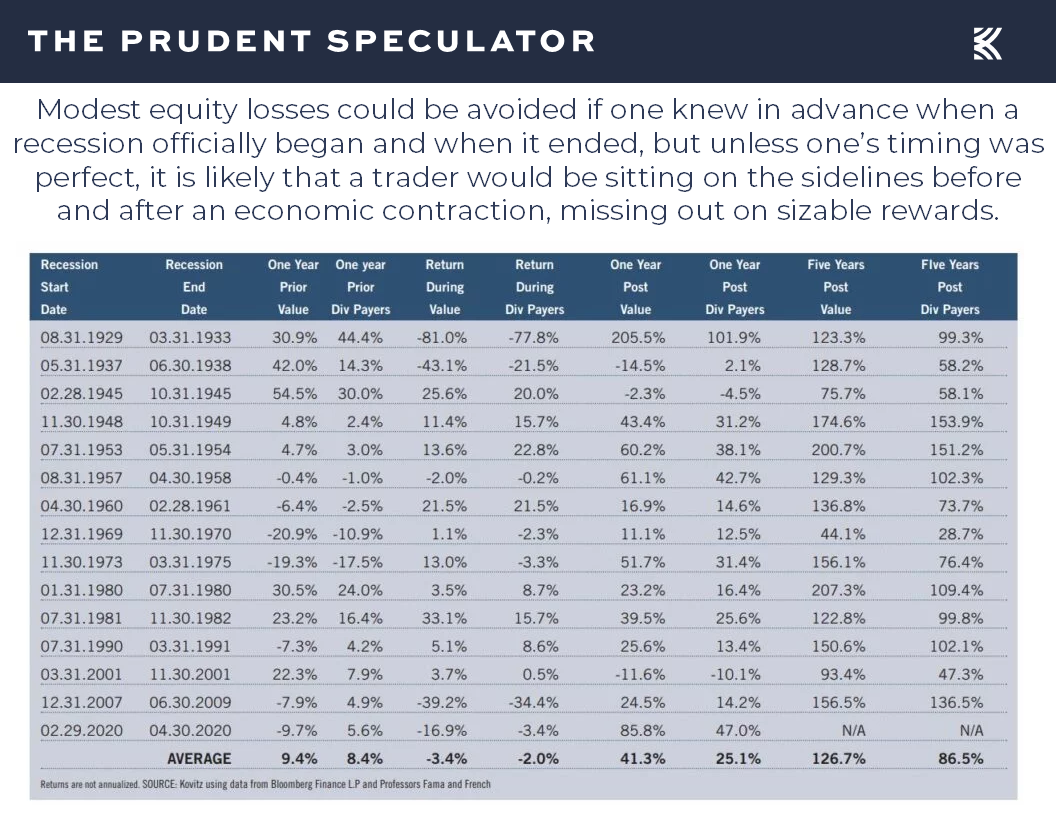

That said, we have long understood that recessions are part of the investment landscape, so as students of market history, we should care about what the return numbers looked like for the kinds of stocks we have long favored. While it is impossible to know the start and end date of economic contractions as the official arbiters do not rule until after the fact, we concede that being out of stocks during the recession would have been beneficial, on average, tax-considerations notwithstanding. However, return figures in the year prior to the economic downturn were solid AND performance in the year after the recession was sensational, on average, adding more evidence to our mantra, time in the market trumps market timing.

