The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Federal Reserve, Inflation, Valuations, Interest Rates and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Big Weekly Rally – Soldiers Beat the Generals

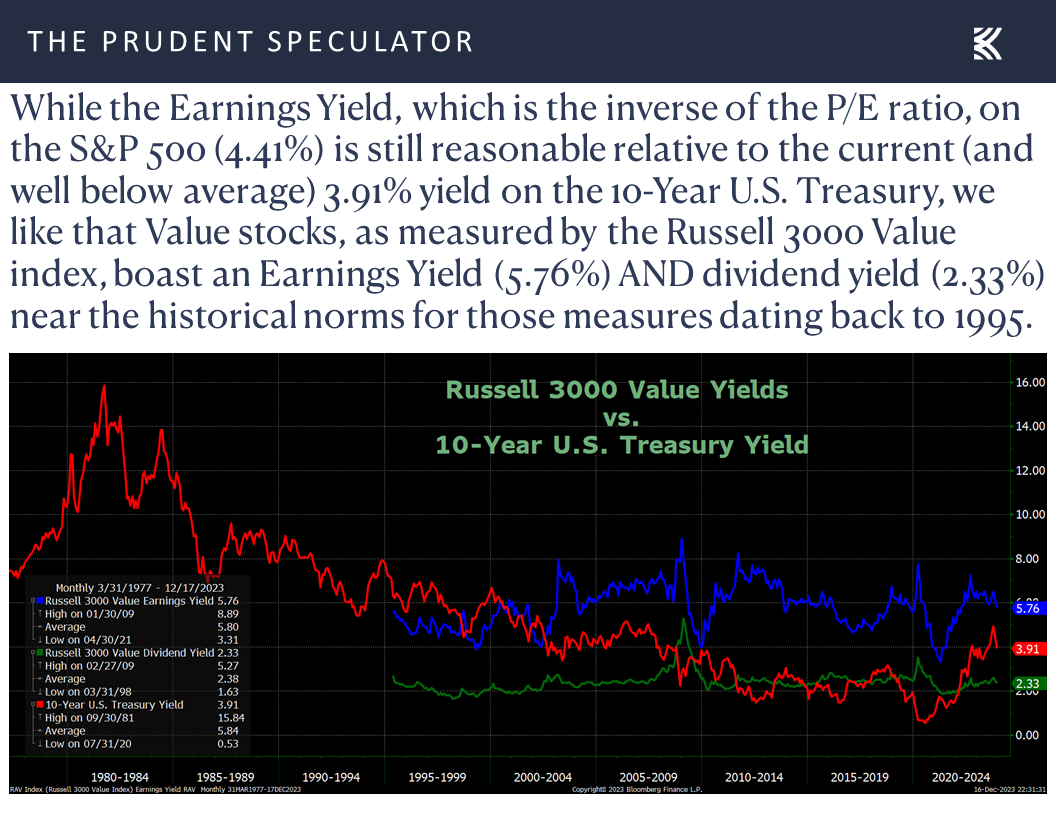

Valuations – Value Stocks Reasonably Priced

Inflation – CPI & PPI Trending in the Right Direction

Fed – FOMC Statement and Press Conference Suggest Rate Hikes are Done

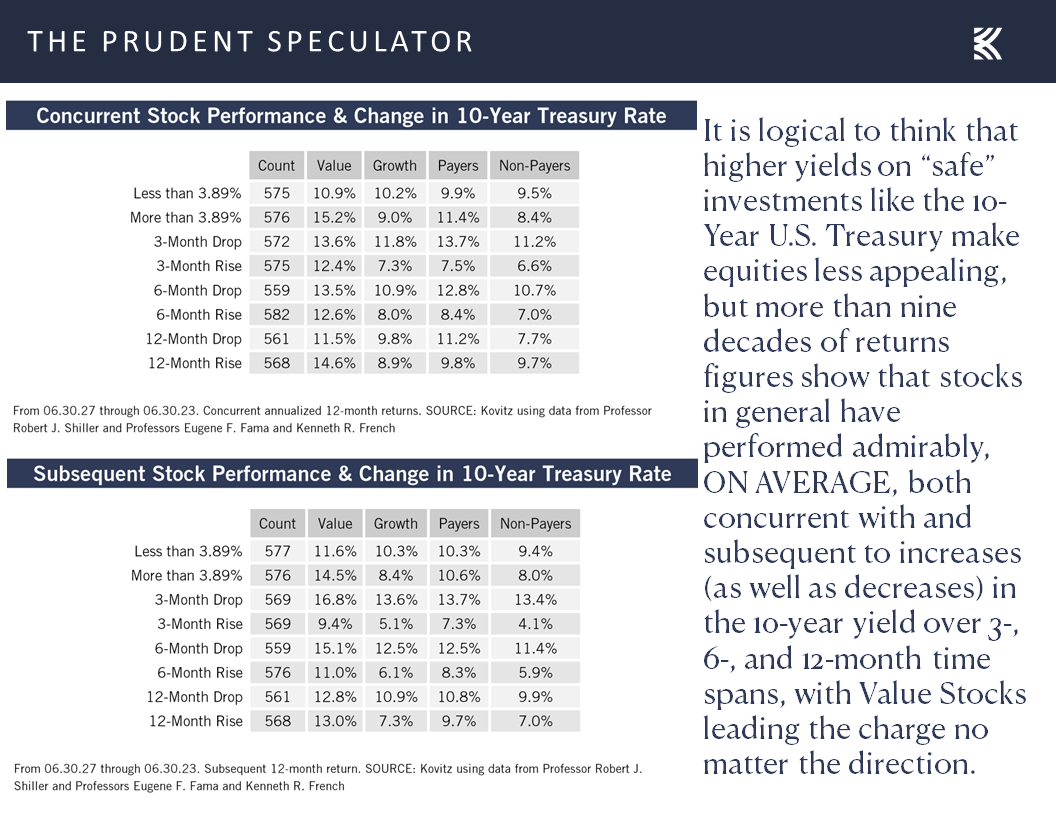

Interest Rates & Stocks – Equities Perform Fine, on Average, in Rising and Falling Rate Environments

Econ News – GDP Growth Outlook Improves

Sentiment – Still Plenty of Skepticism

Stock News – Updates on eight stocks across five different sectors

Big Weekly Rally – Soldiers Beat the Generals

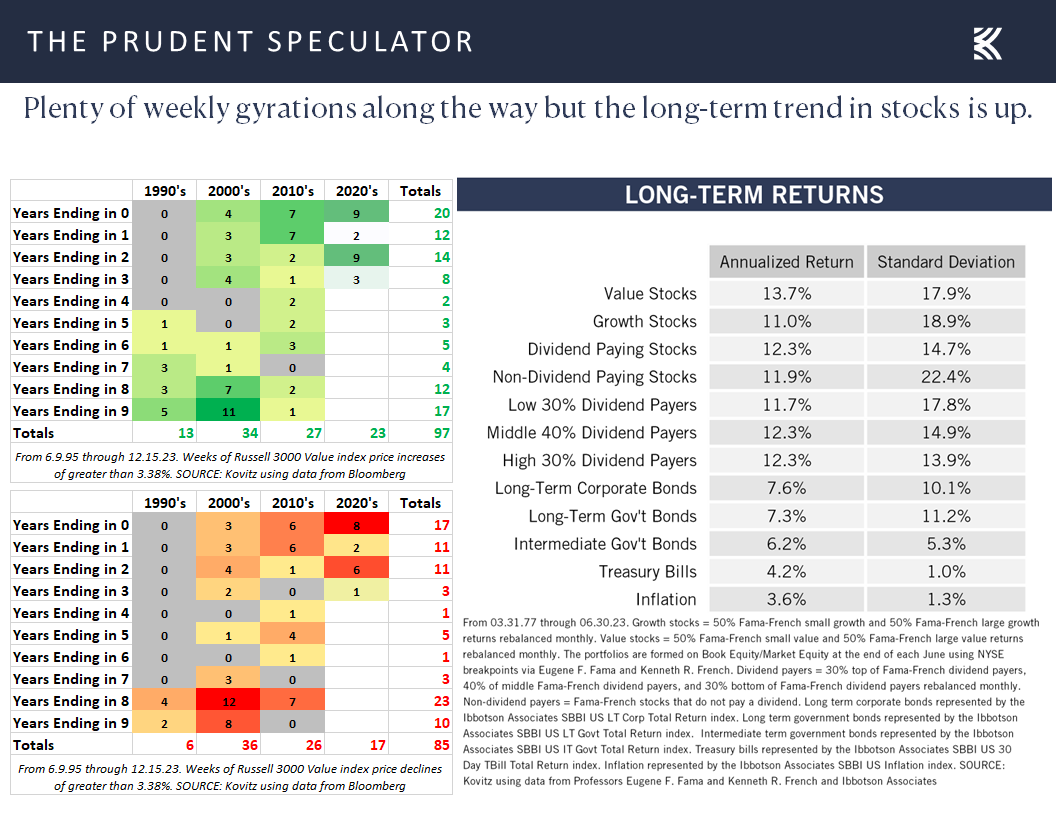

Even with Friday’s pullback in the average stock, it was a fantastic five days for equities as the proverbial Soldiers outperformed the Generals by a solid margin. Even better, the Russell 3000 Value (R3KV) index topped its Russell 3000 Growth (R3KG) counterpart, turning in its 97th best weekly price performance over the past 28 years with a gain of 3.38% and providing another reminder that the historical odds have long favored the buyer and holder of inexpensively priced stocks.

