WHY VALUE?

While 2022 is marked with red ink for the majority of stocks, it’s been a good year for those of the Value persuasion, relatively speaking. Indeed, as of 11.17.22. the Russell 3000 Value index was down only 6.9% year-to-date vs. the 25.3% plunge for its growth counterpart, the Russell 3000 Growth Index.

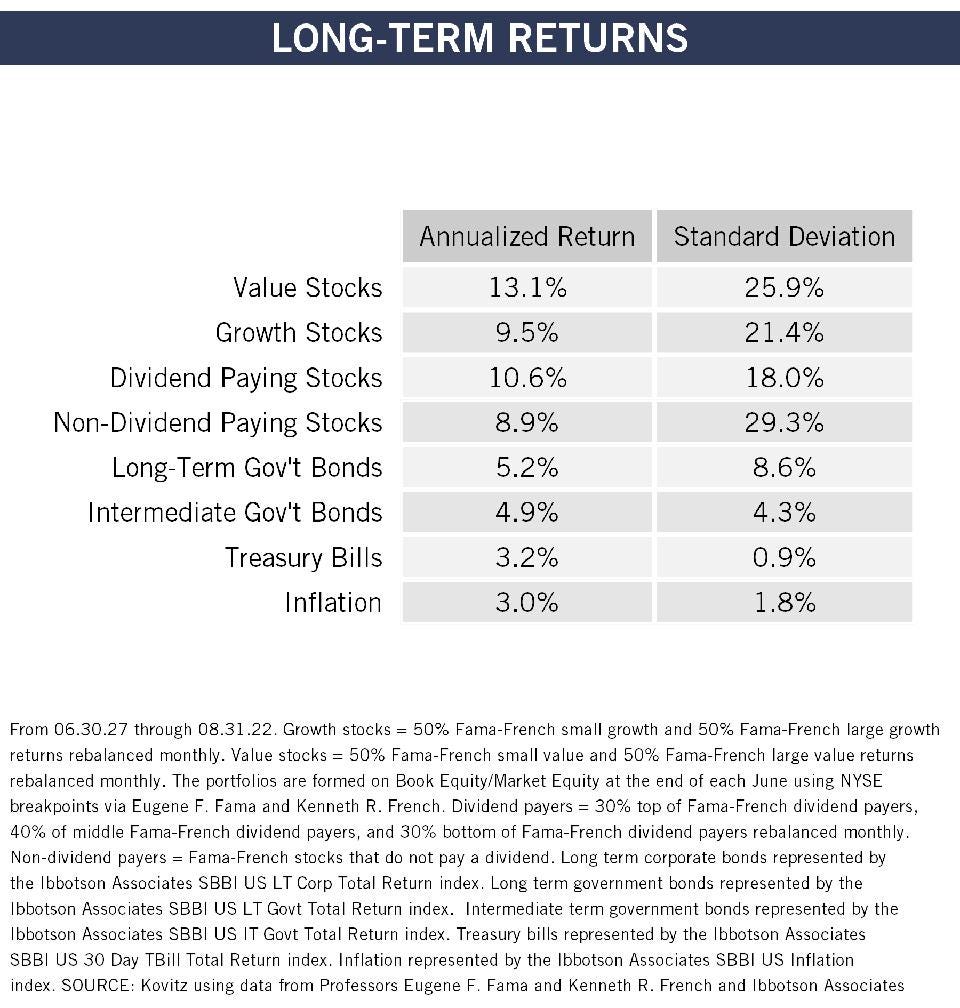

Proponents of Value investing have welcomed the turning tide, which began on Halloween 2020, as the approach had been maligned in recent years. Of course, historical experience favors the style over the long term as well as in periods like the current one that has prominently featured rising interest rates & inflation, a subject covered in a recent report my team has penned.

The Prudent Speculator SPECIAL REPORT: Inflation 101B

To be sure, as is also highlighted in Don’t Forget About Value, such a stringent approach (sticking just to stocks present in either index) is imperfect and could lead investors to miss out on hidden opportunities that await across the aisle.

EQUAL OPPORTUNITY STOCK PICKING

Microsoft (MSFT) is one such example. Shares were once represented within the Russell 3000 Growth AND the Russell 3000 Value indexes. But as the years have gone by, MSFT is now categorized purely as a Growth stock according to the good folks at Russell.

That is because the stock’s Price relative to its Book Value Per Share has more than tripled over the past decade, even as that multiple has shrunk by more than a third over the past year. Still, revenue has also grown by a multiple of 3, while earnings per share have grown by 13% per year on average over the same time frame.

