The first edition of The Prudent Speculator was published on March 10, 1977, and we have not wavered in our commitment to Value investing, riding the market’s ups and downs while remaining focused on uncovering bargain-priced stocks for their long-term potential. More than 47 years later, we continue to partner with clients to keep them on the wealth-building path.

In 2018, Kovitz acquired AFAM Capital and The Prudent Speculator, expanding our capabilities, widening the opportunity set and improving the value-add for our clients. Through our partnership with Kovitz, we now offer personalized Financial Planning, comprehensive asset allocation counsel and tax strategy analysis (alongside your tax professional). While our equity track record put us on the map, we believe our comprehensive and customized wealth management adds value beyond simple investment returns. For example, this Insight is geared to help minimize your tax bill, thereby keeping more money in your pocket. After all, a dollar saved is a dollar earned.

DEATH AND TAXES

In 1789, Ben Franklin wrote in a letter to French physicist Jean-Baptiste Le Roy, “Our new Constitution is now established, and has an appearance that promises permanency; but in this world nothing can be said to be certain, except death and taxes.”

We suspect Mr. Franklin would be impressed with American ingenuity, and not just of the industrial variety. The miracle of modern medicine and technological advancement has pushed off the inevitability of death, adding nearly two decades to life expectancy since Mr. Franklin penned his letter, while an army of accountants, financial professionals, lawyers and planners spend countless hours seeking ways to (legally!) minimize tax bills for Americans.

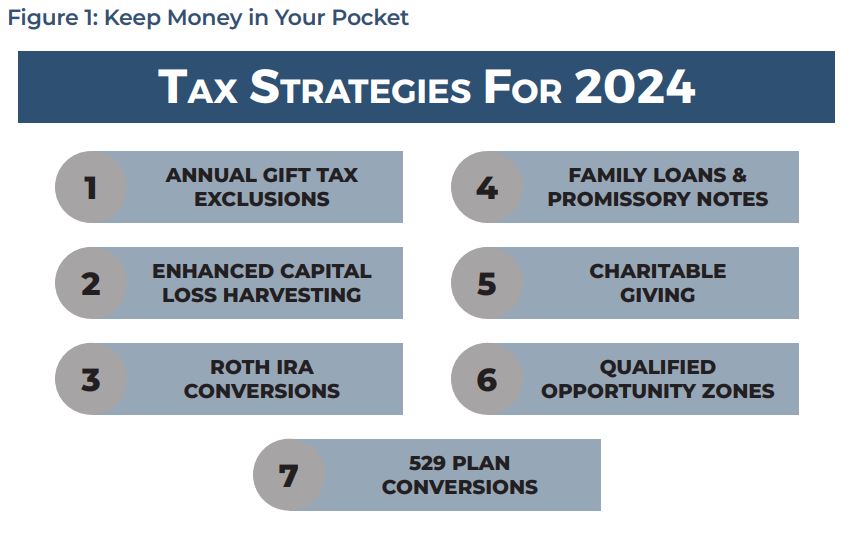

Happily, there are many possibilities to lower tax bills that do not require expensive accounting gymnastics, seven of which we detail in this Insight. Each includes real-world applications, our logic and a set of important considerations.

1. MAXIMIZE THE ANNUAL GIFT TAX EXCLUSION

Overview: The annual gift tax exclusion permits gift-tax-free asset transfers to reduce your estate without affecting your lifetime gift tax exemption.

Example: In 2024, any person can gift up to $18,000 to another individual, free of gift tax. A married couple wanting to gift the maximum amount could combine each of their individual maximum amounts to give $36,000 to as many people as they desire. For example, if a couple has 5 grandchildren, they could give away $180,000 without any gift tax consequences.

Limits/Exceptions: Gifts above $18,000 (or $36,000 as a couple) per recipient will require filing a gift tax return and may reduce your lifetime estate and gift tax exemption. It’s worth noting that direct payment of tuition or medical expenses is not considered a taxable event and is not subject to the annual limitation.

Keep in mind: If your estate is federally taxable, seldom exists a bad time to make annual exclusion gifts.

Next Steps: As always, consult your financial advisor and tax professional before making these annual gifts. In partnership with Kovitz, our team is prepared to assist you in navigating annual gift tax exclusion nuances.

2. ENHANCE CAPITAL LOSS HARVESTING

Overview: Strategically selling investments for a loss to offset capital gains can reduce tax liabilities. Net capital losses can also offset up to $3,000 of the current year’s ordinary income. The unused excess net capital loss can be carried forward to use in subsequent years.

