The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Regional Banks, Federal Reserve meeting Economic Data, Earnings and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – 6 Purchases for 4 Portfolios

Week in Review – 242nd Worst Week for the Russell 3000 Value Index

Regional Banks – Buffett Argues Deposits are Safe; Latest TPS Special Report; CRE Worries but Diverse Loan Books, Solid Capital Ratios & Strong Credit Quality

Fed Meeting – 25-Basis-Point Hike; Mixed Messaging

Recession – Not the Current Powell or Atlanta Fed Projection, But No Reason to Panic if a Contraction Eventually Occurs

Econ Data – Strong Employment Situation Report; Better-than-Expected ISM Numbers

Earnings – Solid Results from Corporate America

Dividends – Payouts Grow Over Time

Valuations – Stocks Still Reasonably Priced vs. Long-Term Treasuries

Contrarian Sentiment – AAII Even More Pessimistic

Stock News – Updates on sixteen stocks across ten different sectors

Week in Review – 242nd Worst Week for the Russell 3000 Value Index

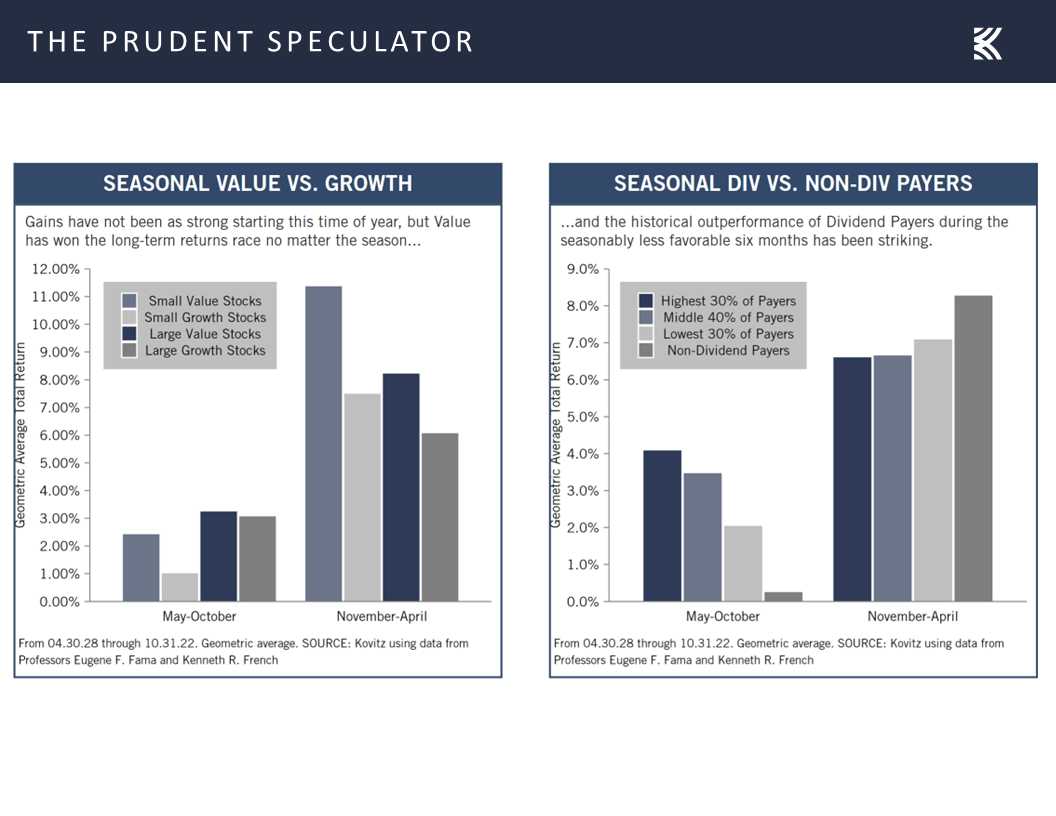

The seasonally less favorable (it is still positive, on average, for Value Stocks and Dividend Payers) May – October period,

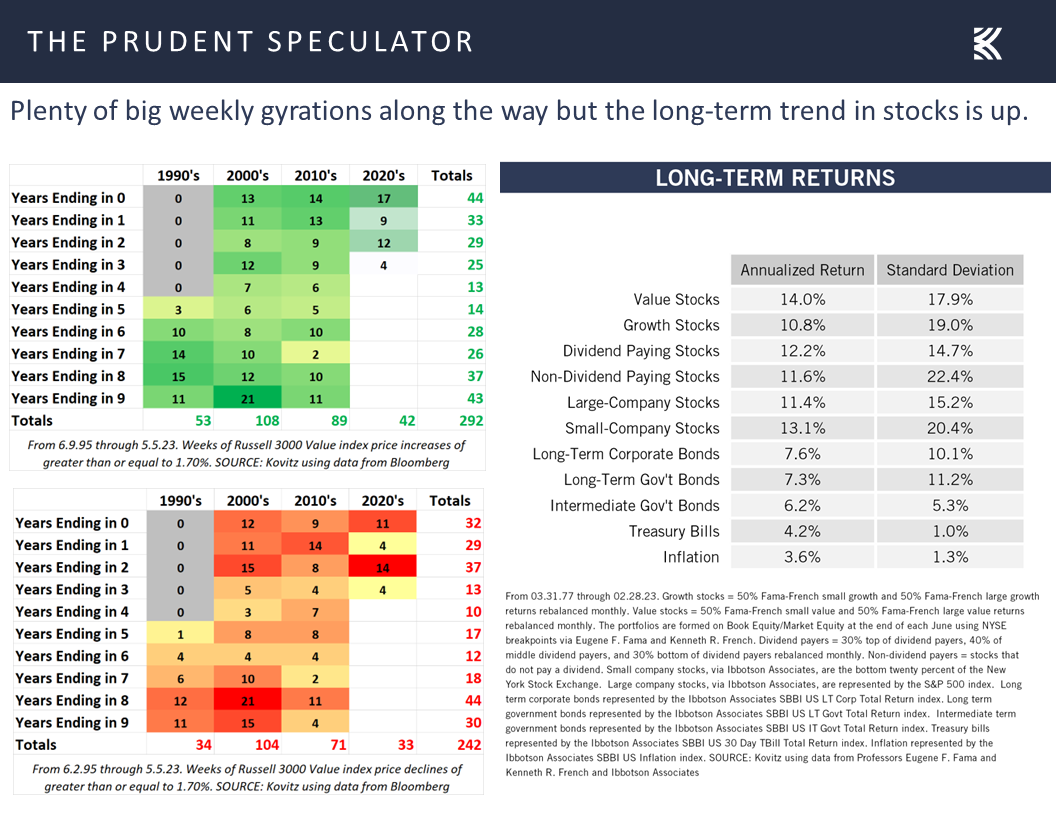

certainly began on an ugly note last week as it took a big rebound on Friday to pare losses on the Russell 3000 Value index to only 1.7% for the five days. No doubt, volatility is normal as the week just ended was the 242nd worst for that index since its creation in 1995. Happily, there have been 292 weeks over the past 28 years with gains of similar or greater magnitude, while long-term average annualized returns for Value stocks since the inception of The Prudent Speculator in 1977 have been terrific.

Regional Banks – Buffett Argues Deposits are Safe; Latest TPS Special Report; CRE Worries but Diverse Loan Books, Solid Capital Ratios & Strong Credit Quality

One of the reasons for the equity market struggles last week was renewed worries about the regional banks. Our latest thoughts on the matter are available here, and we were happy to see the sizable bounce in shares of the regional banks on Friday, even as a one-day respite from the selling hardly a trend makes. Still, it was nice to hear Warren Buffett on Saturday proclaim that deposits are safe, which is in keeping with the facts (as opposed to the fiction put forth by short-sellers as well as several prominent billionaires) thus far that there has not been a systemic run on the bank.

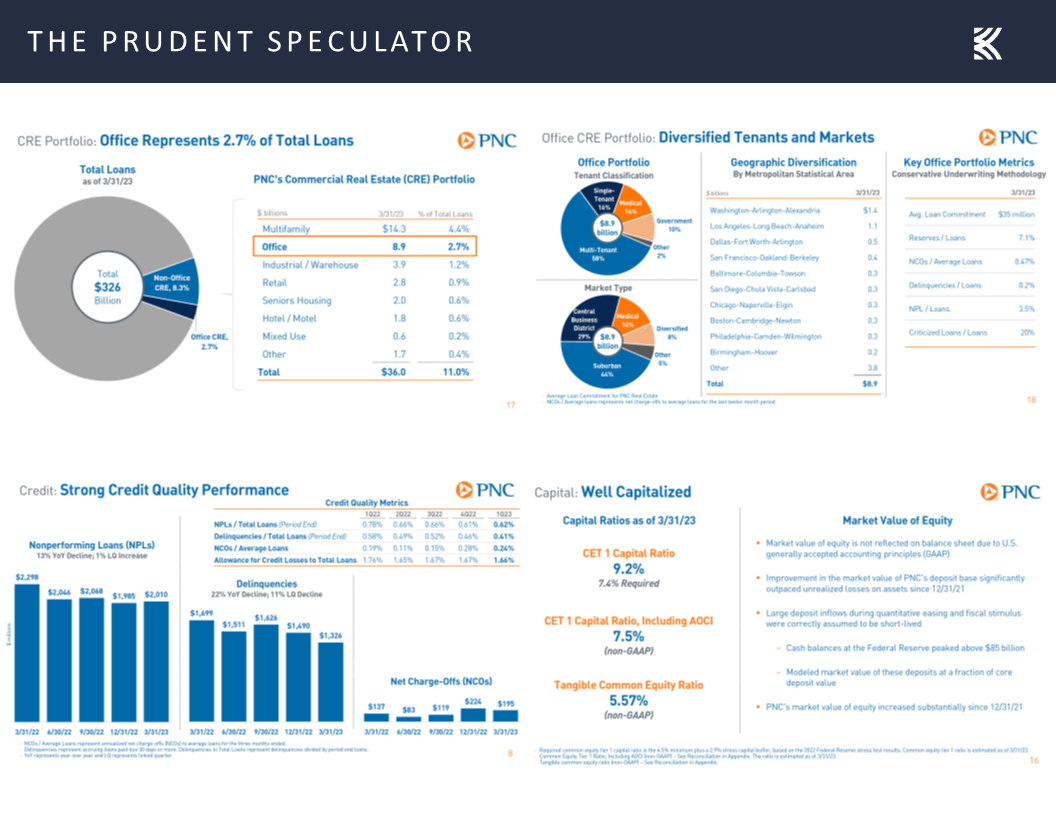

To be sure, the Oracle of Omaha was quick to add that the increase in interest rates we have witnessed over the past year or so is problematic for commercial real estate and we do not deny that non-performing assets on bank balance sheets will rise. However, we are of the mind that the banks we own, like PNC Financial (PNC – $116.18), have broadly diversified loan books, solid capital ratios and strong credit quality. Commercial real estate is 11.0% of PNC’s total loans, with the more worrisome Office category geographically diverse and accounting for 2.7% of total loans.