Valuations – Value Stocks Reasonably Priced

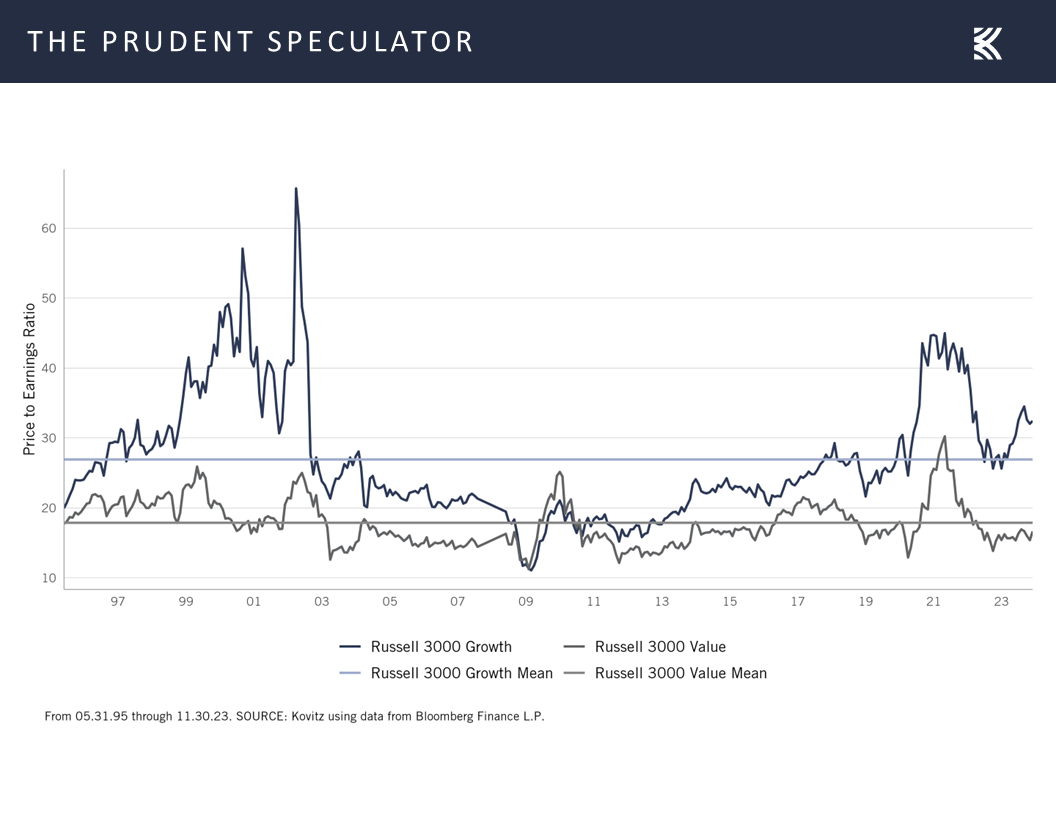

In addition to its historical propensity for outperformance, we shouldn’t be surprised by Value’s recent resurgence, given that the R3KV has been trading below its long-term norm on a price-to-earnings basis while the R3KG has been priced well above its historical average. In short, Value stocks are cheap on both a relative and absolute basis.

Inflation – CPI & PPI Trending in the Right Direction

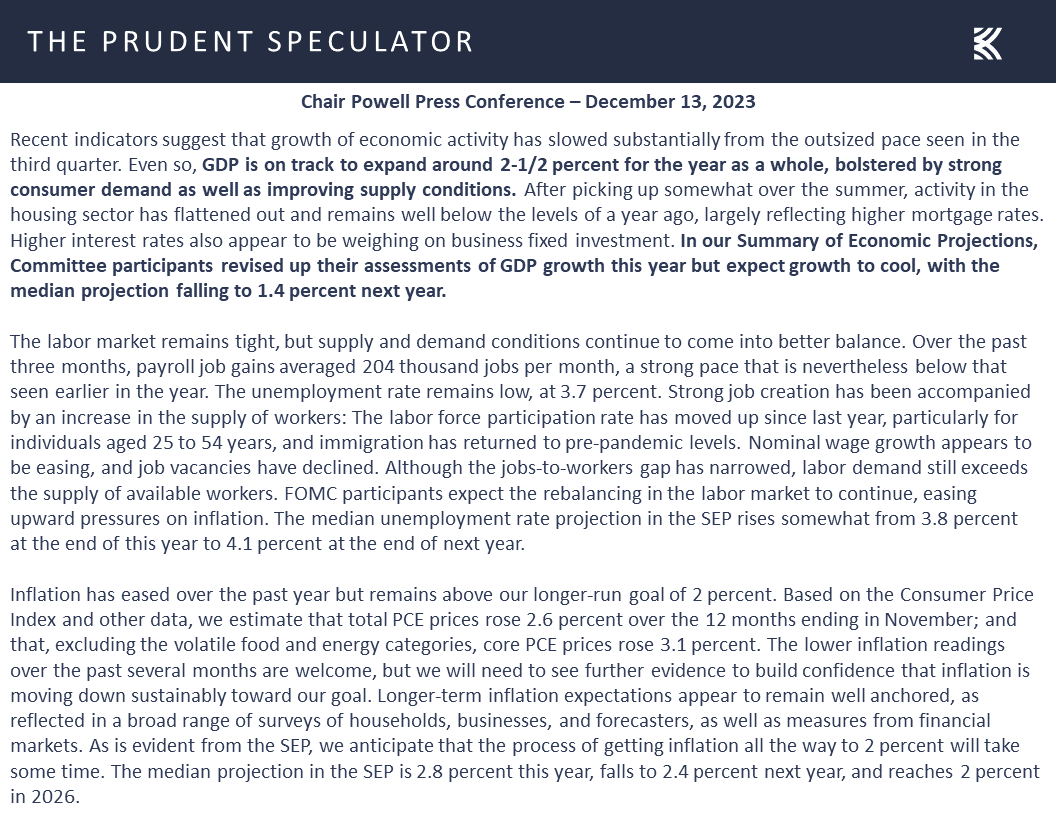

Of course, the equity markets enjoyed a terrific advance on Wednesday and Thursday, following the release of the December FOMC Statement and the responses offered by Fed Chair Jerome H. Powell at the FOMC Press Conference.

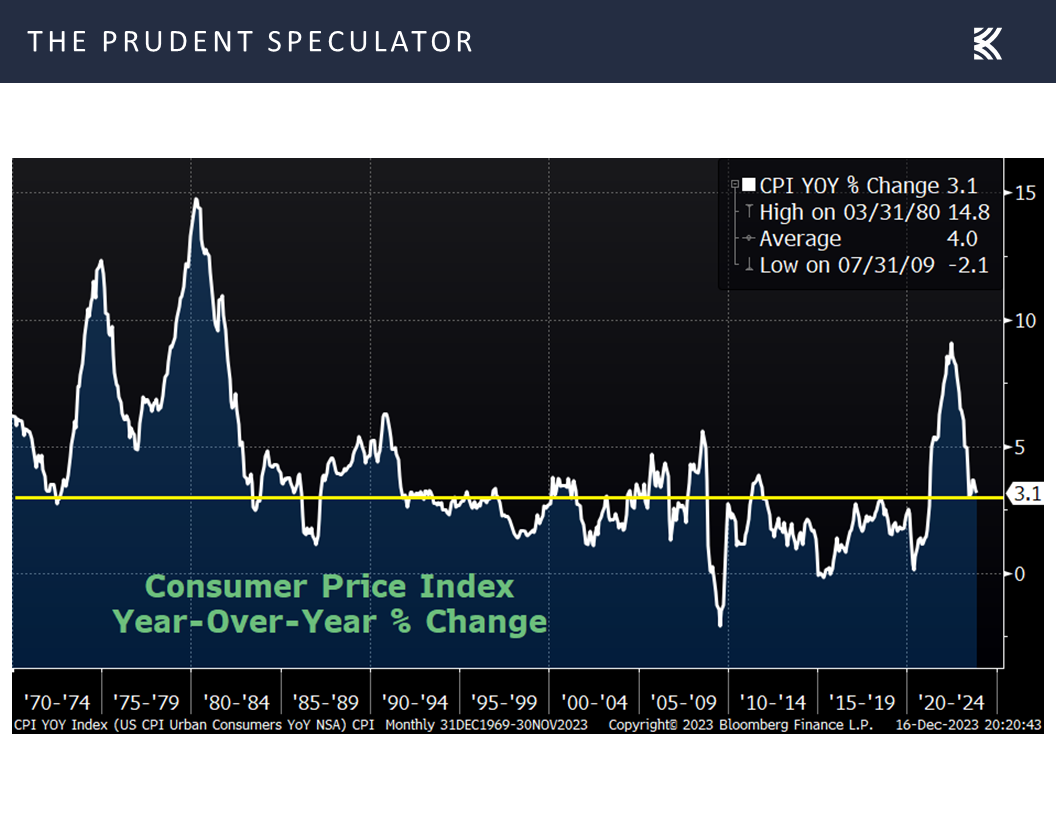

With continued progress on inflation revealed earlier in the week as the year-over-year change in the Consumer Price Index (CPI) dropped to 3.1% in November, down from 3.2% in October,

