The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Volatility, Inflation, Equity Returns and Tariffs. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – One Sell in 4 Accounts

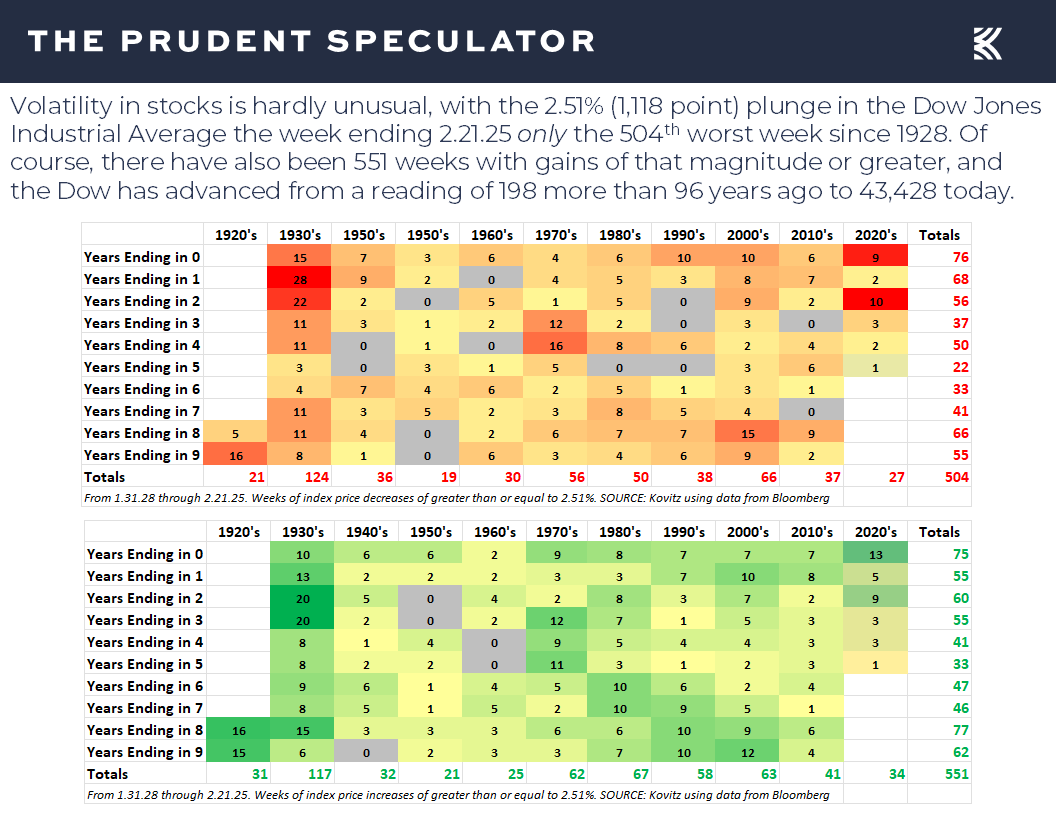

Perspective – 504th Worst Weekly Loss for the Dow

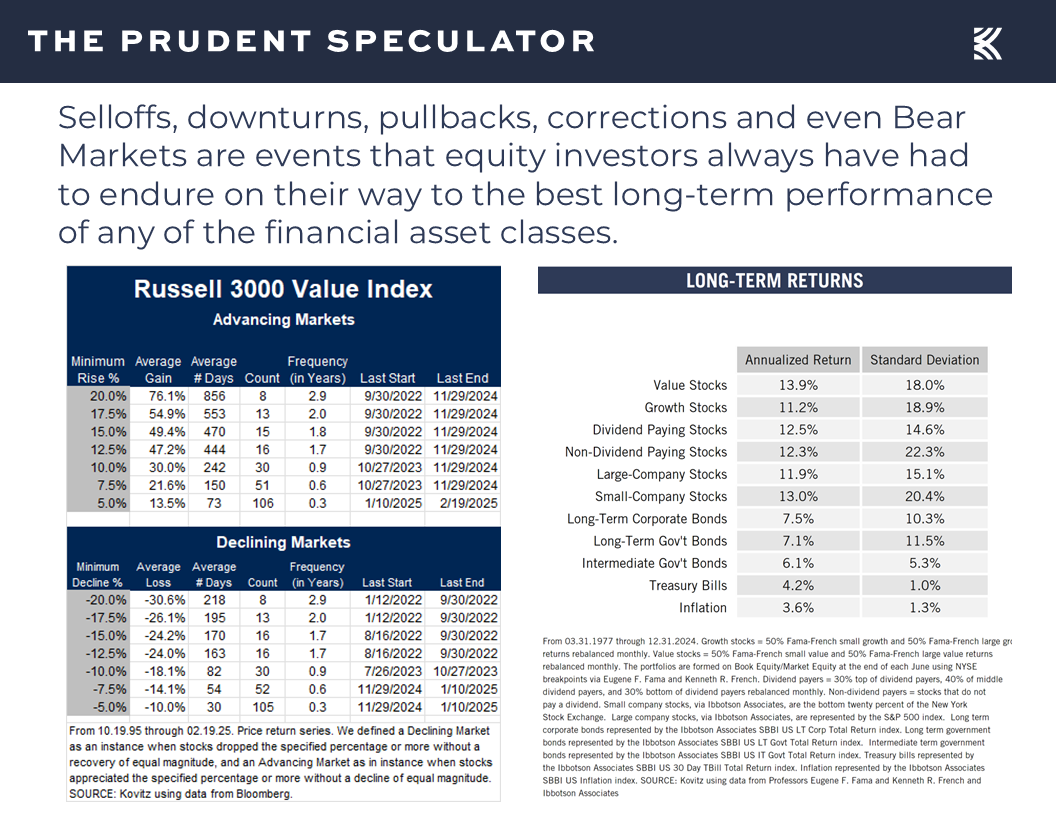

Volatility – Stocks Go Up and Down in the Short Term, But Have Provided Handsome Rewards in the Long-Term

Econ Data – Mixed Numbers but Solid GDP and EPS Growth Projected for 2025

Valuations – Value Stocks Remain Reasonably Priced

Historical Evidence – On Average, Stocks Have Performed Fine Whether Inflation/Fed Funds/Interest Rates are Rising/Falling

Sentiment – Contrarian AAII Buy Signal

Stock News – Updates on MDT, DVN, CE, NTR, DINO, HAS, WMT, NEM, PHG & WKC

Perspective – 504th Worst Weekly Loss for the Dow

While the trading week started well, it was a very ugly finish, so much so that the widely followed Dow Jones Industrial Average skidded more than 1,100 points over the full four trading days. Believe it or not, the 2.51% percentage skid did not quite rank in the top 500 of the all-time worst weeks for the popular index,

Volatility – Stocks Go Up and Down in the Short Term, But Have Provided Handsome Rewards in the Long-Term

but it did offer another reminder that downside volatility has always been part of the long-term investment process, even as stocks have provided handsome overall long-term returns.

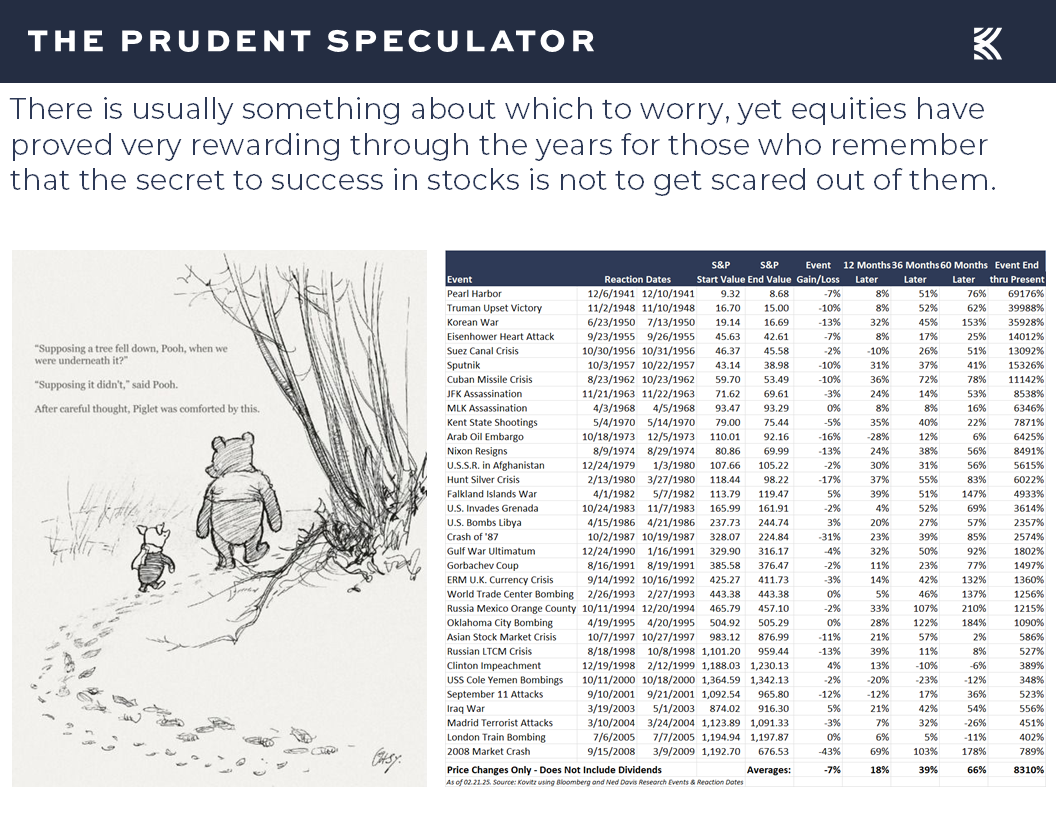

No doubt, there were concerning events last week, including more drama on the geopolitical stage, questions about the efforts of the Department of Government Efficiency and even news of a new bat coronavirus in China. Of course, there have always been fears to contend with for investors as the equity markets have long climbed a wall of worry, with near-term difficulties always overcome in the fullness of time.