Fed Meeting – 25-Basis-Point Hike; Mixed Messaging

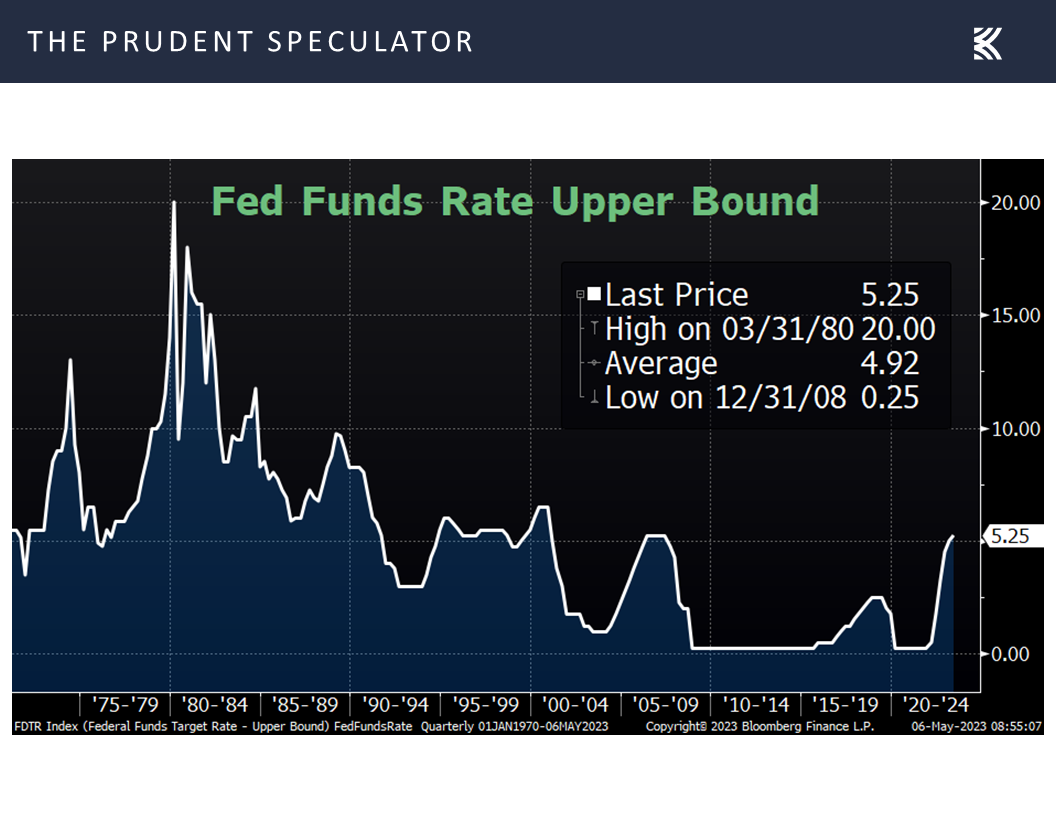

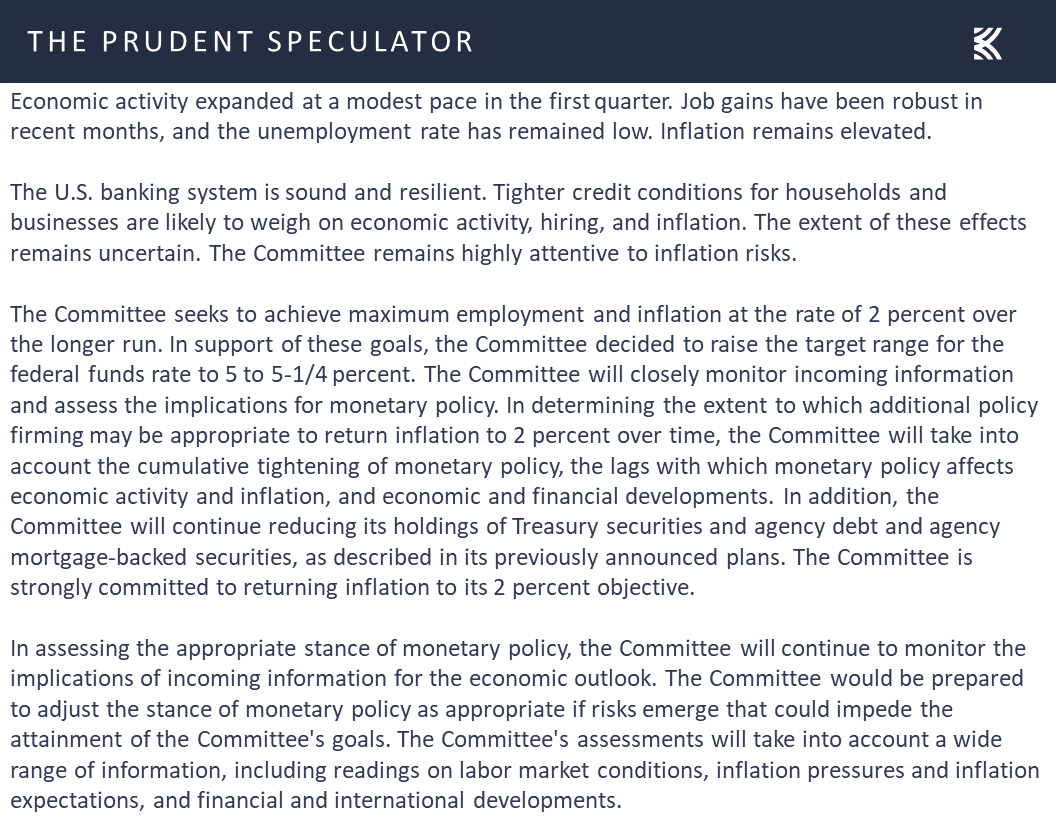

The other market-moving news of the week was the decision on interest rates from the Federal Open Market Committee (FOMC) and Jerome H. Powell’s Press Conference that followed. The fact that the Fed Chair and his colleagues chose to hike their target for the Federal Funds rate by another 25 basis points to a range of 5.00% to 5.25% was not a surprise,

and the equity markets initially did not seem unhappy with the FOMC statement.

The problem for the stock market, at least for two days, was that Mr. Powell was a bit wishy-washy in his Q&A in regard to future interest rate increases. On the one hand, he said, “People did talk about pausing, but not so much at this meeting. We feel like we’re getting closer or maybe even there.” On the other hand, he asserted, “I think that policy is tight, but we are prepared to do more if greater monetary policy restraint is warranted.”

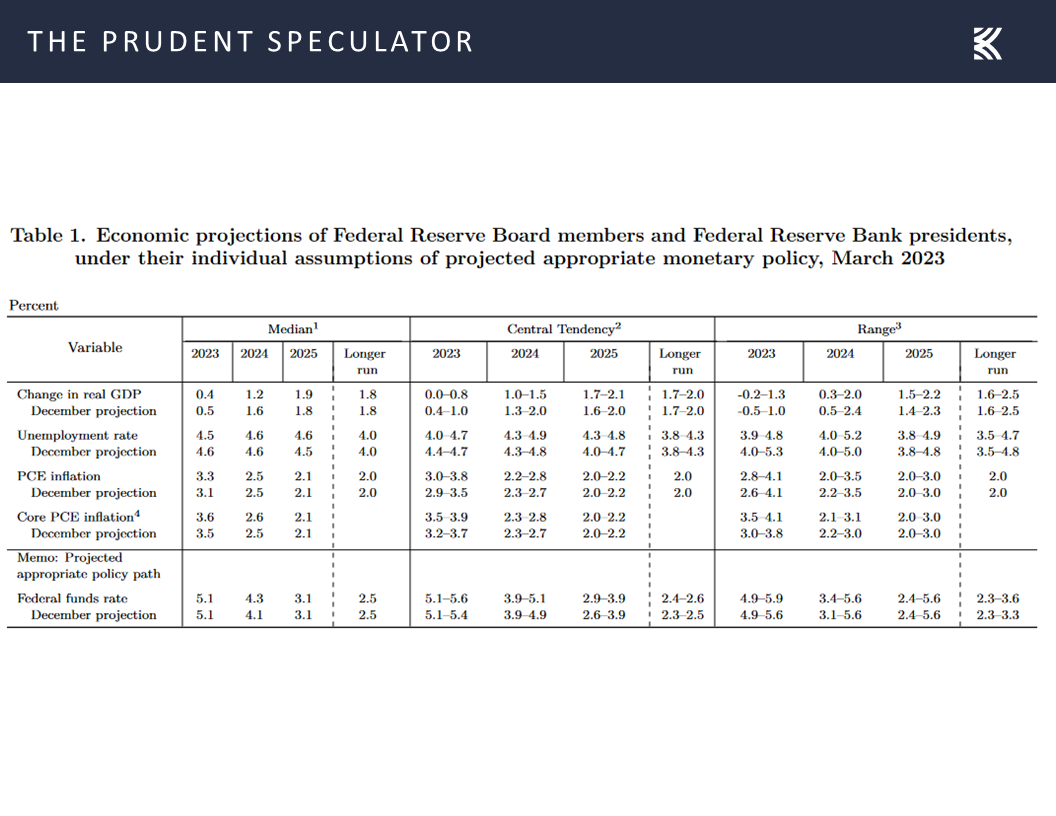

Further, he reminded, “Looking ahead, we will take a data-dependent approach in determining the extent to which additional policy firming may be appropriate,” but the Fed Funds rate is now at the year-end 2023 projection offered in the quarterly economic projections put forth by the Federal Reserve Board members and Federal Reserve Bank presidents back in March.

Recession – Not the Current Powell or Atlanta Fed Projection, But No Reason to Panic if a Contraction Eventually Occurs

Those March projections also called for 0.4% real (inflation-adjusted) GDP growth for 2023, but Chair Powell intimated that updated projections were arguably a bit more pessimistic. He said, “So, broadly, the forecast was for a mild recession, and by that I would characterize as one in which the rising unemployment is smaller than is has been typical in modern era recessions. I wouldn’t want to characterize the staff’s forecast for this meeting. We’ll leave that to the minutes but broadly — broadly similar to that.”