Example: Suppose you bought 1000 shares of Company A stock for $50 per share in January 2024, and the price dropped to $40 per share by December 2024. You also bought 1000 shares of Company B stock for $30 per share in March 2024, and the price rose to $40 per share by December 2024. You decide to sell both stocks before the end of the year.

Here is how you can use capital loss harvesting to offset your capital gains:

You sell 1000 shares of Company A stock for $40 per share, resulting in a capital loss of $10,000 ($40,000 – $50,000).

You sell 1000 shares of Company B stock for $40 per share, resulting in a capital gain of $10,000 ($40,000 – $30,000).

You use the capital loss from Company A to offset the capital gain from Company B, resulting in a net capital gain of $0 ($10,000 – $10,000).

You can expect to pay no capital gains tax on the sale of both stocks, saving you money on your taxes and you may choose to reinvest the proceeds from the sale of both stocks in a similar (but not identical) investment to maintain your portfolio allocation. Of course, you might like Stock A (that had the loss) and you can repurchase it 31 days later without consequences.

Keep in mind: Capital losses harvested must first offset gains of the same type, and the wash-sale rule (selling a security to capture a loss and then buying a similar security back within 30 days) can disallow a loss.

When Not to Use: If realizing the capital loss would not provide a tax benefit due to your income level or there are minimal capital gains to offset. To be sure, those that think the long-term prospects of a specific stock are positive in nature should look elsewhere to harvest losses.

Next Steps: As always, consult your financial advisor and tax professional before harvesting losses. Our team is prepared to assist you in navigating capital loss harvesting.

3. MAKE ROTH IRA CONVERSIONS IN LOW-INCOME YEARS

Overview: Aligning retirement contributions and Roth IRA conversions during low-income years can enhance tax savings. Qualified Roth distributions are tax-free.

Example: A $15,000 conversion from a Traditional IRA to a Roth IRA during a low-income year can provide long-term tax benefits. By converting the money now, you pay taxes at today’s rate, but all future growth within the Roth IRA is tax-free. Roth IRAs are not subject to required minimum distributions when you come of age. A $15,000 conversion today would be subject to federal and/or state taxes, however, if that converted account were to grow to $50,000 in the future, the $50,000 could be tax-free. Some states, such as Illinois, also exclude retirement income (Roth IRA conversions included) from state income taxes.

Keep in mind: Roth conversions are irreversible and if you meet the five-year minimum holding requirement, there are no taxes on withdrawals, unlike a traditional IRA.

When Not to Use: In years when your income is not substantially lower than usual. One should also keep in mind the Tax Cuts and Jobs Act (TCJA) of 2017 is scheduled to sunset at the end of 2025, and if no new law is passed, certain tax brackets will see increases. These changes may alter when or how you utilize Roth conversions.

Next Steps: As always, consult your financial advisor and tax professional before the conversion. Our team is prepared to assist you with Roth IRA conversions.

4. OFFER INTRA-FAMILY LOANS AND PROMISSORY NOTES

Overview: Leveraging intra-family loans can facilitate estate planning and wealth transfer while minimizing taxes.

Example: A parent lends $450,000 to their child for 10 years at the current Applicable Federal Rate (AFR). The child uses the loan to buy stocks and bonds and pays back the parent over time. If the stocks and bonds appreciate in value more than the interest rate charged, there is a benefit from the difference, and the parent will effectively transfer some wealth to the child without using any of their lifetime gift tax exemption. Making this an even stronger strategy, charged interest can be forgiven under the annual gift tax exclusion.

Keep in mind: Strict IRS rules apply, and interest rates must meet or exceed the AFR to avoid gift tax implications.

When Not to Use: If there is a low likelihood of the assets (purchased with the loaned money) outperforming the loan interest rate, or if you need the loaned funds.

Next Steps: Consult your financial advisor, attorney and tax professional before making the loan. Promissory notes will be needed. Our team is prepared to assist you with family loans.

5. AMPLIFLY DEDUCITONS THROUGH CHARITABLE GIVING

Overview: Charitable donations can provide sizable tax deductions, especially for those who itemize, blending philanthropy with tax efficiency.

