Preview of March 2022 Newsletter

The Prudent Speculator – Editor’s Note

“The stock market is a device for transferring money from the impatient to the patient.” — Warren Buffett

As we add the Russian Invasion of Ukraine to the long list of disconcerting headlines with which we have had to contend in 45 years of publishing The Prudent Speculator, we never lose sight of what our founder Al Frank wrote in the first edition of the newsletter on March 12, 1977.

I like the stock market; prefer it to other kinds of speculation such as real estate or precious metals and stones. Certainly it has its faults; what institution is not flawed? It is the cleanest way I know of making and losing money. Where else can I buy something of value without a face-to-face confrontation? And where else can I sell something of value without pitching it to someone?

Although the S&P 500 has overcome scores of frightening events and returned some 15,000% (11.8% per annum – oh, the miracle of compounding!) since Al penned those comments, we realize that investor affection for equities has waned of late. Indeed, the count of Bears in the latest American Association of Individual Investors Sentiment Survey hit 53.7, the highest since April 2013. Of course, with the fewest number of pessimists ever registered in August 1987, not long before Black Monday, and the greatest tally of Bears ever recorded the first week of March 2009, just a few days from the equity market bottom during the Great Financial Crisis, the AAII gauge has long been viewed as a terrific contrarian indicator. There is a reason for the stock market adage, “Be greedy when others are fearful and fearful when others are greedy!”

Al recognized the importance of keeping emotions in check, writing in that inaugural issue: After several years of helter-skelter buying and selling, I learned that successful speculating is more a matter of character than mathematics, analysis or luck. Obviously, the latter are required, but the great gains and losses seem to occur in consequence to individual psychology. Easier said than done we know, especially in today’s 24/7/365 media world, but volatility has always been a part of the investment landscape with the recent 10%+ setback in the S&P 500 the 35th correction of that magnitude or greater without an intervening 10% advance since 1977.

We do not mean to downplay the humanitarian crisis in Eastern Europe and the risk of even further escalation as NATO allies increase their support of Ukraine and much of the world tightens the economic screws on Russia, but equities in the fullness of time always have overcome conflict on the global stage. The current events are not yet on par with the Cuban Missile Crisis, but the S&P 500 was then trading at 57 (it is 4386 today), having endured a negative-14% total return the six months prior, yet six and 12 months later, that index had rebounded 23% and 32%, respectively.

We also understand that the price of oil spiking above $100 per barrel has fanned inflation fears, but worries about a 50-basis-point hike in the Fed Funds rate at the upcoming FOMC meeting actually have diminished, while the benchmark 10-Year U.S. Treasury yield is lower today than when Russia’s military action commenced. And, for folks concerned that these issues will return to the fore, our studies show that Value stocks, like those that we have long favored, have performed very well, on average, when inflation is high or when the Fed is tightening or when interest rates are rising.

The strength of U.S. and global GDP growth is also in question, and we are not suggesting that the war in Ukraine will have no impact. However, the pandemic is receding for much of the world, the most recent domestic economic stats have been good and corporate profits have been superb, with EPS growth likely to remain robust.

We are always braced for elevated volatility, but we like the inexpensive valuations and generous dividend yields on our portfolios. As Warren Buffett wrote last week, “People who are comfortable with their investments will, on average, achieve better results than those who are motivated by ever-changing headlines, chatter and promises.