When asked specifically about his own economic forecast, the Chair responded, “The case of avoiding a recession is, in my view, more likely than that of having a recession. But it’s not — it’s not that the case of having a recession is — I don’t rule that out, either. It’s possible that we will have what I hope would be a mild recession.”

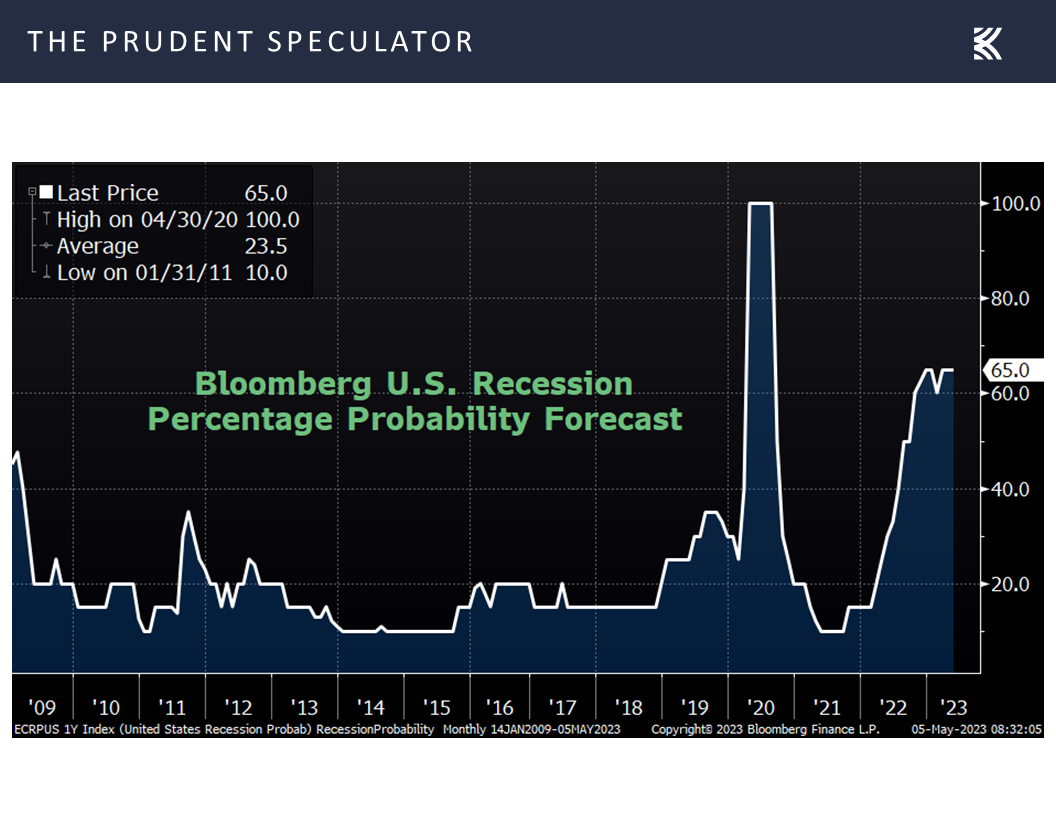

Is it any surprise that famed American Economist Paul Samuelson said, “Economists have predicted nine of the last five recessions?” After all, the current odds of an economic contraction in the next 12 months, as tabulated by Bloomberg, have been at 60% or higher since October,

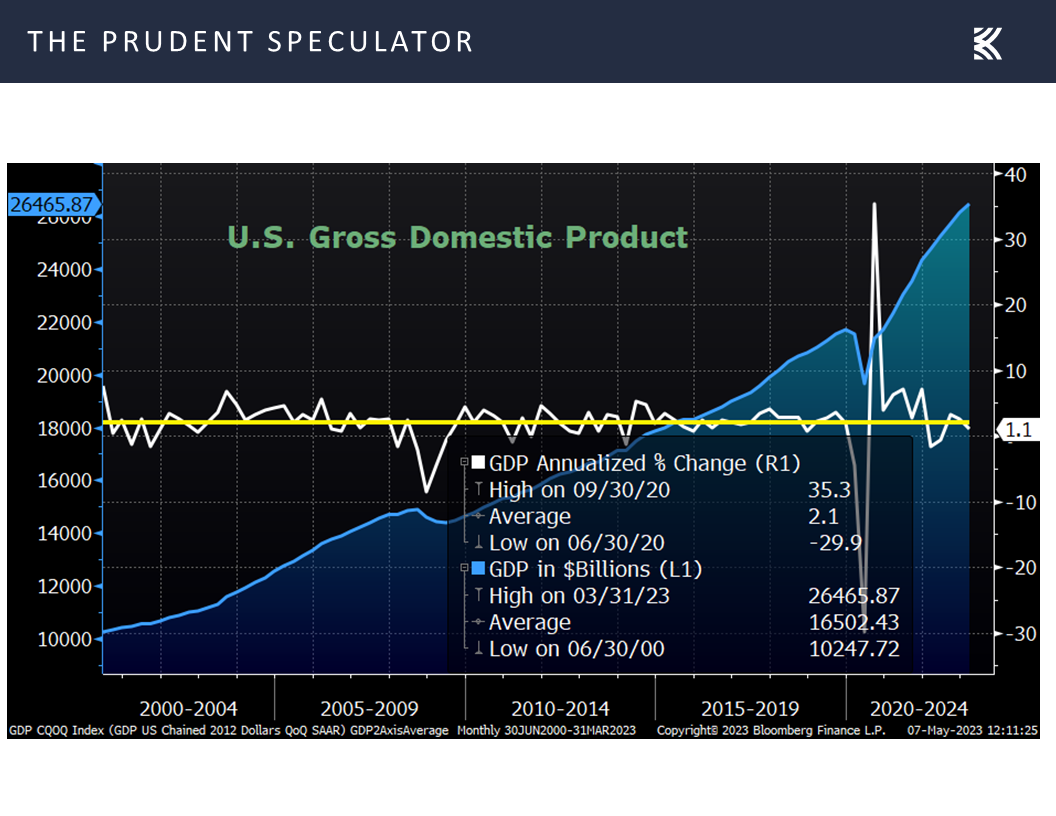

yet real GDP growth came in at 2.6% in Q4 2022 and 1.1% in Q1 2023.

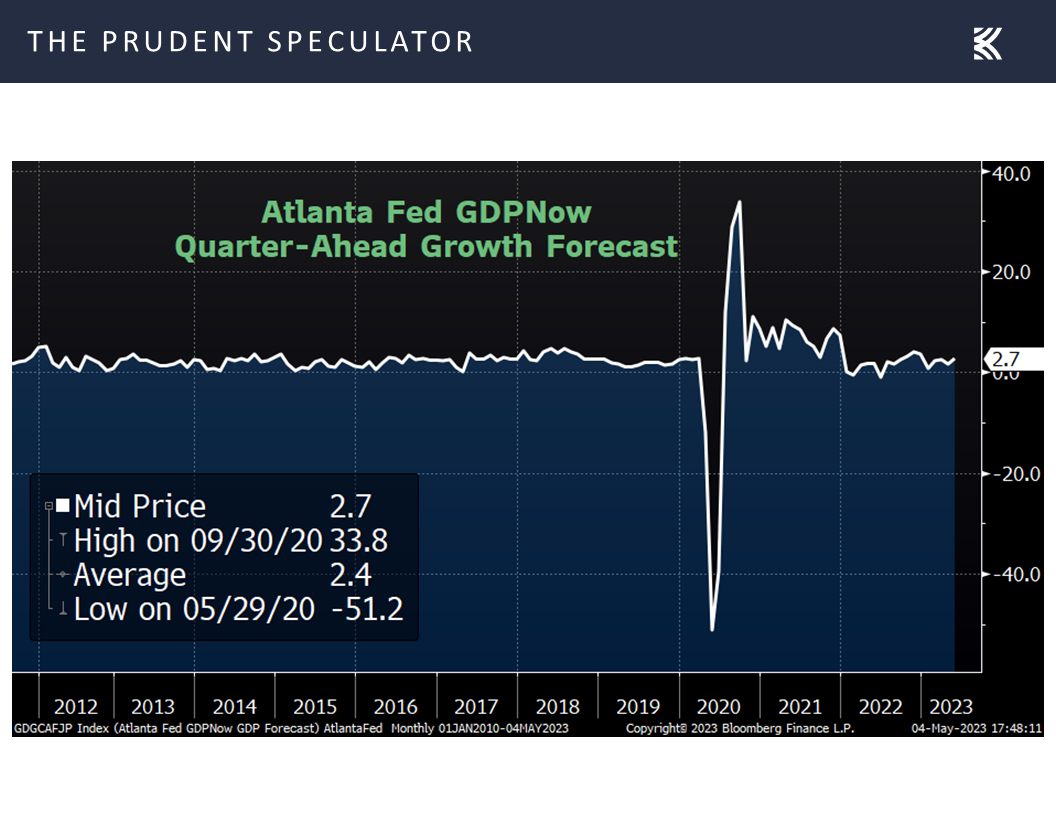

while the current estimate for real Q2 GDP growth from the Atlanta Fed rose last week to 2.7%.

