The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. This week, we cover the rising and falling rate environments, volatility, AAII sentiment, the Fed tightening, corporate profits and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

- Interest Rates: Stocks Historically Indifferent to Rising/Falling Rates

- Volatility: Ups and Downs Aplenty, but Long-Term Trend is Higher

- Sentiment: AAII More Pessimistic than Usual

- Econ Numbers: Mixed Picture; More Good than Bad

- Inflation: CPI & PPI Higher than Expected; Fed Likely to Remain Hawkish

- Fed Tightening & High Inflation: Historical Equity Return Perspective

- Valuations: Inexpensive Metrics for our Portfolios

- Corporate Profits: Solid Q4 EPS and Decent Outlook for 2023

- Stock News: Updates on ten stocks across eight different sectors

Interest Rates: Stocks Historically Indifferent to Rising/Falling Rates

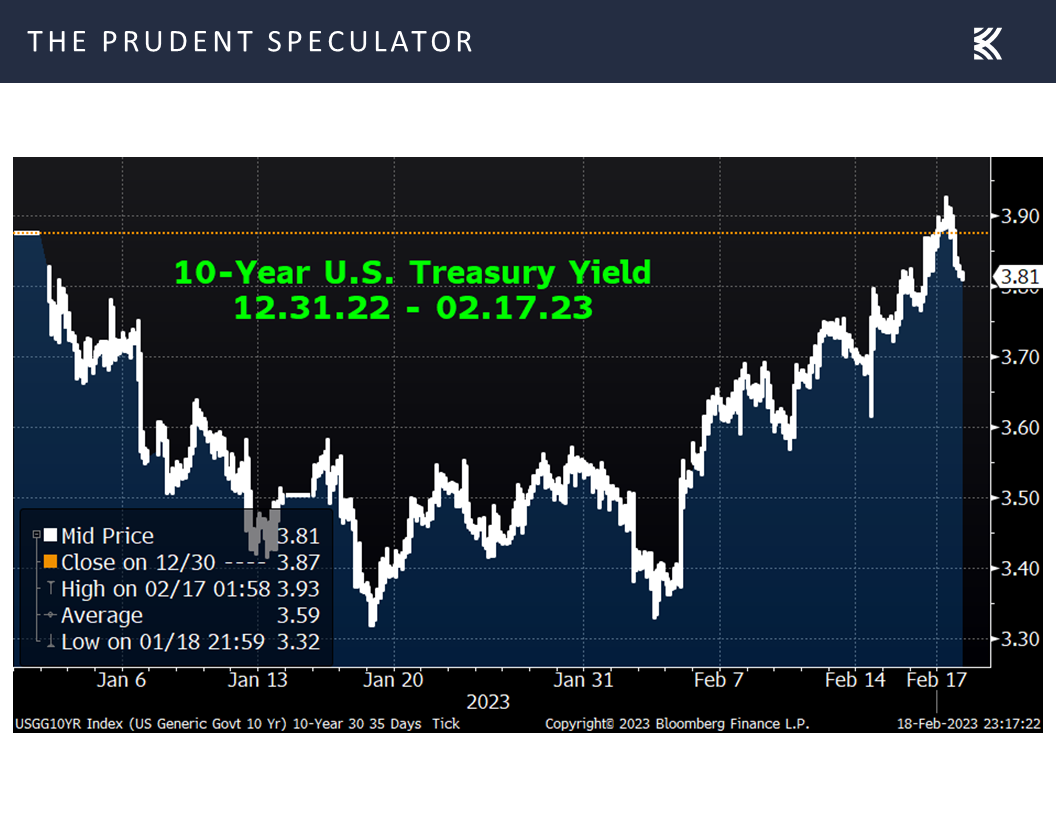

Saturday’s edition of The New York Times told us, “Stocks Drop On Worries About Rates,” which we found interesting in that interest rates fell on Friday, with the yield on the 10-Year U.S. Treasury now a few basis points below where it began the year. The yield on the 10-Year U.S. Treasury is today about where it was at the start of 2023.

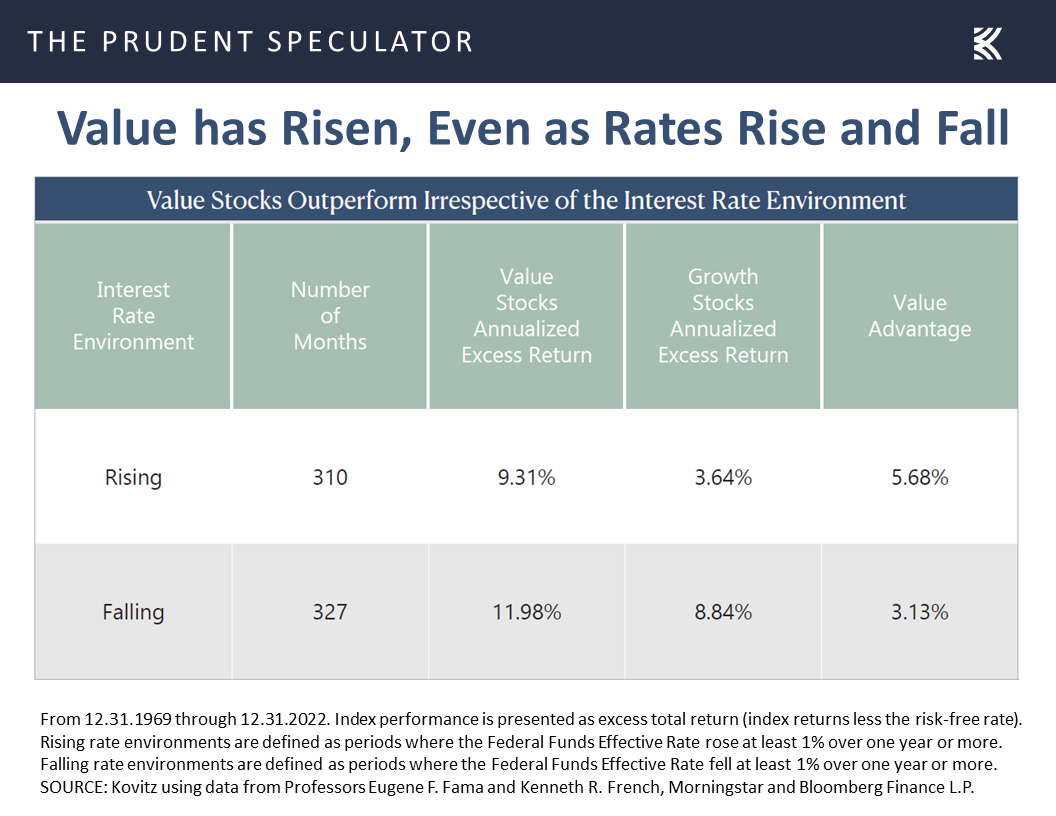

Of course, as we discuss in our latest Special Report, Consider Cheering Higher Rates, the historical evidence shows that equities have performed well, on average, whether interest rates are rising or falling, no matter how the data is sliced and diced.

Volatility: Ups and Downs Aplenty, but Long-Term Trend is Higher

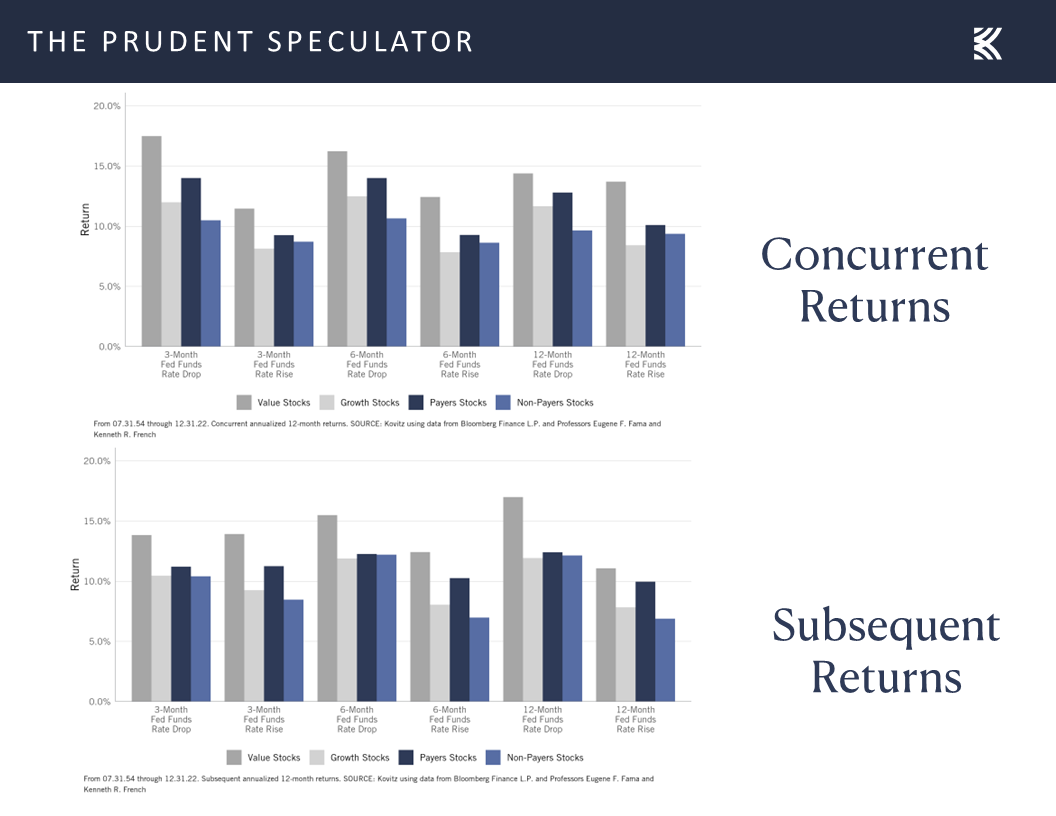

Contrary to popular belief, equities, especially Value stocks, have performed admirably, on average, both concurrent with and subsequent to hikes in the Fed Funds rate.

The NY Times further explained, “Stocks have oscillated between gains and losses as new economic data have clouded the outlook for investors, marking a notable shift in the market after stocks jumped more than 6 percent in January.”