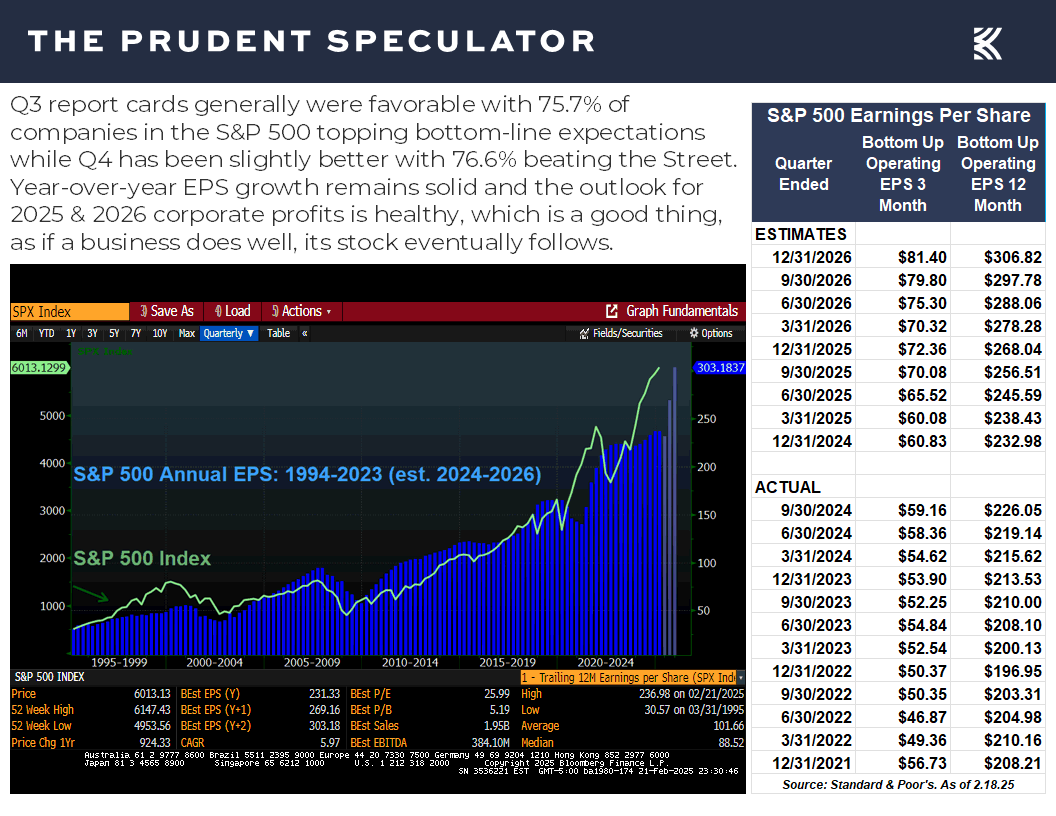

Econ Data – Mixed Numbers but Solid GDP and EPS Growth Projected for 2025

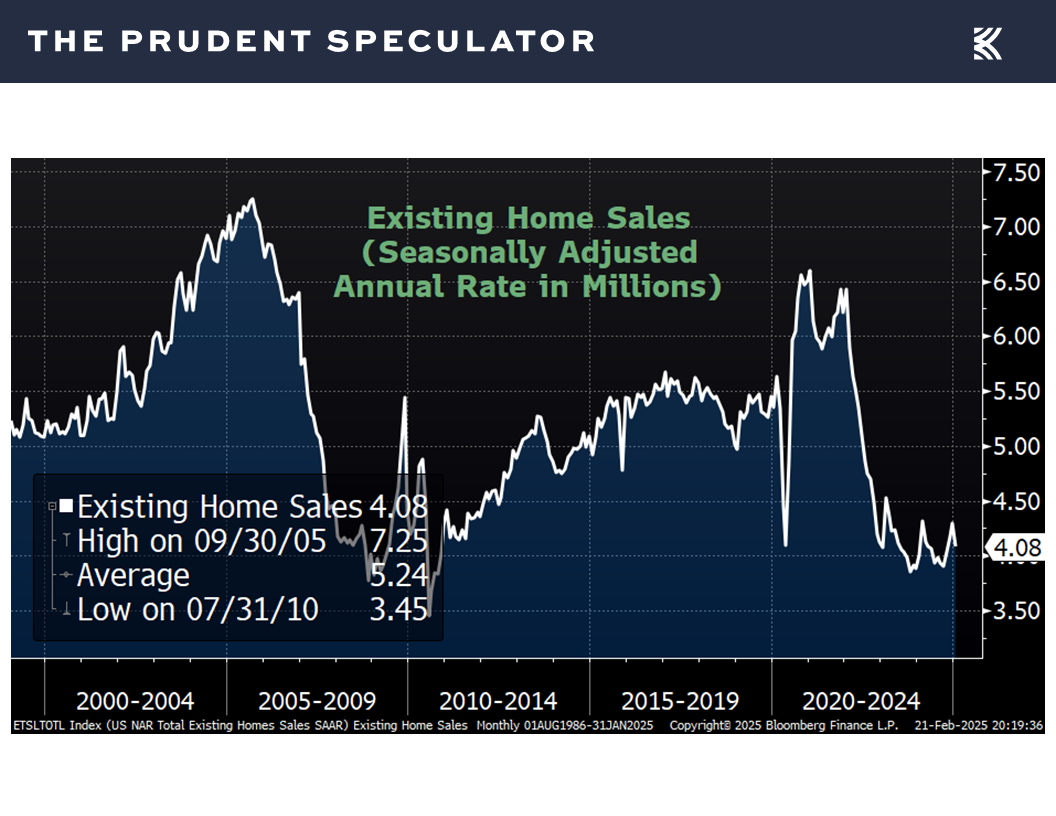

Certainly, questions about the health of the U.S. economy also played a large part in the selloff to end the week, as existing home sales for January dipped to an annual rate of 4.08 million, below expectations and down from a revised annual rate of 4.29 million in December,

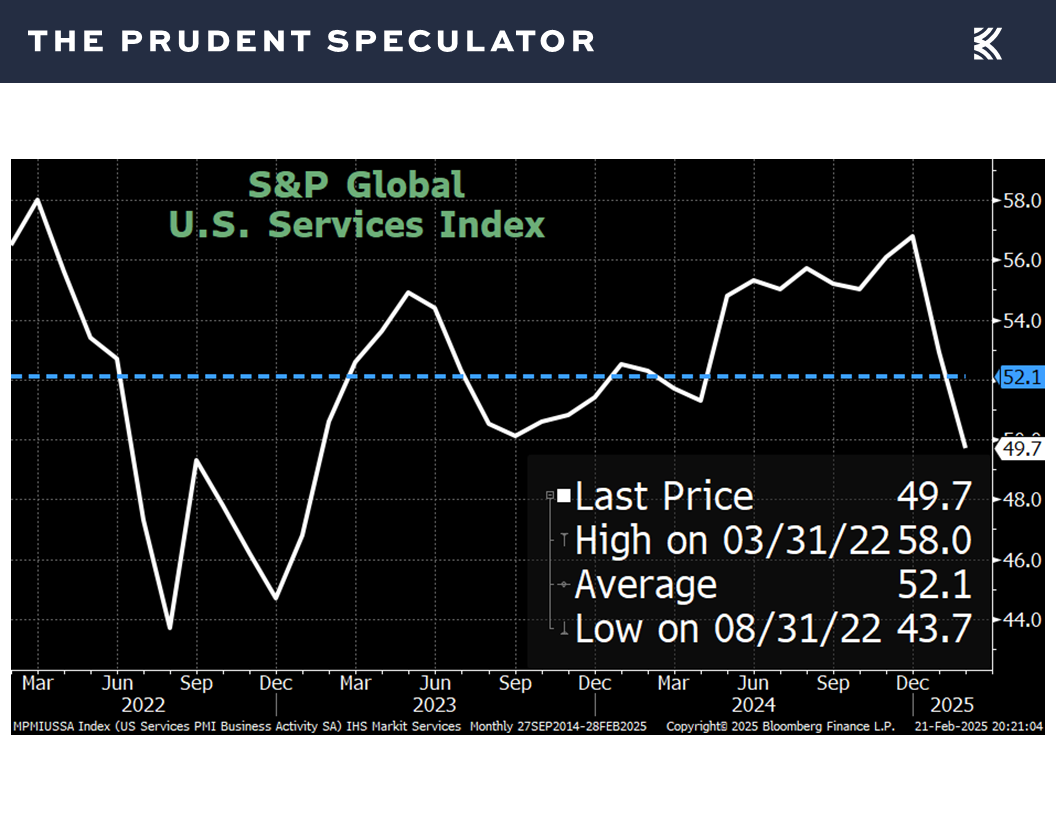

S&P Global’s preliminary measure of U.S. service sector activity for February fell to 49.7, well below forecasts of 53.0 and down considerably from a reading of 52.9 in January

