The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Volatility, GDP Outlook, Geopolitics, Interest Rates and more. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Newsletter Portfolio Trades – Exited DHLGY

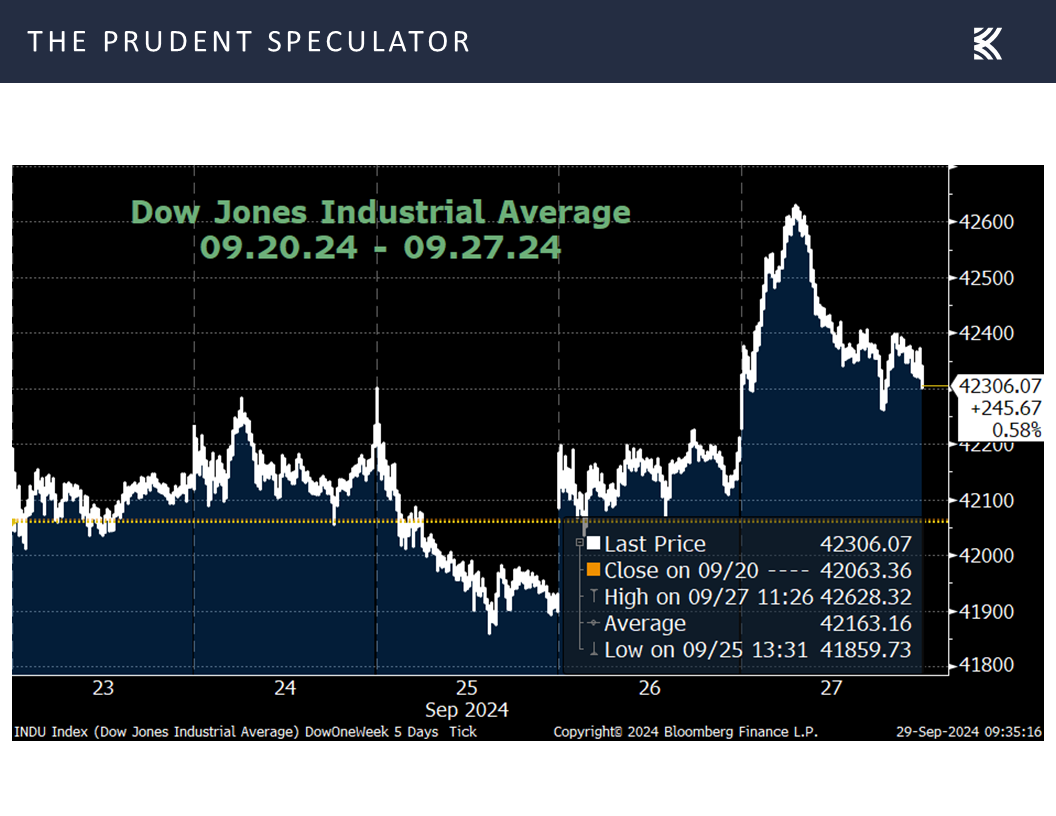

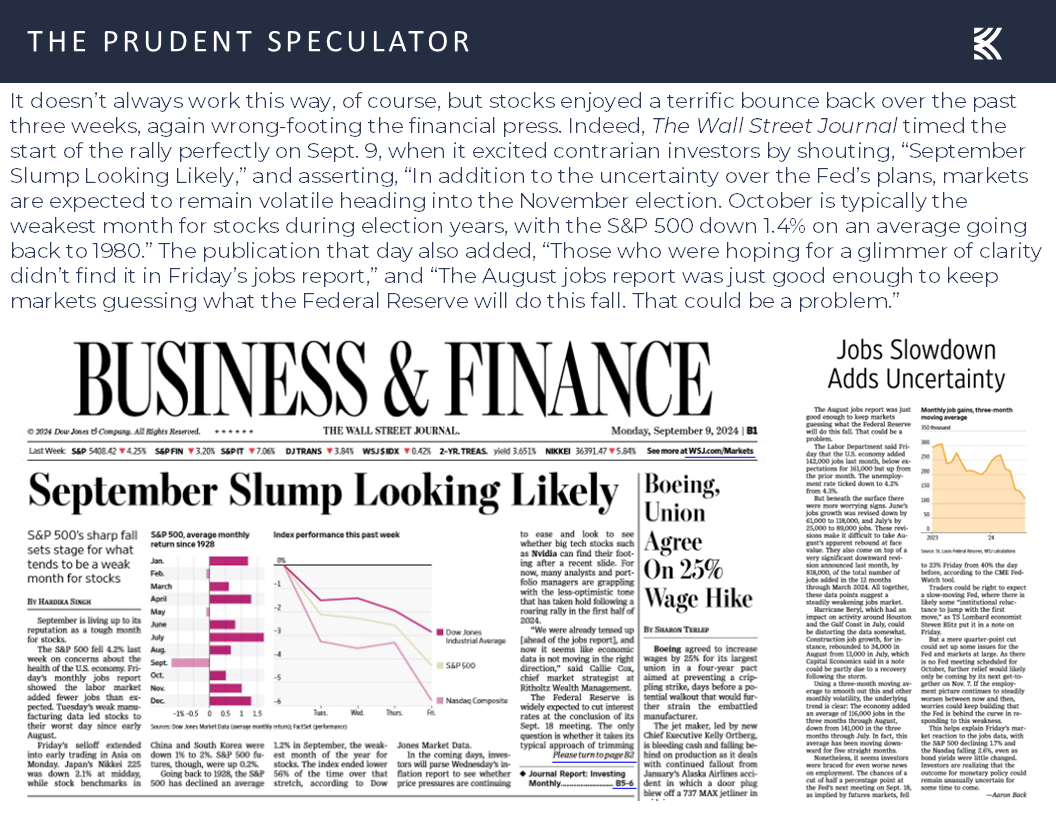

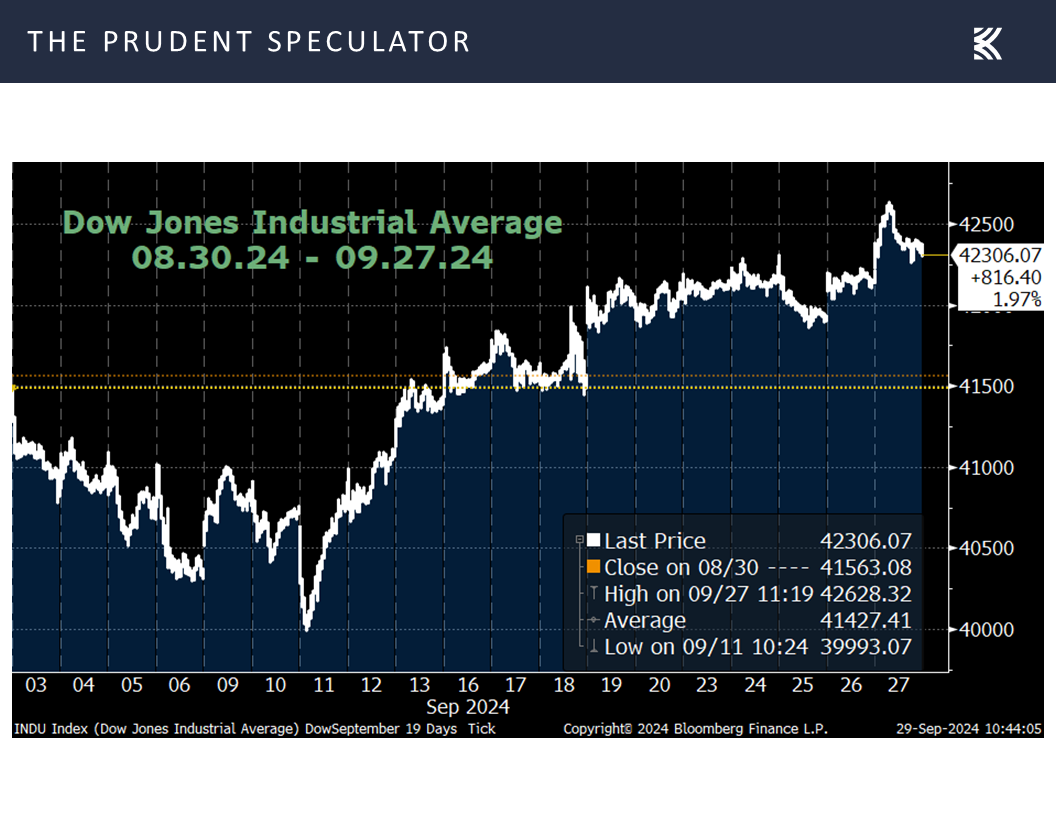

Week in Review – Rally Off Early-September Lows Continues

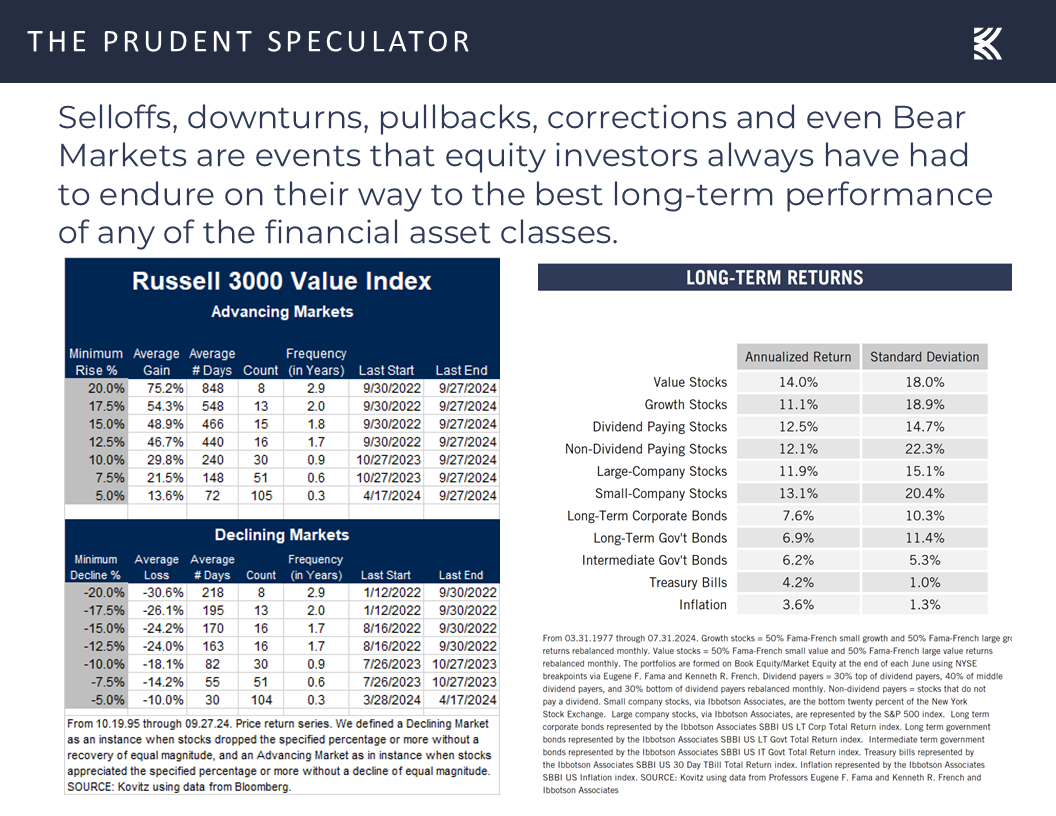