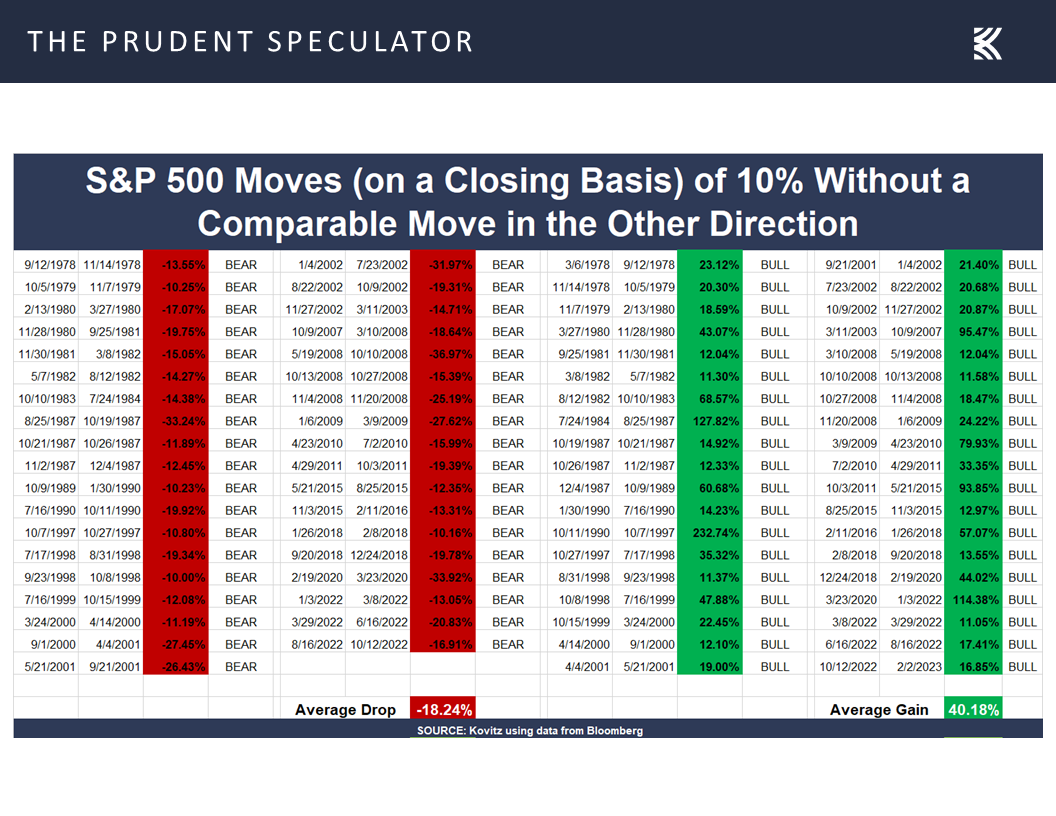

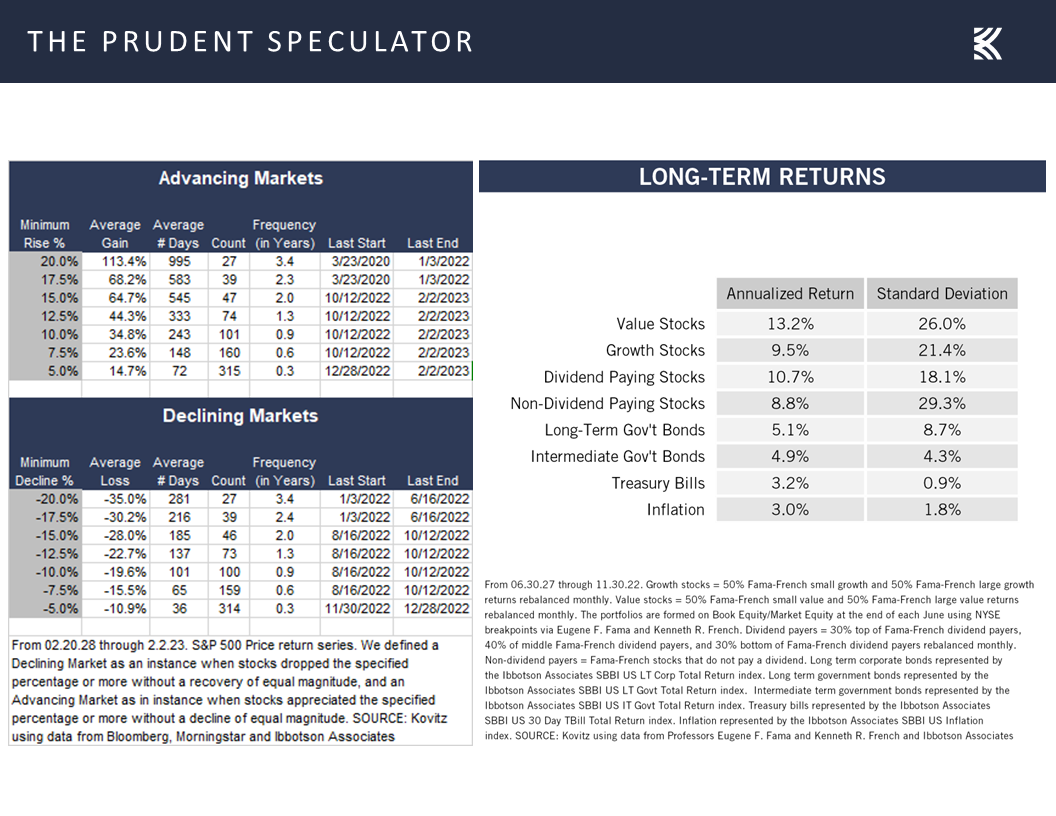

With all due respect to the financial journalism profession, the outlook for investors is always uncertain. About the only thing that is clear is that the equity markets will always endure substantial volatility over time as the significant number of 10% rallies and corrections since the launch of The Prudent Speculator 46 years ago will attest.

Ups and downs are not unusual for equities, as there have been 38 advances and 37 declines of 10% or greater since the launch of The Prudent Speculator 46 years ago.

Happily, the magnitude of the gains during the times in the green have dwarfed that of the losing periods, so much so that those who stick with stocks through thick and thin have been handsomely rewarded in the fullness of time with annualized returns ranging from 8.8% to 13.2%.

The secret to success in stocks is not to get scared out of them as every downturn has been followed by an upswing of far greater magnitude, so much so that long-term returns for Value stocks have exceeded 13% per annum.

Sentiment: AAII More Pessimistic than Usual

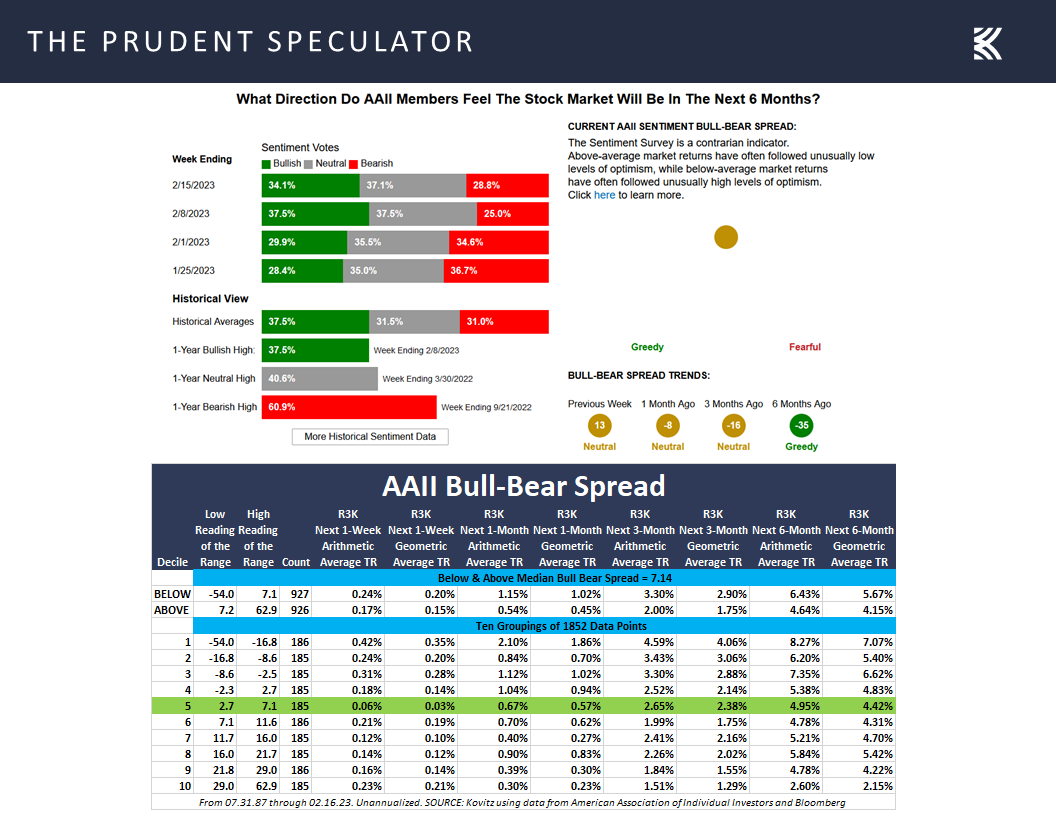

Easier said than done, we know, as far too many folks end up zigging when they should have zagged, which is why sentiment gauges like the one compiled each week since 1987 from the American Association of Individual Investors (AAII) have proven to be contra-indicators. Indeed, the admonition to be greedy when others are fearful is based on sound empirical evidence and today we continue to see less optimism and more pessimism than usual from the folks on Main Street.

The good folks in the AAII Sentiment Survey became a little more pessimistic last week, which is a good thing for potential near-term equity market gains.