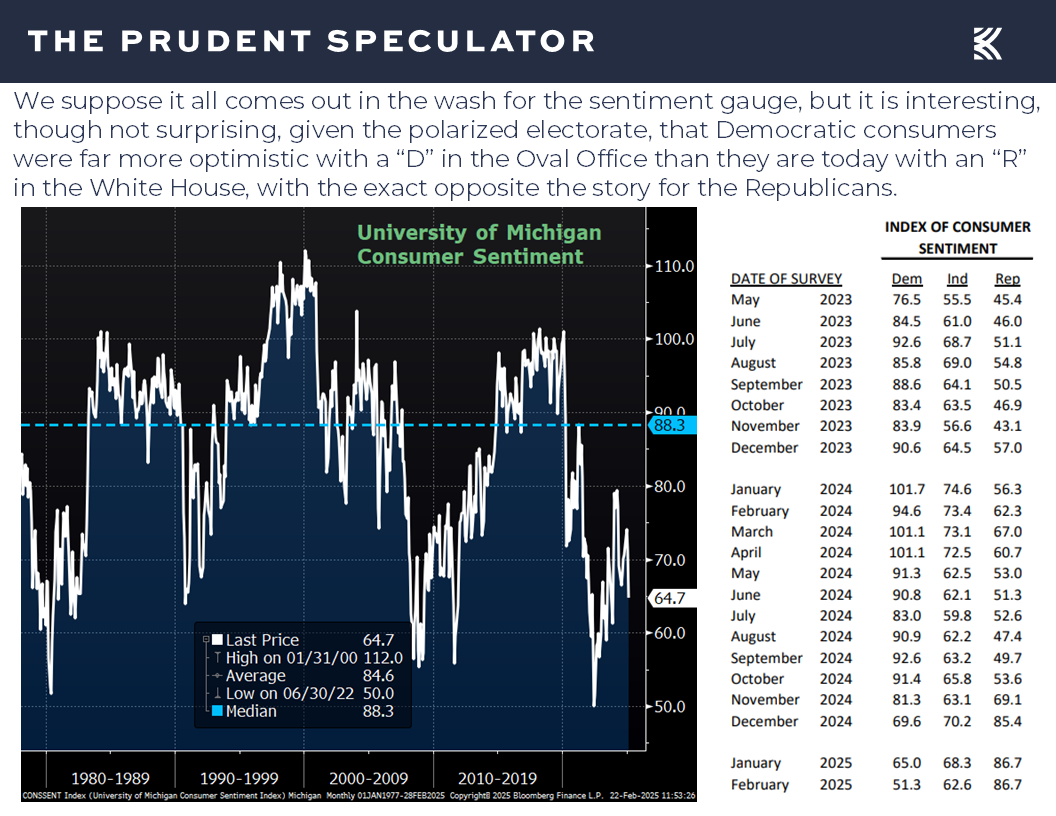

and the University of Michigan’s gauge of consumer sentiment for February sank to 64.7 versus estimates of 67.8, though the measure is heavily influenced by political biases.

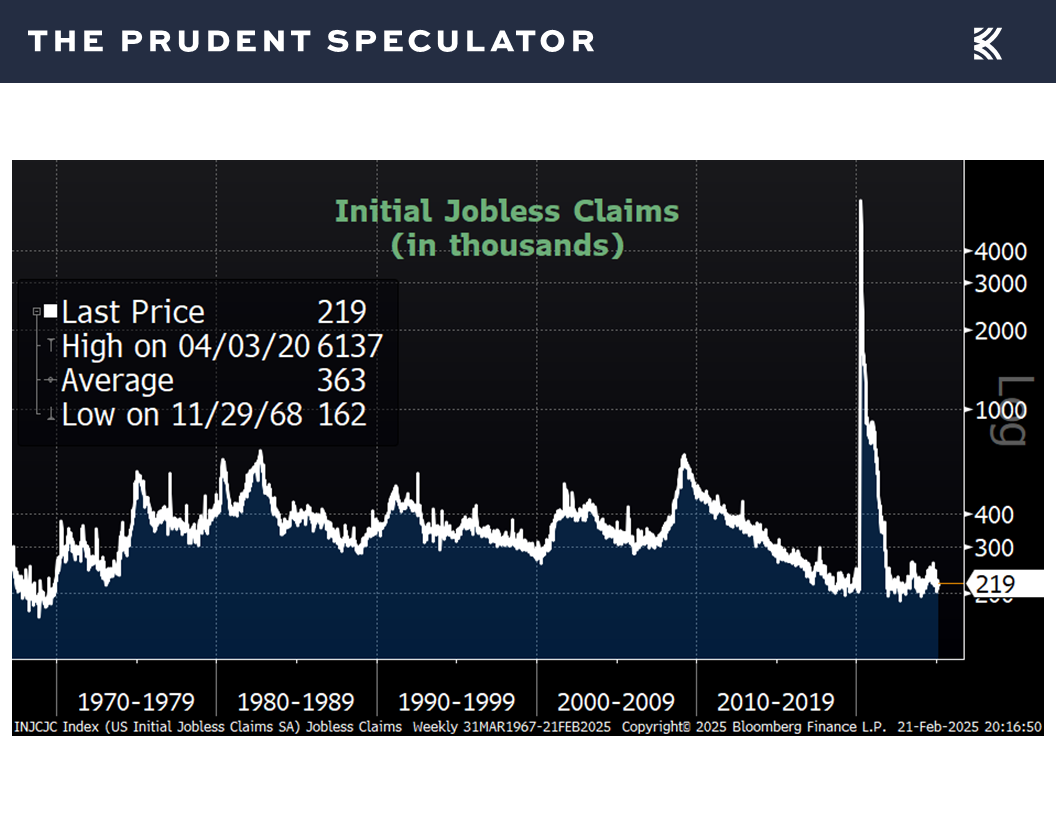

On the other hand, the labor market remained healthy, with first-time filings for unemployment benefits in the latest reported week remaining near multi-generational lows,

