Warren Buffett, the legendary investor and fan of value stocks, offered up the following advice in 1986 when the Dow Jones Industrial Average was south of 2000, “Occasional outbreaks of those two super-contagious diseases, fear and greed, will forever occur in the investment community. The timing of these epidemics will be unpredictable. And the market aberrations produced by them will be equally unpredictable, both as to duration and degree. Therefore, we never try to anticipate the arrival or departure of either disease. Our goal is more modest: We simply attempt to be fearful when others are greedy, and to be greedy only when others are fearful.”

Obviously, with the Dow above 30000 today, the long-term trend for equities has been significantly higher, especially if dividends and their reinvestment are included, though there have been plenty of scary sell-offs along the way.

SILICON VALLEY BANK – OY VEY!

The year’s positive return for the S&P 500 index was temporarily undone in March by huge disruption in the Financials sector, which ended up spilling into virtually all corners of the investment world. While cracks formed very quickly and a full post-mortem is not yet complete, the damage has been significant. Per Bloomberg, investors and depositors tried to pull a whopping $42 billion from Silicon Valley Bank (SIVB) on March 9 in a colossal run on the bank, which was triggered by a crisis in confidence after Silicon Valley Bank’s management disclosed that the company sold $21 billion of available-for-sale securities, realizing a $1.9 billion loss, and announced a proposed public offering of $1.25 billion of common stock and another $500 million of preferred stock.

To be sure, with the benefit of 20-20 hindsight, Silicon Valley was incredibly reckless, given that management poured billions of dollars into long-term mortgage-backed securities and municipal bonds with minimal interest rate hedging as assets literally tripled during the Pandemic. The $91 billion (cost) of securities had an unrealized loss of $15 billion or so at the end of 2022, but regulatory requirements did not necessitate a write down as the assets arguably had minimal credit risk and they were intended to be held to maturity.

As such, there would not have been a liquidity issue if everyone wasn’t pounding on the proverbial doors demanding their money back. And it is highly unlikely that depositors would have been heading for the exits if they had the benefit of FDIC insurance, but sadly $151.5 billion of deposits in U.S. offices exceeded the FDIC insurance limit and $13.9 billion of foreign deposits had no backstopping from Uncle Sam. Total deposits showing on the balance sheet at the end of 2022 were $173.1 billion, meaning that a massive percentage (more than 95%) of the total had plenty of incentive to pull money out of SIVB.

THERE CAN BE RISK WITH MORTGAGE-BACKED SECURITIES

Happily, few banks in this country look like SIVB and we think the issues in play there are very much isolated. We do not know of any other bank that held the lion’s share of its assets in unhedged 10-years-or-longer-to-maturity mortgage-backed securities (MBS), while operating with a massively uninsured deposit base made up of a set of customers across the private equity/venture capital landscape with very short-term cash needs at a time when capital committed to the space had dried up.

Contrast this with most regional banks across the country (especially those in our ValuePlus and Small-Mid Dividend Income portfolios), whose depositors are typically a highly diverse group of individuals and businesses (the majority of whom tend to be substantially protected by FDIC insurance) and that we expect are unlikely to uproot their day-to-day operating funds.

Despite our arguments that the SIVB situation is idiosyncratic, we realize that the breathtaking run-on-the-bank has led to plenty of consternation for bank-stock investors in particular and the equity markets in general. Naturally, comparisons have been made to the collapse of Lehman Brothers and Washington Mutual during the Great Financial Crisis, but we believe that banks are far better capitalized these days.

THE FEDERAL RESERVE TRYING TO ARREST THE DOMINO EFFECT

Next to fall was Signature Bank. Spooked by the quick demise of SIVB, a large proportion of uninsured deposits and high exposure to crypto assets, customer withdrawal requests exceeded $10 billion on March 10. The FDIC stepped in two days later, putting the bank into receivership. Signature had 40 branches in five states with $110.4 billion of assets and $88.6 billion of deposits.