Econ Numbers: Mixed Picture; More Good than Bad

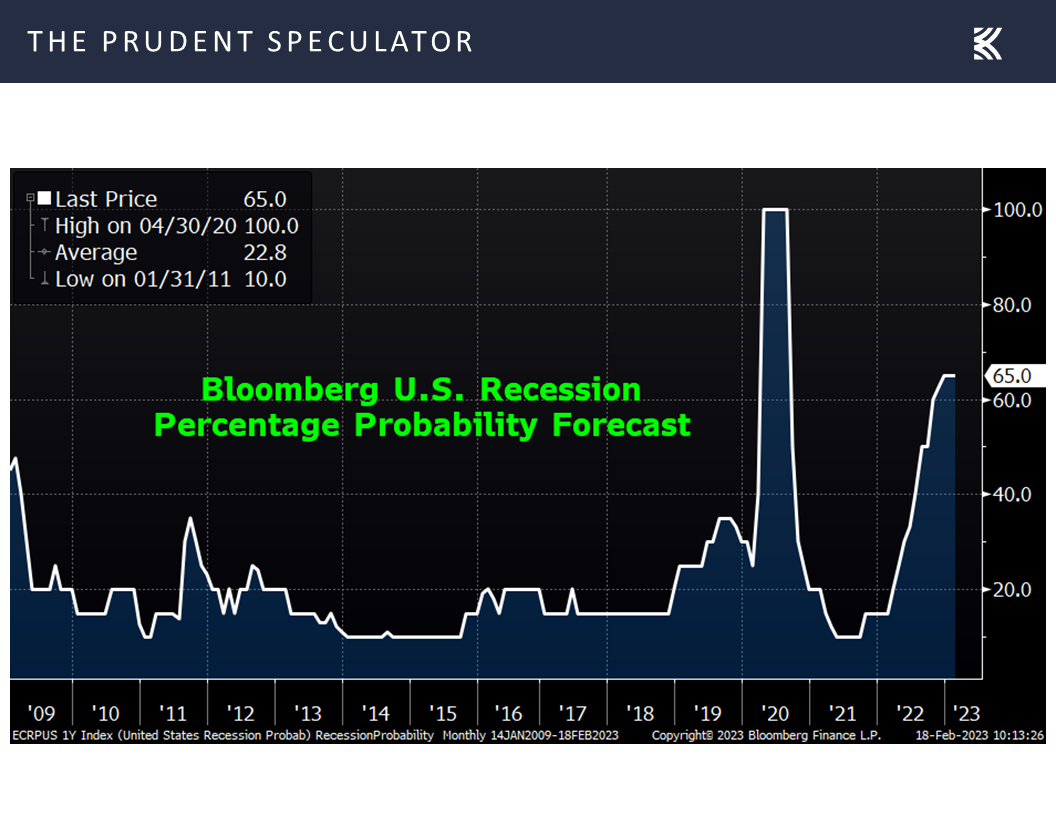

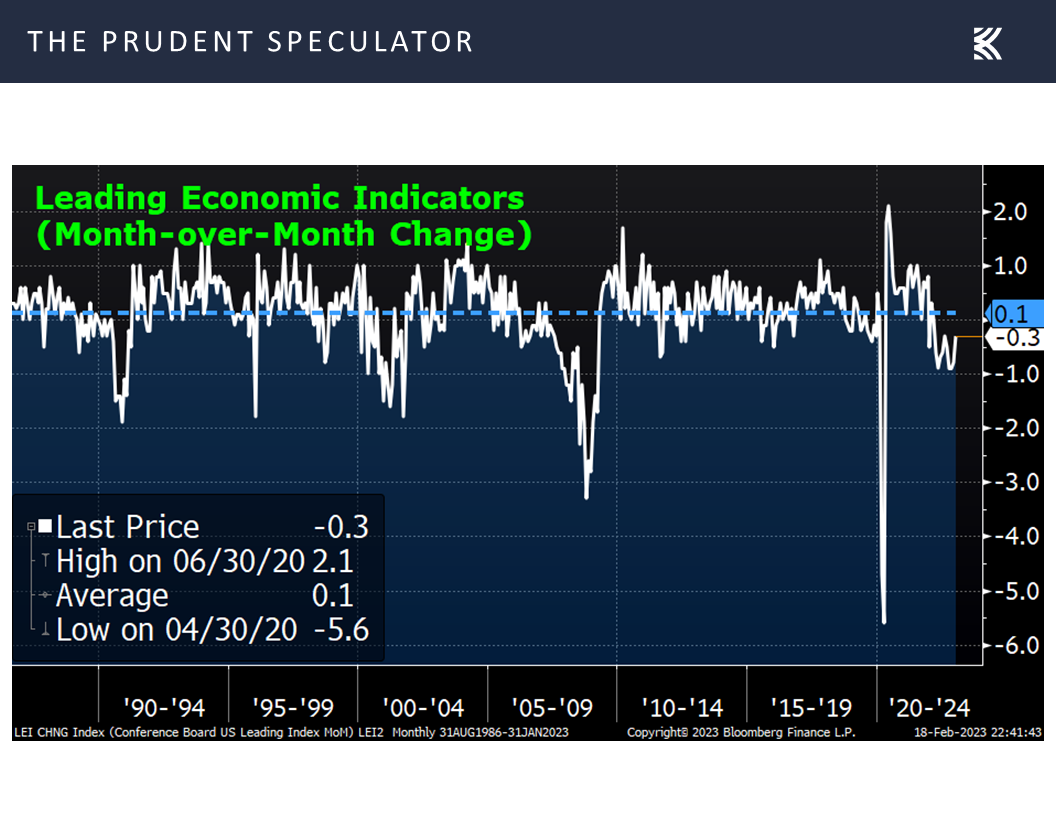

To be fair to our friends at the Times, the economic outlook is especially confounding these days as economists suggest the odds of recession are very high, while the latest Leading Economic Index fell by 0.3% in January.

The keeper of that gauge, the Conference Board, explained:

The U.S. LEI remained on a downward trajectory, but its rate of decline moderated slightly in January. Among the leading indicators, deteriorating manufacturing new orders, consumers’ expectations of business conditions, and credit conditions more than offset strengths in labor markets and stock prices to drive the index lower in the month. The contribution of the yield spread component of the LEI also turned negative in the last two months, which is often a signal of recession to come. While the LEI continues to signal recession in the near term, indicators related to the labor market—including employment and personal income—remain robust so far. Nonetheless, The Conference Board still expects high inflation, rising interest rates, and contracting consumer spending to tip the US economy into recession in 2023.

The Conference Board’s Leading Economic Index dropped “only” 0.3% in January, an improvement from December’s 0.8% decline.

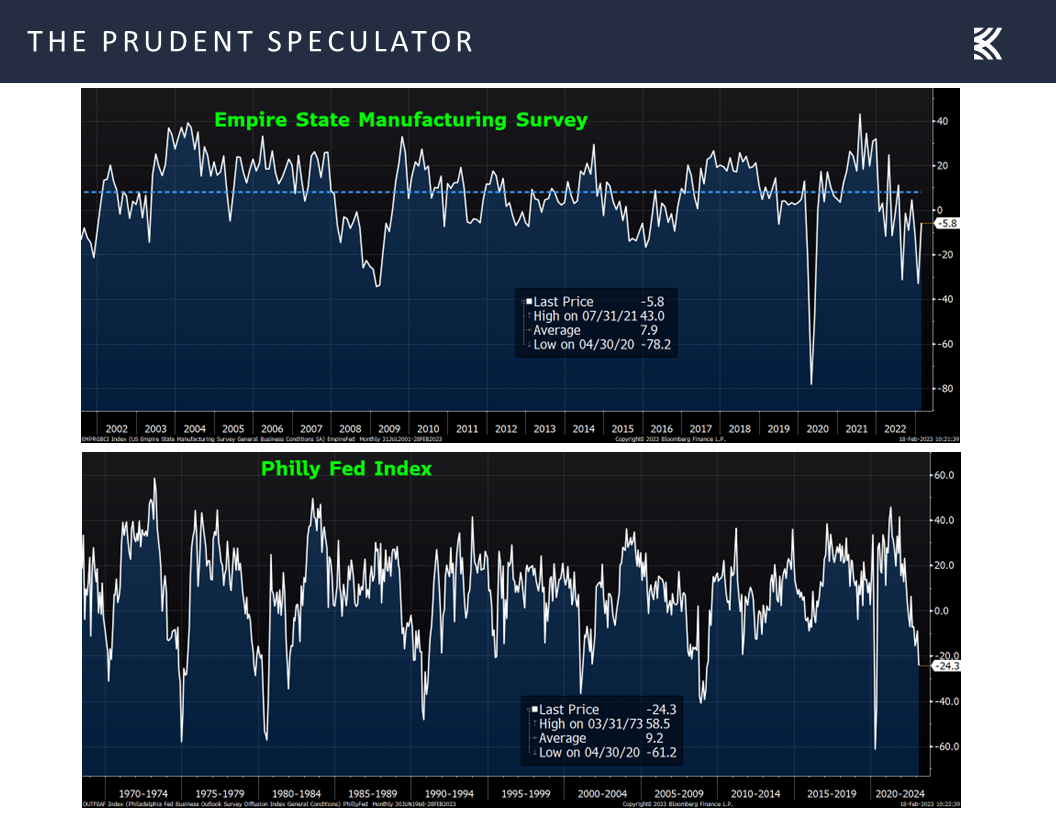

That outlook sounds ominous, especially as the manufacturing sector is arguably already in contraction, given the latest negative readings on East Coast factory activity

Two key manufacturing gauges are in contraction, though the Empire Fed factory index improved markedly this month.