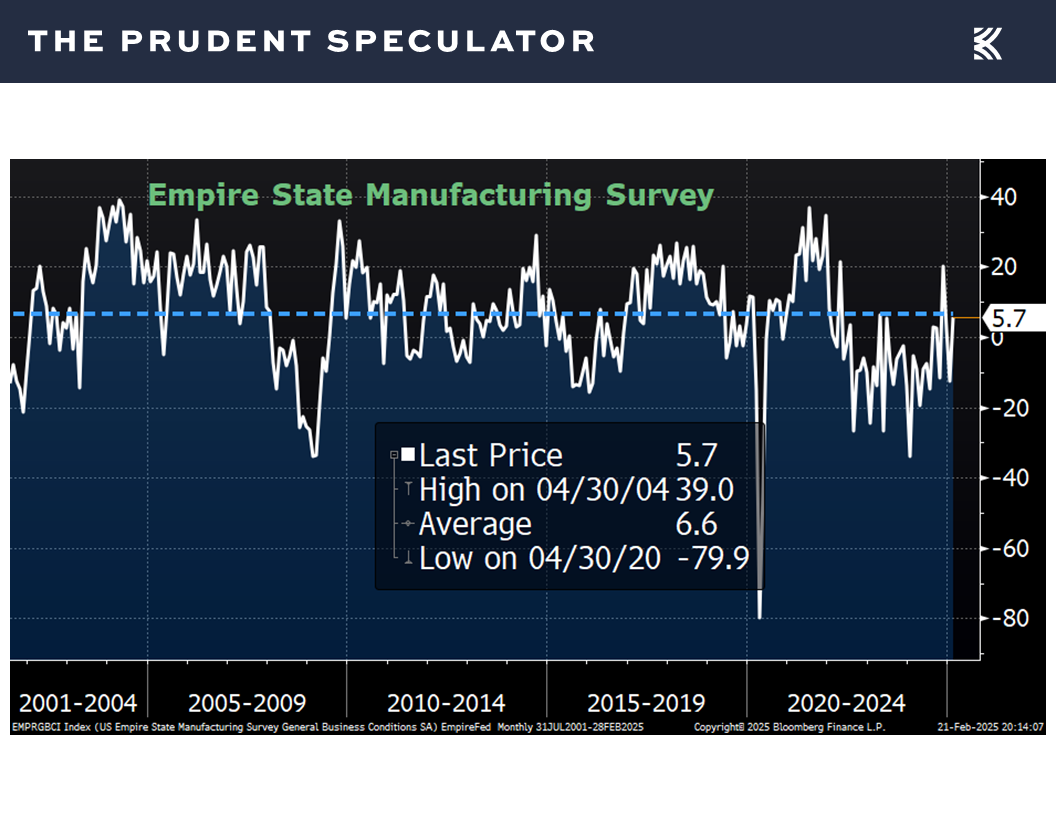

factory activity in the New York area,

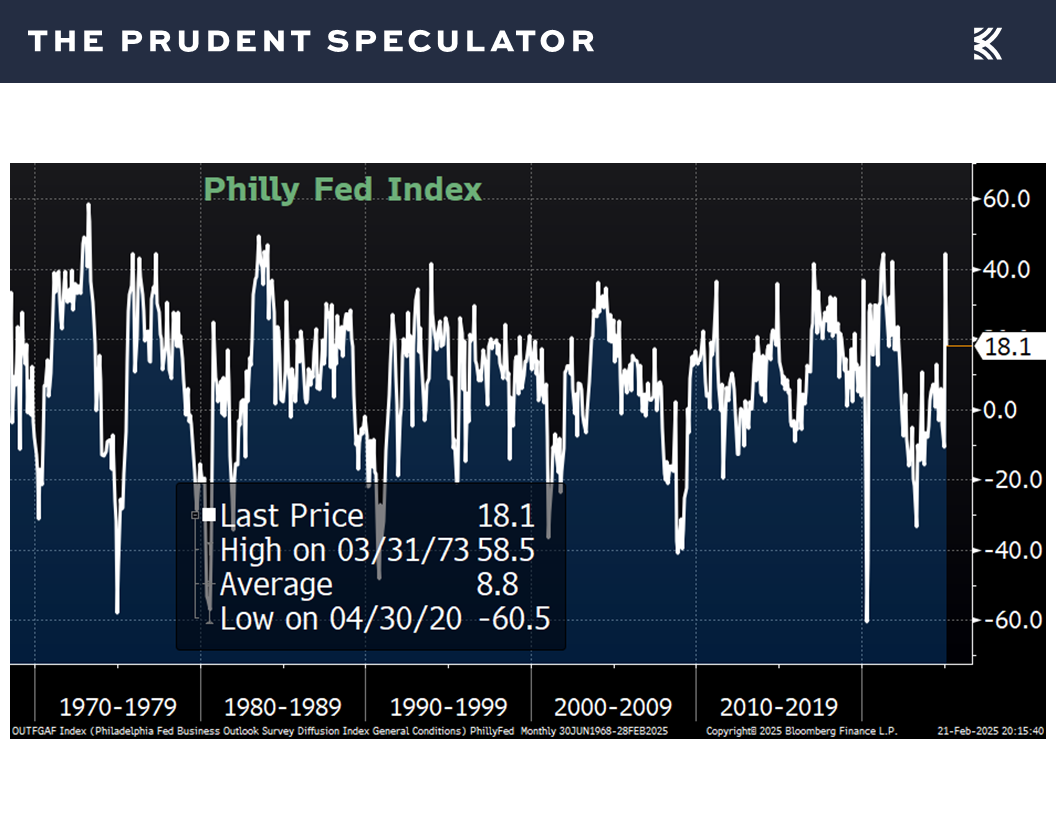

and the Philadelphia region this month both topped expectations,

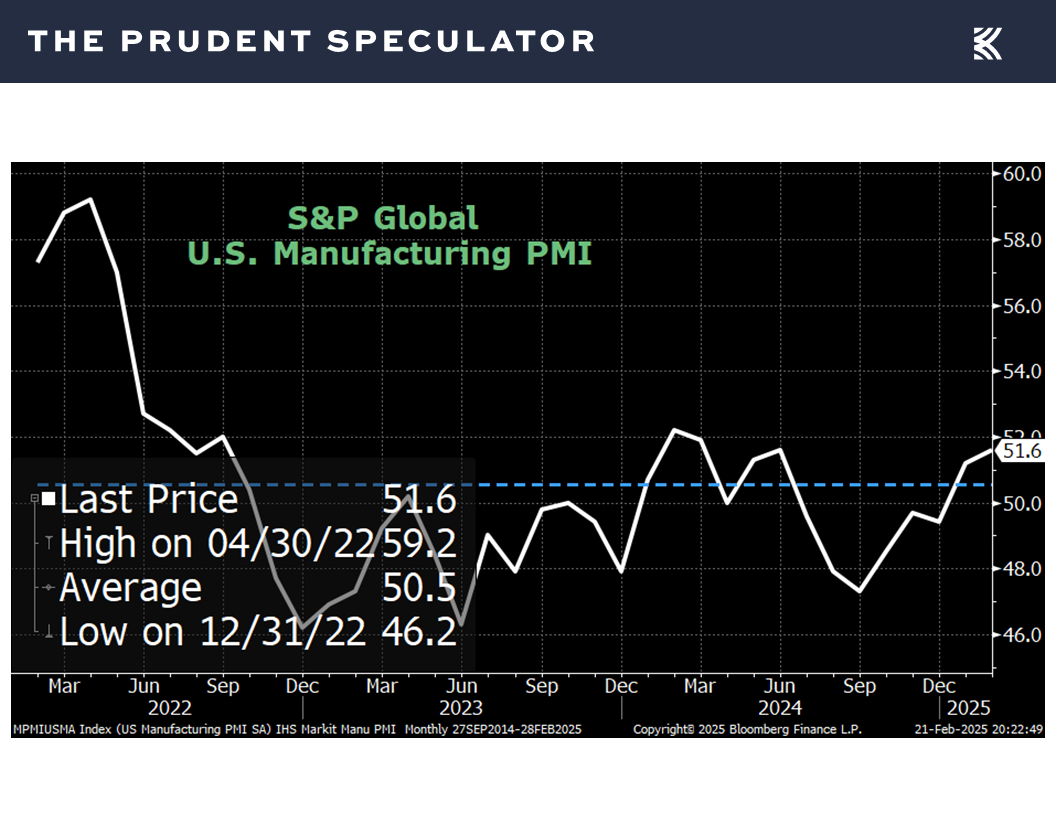

and S&P Global’s preliminary measure of U.S. manufacturing activity for February of 51.6 edged past estimates of 51.4 and inched up from January’s tally of 51.2.

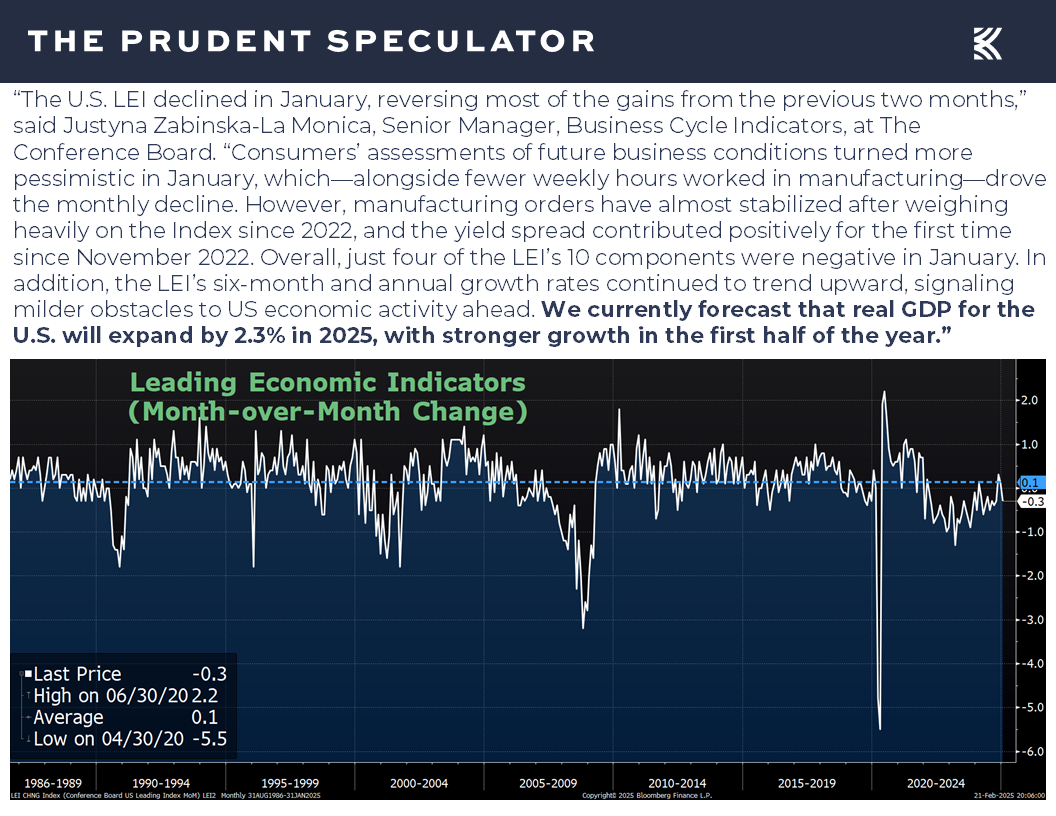

To be sure, the outlook for the U.S. economy is hardly clear as the forward-looking Leading Economic Index from the Conference Board fell a greater-than-projected 0.3% last month, yet the keeper of the index proclaimed, “We currently forecast that real GDP for the U.S. will expand by 2.3% in 2025, with stronger growth in the first half of the year.”

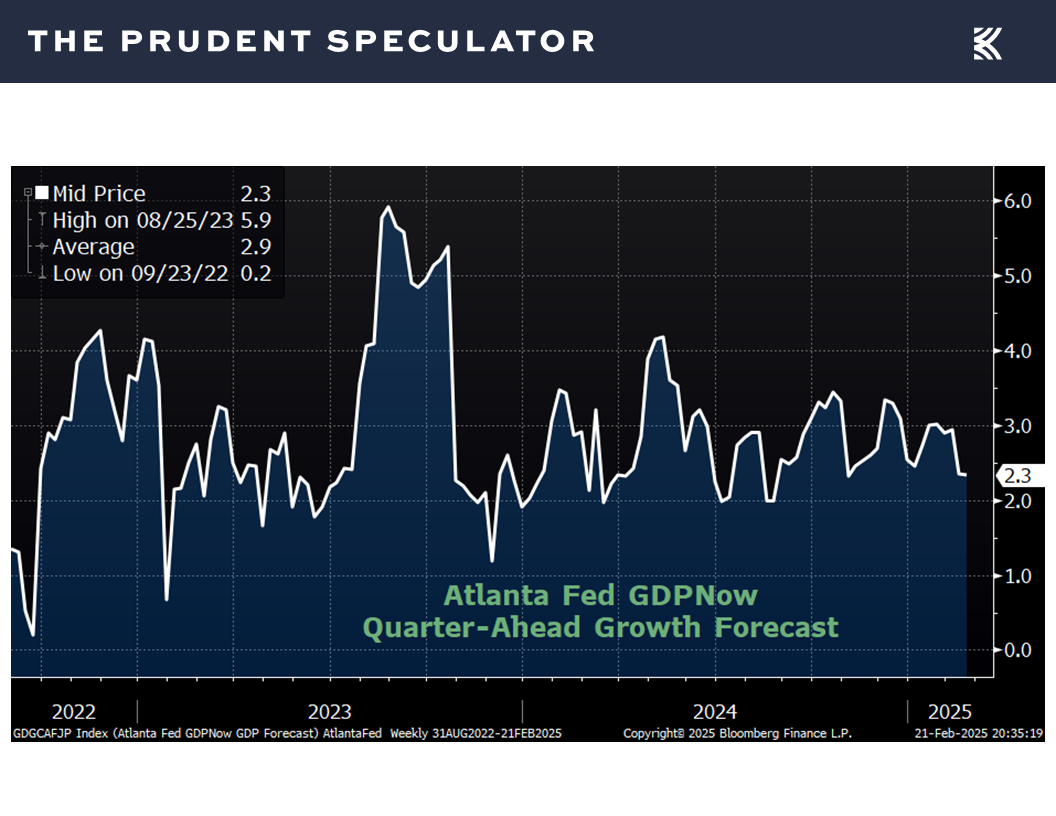

Interestingly, that GDP forecast for all of 2025 matches the latest estimate from the Atlanta Fed for Q1 real (inflation-adjusted) growth,

with expectations for a decent economy supporting estimates for favorable corporate profit growth this year and next,