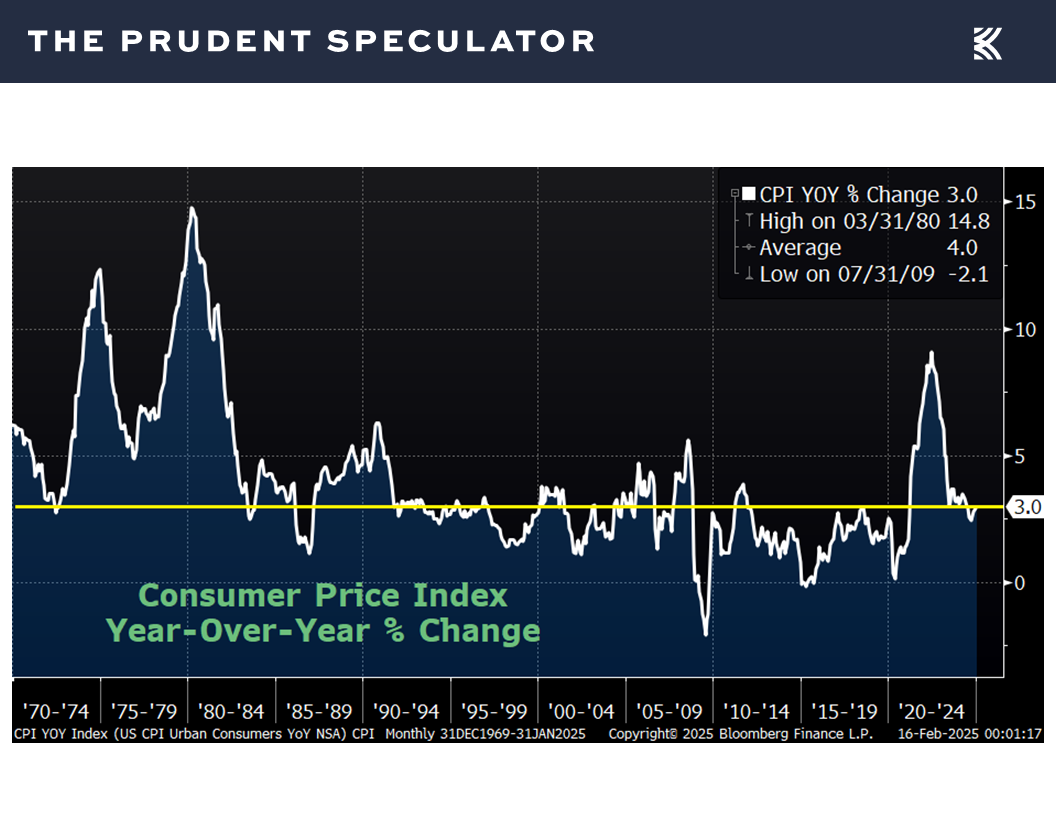

While this (and every time) is different, we continue to believe that the Great Inflation of the early 1980s might be a good comparison to the current environment,

as that was the last time before the current period that the Federal Reserve, then under the leadership of Paul Volcker, had to battle a big spike in consumer prices. Happily, that time span proved to be extraordinarily lucrative for investors, even as there were two U.S. recessions along the way.

