Every month, The Prudent Speculator produces a newsletter that includes a market summary, helpful charts and graphs, recent equity market news, economic outlook and specific stock investment strategies focused on value stock investing. This month, our Editor’s Note offers more perspective on navigating the headlines. In our Portfolio Builder section, we continue to add stocks to three of our newsletter portfolios, while our Graphic Detail takes a look at banks and their metrics. We also include a preview of our current Recommended Stock List and Portfolio Builder section with ten highlighted stocks. Note that the entire list is available to our community of loyal subscribers only.

Editor’s Note: Bank Metrics

“Bad news sells because the amygdala is always looking for something to fear.” – Peter Diamandis

While our contrarian bent might lament headlines at the end of July like, “A Soft Landing in Sight for U.S. Economy,” in The Wall Street Journal and “Economic Data Swelling Hopes of Soft Landing,” in The New York Times, both publications were simply acknowledging that recent economic statistics were better than most market watchers were expecting.

Lest like-minded folks worry too much, even with real (inflation-adjusted) Q2 GDP growth climbing 2.4%, consumer confidence and retail sales holding up well, the labor market remaining strong and key measures of inflation moderating, economic conditions were only rosy enough to push Bloomberg’s calculation of the odds of recession in the next 12 months down to 60%, versus 65% for much of 2023.

Such a pessimistic view is echoed by the widely watched Leading Economic Index declining by 0.7% in June, the fifteenth straight monthly drop. The keeper of the gauge, The Conference Board, proclaimed, “We forecast that the U.S. economy is likely to be in recession from Q3 2023 to Q1 2024. Elevated prices, tighter monetary policy, harder-to-get credit, and reduced government spending are poised to dampen economic growth further.”

Never mind that the Federal Reserve indicated a week ago that a contraction this year is no longer its consensus forecast, while the International Monetary Fund (IMF) just upgraded its outlook for global economic growth, stating: “The recent resolution of the U.S. debt ceiling standoff and, earlier this year, strong action by authorities to contain turbulence in U.S. and Swiss banking reduced the immediate risks of financial sector turmoil. This moderated adverse risks to the outlook.”

Of course, the IMF was quick to add: “The balance of risks to global growth remains tilted to the downside. Inflation could remain high and even rise if further shocks occur, including those from an intensification of the war in Ukraine and extreme weather-related events, triggering more restrictive monetary policy. Financial sector turbulence could resume as markets adjust to further policy tightening by central banks. China’s recovery could slow, in part as a result of unresolved real estate problems, with negative cross-border spillovers. Sovereign debt distress could spread to a wider group of economies.”

No doubt, such caveats are reasonable and we note that The New York Times saw fit to publish a more downbeat front-page story the same day as the aforementioned Bullish piece. This one highlighted the Bearish cases made by a pair of prominent market strategists who thus far in 2023 have kept their followers on the sidelines, even as the market rally has broadened markedly to propel the average stock to double-digit year-to-date returns.

Even one of your Editor’s favorite Wall Street Journal columnists wrote, “Stocks Have Had a Torrid Start to the Year. It Could End Badly,” in which he argued, “Through the first 135 trading days of the year since 1928, the best four starts to a year all were followed by drops with an average loss of 9.8%.” As one of those ugly years was 1987, danger supposedly is lurking, even as we would assert that a better comparison set is first-half S&P 500 returns similar to this year’s, where the average subsequent return from July 19 to December 31 has been 6.1%, compared to 4.1% for all years. Mark Twain says, “Get your fact first, then you can distort them as you please,” so market prognostications should come with a grain of salt.

Obviously, the terrific July that followed a sensational June adds credence to our long-held admonition that time in the market trumps market timing, but nobody knows if the rally will continue in the near term. What we believe, however, is that over time the economy will grow, corporate profits will expand and stock prices will increase. The key, as Bill Gates states, is to remember, “Headlines, in a way, are what mislead you because bad news is a headline, and gradual improvement is not.”