Obviously, we prefer not to have a rerun of the Great Financial Crisis, but that seems very unlikely after the following from the Department of the Treasury, Federal Reserve and FDIC on the afternoon of Sunday March 12:

Today we are taking decisive actions to protect the U.S. economy by strengthening public confidence in our banking system. This step will ensure that the U.S. banking system continues to perform its vital roles of protecting deposits and providing access to credit to households and businesses in a manner that promotes strong and sustainable economic growth.

After receiving a recommendation from the boards of the FDIC and the Federal Reserve, and consulting with the President, Secretary Yellen approved actions enabling the FDIC to complete its resolution of Silicon Valley Bank, Santa Clara, California, in a manner that fully protects all depositors. Depositors will have access to all of their money starting Monday, March 13. No losses associated with the resolution of Silicon Valley Bank will be borne by the taxpayer.

We are also announcing a similar systemic risk exception for Signature Bank, New York, New York, which was closed today by its state chartering authority. All depositors of this institution will be made whole. As with the resolution of Silicon Valley Bank, no losses will be borne by the taxpayer.

Shareholders and certain unsecured debtholders will not be protected. Senior management has also been removed. Any losses to the Deposit Insurance Fund to support uninsured depositors will be recovered by a special assessment on banks, as required by law.

Finally, the Federal Reserve Board on Sunday announced it will make available additional funding to eligible depository institutions to help assure banks have the ability to meet the needs of all their depositors.

The U.S. banking system remains resilient and on a solid foundation, in large part due to reforms that were made after the financial crisis that ensured better safeguards for the banking industry. Those reforms combined with today’s actions demonstrate our commitment to take the necessary steps to ensure that depositors’ savings remain safe.

Certainly, making all depositors whole at Silicon Valley and Signature, included those who were uninsured, is powerful support against further runs on banks, while the tools provided well-capitalized regional banks allows them to handle sizable near-term deposit outflows.

DEBIT SUISSE

Even though the regulators’ actions were swift and deliberate, investors and depositors appeared unconvinced the possibility for disaster was truly in the rear-view mirror. On Thursday, March 16, embattled European banking giant Credit Suisse said it would borrow up to 50 billion Swiss francs ($54 billion) from the Swiss Central bank in an effort to shore up its liquidity. Then, three days later a hastily arranged shotgun marriage was orchestrated in which rival UBS agreed to buy Credit Suisse for $3.25 billion in stock, with the Swiss National Bank providing 100 billion Swiss francs in liquidity assistance.

The demise of Credit Suisse was extraordinary, with Swiss President Alain Berset saying it was impossible to restore confidence in the company and Swiss Finance Minister Karin Keller-Sutter stating, “The takeover plan will offer greater stability both in Switzerland and internationally.” Swiss National Bank President Thomas Jordan further asserted, “It was indispensable that we acted quickly and find a solution as quickly as possible, given that Credit Suisse is a systemically important bank.”

While many will argue that Credit Suisse was mismanaged, it really was a crisis of confidence that triggered the collapse as accelerating deposit outflows were cited as the core reason, just as was the case with Silicon Valley and Signature banks. Speaking of that duo, Janet Yellen explained in March, “No matter how strong capital and liquidity supervision are, if a bank has an overwhelming run that’s spurred by social media so that it’s seeing deposits flee at that pace, a bank can be put in danger of failing.”

FRC FOLDS AND THE TREASURY TRIES TO SHORE UP THE SYSTEM

That in mind, the Treasury Secretary on March 16 helped orchestrate a deposit infusion into West Coast regional bank First Republic (FRC), whose concentration of high-net-worth customers had contributed to an uninsured deposit balance of $119.5 billion (over two-thirds of total deposits) as of December 31, 2022, a significant amount of which were demand deposits.