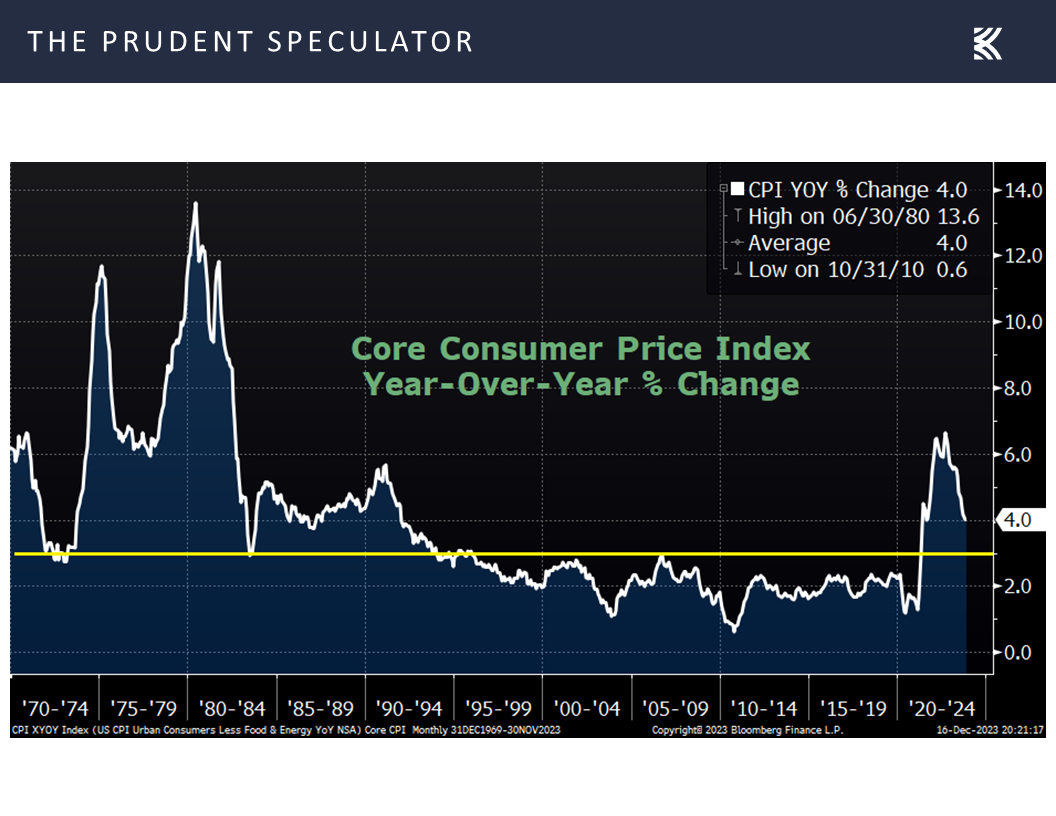

while the Core CPI (excludes volatile food and energy) held steady at a 4.0% annual increase,

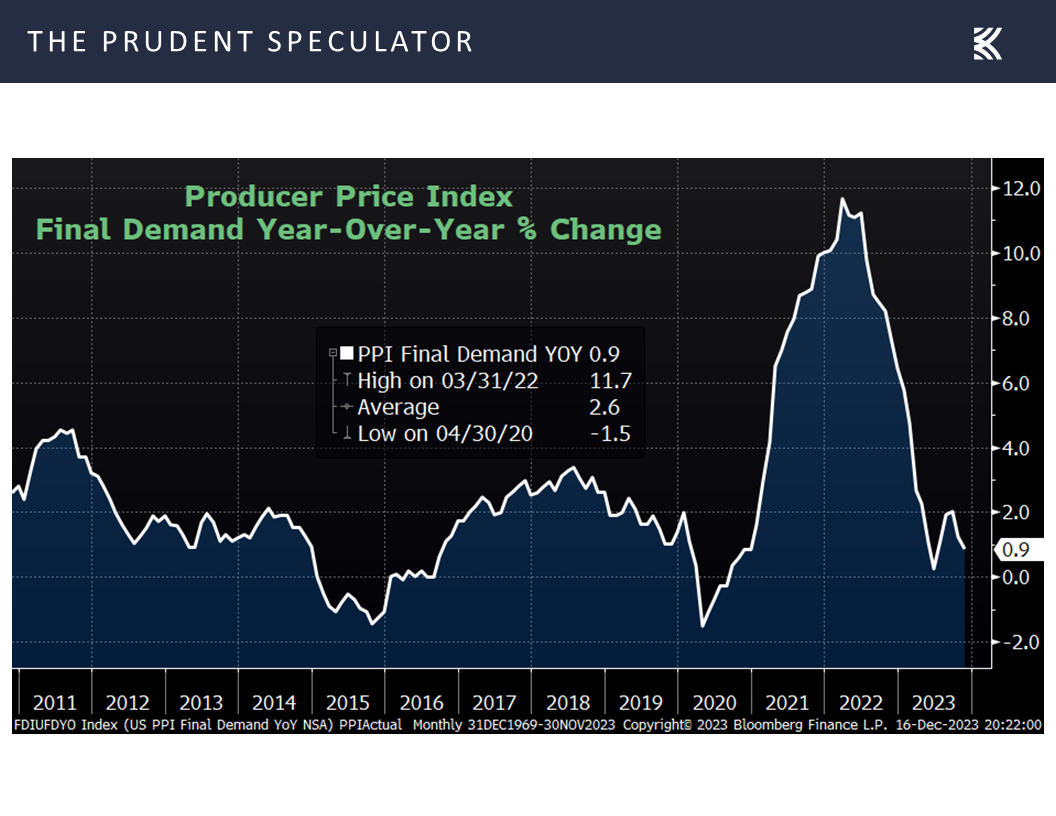

and the Producer Price Index rose only 0.9% on an annual basis, down from 1.3% the month prior,

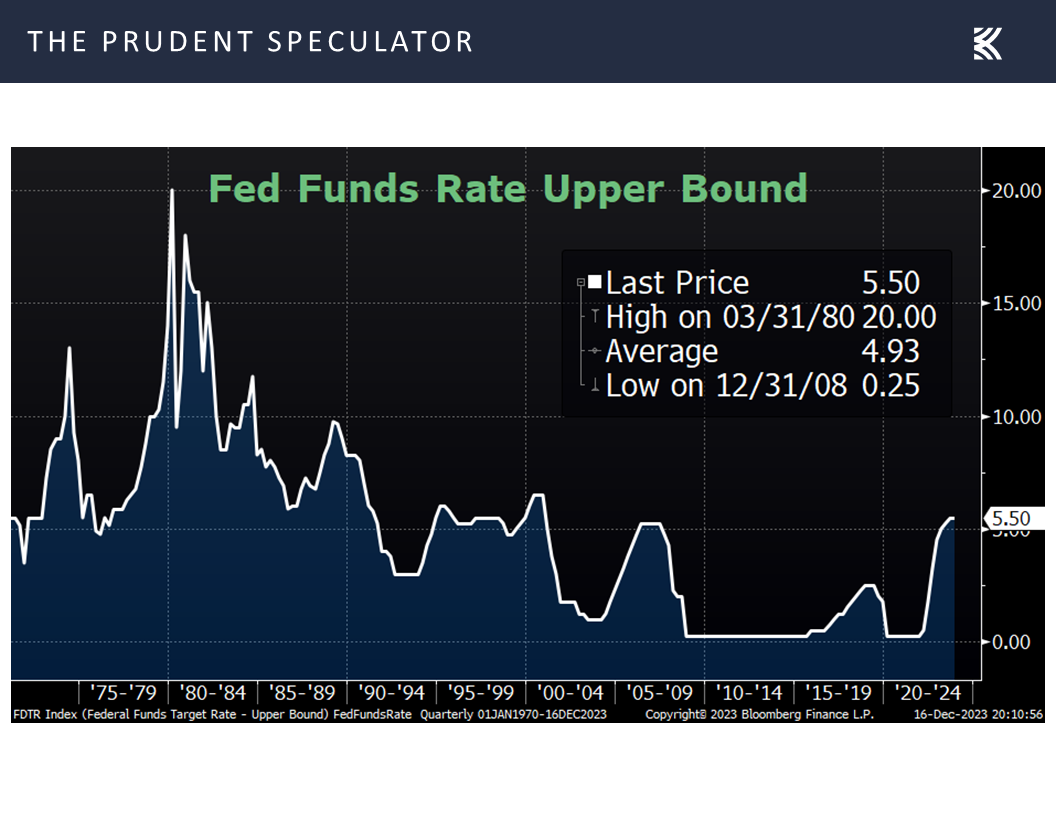

the Fed left the target for the Fed Funds rate unchanged at a range of 5.25% to 5.50%.

the Fed left the target for the Fed Funds rate unchanged at a range of 5.25% to 5.50%.

