Every month, The Prudent Speculator produces a newsletter that includes a market summary, helpful charts and graphs, recent equity market news, economic outlook and specific stock investment strategies focused on value stock investing. This month, This month, we put some of the proceeds of recent sales to work in our four newsletter portfolios, while our Graphic Detail looks at the Calendar and Equity returns, in addition to updating our latest thinking on Regional Banks. We also include a preview of our current Recommended Stock List and Portfolio Builder section with ten highlighted stocks. Note that the entire list is available to our community of loyal subscribers only.

Editor’s Note: Value Stocks, Q4 Earnings, GDP

Awakened from his wintry nap at dawn on Gobblers Knob on February 2, America’s favorite rodent, oops woodchuck, proclaimed: “One thing the weather did NOT provide is a SHADOW and a reason to hide. Glad tidings on this Groundhog Day! An early Spring is on the way.”

Or maybe not. Although the official Groundhog Club proclaims, “Punxsutawney Phil is the seer of seers, the prognosticator of all prognosticators,” his track record leaves a lot to be desired. Per the Stormfax Almanac, Phil has been right just 39% of the time going back to his first recorded prediction in 1887. He hasn’t been any better recently, as the National Oceanic and Atmospheric Administration concluded that he was correct 4 times in 11 years since 2013, for a 36% accuracy rate.

While most understand that the weather is unpredictable, we remain perplexed that so many think they can outguess the short-term gyrations of the equity markets. For example, your Editor’s email box has again been cluttered with solicitations from a rival publication that claims to have called every significant market decline since its launch in 1977. This is nothing new as this outfit has been trumpeting its market-timing prowess for years, with a personal query on how well it has done of a noted investment-newsletter-watchdog back in December 2019 prompting this response, “My mother used to tell me not to say anything if I can’t say something nice!” Given that the Dow Jones Industrial Average is 10,000 points higher four-plus years later, we doubt the performance story is any different today.

Certainly, we realize that one shouldn’t throw stones when dwelling in a glass house, and we concede that we have endured every significant market decline in our 46 years, yet the watchdog has had nice things to say about The Prudent Speculator on many occasions. As we have long believed that time in the market trumps market timing and we have always hewed the advice of Charlie Munger, “The first rule of compounding is to never interrupt it unnecessarily,” we have participated in every significant market advance since 1977.

Happily, the gains from the advances have dwarfed the losses from the declines, so much so that Value Stocks have enjoyed average annualized returns of 13.6% since the launch of our newsletter, while Dividend Payers have returned 12.2% per annum. The odds obviously have been in favor of the long-term-oriented investor.

We know some market Bulls are taking a victory lap with the major market averages at or near all-time highs, but the average stock is nowhere near its peak. Our aforementioned market timer argues this divergence is a sign that “Rally Tops are Forming,” but we see it as opportunity to sell fairly valued and redeploy into undervalued stocks.

This is especially true as markets have become more volatile. In addition to sometimes-violent individual-stock reactions to Q4 corporate earnings and outlooks, the Federal Reserve has been a catalyst for big moves. Indeed, just last week, Jerome H. Powell & Co. left the Fed Funds rate unchanged in January, but stocks sold off on tempered expectations that the first rate cut is imminent.

Chair Powell said, “I don’t think it’s likely the committee will reach a level of confidence by the time of the March meeting, but that’s to be seen.” Nothing wrong with that in our view, as the significantly better-than-expected 353,000 new jobs created last month added to the prospects for an economic soft landing, with the latest estimate of Q1 real (inflation-adjusted) U.S. GDP growth standing at a robust 4.2%. Hard to complain about a favorable economic backdrop, and the likelihood of lower interest rates later in the year, especially when TPS Portfolio sports a very reasonable forward P/E ratio near 14. We’ll leave the market forecasting to the crystal ball readers, as we simply stay the usual course, continuing to execute our time-tested, buy-and-harvest Value strategy.