Example: Gifting $3,000 to a qualified charity, if itemizing deductions, can decrease your taxable income by an equivalent amount. If considering a larger donation, or donations across consecutive years, one might consider setting up a Donor Advised Fund (DAF) to maximize the tax deduction within a single year. A DAF is a public charity program that allows a taxpayer to make fair market value contributions to the fund, and thus avoid capital gains taxes on the appreciated securities contributed to the DAF, while receiving a tax deduction for the contribution. Once the DAF is funded, the taxpayer will then make recommendations for distributing the funds to qualified nonprofit organizations. A DAF is a flexible way to donate over time while enjoying an immediate tax benefit now.

Keep in mind: Deduction limits depend on the type of charity and the taxpayer’s adjusted gross income.

When Not to Use: If you don’t itemize on your tax return, the direct tax benefit will be limited or zero.

Next Steps: Consult your financial advisor and tax professional before making large charitable contributions because you have options. Our team is prepared to assist you with your charitable giving needs.

6. INVEST IN QUALIFIED OPPORTUNITY ZONES

Overview: Investments in Qualified Opportunity Zones (QOZs) can offer significant tax benefits, including deferral of capital gains taxes, as well as the possibility of tax-free growth for investments held over 10 years.

Example: If you invest $50,000 of realized short- or long-term capital gains from selling a business or other asset (such as equities, real estate, real property, or alternatives like art or rare coins) into a QOZ through the end of 2026, you could defer the tax on those gains for 10 years and potentially eliminate taxes on gains accrued from the QOZ investment.

Keep in mind: The tax benefits apply only to capital gains reinvested in QOZs within 180 days of the sale of the original asset. The tax deferral ends on December 31st, 2026, and there are specific requirements around tax reporting. The investor can expect to pay the prevailing tax rates in 2027.

When Not to Use: Liquidity needs impact the attractiveness of QOZ investments, which should be considered long-term in nature. Additionally, investors may not be comfortable with the risks associated with investing in potentially underdeveloped areas.

Next Steps: Consult your financial advisor and tax professional for QOZ opportunities. Our team is prepared to assist if interested.

7. CONVERT 529 PLAN ASSETS TO ROTH IRAS UNDER THE SECURE ACT 2.0

Overview: The SECURE 2.0 Act, part of the Consolidated Appropriations Act of 2023, introduces a transformative option for 529 plan, also known as Qualified Tuition Program, account holders. Beginning this year, it is possible to roll over funds from a 529 plan into a beneficiary’s Roth IRA, offering a new method to manage and utilize extra savings previously earmarked for education expenses.

Example: This change (first offered in 2024) provides a valuable avenue to enhance the utility of your 529 plans, and is especially beneficial for those with remaining funds after educational expenses have been paid out. It introduces opportunities for financial flexibility and tax-advantaged growth for your family.

Keep in mind:

Eligibility: To qualify, the 529 plan must have been open for a minimum of 15 years. Any contributions made within the past five years (and earnings on the contributions) are ineligible to be moved into the Roth IRA. The Roth IRA must be in the name of the beneficiary of the 529 plan. The beneficiary must have earned income. Note: It’s still unclear how 529 plans that have had multiple beneficiaries will be impacted by these rules.

Lifetime Limit: There’s a cap of $35,000 per beneficiary for the total rollover amount.

Annual Limit: The rollover each year is restricted to the lesser of the IRA contribution limit or earned income for that year less any other IRA (traditional or Roth) contributions made by the beneficiary.

Next Steps: While SECURE 2.0 provides increased opportunities for tax savings, everyone’s financial situation is different. As always, consult your financial advisor and a tax professional to understand how this change applies to you. Our team is prepared to assist you in navigating this new option.

Review Your Plans: An evaluation of your existing 529 plans will help determine the potential for rollovers.

Rollover Process: Rollovers must be conducted directly (either plan-to-plan or trustee-to-trustee). Beneficiaries can roll over funds irrespective of their income levels, although the rollover amount should align with the beneficiary’s earned income and Roth contribution limits.

CONCLUSION

The strategies discussed above are general guidelines and there are details and exceptions that might apply to your individual financial situation. We recommend consulting with your tax professional and wealth advisor team to devise solutions tailored to your specific needs.

Through our partnership with Kovitz, our team collaborates to make your wealth work for you. We are committed to ensuring that your comprehensive financial strategy is thoughtful, personalized and effective. For more details about our wealth management and asset management services, kindly reach out to Jason R. Clark, CFA at 949.424.1013 or jclark@kovitz.com.