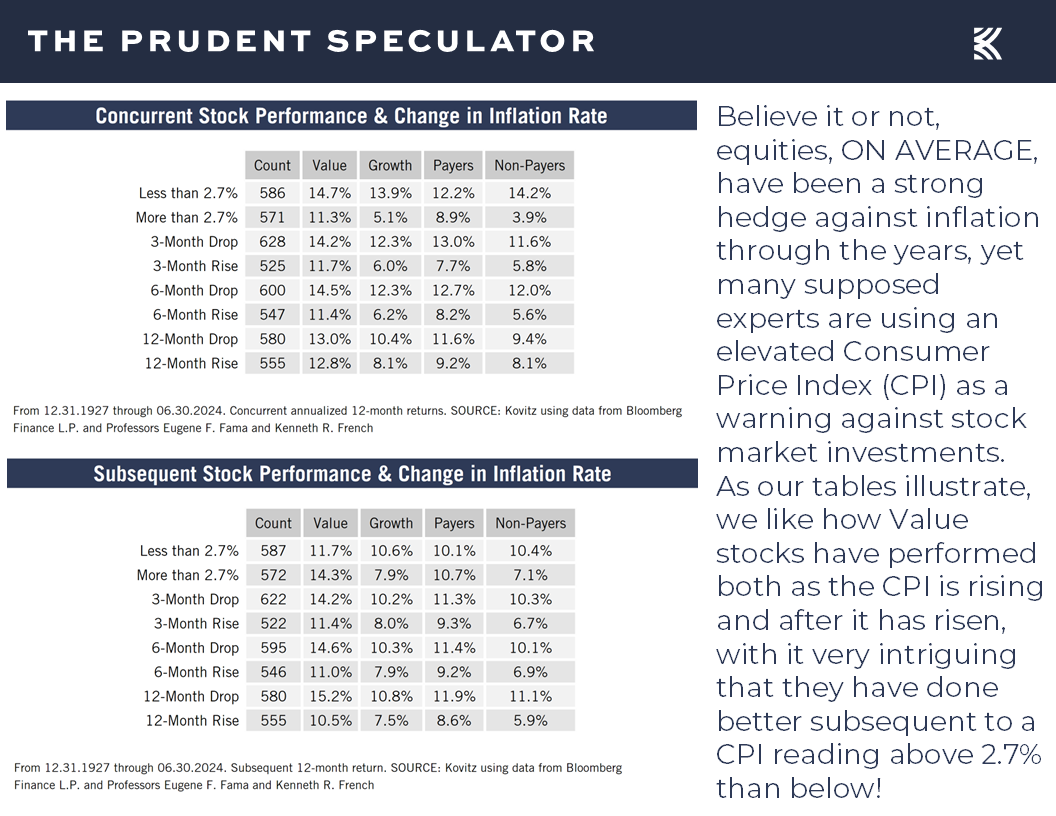

Of course, history tells us that stocks are terrific places to invest, on average, whether inflation is rising or falling,

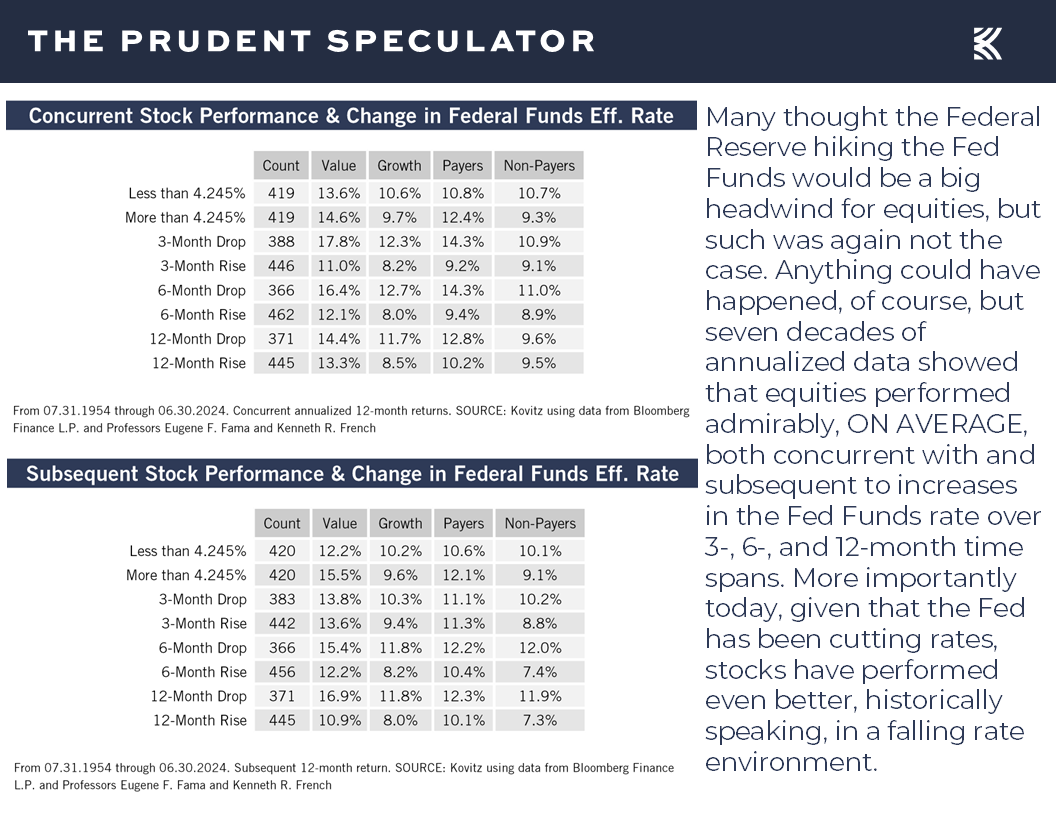

or whether the Fed is tightening or easing monetary policy.