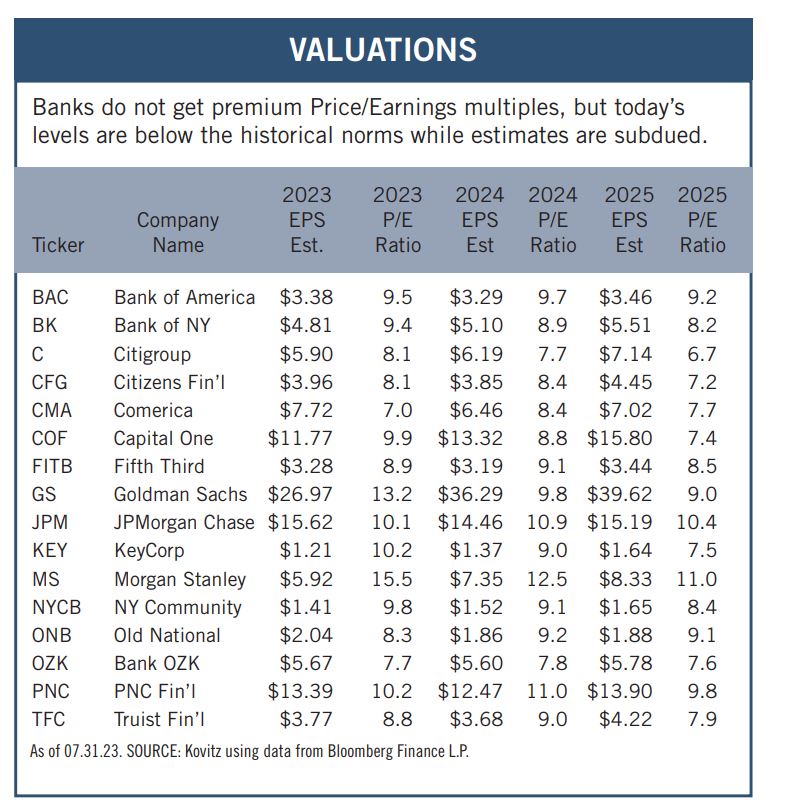

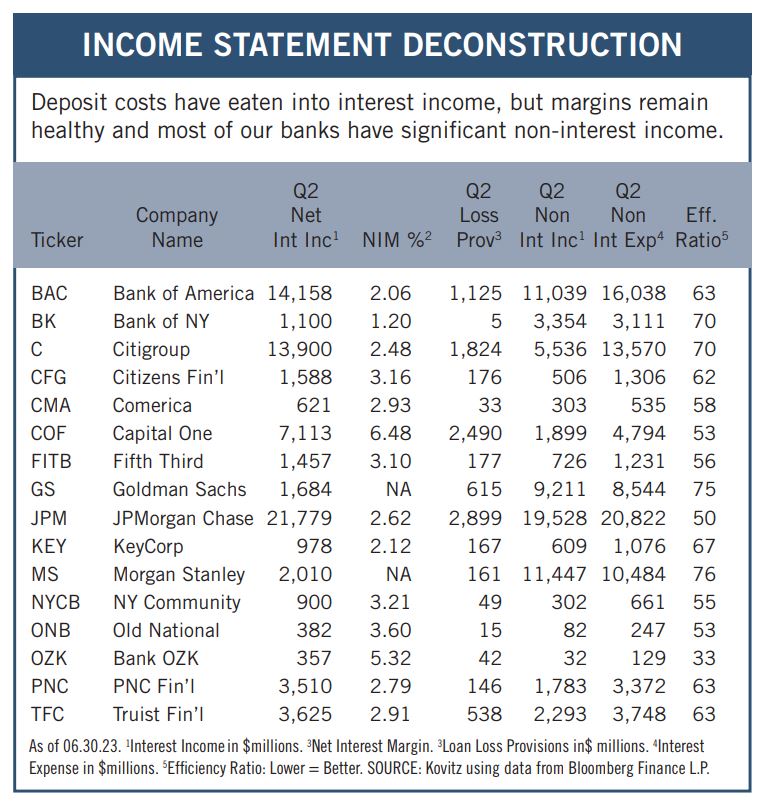

Graphic Detail:

