Every month, The Prudent Speculator produces a newsletter that includes a market summary, helpful charts and graphs, recent equity market news, economic outlook and specific stock investment strategies focused on value stock investing. This month, we are again adding stocks to our four newsletter portfolios, while our Graphic Detail features our quarterly Earnings Scorecard. Note that the entire list is available to our community of loyal subscribers only.

Editor’s Note: Meme Stocks, Economic News and Interest Rates

It was an obvious New York Stock Exchange technical glitch the morning of June 3, but what if Berkshire Hathaway’s Class A shares really were trading at $185, down 99.97% from their prior close above $627,000? Considering that the forward P/E ratio on the stock would have been 0.006, Warren Buffett would have been fighting every investor who cares about valuation metrics to buy hand over fist.

Of course, as evidenced by the revival of so-called Meme stocks on the apparent reemergence in the last few weeks (not once but twice) of GameStop (GME) aficionado Keith Gill, aka Roaring Kitty, plenty of folks have no interest in financial fundamentals. After all, GME opened 74% higher on June 3, before skidding more than 30% by the close, but still ending the trading session with a one-day gain of 21% to trade for 2800 times estimated next-12-month earnings! To be sure, nobody is buying the video-game retailer based on the $0.01 of EPS expected for 2024, and the P/E drops to 483 based on the current $0.06 consensus analyst estimate for 2025, while management refilled the coffers by taking advantage of the mid-May price spike to raise $933 million via an ‘at-the-market’ equity offering. Still, no matter how the valuation is sliced and diced, GME is not a value stock, much less Deep F***ing Value, Mr. Gill’s Reddit handle, but that does not preclude the price from soaring…or crashing.

Indeed, equity prices move up and down for reasons that sometimes defy logic. For example, June began with a sizable selloff in stocks even as oil prices moved sharply lower, reducing inflationary pressures, and interest rates tumbled, arguably making equities more attractive. Of course, the ISM Manufacturing Index for May came in at 48.7 that morning, below expectations and down 0.5 points from April’s reading, but the measure corresponds to a solid 1.7% rate of real (inflation-adjusted) growth for U.S. GDP on an annualized basis.

Now, the financial press must attempt to rationalize the daily gyrations and CNBC.com came up that day with “Stocks fell on Monday as investors struggled to carry the market’s strong May momentum into the new month!”

And speaking of May, it could be asserted that the handsome gains in the equity market averages for the month occurred alongside the same headlines that were present for the first day-of-June swoon.

Inflation readings out in the month were OK. The Core Consumer Price index for April rose 3.4% on a year-over-year basis, down from a 3.5% increase in March, while the Core CPI (excludes food and energy) climbed 3.6%, versus 3.8% the month prior, and the Federal Reserve’s preferred gauge, the Core Personal Consumption Expenditure (PCE) index held steady in April with a 2.8% advance. Longer-term, market-based inflation expectations also were contained.

Meanwhile, interest rates moved lower in May as the yield on the 10-Year U.S. Treasury dropped to 4.50%, down from 4.68% on April 30. The slew of monthly numbers continued to suggest a not-too-hot and not-too-cold economy, as ongoing labor market strength was offset by weaker housing and consumer spending figures.

True, the latest forecast for real Q2 GDP growth from the Atlanta Fed of 1.8% is hardly robust, but the economic backdrop going forward is favorable for corporate profit growth and over the long-haul stock prices have followed earnings higher. Equally important, valuations for the majority of stocks remain attractive, with a forward P/E ratio on TPS Portfolio of 14.6 and dividend yield of 2.5%, especially with Jerome H. Powell stating on May 1, “I think it’s unlikely that the next policy rate move will be a hike.”

So, we will patiently maintain our long-term optimism for our undervalued stocks as we continue to think Paul Samuelson had it right, “Investing should be like watching paint dry or watching grass grow.” As the economist added, “If you want excitement, take $800 and go to Las Vegas,” or chase after the next FOMO Meme stock!