Volatility – Ups and Downs Normal but Long-Term Trend is Higher

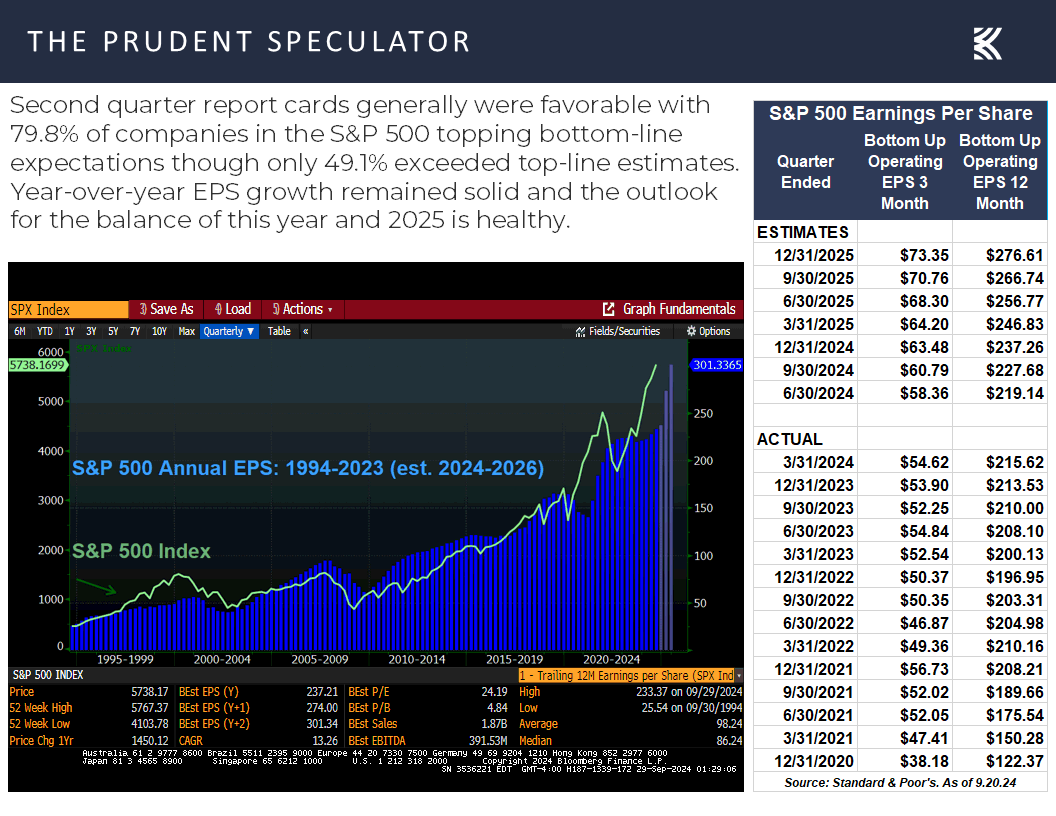

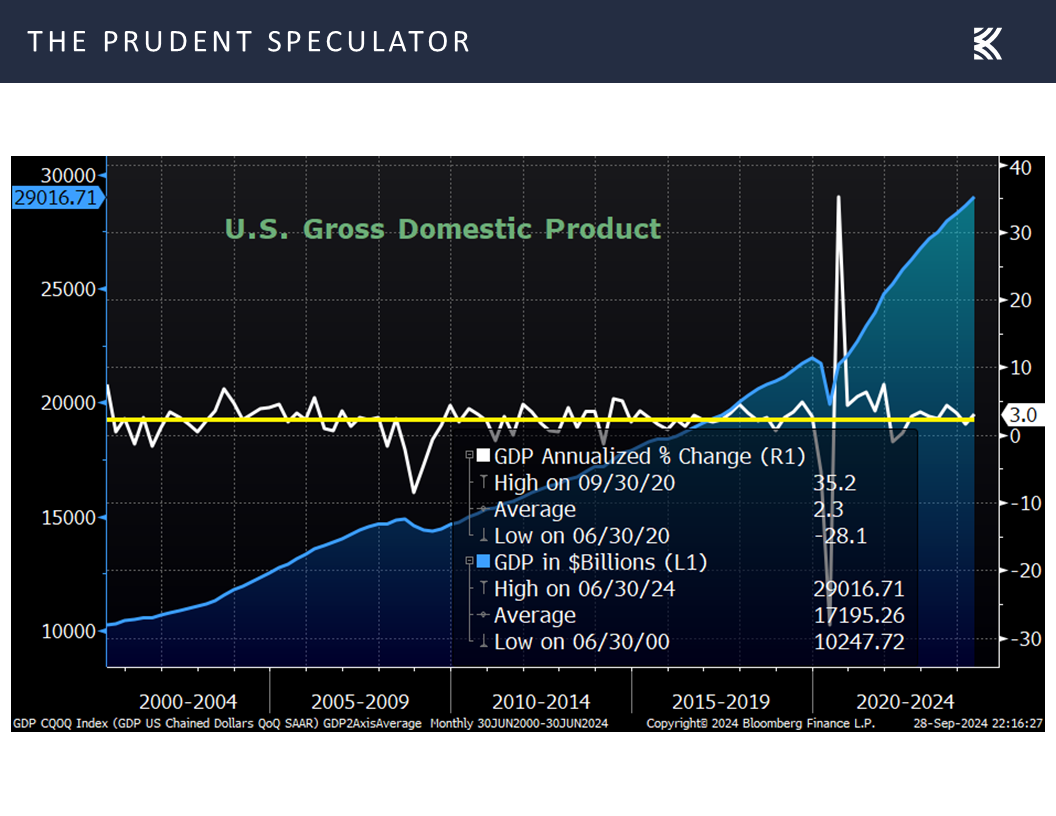

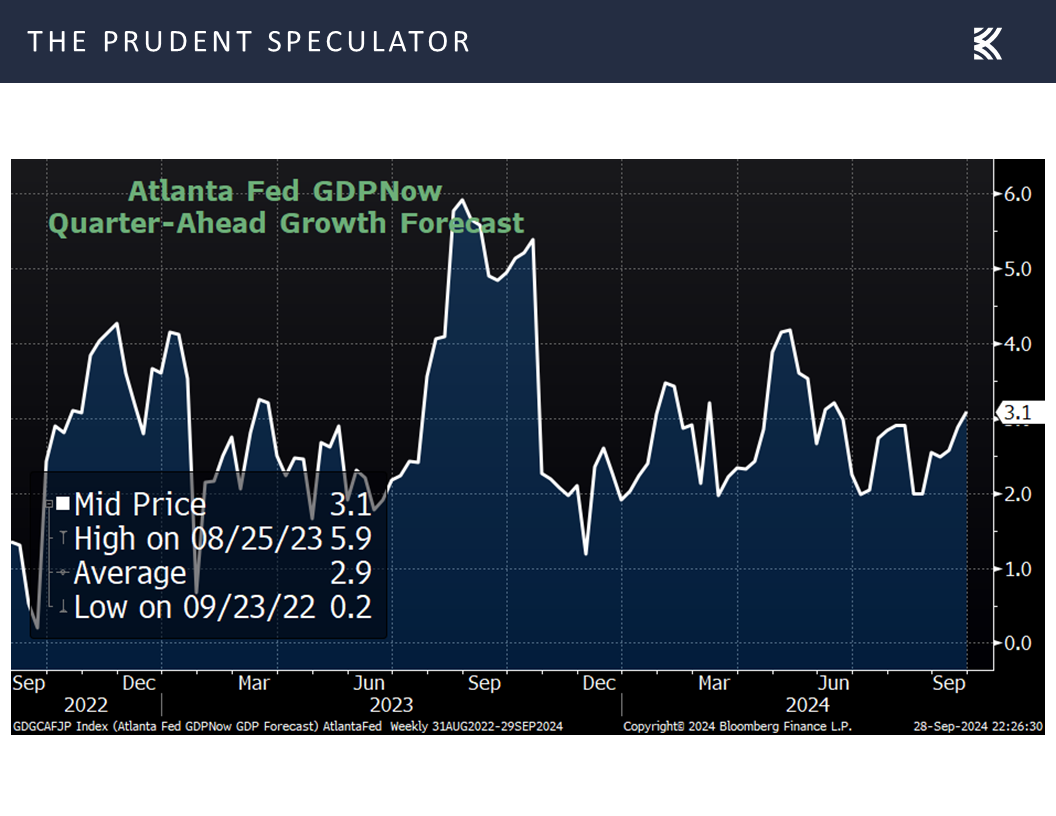

Growth – Corporate Profits and GDP Have Risen Over Time

Econ Stats – Mostly Better-than-Expected Numbers

PCE – Inflation Continues to Trend in the Right Direction

Rates & Stocks – Equities Have Performed Well, on Average, Whether Fed Funds or 10-Year Yield is Rising/Falling