With worries about a run on First Republic growing, a consortium of the nation’s biggest banks and some of the largest regional banks cooperated in a remarkable show of unity to try to stem depositor panic by infusing $30 billion of deposits into FRC from their own balance sheets. The concerted effort to shore up America’s banks was evident in the following press release on March 16:

Bank of America, Citigroup, JPMorgan Chase and Wells Fargo announced they are each making a $5 billion uninsured deposit into First Republic Bank. Goldman Sachs and Morgan Stanley are each making an uninsured deposit of $2.5 billion, and BNY-Mellon, PNC Bank, State Street, Truist and U.S. Bank are each making an uninsured deposit of $1 billion, for a total deposit from the eleven banks of $30 billion. This action by America’s largest banks reflects their confidence in First Republic and in banks of all sizes, and it demonstrates their overall commitment to helping banks serve their customers and communities. Regional, midsize and small banks are critical to the health and functioning of our financial system.

Following the receiverships of Silicon Valley Bank and Signature Bank, there were outflows of uninsured deposits at a small number of banks. America’s financial system is among the best in the world, and America’s banks – large, midsize and community banks – do an extraordinary job serving the banking needs of their unique customers and communities. The banking system has strong credit, plenty of liquidity, strong capital and strong profitability. Recent events did nothing to change this.

The actions of America’s largest banks reflect their confidence in the country’s banking system. Together, we are deploying our financial strength and liquidity into the larger system, where it is needed the most. Smaller- and medium-sized banks support their local customers and businesses, create millions of jobs and help uplift communities. America’s larger banks stand united with all banks to support our economy and all of those around us.

While the numbers on deposit flows are not known, it is presumed that most of the banks involved have been beneficiaries of the banking crisis, at least in terms of new deposits heading their way. Given that we own a number of the consortium’s 11 banks, we see the ability to step up to the table as a positive sign of their own financial strength.

We are not suggesting the banking sector is in better shape today than it was at the start of the year, and we will continually update our thinking as greater regulation and stronger capital requirements, potential supply and demand headwinds for lending, constrained loan supply and greater non-performing assets are likely byproducts of the bank mess. However, we agree with Ms. Yellen and Federal Reserve Chair Jerome H. Powell who said on March 19, “The capital and liquidity positions of the U.S. banking system are strong, and the U.S. financial system is resilient.”

BANKS RIDE THE ROLLER-COASTER

It feels like we’ve been on the Coney Island Cyclone as bank stock investors have had to be strapped in on a roller-coaster ride of late, with financial stocks especially hard-hit in March and the Value indexes taking it on the chin. The average stock in the S&P 500 index suffered a total return of -8.5% in the seven-plus weeks between the end of January and March 23. Stocks in the broad-based Russell 3000 index averaged a loss of 12.8%, close to the 13.8% loss experienced by constituents of the Russell 3000 Value subset. Of course, there is a much larger weight in Financials in the Russell 3000 Value index than in the S&P 500 or the Russell 3000, which means it has been tough going recently for those tracking the oft-cited market weight indexes.

Certainly, we understand that many will see the proverbial glass as half empty in the attempt to rescue First Republic and the Credit Suisse fire-sale, and we won’t be surprised to see bank stocks come in for further rounds of selling as the situation evolves, with the overall market likely dragged down in the process.

Such was the case on Fed Day (March 22) when a post-FOMC-announcement equity-market rally was reversed when Ms. Yellen testified on Capitol Hill, “I have not considered or discussed anything having to do with blanket insurance or guarantees of deposits.”

The Treasury Secretary was queried about increasing protections above the current FDIC-insurance limit of $250,000, but a permanent change would require Congressional approval. She concluded, “This is not something we have looked at. It’s not the right time to determine if the limit should be raised.”

To be sure, it was not clear if Ms. Yellen was referring to a temporary or permanent change in the FDIC cap, but bank stocks bore the brunt of the selling when she added, “It’s important to be clear: Shareholders and debtholders of the failed banks are not being protected by the government.”

Of course, the day prior, financial stocks soared when Ms. Yellen spoke at the American Bankers Association’s Washington DC Summit, with the market heartened when she proclaimed, “The situation is stabilizing. And the U.S. banking system remains sound. The Fed facility and discount window lending are working as intended to provide liquidity to the banking system. Aggregate deposit outflows from regional banks have stabilized.”