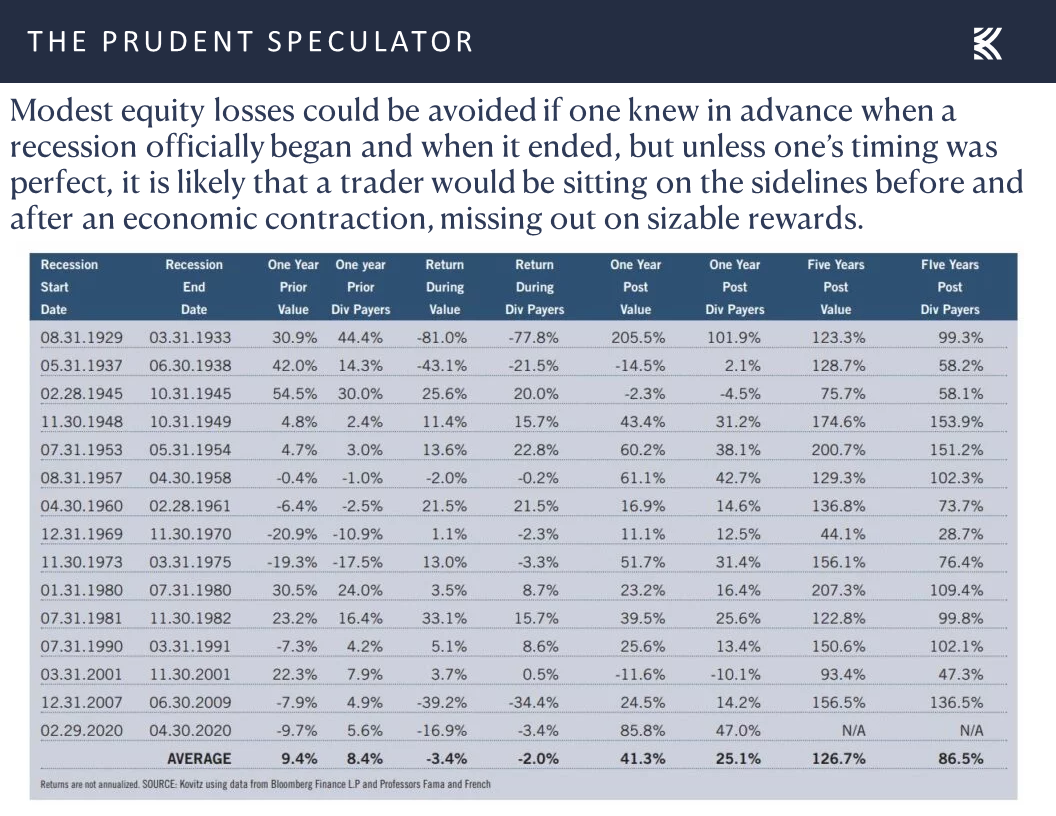

The optimists, including Mr. Powell, could be wrong and a recession may occur, but we do not think that would be reason to abandon Value Stocks and Dividend Payers, or equities in general, even if we could somehow identify the exact beginning and ending of the contraction in advance.

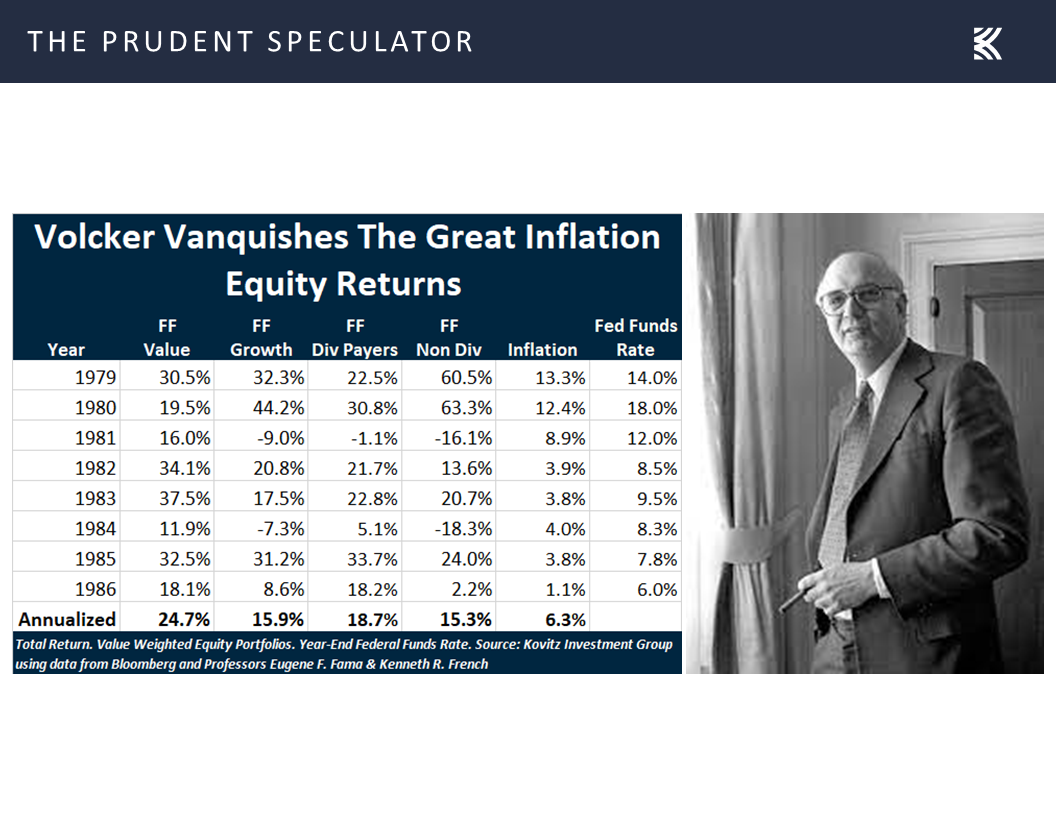

Further, given that Mr. Powell is the first Fed Chair to face the same kind of inflationary pressures as Paul Volcker some 40 years ago, we take comfort in the fantastic equity returns posted under the Volcker Fed from 1979 – 1986, especially as the vanquishing of the Great Inflation included two recessions, one starting in 1980 and another starting in 1981.

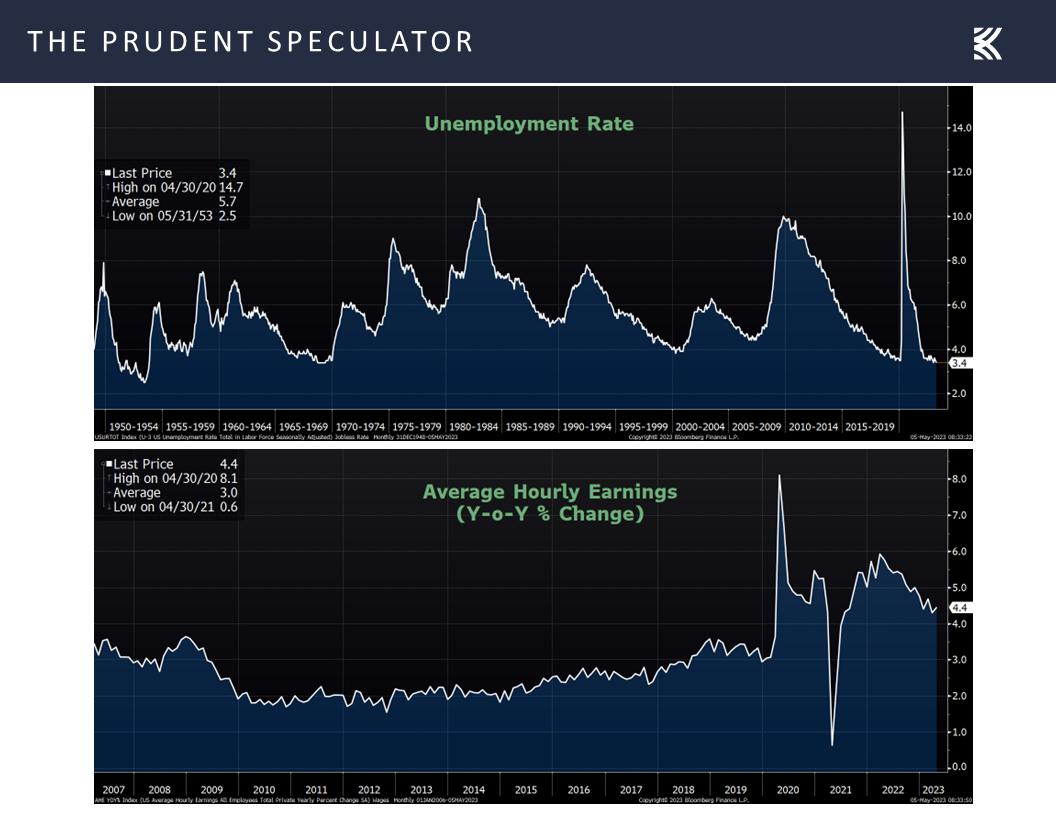

Econ Data – Strong Employment Situation Report; Better-than-Expected ISM Numbers

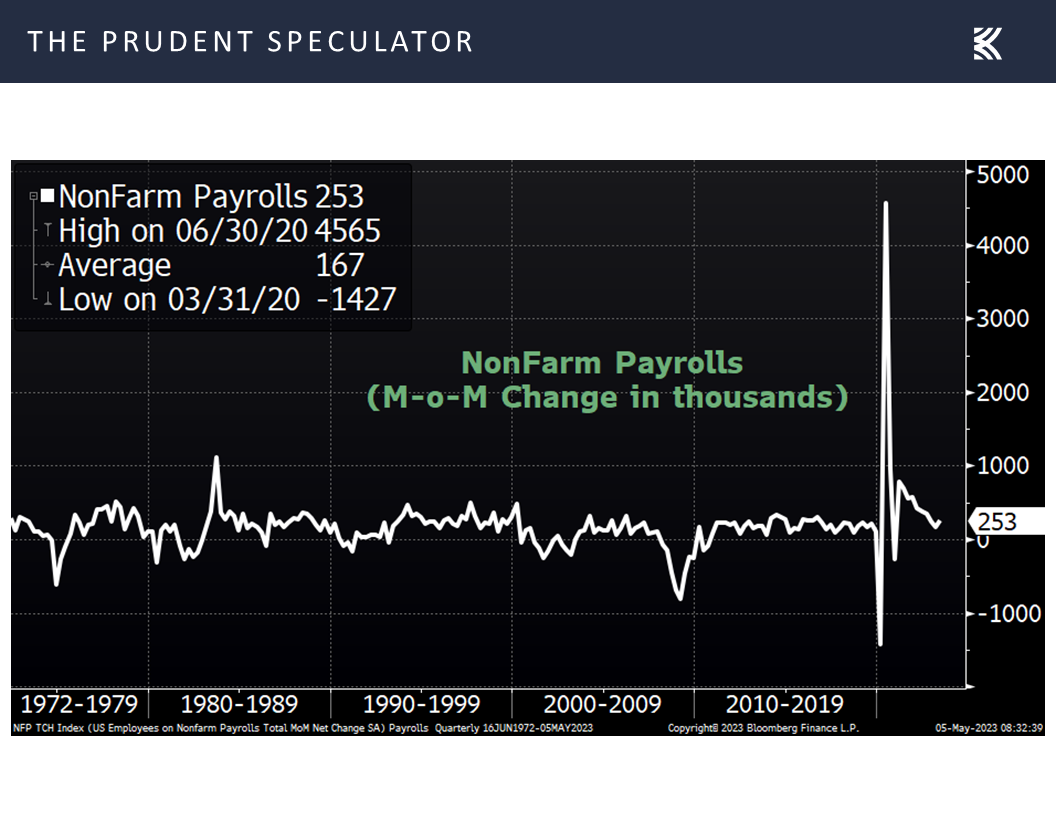

We also can’t ignore the robustness of the labor market as Friday’s impressive monthly employment situation report saw a much better-than-expected 253,000 new jobs created,

and the jobless rate edge down to 3.4%, matching the lowest level since 1969!

