The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Volatility, Financial Press, Interest Rates, Univ. of Michigan more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Financial Press – Not Exactly Helpful

Interest Rates – Fed Funds Futures and 10-Year Yields Move Higher

Volatility – Ups and Downs Normal; Long-Term Trend is Up

Univ. of Michigan – Goldilocks Consumer Sentiment/Inflation Expectations Data

Other Econ Stats – Mixed Numbers

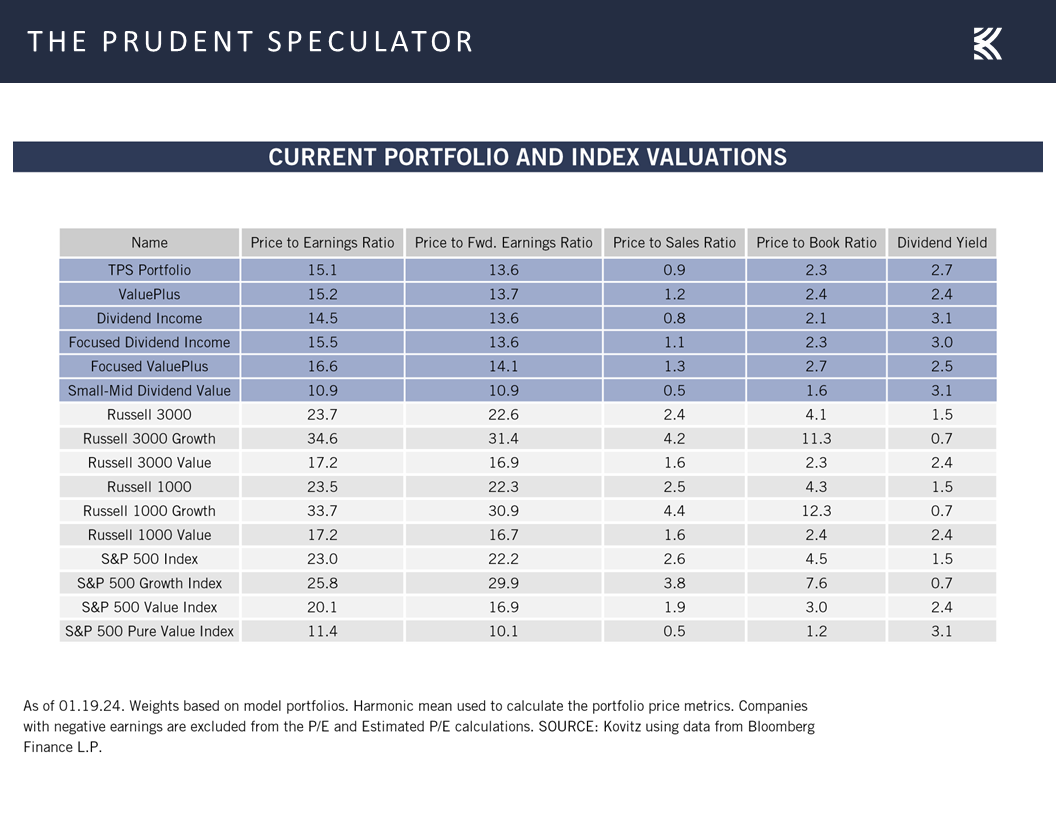

Valuations – Value Stocks Reasonably Priced

EPS – Q4 Profits Beating the Street

Stock News – Updates on thirteen stock across four different sectors

Financial Press – Not Exactly Helpful

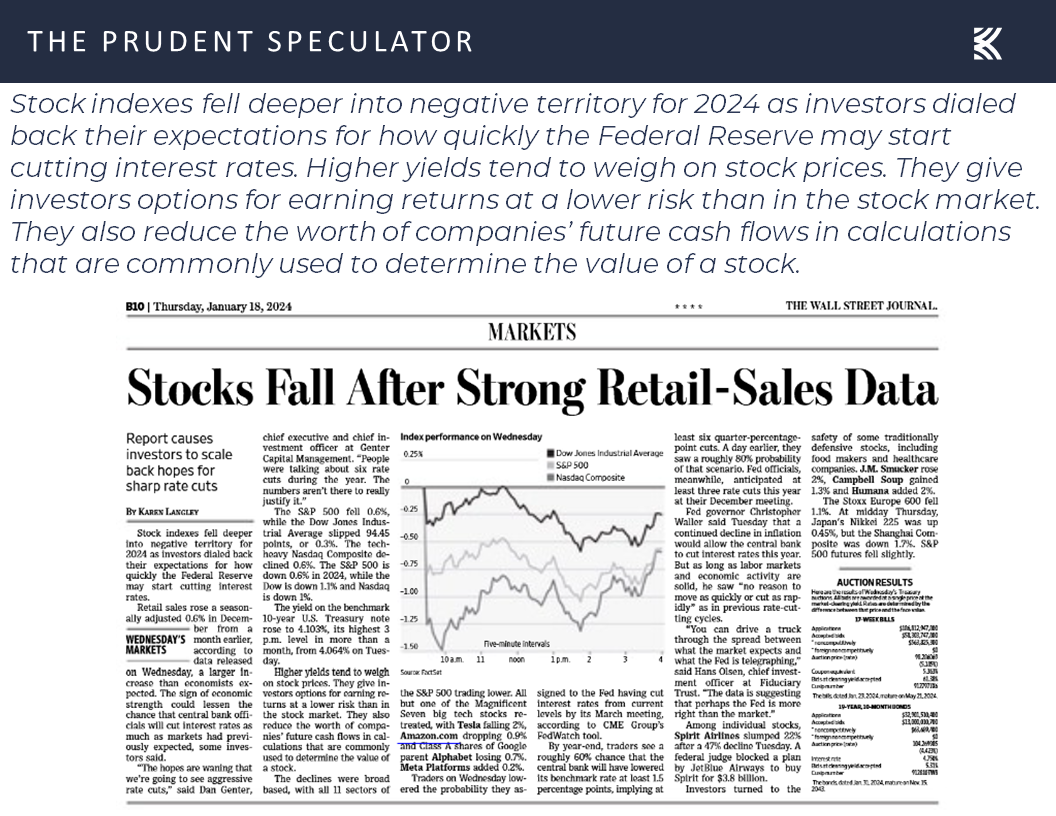

It is always interesting to see the rationale offered for short-term movements in the equity markets. Stocks fell over the first part of last week,

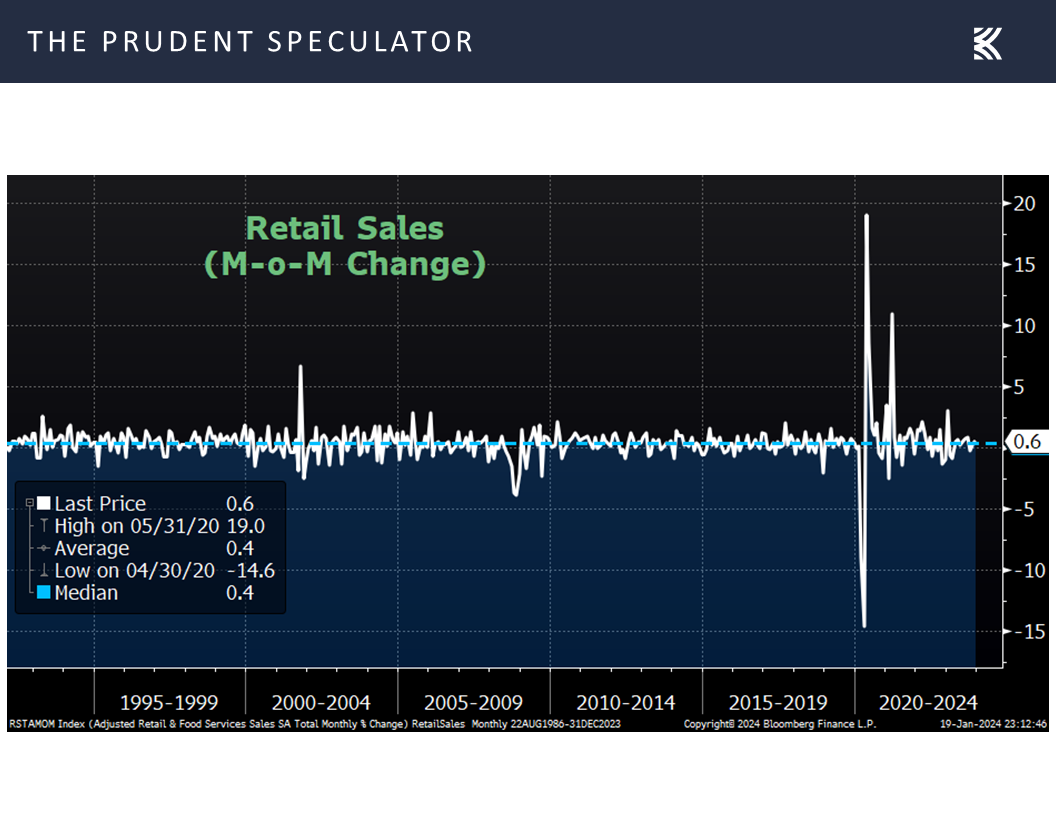

evidently on worries that more favorable economic data, like better-than-expected numbers on consumer spending,