Fed – FOMC Statement and Press Conference Suggest Rate Hikes are Done

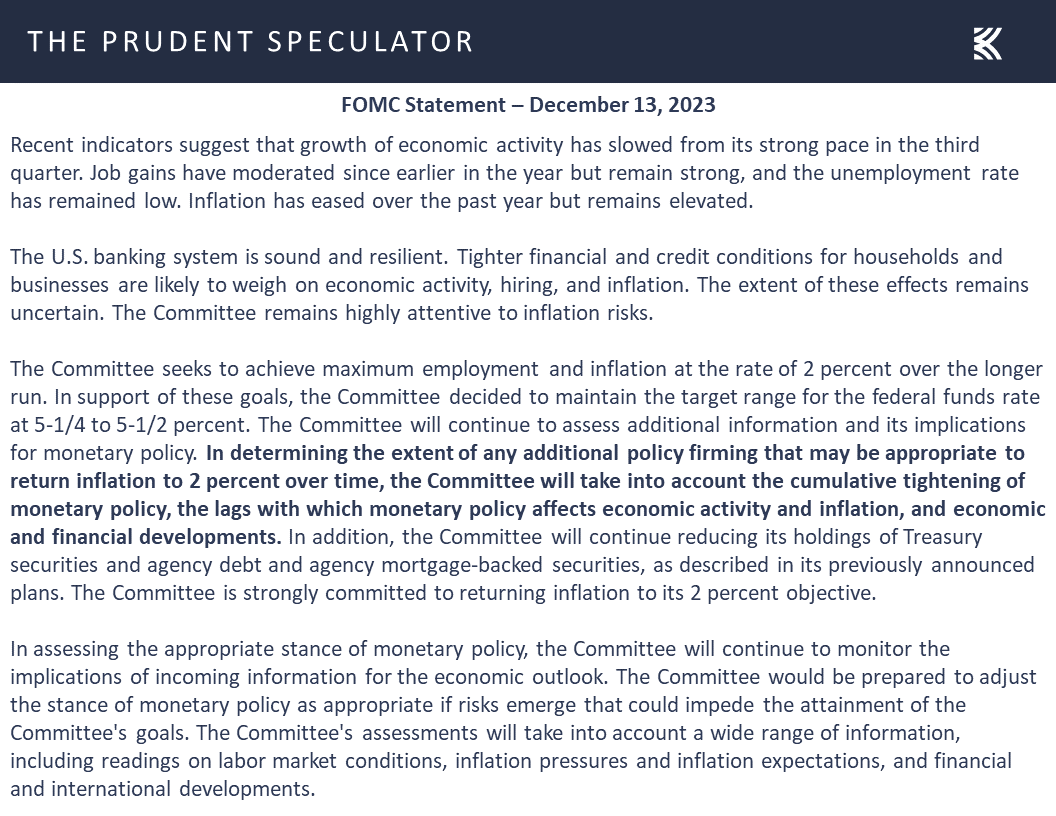

More importantly, the FOMC Statement augmented the view of many market participants that Powell & Co. have reached the end of their rate-hiking cycle, via the addition of the word “any” to the “additional policy firming” language,

as did the first Q&A of the Powell Press Conference:

Q: I wanted to ask, how should we interpret the addition of the word “any” before additional firming in the statement. I mean does that mean that you’re pretty much done with rate hikes, and the Committee has shifted away from a tightening bias and toward a more neutral stance? Thank you.

A: So, specifically on “any,” we do say that in determining the extent of any additional policy firming that may be appropriate. So any additional policy firming, that sentence. So we added the word “any” as an acknowledgement that we believe that we are likely at or near the peak rate for this cycle. Participants didn’t write down additional hikes that we believe are likely, so that’s what we wrote down. But participants also didn’t want to take the possibility of further hikes off the table. So that’s really what we were thinking.

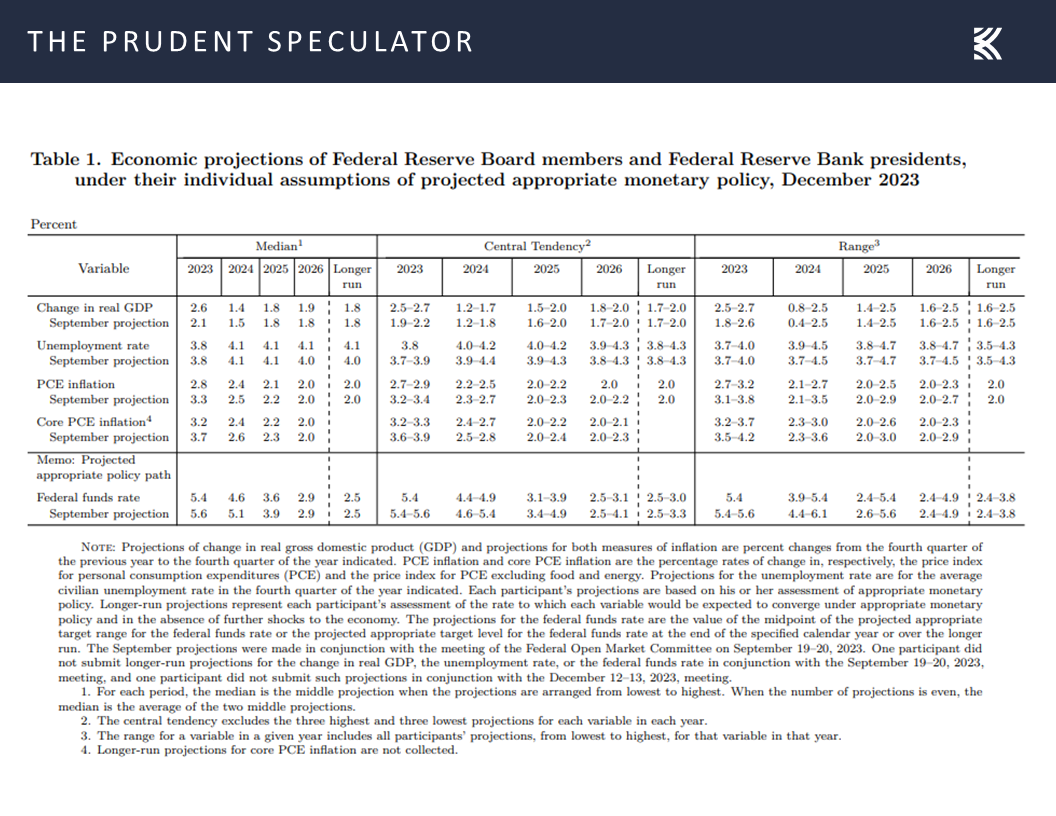

While those FOMC participants Mr. Powell referenced lowered their median outlook for the year-end 2024 Fed Funds rate to 4.6%, down from 5.1% three months ago,

Interest Rates & Stocks – Equities Perform Fine, on Average, in Rising and Falling Rate Environments