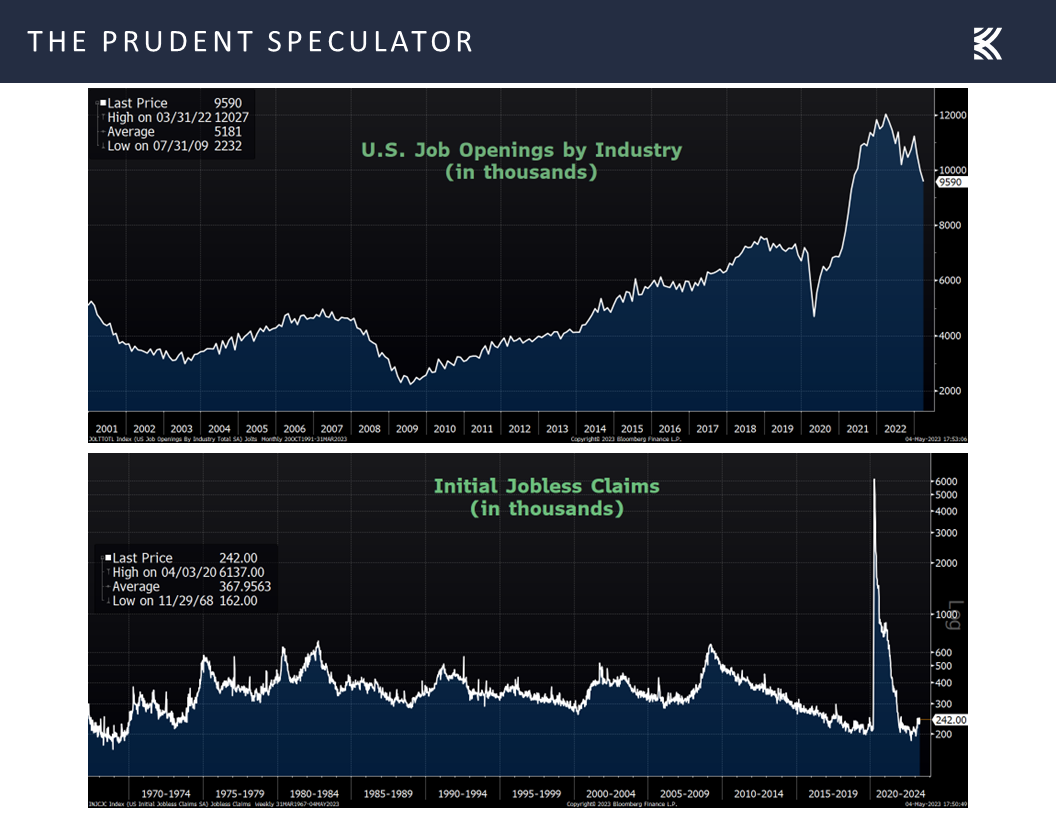

To be sure, the labor picture is weakening somewhat as job openings have been falling and first time filings for unemployment benefits have ticked a bit higher,

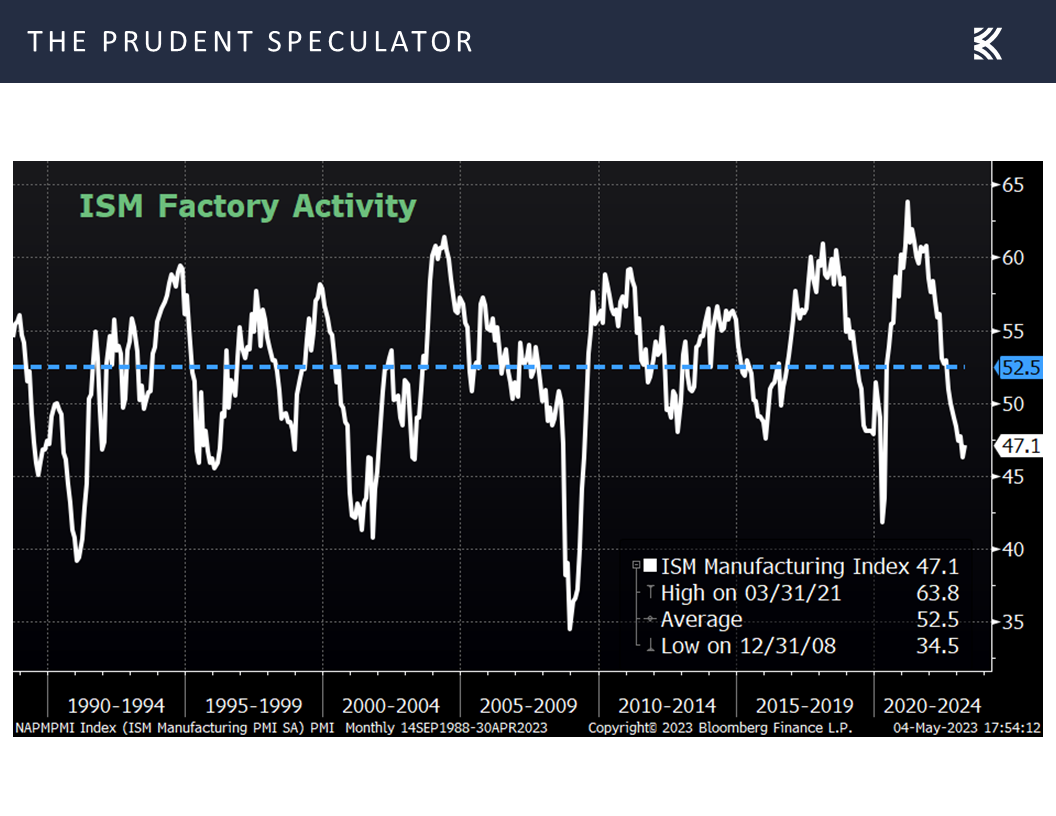

while the factory sector technically is in contraction, as evidenced by the April Manufacturing PMI reading from the Institute for Supply Management (ISM) coming in at 47.1. The tally was better-than-expected but ISM stated, “The past relationship between the Manufacturing PMI® and the overall economy indicates that the April reading (47.1 percent) corresponds to a change of minus-0.6 percent in real gross domestic product (GDP) on an annualized basis.”

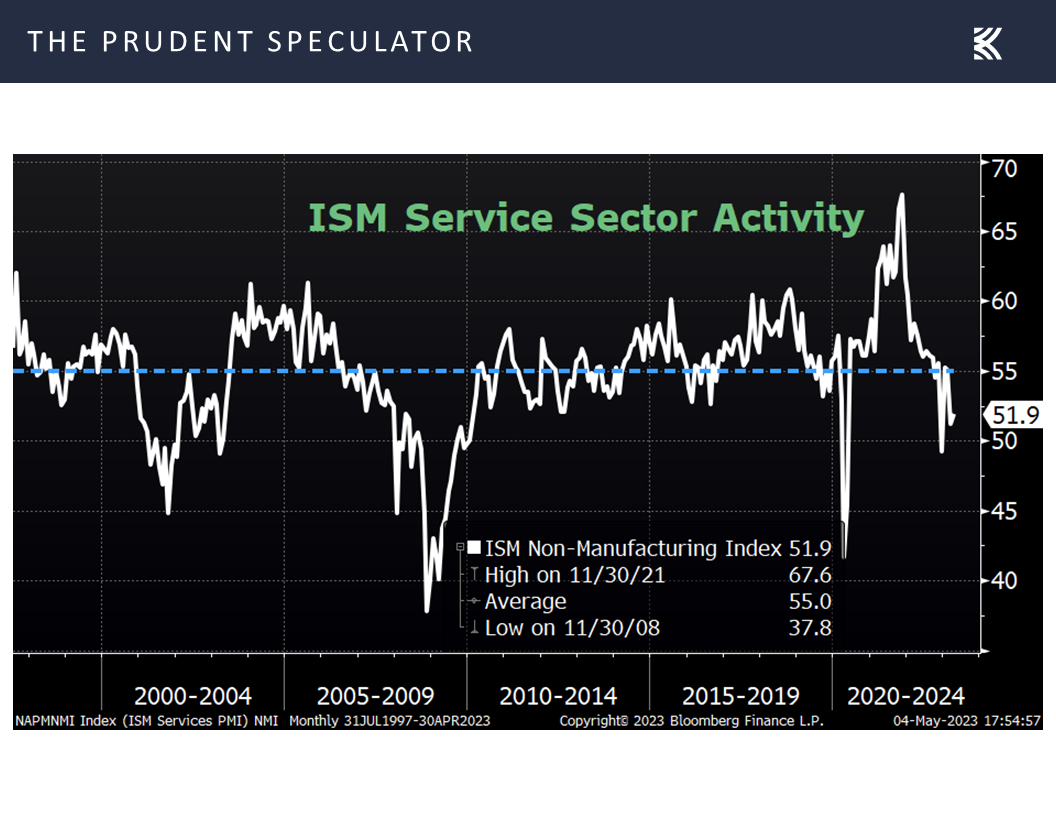

Of course, the ISM’s PMI index for the more important services sector of the economy showed the fourth straight month of expansion when the measure hit 51.9 in April. ISM commented, “The past relationship between the Services PMI® and the overall economy indicates that the Services PMI® for April (51.9 percent) corresponds to a 0.7-percent increase in real gross domestic product (GDP) on an annualized basis.”