Interest Rates – Fed Funds Futures and 10-Year Yields Move Higher

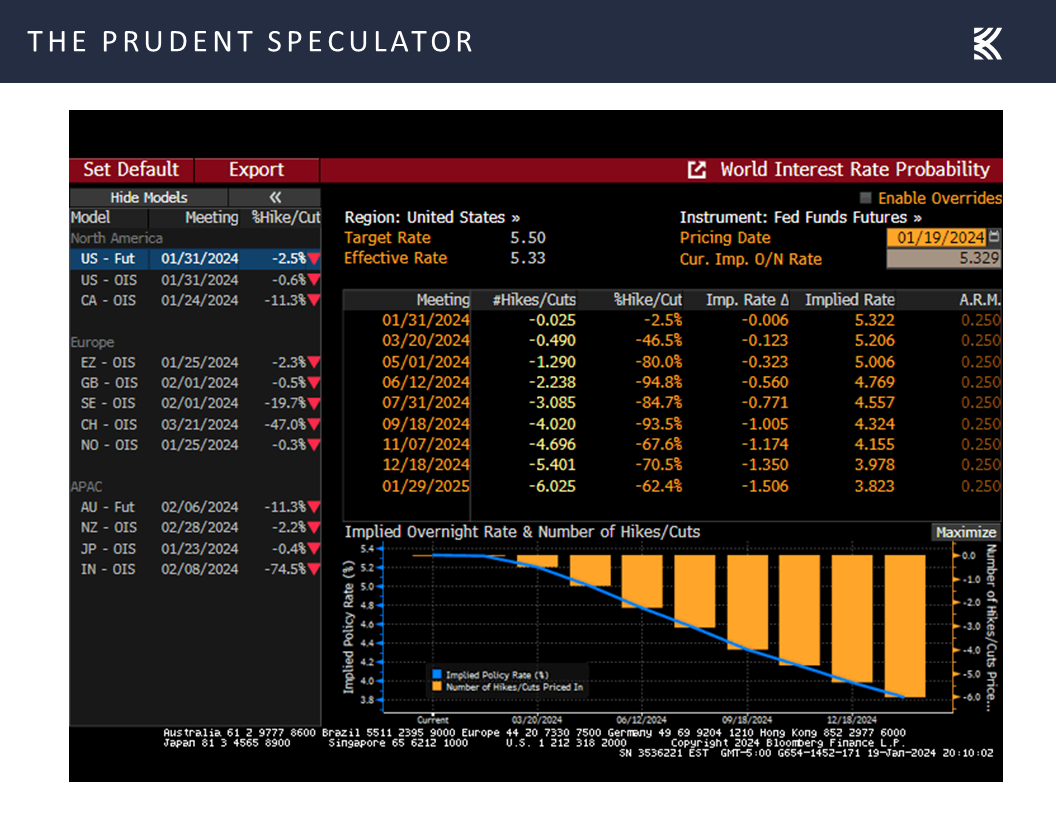

would cause the Federal Reserve to delay loosening monetary policy via cuts in the Federal Funds rate. Indeed, with Atlanta Fed President Raphael Bostic and Fed Governor Christopher Waller each also suggesting that cuts may come later versus sooner, the Fed Funds futures market saw bets on the year-end 2024 U.S. benchmark lending rate climb to 3.98%, up from 3.65% a week ago,