The Secretary added, “Our intervention was necessary to protect the broader U.S. banking system. And similar actions could be warranted if smaller institutions suffer deposit runs that pose the risk of contagion.”

That last bit suggested to many that measures would be taken to protect uninsured depositors if necessary, which seemingly was what Ms. Yellen confirmed again on March 23, when she testified in front of a House Appropriations subcommittee.

She stated, “We have used important tools to act quickly to prevent contagion. And they are tools we could use again.” She reminded legislators, “The strong actions we have taken ensure that Americans’ deposits are safe. Certainly, we would be prepared to take additional actions if warranted.”

Most bank stocks rebounded on the affirmation, especially as Fed Chair Powell the day before again asserted, “The banking system is strong, it is sound, it is resilient, it’s well-capitalized.”

Alas, there was another U-Turn that same day when credit-rating agency Moody’s spooked investors by expressing concern of a rising risk that banking-system stress will spill over into other sectors and the U.S. economy, “unleashing greater financial and economic damage than we anticipated.” Moody’s commented, “The risk is that officials will be unable to curtail the current turmoil without longer-lasting and potentially severe repercussions within and beyond the banking sector.”

Still, Moody’s base case is that U.S. officials will “broadly succeed” in the fight to restore confidence in the banking system and contain any new institution-specific issues.

Needless to say, it is a confusing time for investors. However, as Mr. Buffett states, “The future is never clear; you pay a very high price in the stock market for a cheery consensus. Uncertainty actually is the friend of the buyer of long-term values.”