“There are two kinds of forecasters: those who don’t know and those who don’t know they don’t know.” — John Kenneth Galbraith

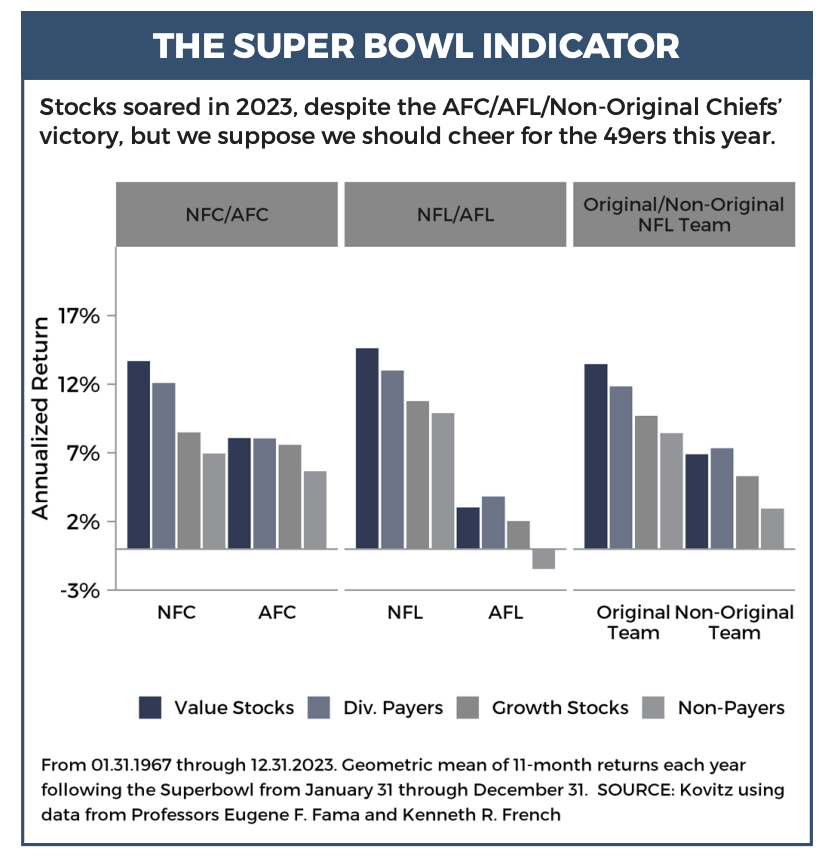

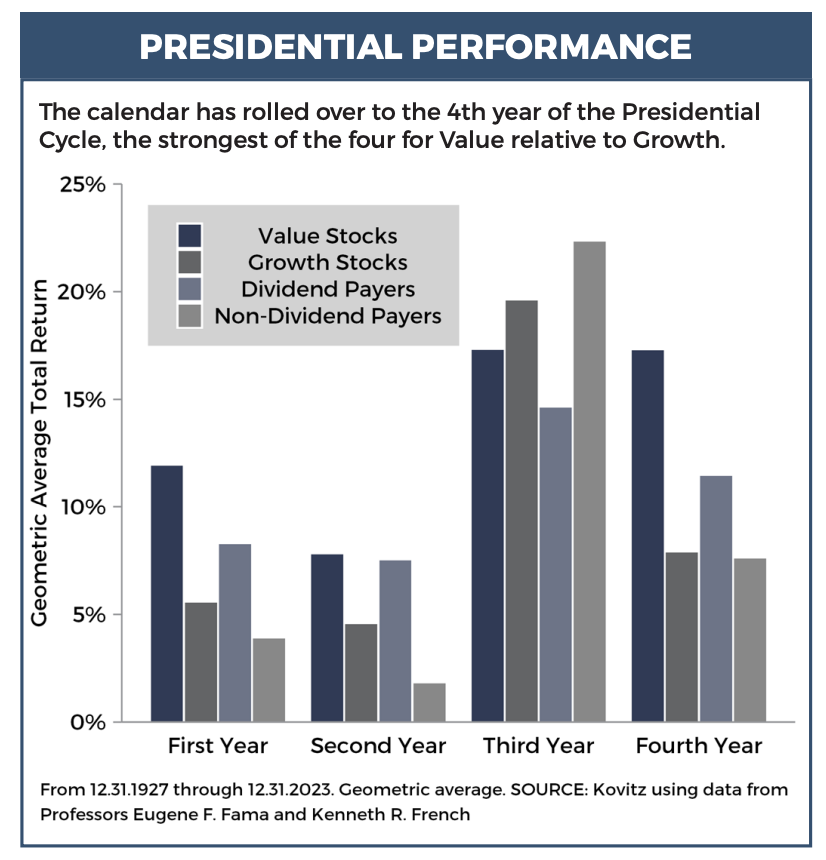

Graphic Detail: Regional Banks, The Super Bowl Indicator and Presidential Performance