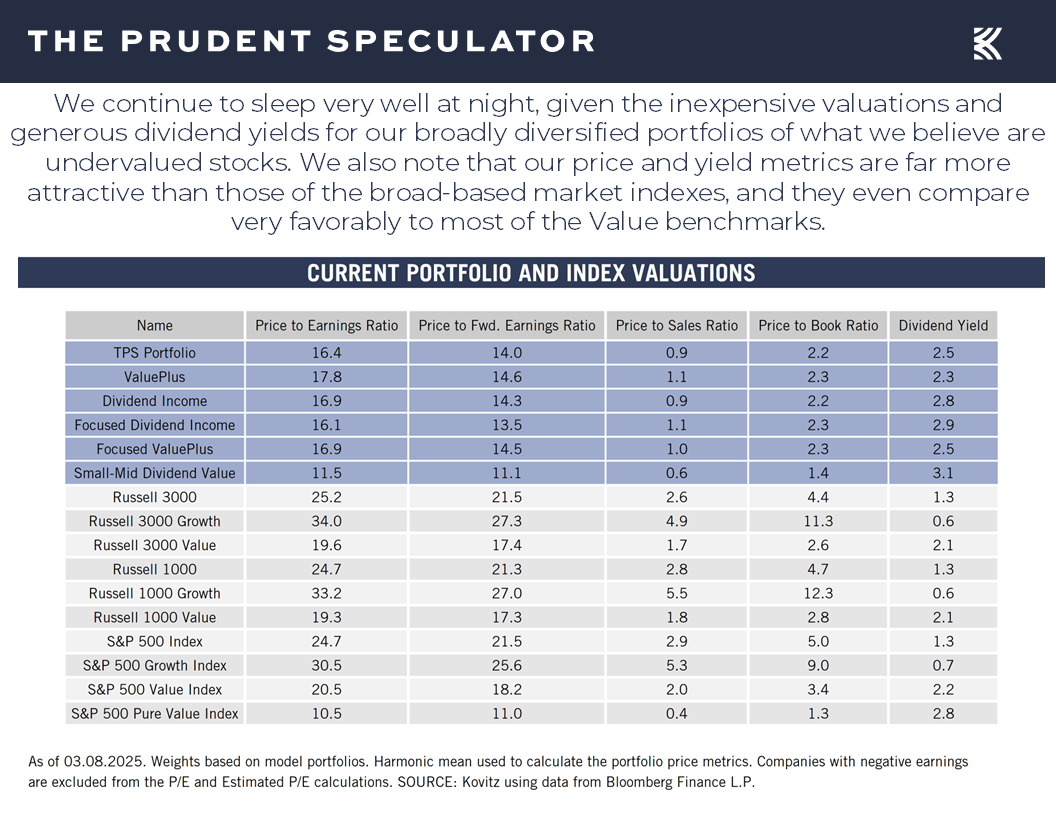

Valuations – Liking the Metrics on our Portfolios

As always, we are braced for more equity market turbulence, and we note that the futures are suggesting a return to the selling when trading resumes this week, but we continue to like the valuation metrics and long-term prospects of our broadly diversified portfolios of what we believe are undervalued stocks,

while we know that all previous disconcerting events have been overcome and then some in the fullness of time.