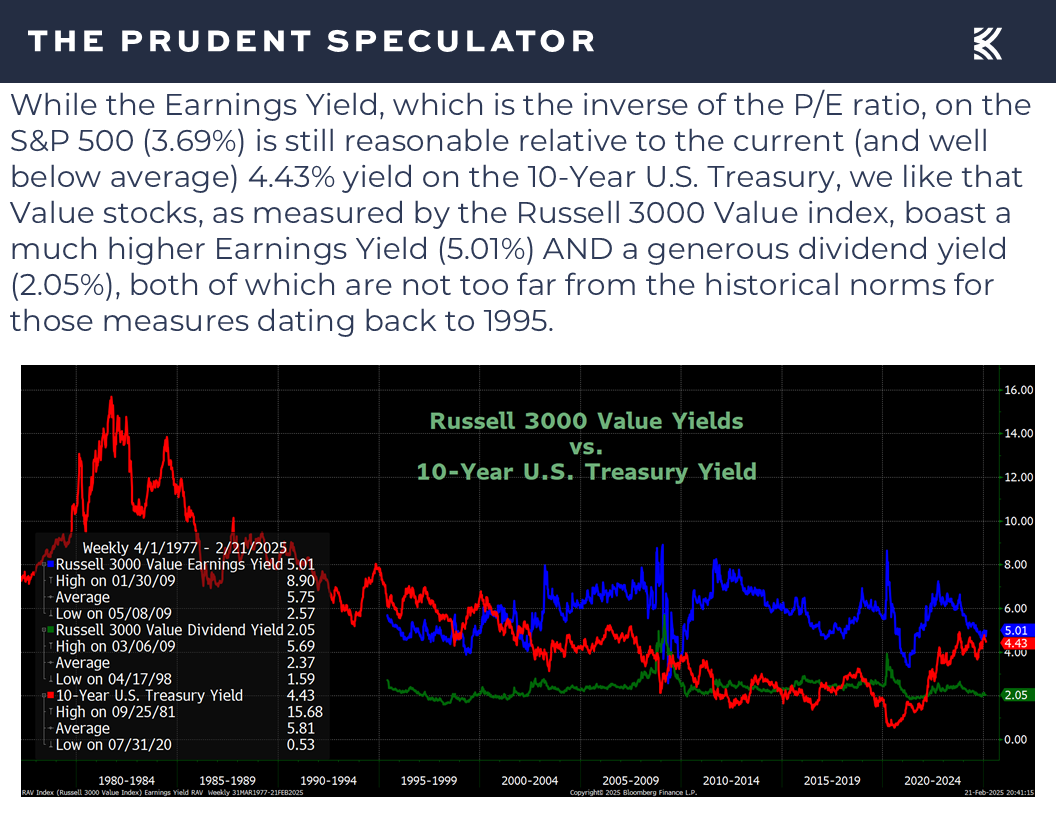

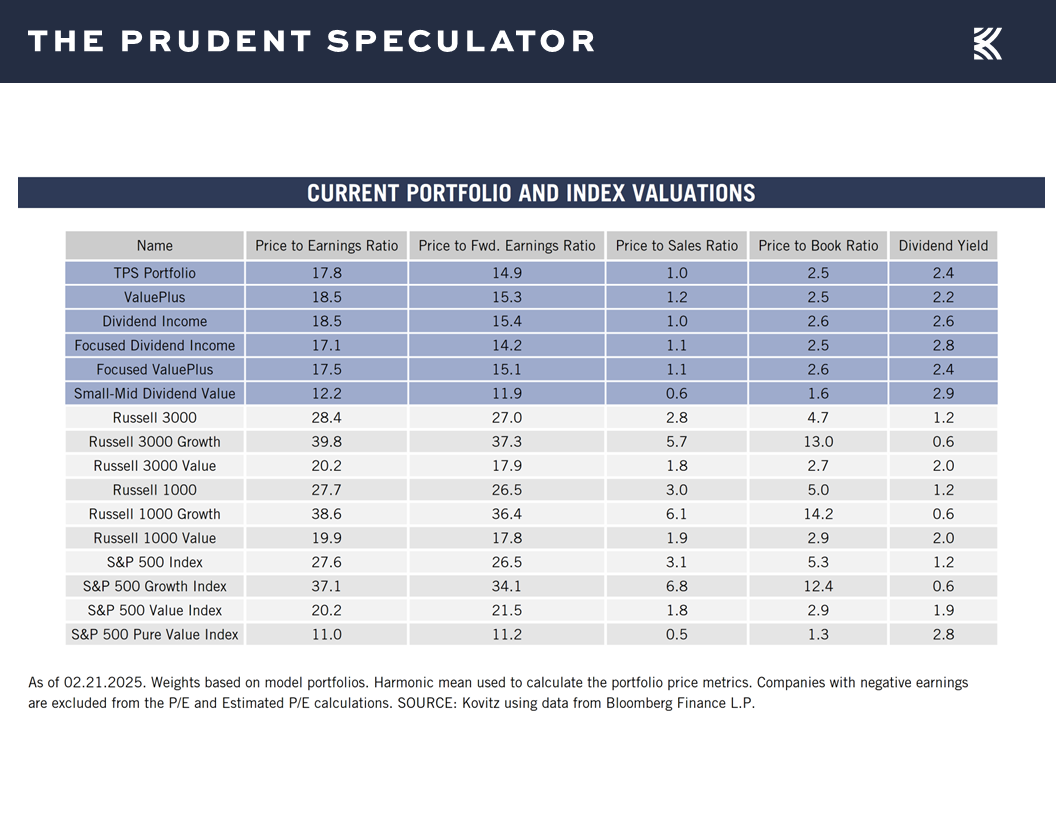

Valuations – Value Stocks Remain Reasonably Priced

which we think adds to the reasonable-valuation argument for Value stocks in general,

and our broadly diversified portfolios of what we believe are undervalued stocks in particular.