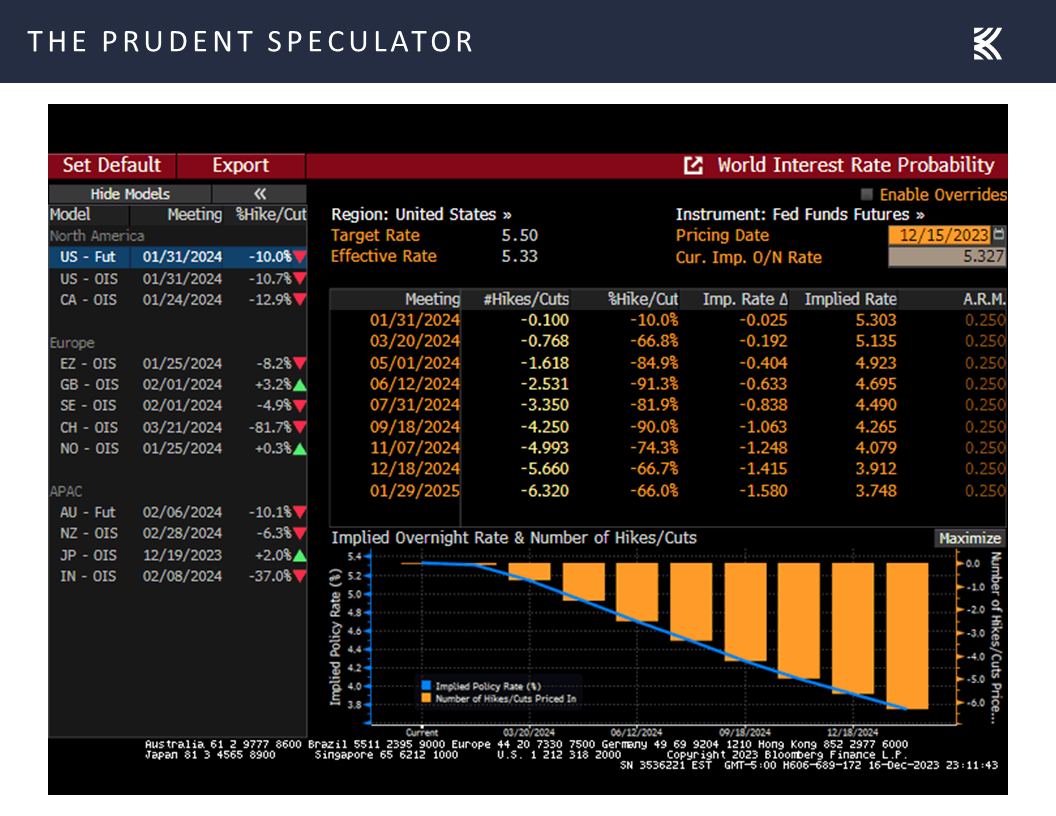

the response in the Fed Funds futures market was more dramatic, with traders now betting on a big drop in the benchmark lending rate to below 4% by the end of next year,

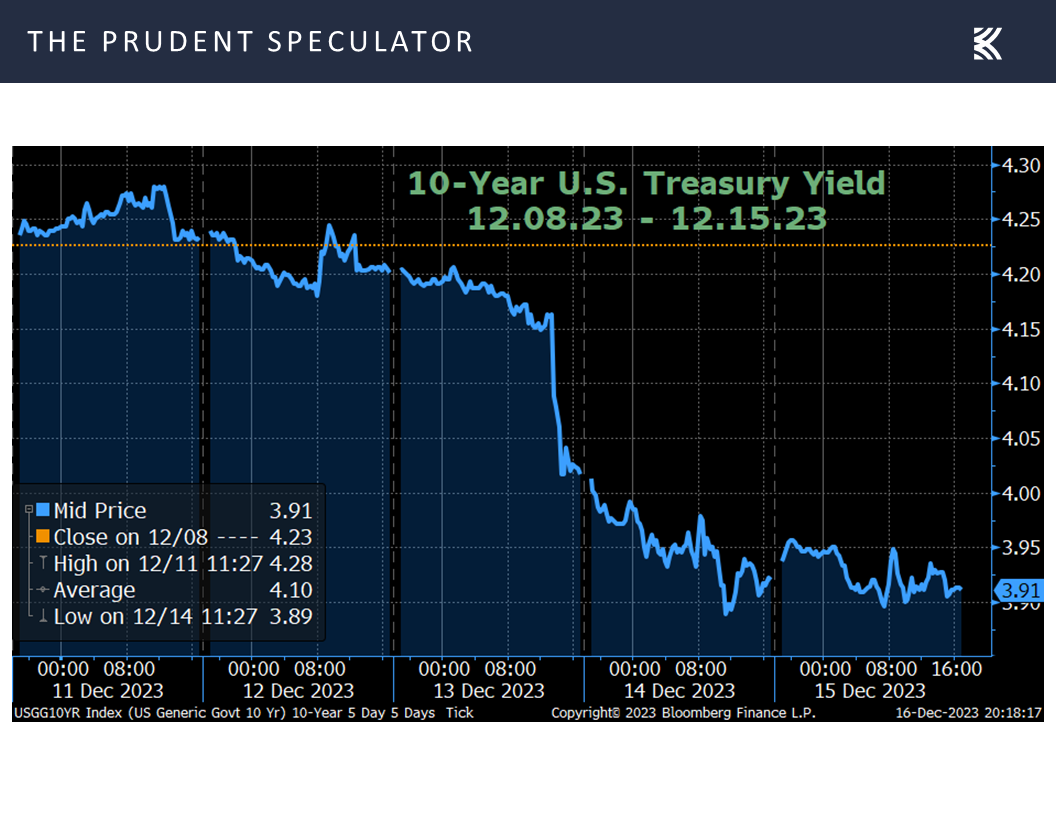

leading to a big rally in long-term government bonds last week which sent the yield on the 10-Year U.S. Treasury plunging to 3.91% from 4.23% the week prior.

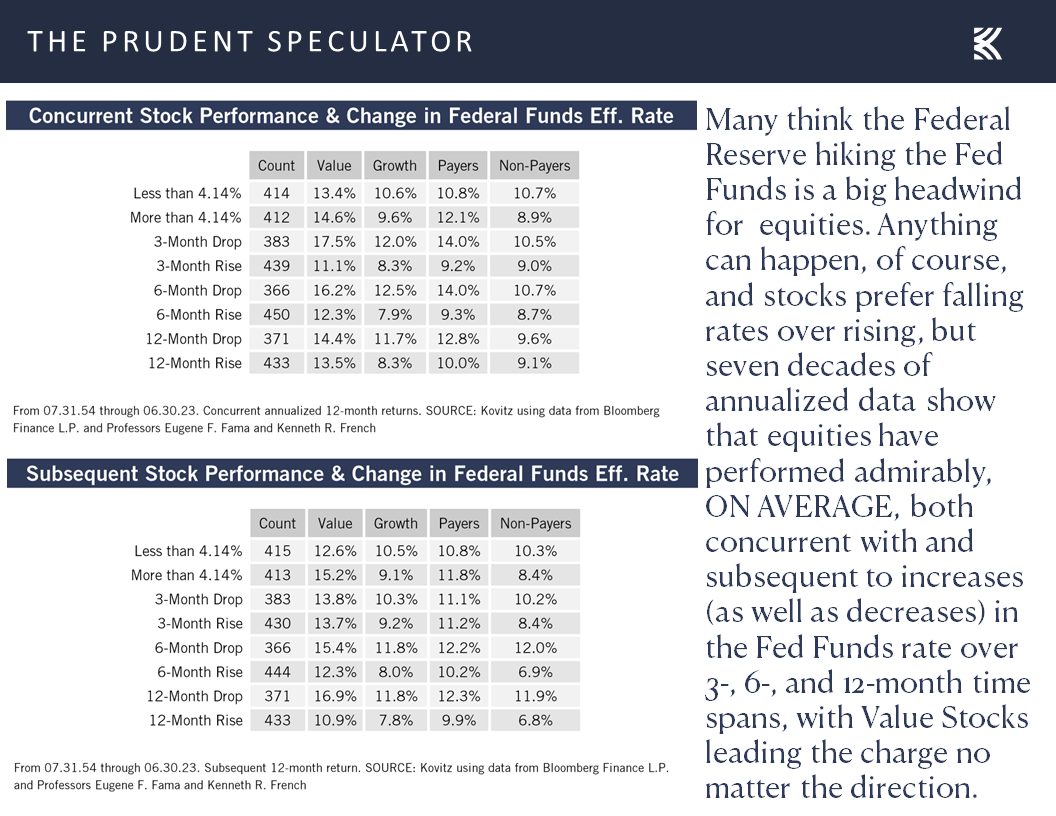

Now, history suggests that stocks, especially Value, have performed fine whether the Fed Funds rate is rising or falling,

and whether the 10-Year Treasury yield is moving up or down,

but lower interest rates add to the valuation argument in support of equities.