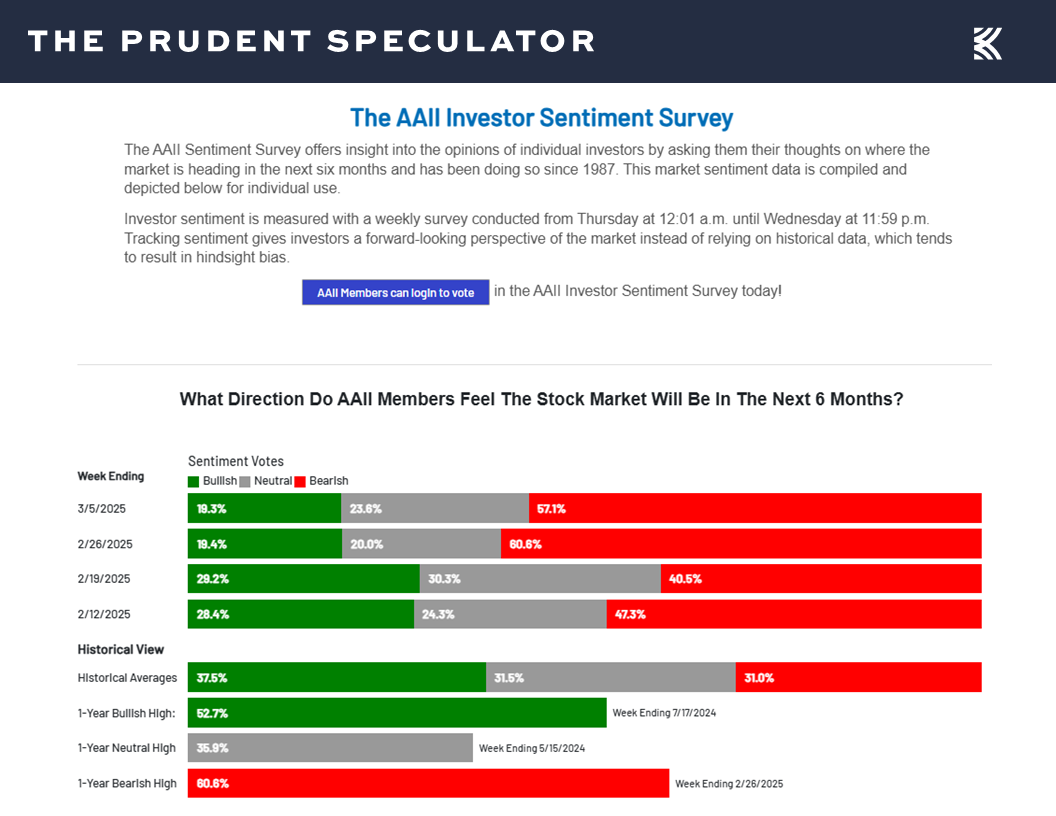

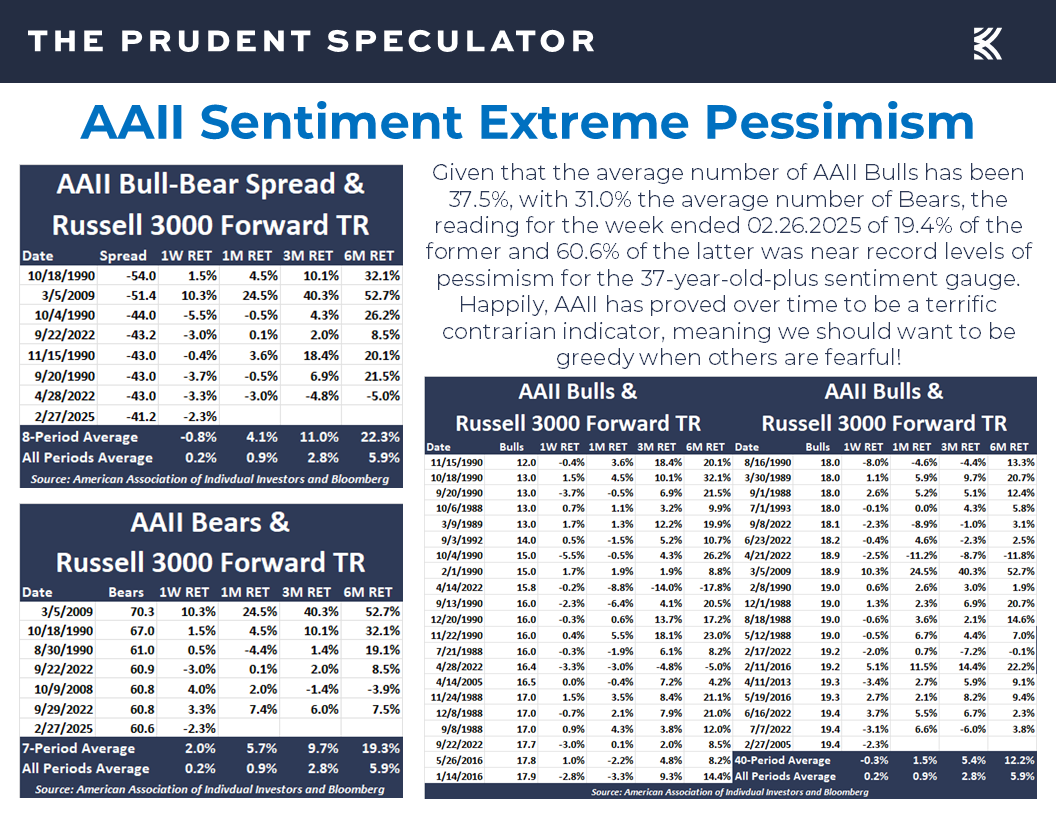

Sentiment – Major AAII Contrarian Buy Signal

We also note that the folks on Main Street remain extraordinarily pessimistic,

which has been a terrific contra-indicator, on average, for the ensuing one, three and six months over the 37-year history of the American Association of Individual Investors Sentiment survey, even as the one-week subsequent returns, on average, were dismal.

Generally speaking, it has paid to be very greedy when others are very fearful!

Stock News – Updates on seven stocks six different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Volatility, Economic Data, Valuations and more Stock News

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Volatility, Economic Data, Valuations and more Stock News. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

TPS Webinar – Replay and Slide Deck Available

Newsletter Trades – 7 Buys for 4 Portfolios

Week – Modest Rebound on Friday, But 365th Worst Five-Day Period Ever

Volatility – Stocks Go Up and Down in the Short Term, But Have Provided Handsome Rewards in the Long-Term

Econ Data – Atlanta Fed Turns Negative on GDP; ISM Says Otherwise

Powell – U.S. Economy in a Good Place

Perspective – Holding Through Recessions & Inflation Fluctuations

Valuations – Liking the Metrics on our Portfolios

Sentiment – Major AAII Contrarian Buy Signal

Stock News – Updates on TGT, BLK, FL, KR, HPE & AVGO

Week – Modest Rebound on Friday, But 365th Worst Five-Day Period Ever

You know it was a tough run when it took a late-day rebound on Friday to cut the retreat for the S&P 500 on a price basis for the full five days to 3.10%, which marked the 365th worst trading week in nearly a century. Of course, the statistics show that we have averaged more than three weeks per year of equal or worse magnitude for the popular index, while the same is true for comparable periods to the upside.