GDP Outlook – Solid Global Economic Growth Expected by the OECD

Sentiment – AAII Bullishness is High

Geopolitics – Equities Have Persevered in the Fullness of Time through All Previous Middle East Hostilities

Valuations – Liking our Metrics

Stock News – Updates on MU, JBL, AMGN, GM & TSN

Week in Review – Rally Off Early-September Lows Continues

Stocks tacked on modest gains last week, albeit with plenty of ups and downs,

Volatility – Ups and Downs Normal but Long-Term Trend is Higher

continuing the rebound from the early-September lows, that prompted The Wall Street Journal on September 9 to proclaim, “September Slump Looking Likely.” The publication added, “In addition to the uncertainty over the Fed’s plans, markets are expected to remain volatile heading into the November election. October is typically the weakest month for stocks during election years, with the S&P 500 down 1.4% on an average going back to 1980.”

Certainly, equites could have headed further south, as the September-October time span historically is the worst of the year,

but with one day to go in the first of those two scary months, we have again been reminded that the secret to success in stocks is not to get scared out of them.

To be sure, volatility will always be part of the investment equation, with 5% setbacks happening three times a year on average, 10% corrections taking place every 11 months or so on average and even 20% Bear Markets occurring every 3 years on average. On the other hand, gains of even greater magnitude have come with similar frequency and long-term returns have been terrific for those who share our belief that time in the market trumps market timing.

Growth – Corporate Profits and GDP Have Risen Over Time

The reason stocks have performed well over time is that corporate profits (which are measured in actual dollars) have grown over time,

as the U.S. economy has expanded, with even periods of arguably lackluster real (inflation-adjusted) GDP growth pushing nominal (actual) growth higher.

Of course, lackluster would not seem to be the correct word for what we have been seeing lately as real Q2 GDP was revised upward to 3.0%, while the latest projection from the Atlanta Fed for real Q3 GDP growth inched up to 3.1% last week.

Econ Stats – Mostly Better-than-Expected Numbers

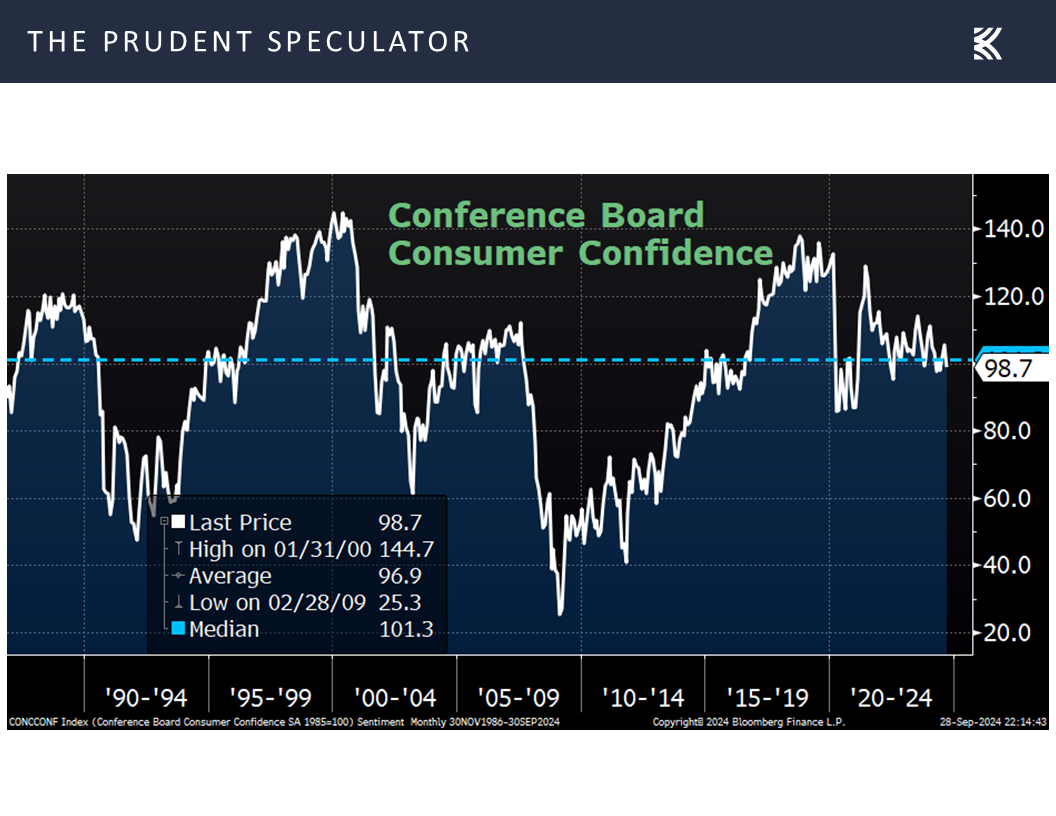

This was the case as the latest read on Consumer Confidence for September from the Conference Board coming in at 98.7, well below expectations of 104.0,

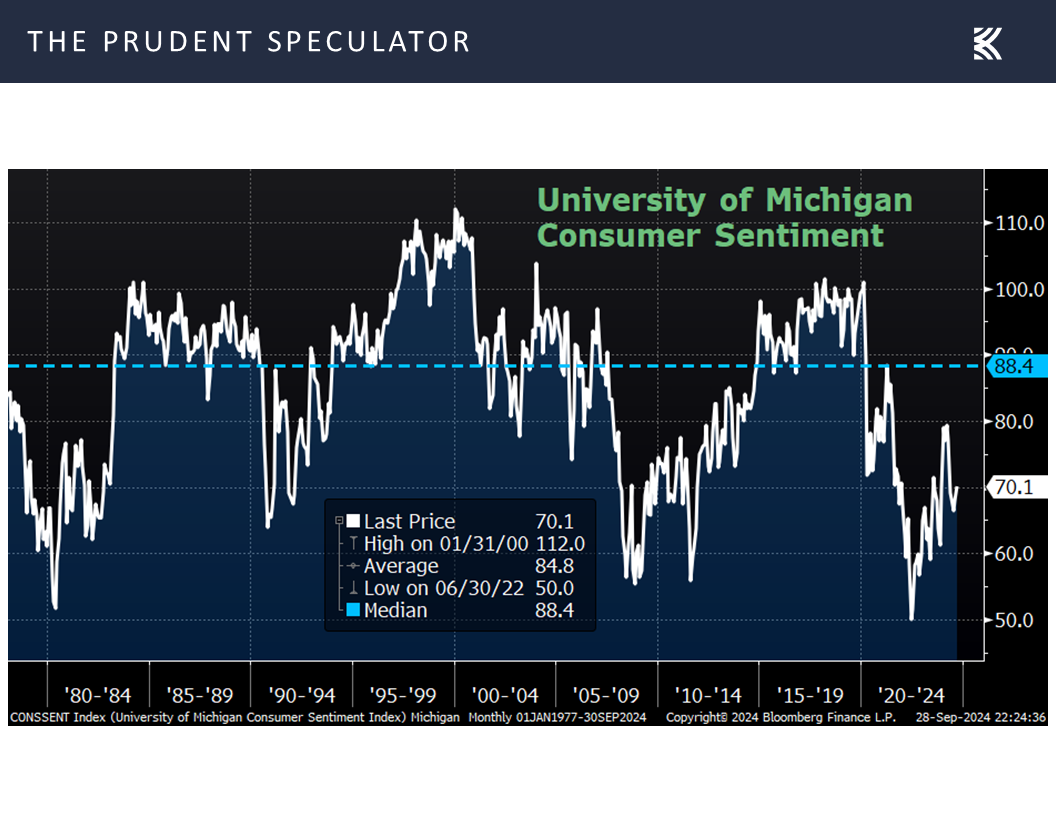

was offset by the University of Michigan’s Sentiment gauge climbing to 70.1 this month, above estimates of 69.4,