MARKET TURBULENCE ISN’T UNUSUAL

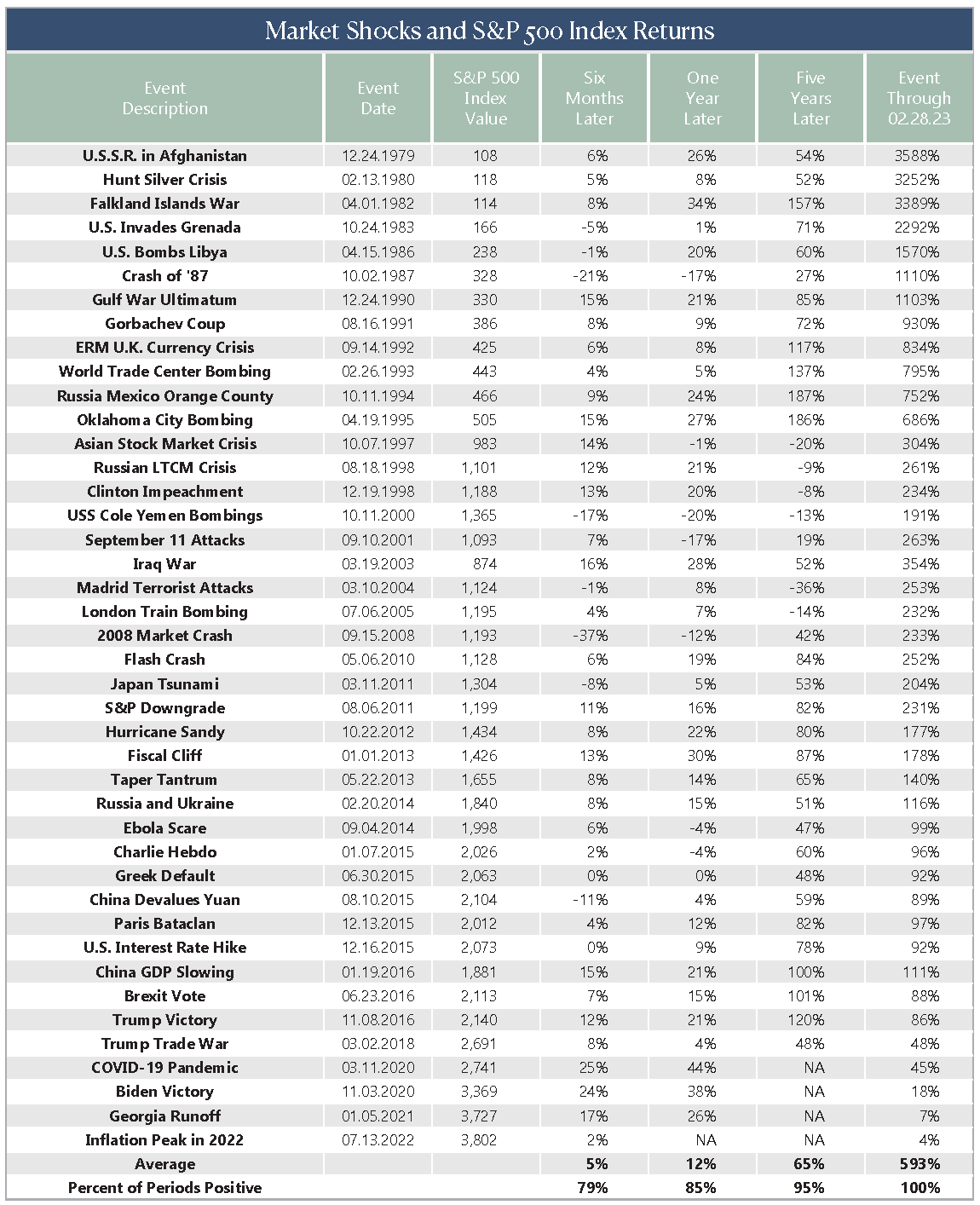

The Prudent Speculator began in March 1977 as a fortnightly epistle, and we’ve been sharing our thoughts with readers ever since. Over the ensuing 46 years and counting, we’ve navigated through a variety of scary headlines (Figure 1), with each frightening event overcome in the fullness of time so much so that long-term returns on equities have been terrific, despite numerous downturns, selloffs, corrections and Bear Markets along the way.

Every disconcerting decline is unique, but they always seem to bring out a slew of doom-and-gloom prognosticators predicting that an even greater plunge is imminent. Of course, nobody has a crystal ball as the future is unknowable, but fear certainly attracts plenty of eyeballs, and many investors feel compelled to act. Given that we think the key to success in stocks is not to get scared out of them, we like the advice offered by Vanguard founder Jack Bogle in August 2011 when S&P downgraded the U.S. credit rating, “Don’t just do something. Stand there!”

BANKING ON VALUE STOCKS

Fear is a powerful emotion, especially in a world that is more interconnected than ever, which is why central bankers have acted with alacrity to insure uninsured deposits at Silicon Valley & Signature, provide additional lending facilities to all banks and “encourage” deposits into First Republic from 11 big U.S. banks.

Only time will tell whether the extensive ammunition expended in the U.S. and across the pond will turn the tide on sentiment, but eventually we think it will. In our view, the potential risks from keeping money on deposit in the domestic banking system continue to be outweighed mightily by the risks and frictions from stuffing bills under the mattress or exchanging for alternative currencies.

For our managed account strategies, we hold an assortment of stocks in the Financials sector, including those in the industry groups Financial Services, Insurance and Banks. The whack to those holdings wasn’t helpful to recent performance, but the broad diversification we have long employed did its job in limiting overall downside. And as we frequently note in these pages, we use market turbulence to make opportunistic changes in our portfolios. We thoroughly enjoy buying things on sale and some of the discounts in the Financials sector lately have been terrific in our view. Of course, the steeper the discount, the more excited we get, so it was tempting to buy large quantities of beaten-down banks. We did make changes, but still are partial to the broad industry and sector diversification we have employed for more than four decades.