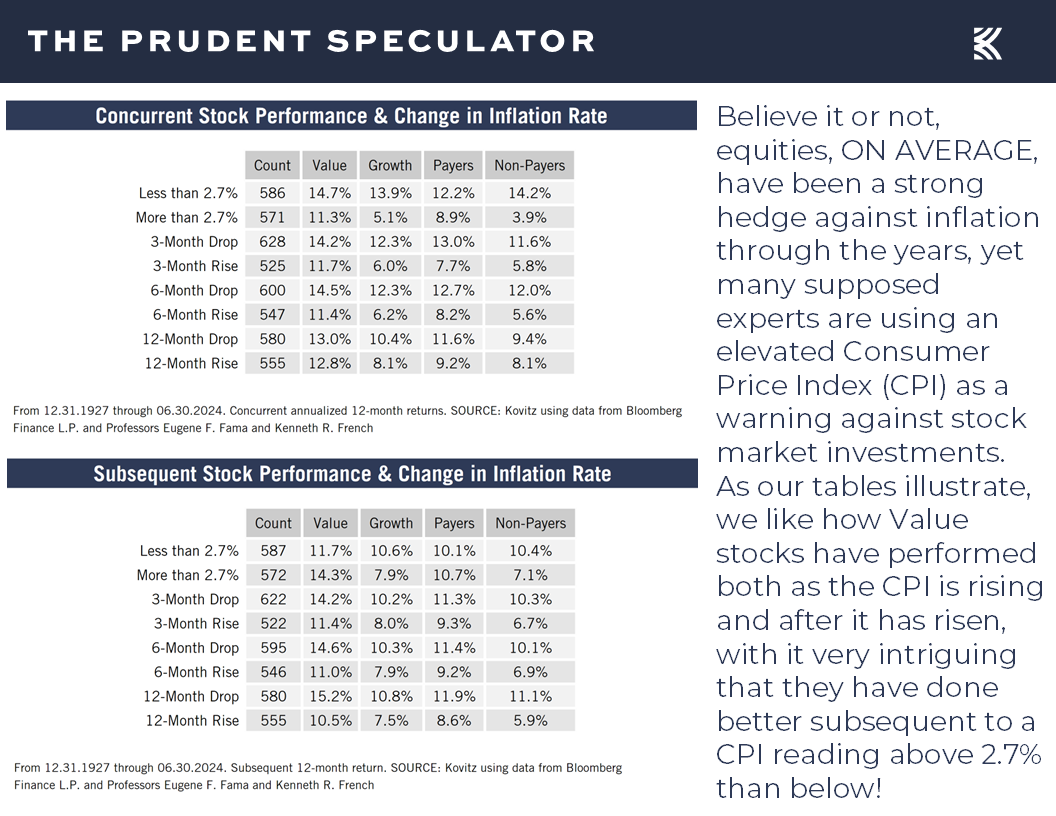

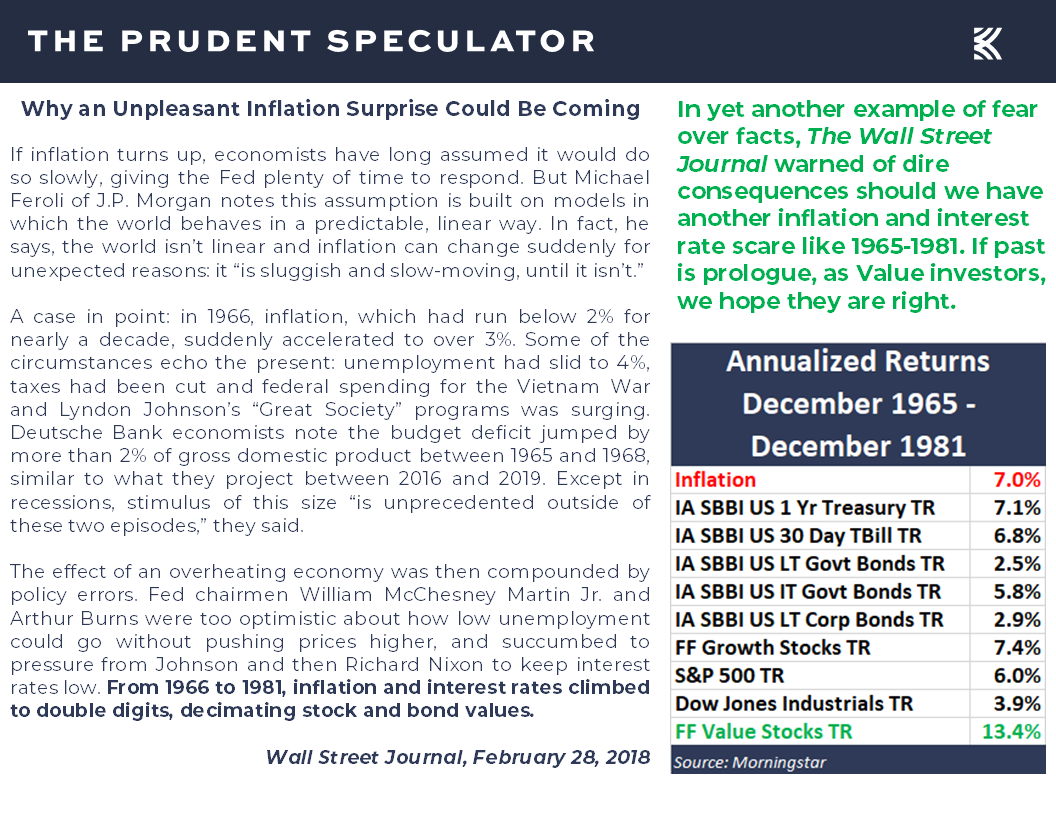

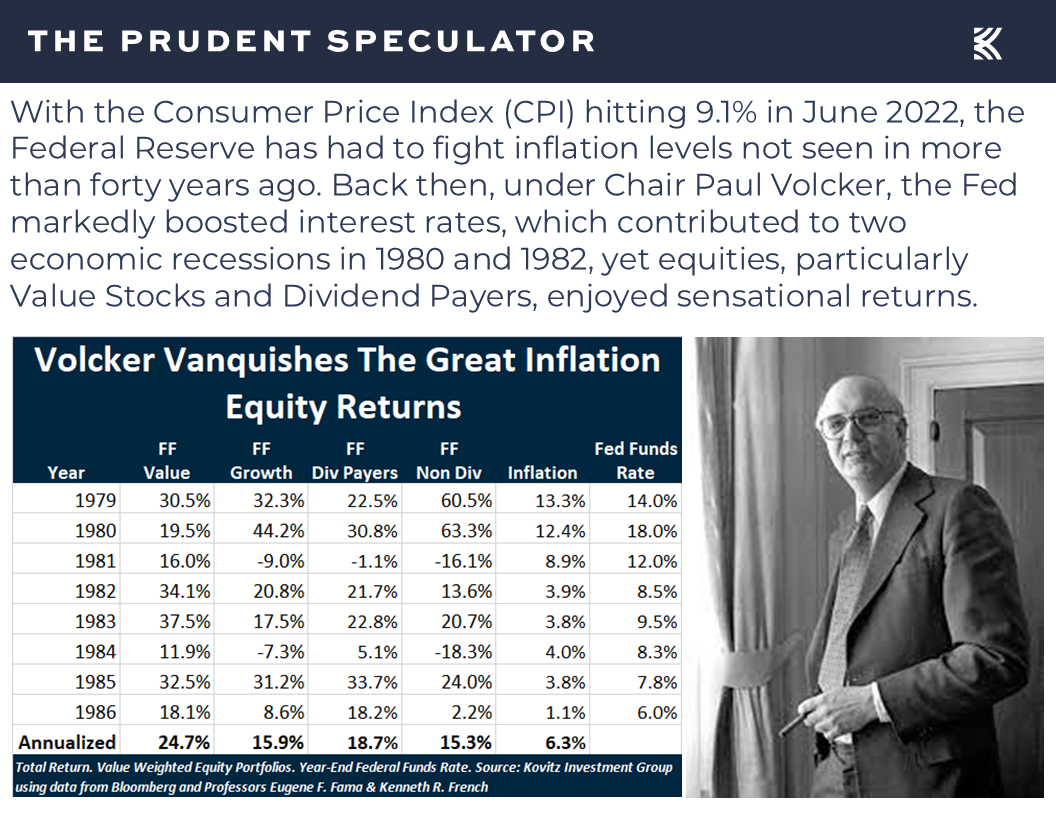

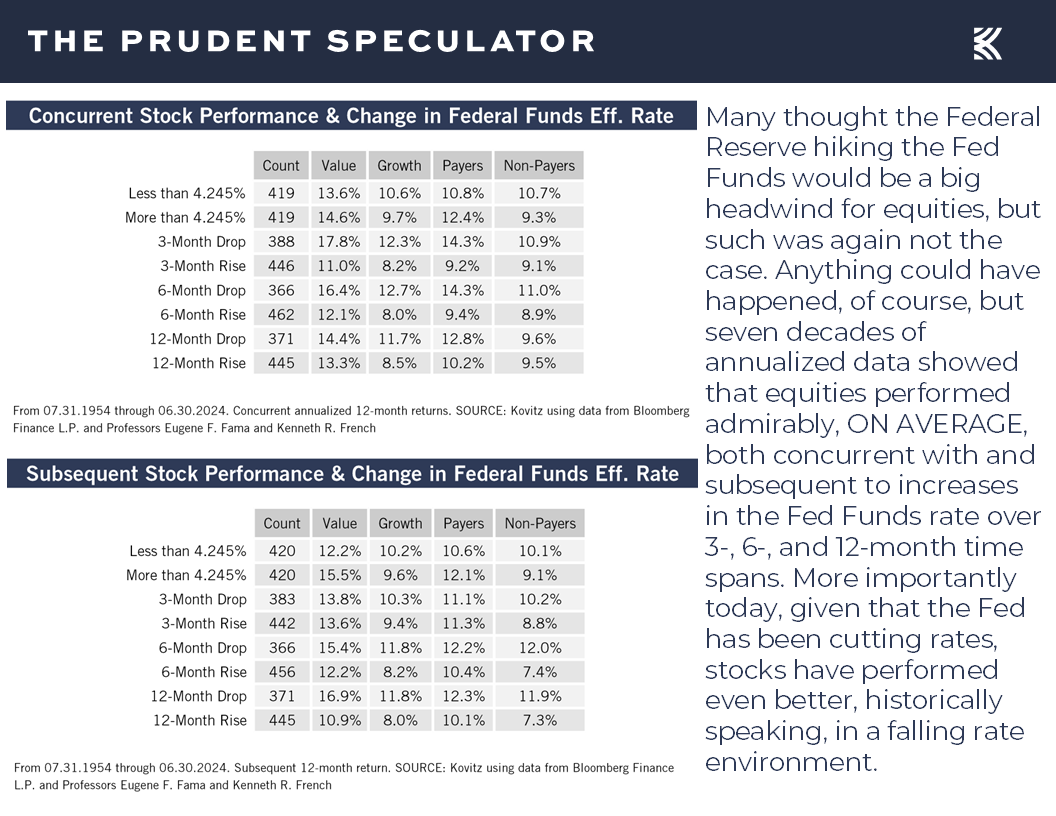

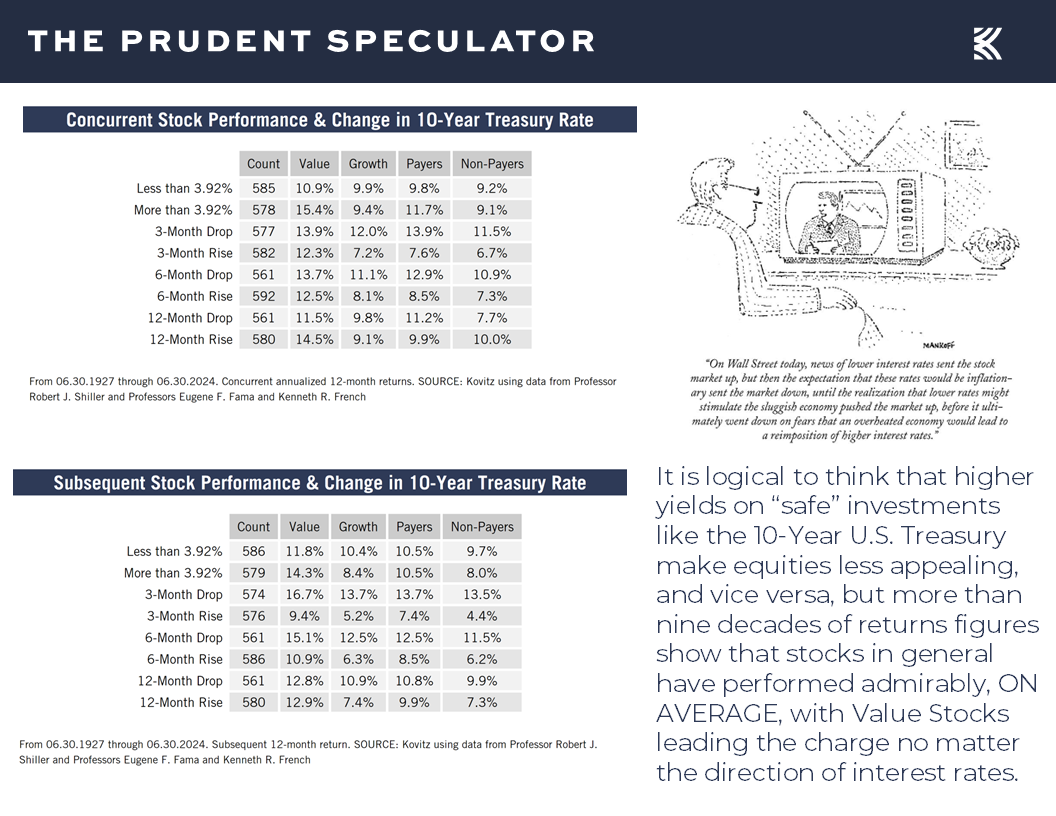

Historical Evidence – On Average, Stocks Have Performed Fine Whether Inflation/Fed Funds/Interest Rates are Rising/Falling

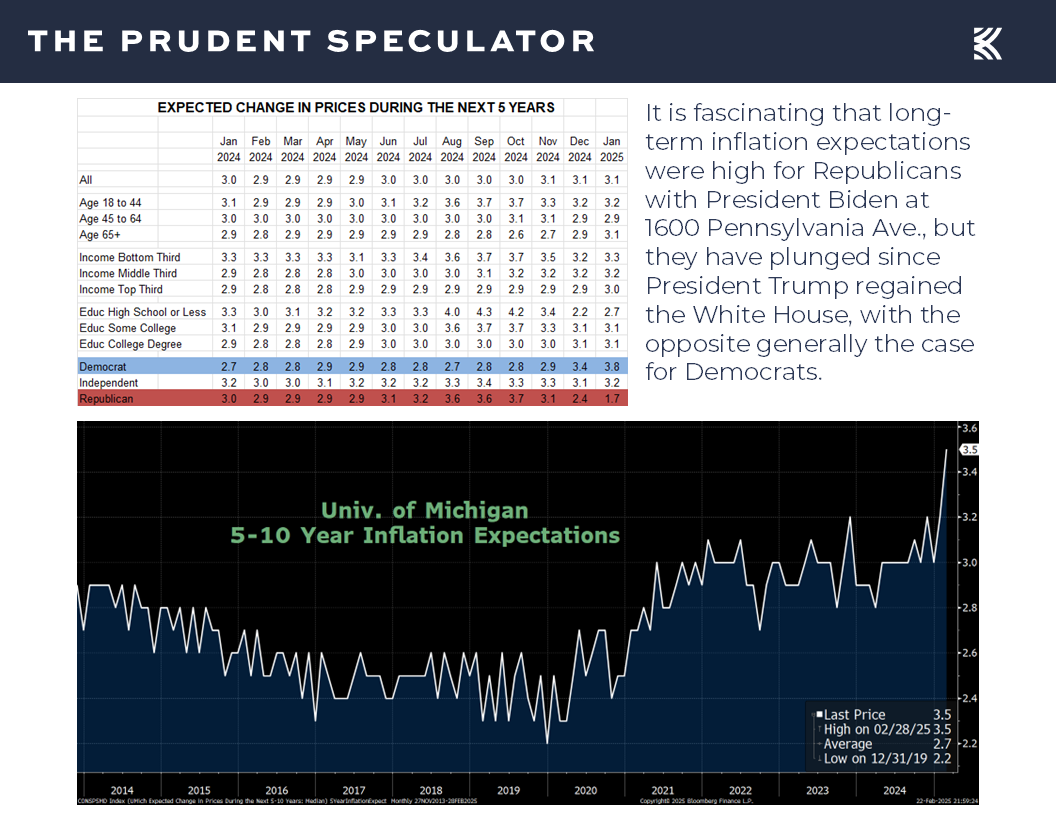

Our optimistic long-term outlook always comes with the caveat that we have no idea which way traders will push stocks in the short run. Indeed, we realize that inflation worries also hit stocks on Friday after the Univ. of Michigan’s sentiment survey showed a jump in longer-term price expectations,

but we again offer the reminder that equities have proved to be terrific inflation hedge,

with Value stocks performing very well during prior elevated inflation regimes, including the period from 1965 to 1981 when the CPI rose 7.0% per annum,