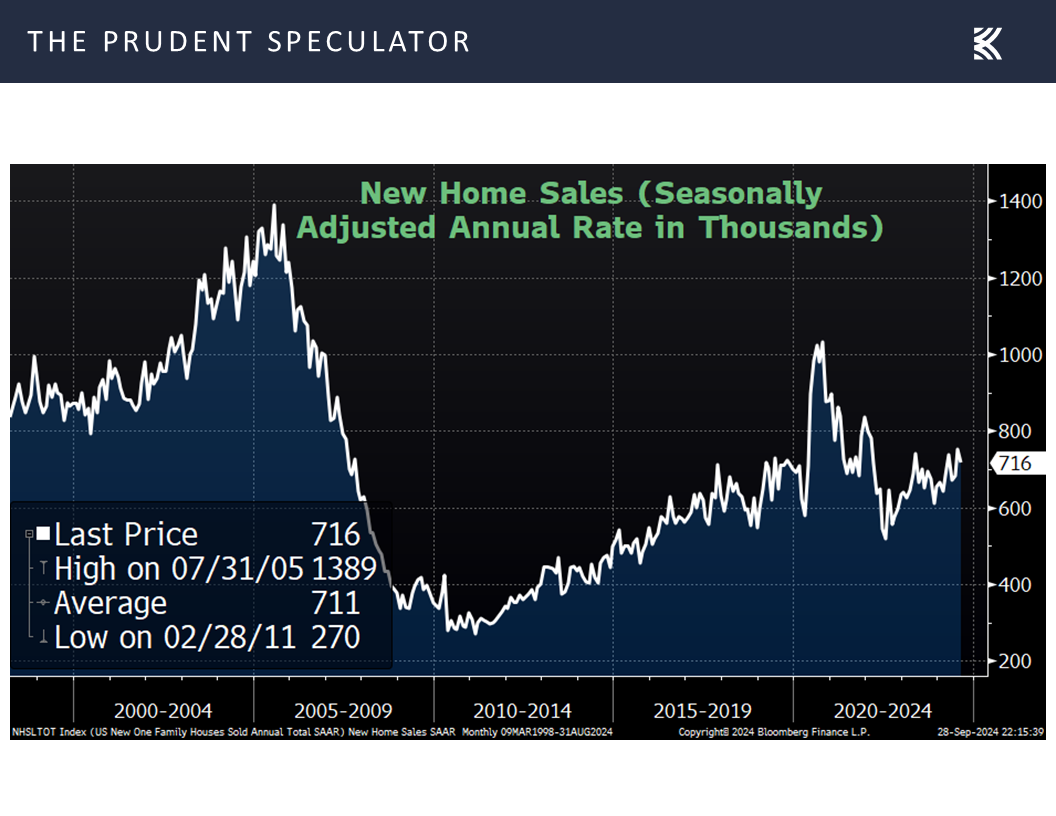

new home sales for August of 716,000 topping expectations of 700,000,

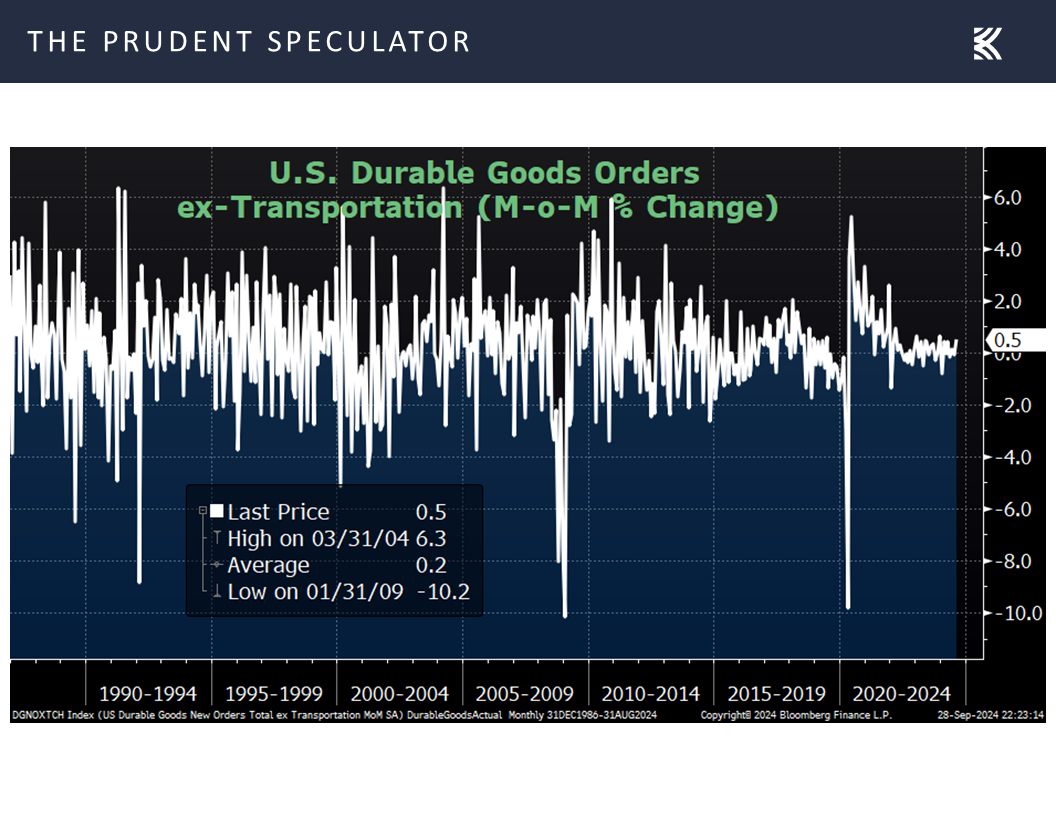

durable goods orders, excluding the volatile transportation sector, advancing 0.5%, versus the consensus analyst estimate of a 0.1% increase,

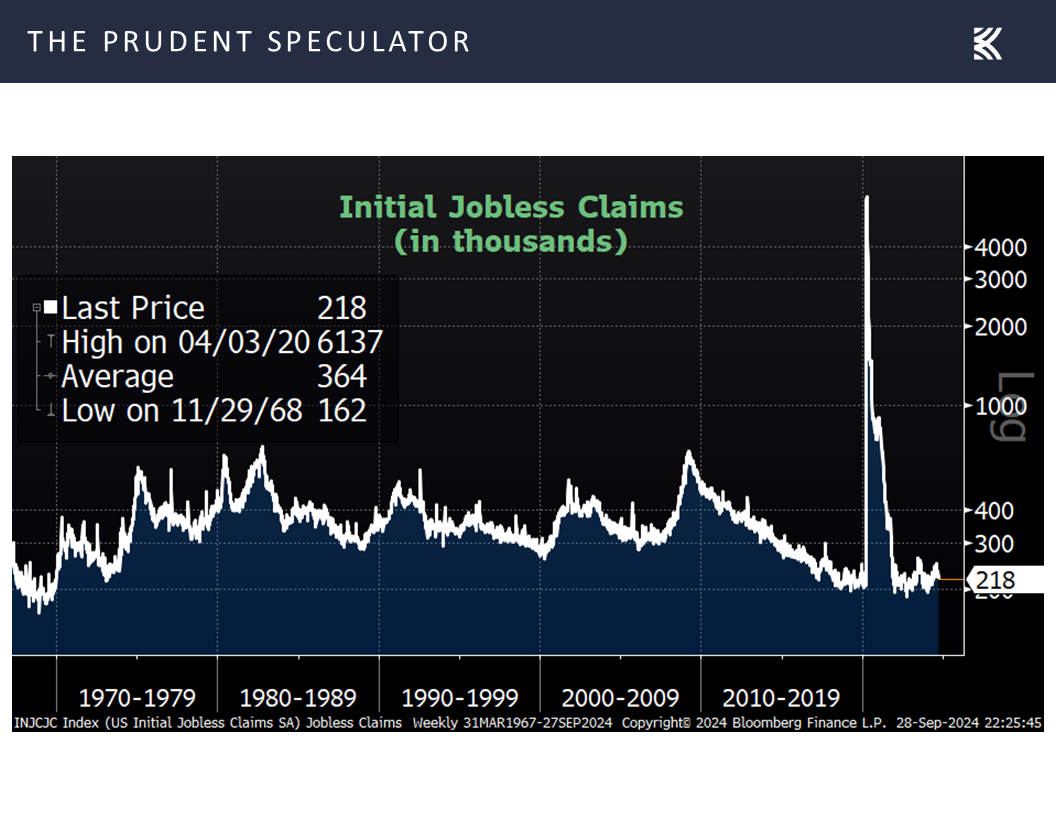

and first-time filings for unemployment benefits in the latest week dropping to 218,000, down from a revised 222,000 the week prior.

PCE – Inflation Continues to Trend in the Right Direction

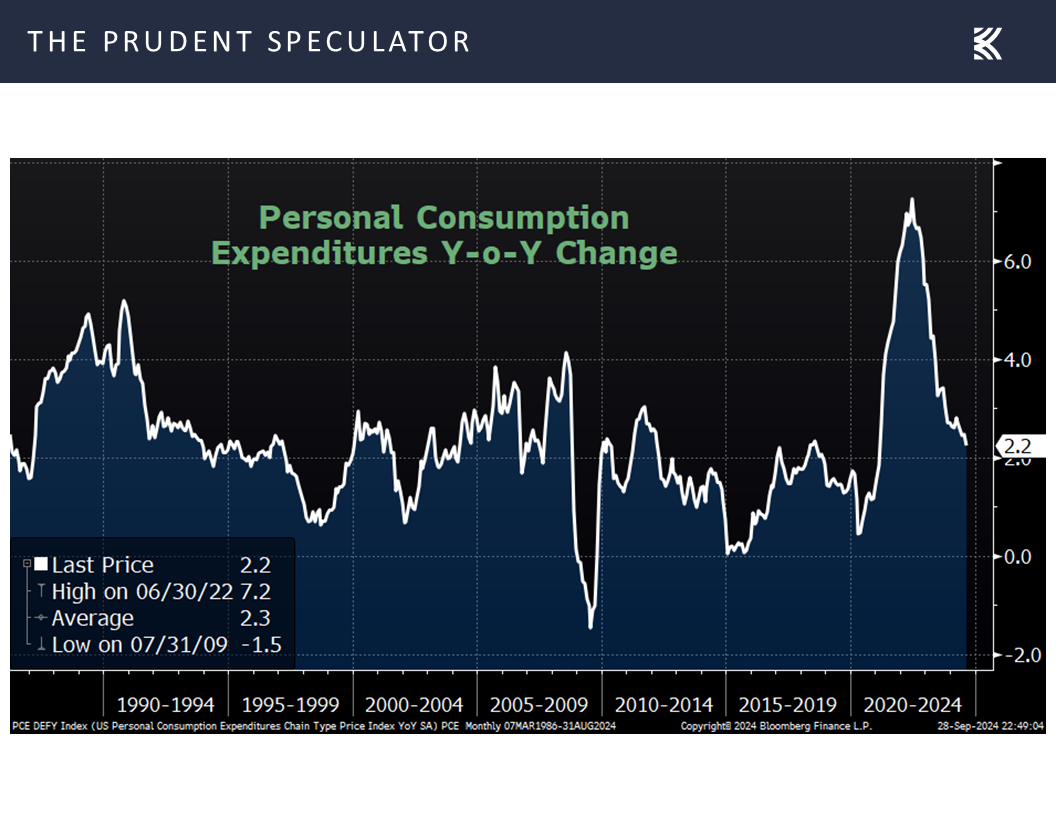

Perhaps even more important last week, the Federal Reserve’s preferred measure of inflation, the Personal Consumption Expenditures index (PCE), rose 2.2% in August, less than the 2.3% projection.