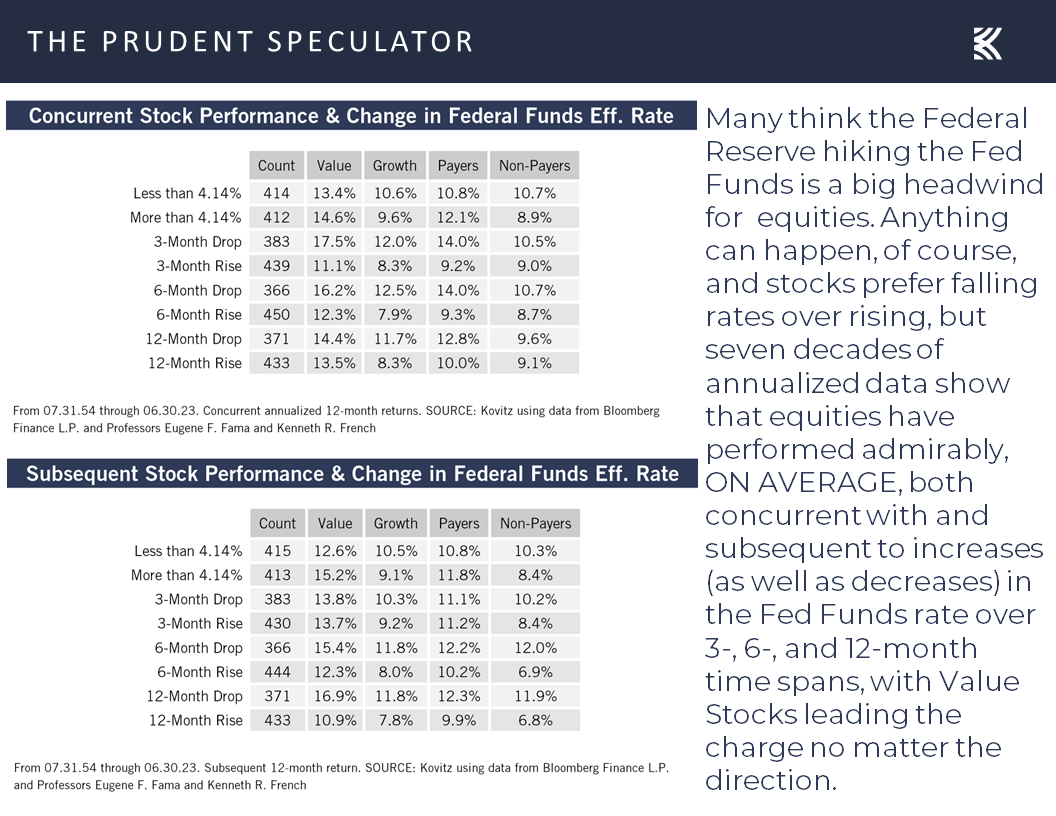

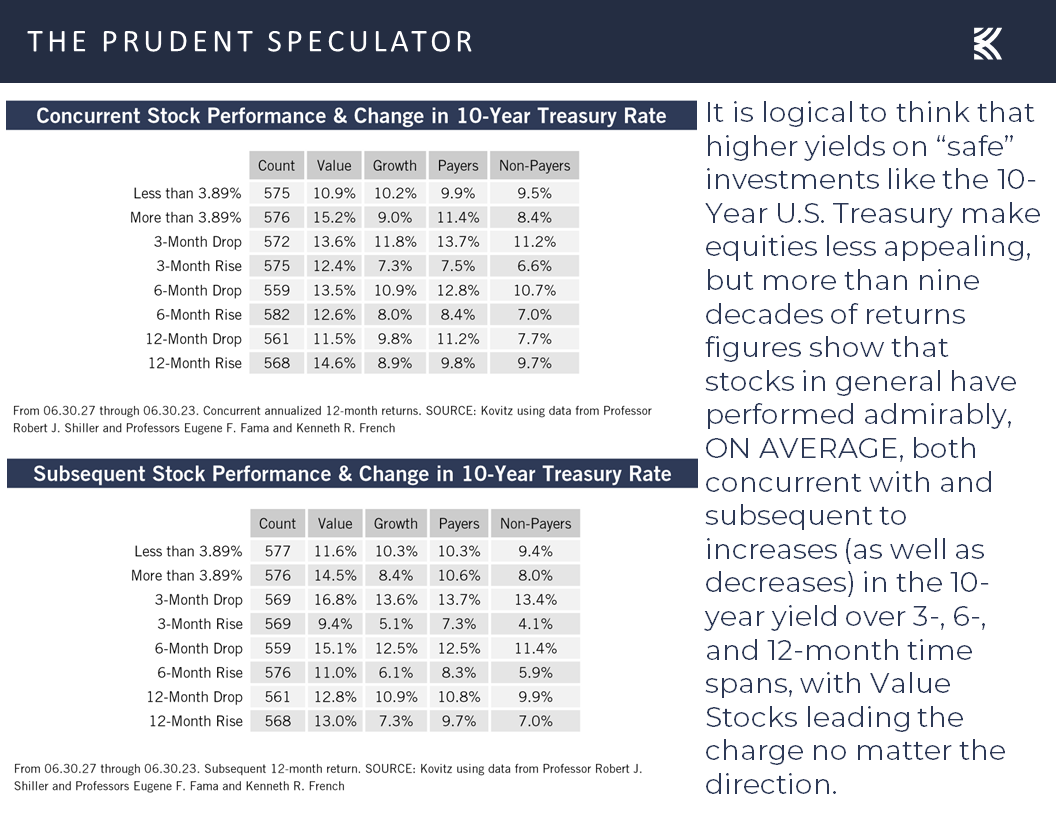

but seven decades of market history argue that whether the Fed is raising or lowering interest rates, stocks, on average, have performed just fine.

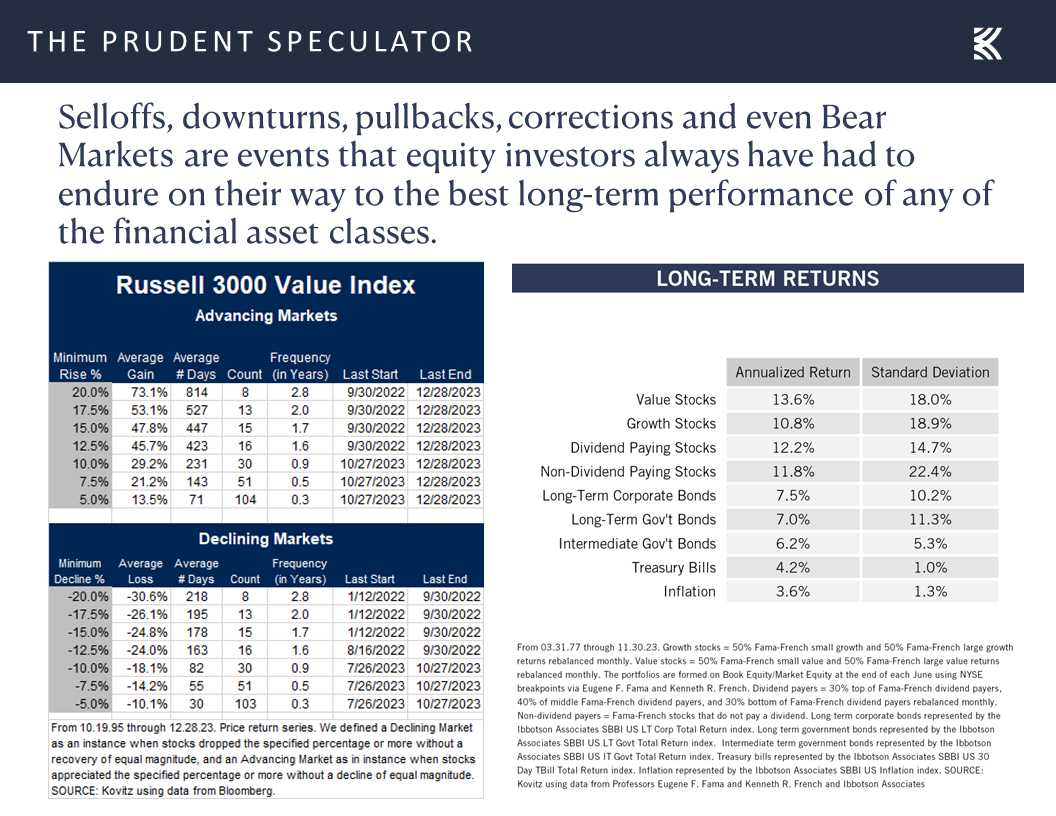

Volatility – Ups and Downs Normal; Long-Term Trend is Up

That is not to say that there aren’t bumps in the road along the way, as 5% setbacks in the Russell 3000 Value index have happened three times per year on average, 10% corrections have occurred every 11 months on average and 20% Bear Markets have taken place every 2.8 years, on average, but equities have proved to be very rewarding,