“Nowadays people know the price of everything and the value of nothing.” — Oscar Wilde

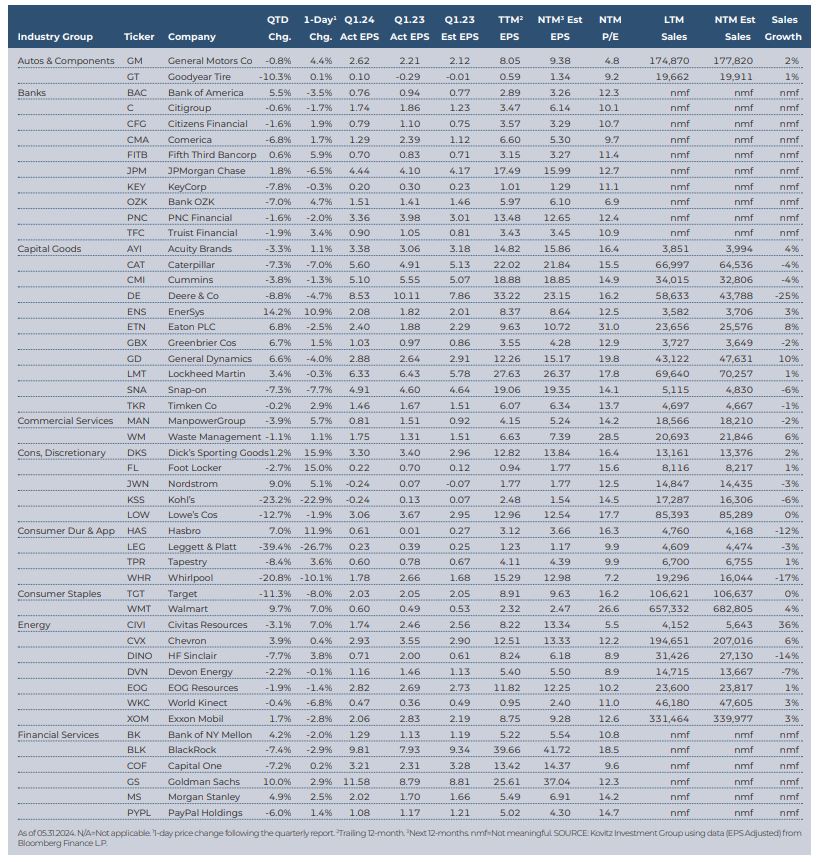

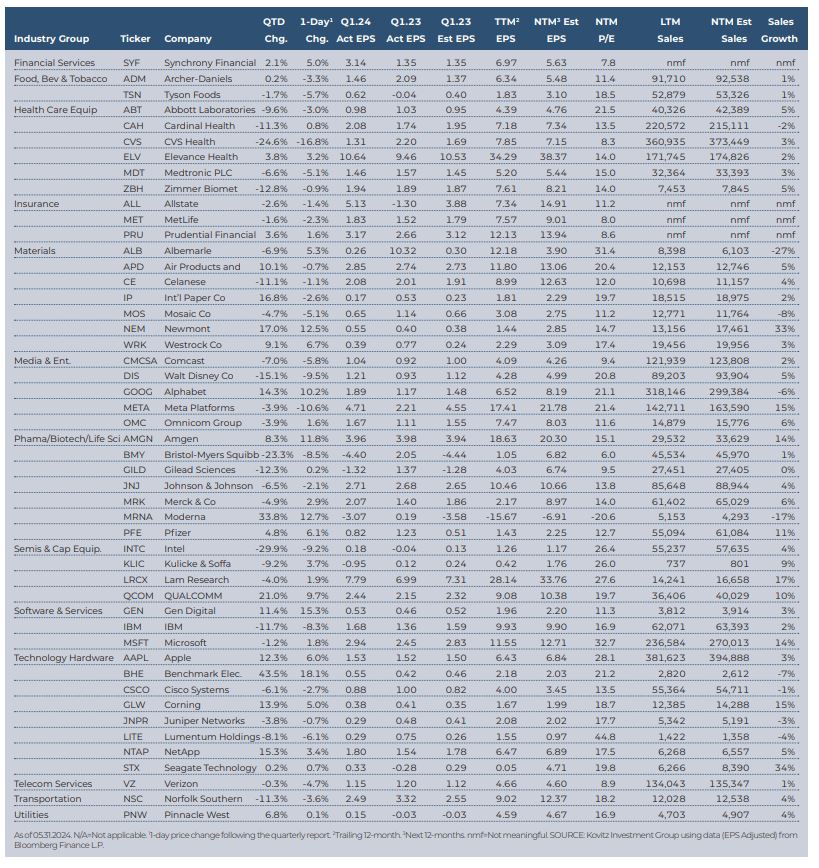

Graphic Detail: Earnings Scorecard

Economic data in the period was solid, though real (inflation-adjusted) U.S. GDP growth came in at a lackluster 1.3% in Q1, but Corporate America again enjoyed favorable revenue and net income tallies, even as management teams engaged in their usual tempering of guidance. Impressively, the number of S&P 500 companies that exceeded bottom-line forecasts was 80.5%, above the usual “beat” rate, and 53.8% eclipsed top-line projections. Of The Prudent Speculator’s 98 stocks presented below, 75% topped EPS expectations, and the average one-day price reaction was a gain of 0.2%, but the average two-month loss since 03.31.24 was 1.4%.

Standard & Poor’s projects (as of 05.31.24) that after rising from $196.95 in 2022 to $213.53 in 2023 (those figures include massive $66.9 billion ($4.74 per share) in Q2 ‘22 and $23.5 billion ($2.82 per share) in Q3 ‘23 “unrealized investment” losses for Berkshire Hathaway), bottom-up operating EPS for the S&P 500 are projected to climb to $241.02 in 2024 and $276.50 in 2025. Estimates are subject to change (current forecasts actually are higher than those two months ago), but anything close to those ‘24 and ‘25 EPS levels should support higher stock prices.

Recommended Stock List

In this space, we list all of the stocks we own across our multi-cap-value managed account strategies and in our four newsletter portfolios. See the last page for pertinent information on our flagship TPS strategy, which has been in existence since the launch of The Prudent Speculator in March 1977.

Readers are likely aware that TPS has long been monitored by The Hulbert Financial Digest (“Hulbert”). As industry watchdog Mark Hulbert states, “Hulbert was founded in 1980 with the goal of tracking investment advisory newsletters. Ever since it has been the premiere source of objective and independent performance ratings for the industry.” For info on the newsletters tracked by Hulbert, visit: http://hulbertratings.com/since-inception/.