and enjoying spectacular gains when then Fed Chair Paul Volcker markedly raised interest rates to eventually vanquish that period’s Great Inflation.

We know some may believe us to be pollyannish in our stock market views, but we are students of market history, with decades of evidence showing that equities, on average, have performed well in the face of perceived headwinds, despite financial pundits constantly arguing otherwise.

As Vannevar Bush states, “Fear cannot be banished, but it can be calm and without panic; it can be mitigated by reason and evaluation.” So, we will continue to point out that equites have appreciated nicely, on average, whether the Federal Reserve is tightening or easing monetary policy,

or whether long-term government bond yields are rising or falling.

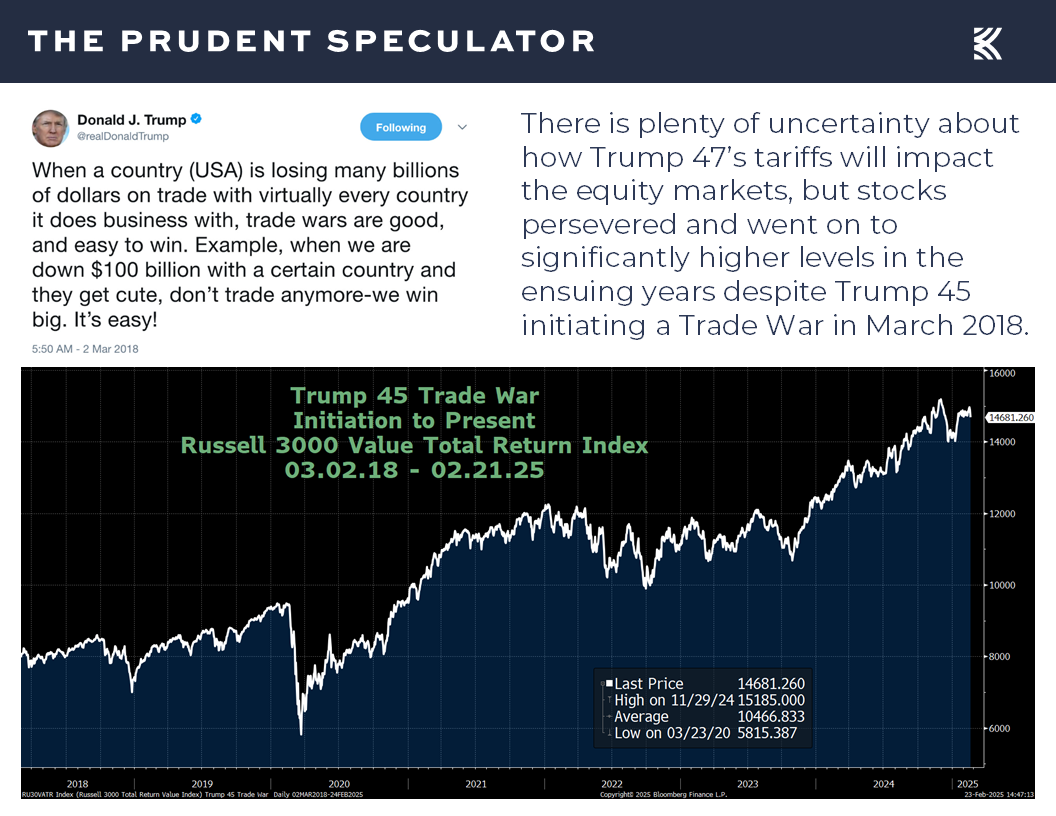

And, with tariff talk continuing to heavily influence short-term market gyrations, we note that stocks have managed to advance nicely since Trump 45’s Trade War began seven years ago.