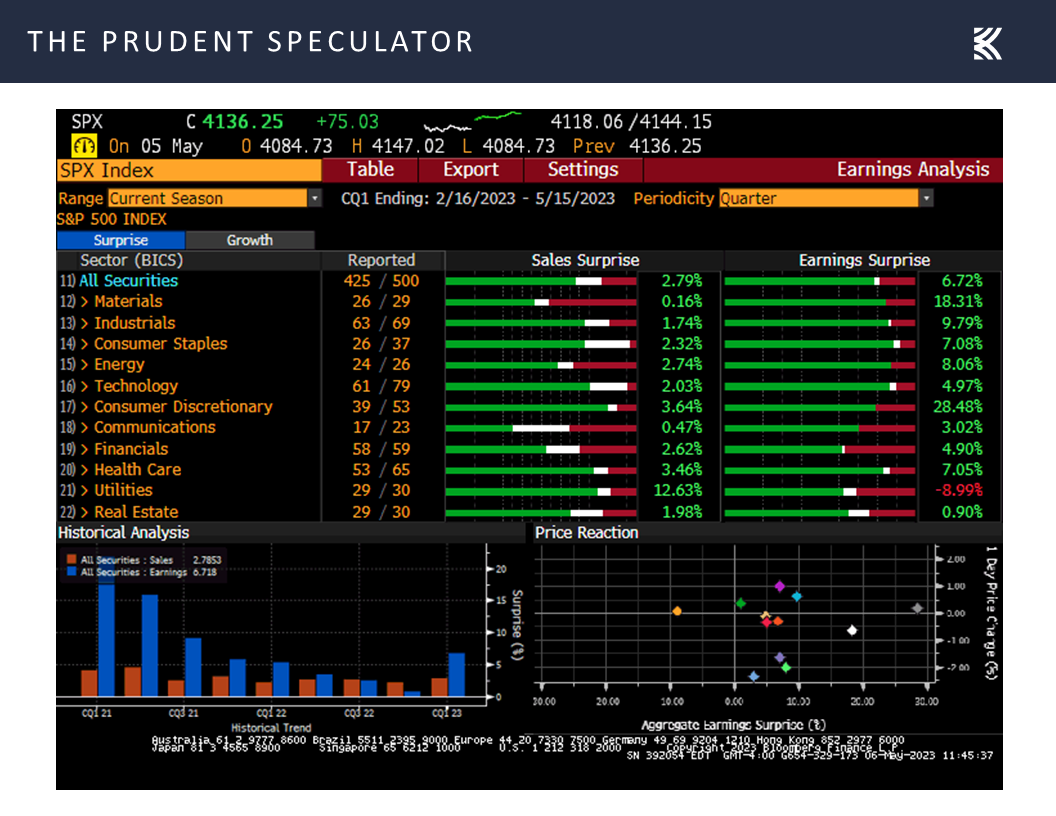

Earnings – Solid Results from Corporate America

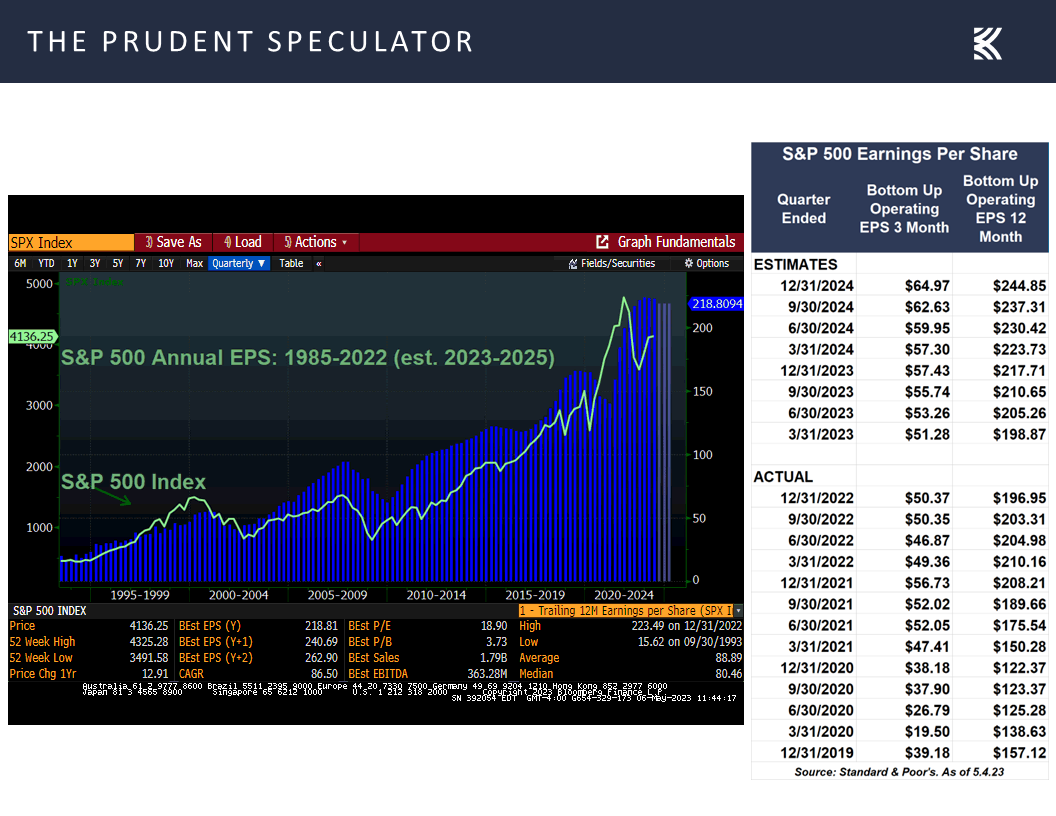

Needless to say, the economic crystal ball is as cloudy as ever, but Q1 corporate profit reports generally have been terrific, even as guidance has been subdued for many companies. Indeed, with 85% of the S&P 500 having announced results, 78.3% of companies have beaten top-line expectations while 68.2% have topped bottom-line estimates.

Analysts are often overly optimistic in their projections, but the outlook from Standard & Poor’s itself for EPS going forward is for handsome growth this year and in 2024,

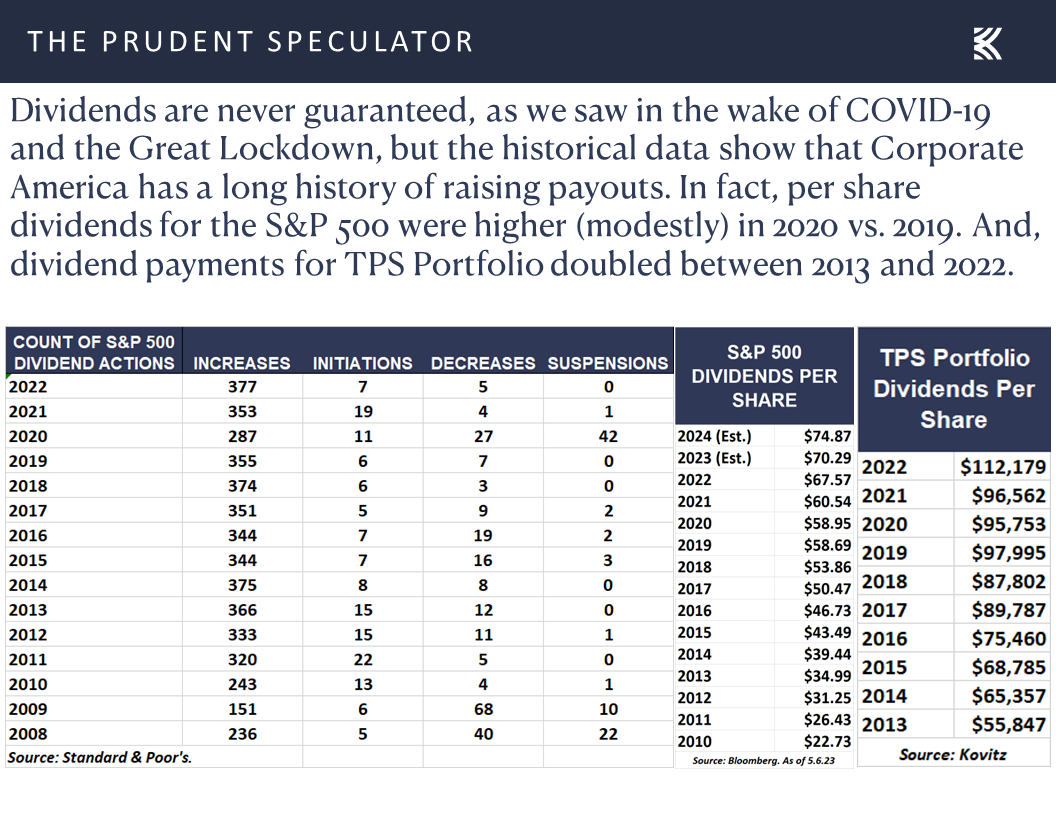

Dividends – Payouts Grow Over Time

which would provide plenty of support for further dividend increases, a trend that has been long-playing.