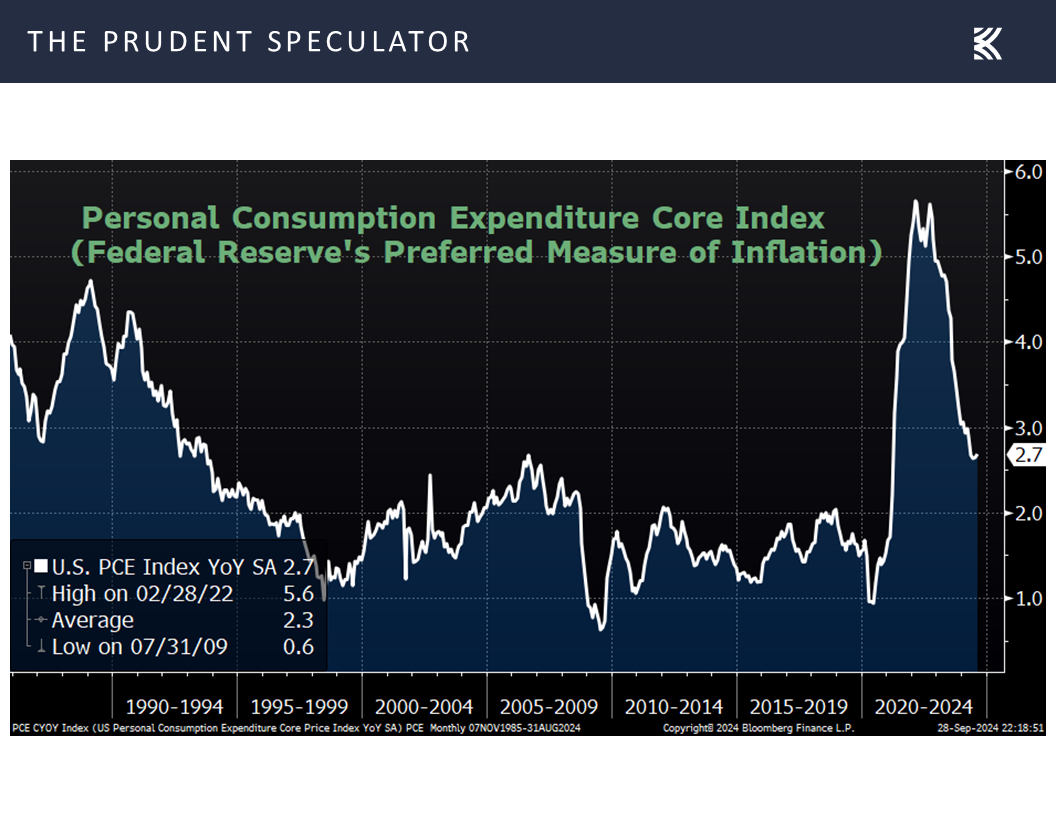

True, the core PCE, which excludes volatile food and energy prices, rose a higher-than-expected 2.7% last month,

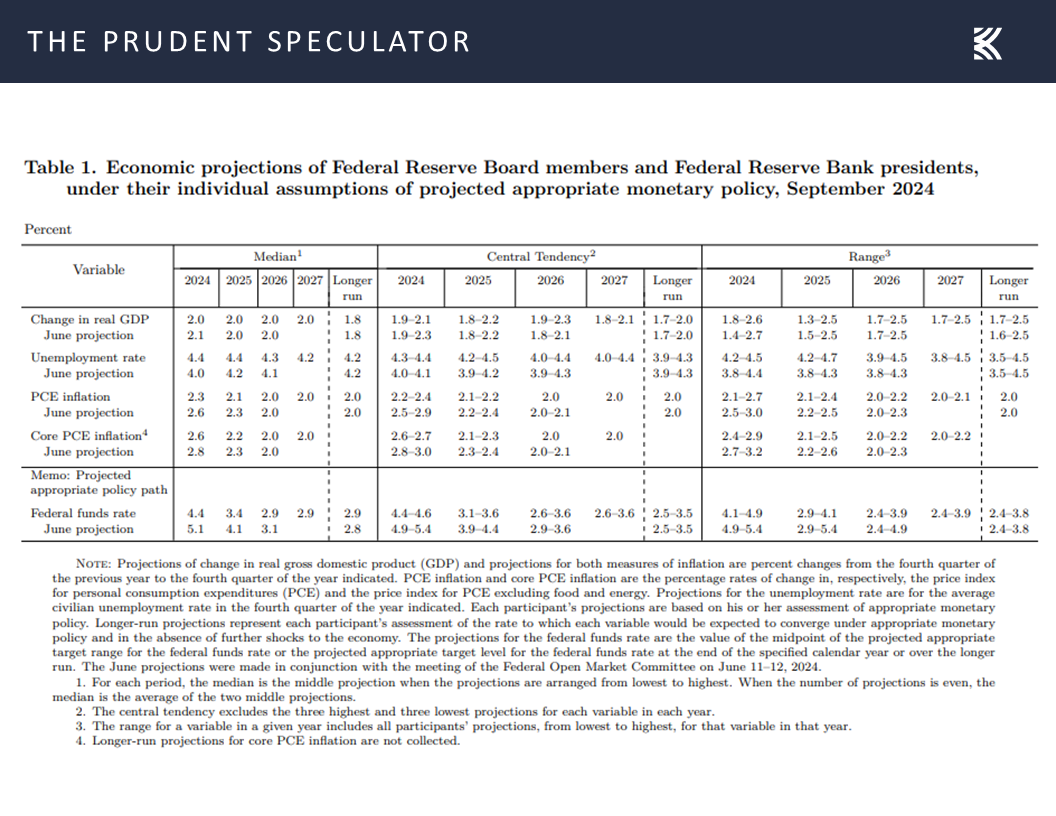

but inflation readings would seem to support the economic projections offered a couple of weeks back by the Federal Reserve,

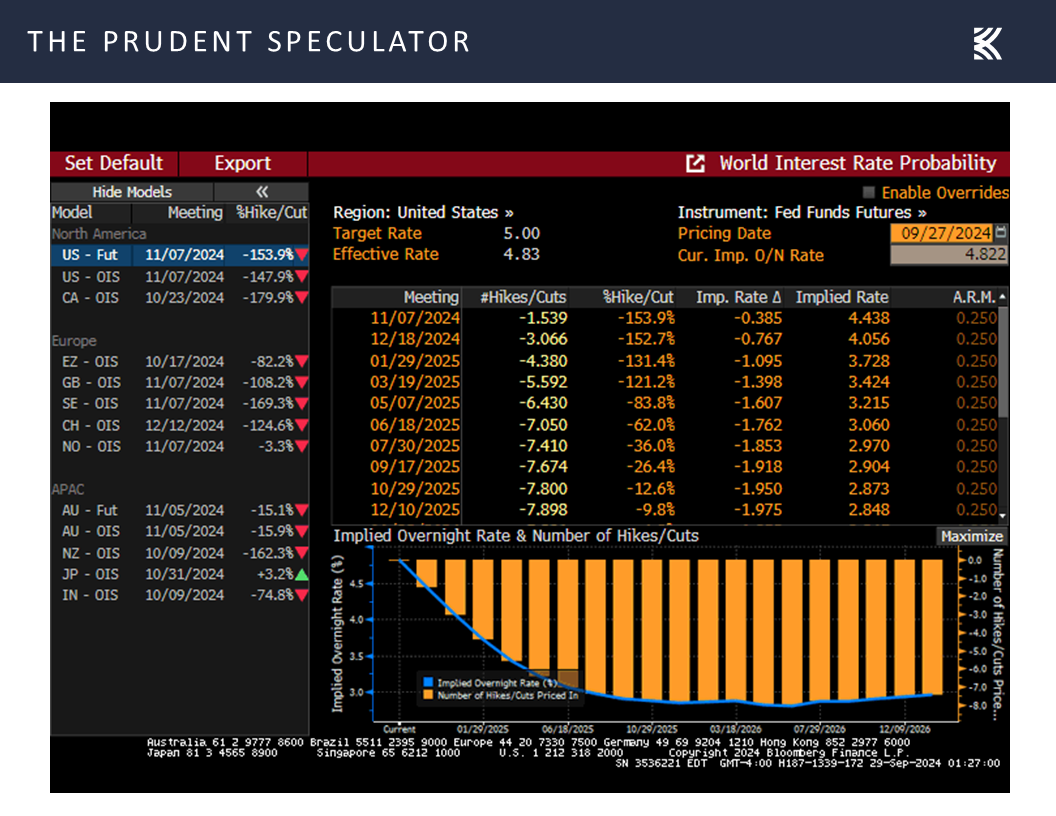

which led futures market bettors last week to drive down the targets for the Fed Funds rate to 4.06% for the end of this year and to 2.85% for the end of 2025.