STAY THE COURSE

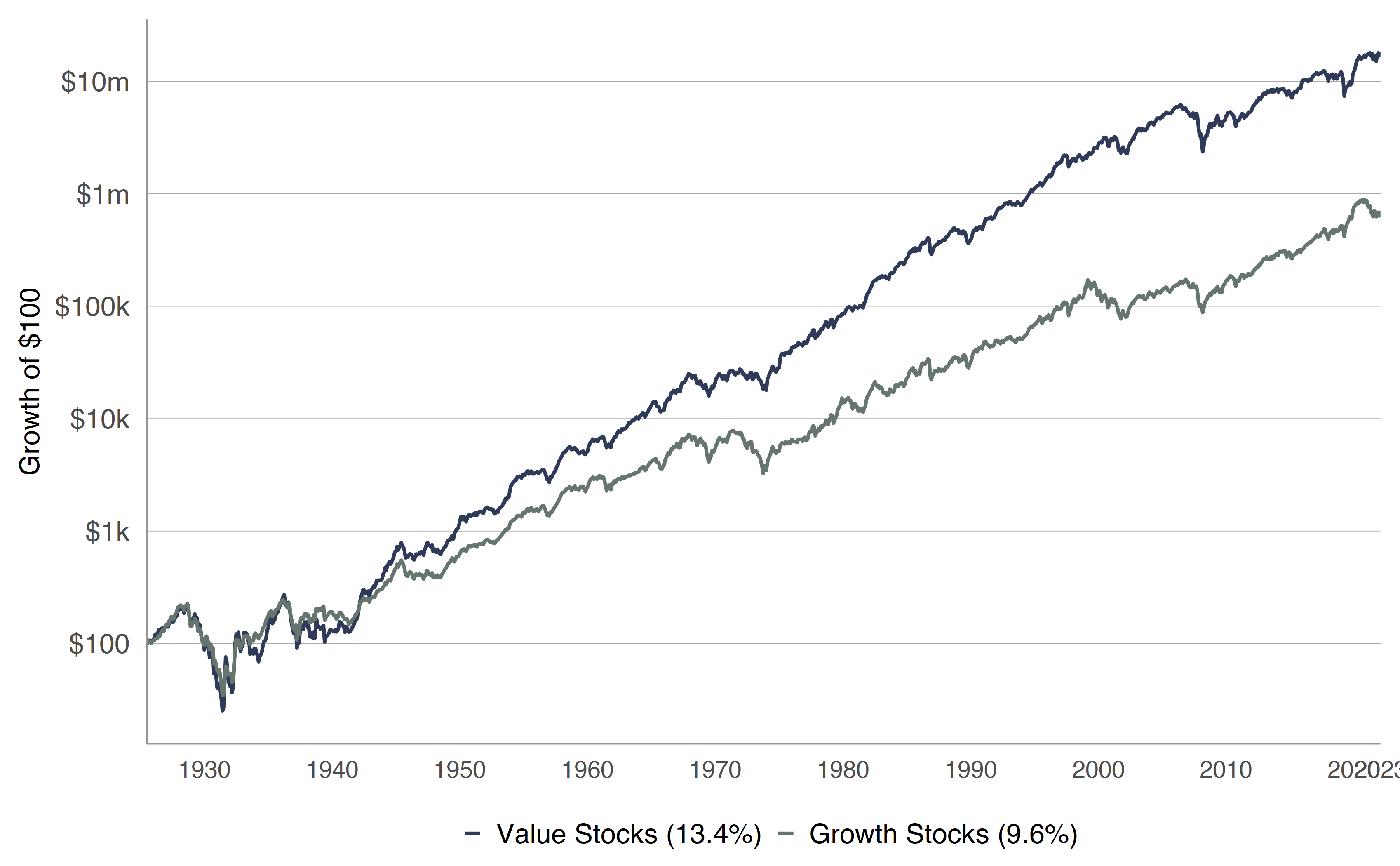

None of this precludes more choppy seas for investors in the near term, but for those who have a long-term time horizon, keeping the faith in equities in general, and Value in particular, through thick and thin historically has been the way to go. Figure 2 shows growth of $100 invested in Value and Growth stocks since 1926. Over that span, the mean annualized return for Value stocks was 13.4%, which is strongly positive despite a high number of punishing periods for individual stocks, the wider sectors and the overall equity market.