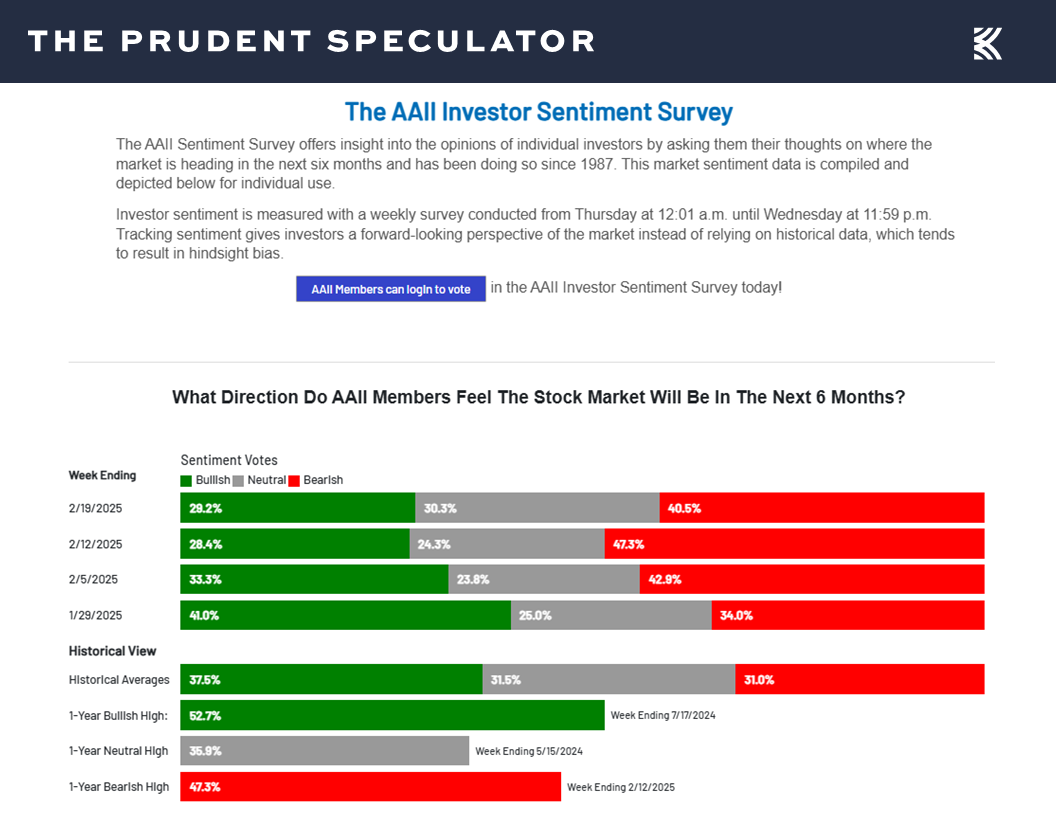

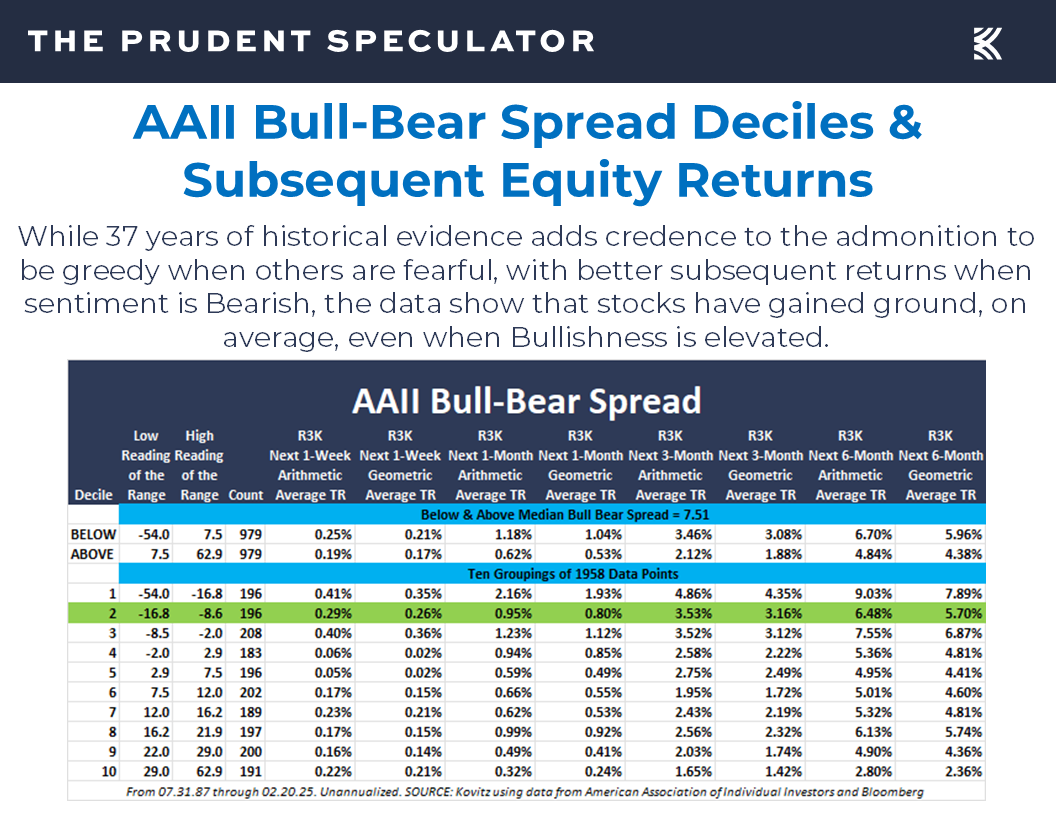

Sentiment – Contrarian AAII Buy Signal

We respect that fear is a tough emotion to overcome for many market participants, and the latest Bull-Bear Sentiment Survey shows a preponderance of pessimists,

but 37 years of data illustrate it is good to be greedy when others are fearful.

Stock News – Updates on ten stocks eight different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

Volatility, Inflation, Equity Returns and Tariffs

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Volatility, Inflation, Equity Returns and Tariffs. We also include a short preview of our specific stock picks for the week, the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – One Sell in 4 Accounts

Perspective – 504th Worst Weekly Loss for the Dow

Volatility – Stocks Go Up and Down in the Short Term, But Have Provided Handsome Rewards in the Long-Term

Econ Data – Mixed Numbers but Solid GDP and EPS Growth Projected for 2025

Valuations – Value Stocks Remain Reasonably Priced

Historical Evidence – On Average, Stocks Have Performed Fine Whether Inflation/Fed Funds/Interest Rates are Rising/Falling

Sentiment – Contrarian AAII Buy Signal

Stock News – Updates on MDT, DVN, CE, NTR, DINO, HAS, WMT, NEM, PHG & WKC

Perspective – 504th Worst Weekly Loss for the Dow

While the trading week started well, it was a very ugly finish, so much so that the widely followed Dow Jones Industrial Average skidded more than 1,100 points over the full four trading days. Believe it or not, the 2.51% percentage skid did not quite rank in the top 500 of the all-time worst weeks for the popular index,

Volatility – Stocks Go Up and Down in the Short Term, But Have Provided Handsome Rewards in the Long-Term

but it did offer another reminder that downside volatility has always been part of the long-term investment process, even as stocks have provided handsome overall long-term returns.

No doubt, there were concerning events last week, including more drama on the geopolitical stage, questions about the efforts of the Department of Government Efficiency and even news of a new bat coronavirus in China. Of course, there have always been fears to contend with for investors as the equity markets have long climbed a wall of worry, with near-term difficulties always overcome in the fullness of time.

Econ Data – Mixed Numbers but Solid GDP and EPS Growth Projected for 2025

Certainly, questions about the health of the U.S. economy also played a large part in the selloff to end the week, as existing home sales for January dipped to an annual rate of 4.08 million, below expectations and down from a revised annual rate of 4.29 million in December,

S&P Global’s preliminary measure of U.S. service sector activity for February fell to 49.7, well below forecasts of 53.0 and down considerably from a reading of 52.9 in January

and the University of Michigan’s gauge of consumer sentiment for February sank to 64.7 versus estimates of 67.8, though the measure is heavily influenced by political biases.

On the other hand, the labor market remained healthy, with first-time filings for unemployment benefits in the latest reported week remaining near multi-generational lows,

factory activity in the New York area,

and the Philadelphia region this month both topped expectations,

and S&P Global’s preliminary measure of U.S. manufacturing activity for February of 51.6 edged past estimates of 51.4 and inched up from January’s tally of 51.2.

To be sure, the outlook for the U.S. economy is hardly clear as the forward-looking Leading Economic Index from the Conference Board fell a greater-than-projected 0.3% last month, yet the keeper of the index proclaimed, “We currently forecast that real GDP for the U.S. will expand by 2.3% in 2025, with stronger growth in the first half of the year.”

Interestingly, that GDP forecast for all of 2025 matches the latest estimate from the Atlanta Fed for Q1 real (inflation-adjusted) growth,

with expectations for a decent economy supporting estimates for favorable corporate profit growth this year and next,

Valuations – Value Stocks Remain Reasonably Priced

which we think adds to the reasonable-valuation argument for Value stocks in general,

and our broadly diversified portfolios of what we believe are undervalued stocks in particular.

Historical Evidence – On Average, Stocks Have Performed Fine Whether Inflation/Fed Funds/Interest Rates are Rising/Falling

Our optimistic long-term outlook always comes with the caveat that we have no idea which way traders will push stocks in the short run. Indeed, we realize that inflation worries also hit stocks on Friday after the Univ. of Michigan’s sentiment survey showed a jump in longer-term price expectations,

but we again offer the reminder that equities have proved to be terrific inflation hedge,

with Value stocks performing very well during prior elevated inflation regimes, including the period from 1965 to 1981 when the CPI rose 7.0% per annum,

and enjoying spectacular gains when then Fed Chair Paul Volcker markedly raised interest rates to eventually vanquish that period’s Great Inflation.

We know some may believe us to be pollyannish in our stock market views, but we are students of market history, with decades of evidence showing that equities, on average, have performed well in the face of perceived headwinds, despite financial pundits constantly arguing otherwise.

As Vannevar Bush states, “Fear cannot be banished, but it can be calm and without panic; it can be mitigated by reason and evaluation.” So, we will continue to point out that equites have appreciated nicely, on average, whether the Federal Reserve is tightening or easing monetary policy,

or whether long-term government bond yields are rising or falling.

And, with tariff talk continuing to heavily influence short-term market gyrations, we note that stocks have managed to advance nicely since Trump 45’s Trade War began seven years ago.

Sentiment – Contrarian AAII Buy Signal

We respect that fear is a tough emotion to overcome for many market participants, and the latest Bull-Bear Sentiment Survey shows a preponderance of pessimists,

but 37 years of data illustrate it is good to be greedy when others are fearful.

Stock News – Updates on ten stocks eight different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.