for those who remember that time in the market trumps market timing,

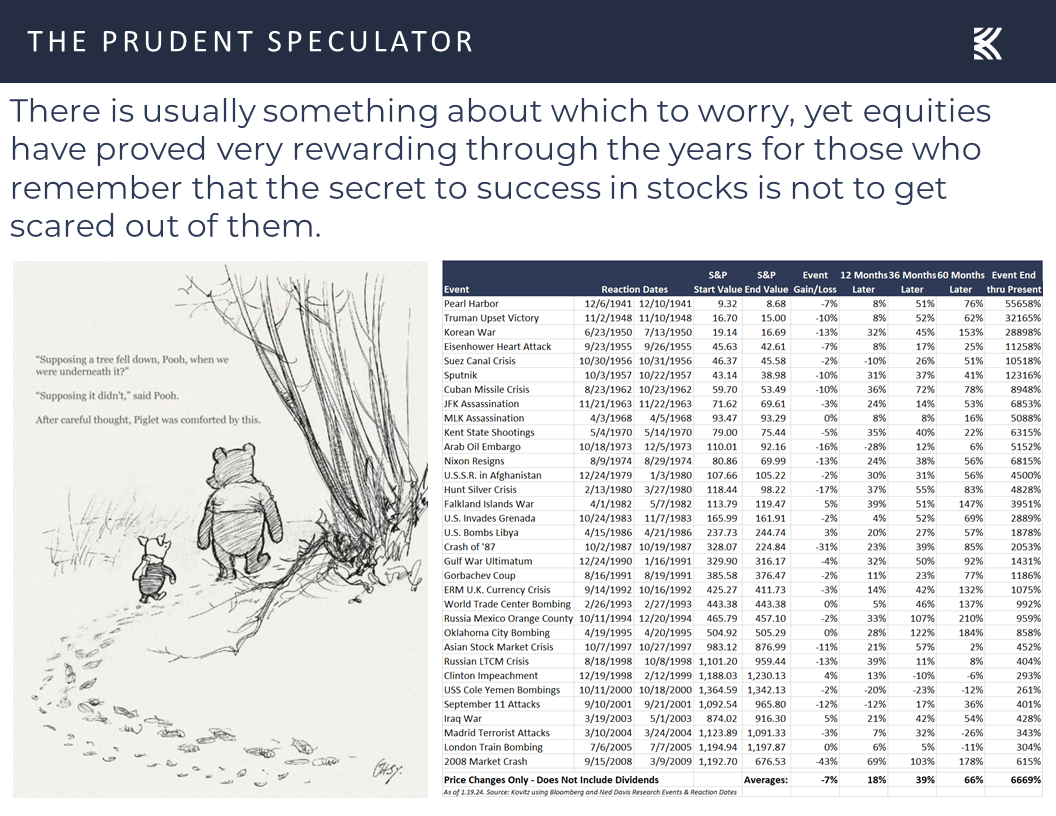

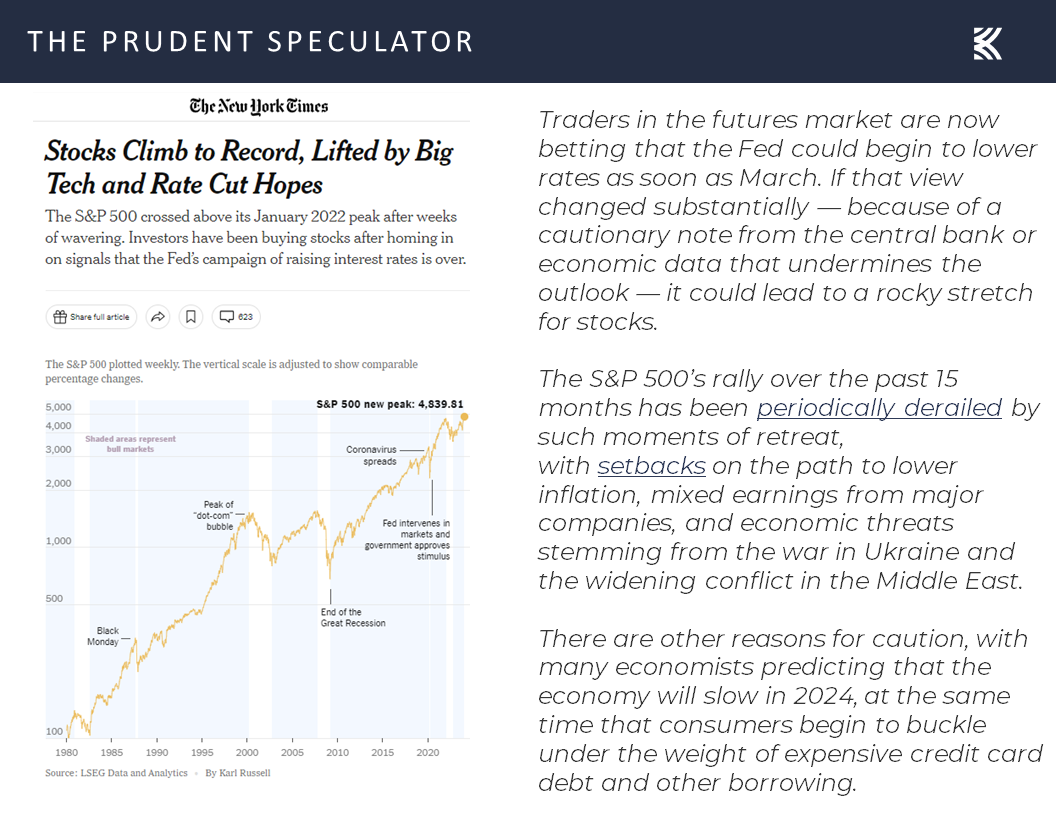

True, it isn’t always easy to keep the faith through thick and thin, as the financial press seemingly errs on the side of warning folks of the risks associated with stocks while downplaying the rewards and drawing different conclusions from one day to the next. Case in point is the latest feature story in The New York Times,

acknowledging the all-time just set on Friday for the broad-based S&P 500 and crediting hopes for Fed Rate cuts (weren’t these just dashed two days earlier?), yet suggesting that a significant shift in the timing could lead to a “rocky stretch” for equities.

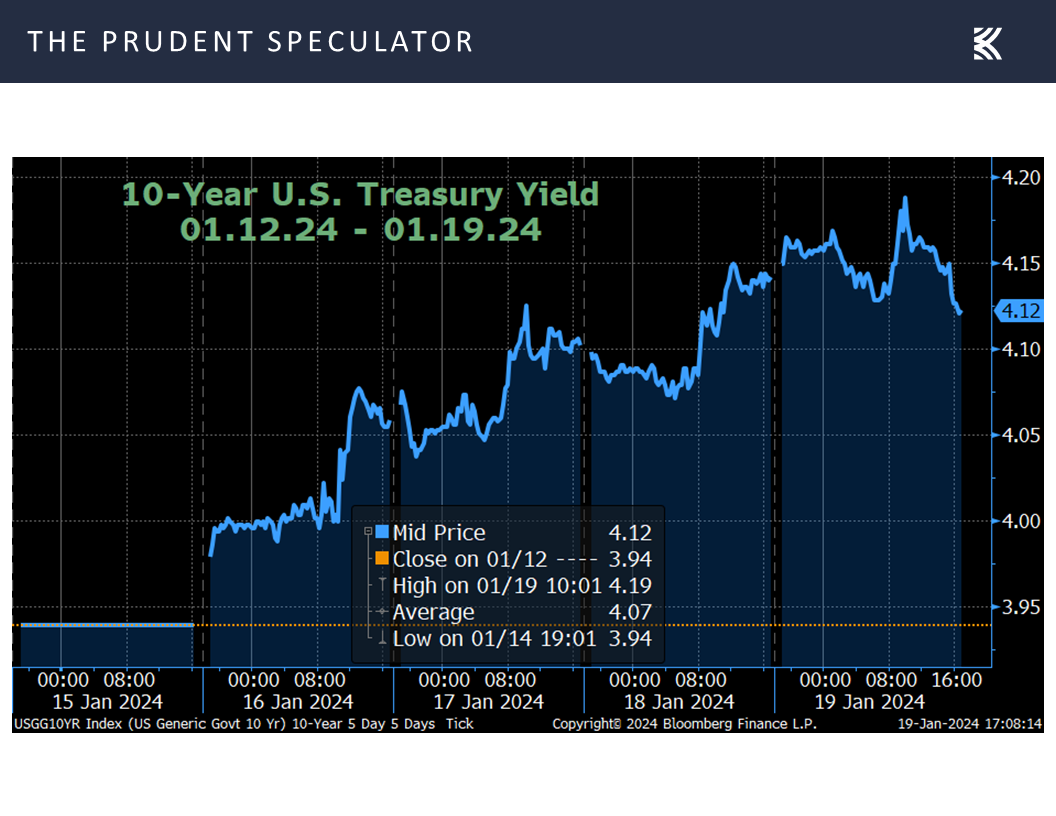

As detailed on the Fed Funds futures discussion above, there was a significant shift in the timing of rate cuts last week, which led to the yield on the 10-Year U.S. Treasury jumping from 3.94% to 4.12% and climbing above the psychologically significant 4% threshold,

yet rising rates also have not proved to be a near-term headwind, on average, for stocks.