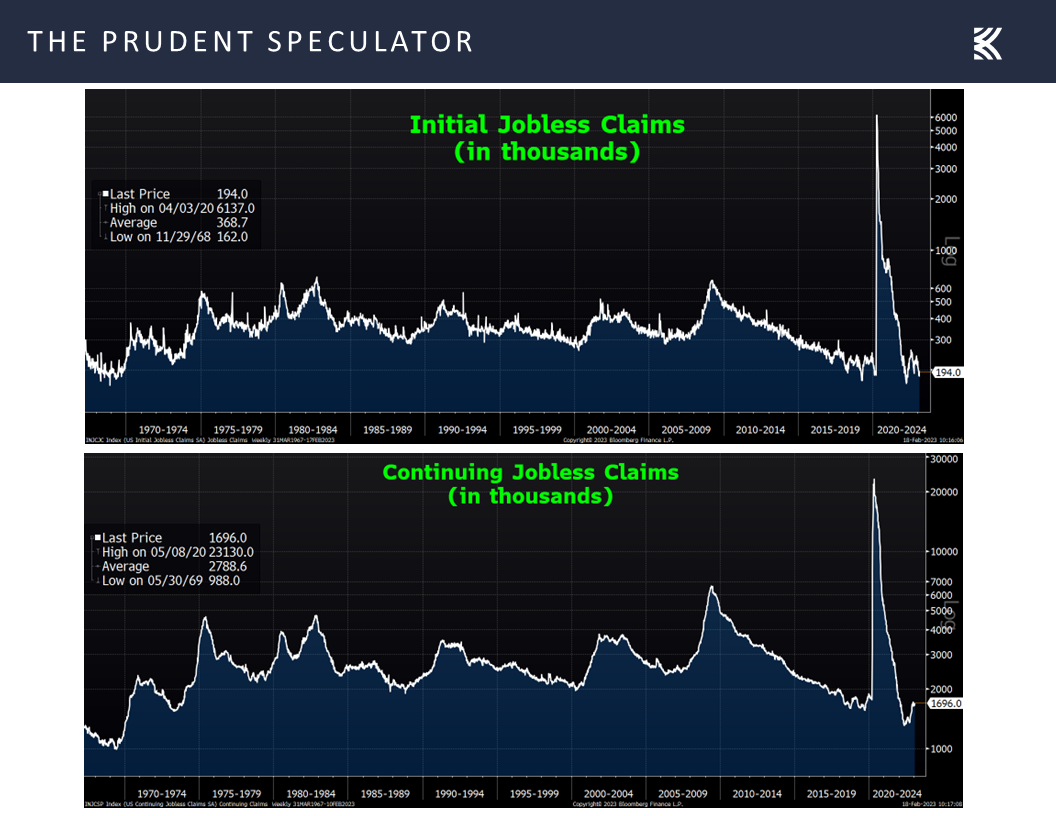

but the labor picture remains incredibly strong, with weekly initial filings for jobless claims still below 200,000, a level not seen since the 1960s when the workforce was much smaller and consumer spending has held up remarkably well as evidenced by a much-better-than-expected retail sales tally in January.

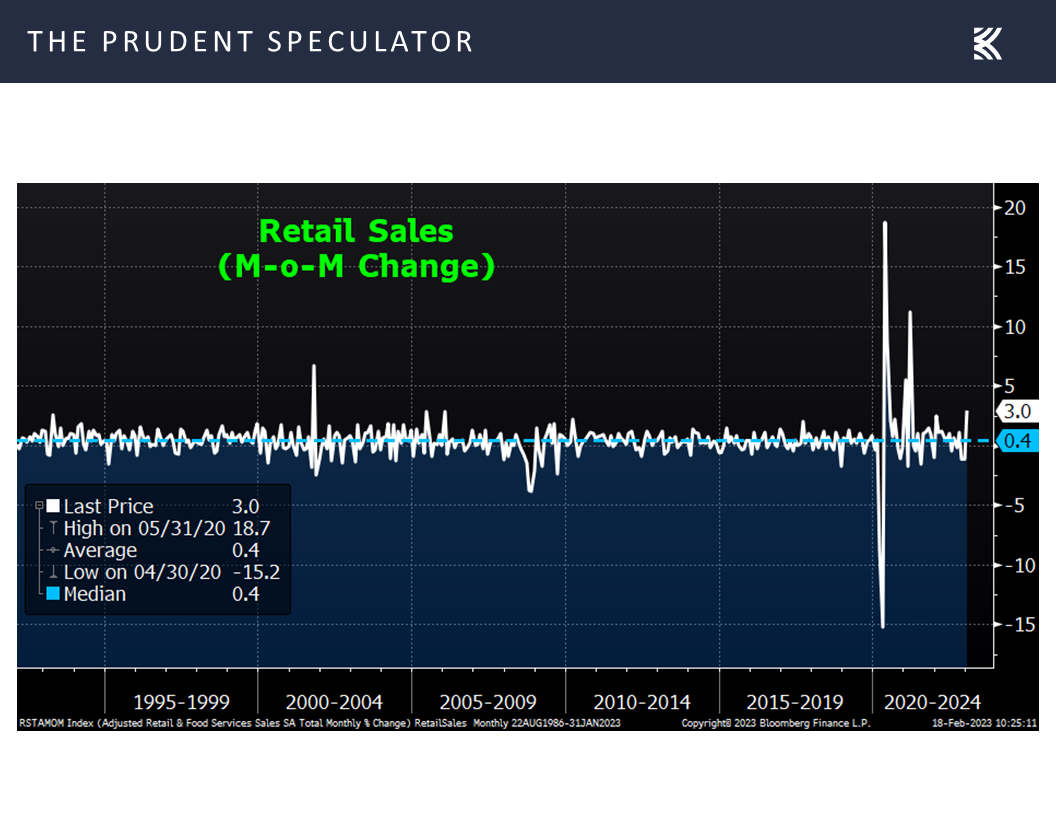

Retails sales started the year strong, with the 3% jump in January the best monthly gain in nearly two years.

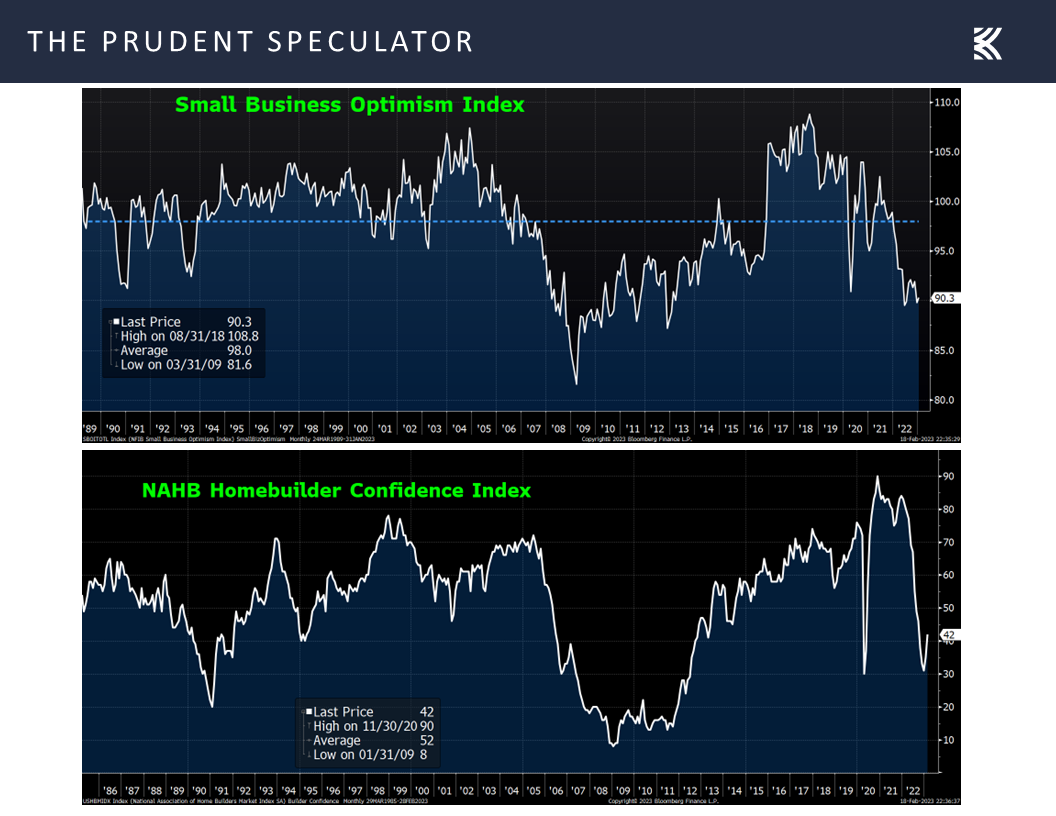

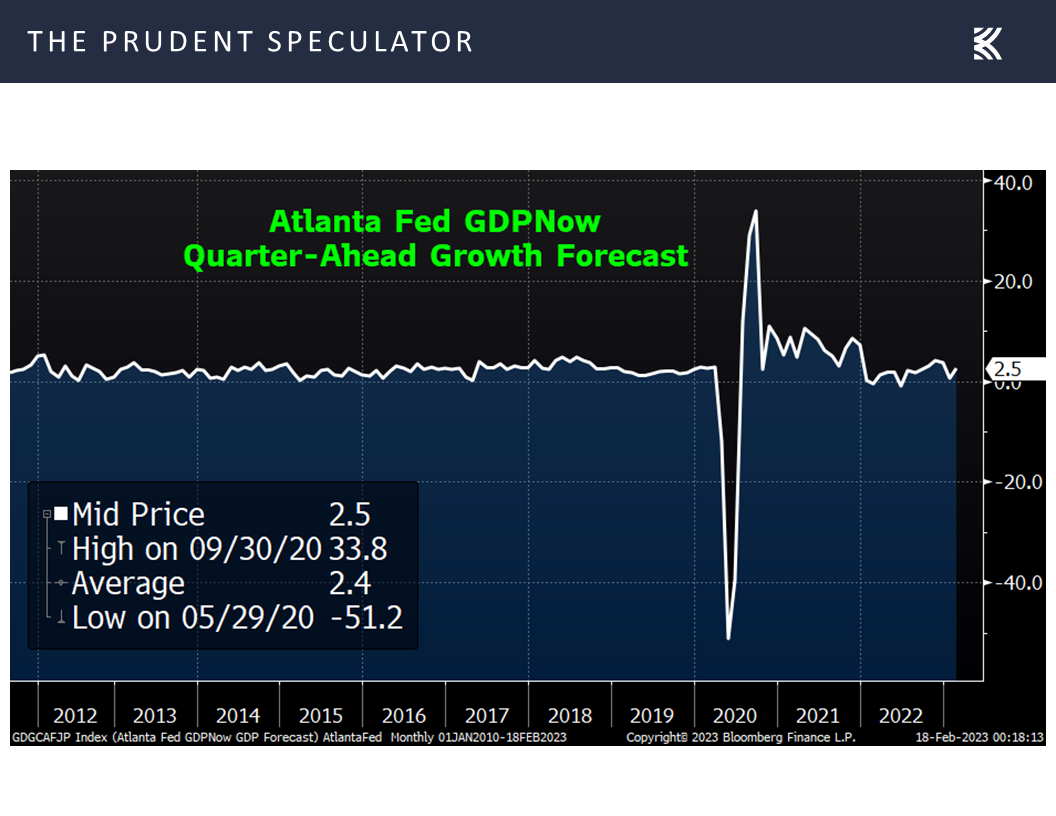

Though they are still at very depressed levels, even the latest sentiment gauges for small business and home-builders ticked higher, with the net result of the latest economic numbers leading to an increase in the outlook for Q1 U.S. GDP growth from the Atlanta Fed last week.