Volatility – Stocks Go Up and Down in the Short Term, But Have Provided Handsome Rewards in the Long-Term

Happily, despite inevitable trips south, the gains from times when the markets have headed north have dwarfed the short-term losses, so much so that the long-term returns from equities have been sensational…provided folks stick with stocks through thick and thin.

No doubt, the reason for the red ink last week was continued worries about tariffs, even as we have been living with high-profile U.S. tariffs on foreign goods since Trump 45 and carrying through the Biden Administration.

True, part of the near-term problem for stocks is uncertainty given that tariffs were lifted on American carmakers producing in Canada and Mexico early last week, and then later postponed again on virtually all imports to the U.S., even as they were maintained on goods from China. Though President Trump proclaimed that plans for broader “reciprocal” tariffs will go into effect on April 2, it is impossible to know if, when and what impact they will have, so we must take current estimates for handsome corporate profit growth this year and next with more than the usual grain of salt.

Econ Data – Atlanta Fed Turns Negative on GDP; ISM Says Otherwise

Certainly, there are question marks about the health of the U.S. economy as the latest estimate for real (inflation-adjusted) Q1 GDP from the Atlanta Fed stood at a contraction of 2.4%,

even as that is not the conclusion that would be drawn from the latest readings from the Institute for Supply Management (ISM) for the domestic manufacturing and non-manufacturing sectors.