Bank Metrics

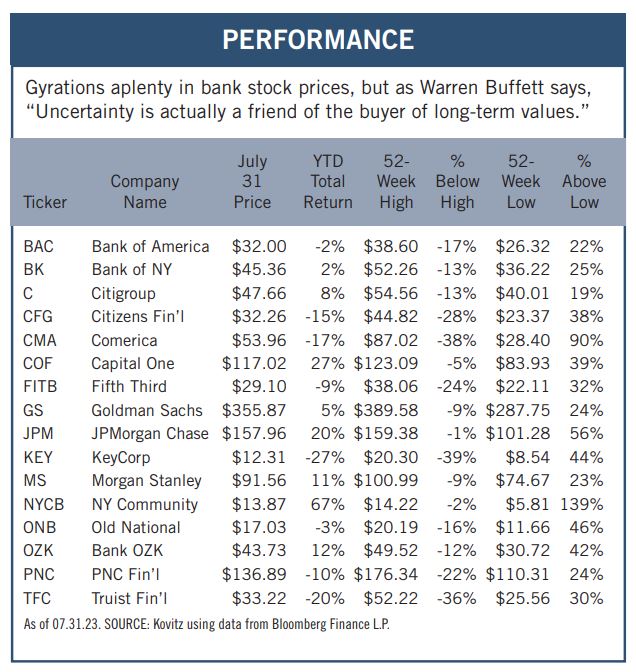

It continues to be a very tough 2023 for stocks in the banking industry. Despite significant rebounds from recent lows, the KBW Bank Index is still off more than 10% for the year, while the S&P Regional Bank ETF is down more than 16%, even as the runs on the bank in the Spring that took down Silicon Valley Bank, Signature Bank and First Republic have not led to more failures.

To be sure, the collapse of those institutions, as well as Credit Suisse, has created very itchy trigger fingers. For example, when news broke late last month that Bank of California (BANC) and fellow-California-based lender PacWest Bancorp (PACW) were in merger talks, traders feared the worst, with shares of the latter quickly plunging 25% on worries that the union might be a shotgun marriage arranged by Uncle Sam. Happily, though the smaller institution swallowed the larger, while two private equity shops made a $400 million investment in Banc of California and JPMorgan Chase was said to have bought $1.8 billion of PacWest mortgages to facilitate the deal, PACW shares will be swapped for 0.6959 of a BANC share. This was quite a surprise for short-sighted traders as PACW shares recouped a large part of the knee-jerk decline, with Barron’s proclaiming, “PacWest stock tanked, then soared, all on the same takeover news.”

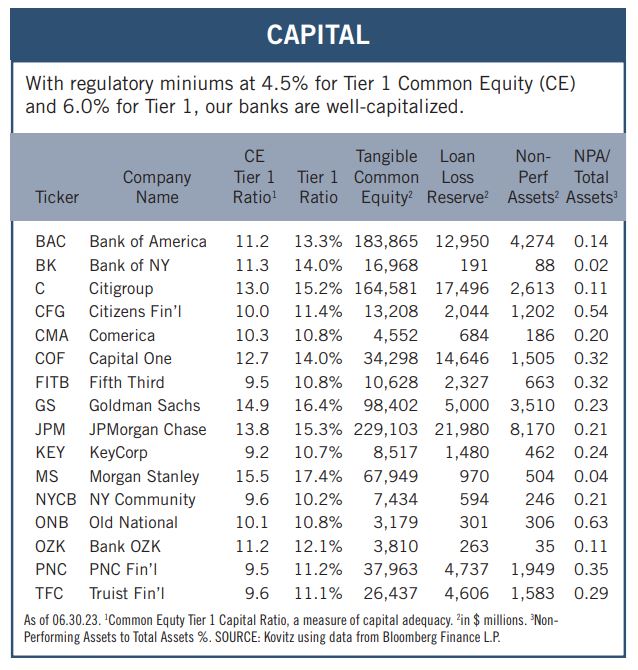

Of course, plenty of uncertainty remains across the industry as U.S. regulators have unveiled sweeping changes to tighten capital requirements for banks. Those institutions with assets of $100 billion will face the greatest impact, even as most already are sufficiently capitalized and the new rules won’t be fully phased in until July 2028.