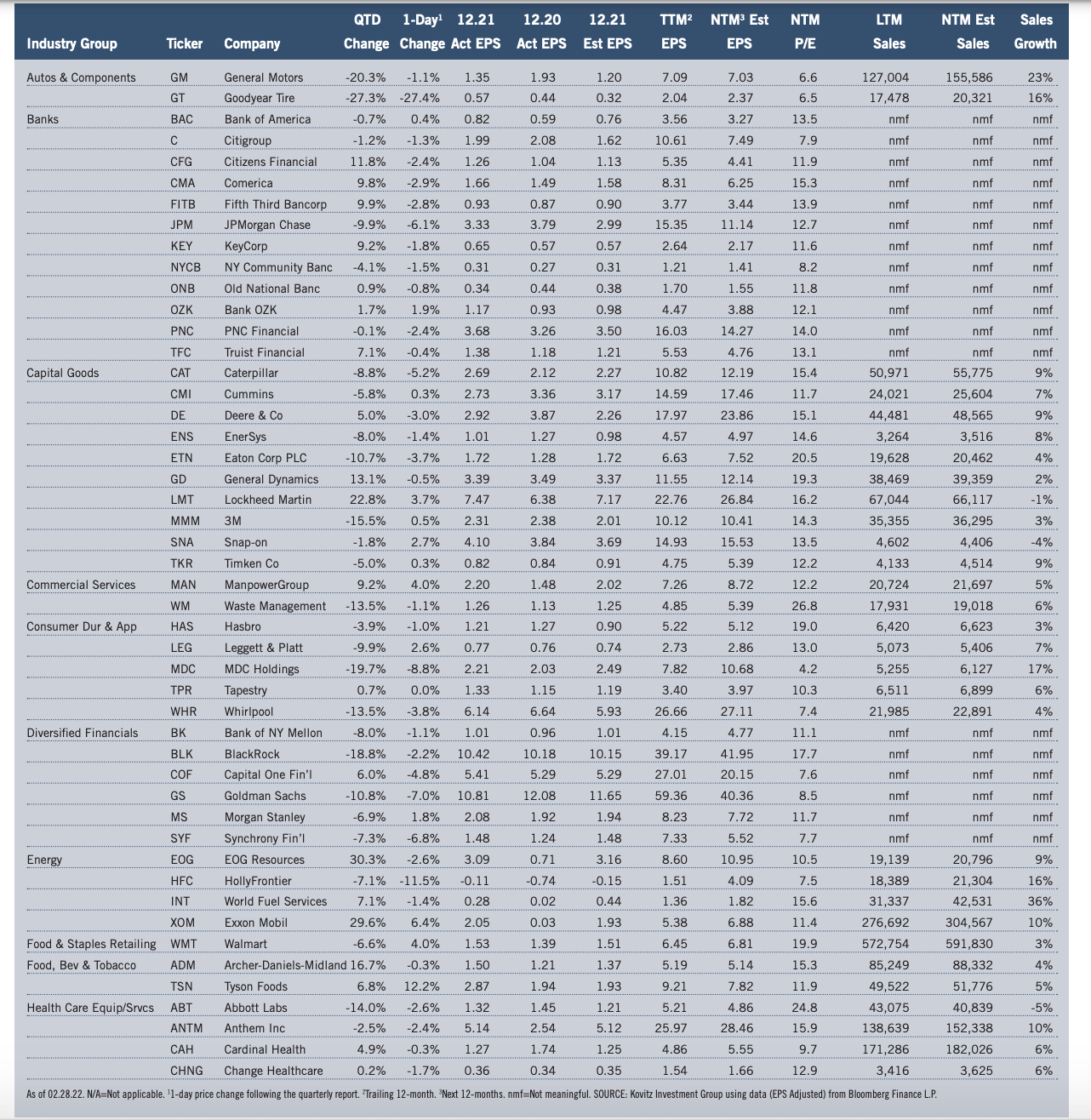

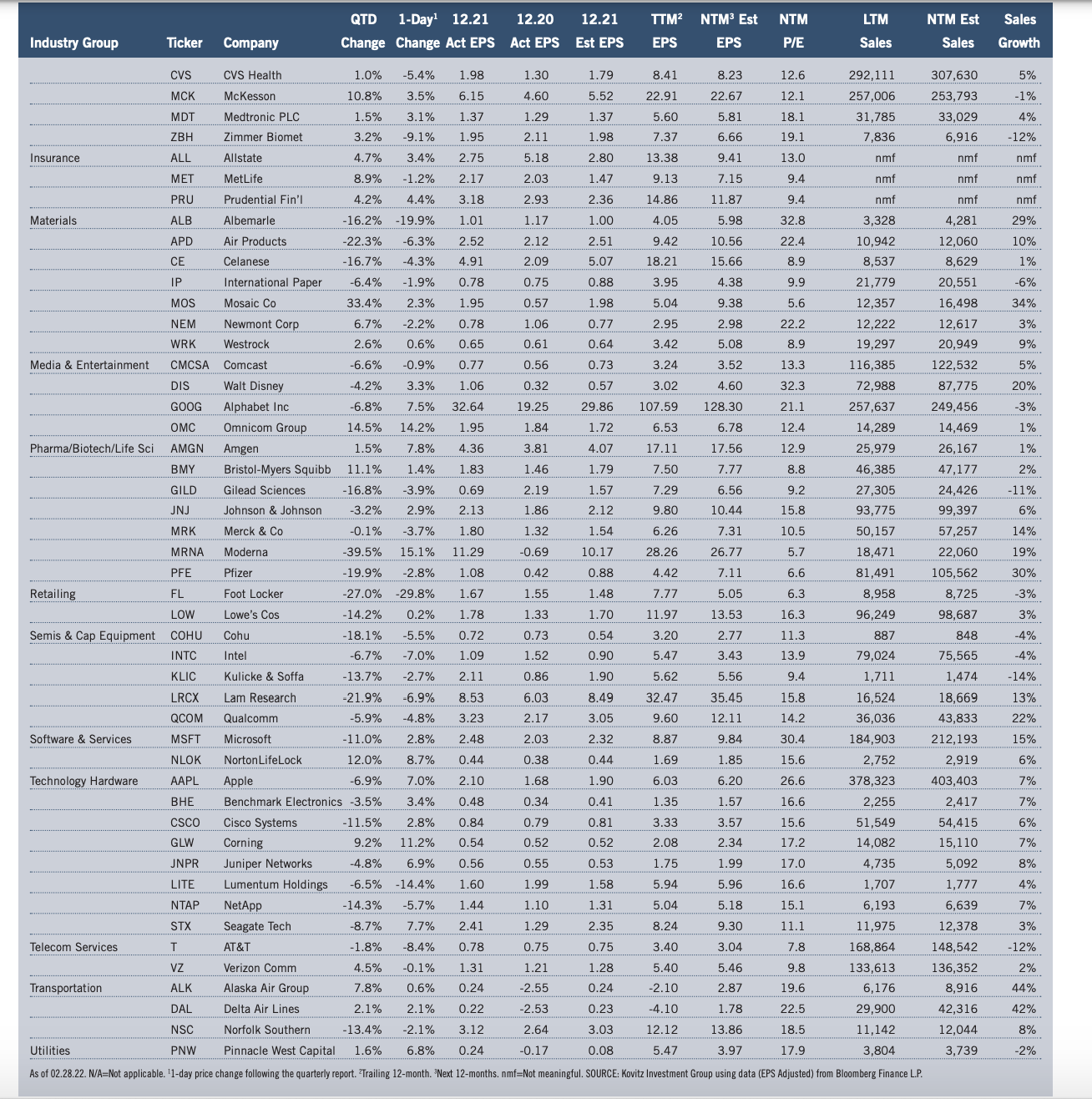

Graphic Detail: Earnings Scorecard

Q4 Season

With U.S. GDP growth jumping by 7.0% in the fourth quarter, up from 2.3% in the third quarter, Q4 earnings reports were again terrific, with management teams doing their usual great job of under-promising and overdelivering. S&P Dow Jones Indices calculated that Q4 “operating” and “as-reported” earnings per share for the S&P 500 soared 41% and 63%, respectively, compared to Q4 2020, with both tallies again hitting all-time highs.

Impressively, the number of S&P 500 companies that exceeded bottom-line forecasts was 76.2%, much better than the usual “beat” rate, while 69.3% eclipsed top-line projections. Of The Prudent Speculator’s 96 stocks presented in our Earnings Scorecard, an impressive 78.1% topped EPS expectations, yet the average one-day price reaction was a sizable decline of 1.1%.

Standard & Poor’s projects (as of 02.28.22) that after jumping from $122.37 in 2020 to $205.36 in 2021, bottomup operating EPS for the S&P 500 will climb to $223.14 this year and to $244.32 in 2023. No doubt, estimates always are subject to change, but we think anything close to those numbers would support much higher stock prices, especially with interest rates still at very low levels.

Recommended Stock List

In this space, we list all of the stocks we own across our multi-cap-value managed account strategies and in our four newsletter portfolios. See the last page for pertinent information on our flagship TPS strategy, which has been in existence since the launch of The Prudent Speculator in March 1977.

Readers are likely aware that TPS has long been monitored by The Hulbert Financial Digest (“Hulbert”). As industry watchdog Mark Hulbert states, “Hulbert was founded in 1980 with the goal of tracking investment advisory newsletters. Ever since it has been the premiere source of objective and independent performance ratings for the industry.” For info on the newsletters tracked by Hulbert, visit: http://hulbertratings.com/since-inception/