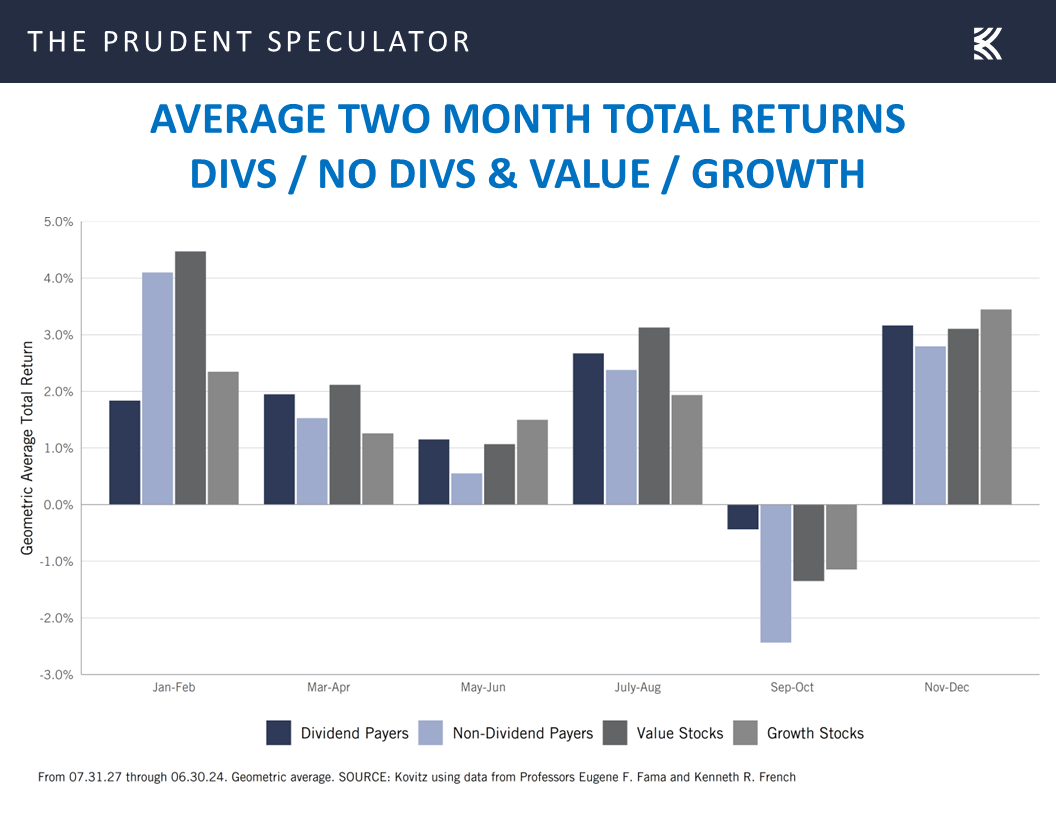

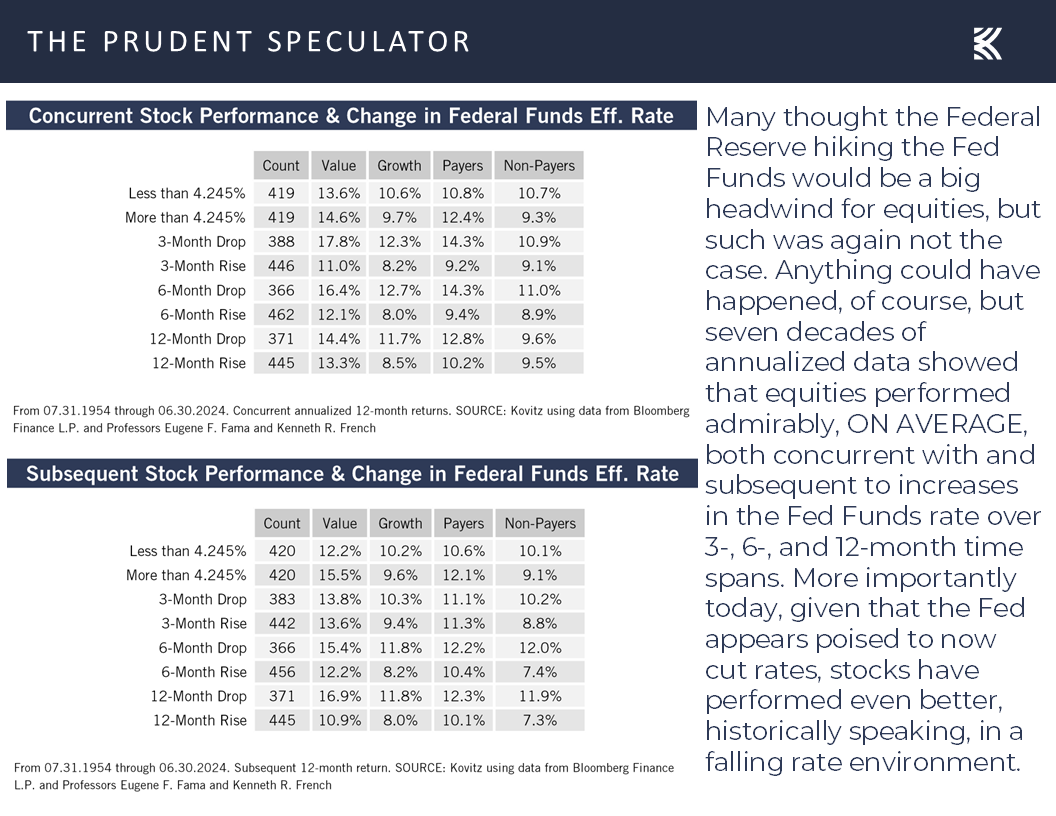

Rates & Stocks – Equities Have Performed Well, on Average, Whether Fed Funds or 10-Year Yield is Rising/Falling

While stocks perform fine whether the U.S. central bank is tightening or easing monetary policy, we note that Value stocks and Dividend Payers, like those we have long favored, have done even better when the Fed is cutting interest rates,

while stock prices become more attractive, all else equal, when yields on competing investments are lower,

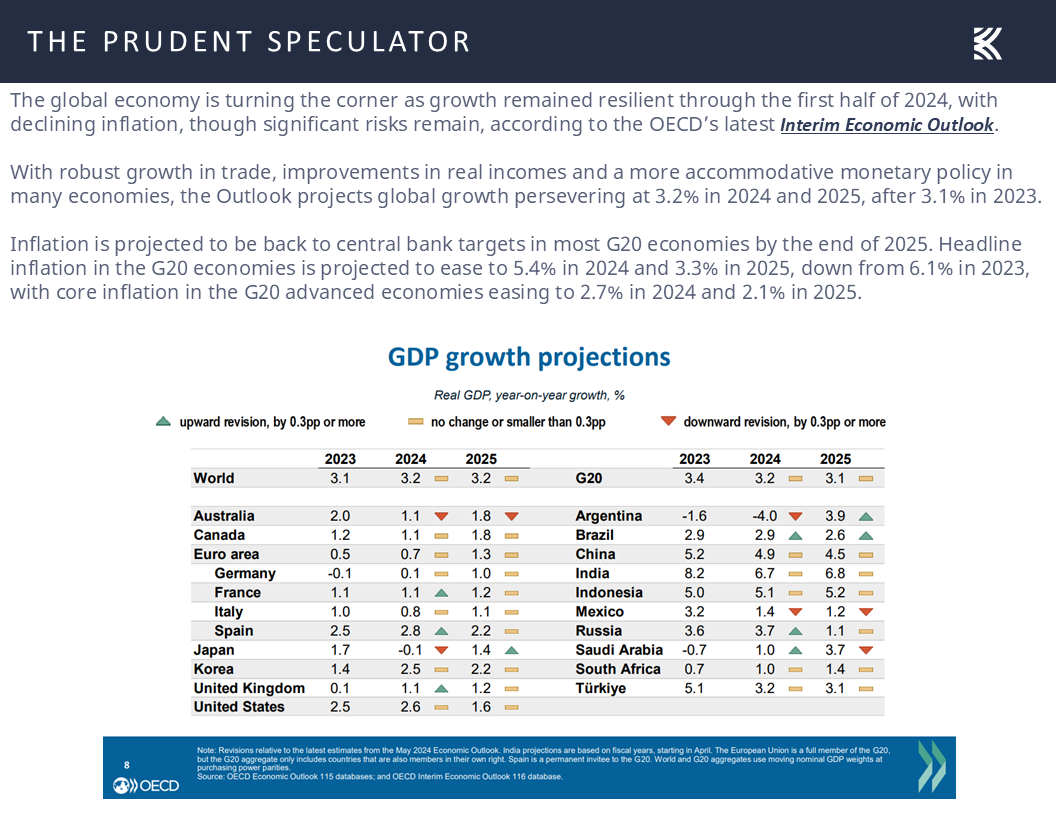

GDP Outlook – Solid Global Economic Growth Expected by the OECD

especially as the outlook for global and U.S. GDP released last week from the Organisation for Economic Co-operation and Development (OECD) remained solid (real growth of 3.2% this year and next year for the world and 2.6% and 1.6%, respectively, for the U.S.).