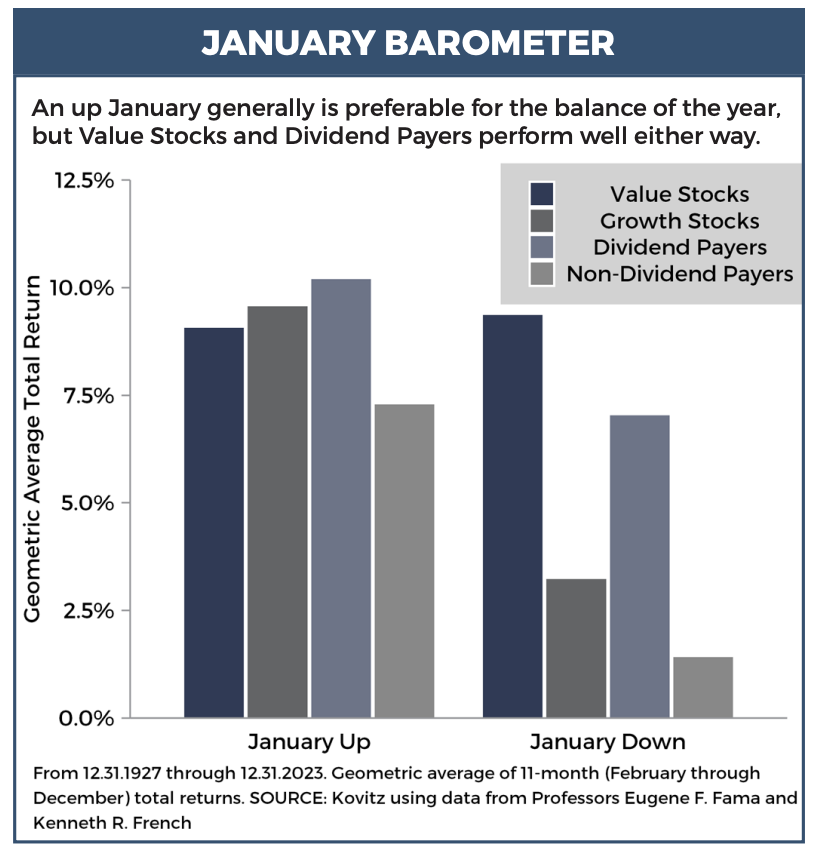

As January Goes…

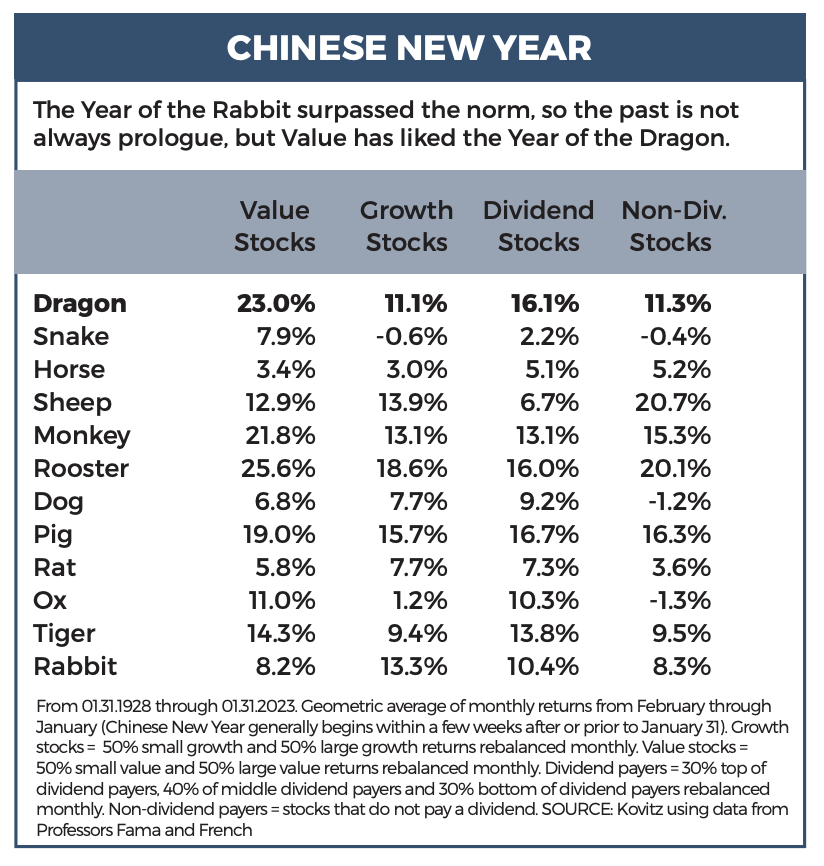

With stocks experiencing positive returns in the first month of 2024, the January Barometer would argue for stronger-than-usual performance over the balance of the year. Of course, the past is merely a guide and not the gospel as stocks rallied sharply last year, in line with Presidential 3rd Years, even as the Kansas City Chiefs Super Bowl LVII victory and the Year of the Rabbit in the Chinese Zodiac might have suggested otherwise. Of course, no matter the calendar study, almost every review of the historical data favors Value-oriented strategies.