It is fascinating to see so much pessimism toward the U.S. economy when the current estimate for Q1 real (inflation-adjusted) GDP growth stands at a decent level.

Inflation: CPI & PPI Higher than Expected; Fed Likely to Remain Hawkish

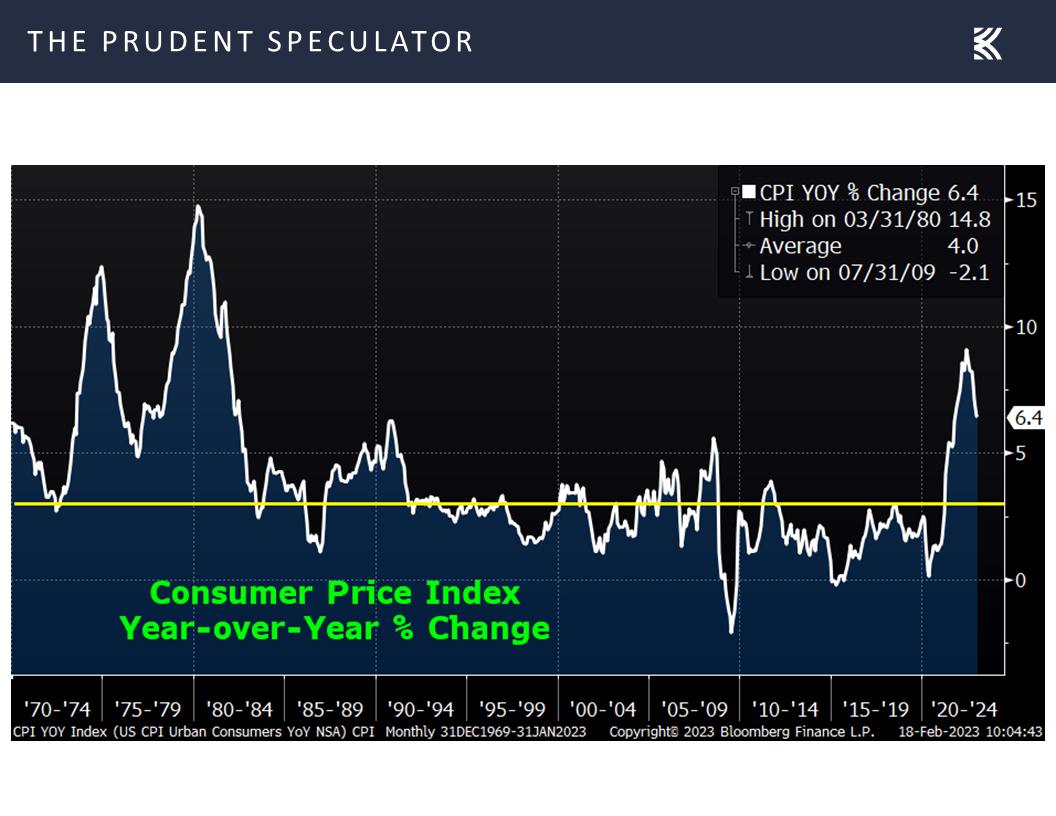

These days, healthy economic data seems to be more of a negative than a positive for stocks, as all eyes are on the Federal Reserve and its battle to keep inflation in check. Said fight is not going as well as some would like, given that the cost of living rose 0.5% in January, the largest hike in three months, with the year-over-year increase coming in at 6.4%, well above the long-term target for Jerome H. Powell & Co. of 2.0%.

Inflation at the consumer level pulled back a tad to 6.4% in January, while the core rate inched down to 5.6%.

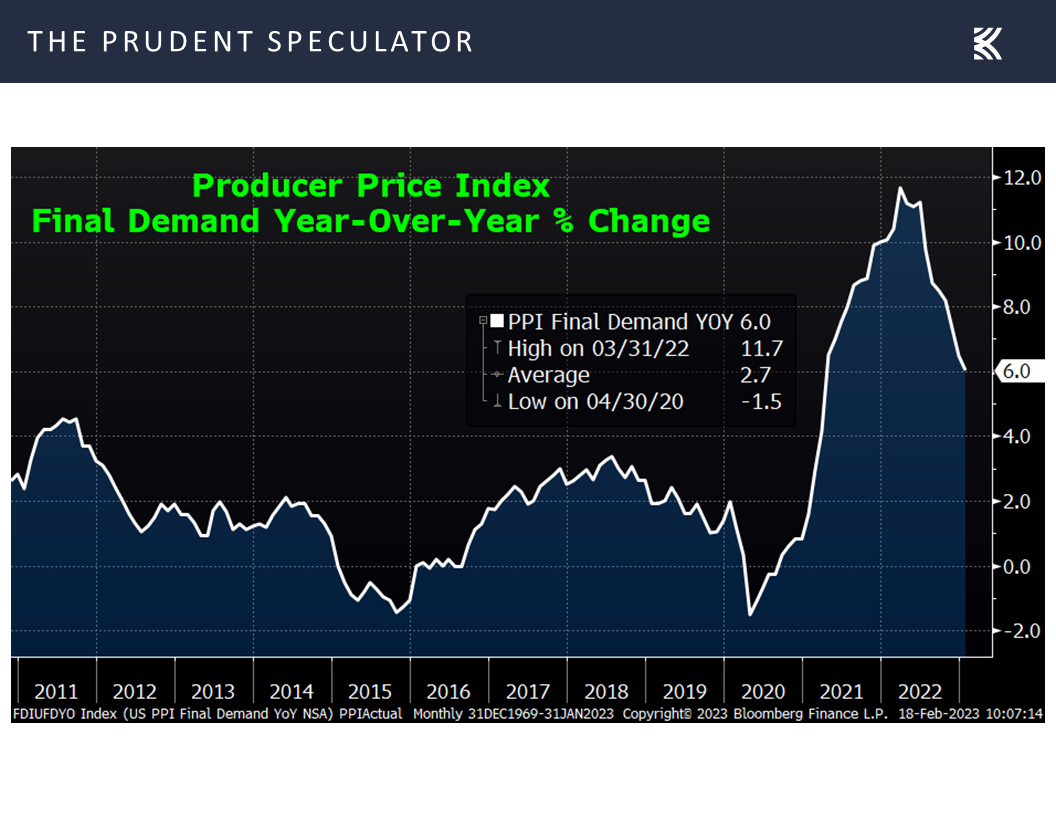

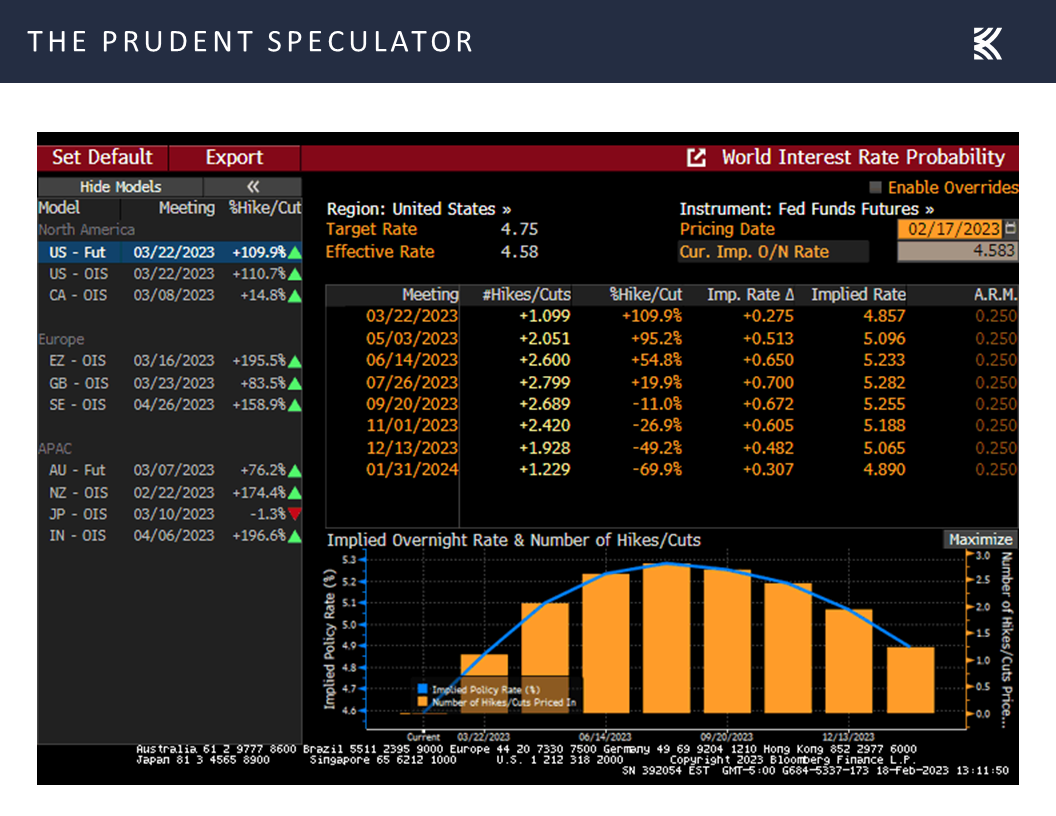

With prices at the wholesale level also remaining stubbornly high as the year-over-year increase in the Producer Price Index (PPI) came in at 6.0% last month, expectations that the Fed will remain tighter for longer increased last week, with the year-end 2023 market projection for the Fed Funds rate of 5.07% now in line with the FOMC’s most recent median forecast of 5.1% offered in December.