Univ. of Michigan – Goldilocks Consumer Sentiment/Inflation Expectations Data

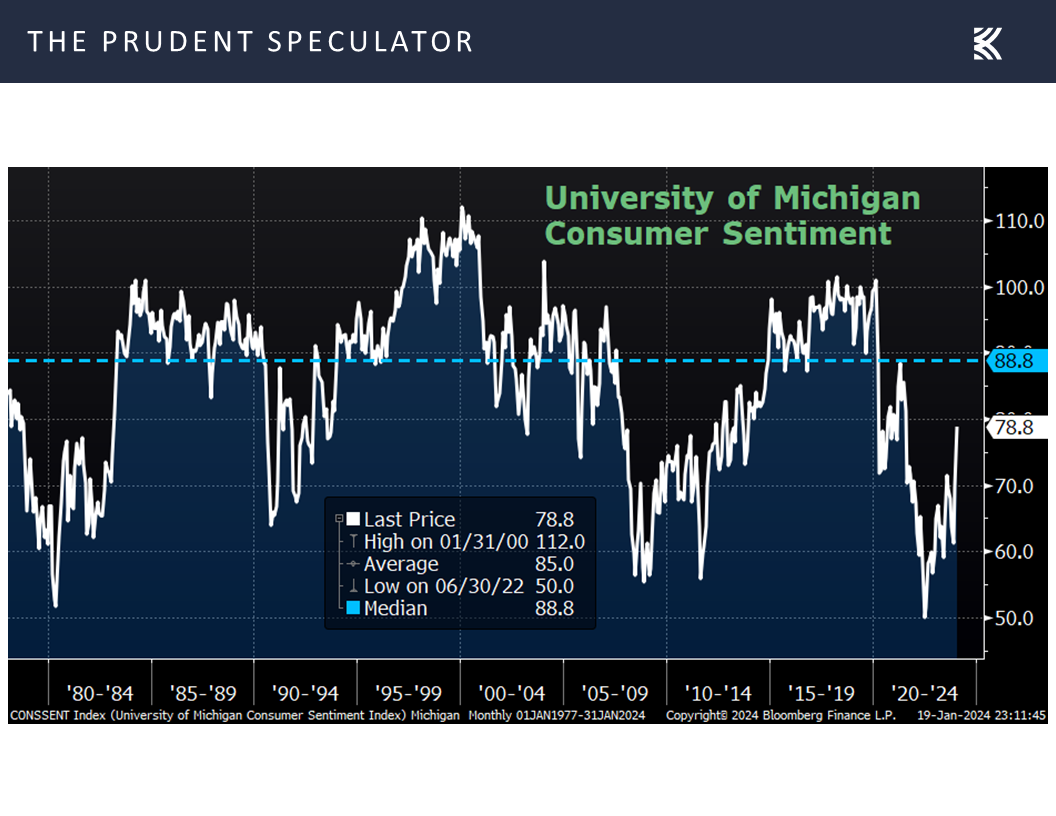

To be fair, it certainly was a positive on Friday that the University of Michigan Consumer Sentiment Survey saw a big jump to the best reading in more than two years,

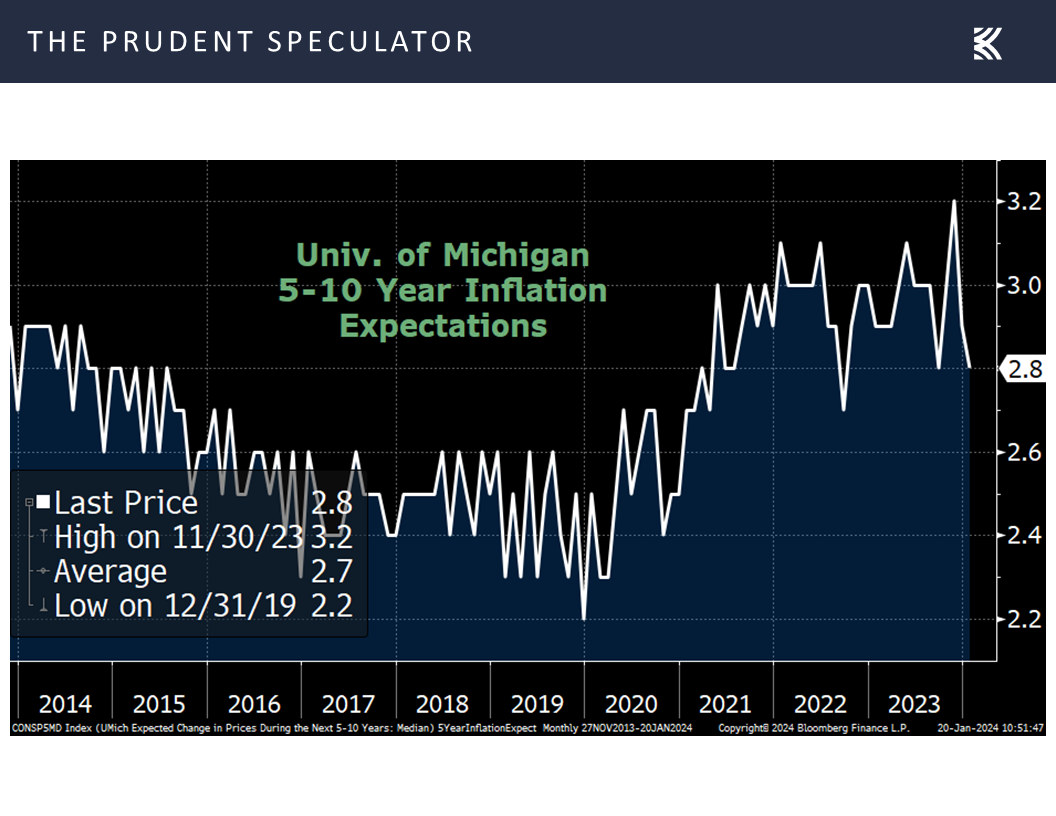

while longer-term Inflation Expectations declined to a level nearly in line with the 10-year norm,

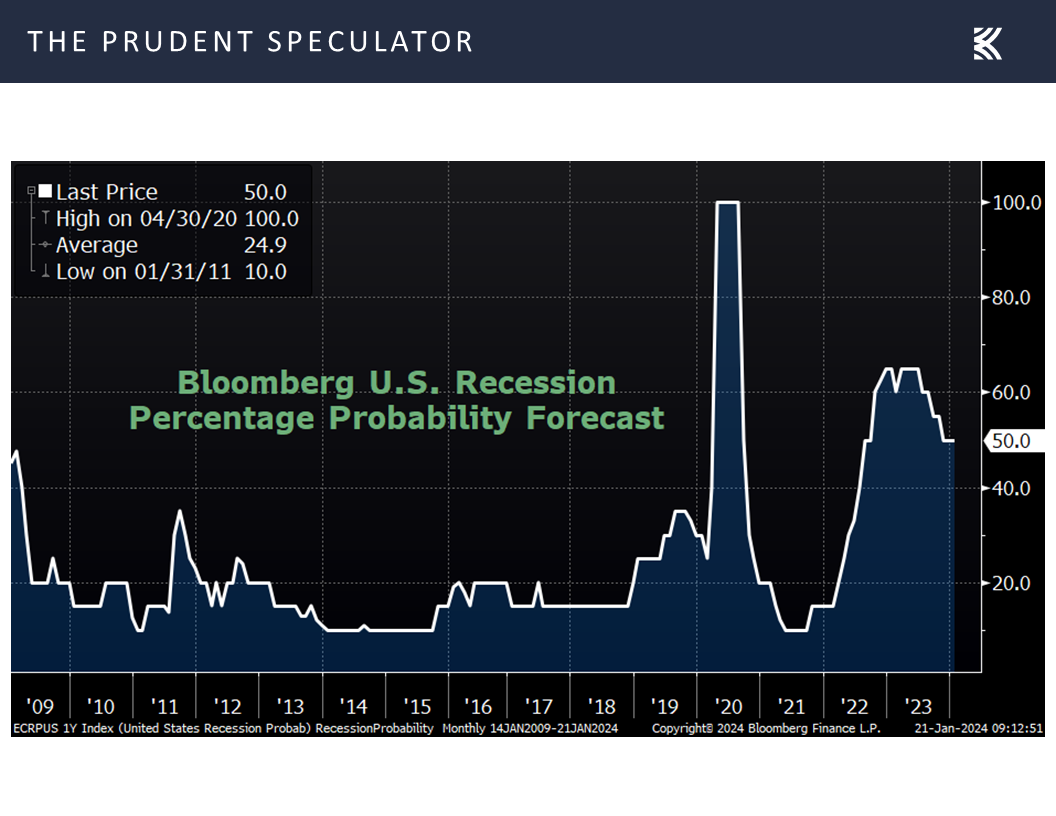

bolstering the argument for a so-called economic “soft landing,” even as the odds of recession in the next 12 months, as tabulated by Bloomberg, remained at 50%.