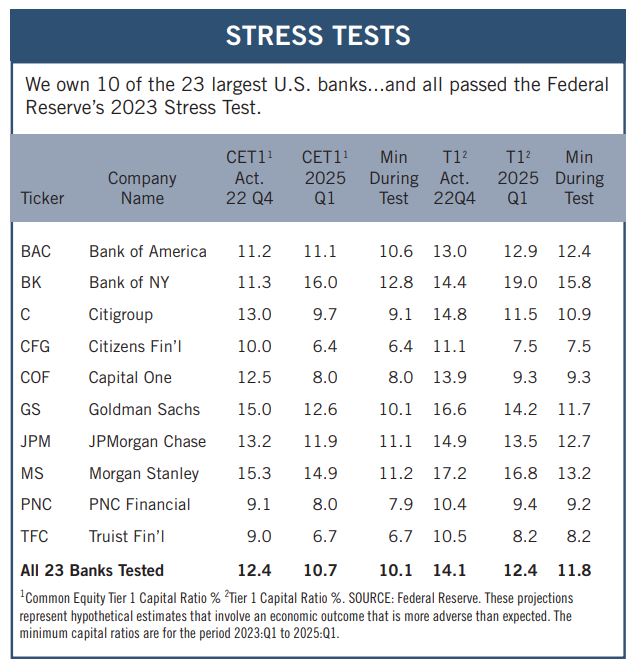

Speaking of capital, we were pleased with the results last month of the Federal Reserve’s annual Stress Test of the nation’s largest banks. This year’s criteria seemed harsh as it included a severe global recession with a 40% decline in commercial real estate prices, a substantial increase in office vacancies, and a 38% decline in house prices. It also included the unemployment rate rising by 6.4 percentage points to a peak of 10% and economic output declining commensurately. However, the Fed concluded, “All 23 banks tested remained above their minimum capital requirements during the hypothetical recession, despite total projected losses of $541 billion. Under stress, the aggregate common equity risk-based capital ratio—which provides a cushion against losses—is projected to decline by 2.3 percentage points to a minimum of 10.1%.”