Econ News – GDP Growth Outlook Improves

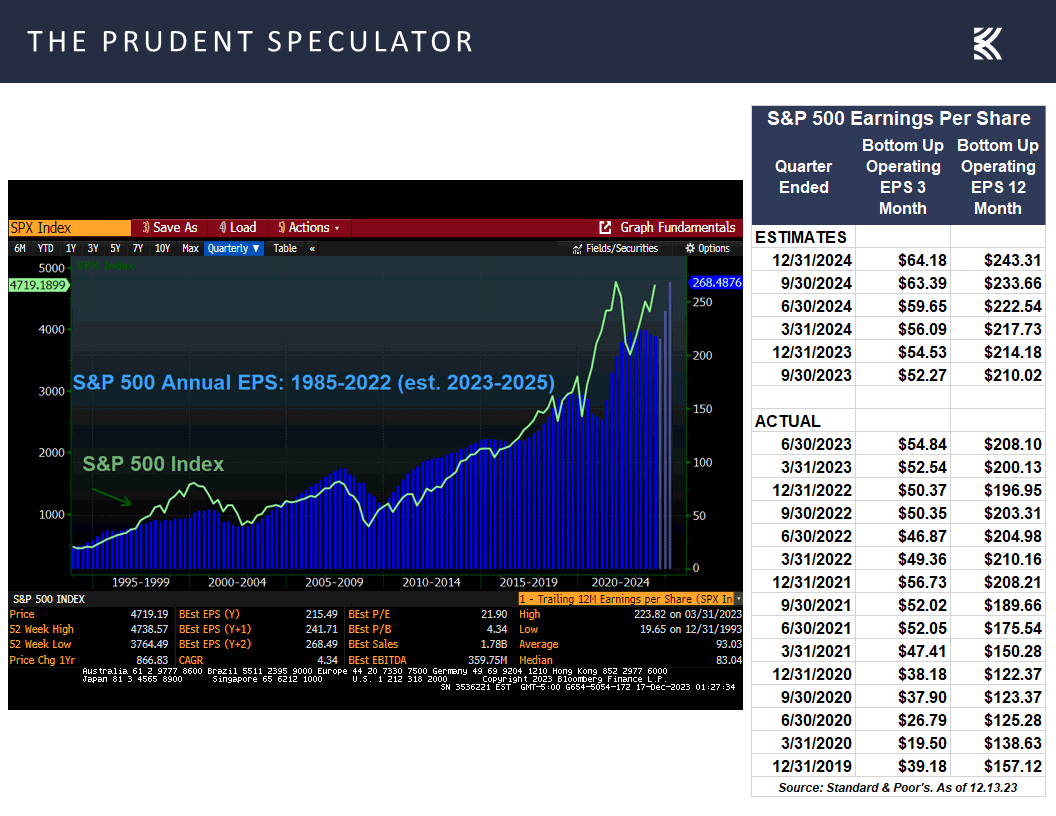

This is especially true, given that the outlook for corporate profits remains healthy,

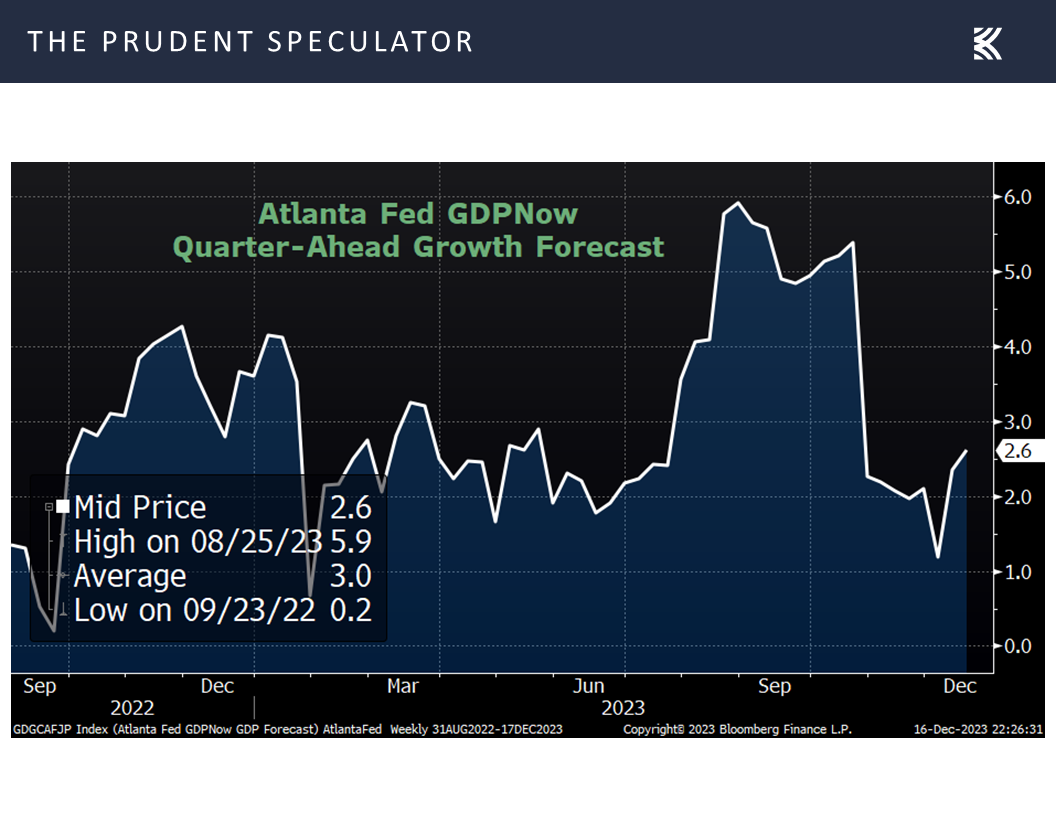

with the Q4 U.S. real (inflation-adjusted) GDP projection from the Atlanta Fed rising to 2.6% last week from 1.2% a week ago,