Indeed, though the ISM factory gauge for February trailed expectations with a dip to 50.3, down from 50.9 in January, ISM states, “A Manufacturing PMI® above 42.3 percent, over a period of time, generally indicates an expansion of the overall economy. Therefore, the February Manufacturing PMI® indicates the overall economy grew for the 58th straight month after last contracting in April 2020. The past relationship between the Manufacturing PMI® and the overall economy indicates that the February reading (50.3 percent) corresponds to a change of plus-2.2 percent in real gross domestic product (GDP) on an annualized basis.”

It is an even more interesting story for the ISM Services measure, as the tally for February of 53.5 topped estimates of 52.5 and rose from the 52.8 tabulation for January. ISM states, “A Services PMI® above 48.6 percent, over time, generally indicates an expansion of the overall economy. Therefore, the February Services PMI® indicates the overall economy is expanding for the 57th straight month. The past relationship between the Services PMI® and the overall economy indicates that the Services PMI® for February (53.5 percent) corresponds to a 1.6-percentage point increase in real gross domestic product (GDP) on an annualized basis.”

Powell – U.S. Economy in a Good Place

We do not mean to suggest that the economy will boom in the short run, though we might expect extra activity as corporations work to get ahead of possible tariffs, but we can’t ignore comments from Jerome H. Powell on Friday afternoon. In a planned speech in New York, the Fed Chair led off with, “Despite elevated levels of uncertainty, the U.S. economy continues to be in a good place. The labor market is solid, and inflation has moved closer to our 2 percent longer-run goal,” and provided additional color to support his always-data-dependent viewpoint.

His less pessimistic outlook than that of many market watchers received some support from the employment statistics out last week, as the number of net new jobs created during February of 151,000 was up from a revised 125,000 in January and was not too far below projections.

The unemployment rate for February ticked up to 4.1%, which is still well below the historical average,

average hourly earnings rose 4.0% last month, a smidge better than the January number of 3.9%,

and first-time filings for unemployment benefits in the latest week dropped to 221,000, down from 242,000 the week prior.

To be sure, an economic slowdown is a very real possibility, and we realize that the latest yield-curve inversion where the yield on the short-term 3-month U.S. Treasury went above that of the long-term 10-Year Treasury has some arguing a recession is in the cards.

An inversion has not had a foolproof forecasting record, while history shows we wouldn’t have wanted to sell stocks, given the favorable forward average returns detailed in the chart above. Further, the present odds of recession at 25%, as tabulated by Bloomberg, remain very low.

Perspective – Holding Through Recessions & Inflation Fluctuations

That said, we have long understood that recessions are part of the investment landscape, so as students of market history, we should care about what the return numbers looked like for the kinds of stocks we have long favored. While it is impossible to know the start and end date of economic contractions as the official arbiters do not rule until after the fact, we concede that being out of stocks during the recession would have been beneficial, on average, tax-considerations notwithstanding. However, return figures in the year prior to the economic downturn were solid AND performance in the year after the recession was sensational, on average, adding more evidence to our mantra, time in the market trumps market timing.

While this (and every time) is different, we continue to believe that the Great Inflation of the early 1980s might be a good comparison to the current environment,

as that was the last time before the current period that the Federal Reserve, then under the leadership of Paul Volcker, had to battle a big spike in consumer prices. Happily, that time span proved to be extraordinarily lucrative for investors, even as there were two U.S. recessions along the way.

Of course, history tells us that stocks are terrific places to invest, on average, whether inflation is rising or falling,

or whether the Fed is tightening or easing monetary policy.

Valuations – Liking the Metrics on our Portfolios

As always, we are braced for more equity market turbulence, and we note that the futures are suggesting a return to the selling when trading resumes this week, but we continue to like the valuation metrics and long-term prospects of our broadly diversified portfolios of what we believe are undervalued stocks,

while we know that all previous disconcerting events have been overcome and then some in the fullness of time.

Sentiment – Major AAII Contrarian Buy Signal

We also note that the folks on Main Street remain extraordinarily pessimistic,

which has been a terrific contra-indicator, on average, for the ensuing one, three and six months over the 37-year history of the American Association of Individual Investors Sentiment survey, even as the one-week subsequent returns, on average, were dismal.

Generally speaking, it has paid to be very greedy when others are very fearful!

Stock News – Updates on seven stocks six different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.