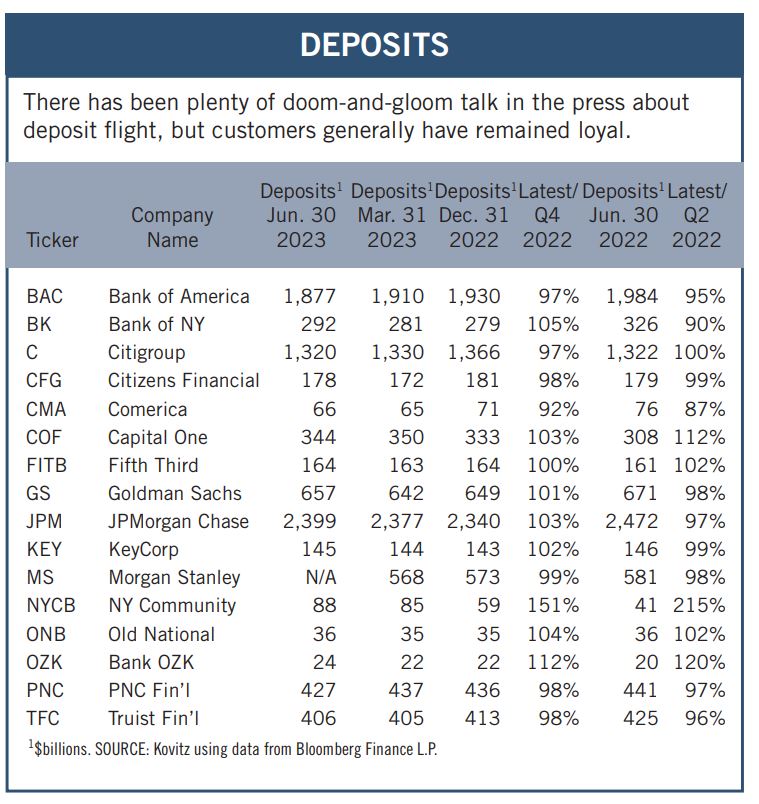

Alas, last year’s Stress Test failed to foresee that the plunge in bond prices due to the Fed’s rate-rising regime might contribute to the aforementioned social-media-fueled runs on the bank, so it isn’t as if the industry is out of the woods. After all, banks have had to pay up to keep deposits, net interest margin has been contracting, the yield curve remains inverted and non-performing assets are likely to move up from near-zero levels.

Nevertheless, we think sizable upside exists in the banking space for long-term-oriented folks, given the share price hits many of the stocks have endured this year. True, some of the biggest banks are in the green in 2023, as they have benefitted from the regional-bank turmoil, but banks across the board continue to trade for very inexpensive valuations. Fed Chair Jerome H. Powell helped argue our case on July 26, stating, “Deposit flows have stabilized, capital and liquidity remain strong. Aggregate bank lending was stable quarter over quarter, and is up significantly year over year. Banking sector profits, generally are coming in strong this quarter and overall the banking system remains strong and resilient.”

Recommended Stock List

In this space, we list all of the stocks we own across our multi-cap-value managed account strategies and in our four newsletter portfolios. See the last page for pertinent information on our flagship TPS strategy, which has been in existence since the launch of The Prudent Speculator in March 1977.

Readers are likely aware that TPS has long been monitored by The Hulbert Financial Digest (“Hulbert”). As industry watchdog Mark Hulbert states, “Hulbert was founded in 1980 with the goal of tracking investment advisory newsletters. Ever since it has been the premiere source of objective and independent performance ratings for the industry.” For info on the newsletters tracked by Hulbert, visit: http://hulbertratings.com/since-inception/.

Keeping in mind that all stocks are rated as “Buys” until such time as we issue an official Sales Alert, we believe that all of the companies in the tables on these pages trade for significant discounts to our determination of long-term fair value and/or offer favorable risk/reward profiles. Note that, while we always seek substantial capital gains, we require lower appreciation potential for stocks that we deem to have more stable earnings streams, more diversified businesses and stronger balance sheets. The natural corollary is that riskier companies must offer far greater upside to warrant a recommendation. Further, as total return is how performance is ultimately judged, we explicitly factor dividend payments into our analytical work.

While we always like to state that we like all of our children equally, meaning that we would be fine in purchasing any of the 100+ stocks, we remind subscribers that we very much advocate broad portfolio diversification with TPS Portfolio holding more than eighty of these companies. Of course, we respect that some folks may prefer a more concentrated portfolio, however our minimum comfort level in terms of number of overall holdings in a broadly diversified portfolio is at least thirty!

TPS rankings and performance are derived from hypothetical transactions “entered” by Hulbert based on recommendations provided within TPS, and according to Hulbert’s own procedures, irrespective of specific prices shown within TPS, where applicable. Such performance does not reflect the actual experience of any TPS subscriber. Hulbert applies a hypothetical commission to all “transactions” based on an average rate that is charged by the largest discount brokers in the U.S., and which rate is solely determined by Hulbert. Hulbert’s performance calculations do not incorporate the effects of taxes, fees, or other expenses. TPS pays an annual fee to be monitored and ranked by Hulbert. With respect to “since inception” performance, Hulbert has compared TPS to 19 other newsletters across 62 strategies (as of the date of this publication). Past performance is not an indication of future results. For additional information about Hulbert’s methodology, visit: http://hulbertratings.com/methodology/.

Portfolio Builder

Each month in this column, we highlight 10 stocks with which readers might populate their portfolios: International Paper (IP), World Kinect (WKC), Waste Management (WM) and seven others.