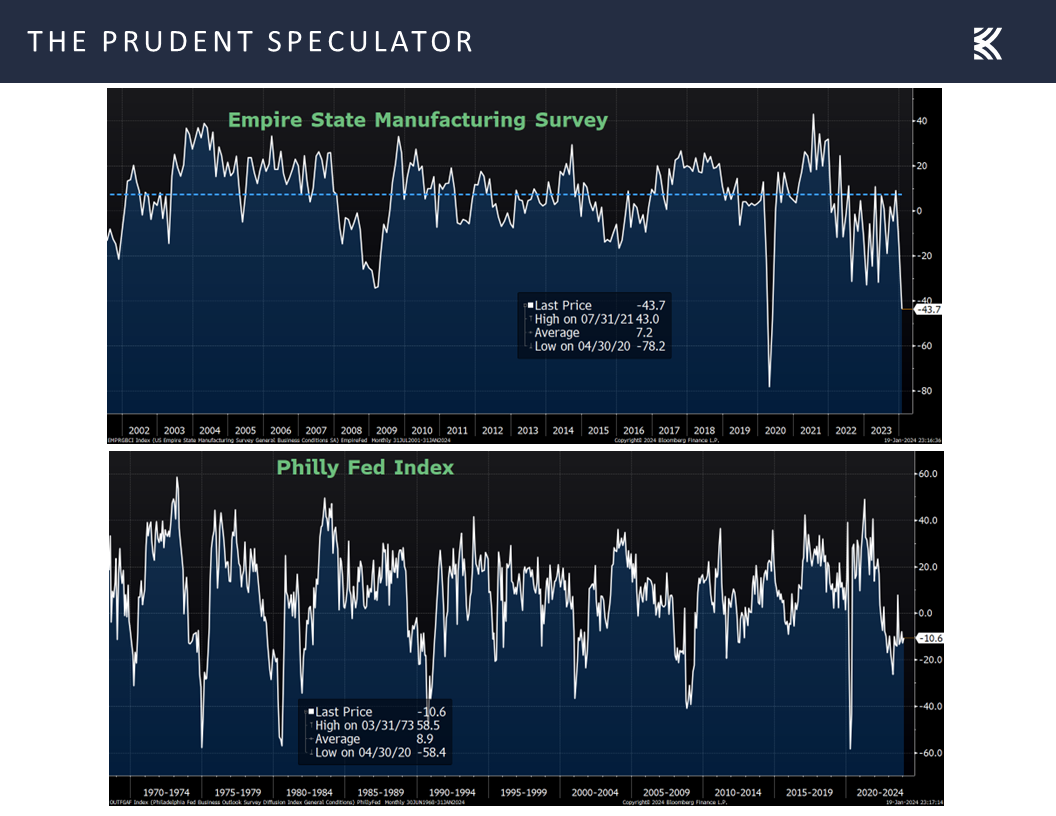

Other Econ Stats – Mixed Numbers

Given that other economic numbers out last week were mixed, with poor readings on the health of the factory sector on the East Coast,