Keeping in mind that all stocks are rated as “Buys” until such time as we issue an official Sales Alert, we believe that all of the companies in the tables on these pages trade for significant discounts to our determination of longterm fair value and/or offer favorable risk/reward profiles. Note that, while we always seek substantial capital gains, we require lower appreciation potential for stocks that we deem to have more stable earnings streams, more diversified businesses and stronger balance sheets. The natural corollary is that riskier companies must offer far greater upside to warrant a recommendation. Further, as total return is how performance is ultimately judged, we explicitly factor dividend payments into our analytical work.

While we always like to state that we like all of our children equally, meaning that we would be fine in purchasing any of the 100+ stocks, we remind subscribers that we very much advocate broad portfolio diversification with TPS Portfolio holding more than eighty of these companies. Of course, we respect that some folks may prefer a more concentrated portfolio, however our minimum comfort level in terms of number of overall holdings in a broadly diversified portfolio is at least thirty!

TPS rankings and performance are derived from hypothetical transactions “entered” by Hulbert based on recommendations provided within TPS, and according to Hulbert’s own procedures, irrespective of specific prices shown within TPS, where applicable. Such performance does not reflect the actual experience of any TPS subscriber. Hulbert applies a hypothetical commission to all “transactions” based on an average rate that is charged by the largest discount brokers in the U.S., and which rate is solely determined by Hulbert. Hulbert’s performance calculations do not incorporate the effects of taxes, fees, or other expenses. TPS pays an annual fee to be monitored and ranked by Hulbert. With respect to “since inception” performance, Hulbert has compared TPS to 19 other newsletters across 62 strategies (as of the date of this publication). Past performance is not an indication of future results. For additional information about Hulbert’s methodology, visit: http://hulbertratings.com/methodology/.

Portfolio Builder

Each month in this column, we highlight 10 stocks with which readers might populate their portfolios: Cummins (CMI), Meta Platforms (FB), 3M Co (MMM) and seven others.