The Fed Fund futures became more hawkish last week, projecting a peak in the rate at more than 5.25% this summer.

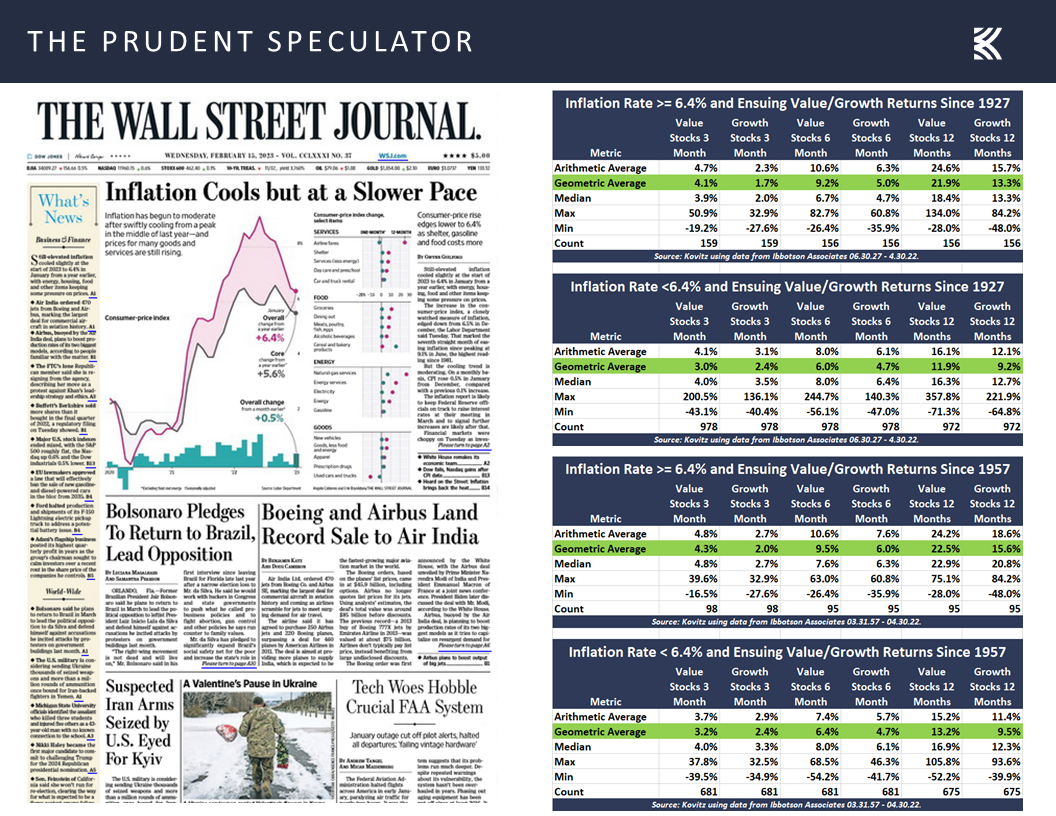

No doubt, there is plenty of hand wringing about the inflation level, even as equities since 1927 and since 1957 have proved to be a terrific hedge, on average, with Value stocks enjoying sensational ensuing returns when the Consumer Price Index (CPI) has been at 6.4% or higher.

There is plenty of consternation about elevated inflation levels, but history suggests that equities, especially Value stocks, have performed better when inflation is 6.4% or higher than when it is lower than that mark.

Fed Tightening & High Inflation: Historical Equity Return Perspective

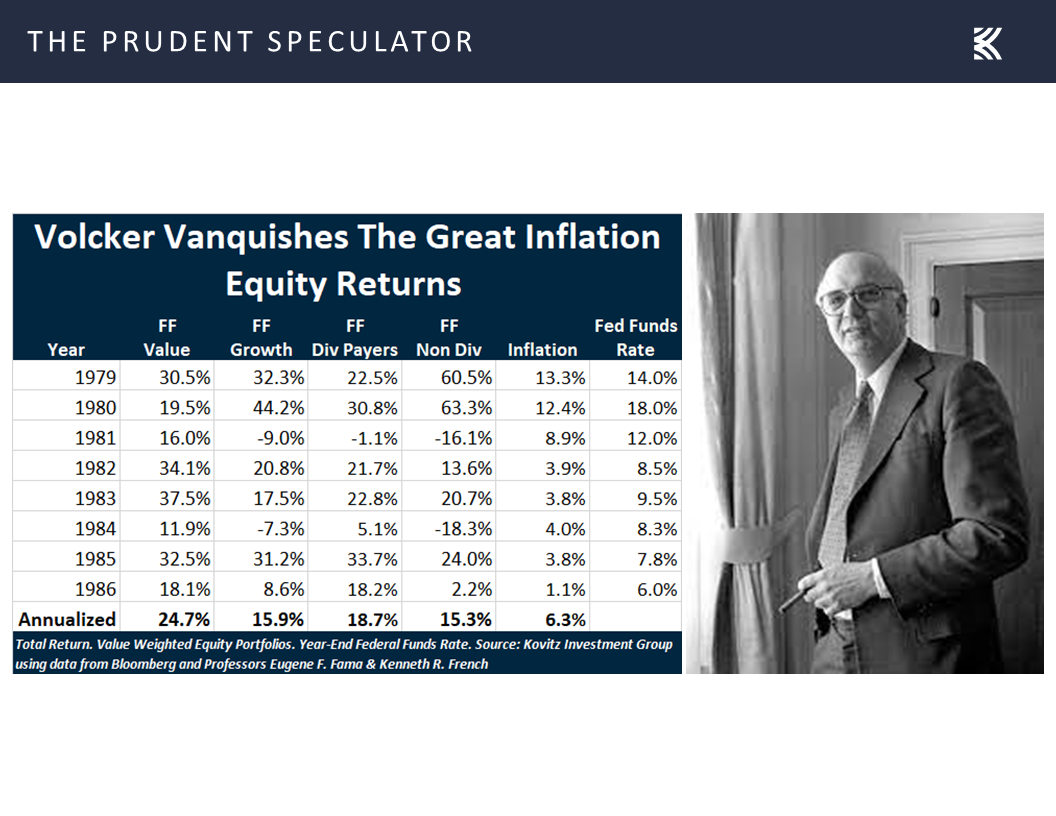

We also can’t forget that the last time the Federal Reserve had to confront sky-high inflation levels at the end of the 1970s, Fed Chair Paul Volcker ended up pushing the economy into recession on two occasions in 1980 and 1981. Interestingly, equity returns during his tenure from 1979 through 1986 were off the charts in a good way, with Value stocks gaining 24.7% PER ANNUM!

It is puzzling that so many fret about today’s Fed battle with inflation, given that the Volcker Fed’s fight against the Great Inflation saw sensational equity market returns despite recessions along the way.

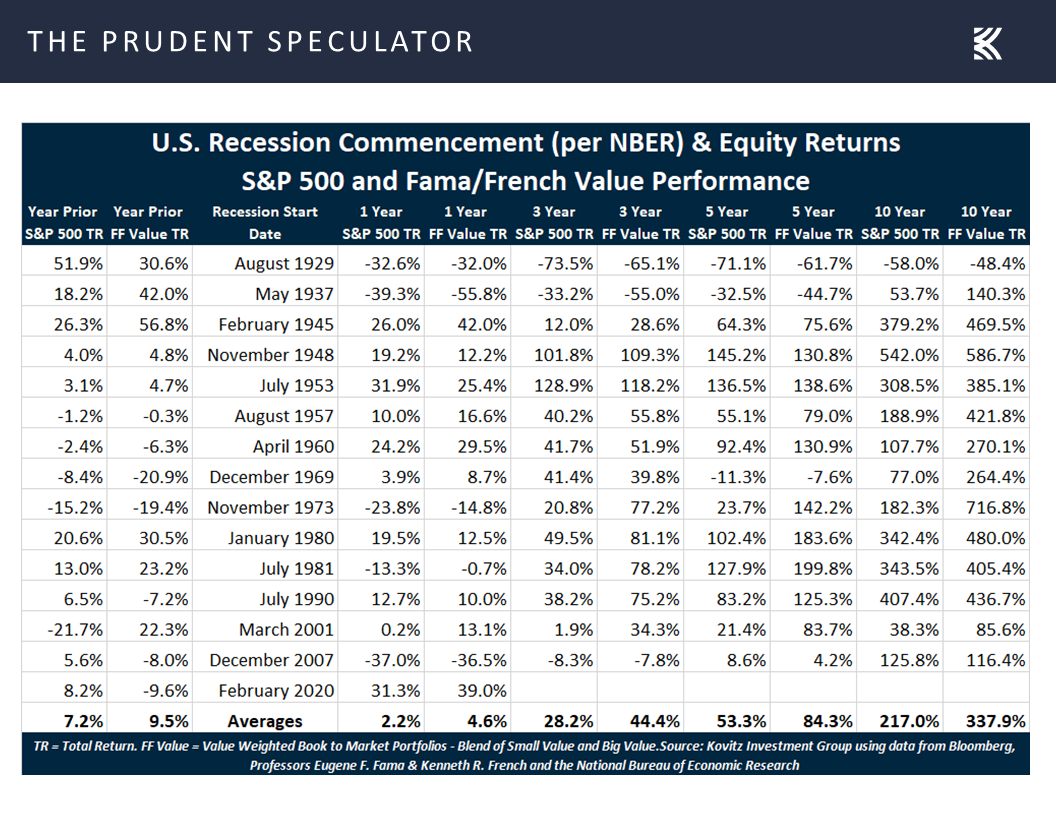

The Volcker years were different, of course, but we also point out that even if we knew that a recession was about to begin, the subsequent return numbers argue for staying the course with equities, on average, even for those with shorter-term time horizons.