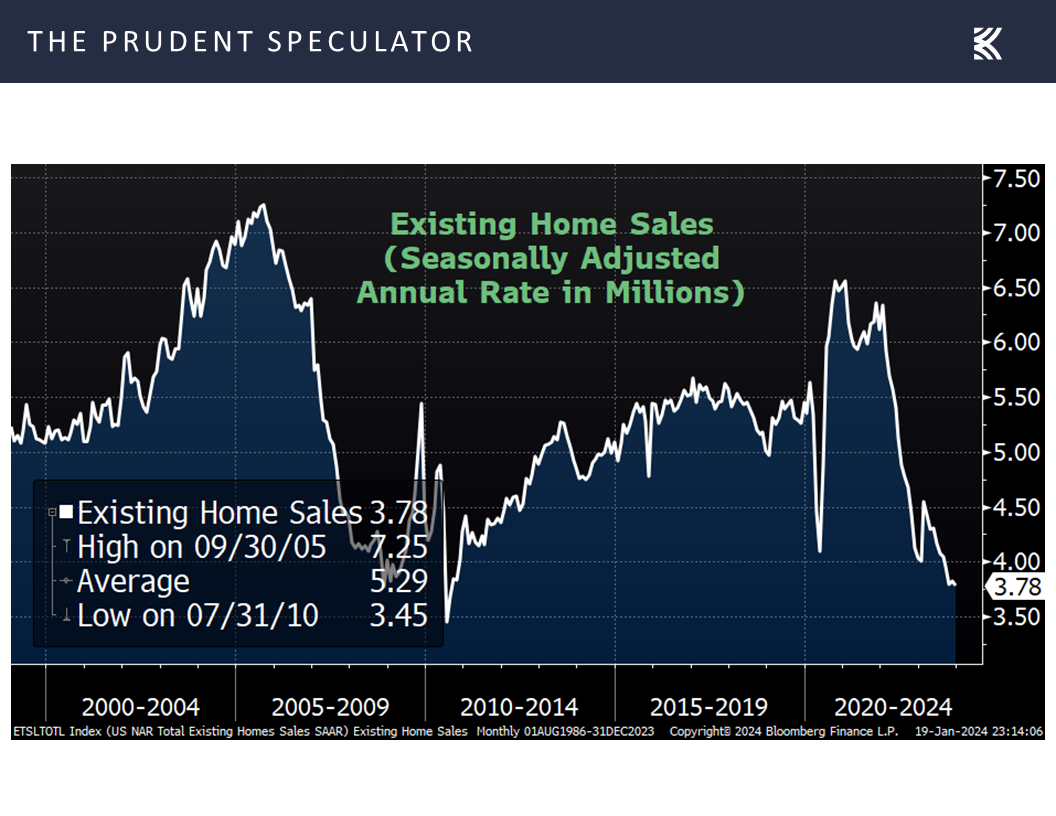

and weaker-than-expected sales of existing homes in December,

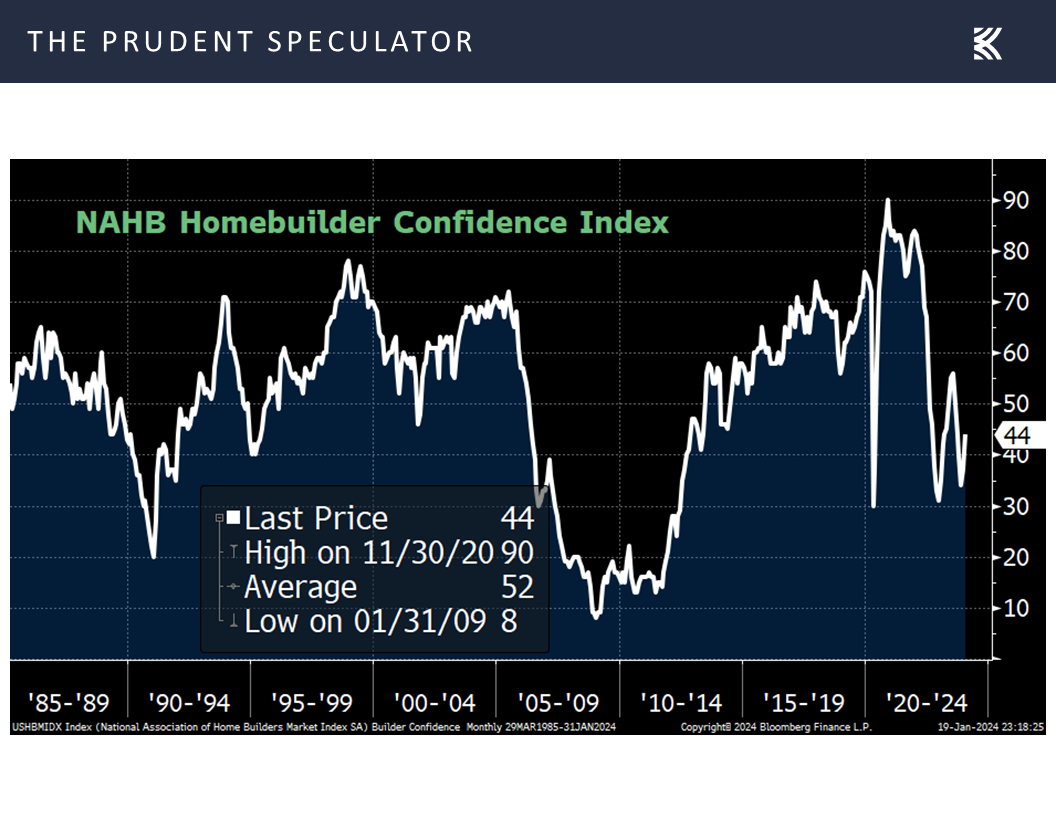

arguably offset by better-than-estimated homebuilder confidence,

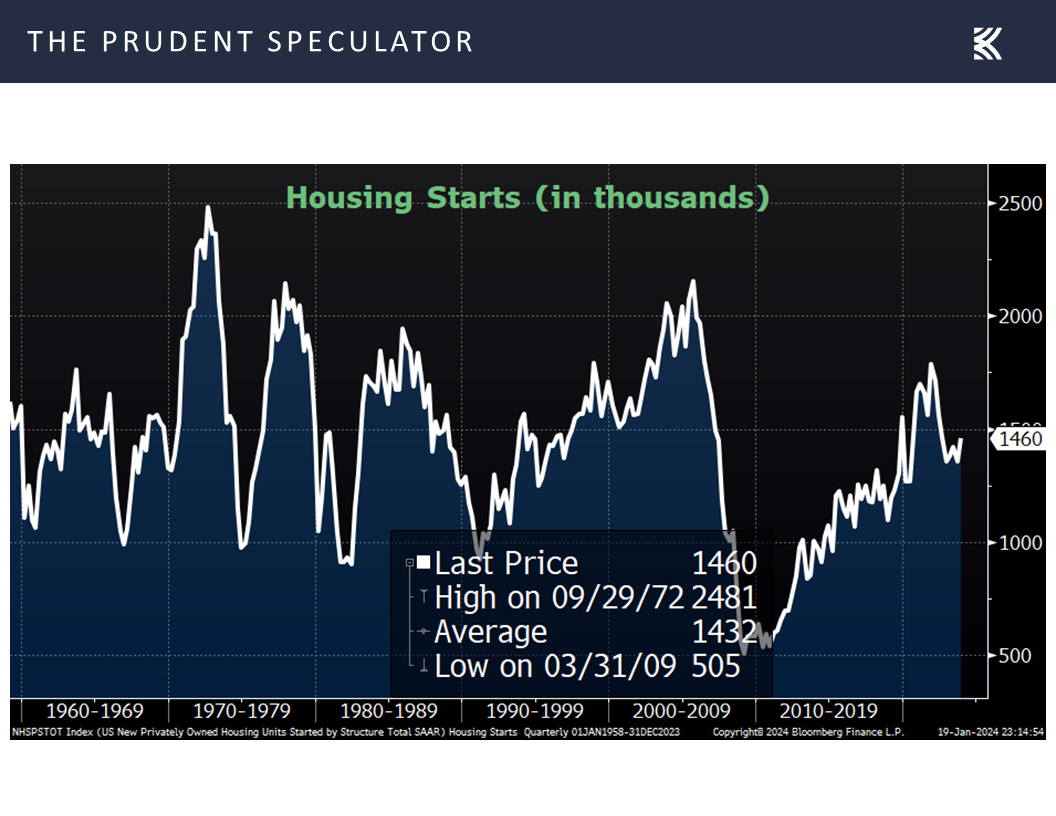

and housing starts,

not to mention a continuation of the very strong labor market,

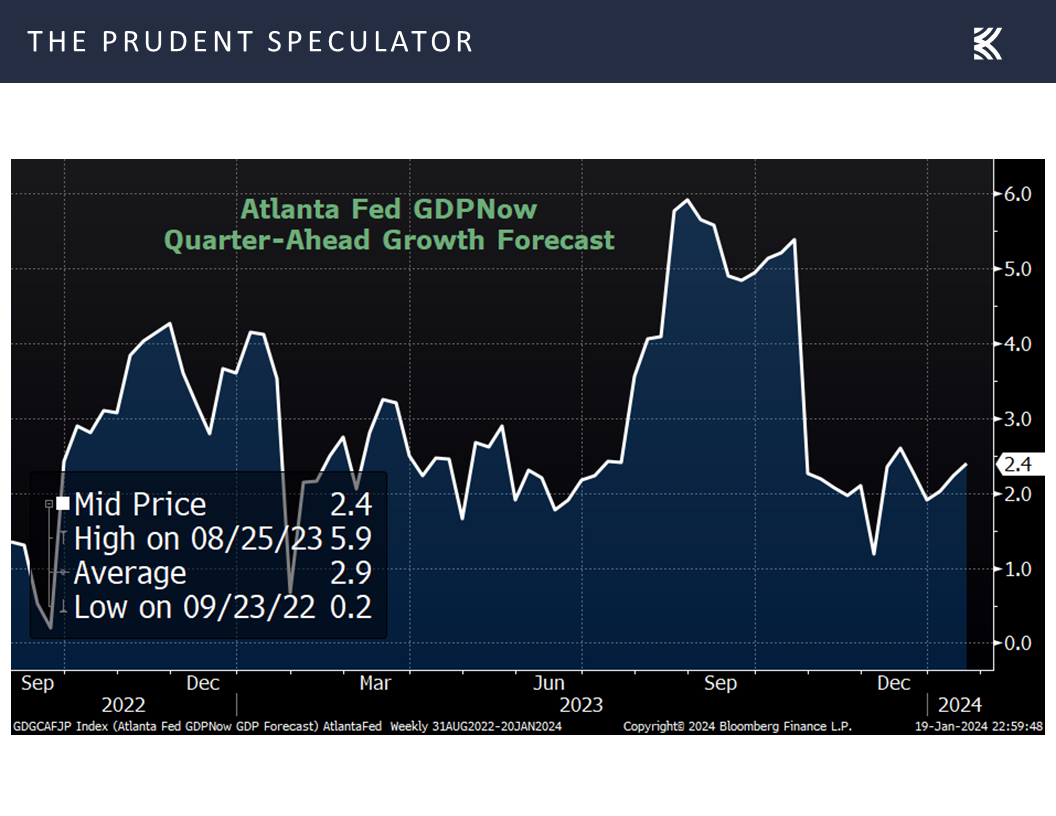

we suppose that it isn’t surprising to see many thinking the economic glass is half-empty despite a modest uptick to 2.4% in the outlook for real (inflation-adjusted) Q4 U.S. GDP growth, per the Atlanta Fed.

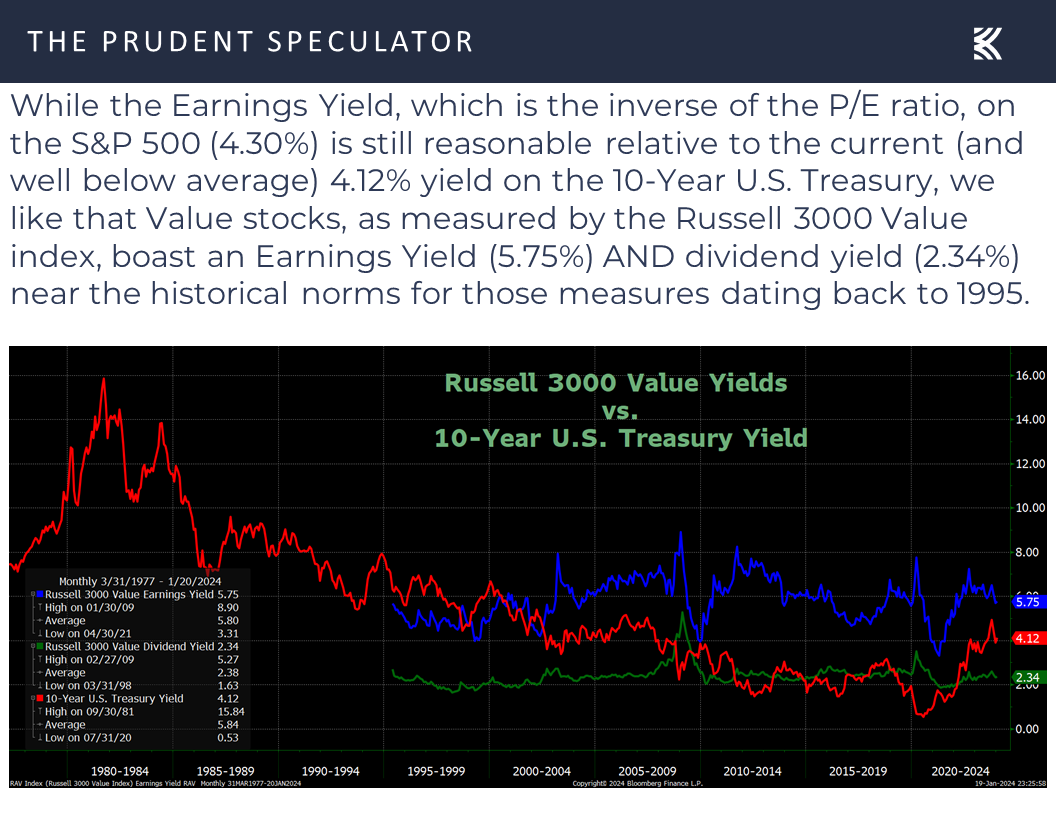

Valuations – Value Stocks Reasonably Priced

We shall see if the S&P milestone leads to profit-taking in the near term or a continuation of the rally since the recent October 27, 2023, market bottom, but we find no reason to alter our enthusiasm for the long-term prospects of our broadly diversified portfolios of what we believe to be undervalued stocks,