Graphic Detail

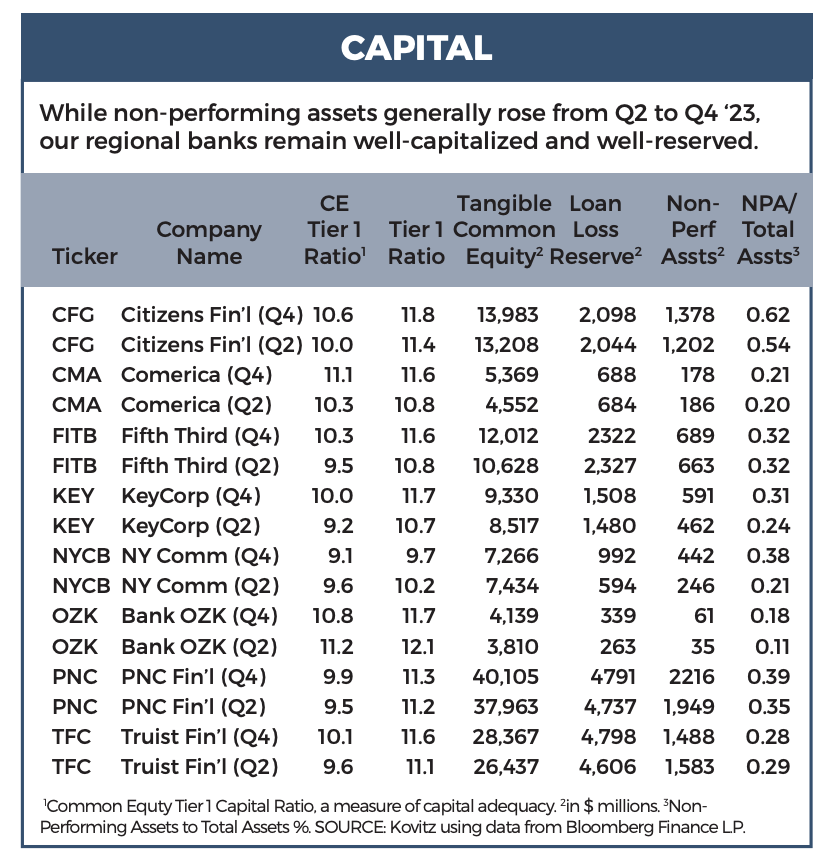

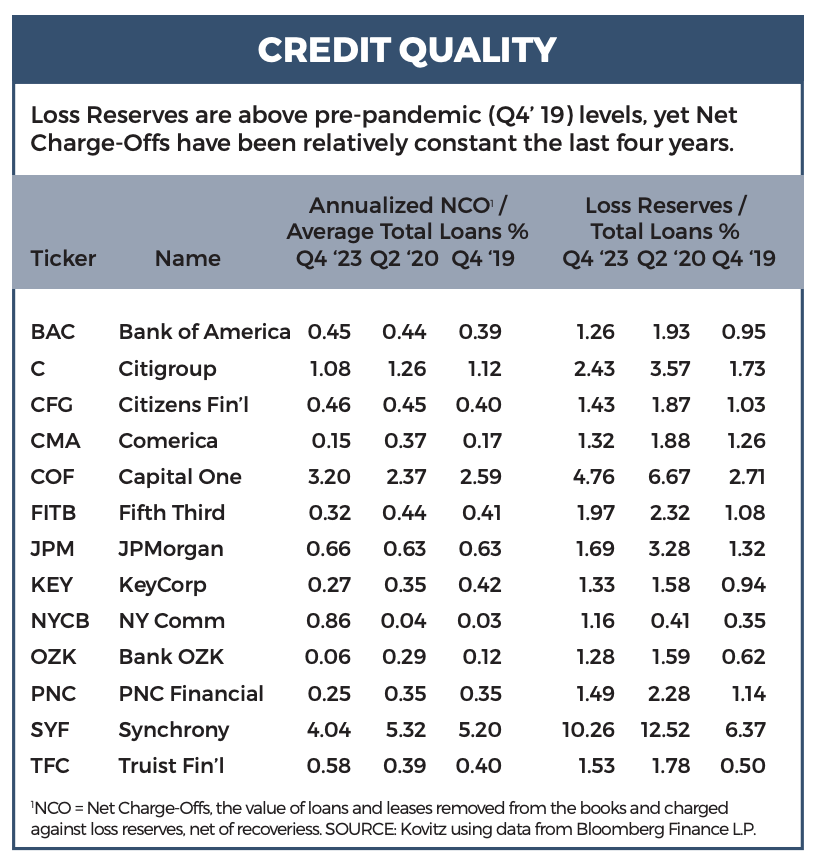

Regional Banks

While Citizens Financial Group CEO Bruce Van Saun argued last week, “For the most part, everything’s in the rear-view mirror now, so things are starting to feel more normal,” traders ran for the regional bank exits once again as January was ending. Signature Bank was one of the culprits 10 months ago when it joined Silicon Valley Group, First Republic and Credit Suisse on the scrap heap, and that New York-based institution was again responsible for another run on the bank stocks.

Readers will recall that New York Community Bank with the help of Uncle Sam last March agreed to assume about $36 billion of liabilities (including $34 billion of deposits) to acquire $38 billion of assets (including $25 billion of cash) from failed Signature Bank. NYCB CEO Thomas Congemi said at the time, “This transaction continues our transformation from a predominantly multi-family lender to a diversified full-service commercial bank.”