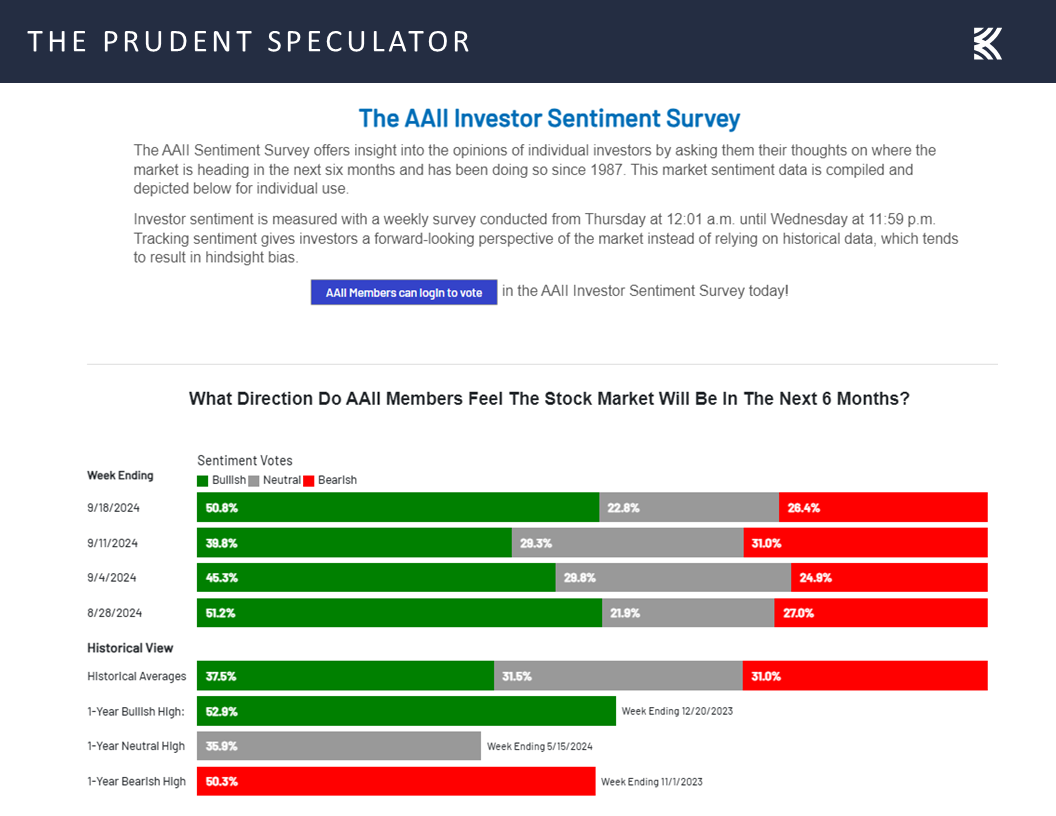

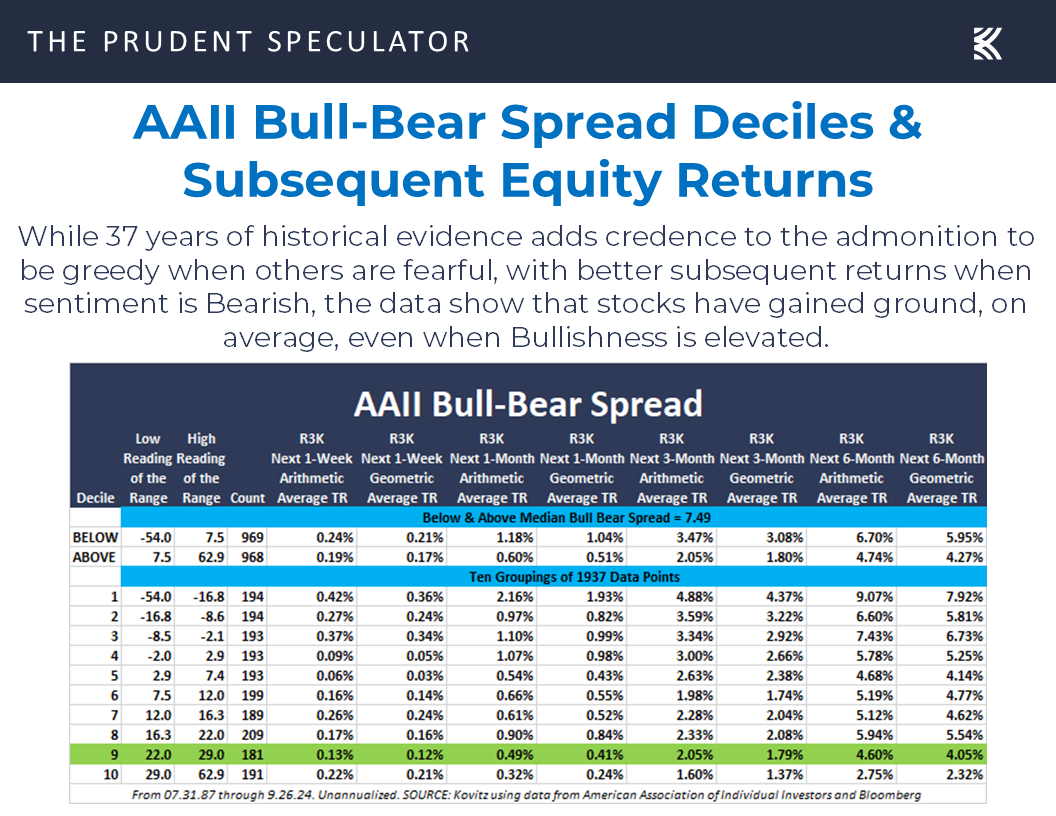

Sentiment – AAII Bullishness is High

We realize that folks on Main Street are quite Bullish these days,

which would suggest potentially lower (but still positive) returns for equities in the near term,

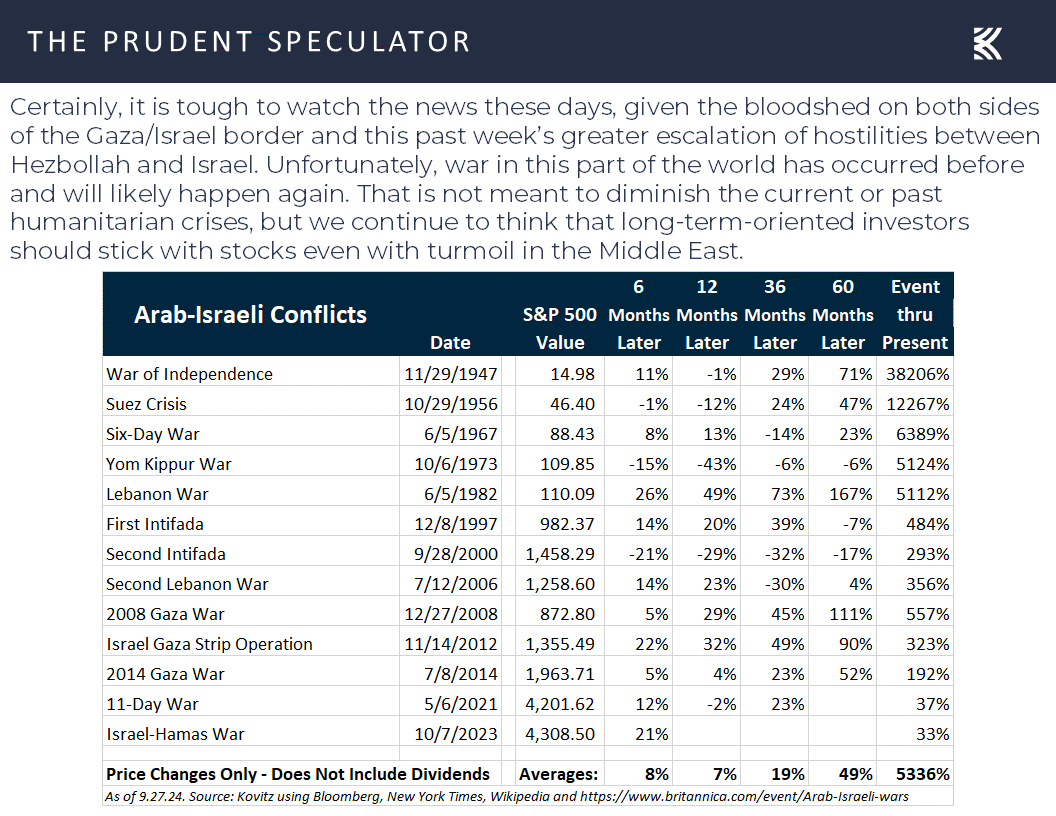

Geopolitics – Equities Have Persevered in the Fullness of Time through All Previous Middle East Hostilities

and tensions in the Middle East have continued to rise, so we remain braced for downside volatility,