STILL POISED FOR LONG-TERM GROWTH

The enterprise computing giant sits at the intersection of digital transformations and cloud adoption and is an immensely critical and indispensable IT mega-vendor. The company’s massive installed base of solutions makes it easier for customers to adopt the Azure cloud platform or experiment with new products and services, while remaining in the same Microsoft ecosystem.

An example of the latter is the rollout of its Teams product early on in the COVID-19 pandemic. When it seemed that competitors had succeeded in establishing leadership in filling the need for the global workforce to communicate remotely, Microsoft was able to leverage its ecosystem. Today, Teams remains among the most popular virtual meeting solutions on the market.

I think the future remains bright, especially with the stock down 28% year-to-date. Under the leadership of CEO Satya Nadella, the company has proven its ability to adapt to new environments, particularly as a cloud leader.

As firms across the Tech landscape are reducing the size of their workforces in the face of slowing demand, Mr. Nadella recently commented, “In this environment, we are focused on 3 things: first, no company is better positioned than Microsoft to help organizations deliver on their digital imperative so that they can do more with less. From infrastructure and data to business applications and hybrid work, we provide unique differentiated value to our customers. Second, we will invest to take share and build new businesses and categories where we have long-term structural advantage. Lastly, we will manage through this period with an intense focus on prioritization and executional excellence in our own operations to drive operational leverage.”

In a recent interview with CNBC, the CEO highlighted his enthusiasm about the future, particularly regarding Asia as a growth market. He said, “We’re very, very bullish about what’s happening in Asia…We’re absolutely committed to all of these countries and in China too. Today, we primarily work to support multinational companies that operate in China and multinational companies out of China…Microsoft’s presence in India was about mostly multinational companies operating in India. But for now, it’s completely changed.”

QUANTITATIVE AND QUALITATIVE REVIEW

At The Prudent Speculator, we analyze the fundamentals supporting about 3,000 individual stocks, both domestic and international. We synthesize financial measures we deem important predictors of favorable long-term performance into a value algorithm. We aggregate individual metrics into a composite stock scoring system that ranks individual stock valuations in the context of valuations among peers and the broader universe. Microsoft ranks highly in our scores.

Of course, focusing on backward-looking multiples says little about the future prospects of the business or its stock, so we engage in additional analytics. We take a deeper quantitative review of financial strength, earnings quality, debt maturities and capital expenditures. We also review higher-level qualitative aspects such as brand strength, competitive positioning, intellectual property defensibility, management tenure and product breadth & depth.

Needless to say, perhaps, but Microsoft passes those tests with flying colors. We are enamored with the mountain of cash in excess of debt on the balance sheet, the handsome profit margins and the tremendous cash-flow-generation position.

We also evaluate our companies via a forward-looking valuation engine in which we make a determination of fair value for the stock over the next three-to-five years. True, our spreadsheet is only as good as its inputs and predicting earnings, sales and book value is an art as much as a science. However, we like that MSFT is priced well below its three- and five-year historical norms on those important measures.

Yes, the trailing P/E ratio of 26 today is not exactly cheap, but we think profits are likely to grow handsomely over our holding period. In fact, the consensus analyst EPS estimates for fiscal ‘23, fiscal ‘24, fiscal ‘25 and fiscal ‘26 presently stand at $9.68, $11.25, $13.27 and $15.52, respectively. Wall Street is often over optimistic in its forecasts, but the price multiple based on ‘26 earnings is just 15.5.

GROWTH AT A REASONABLE PRICE

No doubt, Value purists will argue that Microsoft’s metrics are too rich to justify a buy today, but they were saying the same thing when we first recommended the stock in The Prudent Speculator in February 2005. Believe it or not, MSFT was then trading for $25 and the P/E ratio was a bit higher than where it is today! I also note that Microsoft is returning tons of cash to shareholders today via massive stock repurchases and a decent-sized (the yield is 1.1%) dividend.

So, is Microsoft a Value or a Growth Stock? I think the answer is Yes!

Learn More:

This is a refresh of our October 28, 2015 Forbes column titled “Is Microsoft A Value Or Growth Stock?” and is available here.

We frequently publish investment-oriented content on our Blog and reach thousands of subscribers through our weekly Market Commentary and monthly Newsletter. Please click here for subscription information.

For more details about our wealth management and asset management services, kindly fill out this Contact Us form and we’ll reach out to you shortly.