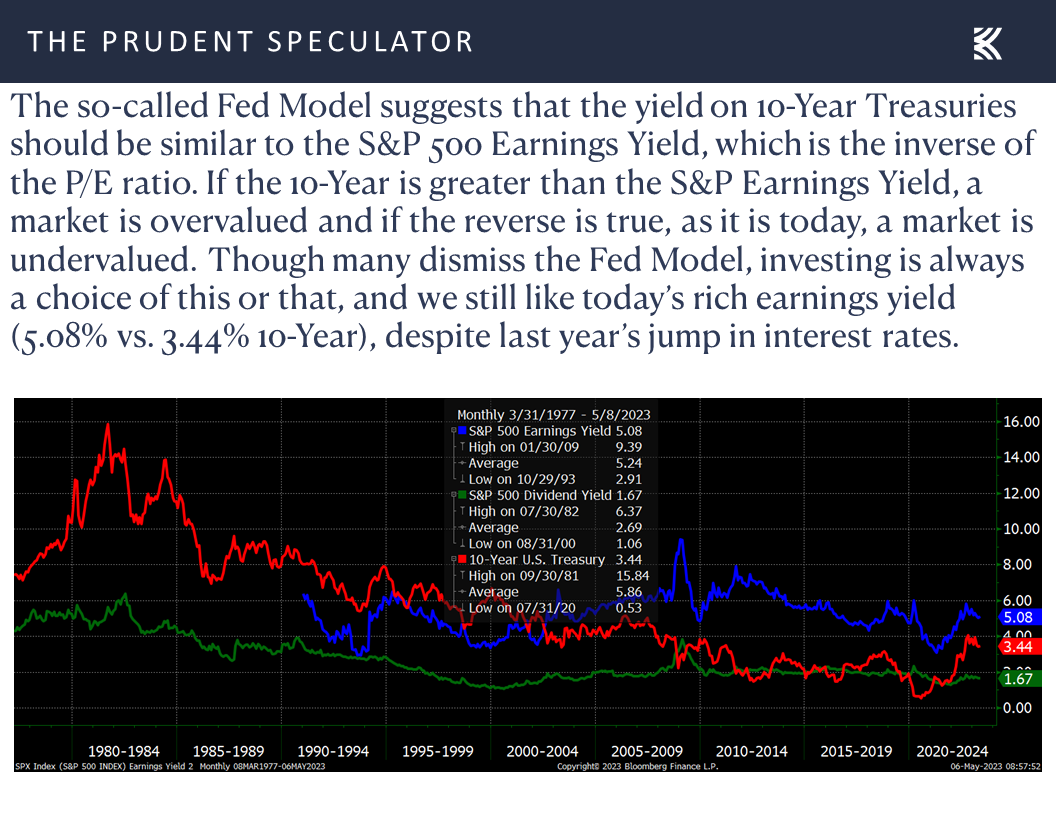

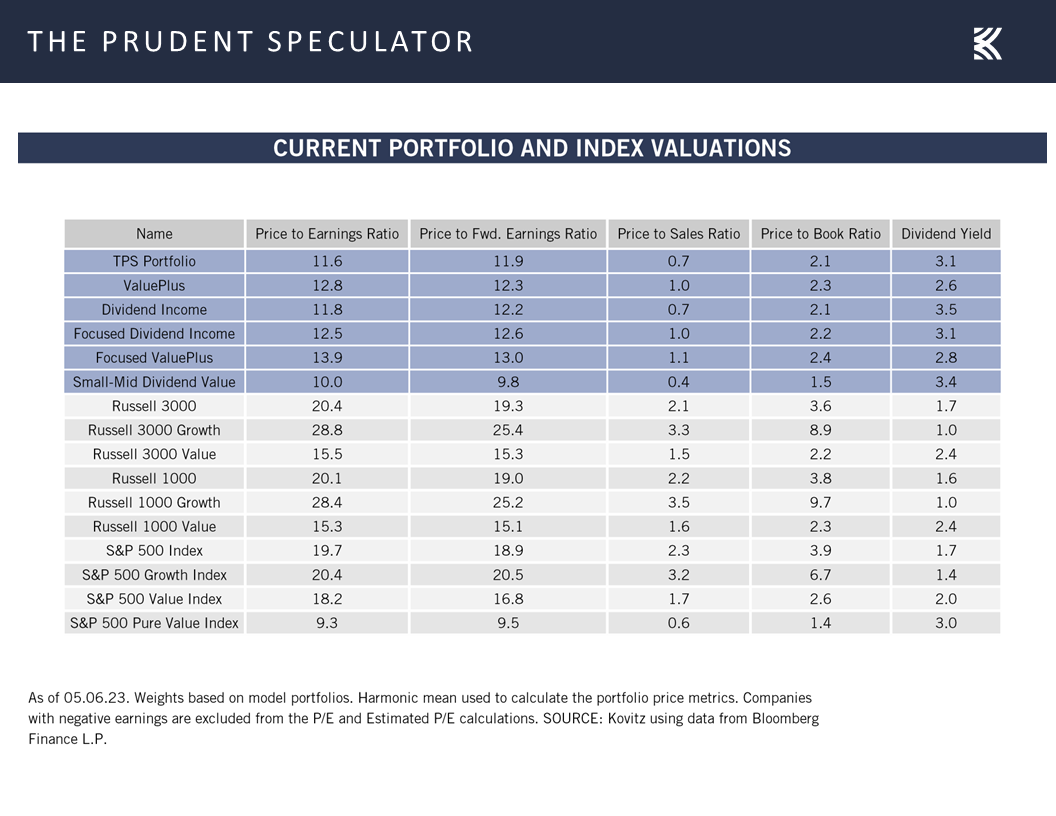

It would also lead to a continuation of the attractive valuation comparison for stocks, with the current S&P 500 earnings yield modestly below the average level since 1977,

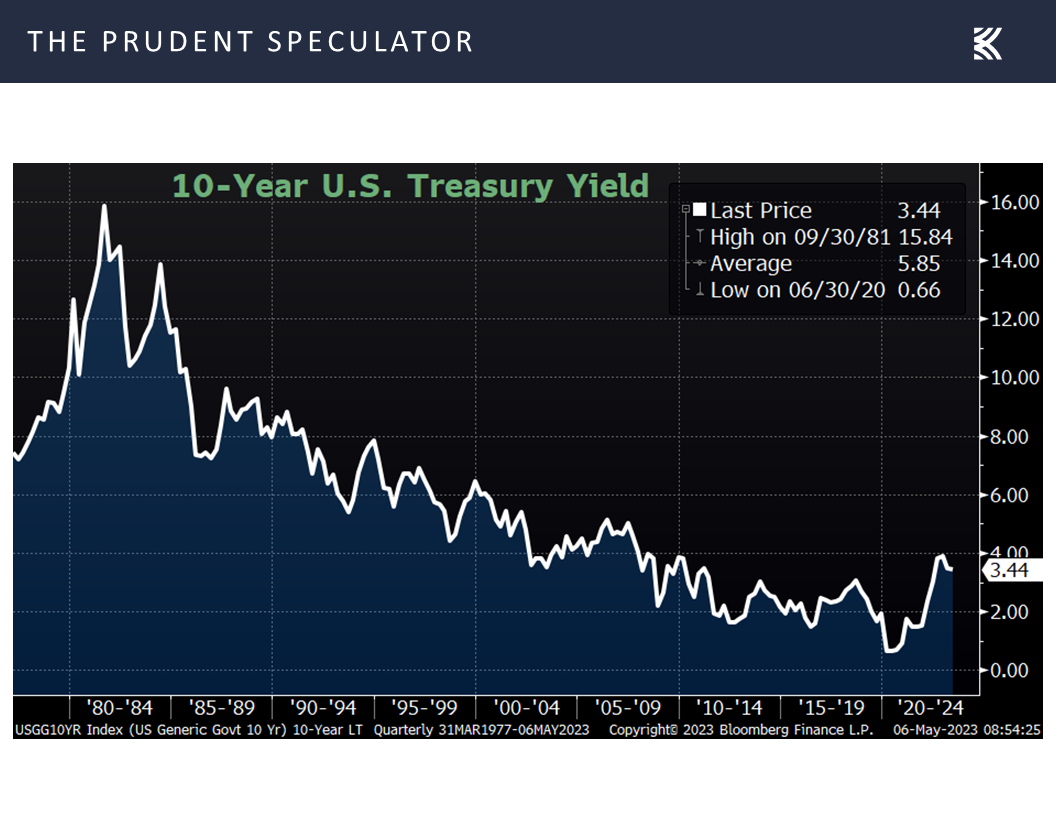

and longer-term interest rates also well below their historical average,

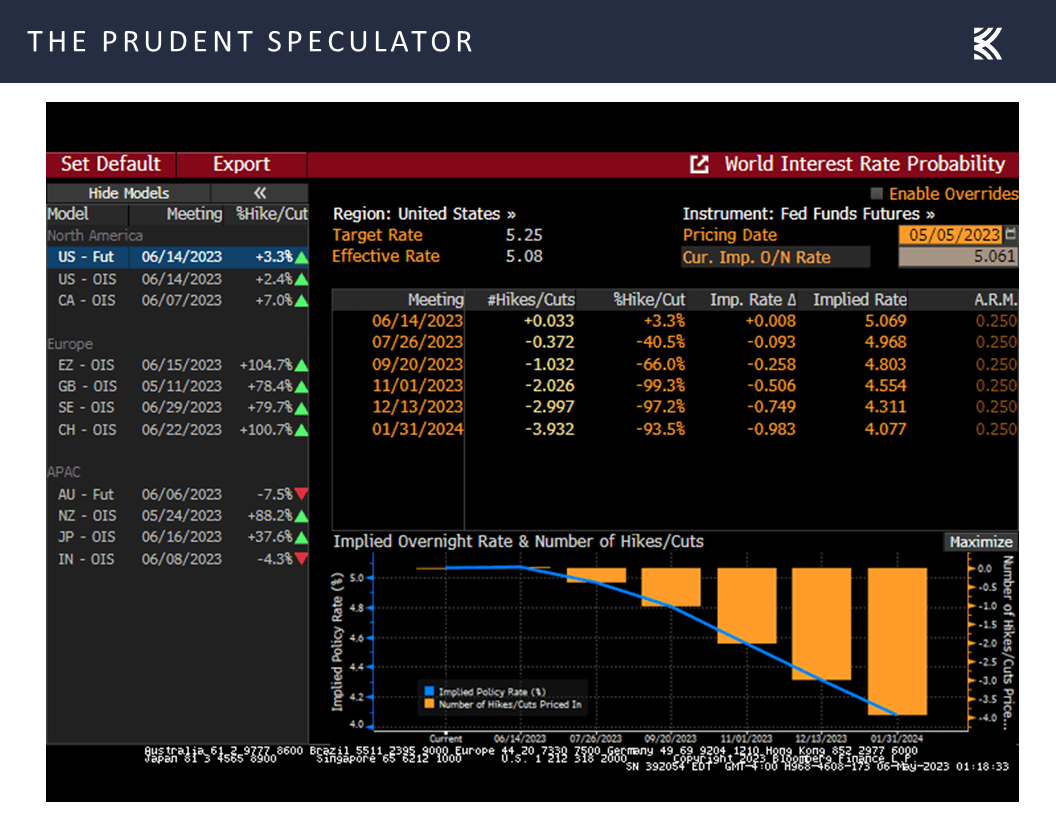

with the Fed Funds futures suggesting that the direction of that benchmark interest rate over the balance of the year will be south.

