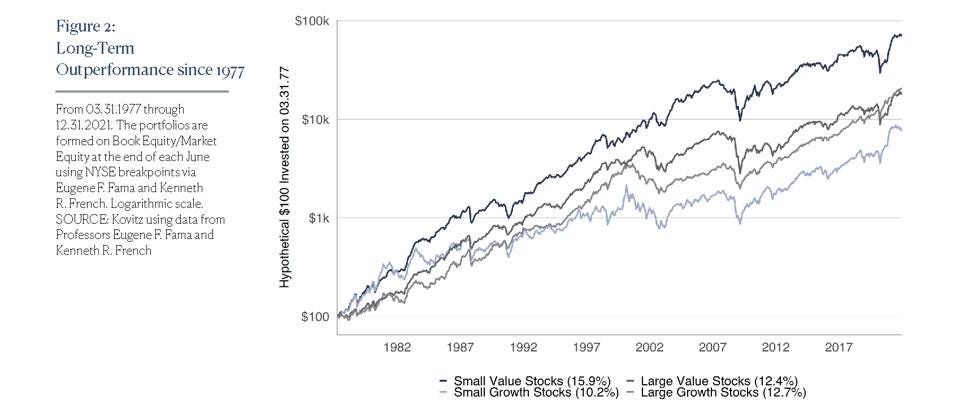

Since the inaugural issue of The Prudent Speculator was published in March 1977, the Small-Cap Value subset of stocks (as determined by portfolios constructed by Professors Eugene F. Fama and Kenneth R. French based on size and book-to-market) have trounced the comparable Growth indexes, even as the horse race between Large Value and Large Growth over the same period has favored the latter by a neck.

Red ink is nothing to celebrate, but losing less in down markets and making more in up markets illustrates why we think there is opportunity in Small-Cap Value. That in mind, we serve up two more inexpensive Small-Cap bargains.

RIDING THE RAILS

Greenbrier is predominately a manufacturer of railcars, even as its servicing division has grown, and the firm has moved further into leasing over the past year.

One of a number of cyclical companies whose stocks have been pummeled on recession fears, GBX trades at a 52-week low, down 45% year-to-date and 50% below its high from March. The company receives little coverage from the analyst community, but 2023 is expected to be a robust year as metal prices recede and Greenbrier works through its backlog to improve volumes.

Since the mid-1980s, when previous CEO Bill Furman co-founded the current iteration of the company, Greenbrier has also expanded to become one of the leading railcar manufacturers in South America and Europe, with operations in Brazil and Poland.

Following an appointment in March, former President Lorie Tekorius officially took the reins from Mr. Furman to become CEO. Ms. Tekorius recently visited the company’s operations in Central Europe, home of one of the world’s largest freight car factories in Caracal, Romania.

She said, “We want to build an internal community within Astra Rail, much stronger and more active than it already is. We are already developing training programs for our employees to offer them the best professional training and we are investing in expanding our business in Romania.“

Europe remains a wild card given the war in Ukraine, but raging petrol costs ought to support rail transport over truck. On this front, Ms. Tekorius added, “We also want to prove to the Romanian society that we are a responsible company that gets involved and supports the European Union’s efforts to support the reduction of carbon emissions. As the only player on the Romanian locomotive and wagon production market, we want to expand the business to be able to respond as best as possible to this endeavor, at the European level.”

The balance sheet carries a bit more debt than in the past, but the average maturity of four years with an average coupon of just 2.9% make the burden bearable.

Shares trade for less than 9 times the drastically reduced 2023 EPS projection and offer a very generous 4.2% dividend yield.

PAPER ASSETS

One of North America’s paper giants, Westrock produces packaging for food, hardware, apparel and other consumer goods. The company’s lineup includes recycled and bleached paperboard, containerboard, consumer and corrugated packaging, and point-of-purchase displays.

Consolidation within the containerboard industry in recent years should support rational production and pricing, as the top 5 producers make up over 75% of capacity, vs. an estimated 43% nearly two decades ago.

Westrock is targeting EBITDA (earnings before interest, taxes, depreciation and amortization) margin growth of around 19% by 2025, propelled by process optimization, innovation, efficiency gains and improved capital allocation decisions.

With fiber-based packaging solutions in 30 countries, Westrock should benefit from long-term tailwinds from e-commerce (via shipping boxes).

While lingering supply-chain issues and an economic slowdown in many parts of the world might be a near-term wet blanket on aggregate demand, WRK produces important products that aren’t easily replaced.

After slashing its dividend during the early part of the pandemic, a rebound in sales has allowed WRK to resume more generous payments, with the current yield at 3.1%, while a 20% decline for the stock just since August makes it very inexpensive in our view, trading for a single-digit forward P/E ratio.

Learn More:

This post was also published on John Buckingham’s Forbes contributor site.

We frequently publish investment-oriented content on our Blog and reach thousands of subscribers through our weekly Market Commentary and monthly Newsletter. Please click here for subscription information.

For more details about our wealth management and asset management services, kindly fill out this Contact Us form and we’ll reach out to you shortly.