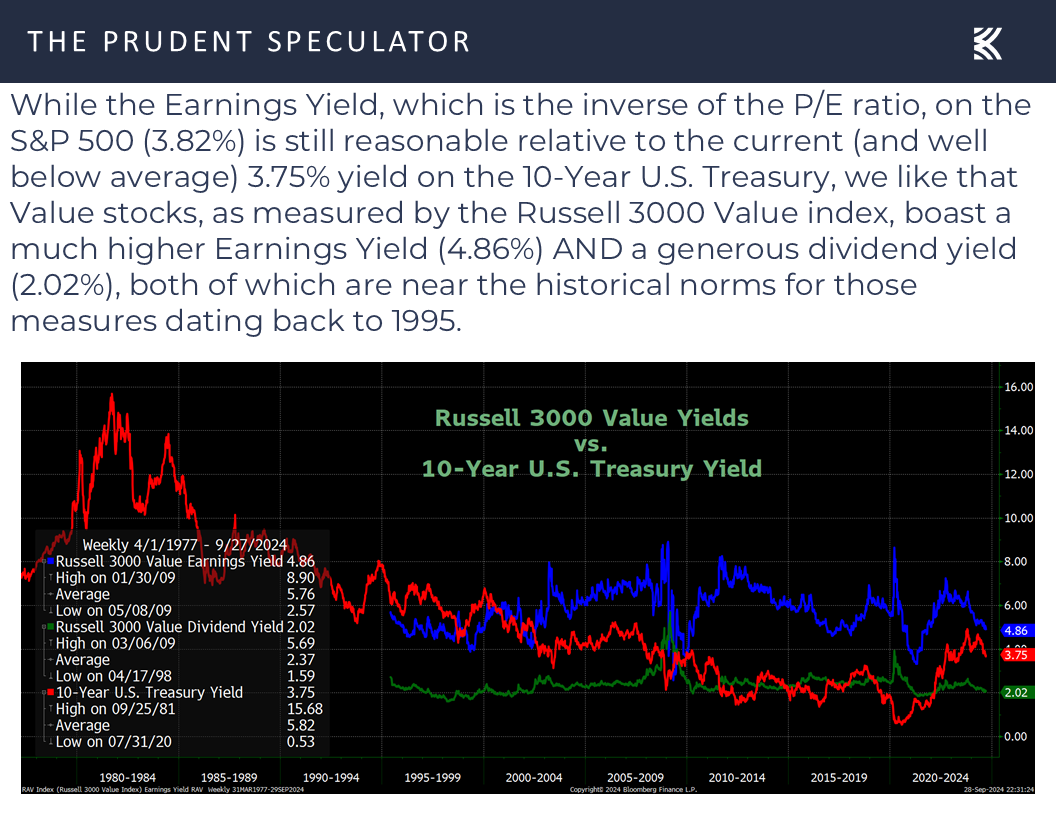

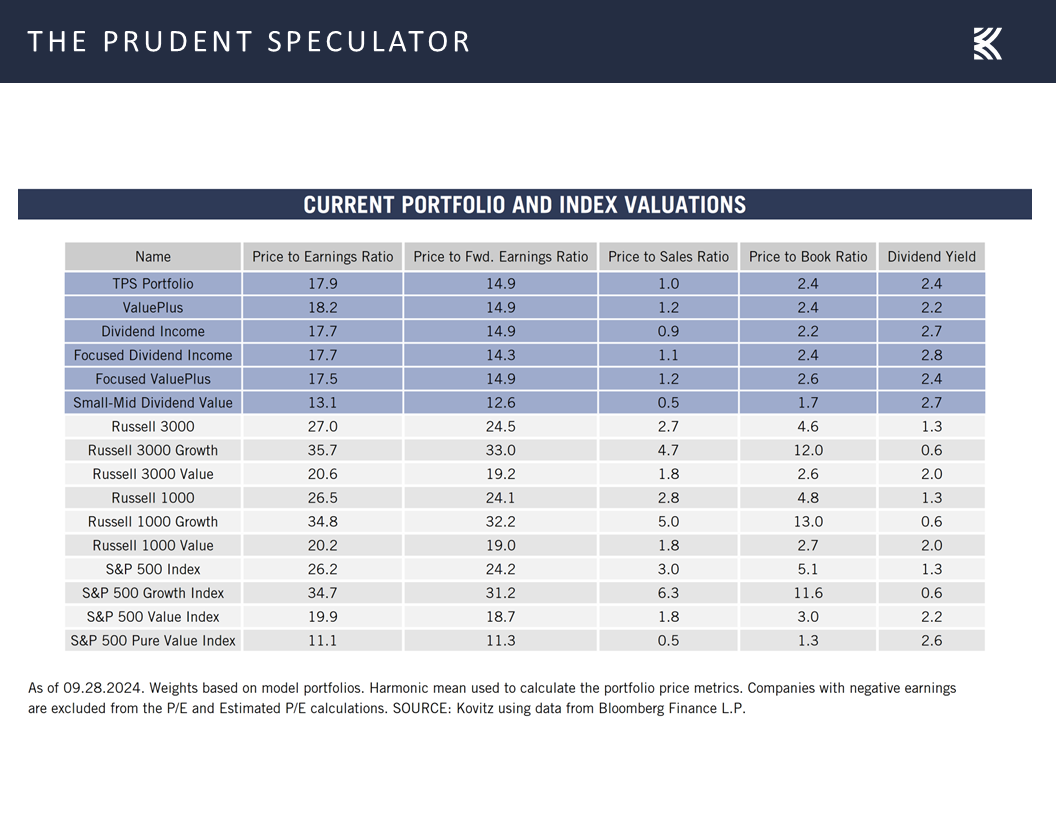

Valuations – Liking our Metrics

but we see no reason to alter our optimism for the long-term prospects of our broadly diversified portfolios of what we believe to be undervalued stocks.

Stock News – Updates on six stocks across four different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Volatility, GDP Outlook, Geopolitics, Interest Rates and more

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Volatility, GDP Outlook, Geopolitics, Interest Rates and more. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Newsletter Portfolio Trades – Exited DHLGY

Week in Review – Rally Off Early-September Lows Continues

Volatility – Ups and Downs Normal but Long-Term Trend is Higher

Growth – Corporate Profits and GDP Have Risen Over Time

Econ Stats – Mostly Better-than-Expected Numbers

PCE – Inflation Continues to Trend in the Right Direction

Rates & Stocks – Equities Have Performed Well, on Average, Whether Fed Funds or 10-Year Yield is Rising/Falling

GDP Outlook – Solid Global Economic Growth Expected by the OECD

Sentiment – AAII Bullishness is High

Geopolitics – Equities Have Persevered in the Fullness of Time through All Previous Middle East Hostilities

Valuations – Liking our Metrics

Stock News – Updates on MU, JBL, AMGN, GM & TSN

Week in Review – Rally Off Early-September Lows Continues

Stocks tacked on modest gains last week, albeit with plenty of ups and downs,

Volatility – Ups and Downs Normal but Long-Term Trend is Higher

continuing the rebound from the early-September lows, that prompted The Wall Street Journal on September 9 to proclaim, “September Slump Looking Likely.” The publication added, “In addition to the uncertainty over the Fed’s plans, markets are expected to remain volatile heading into the November election. October is typically the weakest month for stocks during election years, with the S&P 500 down 1.4% on an average going back to 1980.”

Certainly, equites could have headed further south, as the September-October time span historically is the worst of the year,

but with one day to go in the first of those two scary months, we have again been reminded that the secret to success in stocks is not to get scared out of them.

To be sure, volatility will always be part of the investment equation, with 5% setbacks happening three times a year on average, 10% corrections taking place every 11 months or so on average and even 20% Bear Markets occurring every 3 years on average. On the other hand, gains of even greater magnitude have come with similar frequency and long-term returns have been terrific for those who share our belief that time in the market trumps market timing.

Growth – Corporate Profits and GDP Have Risen Over Time

The reason stocks have performed well over time is that corporate profits (which are measured in actual dollars) have grown over time,

as the U.S. economy has expanded, with even periods of arguably lackluster real (inflation-adjusted) GDP growth pushing nominal (actual) growth higher.

Of course, lackluster would not seem to be the correct word for what we have been seeing lately as real Q2 GDP was revised upward to 3.0%, while the latest projection from the Atlanta Fed for real Q3 GDP growth inched up to 3.1% last week.

Econ Stats – Mostly Better-than-Expected Numbers

This was the case as the latest read on Consumer Confidence for September from the Conference Board coming in at 98.7, well below expectations of 104.0,

was offset by the University of Michigan’s Sentiment gauge climbing to 70.1 this month, above estimates of 69.4,

new home sales for August of 716,000 topping expectations of 700,000,

durable goods orders, excluding the volatile transportation sector, advancing 0.5%, versus the consensus analyst estimate of a 0.1% increase,

and first-time filings for unemployment benefits in the latest week dropping to 218,000, down from a revised 222,000 the week prior.

PCE – Inflation Continues to Trend in the Right Direction

Perhaps even more important last week, the Federal Reserve’s preferred measure of inflation, the Personal Consumption Expenditures index (PCE), rose 2.2% in August, less than the 2.3% projection.

True, the core PCE, which excludes volatile food and energy prices, rose a higher-than-expected 2.7% last month,

but inflation readings would seem to support the economic projections offered a couple of weeks back by the Federal Reserve,

which led futures market bettors last week to drive down the targets for the Fed Funds rate to 4.06% for the end of this year and to 2.85% for the end of 2025.

Rates & Stocks – Equities Have Performed Well, on Average, Whether Fed Funds or 10-Year Yield is Rising/Falling

While stocks perform fine whether the U.S. central bank is tightening or easing monetary policy, we note that Value stocks and Dividend Payers, like those we have long favored, have done even better when the Fed is cutting interest rates,

while stock prices become more attractive, all else equal, when yields on competing investments are lower,

GDP Outlook – Solid Global Economic Growth Expected by the OECD

especially as the outlook for global and U.S. GDP released last week from the Organisation for Economic Co-operation and Development (OECD) remained solid (real growth of 3.2% this year and next year for the world and 2.6% and 1.6%, respectively, for the U.S.).

Sentiment – AAII Bullishness is High

We realize that folks on Main Street are quite Bullish these days,

which would suggest potentially lower (but still positive) returns for equities in the near term,

Geopolitics – Equities Have Persevered in the Fullness of Time through All Previous Middle East Hostilities

and tensions in the Middle East have continued to rise, so we remain braced for downside volatility,

Valuations – Liking our Metrics

but we see no reason to alter our optimism for the long-term prospects of our broadly diversified portfolios of what we believe to be undervalued stocks.

Stock News – Updates on six stocks across four different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.