The move also pushed NYCB into the big leagues (Category IV Bank), with Mr. Congemi dropping a bombshell revelation (as far as short-sighted traders were concerned) on Jan. 31, “During the fourth quarter, we took decisive actions to build capital, reinforce our balance sheet, strengthen our risk management processes, and better align ourselves with the relevant bank peers. We significantly built our reserve levels by recording a $552 million provision for loan losses, bringing our ACL coverage more in line with these peer banks. In addition, we added on-balance sheet liquidity as we prepare for the enhanced prudential standards that apply to banks with $100 billion or more in total assets. To this end, we are also building capital by reducing our quarterly common dividend to $0.05 per common share.”

Both the loss provision spike and the dividend cut caught analysts by surprise, with fire-sale selling clobbering NYCB shares by 45% in two days and sending the KBW Regional Bank index to an 8% loss. This was the case even as NYCB CFO John Pinto asserted, “We are very comfortable with the early delinquencies that we’re seeing. And those trends have not dramatically jumped up.”

No doubt, the equity markets are in a shoot-first-and-ask questions later mindset on banks, but we continue to believe that capital levels are strong and loan-loss reserves are adequate. Yes, commercial real estate woes will lead to more non-performing assets in the quarters ahead, but just as with the deposit-flight panic last March, we think the latest punishment of regional banks has created long-term opportunities, including for NYCB. We must put up with sometimes-disconcerting volatility, but we like having a few inexpensively priced regional bank stocks in our broadly diversified portfolios.

Recommended Stock List

In this space, we list all of the stocks we own across our multi-cap-value managed account strategies and in our four newsletter portfolios. See the last page for pertinent information on our flagship TPS strategy, which has been in existence since the launch of The Prudent Speculator in March 1977.

Readers are likely aware that TPS has long been monitored by The Hulbert Financial Digest (“Hulbert”). As industry watchdog Mark Hulbert states, “Hulbert was founded in 1980 with the goal of tracking investment advisory newsletters. Ever since it has been the premiere source of objective and independent performance ratings for the industry.” For info on the newsletters tracked by Hulbert, visit: http://hulbertratings.com/since-inception/.

Keeping in mind that all stocks are rated as “Buys” until such time as we issue an official Sales Alert, we believe that all of the companies in the tables on these pages trade for significant discounts to our determination of long-term fair value and/or offer favorable risk/reward profiles. Note that, while we always seek substantial capital gains, we require lower appreciation potential for stocks that we deem to have more stable earnings streams, more diversified businesses and stronger balance sheets. The natural corollary is that riskier companies must offer far greater upside to warrant a recommendation. Further, as total return is how performance is ultimately judged, we explicitly factor dividend payments into our analytical work.

While we always like to state that we like all of our children equally, meaning that we would be fine in purchasing any of the 100+ stocks, we remind subscribers that we very much advocate broad portfolio diversification with TPS Portfolio holding more than eighty of these companies. Of course, we respect that some folks may prefer a more concentrated portfolio, however our minimum comfort level in terms of number of overall holdings in a broadly diversified portfolio is at least thirty!

TPS rankings and performance are derived from hypothetical transactions “entered” by Hulbert based on recommendations provided within TPS, and according to Hulbert’s own procedures, irrespective of specific prices shown within TPS, where applicable. Such performance does not reflect the actual experience of any TPS subscriber. Hulbert applies a hypothetical commission to all “transactions” based on an average rate that is charged by the largest discount brokers in the U.S., and which rate is solely determined by Hulbert. Hulbert’s performance calculations do not incorporate the effects of taxes, fees, or other expenses. TPS pays an annual fee to be monitored and ranked by Hulbert. With respect to “since inception” performance, Hulbert has compared TPS to 19 other newsletters across 62 strategies (as of the date of this publication). Past performance is not an indication of future results. For additional information about Hulbert’s methodology, visit: http://hulbertratings.com/methodology/.

Portfolio Builder

Each month in this column, we highlight 10 stocks with which readers might populate their portfolios: Alexandria RE (ARE), General Motors (GM), MetLife (MET) and seven others.