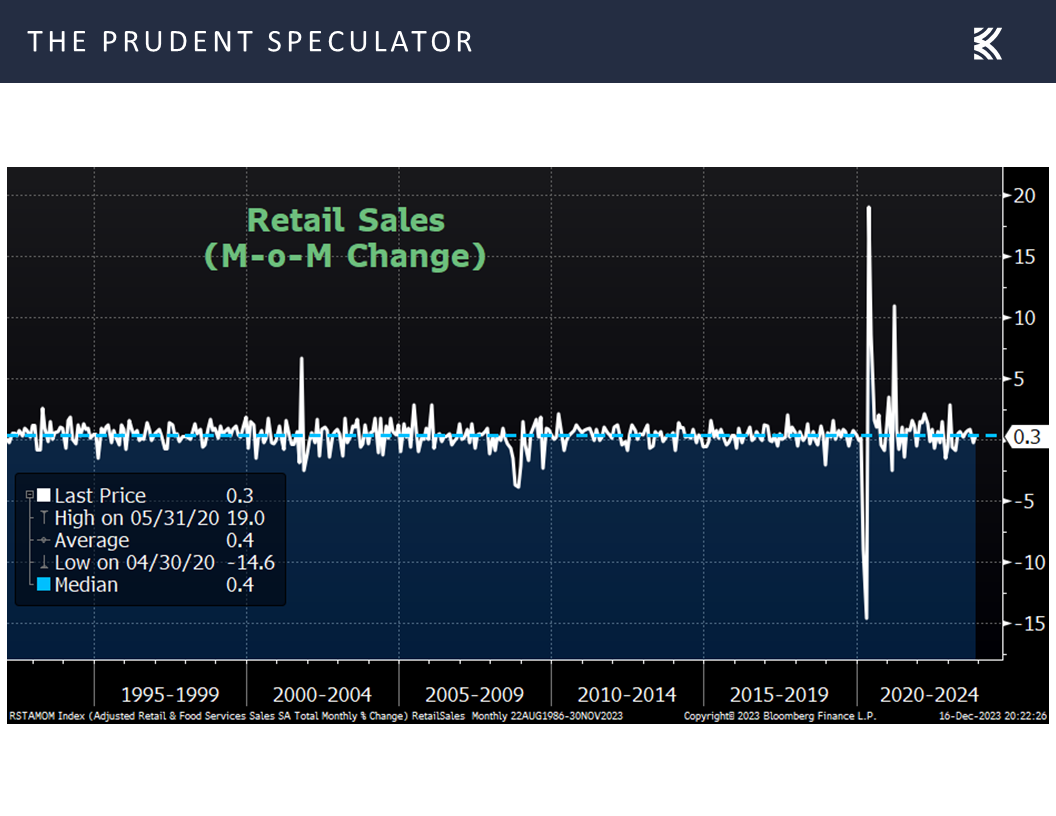

as retail sales came in better than expected in November with a 0.3% increase,

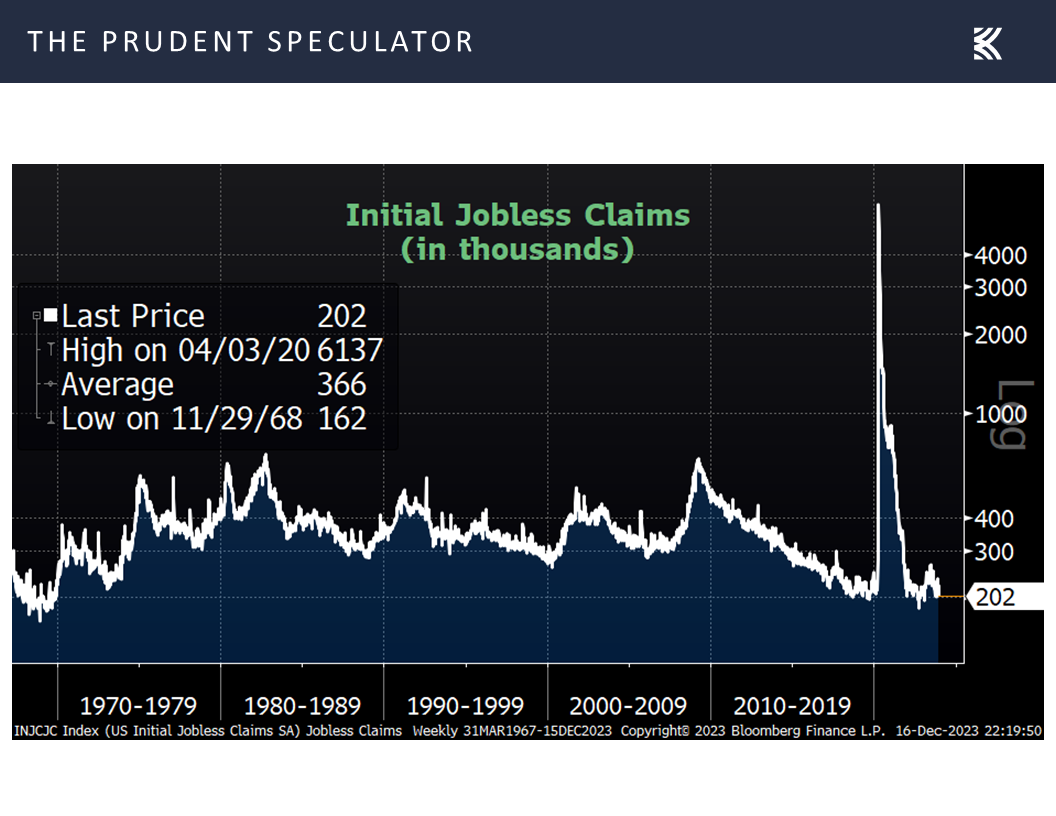

and the jobs market remained robust with the latest tally of weekly first-time-filings for unemployment benefits dipping to a lower-than-expected 202,000 and continuing to reside at multi-generational lows.

Chair Powell commented on the resiliency of the economy in the opening remarks of the FOMC Press Conference, where he reminded that the Fed’s latest summary of economic projections calls for 2.5% real GDP growth this year and 1.4% real GDP growth in 2024,

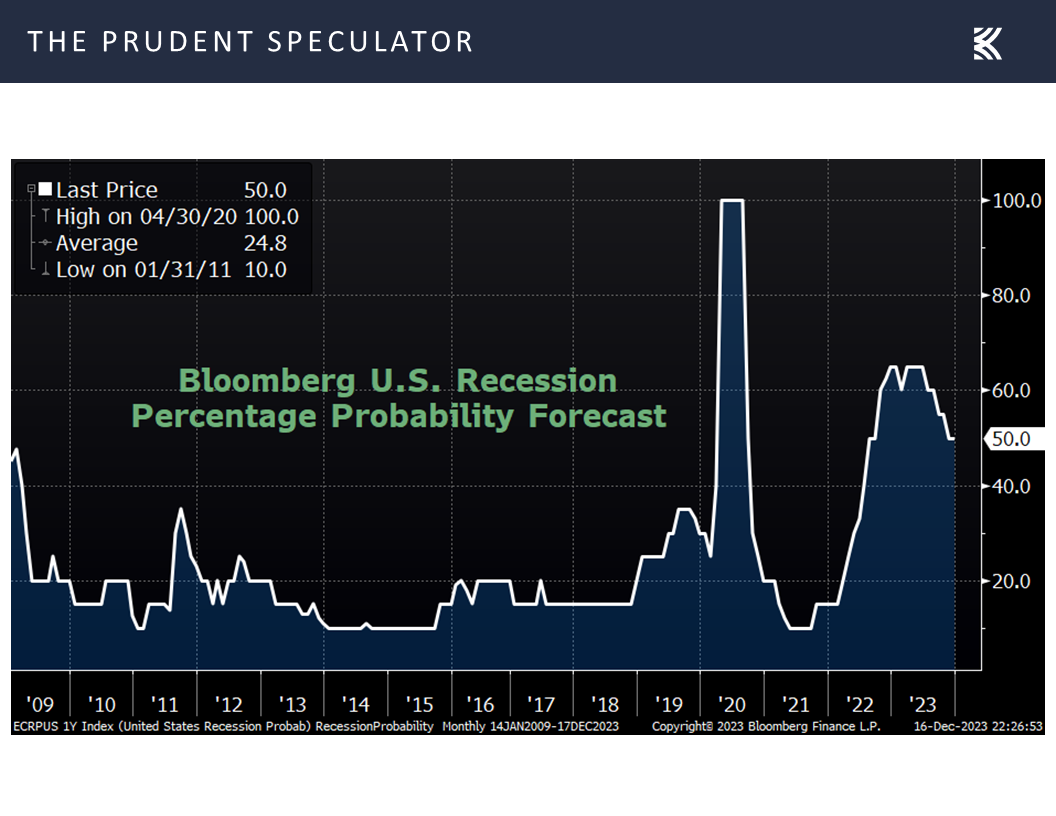

suggesting that the 50% recession probability over the next 12 months that is presently tabulated by Bloomberg might be too high.