There is much hand-wringing over a “hard” or “soft” landing, but the historical evidence shows that even if the U.S. economy officially enters a recession, long-term-oriented investors should stick with stocks.

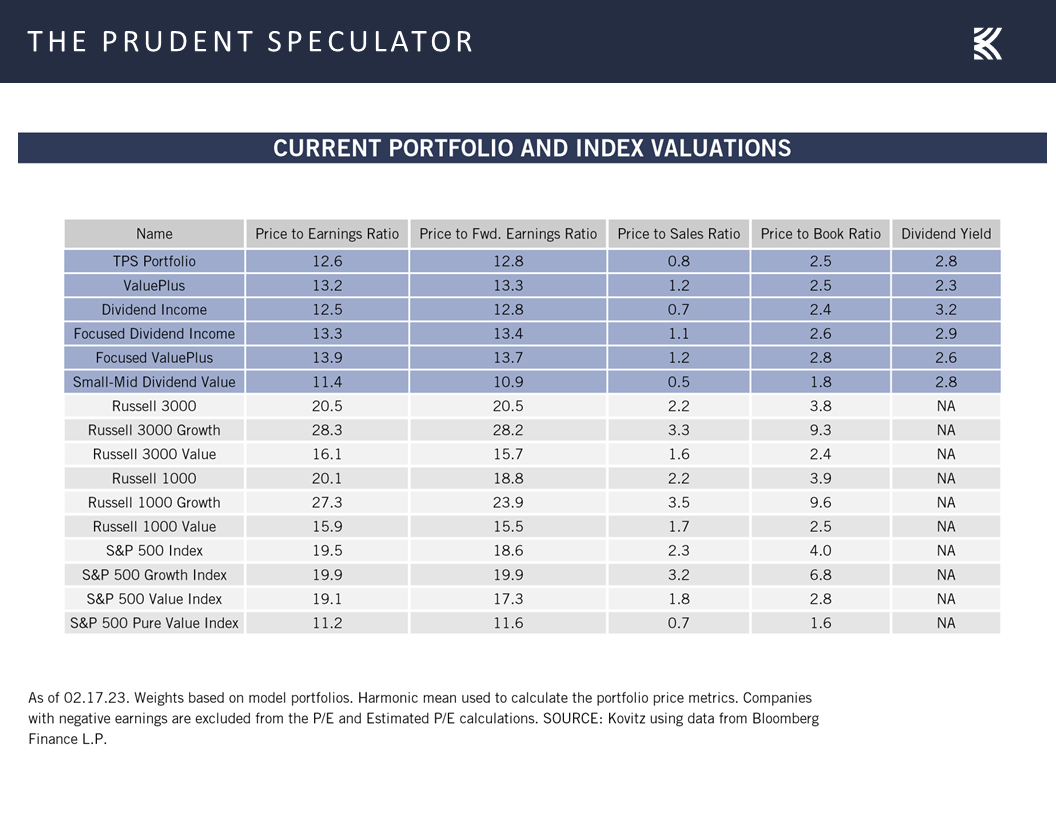

Valuations: Inexpensive Metrics for our Portfolios

We continue to see no reason to alter our long-term enthusiasm for the long-term prospects of our broadly diversified portfolios of what we believe to be undervalued stocks.

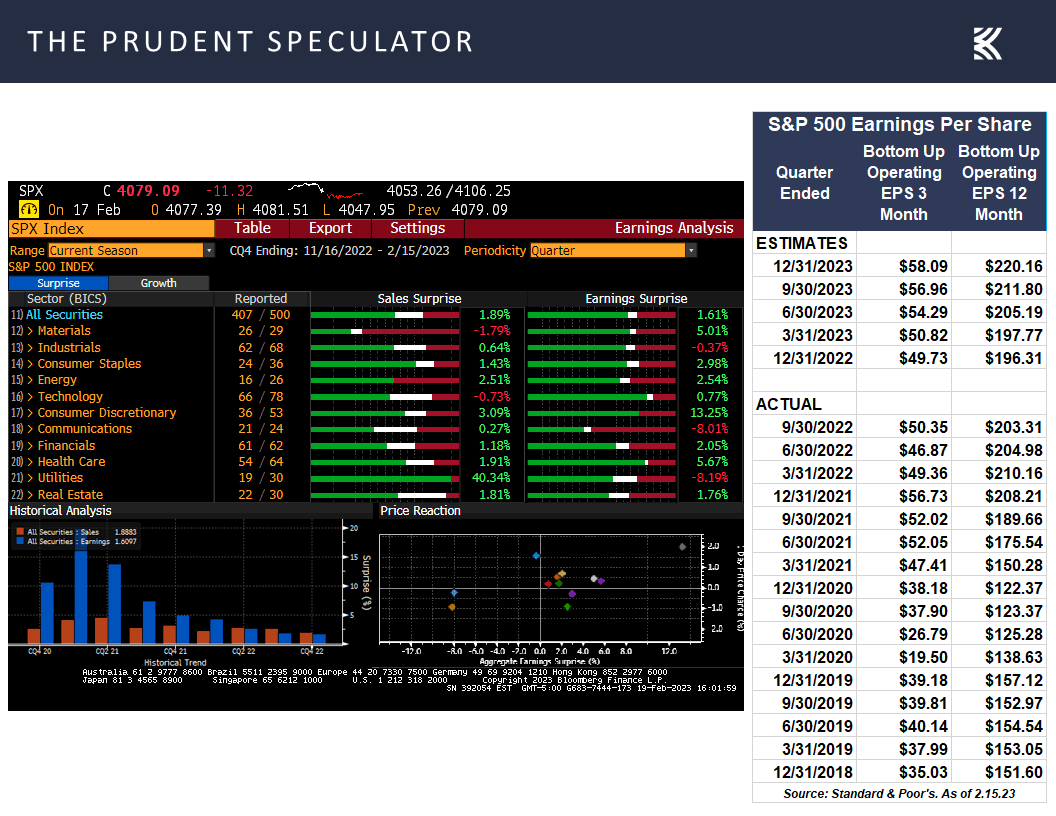

Corporate Profits: Solid Q4 EPS and Decent Outlook for 2023

Certainly, we realize that analysts are often overly optimistic in their earnings outlooks, but Q4 2022 results have been solid thus far and the outlook for 2023 is still for significantly higher EPS.

And it isn’t like we have much to complain about with stock returns so far in 2023, as we believe corporate profits will remain healthy with sizable EPS growth expected in 2023 over 2022.

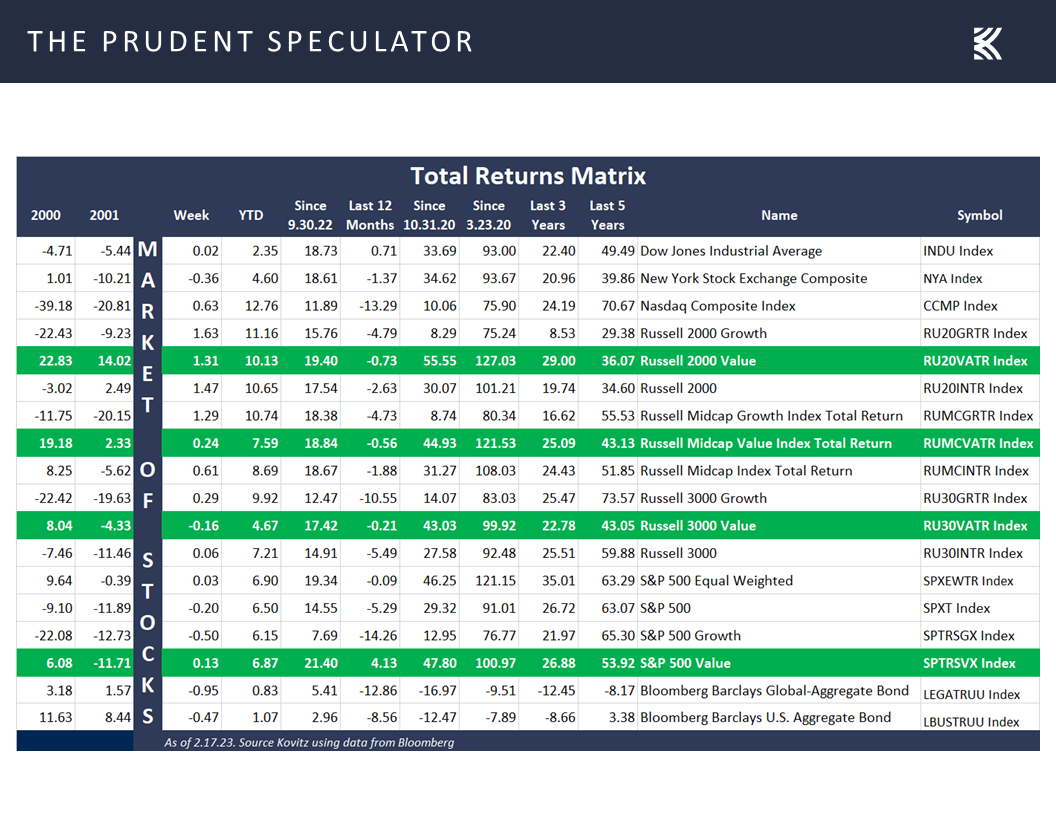

It is a market of stocks and returns over the last couple of years show wide dispersion, similar in magnitude to what was seen after the bursting of the Tech Bubble in the year 2000.