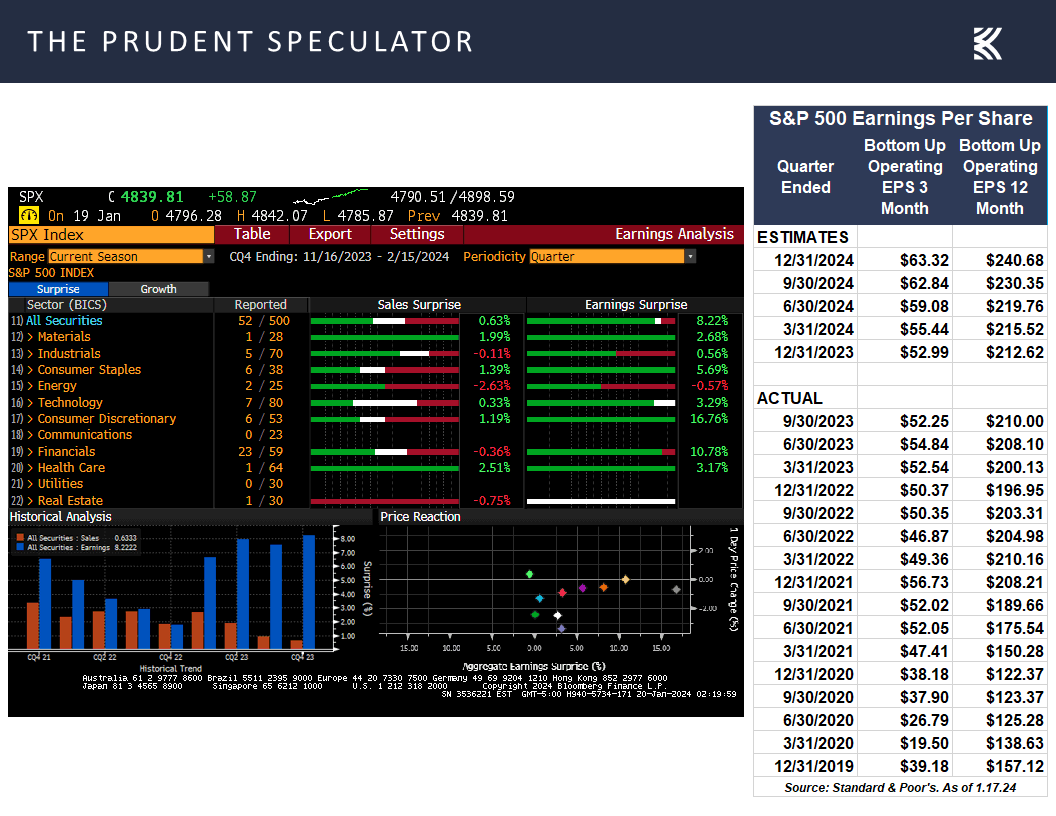

EPS – Q4 Profits Beating the Street

as we like that the outlook for corporate profits remains favorable, with more than 86% of the 52 constituents of the S&P 500 to have announced Q4 results thus far beating consensus EPS analyst forecasts,

and we think Value stocks in general remain reasonably priced, even with the recent back-up in interest rates.

Stock News – Updates on thirteen stocks across four different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Volatility, Financial Press, Interest Rates, Univ. of Michigan and more

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Volatility, Financial Press, Interest Rates, Univ. of Michigan more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Financial Press – Not Exactly Helpful

Interest Rates – Fed Funds Futures and 10-Year Yields Move Higher

Volatility – Ups and Downs Normal; Long-Term Trend is Up

Univ. of Michigan – Goldilocks Consumer Sentiment/Inflation Expectations Data

Other Econ Stats – Mixed Numbers

Valuations – Value Stocks Reasonably Priced

EPS – Q4 Profits Beating the Street

Stock News – Updates on thirteen stock across four different sectors

Financial Press – Not Exactly Helpful

It is always interesting to see the rationale offered for short-term movements in the equity markets. Stocks fell over the first part of last week,

evidently on worries that more favorable economic data, like better-than-expected numbers on consumer spending,

Interest Rates – Fed Funds Futures and 10-Year Yields Move Higher

would cause the Federal Reserve to delay loosening monetary policy via cuts in the Federal Funds rate. Indeed, with Atlanta Fed President Raphael Bostic and Fed Governor Christopher Waller each also suggesting that cuts may come later versus sooner, the Fed Funds futures market saw bets on the year-end 2024 U.S. benchmark lending rate climb to 3.98%, up from 3.65% a week ago,

but seven decades of market history argue that whether the Fed is raising or lowering interest rates, stocks, on average, have performed just fine.

Volatility – Ups and Downs Normal; Long-Term Trend is Up

That is not to say that there aren’t bumps in the road along the way, as 5% setbacks in the Russell 3000 Value index have happened three times per year on average, 10% corrections have occurred every 11 months on average and 20% Bear Markets have taken place every 2.8 years, on average, but equities have proved to be very rewarding,

for those who remember that time in the market trumps market timing,

True, it isn’t always easy to keep the faith through thick and thin, as the financial press seemingly errs on the side of warning folks of the risks associated with stocks while downplaying the rewards and drawing different conclusions from one day to the next. Case in point is the latest feature story in The New York Times,

acknowledging the all-time just set on Friday for the broad-based S&P 500 and crediting hopes for Fed Rate cuts (weren’t these just dashed two days earlier?), yet suggesting that a significant shift in the timing could lead to a “rocky stretch” for equities.

As detailed on the Fed Funds futures discussion above, there was a significant shift in the timing of rate cuts last week, which led to the yield on the 10-Year U.S. Treasury jumping from 3.94% to 4.12% and climbing above the psychologically significant 4% threshold,

yet rising rates also have not proved to be a near-term headwind, on average, for stocks.

Univ. of Michigan – Goldilocks Consumer Sentiment/Inflation Expectations Data

To be fair, it certainly was a positive on Friday that the University of Michigan Consumer Sentiment Survey saw a big jump to the best reading in more than two years,

while longer-term Inflation Expectations declined to a level nearly in line with the 10-year norm,

bolstering the argument for a so-called economic “soft landing,” even as the odds of recession in the next 12 months, as tabulated by Bloomberg, remained at 50%.

Other Econ Stats – Mixed Numbers

Given that other economic numbers out last week were mixed, with poor readings on the health of the factory sector on the East Coast,

and weaker-than-expected sales of existing homes in December,

arguably offset by better-than-estimated homebuilder confidence,

and housing starts,

not to mention a continuation of the very strong labor market,

we suppose that it isn’t surprising to see many thinking the economic glass is half-empty despite a modest uptick to 2.4% in the outlook for real (inflation-adjusted) Q4 U.S. GDP growth, per the Atlanta Fed.

Valuations – Value Stocks Reasonably Priced

We shall see if the S&P milestone leads to profit-taking in the near term or a continuation of the rally since the recent October 27, 2023, market bottom, but we find no reason to alter our enthusiasm for the long-term prospects of our broadly diversified portfolios of what we believe to be undervalued stocks,

EPS – Q4 Profits Beating the Street

as we like that the outlook for corporate profits remains favorable, with more than 86% of the 52 constituents of the S&P 500 to have announced Q4 results thus far beating consensus EPS analyst forecasts,

and we think Value stocks in general remain reasonably priced, even with the recent back-up in interest rates.

Stock News – Updates on thirteen stocks across four different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.