Contrarian Sentiment – AAII Even More Pessimistic

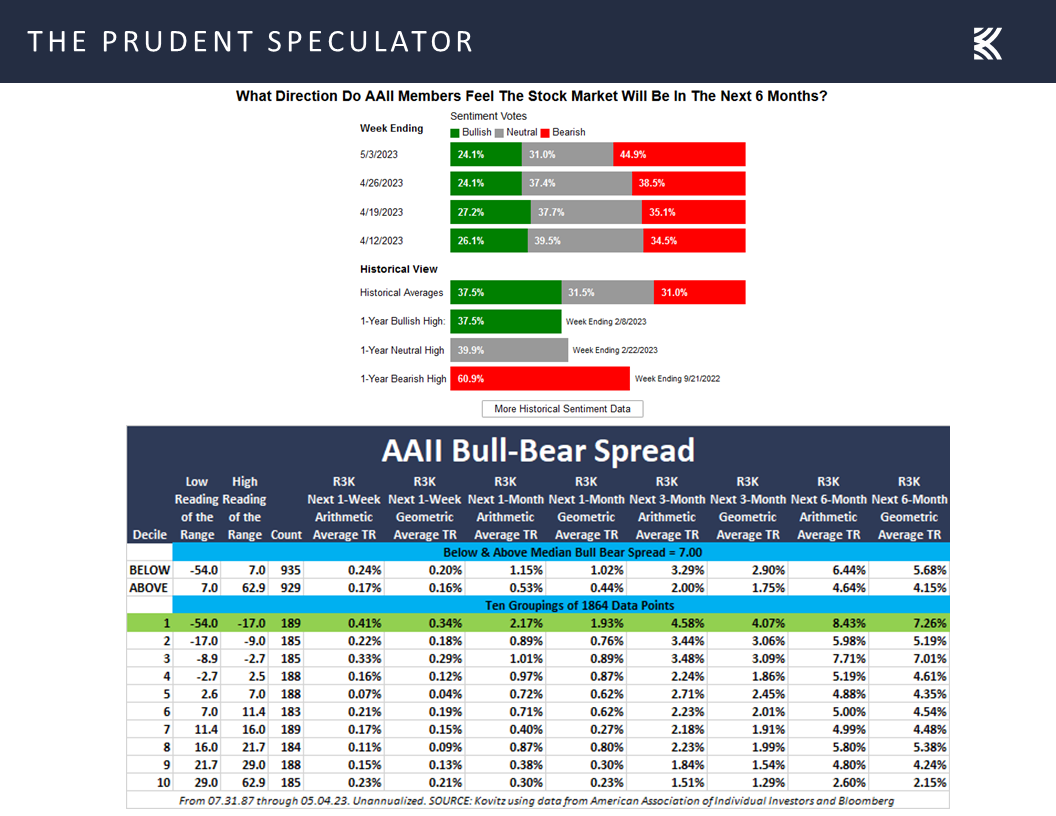

As always we are braced for downside volatility, but we continue to like that folks on Main Street are extremely pessimistic today, with the latest weekly AAII Bull-Bear Sentiment gauge (a strong contrarian measure) showing 24.1% Bulls and 44.9% Bears and the minus 20.8 point Bull-Bear Spread residing in the first decile, the most favorable for future short-term equity returns.

Valuations – Stocks Still Reasonably Priced vs. Long-Term Treasuries

More importantly, we remain very comfortable with the reasonable valuations and generous dividend yields of our broadly diversified portfolios of what we believe to be undervalued stocks.

Stock Market News: Updates on sixteen stocks across ten different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Regional Banks, Federal Reserve Meeting, Economic Data, Earnings and more

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss Regional Banks, Federal Reserve meeting Economic Data, Earnings and more economic news. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Newsletter Trades – 6 Purchases for 4 Portfolios

Week in Review – 242nd Worst Week for the Russell 3000 Value Index

Regional Banks – Buffett Argues Deposits are Safe; Latest TPS Special Report; CRE Worries but Diverse Loan Books, Solid Capital Ratios & Strong Credit Quality

Fed Meeting – 25-Basis-Point Hike; Mixed Messaging

Recession – Not the Current Powell or Atlanta Fed Projection, But No Reason to Panic if a Contraction Eventually Occurs

Econ Data – Strong Employment Situation Report; Better-than-Expected ISM Numbers

Earnings – Solid Results from Corporate America

Dividends – Payouts Grow Over Time

Valuations – Stocks Still Reasonably Priced vs. Long-Term Treasuries

Contrarian Sentiment – AAII Even More Pessimistic

Stock News – Updates on sixteen stocks across ten different sectors

Week in Review – 242nd Worst Week for the Russell 3000 Value Index

The seasonally less favorable (it is still positive, on average, for Value Stocks and Dividend Payers) May – October period,

certainly began on an ugly note last week as it took a big rebound on Friday to pare losses on the Russell 3000 Value index to only 1.7% for the five days. No doubt, volatility is normal as the week just ended was the 242nd worst for that index since its creation in 1995. Happily, there have been 292 weeks over the past 28 years with gains of similar or greater magnitude, while long-term average annualized returns for Value stocks since the inception of The Prudent Speculator in 1977 have been terrific.

Regional Banks – Buffett Argues Deposits are Safe; Latest TPS Special Report; CRE Worries but Diverse Loan Books, Solid Capital Ratios & Strong Credit Quality

One of the reasons for the equity market struggles last week was renewed worries about the regional banks. Our latest thoughts on the matter are available here, and we were happy to see the sizable bounce in shares of the regional banks on Friday, even as a one-day respite from the selling hardly a trend makes. Still, it was nice to hear Warren Buffett on Saturday proclaim that deposits are safe, which is in keeping with the facts (as opposed to the fiction put forth by short-sellers as well as several prominent billionaires) thus far that there has not been a systemic run on the bank.

To be sure, the Oracle of Omaha was quick to add that the increase in interest rates we have witnessed over the past year or so is problematic for commercial real estate and we do not deny that non-performing assets on bank balance sheets will rise. However, we are of the mind that the banks we own, like PNC Financial (PNC – $116.18), have broadly diversified loan books, solid capital ratios and strong credit quality. Commercial real estate is 11.0% of PNC’s total loans, with the more worrisome Office category geographically diverse and accounting for 2.7% of total loans.

Fed Meeting – 25-Basis-Point Hike; Mixed Messaging

The other market-moving news of the week was the decision on interest rates from the Federal Open Market Committee (FOMC) and Jerome H. Powell’s Press Conference that followed. The fact that the Fed Chair and his colleagues chose to hike their target for the Federal Funds rate by another 25 basis points to a range of 5.00% to 5.25% was not a surprise,

and the equity markets initially did not seem unhappy with the FOMC statement.

The problem for the stock market, at least for two days, was that Mr. Powell was a bit wishy-washy in his Q&A in regard to future interest rate increases. On the one hand, he said, “People did talk about pausing, but not so much at this meeting. We feel like we’re getting closer or maybe even there.” On the other hand, he asserted, “I think that policy is tight, but we are prepared to do more if greater monetary policy restraint is warranted.”

Further, he reminded, “Looking ahead, we will take a data-dependent approach in determining the extent to which additional policy firming may be appropriate,” but the Fed Funds rate is now at the year-end 2023 projection offered in the quarterly economic projections put forth by the Federal Reserve Board members and Federal Reserve Bank presidents back in March.

Recession – Not the Current Powell or Atlanta Fed Projection, But No Reason to Panic if a Contraction Eventually Occurs

Those March projections also called for 0.4% real (inflation-adjusted) GDP growth for 2023, but Chair Powell intimated that updated projections were arguably a bit more pessimistic. He said, “So, broadly, the forecast was for a mild recession, and by that I would characterize as one in which the rising unemployment is smaller than is has been typical in modern era recessions. I wouldn’t want to characterize the staff’s forecast for this meeting. We’ll leave that to the minutes but broadly — broadly similar to that.”

When asked specifically about his own economic forecast, the Chair responded, “The case of avoiding a recession is, in my view, more likely than that of having a recession. But it’s not — it’s not that the case of having a recession is — I don’t rule that out, either. It’s possible that we will have what I hope would be a mild recession.”

Is it any surprise that famed American Economist Paul Samuelson said, “Economists have predicted nine of the last five recessions?” After all, the current odds of an economic contraction in the next 12 months, as tabulated by Bloomberg, have been at 60% or higher since October,

yet real GDP growth came in at 2.6% in Q4 2022 and 1.1% in Q1 2023.

while the current estimate for real Q2 GDP growth from the Atlanta Fed rose last week to 2.7%.

The optimists, including Mr. Powell, could be wrong and a recession may occur, but we do not think that would be reason to abandon Value Stocks and Dividend Payers, or equities in general, even if we could somehow identify the exact beginning and ending of the contraction in advance.

Further, given that Mr. Powell is the first Fed Chair to face the same kind of inflationary pressures as Paul Volcker some 40 years ago, we take comfort in the fantastic equity returns posted under the Volcker Fed from 1979 – 1986, especially as the vanquishing of the Great Inflation included two recessions, one starting in 1980 and another starting in 1981.

Econ Data – Strong Employment Situation Report; Better-than-Expected ISM Numbers

We also can’t ignore the robustness of the labor market as Friday’s impressive monthly employment situation report saw a much better-than-expected 253,000 new jobs created,

and the jobless rate edge down to 3.4%, matching the lowest level since 1969!

To be sure, the labor picture is weakening somewhat as job openings have been falling and first time filings for unemployment benefits have ticked a bit higher,

while the factory sector technically is in contraction, as evidenced by the April Manufacturing PMI reading from the Institute for Supply Management (ISM) coming in at 47.1. The tally was better-than-expected but ISM stated, “The past relationship between the Manufacturing PMI® and the overall economy indicates that the April reading (47.1 percent) corresponds to a change of minus-0.6 percent in real gross domestic product (GDP) on an annualized basis.”

Of course, the ISM’s PMI index for the more important services sector of the economy showed the fourth straight month of expansion when the measure hit 51.9 in April. ISM commented, “The past relationship between the Services PMI® and the overall economy indicates that the Services PMI® for April (51.9 percent) corresponds to a 0.7-percent increase in real gross domestic product (GDP) on an annualized basis.”

Earnings – Solid Results from Corporate America

Needless to say, the economic crystal ball is as cloudy as ever, but Q1 corporate profit reports generally have been terrific, even as guidance has been subdued for many companies. Indeed, with 85% of the S&P 500 having announced results, 78.3% of companies have beaten top-line expectations while 68.2% have topped bottom-line estimates.

Analysts are often overly optimistic in their projections, but the outlook from Standard & Poor’s itself for EPS going forward is for handsome growth this year and in 2024,

Dividends – Payouts Grow Over Time

which would provide plenty of support for further dividend increases, a trend that has been long-playing.

It would also lead to a continuation of the attractive valuation comparison for stocks, with the current S&P 500 earnings yield modestly below the average level since 1977,

and longer-term interest rates also well below their historical average,

with the Fed Funds futures suggesting that the direction of that benchmark interest rate over the balance of the year will be south.

Contrarian Sentiment – AAII Even More Pessimistic

As always we are braced for downside volatility, but we continue to like that folks on Main Street are extremely pessimistic today, with the latest weekly AAII Bull-Bear Sentiment gauge (a strong contrarian measure) showing 24.1% Bulls and 44.9% Bears and the minus 20.8 point Bull-Bear Spread residing in the first decile, the most favorable for future short-term equity returns.

Valuations – Stocks Still Reasonably Priced vs. Long-Term Treasuries

More importantly, we remain very comfortable with the reasonable valuations and generous dividend yields of our broadly diversified portfolios of what we believe to be undervalued stocks.

Stock Market News: Updates on sixteen stocks across ten different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.