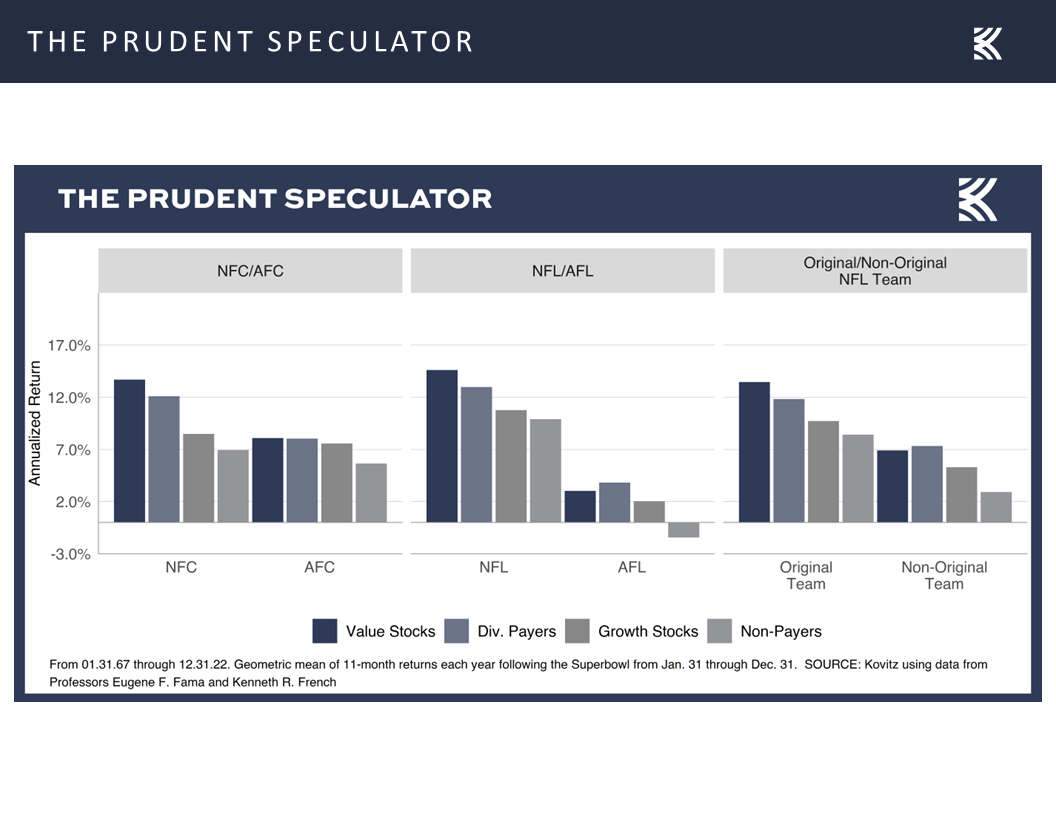

The Chiefs victory in a thrilling Super Bowl LVII was not what the Bulls might have liked, given that Kansas City is an AFC/AFL/Non-Original Team.

Stock News & Earnings – Updates on ten stocks across eight sectors

Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for several of our recommendations.

Stocks Historically Indifferent to Rising and Falling Rates

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. This week, we cover the rising and falling rate environments, volatility, AAII sentiment, the Fed tightening, corporate profits and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Interest Rates: Stocks Historically Indifferent to Rising/Falling Rates

Saturday’s edition of The New York Times told us, “Stocks Drop On Worries About Rates,” which we found interesting in that interest rates fell on Friday, with the yield on the 10-Year U.S. Treasury now a few basis points below where it began the year. The yield on the 10-Year U.S. Treasury is today about where it was at the start of 2023.

Of course, as we discuss in our latest Special Report, Consider Cheering Higher Rates, the historical evidence shows that equities have performed well, on average, whether interest rates are rising or falling, no matter how the data is sliced and diced.

Volatility: Ups and Downs Aplenty, but Long-Term Trend is Higher

Contrary to popular belief, equities, especially Value stocks, have performed admirably, on average, both concurrent with and subsequent to hikes in the Fed Funds rate.

The NY Times further explained, “Stocks have oscillated between gains and losses as new economic data have clouded the outlook for investors, marking a notable shift in the market after stocks jumped more than 6 percent in January.”

With all due respect to the financial journalism profession, the outlook for investors is always uncertain. About the only thing that is clear is that the equity markets will always endure substantial volatility over time as the significant number of 10% rallies and corrections since the launch of The Prudent Speculator 46 years ago will attest.

Ups and downs are not unusual for equities, as there have been 38 advances and 37 declines of 10% or greater since the launch of The Prudent Speculator 46 years ago.

Happily, the magnitude of the gains during the times in the green have dwarfed that of the losing periods, so much so that those who stick with stocks through thick and thin have been handsomely rewarded in the fullness of time with annualized returns ranging from 8.8% to 13.2%.

The secret to success in stocks is not to get scared out of them as every downturn has been followed by an upswing of far greater magnitude, so much so that long-term returns for Value stocks have exceeded 13% per annum.

Sentiment: AAII More Pessimistic than Usual

Easier said than done, we know, as far too many folks end up zigging when they should have zagged, which is why sentiment gauges like the one compiled each week since 1987 from the American Association of Individual Investors (AAII) have proven to be contra-indicators. Indeed, the admonition to be greedy when others are fearful is based on sound empirical evidence and today we continue to see less optimism and more pessimism than usual from the folks on Main Street.

The good folks in the AAII Sentiment Survey became a little more pessimistic last week, which is a good thing for potential near-term equity market gains.

Econ Numbers: Mixed Picture; More Good than Bad

To be fair to our friends at the Times, the economic outlook is especially confounding these days as economists suggest the odds of recession are very high, while the latest Leading Economic Index fell by 0.3% in January.

The keeper of that gauge, the Conference Board, explained:

The U.S. LEI remained on a downward trajectory, but its rate of decline moderated slightly in January. Among the leading indicators, deteriorating manufacturing new orders, consumers’ expectations of business conditions, and credit conditions more than offset strengths in labor markets and stock prices to drive the index lower in the month. The contribution of the yield spread component of the LEI also turned negative in the last two months, which is often a signal of recession to come. While the LEI continues to signal recession in the near term, indicators related to the labor market—including employment and personal income—remain robust so far. Nonetheless, The Conference Board still expects high inflation, rising interest rates, and contracting consumer spending to tip the US economy into recession in 2023.

The Conference Board’s Leading Economic Index dropped “only” 0.3% in January, an improvement from December’s 0.8% decline.

That outlook sounds ominous, especially as the manufacturing sector is arguably already in contraction, given the latest negative readings on East Coast factory activity

Two key manufacturing gauges are in contraction, though the Empire Fed factory index improved markedly this month.

but the labor picture remains incredibly strong, with weekly initial filings for jobless claims still below 200,000, a level not seen since the 1960s when the workforce was much smaller and consumer spending has held up remarkably well as evidenced by a much-better-than-expected retail sales tally in January.

Retails sales started the year strong, with the 3% jump in January the best monthly gain in nearly two years.

Though they are still at very depressed levels, even the latest sentiment gauges for small business and home-builders ticked higher, with the net result of the latest economic numbers leading to an increase in the outlook for Q1 U.S. GDP growth from the Atlanta Fed last week.

It is fascinating to see so much pessimism toward the U.S. economy when the current estimate for Q1 real (inflation-adjusted) GDP growth stands at a decent level.

Inflation: CPI & PPI Higher than Expected; Fed Likely to Remain Hawkish

These days, healthy economic data seems to be more of a negative than a positive for stocks, as all eyes are on the Federal Reserve and its battle to keep inflation in check. Said fight is not going as well as some would like, given that the cost of living rose 0.5% in January, the largest hike in three months, with the year-over-year increase coming in at 6.4%, well above the long-term target for Jerome H. Powell & Co. of 2.0%.

Inflation at the consumer level pulled back a tad to 6.4% in January, while the core rate inched down to 5.6%.

With prices at the wholesale level also remaining stubbornly high as the year-over-year increase in the Producer Price Index (PPI) came in at 6.0% last month, expectations that the Fed will remain tighter for longer increased last week, with the year-end 2023 market projection for the Fed Funds rate of 5.07% now in line with the FOMC’s most recent median forecast of 5.1% offered in December.

The Fed Fund futures became more hawkish last week, projecting a peak in the rate at more than 5.25% this summer.

No doubt, there is plenty of hand wringing about the inflation level, even as equities since 1927 and since 1957 have proved to be a terrific hedge, on average, with Value stocks enjoying sensational ensuing returns when the Consumer Price Index (CPI) has been at 6.4% or higher.

There is plenty of consternation about elevated inflation levels, but history suggests that equities, especially Value stocks, have performed better when inflation is 6.4% or higher than when it is lower than that mark.

Fed Tightening & High Inflation: Historical Equity Return Perspective

We also can’t forget that the last time the Federal Reserve had to confront sky-high inflation levels at the end of the 1970s, Fed Chair Paul Volcker ended up pushing the economy into recession on two occasions in 1980 and 1981. Interestingly, equity returns during his tenure from 1979 through 1986 were off the charts in a good way, with Value stocks gaining 24.7% PER ANNUM!

It is puzzling that so many fret about today’s Fed battle with inflation, given that the Volcker Fed’s fight against the Great Inflation saw sensational equity market returns despite recessions along the way.

The Volcker years were different, of course, but we also point out that even if we knew that a recession was about to begin, the subsequent return numbers argue for staying the course with equities, on average, even for those with shorter-term time horizons.

There is much hand-wringing over a “hard” or “soft” landing, but the historical evidence shows that even if the U.S. economy officially enters a recession, long-term-oriented investors should stick with stocks.

Valuations: Inexpensive Metrics for our Portfolios

We continue to see no reason to alter our long-term enthusiasm for the long-term prospects of our broadly diversified portfolios of what we believe to be undervalued stocks.

Corporate Profits: Solid Q4 EPS and Decent Outlook for 2023

Certainly, we realize that analysts are often overly optimistic in their earnings outlooks, but Q4 2022 results have been solid thus far and the outlook for 2023 is still for significantly higher EPS.

And it isn’t like we have much to complain about with stock returns so far in 2023, as we believe corporate profits will remain healthy with sizable EPS growth expected in 2023 over 2022.

It is a market of stocks and returns over the last couple of years show wide dispersion, similar in magnitude to what was seen after the bursting of the Tech Bubble in the year 2000.

The Chiefs victory in a thrilling Super Bowl LVII was not what the Bulls might have liked, given that Kansas City is an AFC/AFL/Non-Original Team.

Stock News & Earnings – Updates on ten stocks across eight sectors

Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for several of our recommendations.

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.