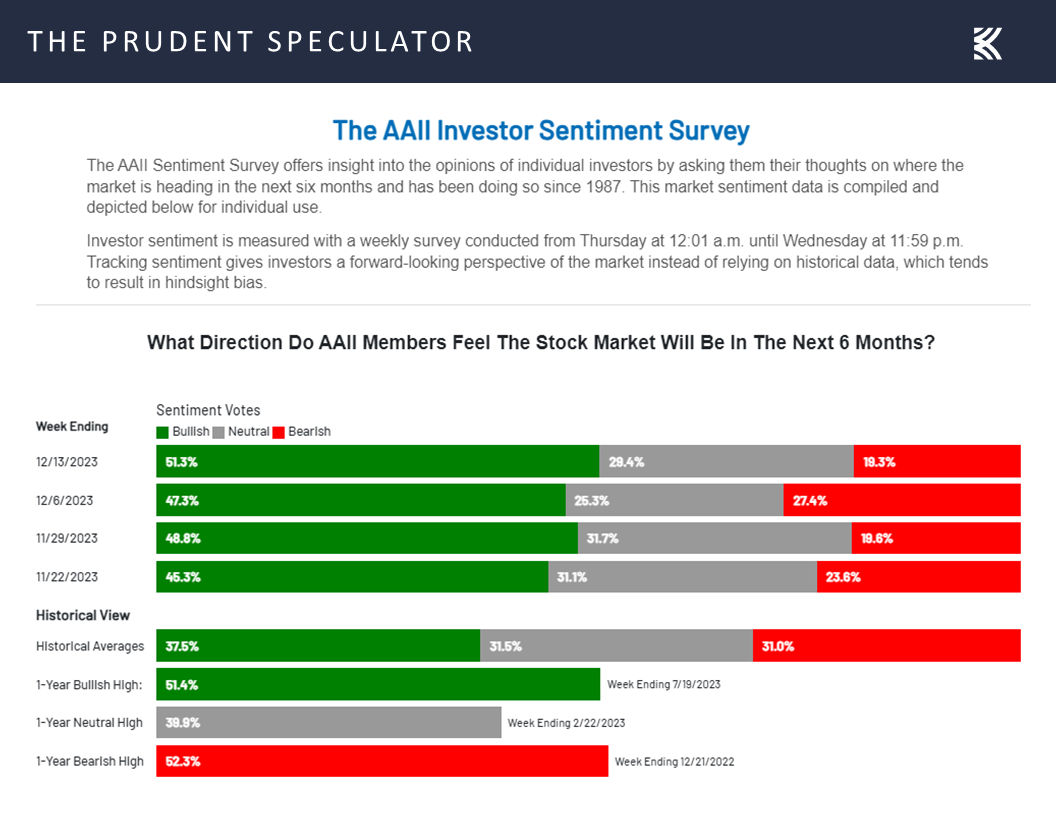

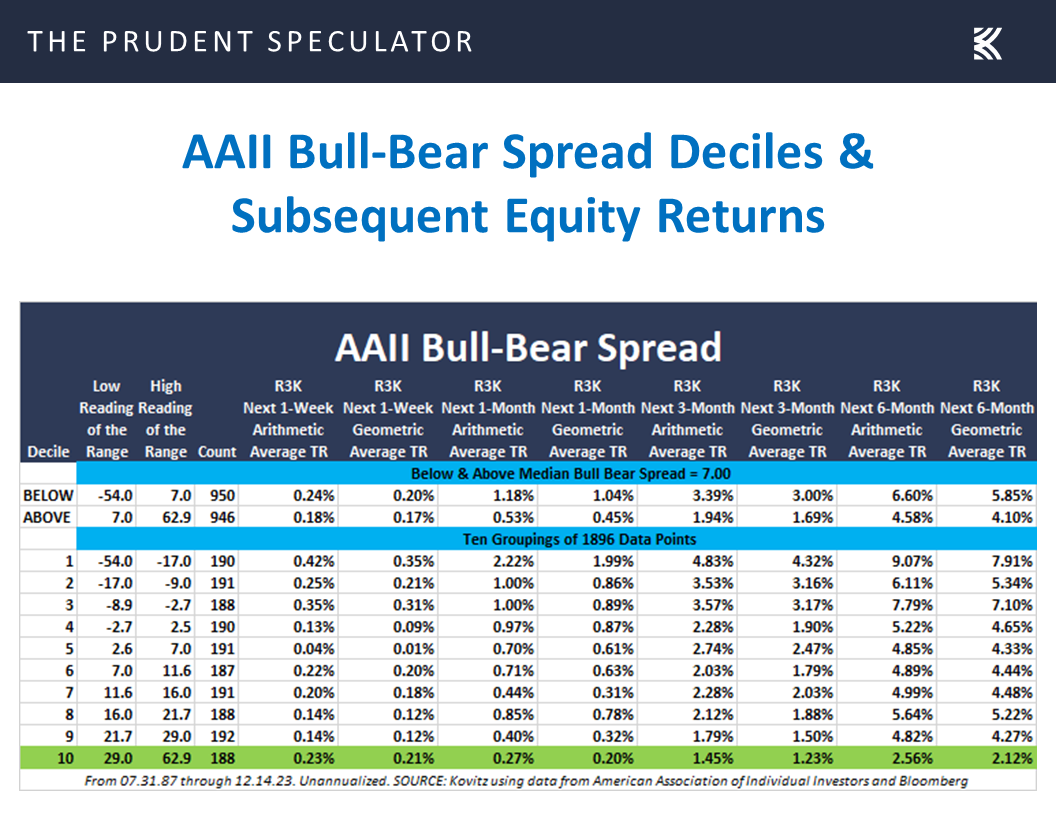

Sentiment – Still Plenty of Skepticism

Given our contrarian stance, we don’t mind that New York Fed President John Williams said on Friday, “We aren’t really talking about rate cuts right now,” and that many remain skeptical of the big rally,

especially as the latest Sentiment Survey from the American Association of Individual Investors (AAII) showed a wealth of Bulls and a dearth of Bears.

Nevertheless, the historical evidence argues for sticking with stocks even if folks on Main Street are enthused about them,

or if the newspaper headlines are disconcerting,

and we sleep soundly at night knowing that we own broadly diversified and generously yielding portfolios of what we believe to be undervalued stocks.

Stock News – Updates on eight stocks across five different sectors

Keeping in mind that all stocks are rated as a “Buy” until such time as they are a “Sell,” a listing of all current recommendations is available for download via the following link:

https://theprudentspeculator.com/dashboard/. We also offer the reminder that any sales we make for our newsletter strategies are announced via our

Sales Alerts. Jason Clark, Chris Quigley and Zack Tart take a look at earnings reports and other market-moving news of note out last week for more than a few of our recommendations.

Kovitz Investment Group Partners, LLC (“Kovitz”) is an investment adviser registered with the Securities and Exchange Commission. This report should only be considered as a tool in any investment decision and should not be used by itself to make investment decisions. Opinions expressed are only our current opinions or our opinions on the posting date. Any graphs, data, or information in this publication are considered reliably sourced, but no representation is made that it is accurate or complete and should not be relied upon as such. This information is subject to change without notice at any time, based on market and other conditions. Past performance is not indicative of future results, which may vary.

The Federal Reserve, Inflation, Valuations, Interests Rates and more

The Prudent Speculator Weekly Commentary is expertly curated every week as a valuable resource for stock market news, investing tips, business insights, and economic trends as it relates to value stock investing. In this week’s market commentary, we discuss the Federal Reserve, Inflation, Valuations, Interest Rates and more. We also include a short preview of our specific stock picks for the week; the entire list is available only to our community of loyal subscribers.

Executive Summary

Big Weekly Rally – Soldiers Beat the Generals

Valuations – Value Stocks Reasonably Priced

Inflation – CPI & PPI Trending in the Right Direction

Fed – FOMC Statement and Press Conference Suggest Rate Hikes are Done

Interest Rates & Stocks – Equities Perform Fine, on Average, in Rising and Falling Rate Environments

Econ News – GDP Growth Outlook Improves

Sentiment – Still Plenty of Skepticism

Stock News – Updates on eight stocks across five different sectors

Big Weekly Rally – Soldiers Beat the Generals

Even with Friday’s pullback in the average stock, it was a fantastic five days for equities as the proverbial Soldiers outperformed the Generals by a solid margin. Even better, the Russell 3000 Value (R3KV) index topped its Russell 3000 Growth (R3KG) counterpart, turning in its 97th best weekly price performance over the past 28 years with a gain of 3.38% and providing another reminder that the historical odds have long favored the buyer and holder of inexpensively priced stocks.

Valuations – Value Stocks Reasonably Priced

In addition to its historical propensity for outperformance, we shouldn’t be surprised by Value’s recent resurgence, given that the R3KV has been trading below its long-term norm on a price-to-earnings basis while the R3KG has been priced well above its historical average. In short, Value stocks are cheap on both a relative and absolute basis.

Inflation – CPI & PPI Trending in the Right Direction

Of course, the equity markets enjoyed a terrific advance on Wednesday and Thursday, following the release of the December FOMC Statement and the responses offered by Fed Chair Jerome H. Powell at the FOMC Press Conference.

With continued progress on inflation revealed earlier in the week as the year-over-year change in the Consumer Price Index (CPI) dropped to 3.1% in November, down from 3.2% in October,

while the Core CPI (excludes volatile food and energy) held steady at a 4.0% annual increase,

and the Producer Price Index rose only 0.9% on an annual basis, down from 1.3% the month prior,

Fed – FOMC Statement and Press Conference Suggest Rate Hikes are Done

More importantly, the FOMC Statement augmented the view of many market participants that Powell & Co. have reached the end of their rate-hiking cycle, via the addition of the word “any” to the “additional policy firming” language,

as did the first Q&A of the Powell Press Conference:

Q: I wanted to ask, how should we interpret the addition of the word “any” before additional firming in the statement. I mean does that mean that you’re pretty much done with rate hikes, and the Committee has shifted away from a tightening bias and toward a more neutral stance? Thank you.

A: So, specifically on “any,” we do say that in determining the extent of any additional policy firming that may be appropriate. So any additional policy firming, that sentence. So we added the word “any” as an acknowledgement that we believe that we are likely at or near the peak rate for this cycle. Participants didn’t write down additional hikes that we believe are likely, so that’s what we wrote down. But participants also didn’t want to take the possibility of further hikes off the table. So that’s really what we were thinking.

While those FOMC participants Mr. Powell referenced lowered their median outlook for the year-end 2024 Fed Funds rate to 4.6%, down from 5.1% three months ago,

Interest Rates & Stocks – Equities Perform Fine, on Average, in Rising and Falling Rate Environments

the response in the Fed Funds futures market was more dramatic, with traders now betting on a big drop in the benchmark lending rate to below 4% by the end of next year,

leading to a big rally in long-term government bonds last week which sent the yield on the 10-Year U.S. Treasury plunging to 3.91% from 4.23% the week prior.

Now, history suggests that stocks, especially Value, have performed fine whether the Fed Funds rate is rising or falling,

and whether the 10-Year Treasury yield is moving up or down,

but lower interest rates add to the valuation argument in support of equities.

Econ News – GDP Growth Outlook Improves

This is especially true, given that the outlook for corporate profits remains healthy,

with the Q4 U.S. real (inflation-adjusted) GDP projection from the Atlanta Fed rising to 2.6% last week from 1.2% a week ago,

as retail sales came in better than expected in November with a 0.3% increase,

and the jobs market remained robust with the latest tally of weekly first-time-filings for unemployment benefits dipping to a lower-than-expected 202,000 and continuing to reside at multi-generational lows.

Chair Powell commented on the resiliency of the economy in the opening remarks of the FOMC Press Conference, where he reminded that the Fed’s latest summary of economic projections calls for 2.5% real GDP growth this year and 1.4% real GDP growth in 2024,

suggesting that the 50% recession probability over the next 12 months that is presently tabulated by Bloomberg might be too high.

Sentiment – Still Plenty of Skepticism

Given our contrarian stance, we don’t mind that New York Fed President John Williams said on Friday, “We aren’t really talking about rate cuts right now,” and that many remain skeptical of the big rally,

especially as the latest Sentiment Survey from the American Association of Individual Investors (AAII) showed a wealth of Bulls and a dearth of Bears.

Nevertheless, the historical evidence argues for sticking with stocks even if folks on Main Street are enthused about them,

or if the newspaper headlines are disconcerting,

and we sleep soundly at night knowing that we own broadly diversified and generously yielding portfolios of what we believe to be undervalued stocks.

Stock News – Updates on eight stocks across five different sectors

About the Author

The Prudent Speculator

Explore

Popular Posts

Connect

Subscribe For Free Stock Picks

Get expert investing tips and market insights delivered straight to your inbox.