Keeping in mind that all stocks are rated as “Buys” until such time as we issue an official Sales Alert, we believe that all of the companies in the tables on these pages trade for significant discounts to our determination of long-term fair value and/or offer favorable risk/reward profiles. Note that, while we always seek substantial capital gains, we require lower appreciation potential for stocks that we deem to have more stable earnings streams, more diversified businesses and stronger balance sheets. The natural corollary is that riskier companies must offer far greater upside to warrant a recommendation. Further, as total return is how performance is ultimately judged, we explicitly factor dividend payments into our analytical work.

While we always like to state that we like all of our children equally, meaning that we would be fine in purchasing any of the 100+ stocks, we remind subscribers that we very much advocate broad portfolio diversification with TPS Portfolio holding more than eighty of these companies. Of course, we respect that some folks may prefer a more concentrated portfolio, however our minimum comfort level in terms of number of overall holdings in a broadly diversified portfolio is at least thirty!

TPS rankings and performance are derived from hypothetical transactions “entered” by Hulbert based on recommendations provided within TPS, and according to Hulbert’s own procedures, irrespective of specific prices shown within TPS, where applicable. Such performance does not reflect the actual experience of any TPS subscriber. Hulbert applies a hypothetical commission to all “transactions” based on an average rate that is charged by the largest discount brokers in the U.S., and which rate is solely determined by Hulbert. Hulbert’s performance calculations do not incorporate the effects of taxes, fees, or other expenses. TPS pays an annual fee to be monitored and ranked by Hulbert. With respect to “since inception” performance, Hulbert has compared TPS to 19 other newsletters across 62 strategies (as of the date of this publication). Past performance is not an indication of future results. For additional information about Hulbert’s methodology, visit: http://hulbertratings.com/methodology/.

Portfolio Builder

Each month in this column, we highlight 10 stocks with which readers might populate their portfolios: Walt Disney (DIS), Cisco Systems (CSCO), and Volkswagen AG Pref. (VWAPY)

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.